India Frontline Worker Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

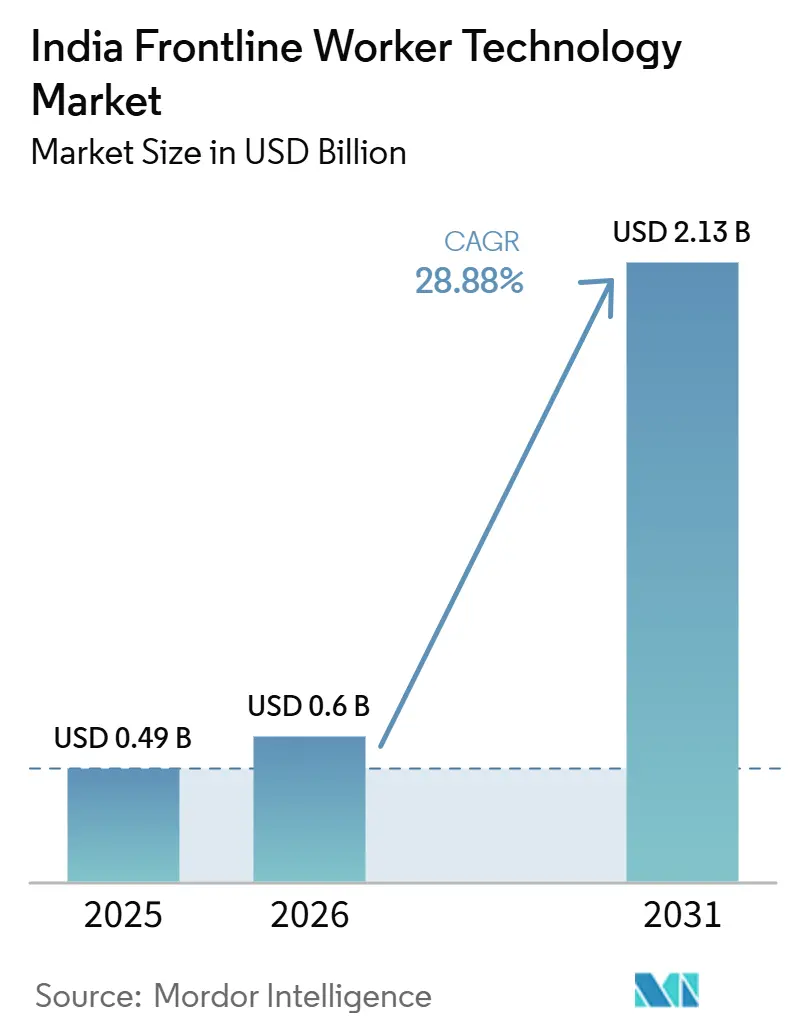

| Base Year Market Size (2025) | USD 0.49 Billion |

| Market Size (2026) | USD 0.6 Billion |

| Market Size (2031) | USD 2.13 Billion |

| Growth Rate (2026 - 2031) | 28.88% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Frontline Worker Technology Market Analysis by Mordor Intelligence

The India frontline worker technology market size is expected to increase from USD 0.49 billion in 2025 to USD 0.60 billion in 2026 and reach USD 2.13 billion by 2031, growing at a CAGR of 28.88% over 2026-2031. This pace reflects a broad shift in how Indian employers are managing large non-desk workforces across retail, logistics, healthcare, manufacturing, and field operations. Smartphone access has shifted from a limiting factor to a viable operating base, making mobile-first deployment practical across frontline settings and not just in large metro offices. The shift toward WhatsApp-based training, offline task completion, and multilingual interfaces is widening adoption beyond early enterprise pilots and into daily operating workflows. Compliance pressure is also pushing the India frontline worker technology market forward, because formal employers increasingly need reliable digital records, task traceability, and role-based communication tools. Competition is tightening as specialist vendors add workflow automation and AI features while large enterprise platforms extend their existing HR, service, and productivity suites into frontline use cases.

Key Report Takeaways

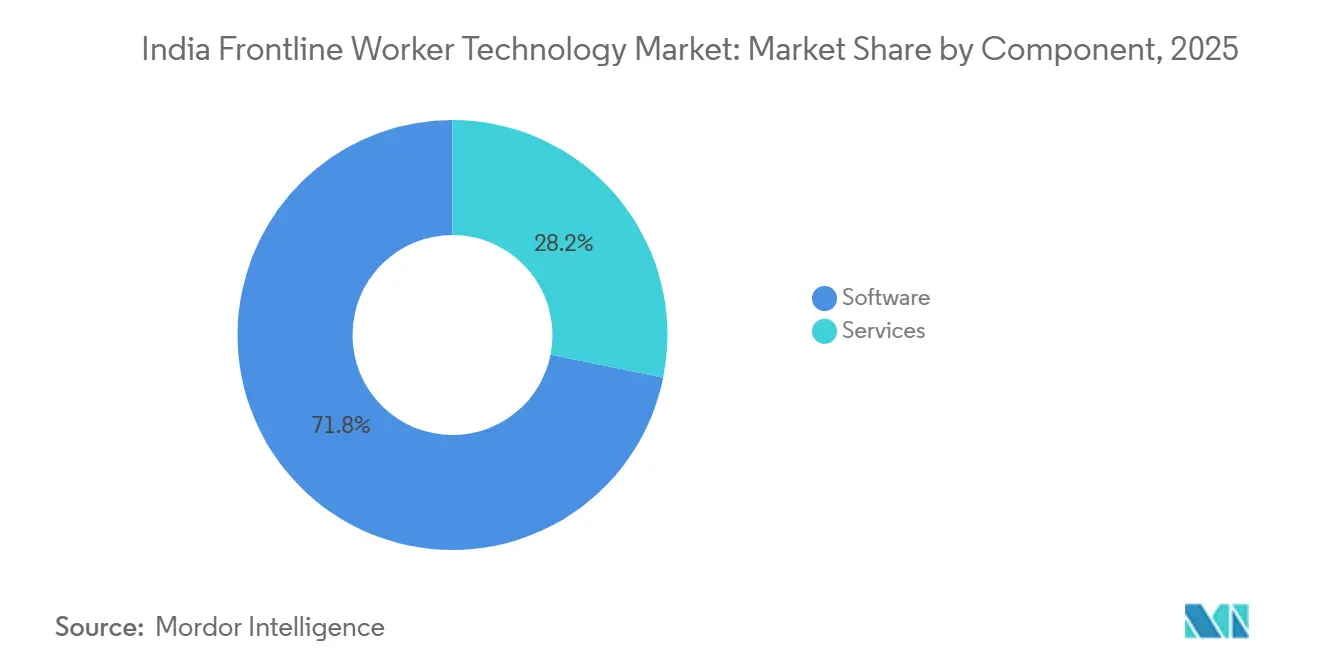

- By component, software held 71.84% of the India frontline worker technology market share in 2025, while services are projected to expand at a 31.26% CAGR through 2031.

- By deployment, cloud-based platforms accounted for 69.27% of the India frontline worker technology market size in 2025 and are projected to grow at a 32.18% CAGR through 2031.

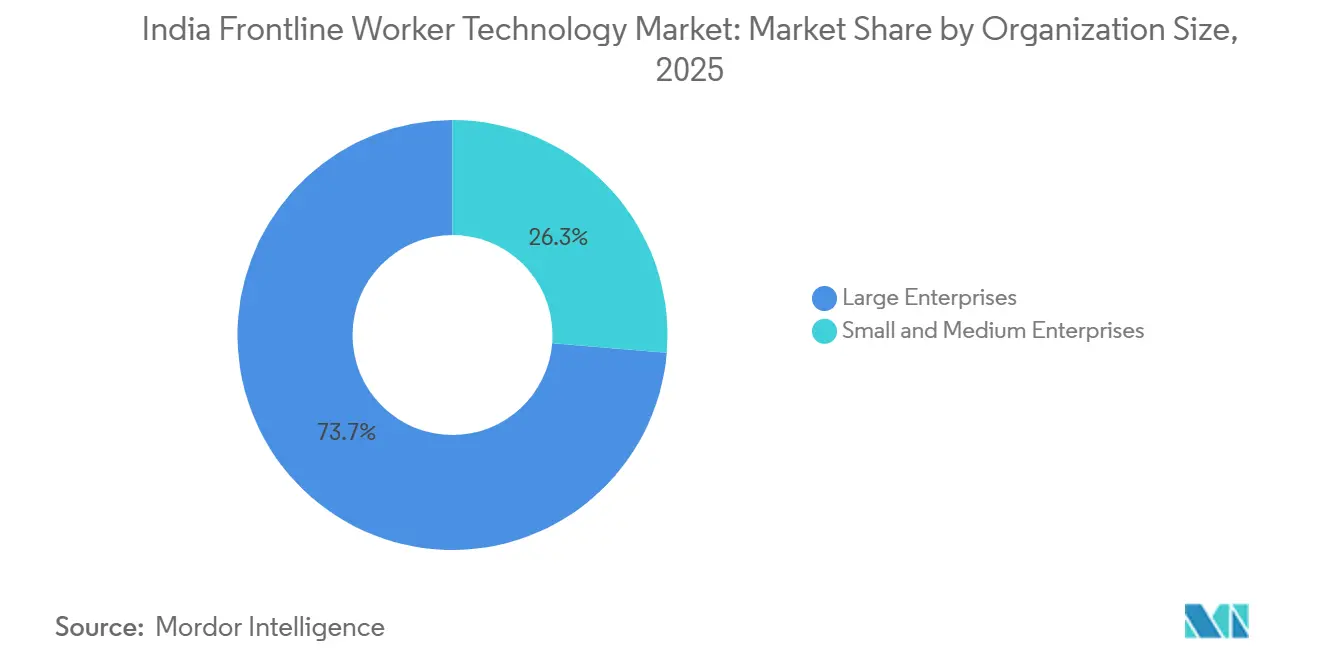

- By organization size, large enterprises held 73.68% share in 2025, while SMEs are expected to record the highest CAGR of 31.74% through 2031.

- By application, Workforce Execution and Task Management accounted for 26.41% share in 2025, while Workforce Analytics and Performance Management is projected to expand at a 33.45% CAGR through 2031.

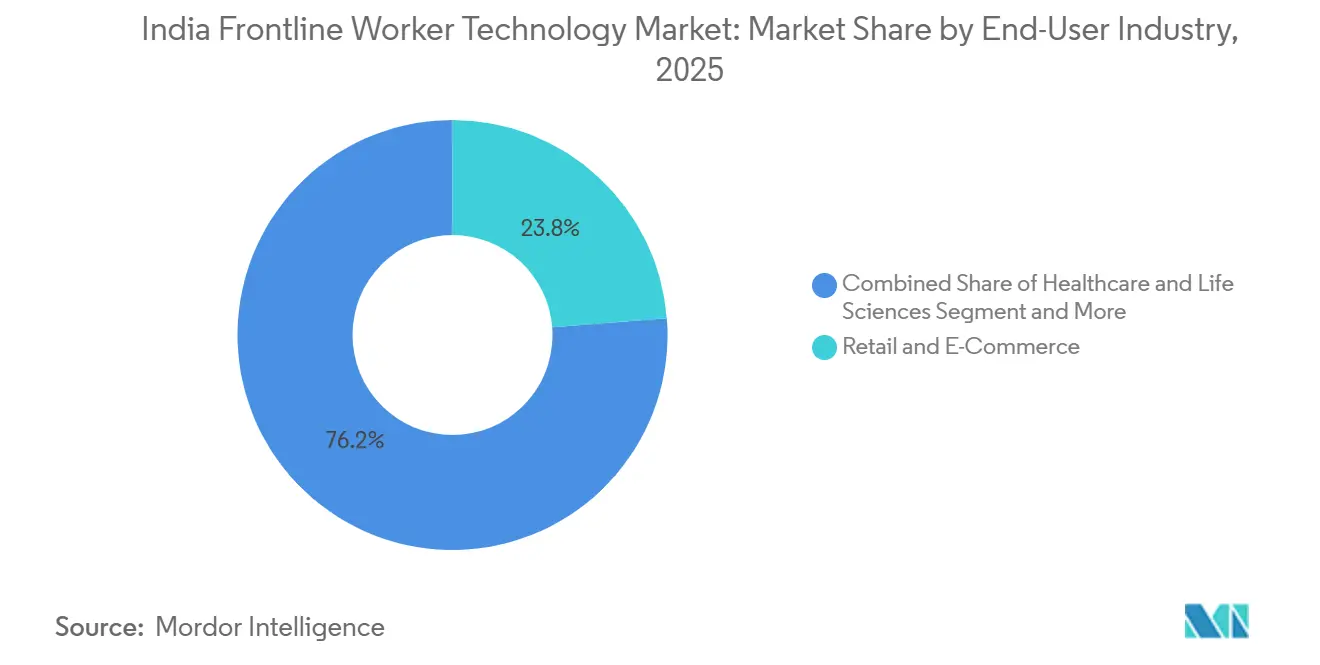

- By end-user industry, Retail and E-Commerce held 23.76% share in 2025, while Healthcare and Life Sciences are expected to grow at a 32.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Frontline Worker Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Smartphone-First Workforce Adoption | +8.5% | National, with early gains in Mumbai, Bengaluru, Delhi-NCR, Chennai | Short term (≤ 2 years) |

| Rapid Digitization Of Retail, Logistics, And Manufacturing Operations | +6.5% | National, concentrated in Tier 1 and Tier 2 industrial corridors | Medium term (2-4 years) |

| Escalating Compliance And Safety Visibility Requirements | +5.0% | National, regulatory influence strongest in organized manufacturing and healthcare | Medium term (2-4 years) |

| Need For Real-Time Task Orchestration Across Shifts | +3.5% | National, with intensity in quick-commerce and dark-store hubs | Short term (≤ 2 years) |

| AI-Based Translation And Microlearning For Multilingual Frontlines | +2.5% | National, highest impact in vernacular-dominant states including Uttar Pradesh, Tamil Nadu, and West Bengal | Medium term (2-4 years) |

| Integration Demand With HCM, WFM, ERP, And Payroll Stacks | +2.0% | National, concentrated in large enterprises with existing ERP footprints | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Smartphone-First Workforce Adoption

India’s non-desk labor base has crossed the device threshold that once limited enterprise rollout at scale. The Ministry of Statistics and Program Implementation reported that 85.5% of Indian households owned at least 1 smartphone in 2025, and smartphone use among rural youth aged 15-29 was 95.5%, which matters because this age group supplies a large share of frontline labor across several sectors.[1]Ministry of Statistics and Programme Implementation, “Comprehensive Modular Survey: Telecom, 2025,” Government of India, mospi.gov.in That baseline is changing software delivery in the India frontline worker technology market, as vendors can now reach workers through familiar mobile channels rather than relying on employer-issued hardware. Leap10x positioned its microlearning product around WhatsApp delivery and multilingual access, which aligns with India’s frontline deployment conditions and reduces the friction of app downloads and repeated logins. This design choice matters in sectors where onboarding speed affects shift readiness, because training, task alerts, and updates can move through the same mobile environment workers already use. The result is that the India frontline worker technology market is expanding on a broader operational basis, not just on large enterprise IT budgets.

Rapid Digitization Of Retail, Logistics, And Manufacturing Operations

The India frontline worker technology market is also being pushed by the faster digitization of labor-heavy operating environments. The Union Budget FY 2026-27 linked manufacturing expansion to stronger productivity, workforce readiness, and industrial capability, placing digital frontline execution within a wider national competitiveness agenda.[2]Ministry of Finance, “Union Budget FY 2026-27,” Government of India, pib.gov.in NITI Aayog’s advanced manufacturing roadmap also ties technology adoption and workforce capability to India’s push for a larger manufacturing role in the economy, reinforcing the case for digital training, task verification, and floor-level execution tools.[3]NITI Aayog, “Reimagining Manufacturing, India’s Roadmap to Global Leadership in Advanced Manufacturing,” Government of India, niti.gov.in This matters because new plants and logistics nodes not only increase labor demand, but also raise the need for consistent operating standards across shifts and sites. In the Indian frontline worker technology market, there is room for platforms that combine communication, learning, task flows, and audit-readiness in a single operating layer. It also supports demand beyond retail and into factories, warehouses, and service networks where fragmented manual processes are harder to sustain during expansion.

Escalating Compliance And Safety Visibility Requirements

Formal compliance requirements are turning digital workforce tools into a necessary operating layer for many employers. The notified Occupational Safety, Health, and Working Conditions Central Rules 2026 required electronic registers, time-bound reporting of dangerous occurrences, safety committees for larger establishments, and annual electronic returns, thereby underscoring the value of traceable digital workflows. The notification of the Labor Codes in November 2025 also placed greater emphasis on electronic records, mandatory appointment letters, and the preservation of compliance documentation, thereby increasing the operating costs of manual or disconnected systems. In the India frontline worker technology market, this shift in vendor selection favors platforms that can store records, assign tasks, document completion, and maintain usable audit trails. Safety and compliance management no longer sit apart from productivity tools, because both now depend on the same digital evidence chain. That is why demand in the India frontline worker technology market is becoming less discretionary in organized manufacturing, healthcare, and other formal-sector operations.

Need For Real-Time Task Orchestration Across Shifts

The India frontline worker technology market is also benefiting from the need to coordinate work in real time across dispersed shifts, locations, and teams. In fast-turn operations such as dark stores, lean-staffed store formats, hospital units, and high-volume service centers, missed handoffs cause immediate disruption to execution quality. WorkJam’s January 2026 release embedded AI into workflow triggers, exception handling, SOP enforcement, KPI widgets, and offline task completion, which shows where product design is moving in frontline execution environments.[4]WorkJam, “WorkJam Raises the Bar for Frontline Operations Platforms with Major Release,” WorkJam, workjam.com That matters because buyers are moving beyond messaging and toward systems that can assign work, verify completion, and escalate issues inside the same operational loop. The shift raises the value of structured task flows over general communication tools in time-sensitive environments. As a result, the India frontline worker technology market is seeing stronger demand for execution platforms that support active coordination rather than passive communication alone.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low Digital Literacy Across Certain Worker Cohorts | -3.0% | National, concentrated in Tier 2 and Tier 3 cities and rural manufacturing clusters | Medium term (2-4 years) |

| Integration Complexity With Legacy Operational Systems | -2.2% | National, particularly affects large enterprises with multi-vendor ERP and HRMS footprints | Long term (≥ 4 years) |

| Thin ROI Visibility In Small And Mid-Sized Deployments | -1.5% | National, concentrated in MSME-heavy states including Gujarat, Tamil Nadu, and Rajasthan | Short term (≤ 2 years) |

| Data Privacy And Worker Surveillance Concerns | -1.0% | National, heightened in healthcare and public-sector frontline deployments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low Digital Literacy Across Certain Worker Cohorts

Digital access is not the same as digital fluency, and that remains a real restraint in the India frontline worker technology market. The World Economic Forum and the Principal Scientific Adviser’s AI playbook for India’s SMEs identified resistance to new technologies and inadequate access to training programs as structural barriers to adoption, especially in smaller business settings.[5]World Economic Forum and Principal Scientific Adviser, “Transforming Small Businesses, An AI Playbook for India’s SMEs,” World Economic Forum, reports.weforum.org That means vendors cannot assume that smartphone ownership automatically leads to full use of workflows, dashboards, learning modules, or compliance forms. Products often need voice support, short learning loops, and guided navigation before achieving steady field adoption. This raises onboarding costs and slows deployment speed in parts of the India frontline worker technology market that should otherwise benefit from low-cost mobile distribution. It also creates a split: advanced employers move faster, while emerging industrial clusters need more support before usage becomes routine. The constraint is not about device ownership alone; it is about repeated, confident use in daily work settings.

Integration Complexity With Legacy Operational Systems

Integration remains a difficult barrier for larger deployments in the India frontline worker technology market. ICRIER’s annual survey of MSMEs in India found that smaller firms often cannot unlock the full value of technology platforms without external support, reflecting a wider challenge of connecting new digital tools to older systems and processes. In large enterprises, the issue is even broader because frontline platforms must often connect to payroll, attendance, HR, service, and ERP systems built for desktop users and centralized administration. India-specific payroll and labor rules add another layer of setup work, because employers need local compliance accuracy, not just generic scheduling or communication features. WorkJam’s FastTrack program with UKG showed why pre-built, bidirectional connectors are gaining commercial importance, because faster deployment reduces time to value and lowers implementation friction. Until integration effort becomes lighter, the India frontline worker technology market will continue to face slower adoption in complex, multi-system environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Anchors Revenue, Services Reflect Market Maturation

Software held 71.84% of the India frontline worker technology market in 2025, indicating that buyers still start with core applications for communication, execution, scheduling, and learning before spending heavily on external support. That share also means the India frontline worker technology market size remains tied to recurring SaaS models that scale across large worker bases without matching growth in physical infrastructure. Early deployments usually focus on direct workflow value because enterprises want a usable frontline layer before expanding integration scope or long-term services. In practical terms, software remains the first purchase because it gives managers a direct way to assign tasks, push updates, record completion, and organize field communication in 1 system. It also remains the visible control layer for employers that want better shift consistency across distributed teams.

Services are projected to grow at a 31.26% CAGR through 2031, indicating that the India frontline worker technology market is moving beyond pilot-led buying toward more structured deployment programs. This growth pattern points to rising demand for implementation support, API work, process redesign, and change management as customers connect frontline tools with wider enterprise systems. The shift also suggests that buyers now expect vendors to remain involved after the initial rollout, especially when projects span multiple locations, languages, and compliance settings. WorkJam’s emphasis on certifications, multilingual availability, and enterprise readiness reflects this change in buyer expectations, as platform choice is increasingly shaped by long-term operational fit rather than just feature checklists. In that sense, service growth strengthens the Indian frontline worker technology market by making vendor relationships more durable and more embedded in daily operations.

By Deployment: Cloud Leads On Share, While Hybrid Retains Operational Relevance

Cloud-based deployment accounted for 69.27% of revenue in 2025, making it the center of the India frontline worker technology market in current use. Cloud also posts the fastest projected growth at a 32.18% CAGR through 2031, indicating the same model that leads today is also widening its advantage over the forecast period. This pattern fits newer employers and newer operating formats that prefer fast deployment, lower infrastructure responsibility, and easier updates across dispersed teams. In the India frontline worker technology market, cloud is particularly well-suited to mobile-led workflows, where task instructions, training, communication, and audits need to move quickly across sites. It also works well for employers that want centralized visibility without heavy local IT management.

Hybrid deployment remains relevant because not every frontline environment has stable connectivity or the same level of comfort with full cloud dependence. Manufacturing sites, regulated operations, and connectivity-variable field settings still need resilience at the point of work, even when the core system is cloud-based. WorkJam’s offline task completion mode illustrates why this matters, because execution cannot stop when workers move through low-signal environments or temporarily disconnected floors. On-premises deployment will likely remain a smaller niche in the India frontline worker technology market, mostly where institutional control requirements or legacy technology habits still shape procurement. The wider takeaway is that cloud leads the market, while hybrid remains a useful operating answer for settings where continuity matters as much as central visibility.

By Organization Size: Large Enterprises Lead, While SMEs Expand The Next Demand Pool

Large enterprises held 73.68% of the India frontline worker technology market in 2025, reflecting their stronger purchasing power, broader compliance burden, and greater ability to roll out systems across multiple locations. That concentration means the India frontline worker technology market share has so far been driven by organized retailers, major logistics operators, large healthcare networks, and other employers with established technology budgets. These organizations also tend to gain value faster because they manage larger worker counts, more standardized procedures, and greater operational risk from manual coordination. In many cases, they already operate digital HR or service systems, which makes it easier to position the frontline layer as an extension rather than a separate technology bet. Their scale also supports multi-year contracts that specialist vendors find commercially attractive.

SMEs are projected to grow at a 31.74% CAGR through 2031, signaling the next meaningful expansion phase in the India frontline worker technology market. This growth is tied to a clear need for India-specific compliance handling, localized pricing, and simpler deployment models that do not require large internal IT teams. The formalization effect of the Labor Codes also supports SME demand, as recordkeeping and process discipline matter more when regulatory expectations tighten. The World Economic Forum and the Principal Scientific Adviser’s SME playbook also emphasized technology adoption as a practical requirement for smaller firms that want productivity gains, which aligns with the long-term opportunity in this buyer group. As these employers look for lighter, mobile-first tools, the India frontline worker technology market is likely to expand beyond enterprise-led adoption into a broader mid-market base.

By Application: Task Management Leads Today, Analytics Gains Strategic Weight

Workforce Execution and Task Management held the largest application share at 26.41% in 2025, which makes it the current center of day-to-day usage in the India frontline worker technology market. That lead is logical because employers first need a reliable system to assign work, track completion, manage exceptions, and maintain continuity across shifts. In the India frontline worker technology market size mix, this application sits closest to direct operational outcomes because it affects store routines, field activities, unit handoffs, and floor-level compliance. It is also easier for buyers to justify early, since task visibility solves immediate pain points even before broader analytics or engagement capabilities are fully adopted. As a result, task management remains the main entry point for many deployments.

Workforce Analytics and Performance Management is projected to expand at a 33.45% CAGR through 2031, indicating that buyers are increasingly looking beyond execution toward measured productivity, readiness, and workforce performance. This change matters because once daily workflows go digital, managers can use the same system to analyze patterns, identify gaps, and act more quickly on operational issues. Axonify’s May 2026 launch of AI Coaching, Max Frontline Assistant, Co-Creator, Conversational Insights, and Rollout features shows how vendors are turning frontline data into more active management support. That progression raises the role of analytics in the India frontline worker technology market, not as a separate reporting layer, but as part of the operating system used by managers and supervisors. It also means competitive advantage is shifting toward vendors that can convert execution data into usable decisions without making the frontline experience harder to navigate.

By End-User Industry: Retail Holds The Revenue Base, While Healthcare Builds A Distinct Growth Path

Retail and E-Commerce led with a 23.76% share in 2025, which gave this segment the largest position in the India frontline worker technology market among end-user industries. The segment’s lead comes from dense frontline labor use, frequent shift changes, store and fulfillment routines, and a constant need for communication and execution consistency. In the India frontline worker technology market, retail environments also benefit from mobile task flows, as managers need a clear way to push changes quickly across outlets and dark-store-style operations. Industrial manufacturing also remains an important demand pool, especially where production growth requires standardized task completion, training records, and safety documentation. These sectors have helped anchor the current revenue base by translating process discipline into direct operating value.

Healthcare and Life Sciences is projected to grow at a 32.81% CAGR through 2031, providing the India frontline worker technology market with a second demand path beyond private commercial procurement. The key factor is the government-backed expansion of digital health workflows under ABDM, where frontline health workers increasingly operate within structured digital systems. The Ministry of Health and Family Welfare stated that Aarogya Setu 2.0 was relaunched in June 2026 as an AI-enabled personal health record platform under ABDM, with support features for frontline health use, reinforcing institutional demand for digital workflow tools. This gives the India frontline worker technology market a distinctive public health growth channel alongside retail, logistics, and manufacturing demand. It also means vendor relevance in healthcare will depend on workflow fit, compliance control, and support for large distributed worker networks rather than on general HR software alone.

Geography Analysis

Southern India remains the strongest adoption base for the India frontline worker technology market because it combines manufacturing depth, familiarity with technology, private healthcare scale, and organized retail activity. The region benefits from a stronger concentration of enterprise decision-making, which helps specialist vendors and platform suites reach large buyers faster. It also supports demand across multiple frontline settings simultaneously, including factories, hospitals, warehouses, stores, and field service networks. NITI Aayog’s advanced manufacturing roadmap reinforced the importance of workforce capability and technology adoption in India’s industrial expansion, and this logic aligns closely with that of southern industrial clusters. In the India frontline worker technology market, this creates a setting where digital execution tools align with both commercial expansion and industrial policy direction.

Western India forms the next major demand belt for the Indian frontline worker technology market because it combines industrial activity, corporate headquarters, warehousing expansion, and large formal employers. The region matters not only for adoption volume, but also for procurement influence, since many major enterprises shape technology buying from Western business centers while deploying across national networks. Manufacturing growth, logistics activity, and retail operations all support the need for mobile scheduling, communication, and task management systems. The Union Budget FY 2026-27 highlighted manufacturing and infrastructure as pillars of growth, which support continued frontline digitization needs in western industrial corridors. The India frontline worker technology market, therefore, finds both scale and breadth of implementation in Western states, especially where labor-intensive operations are growing faster than manual processes can handle.

Northern and eastern India are becoming more strategic for the India frontline worker technology market as formalization, public programs, and new industrial activity widen the user base. Delhi-NCR matters because large e-commerce, retail, and service employers operate from the region and require stronger shift coordination and store-level execution across a broad surrounding belt. Eastern corridors remain earlier in the adoption cycle, yet they are gaining relevance as manufacturing expansion spreads and digital administration expectations rise. NITI Aayog’s roadmap on AI for inclusive development emphasized digital enablement for underserved districts and public-service delivery, which supports the case for simpler, low-friction frontline tools in these regions. Over time, that should help the India frontline worker technology market broaden beyond its strongest southern and western bases and reach more public-sector and emerging industrial use cases.

Competitive Landscape

The India frontline worker technology market is fragmented, with global specialist platforms, enterprise software vendors, and India-focused challengers all competing for relevance. The core split is between vendors built around frontline communication, training, task execution, and analytics, and larger suites that extend existing HR, CRM, service, or productivity platforms into frontline use. This structure keeps barriers to entry moderate in software terms, yet it also raises the importance of product depth, integration readiness, and localization. The most visible consolidation move was the July 2025 merger of LumApps and Beekeeper, which created an AI-powered employee hub serving more than 7 million users across 2,000-plus clients and generating more than USD 150 million in recurring revenue. That move matters in the India frontline worker technology market because it compresses the space available to vendors that address only a narrow slice of the employee experience or frontline communication.

Specialist platforms are responding by adding greater operational depth rather than relying solely on communication. WorkJam’s January 2026 release integrated AI directly into workflows through task triggering, SOP enforcement, image annotation, KPI widgets, and offline completion, strengthening its position in execution-heavy environments. Axonify focused on AI coaching, conversational insights, and rollout support in May 2026, which shows that capability building and manager assistance are becoming stronger competitive themes. Legion Technologies also expanded workforce management functionality with more than 90 new features in January 2026, signaling that scheduling, labor optimization, and analytics remain active product battlegrounds. In this setting, the India frontline worker technology market favors vendors that can show measurable workflow value while keeping daily use simple for large frontline populations.

Large enterprise platforms compete differently in the India frontline worker technology market, because they use installed relationships and system integration rather than pure frontline specialization. Microsoft, SAP, Salesforce, Oracle, and ServiceNow can position frontline modules as lower-friction add-ons for customers already using wider enterprise platforms. SAP’s June 2026 field service and asset management release shows how established vendors are deepening mobile-first execution and embedded AI for field and frontline workers. The main white space lies with vendors that can handle Indian compliance requirements, provide multilingual support, and enable faster integration into mixed HR and payroll environments. That is why the India frontline worker technology market continues to leave room for specialized, localized providers even as the largest software ecosystems expand their reach.

India Frontline Worker Technology Industry Leaders

WorkJam Inc.

LumApps

Mobilesson Ltd. d/b/a Connecteam

Deputy Corporation

Quinyx AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: The Ministry of Health and Family Welfare, Government of India, launched Aarogya Setu 2.0 on June 29, 2026, repurposing the application as an AI-enabled Personal Health Record platform under ABDM and integrating Google's Gemma AI model for clinical decision support. The launch institutionalized a government-mandated digital workflow layer for India's frontline healthcare workers, ASHA workers, ANMs, and Community Health Officers, creating an institutional demand stream structurally independent of commercial HR software procurement.

- May 2026: Axonify launched significant AI enhancements at the Association for Talent Development annual conference on May 18, 2026, including AI Coaching, Max Frontline Assistant, Co-Creator, Conversational Insights, and Rollout capabilities. Customers using the platform have reported a 47% reduction in lost sales, a 23% decrease in call handling time, and an 8% increase in sales, performance benchmarks that enterprise buyers in India's ROI-focused procurement cycles are increasingly demanding as preconditions for vendor selection.

- May 2026: The Ministry of Labour and Employment, Government of India, notified the OSH Central Rules 2026 on May 8, 2026, mandating electronic registers, 12-hour dangerous-occurrence reporting, mandatory safety committees for establishments with 500-plus workers, and annual electronic returns. The rules directly expanded the compliance-addressable market for safety and compliance management modules within frontline worker platforms.

- January 2026: WorkJam released a major platform update on January 7, 2026, introducing Visual Merchandising with Image Annotation, Custom Widgets for real-time KPIs, AI embedded directly into workflows for task triggering and SOP enforcement, and an offline task completion mode. The platform simultaneously achieved HIPAA compliance alongside existing ISO 27001, SOC II Type 2, and CSA Star certifications, targeting healthcare and life sciences as a priority expansion vertical.

India Frontline Worker Technology Market Report Scope

The India Frontline Worker Technology Market Report is Segmented by Component (Software, and Services), Deployment (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Employee Communication and Engagement, and More), and End-User Industry (Retail and E-Commerce, Industrial Manufacturing, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Employee Communication and Engagement |

| Workforce Execution and Task Management |

| Workforce Scheduling and Coordination |

| Learning and Knowledge Enablement |

| Workforce Analytics and Performance Management |

| Safety and Compliance Management |

| Other Applications |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Healthcare and Life Sciences |

| Transportation and Logistics |

| Hospitality |

| Construction |

| Government and Public Administration |

| Other Industries |

| By Component | Software |

| Services | |

| By Deployment | Cloud-Based |

| Hybrid | |

| On-Premises | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Employee Communication and Engagement |

| Workforce Execution and Task Management | |

| Workforce Scheduling and Coordination | |

| Learning and Knowledge Enablement | |

| Workforce Analytics and Performance Management | |

| Safety and Compliance Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Industrial Manufacturing | |

| Healthcare and Life Sciences | |

| Transportation and Logistics | |

| Hospitality | |

| Construction | |

| Government and Public Administration | |

| Other Industries |

Key Questions Answered in the Report

What is the India frontline worker technology market size in 2026 and where is it expected to reach by 2031?

The India frontline worker technology market size is estimated at USD 0.60 billion in 2026 and is forecast to reach USD 2.13 billion by 2031 at a CAGR of 28.88%.

What is driving growth in frontline worker technology adoption in India?

The main drivers are high smartphone penetration, broader use of mobile-first training and task tools, stronger compliance needs, and rising digitization across retail, logistics, healthcare, and manufacturing.

Which component leads revenue in this space?

Software led with 71.84% share in 2025, showing that employers still prioritize core applications before they expand spending on implementation and managed services.

Why is cloud deployment leading adoption?

Cloud-based deployment held 69.27% share in 2025 and is also the fastest-growing format at 32.18% CAGR, supported by fast rollout needs and mobile-first operating models.

Which application area is expanding the fastest?

Workforce Analytics and Performance Management is projected to grow at a 33.45% CAGR through 2031, reflecting demand for stronger productivity visibility and manager decision support.

Which end-user group offers the strongest growth outlook?

Healthcare and Life Sciences is expected to grow at a 32.81% CAGR through 2031, supported by digital public health workflows and wider institutional use of frontline tools.

Page last updated on: