India Extruded Plastics Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

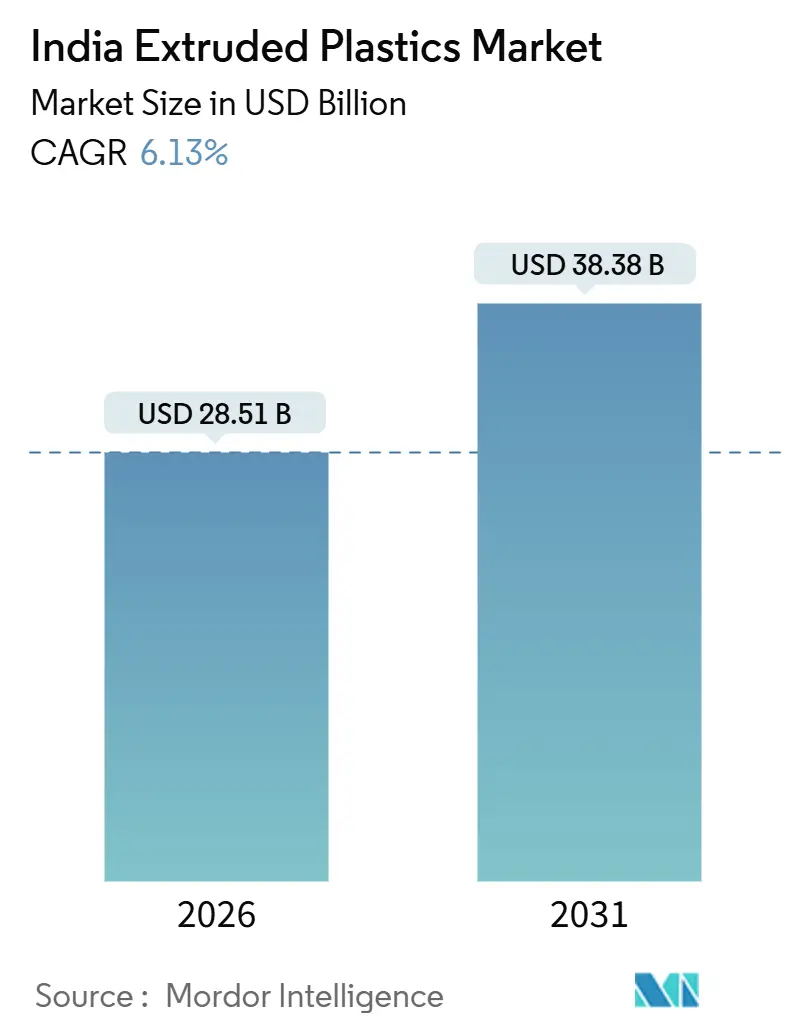

| Market Size (2026) | USD 28.51 Billion |

| Market Size (2031) | USD 38.38 Billion |

| Growth Rate (2026 - 2031) | 6.13% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Extruded Plastics Market Analysis by Mordor Intelligence

The India Extruded Plastics Market size is estimated at USD 28.51 billion in 2026, and is expected to reach USD 38.38 billion by 2031, at a CAGR of 6.13% during the forecast period (2026-2031). This expansion of the India extruded plastics market stems from a feedstock surplus generated by domestic petrochemical capacity additions, government-funded water infrastructure programs, and the steady pivot of brand owners toward high-barrier flexible packaging. Competitive gains accrue to producers able to certify products under Bureau of Indian Standards (BIS) norms and to leverage in-house recycling that monetizes Extended Producer Responsibility (EPR) credits. Meanwhile, converters serving quick-commerce and cold-chain logistics are specifying thinner-gauge films and multilayer laminates that preserve product integrity while reducing material intensity. Shifts in consumer purchasing behavior—especially the migration to online grocery and same-day delivery—are amplifying unit-volume growth across mailers, courier pouches, and insulated sheets. At the same time, domestic resin availability is reducing exposure to currency swings, improving working-capital cycles for regional film, pipe, and profile extruders.

Key Report Takeaways

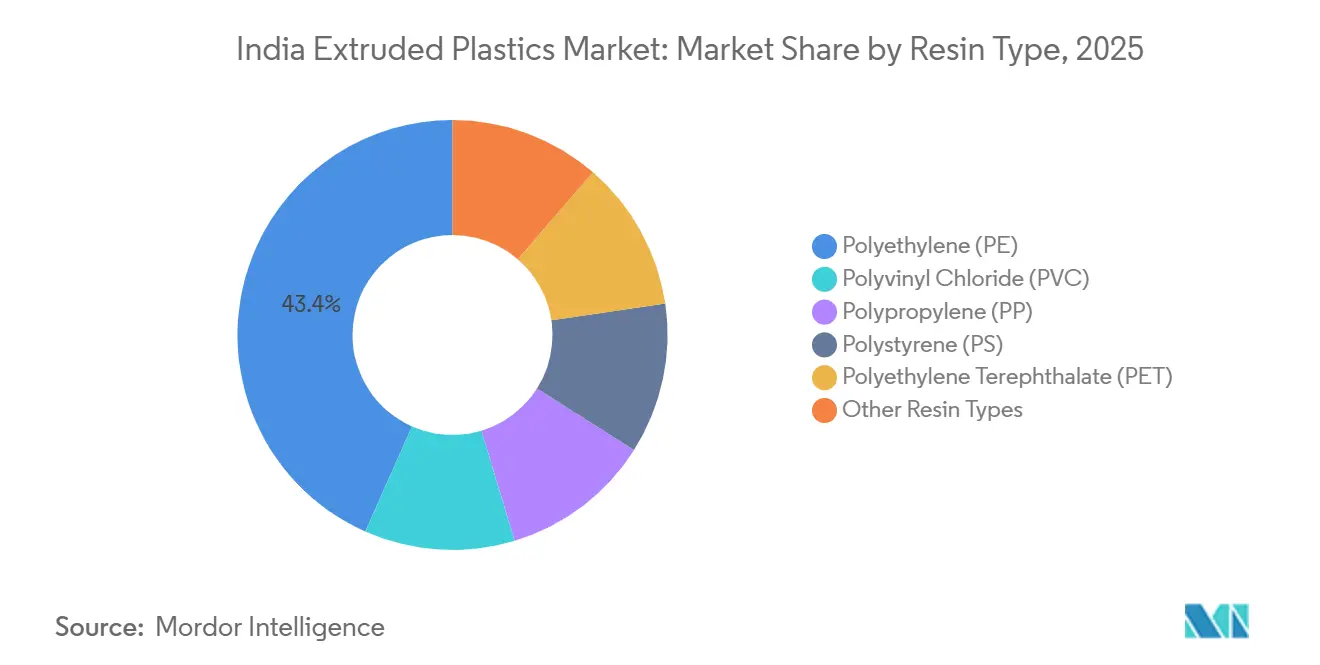

- By resin type, polyethylene led with 43.35% of India's extruded plastics market share in 2025 and is forecast to advance at a 6.78% CAGR to 2031, benefitting from infrastructure‐grade high-density formulations.

- By application, film and sheets captured 49.51% of the India extruded plastics market size in 2025 and are poised to grow at 6.57% through 2031 as e-commerce and food-safety rules accelerate multilayer adoption.

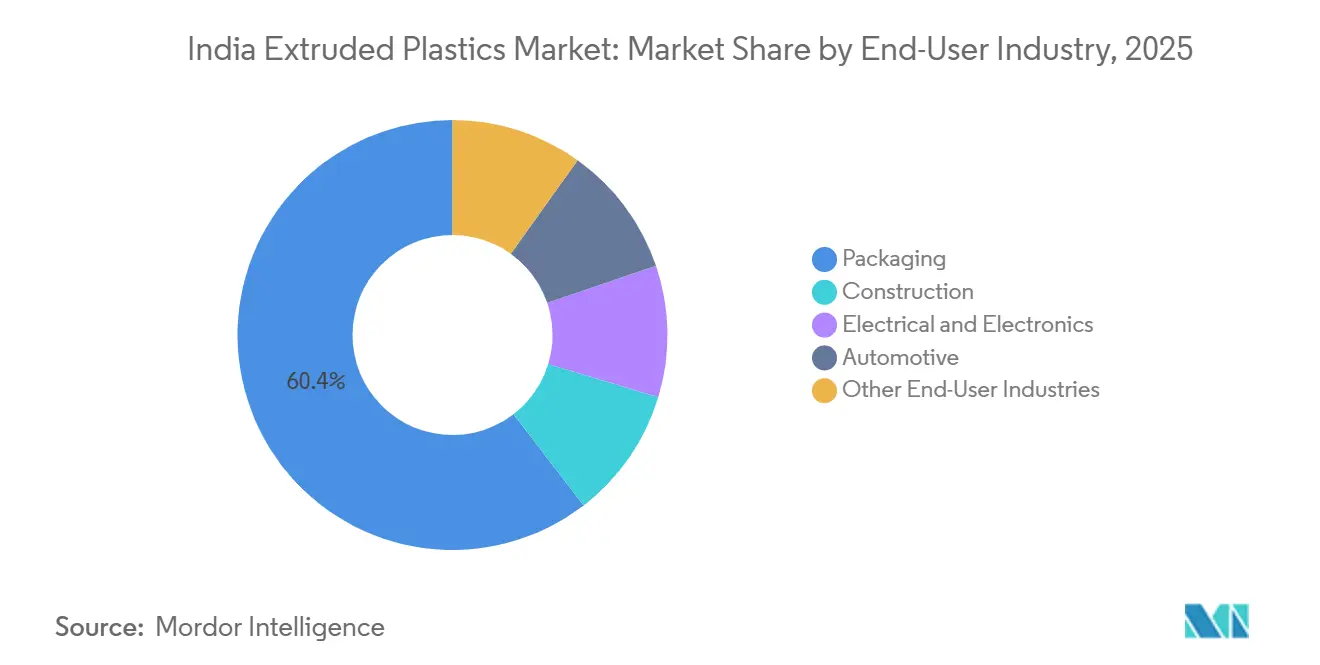

- By end-user industry, packaging accounted for 60.44% of demand in 2025 and is projected to expand at a 6.69% CAGR, buoyed by quick-commerce platforms and brand commitments to recycled content.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Extruded Plastics Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of India's Petrochemical Sector and Infrastructure Expansion | +1.8% | Gujarat, Maharashtra, Odisha | Long term (≥ 4 years) |

| Policy Incentives and Industrial Modernization | +1.4% | Tamil Nadu, Karnataka, Uttar Pradesh | Medium term (2-4 years) |

| Rise in Agricultural Applications and Government-Backed Subsidies | +1.2% | Punjab, Haryana, Maharashtra, Andhra Pradesh | Medium term (2-4 years) |

| Rising Demand from the Packaging Sector | +1.5% | Metro clusters nationwide | Short term (≤ 2 years) |

| Shift toward High-Barrier Specialty Films and Flexible Formats | +0.9% | Mumbai, Delhi NCR, Bengaluru | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth of India’s Petrochemical Sector and Infrastructure Expansion

As national polymer capacity is set to rise, feedstock availability is expanding. This surge is not only reducing resin acquisition costs but also diminishing the nation's historical reliance on imports for polyethylene and polypropylene. In 2024, Reliance Industries bolstered this trend by commissioning a polypropylene unit in Harihar. This move strengthens backward integration, shielding converters from global price fluctuations. Thanks to the Jal Jeevan Mission's substantial funding, households now enjoy tap connections. This initiative has nudged municipal tenders towards adopting BIS-compliant HDPE and PVC pipe systems, known for their extended service life and reduced leakage. Moreover, AMRUT 2.0's generous allocation, spread across cities, is further propelling the adoption of polymer pipes in water and sewerage grids. Collectively, these initiatives ensure a robust and sustained demand for India's extruded plastics market.

Policy Incentives and Industrial Modernization

India's Production Linked Incentive (PLI) scheme, with a massive envelope of INR 1.97 lakh crore, has already channeled significant capital expenditures[1]“PLI Scheme Investments Cross INR 1.46 Lakh Crore,” Press Information Bureau, pib.gov.in. This investment spans sectors like electronics, automotive, and white goods, and has indirectly bolstered demand for extruded housings, ducts, and interior modules. With ten operational Plastic Parks now in the fray, these parks are providing subsidized land, effluent treatment, and accredited testing facilities. This support is significantly lowering entry barriers for export-oriented small and medium enterprises. Furthermore, the India extruded plastics market is being steered towards larger players, thanks to the mandatory BIS Quality Control Orders that span 371 product categories and the introduction of EPR targets. These larger entities are better positioned to absorb audit fees and uphold traceability standards. In the electric vehicle sector, sales have increased significantly in 2024. This spike is intensifying the demand for lightweight polypropylene and polyamide under-hood structures, which not only enhance vehicle range but also streamline thermal management. Such synergistic policies clearly favor firms that are quick to adopt advanced compounding techniques, online rheology monitoring, and automated defect detection systems.

Rise in Agricultural Applications and Government-Backed Subsidies

Subsidies on drip-irrigation investments, part of the Pradhan Mantri Krishi Sinchayee Yojana, have expanded micro-irrigation coverage significantly by 2024. As a result, the demand for UV-stable lateral pipes, emitters, and multilayer greenhouse films has surged in the Indian extruded plastics market. In Maharashtra, Karnataka, and Himachal Pradesh, state incentives for protected cultivation are boosting the acreage under polyethylene greenhouse covers. The National Dairy Development Board's promotion of anaerobic fermentation, which reduces fodder spoilage and enhances milk yields, is driving the rising adoption of silage films in dairy regions. Export-oriented fruit and vegetable growers, needing to adhere to strict overseas residue norms, are increasingly turning to biodegradable mulch films. These developments not only deepen the rural footprint of the Indian extruded plastics market but also broaden its revenue streams, reducing reliance on the unpredictable urban construction sector.

Rising Demand from the Packaging Sector

In fiscal 2024, India's packaging industry reached a significant valuation. Plastics accounted for a substantial portion of this, with flexible formats seizing a dominant share. This underscores the pivotal role of barrier films in today's retail landscape. As e-commerce is projected to soar by 2030, there's a heightened demand for tamper-evident mailers and bubble-wrap alternatives, both crucial for protecting parcels during handling. Amendments by the Food Safety and Standards Authority in 2024 mandate lower migration thresholds and impose restrictions on certain phthalates. This has nudged converters towards adopting non-ortho ester plasticizers and low-VOC inks. Commitments from brand owners to incorporate post-consumer recycled content by 2025 have birthed a premium market for odor-neutral, food-grade recycled polyethylene. This niche, dominated by integrated players skilled in de-inking and cascade filtration, is witnessing significant traction. Moreover, flexible stand-up pouches, now featuring laser-scored easy-open designs, are beginning to replace traditional glass jars. This shift not only reduces shipping weight and carbon intensity but also broadens the potential market for India's extruded plastics sector.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Challenges and Compliance Costs | –0.7% | Maharashtra, Karnataka, Tamil Nadu | Short term (≤ 2 years) |

| Raw-Material Price Volatility and Competitiveness | –0.9% | Nationwide import-dependent sites | Short term (≤ 2 years) |

| Quality Gap in Recycling Feedstock | –0.5% | Tier-2 and tier-3 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Challenges and Compliance Costs

More than one lakh entities are now registered under EPR, and converters without in-house recovery must buy EPR credits, lifting operating expenses for small firms. Enforcement inconsistencies across states generate compliance arbitrage that skews competition, with Maharashtra levying penalties while other regions lag in inspections. BIS renewals for pipes, films, and profiles entail lab tests, factory audits, and documentation costs that delay product launches by six to eight weeks and drain cash for regional extruders. FSSAI migration tests add further latency for food-contact materials using recycled layers, discouraging rapid iteration in film formulations. Together, these overheads dampen investment appetite among smaller participants and temper the short-term growth trajectory of the India extruded plastics market.

Raw-Material Price Volatility and Competitiveness

In 2024, domestic spot prices for polyethylene and polypropylene fluctuated, closely mirroring movements in Brent-linked naphtha and responding to intermittent cracker outages[2]Indian Oil Corporation, “Panipat Petrochemical Complex,” iocl.com . As import parity pricing leaves converters vulnerable to fluctuations in the rupee, a decline in the currency led to an increase in landed costs. This shift has particularly impacted exporters bound by fixed-price contracts. Meanwhile, the imposition of anti-dumping duties on PVC imports from China, Taiwan, and South Korea has driven domestic PVC resin prices upward. This move has favored integrated producers but has simultaneously squeezed margins for downstream pipe manufacturers. Mid-tier processors, who lack hedging tools, find themselves in a bind: they can either absorb sudden price spikes or attempt to renegotiate with customers—a challenging task in the highly price-sensitive construction and agriculture sectors. Such market volatility has led to a pullback in capital investments for new extrusion lines, dampening the short-term growth of India's extruded plastics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Polyethylene Anchors Infrastructure and Flexible Packaging

Polyethylene accounted for 43.35% of India's extruded plastics market share in 2025 and is expected to outpace the overall market with a 6.78% CAGR to 2031, lifted by high-density grades specified in municipal water grids and multilayer films for food safety. High-molecular-weight HDPE pipes satisfy IS 4985 pressure ratings while maintaining a 50-year service life, pushing large tenders to favor domestic extruders certified under IS 10146. Polypropylene, benefiting from its 140 °C heat-deflection threshold, is winning share in electric-vehicle battery housings and under-hood ducts, where weight reduction translates directly into extended range. PVC remains entrenched in plumbing and conduit applications but faces cost headwinds following anti-dumping duties that lifted resin prices. Engineering thermoplastics such as polyamide and polycarbonate command niche shares for high-heat, flame-retardant applications; however, their higher price points constrain mass adoption. Resin-substitution dynamics therefore concentrate demand in polyethylene and polypropylene, reinforcing their material dominance in the India extruded plastics market.

Growth drivers for polyethylene include integration of post-consumer recyclate into outer film layers and rapid penetration of corrugated HDPE sewer pipes that permit trenchless installation under congested urban corridors. Reliance Industries and Indian Oil Corporation continue to debut bimodal HDPE grades with superior slow-crack growth resistance, enabling thinner wall thickness without compromising burst pressure. Polypropylene producers, meanwhile, pursue nucleated random-copolymer variants that deliver clarity approaching PET, allowing single-material rigid packaging that meets monomaterial recyclability criteria. Collectively, these resin-level innovations strengthen the competitive positioning of the India extruded plastics market across infrastructure and consumer-package segments.

By Application: Films Scale with Omni-Channel Retail and Cold-Chain

Films and sheets controlled 49.51% of India's extruded plastics market size in 2025 and will grow at a 6.57% clip through 2031, supported by e-grocery adoption and stricter food-contact migration limits that favor multilayer structures. Converter investments in 8-to-11-layer co-extrusion lines with online gauge control allow down-gauging of flexible laminates, reducing resin consumption while preserving barrier performance. Agricultural film demand rises in tandem as micro-irrigation coverage expands; UV-stabilized greenhouse covers extend crop seasons and improve yields. Stand-up pouches featuring re-closable zippers are capturing condiment, sauce, and pet-food markets previously served by rigid jars, though their D-shaped gussets complicate mechanical recycling, inflating EPR certificate outlays for brand owners. Pipe applications ranked second, propelled by Jal Jeevan Mission and AMRUT 2.0; high-density polyethylene outperforms concrete in trenchless installations due to its flexibility and joint integrity. Profile, wire-coating, and sheet segments serve cyclical building, appliance, and automotive channels, adding diversification but contributing less to volume growth than films or pipes. These application trends collectively propel the India extruded plastics market toward higher‐value, function-rich products.

Continuous innovation is defining film sub-segments. Metallized BOPP and recyclable high-barrier cast polypropylene are cannibalizing aluminum foil laminates in savory snacks, coffee, and pharmaceutical unit doses. Demand spikes for breathable PE stretch film in temperature-controlled last-mile delivery underscore the India extruded plastics market’s responsiveness to evolving logistics models. On the pipe front, multilayer corrugated HDPE variants are gaining favor in municipal sewer systems for their ring stiffness and chemical resistance, while PVC foam-core profiles substitute for timber in formwork and window frames, supporting circularity goals due to their recyclability.

By End-User Industry: Packaging Dominates While Construction Accelerates

Packaging generated 60.44% of demand in 2025 and is set to expand at a 6.69% CAGR through 2031, cementing its role as the primary demand engine for the India extruded plastics market. Quick-commerce platforms, promising deliveries in under 20 minutes, are nudging brand owners to opt for thinner yet stronger film gauges. These innovations reduce pack weight per order without compromising on burst strength. Meanwhile, Extended Producer Responsibility rules are pushing a shift away from non-recyclable laminates. These regulations, which impose penalties on such materials, are driving a transition to mono-material structures made entirely of polyethylene or polypropylene. In the construction sector, buoyed by government housing initiatives targeting affordable units, there's a notable emphasis on corrosion-proof polymer pipes and conduits. These are part of extensive water infrastructure upgrades. The automotive sector, witnessing a surge in electric vehicles, is increasingly turning to lightweight polypropylene and glass-filled polyamide parts. These materials are replacing traditional metals, leading to enhanced energy efficiency. The electrical and electronics sectors are leveraging flame-retardant PVC and polypropylene. These materials are being used for wire coatings and appliance housings, with industries valuing polymers for their electrical insulation properties and moldability. Agriculture, medical devices, and consumer goods form a diverse tail, presenting specialized growth opportunities. Extruders that can navigate stringent regulatory and performance benchmarks stand to benefit. This varied end-use landscape not only bolsters resilience but also supports the long-term growth trajectory of India's extruded plastics market.

Geography Analysis

By 2025, Western states—Gujarat, Maharashtra, and Goa—will host a significant portion of India's extrusion capacity. Their strategic locations near refineries, ports, and dense FMCG clusters play a pivotal role. In Gujarat, Reliance’s Jamnagar refinery, along with several downstream polymer complexes, ensures a steady feedstock supply. This is particularly beneficial for pipe and film converters engaged in Jal Jeevan Mission projects. Meanwhile, Maharashtra’s Mumbai–Pune corridor is home to high-barrier flexible-packaging plants. These plants cater to snack and beverage brands nationwide. Furthermore, the state's strict enforcement of single-use plastic bans has shifted demand toward compliant multilayer structures.

As rural water-supply schemes gain momentum, northern and central regions are witnessing the fastest expansion. The Sikandrabad Plastic Park in Uttar Pradesh, which became operational in 2024, is streamlining logistics for SMEs eyeing the North Indian construction market. In Punjab and Haryana, dairy cooperatives are championing the use of UV-stabilized polyethylene wraps. These wraps, promoted as silo-films, significantly reduce fodder spoilage. With agricultural subsidies and increasing rural purchasing power, the market penetration for India's extruded plastics is broadening.

Historically, eastern and northeastern states, especially Odisha and Assam, have trailed in per-capita polymer consumption. However, they're now making strides, thanks to refinery expansions and new infrastructure corridors. Indian Oil Corporation is set to enhance its Paradip refinery, adding polymer units by 2027. This upgrade positions Paradip as a coastal supply hub, catering to both domestic needs and export channels in Southeast Asia. Additionally, government grants under AMRUT 2.0 are channeling municipal funds into water and sewage systems. This initiative is progressively bridging the gap in polymer demand across regions. As a result, by the decade's end, the distribution of capacity and sales in India's extruded plastics market is poised to become more geographically balanced.

Competitive Landscape

The Indian extruded plastics market is moderately fragmented. Technology partnerships are emerging as key differentiators. Finolex focuses on pipe quality by integrating automatic diameter and ovality sensors that ensure compliance with IS 4985 even at higher line speeds. Disruptors such as regional agrifilm specialists leverage subsidy frameworks to sell directly to farmer cooperatives, bypassing multi-tier distribution and capturing incremental margin. White-space opportunity lies in chemical recycling. Capital outlays remain steep, yet brand owner demand for food-grade recycled polyethylene motivates pilot plants near consumption centers. Players able to close the loop gain a dual revenue stream: premium-priced recyclate and tradable EPR certificates. Overall, scale, backward integration, and process automation will define competitive advantage in the India extruded plastics market over the next five years.

India Extruded Plastics Industry Leaders

The Supreme Industries Ltd.

Astral Ltd.

Finolex Industries Ltd.

UFlex Limited

Ashirvad

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Nupur Extrusion announced a new Sampla, Haryana plant slated to produce 5,000-6,000 tpa of extrusion products from FY 2026-27, developed at an investment of INR 200-250 million.

- April 2025: JSW’s certified extruder service partner opened an after-sales facility in India to support its growing polyolefin-extruder installed base, enhancing local technical support and spare-parts availability.

India Extruded Plastics Market Report Scope

Extruded plastics are thermoplastic materials processed through a die to form continuous shapes such as pipes, sheets, films, and profiles. These materials include resins like durable PVC, flexible and rigid Polyethylene (PE), heat-resistant Polypropylene (PP), versatile Polystyrene (PS), and clear, recyclable PET. They are widely used in applications such as packaging, construction, and consumer goods.

The Indian extruded plastics market is segmented by resin type, application, and end-user industry. By resin type, the market is segmented into Polyvinyl Chloride (PVC), Polyethylene (PE), Polypropylene (PP), Polystyrene (PS), Polyethylene Terephthalate (PET), and Other Resin Types. By application, the market is segmented into pipe, film and sheets, and other applications. By end-user industry, the market is segmented into construction, electrical and electronics, packaging, automotive, and other end-user industries. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

| Polyvinyl Chloride (PVC) |

| Polyethylene (PE) |

| Polypropylene (PP) |

| Polystyrene (PS) |

| Polyethylene Terephthalate (PET) |

| Other Resin Types |

| Pipe |

| Film and Sheets |

| Other Applications |

| Construction |

| Electrical and Electronics |

| Packaging |

| Automotive |

| Other End-User Industries |

| By Resin Type | Polyvinyl Chloride (PVC) |

| Polyethylene (PE) | |

| Polypropylene (PP) | |

| Polystyrene (PS) | |

| Polyethylene Terephthalate (PET) | |

| Other Resin Types | |

| By Application | Pipe |

| Film and Sheets | |

| Other Applications | |

| By End-User Industry | Construction |

| Electrical and Electronics | |

| Packaging | |

| Automotive | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the projected value of the India extruded plastics market by 2031?

It is expected to reach USD 38.38 billion, expanding at a 6.13% CAGR from 2026, from USD 28.51 billion in 2026.

Which resin dominates current demand?

Polyethylene leads with a 43.35% share thanks to its versatility, from high-density pipe grades to multilayer film structures.

How are government water programs influencing demand?

Jal Jeevan Mission and AMRUT 2.0 collectively steer procurement toward HDPE and PVC pipes that resist corrosion and lower life-cycle costs.

Why are high-barrier specialty films gaining traction?

They lengthen food shelf life without foil, meet recyclability norms, and align with brand pledges for mono-material packaging.

Page last updated on: