India Enterprise Resource Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

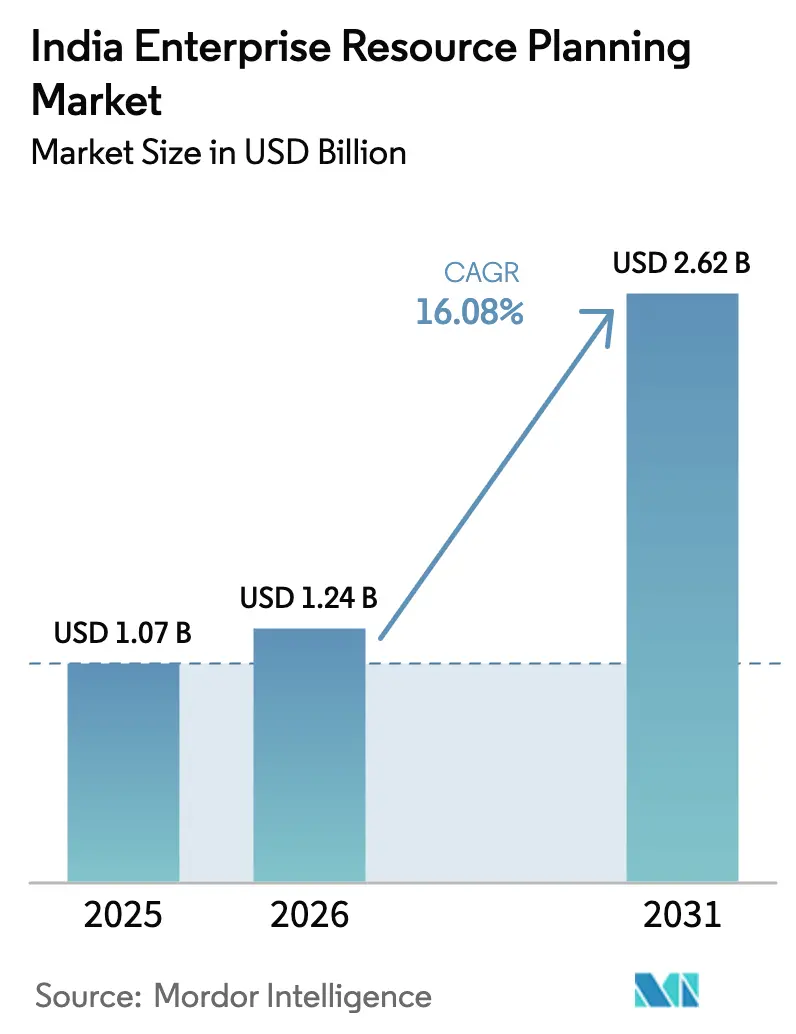

| Base Year Market Size (2025) | USD 1.07 Billion |

| Market Size (2026) | USD 1.24 Billion |

| Market Size (2031) | USD 2.62 Billion |

| Growth Rate (2026 - 2031) | 16.08% CAGR |

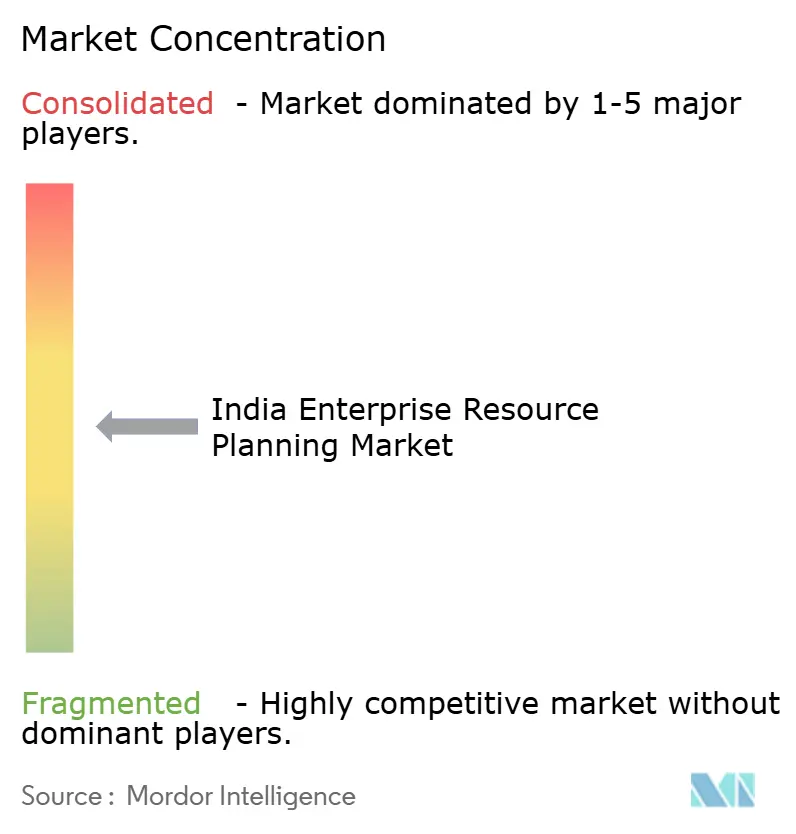

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Enterprise Resource Planning Market Analysis by Mordor Intelligence

The India Enterprise Resource Planning Market size is expected to grow from USD 1.07 billion in 2025 to USD 1.24 billion in 2026 and is forecast to reach USD 2.62 billion by 2031 at 16.08% CAGR over 2026-2031. Accelerated Goods and Services Tax compliance deadlines, Digital India 2.0 subsidies, and aggressive cloud migration among mid-market manufacturers keep the demand curve steep. Regulatory mandates for e-invoicing above INR 5 crore, coupled with the Reserve Bank of India's real-time fraud monitoring rules, make ERP a statutory necessity.[1]Ministry of Electronics and Information Technology, “Digital India 2.0 Framework,” meity.gov.in Cloud hyperscalers now operate availability zones in Hyderabad, Pune, and Mumbai, reducing latency to single-digit milliseconds and eliminating the last technical argument for on-premise systems. Tier-II manufacturing belts in Gujarat, Tamil Nadu, and Maharashtra feed a parallel edge-ERP wave that synchronizes shop-floor sensors with back-office finance modules in near real time, proving that industrial IoT is no longer a privilege reserved for Fortune 500 companies.

Key Report Takeaways

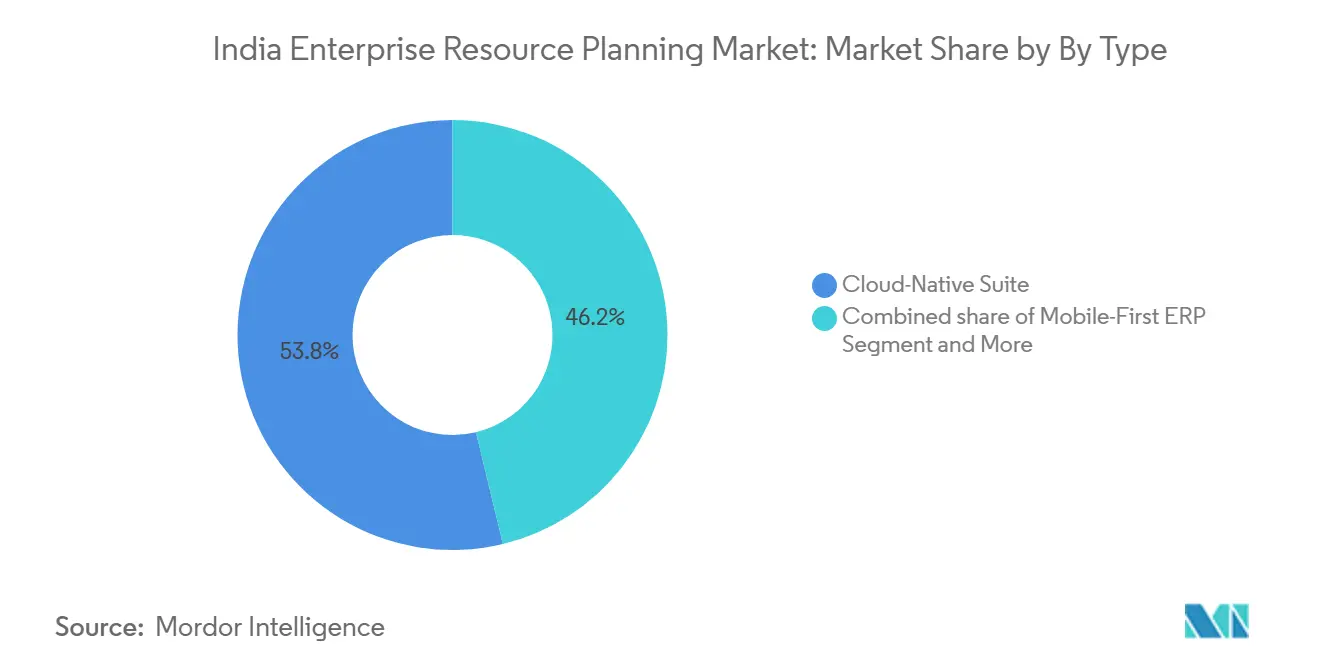

- By type, cloud-native suites led the India enterprise resource planning market with 53.77% market share in 2025.

- By business function, finance and accounting accounted for 29.45% of the India enterprise resource planning market size in 2025 and is projected to grow at an 18.08% CAGR through 2031.

- By deployment model, cloud captured 71.48% of new licenses in 2025 while advancing at a 17.41% CAGR through 2031.

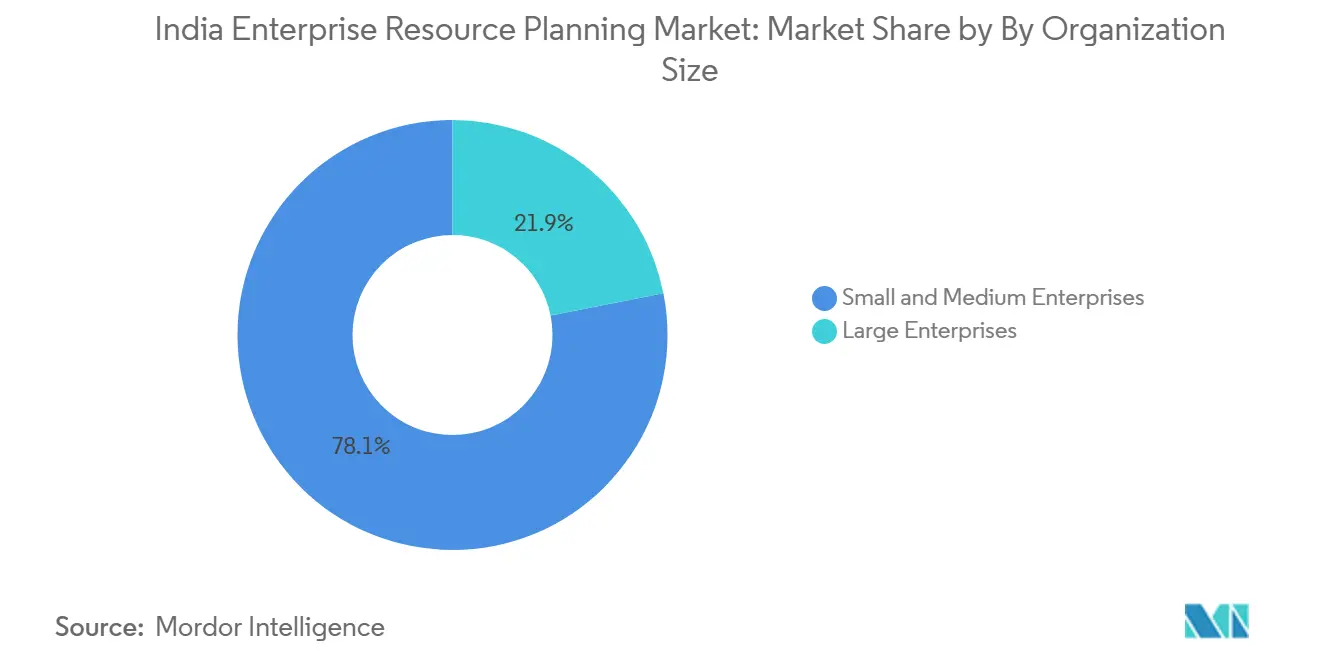

- By organization size, SMEs posted the fastest expansion at a 19.2% CAGR between 2026-2031, outpacing large enterprises at 17.83%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Enterprise Resource Planning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Push for GST and Compliance | +3.5% | National; Peak in West, South, North | Short Term (≤ 2 Years) |

| Growing Digital Transformation Initiatives | +3.2% | National; Led by West and South IT Hubs | Medium Term (2–4 Years) |

| Increasing Adoption of Cloud-Based Solutions | +2.8% | National; Strongest in South and West | Medium Term (2–4 Years) |

| Rising Demand for Industry 4.0-Ready Edge ERP in Tier II Manufacturing Clusters | +2.1% | West, South, North Manufacturing Belts | Medium Term (2–4 Years) |

| Emergence of Unified Payments Interface-Integrated ERP for MSMEs | +1.5% | National; Early Gains in West and South | Short Term (≤ 2 Years) |

| Surge in India-Specific AI Language Models Enabling Vernacular ERP Interfaces | +1.2% | National; Higher Adoption in North, Central, East | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Government Push for GST and Compliance

The phased e-invoice rollout forces 2.8 million enterprises to adopt compliant ERP suites. Ministry of Corporate Affairs audit-trail mandates add timestamp and hash requirements that spreadsheets cannot meet. Vendors with pre-certified GST packs captured 68% of SME installations in H1 2025[2]NASSCOM, “Enterprise Software Tracker 2025,” nasscom.in. A looming reverse-charge mechanism for cross-border services is already driving upgrades to procurement modules, while the 22% jump in e-way bill integrations shows logistics workflows are equally exposed. States differ in legacy VAT nuances, so hyper-local configuration capability has become a decisive vendor differentiator.

Growing Digital Transformation Initiatives

Digital India 2.0 earmarks INR 14,000 crore for public-sector digitization and sets a target of onboarding 500,000 MSMEs onto cloud platforms by 2027. Subsidized ERP licenses offered via Common Services Centres drop acquisition costs by up to 60% for eligible firms. Private surveys of 1,200 CFOs show 71% already executing core-system modernization, with cloud ERP topping the investment list. Production-Linked Incentive schemes across electronics, pharma, and textiles explicitly require real-time production data, embedding ERP deep into subsidy compliance. State-owned enterprises such as Bharat Electronics issue unified ERP tenders, encouraging smaller vendors to obtain ISO 27001 and CERT-In certifications if they wish to compete.

Increasing Adoption of Cloud-Based Solutions

Cloud accounted for 71.48% of new ERP deployments in 2025, thanks to pay-as-you-go economics and the elimination of hardware refresh cycles. Hyperscaler data centers in Hyderabad, Pune, and Mumbai cut latency by 18 milliseconds for Dynamics 365 and similar platforms, enabling real-time inventory sync during festival sales spikes. Updated data-localization rules, enforced from April 2025, require payment and customer data to remain onshore, a requirement readily met by the largest clouds but more costly for offshore SaaS start-ups. Deloitte cost modeling confirms that a 500-user cloud deployment is 42% cheaper over five years than an on-premises equivalent, an advantage SMEs quickly recognize.

Rising Demand for Industry 4.0-Ready Edge ERP in Tier II Manufacturing Clusters

Automotive suppliers in Pune, textile mills in Coimbatore, and pharma contract manufacturers in Ahmedabad install edge gateways that process PLC telemetry locally and sync aggregates to the cloud during off-peak hours. A documented 27% improvement in uptime at an Aurangabad auto-parts plant demonstrates tangible ROI. Electric-vehicle incentives under the FAME-II umbrella demand battery-cell traceability, which edge ERP with blockchain anchors can satisfy. Bosch’s 5G-enabled pilot achieved sub-50-millisecond latency, halving scrap rates, and set a benchmark other manufacturers now pursue. Vendors respond with turnkey appliance bundles pre-loaded with ERP runtimes to bypass complex field engineering.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation Costs | -2.3% | National; Acute in East, Central, Northeast | Short Term (≤ 2 Years) |

| Data Security and Privacy Concerns | -1.8% | National; Pronounced in BFSI and Healthcare | Medium Term (2–4 Years) |

| Shortage of Domain-Skilled ERP Consultants in Non-Metro Cities | -1.1% | East, Central, Northeast | Medium Term (2–4 Years) |

| Resistance from Family-Owned SMEs to Process Standardization | -0.9% | National; Strong in North and Central | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

High Implementation Costs

Total ownership for a mid-market roll-out spans USD 150,000-500,000, well above the comfort zone of micro-enterprises. A SIDBI survey shows 48% of SMEs cite cost as the top deterrent, even with 36-month cloud subscriptions. Customization inflates budgets by another 40% because informal credit cycles and consignment sales need bespoke code. Collateral-free loans for digitization posted only 12,000 approvals by January 2026, reflecting both lender caution and borrower reluctance. Vendors experiment with starter tiers priced at INR 499 per user per month, yet stripped-down features often trigger mid-contract upgrades, recreating the affordability barrier they aimed to solve.

Data Security and Privacy Concerns

Strict breach-notification timelines of 72 hours and uncertainty over data-controller liability heighten corporate anxiety. CERT-In flagged 14 critical ERP vulnerabilities in 2025, including a zero-day exploit that exposed records at 230 firms. BFSI and healthcare clients facing sector-specific penalties lean toward hybrid or on-premises topologies, decelerating the cloud adoption curve. Premium single-tenant cloud tiers with customer-managed encryption keys cost 25-35% more than multi-tenant offerings, offsetting some of the financial appeal of SaaS. Cyber-liability insurers frequently exclude cloud-hosted financial data, further complicating the risk calculus for CFOs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Cloud-Native Suite Holds the Lion’s Share, Edge ERP Accelerates

Cloud-native suites represented 53.77% of deployments in 2025. Vendors decouple modules, letting customers consume microservices on demand and update features without downtime. This approach delivers a 17.68% CAGR by 2031, as transaction-based pricing aligns costs with business cycles. Mobile-first ERP appeals to warehouse staff and field sales who need inventory and order visibility on smartphones; roll-outs at large retailers validate its utility at scale. Social and collaborative ERP weaves chat and co-editing into transactional screens but remains a niche preference among professional-services firms. Two-tier and edge ERP, forecast to expand at 18.7% CAGR, wins favor with multinationals that keep a lean regional ledger for tax compliance while aggregating globally. Tata Motors’ January 2026 pilot at Sanand and Pune plants processes quality images locally, proving edge ERP’s latency advantage. Draft cyber-physical standards from the Bureau of Indian Standards recommend edge computing for industrial latency under 100 milliseconds, further legitimizing the architecture.[3]Bureau of Indian Standards, “Draft Specification for Cyber-Physical Systems,” bis.gov.in

By Business Function: Finance Dominates, Manufacturing Execution Races Ahead

Finance and accounting accounted for 29.45% of the functional share in 2025. Continuous audit-trail mandates and GST e-invoice thresholds make automated reconciliation non-negotiable. ICICI Bank APIs link ERP cash positions to treasury desks for real-time liquidity optimization, driving deeper integration. Supply-chain and operations modules keep e-commerce warehouses stocked through algorithmic replenishment, while HR updates track provident-fund compliance. Manufacturing execution and quality grow fastest, at a 17.1% CAGR, as PLI schemes tie subsidies to verified digital output. Pharma producers embed electronic batch records to meet new Schedule M guidelines, and customer relationship modules let tractor buyers configure equipment online, bridging traditional and digital channels. Vendors offering pre-integrated MES and ERP suites secure the inside track for the next upgrade cycle.

By Deployment Model: Cloud Surges, Hybrid Gains Credibility

Cloud captured 71.48% of new licenses in 2025 and is forecast to post a 17.41% CAGR through 2031, anchored by subscription economics and hyperscaler data-center availability. Time-to-value drops from 18 months to under 12 weeks in mid-market projects, an agility boost CFOs prize. AWS joined Azure and Google with a Hyderabad region in late 2025, intensifying price competition and trimming hosting costs by almost 20%. On-premises, though shrinking, persists among defense contractors, pharmaceutical R&D labs, and certain banks that classify data as national security assets. Hybrid roll-outs, such as SAP’s RISE program, attract enterprises transitioning modules piecemeal, reassuring boards that core ledgers remain on familiar ground while analytics leap to the cloud.

By Organization Size: SMEs Power the Growth Engine

Large enterprises accounted for 21.89% of seats in 2025 and will grow at a 17.83% CAGR, mainly by adding sustainability, ESG, or supplier-collaboration extensions. SMEs, however, expand at a 19.2% CAGR, riding the first-time adoption wave across 6.3 million registered firms. ZED certification subsidies push quality management, indirectly nudging companies toward ERP investments they had postponed. TallyPrime still dominates micro-enterprise bookkeeping with over 2 million active licenses, yet its functional limits prompt scale-ups to migrate to Zoho or Busy as transaction complexity rises. Bank-fintech alliances that pre-approve credit for firms willing to share ERP data create a positive feedback loop between digitization and working-capital access.

By Industry Vertical: Manufacturing Leads, Healthcare Picks Up Speed

Manufacturing accounted for 31.23% of ERP spending in 2025 and will grow at a 17.89% CAGR. Production-linked subsidies in electronics, autos, and textiles require digital production logs, making ERP a prerequisite for claiming incentives. Larsen and Toubro standardized procurement on a single system covering 40 projects, illustrating margin-visibility gains. Retail and e-commerce follow suit, using omnichannel order engines to reduce stockouts during mega-sales events. BFSI invests in regulatory reporting modules to meet the Reserve Bank’s scale-based supervision norms, while government agencies accelerate under Digital India mandates, the Ministry of Railways tender spans 1.2 million employees. Healthcare shows the fastest climb at 18.0% CAGR as interoperable records under the Ayushman Bharat initiative and serialization in drug supply chains become law. Apollo Hospitals’ 70-facility roll-out of an integrated ERP-EMR stack typifies the vertical’s digital leap.

Geography Analysis

West India led with 29.1% of spending in 2025, driven by Maharashtra’s and Gujarat’s dense manufacturing and headquarters clusters. Real-time invoice matching mandated by the state tax department forces 140,000 dealers onto GST-compliant systems, boosting vendor pipelines. South India followed closely at roughly 28%, fueled by Bengaluru’s IT sector and Chennai’s auto corridor. Subsidized ERP licenses for 500 start-ups through the T-Hub and Microsoft partnership seed long-term demand. North India contributed about 22% in 2025; Delhi NCR’s corporate offices offset slower digitization in Uttar Pradesh and Bihar.

Northeast India is growing fastest at a 20.5% CAGR through 2031, driven by INR 3,200 crore in Digital Northeast Vision subsidies that boost broadband and cloud service adoption.[4]North Eastern Council, “Digital Northeast Vision 2025 Program,” necouncil.gov.in Tea estates in Assam and tourism operators in Meghalaya use cloud ERP to streamline export paperwork and multi-property reservations. East India trails because unorganized manufacturing in West Bengal and Odisha depends heavily on manual processes, though emerging steel and aluminum investments signal pockets of growth. Central India’s mining and cement producers are deploying ERP systems to comply with new online environmental clearance protocols, highlighting how niche regulations can spur local demand.

Consultant scarcity outside Tier-I cities elongates project times: a Deloitte study shows Tier-II roll-outs taking 14.6 months versus 9.2 months in metros. Vendors counter with regional-language interfaces; Ramco’s Tamil and Telugu HCM versions cut shop-floor training time by 30%. Improved telecom infrastructure, Bharti Airtel completed 5G coverage across 200 cities, should gradually reduce regional implementation gaps.

Competitive Landscape

The India enterprise resource planning market is moderately concentrated: SAP, Oracle, Microsoft, Infor, and Ramco hold a combined 59% share, corresponding to a market-concentration score of 5 on a 10-point scale. Competitive vectors cluster around cloud-first roadmaps, hyper-local compliance modules, and ecosystem bundling. SAP added Hindi and Tamil voice commands in April 2025 to reach non-English-speaking users. Domestic disrupters Tally Solutions and Zoho brought 120,000 SMEs onto their platforms in 2025 by packaging vernacular UIs and UPI gateways at prices 40-50% below multinational peers.

White space remains abundant: 78% of Tier-II and Tier-III manufacturers still run manual ledgers, and verticals such as education and hospitality remain under-penetrated. Deskera raised USD 100 million to extend its all-in-one suite into Southeast Asia, while Busy Infotech’s offline-capable design wins retailers in low-connectivity zones. Technology differentiation now revolves around embedded AI, blockchain audit trails, and API-first architectures that snap into Aadhaar and UPI rails. Oracle’s January 2026 patent for a machine-learning engine that auto-classifies invoice line items underscores the AI arms race. Smaller vendors lacking ISO 27001 and SOC 2 certification face exclusion from government tenders, likely accelerating roll-ups as private equity funds seek to stitch regional specialists into national contenders.

India Enterprise Resource Planning Industry Leaders

SAP SE

Oracle Corporation

Microsoft Corporation

Infor Inc.

Ramco Systems Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: SAP announced a USD 250 million expansion in Bengaluru, adding 2,000 engineers focused on AI-driven close automation and vernacular NLP.

- January 2026: Oracle and State Bank of India launched pre-approved working-capital loans for Fusion Cloud ERP users, targeting USD 500 million of disbursements within the year.

- December 2025: Microsoft released Dynamics 365 Copilot for India, embedding Hindi and Tamil generative assistants that cut transactional processing time by up to 30%.

- November 2025: Tata Consultancy Services and SAP opened a Pune innovation center to co-develop Industry 4.0 use cases for automotive and aerospace plants.

India Enterprise Resource Planning Market Report Scope

The India Enterprise Resource Planning Market Report is Segmented by Type (Cloud-Native Suite, Mobile-First ERP, Social/Collaborative ERP, Two-Tier/Edge ERP), Business Function (Finance and Accounting, Supply-Chain and Operations, Human Capital Management, Customer Relationship and Commerce, Manufacturing Execution and Quality), Deployment Model (On-Premise, and Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (Manufacturing, Retail and E-Commerce, BFSI, Government and Public Sector, IT and Telecom, Healthcare and Life Sciences, Other Industry Verticals), and Geography (North India, South India, East India, West India, Central India, Northeast India). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Native Suite |

| Mobile-First ERP |

| Social / Collaborative ERP |

| Two-Tier / Edge ERP |

| Finance and Accounting |

| Supply-Chain and Operations |

| Human Capital Management |

| Customer Relationship and Commerce |

| Manufacturing Execution and Quality |

| On-Premise |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises |

| Manufacturing |

| Retail and E-commerce |

| BFSI |

| Government and Public Sector |

| IT and Telecom |

| Healthcare and Life Sciences |

| Others Industry Vertical |

| By Type | Cloud-Native Suite |

| Mobile-First ERP | |

| Social / Collaborative ERP | |

| Two-Tier / Edge ERP | |

| By Business Function | Finance and Accounting |

| Supply-Chain and Operations | |

| Human Capital Management | |

| Customer Relationship and Commerce | |

| Manufacturing Execution and Quality | |

| By Deployment Model | On-Premise |

| Cloud | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Industry Vertical | Manufacturing |

| Retail and E-commerce | |

| BFSI | |

| Government and Public Sector | |

| IT and Telecom | |

| Healthcare and Life Sciences | |

| Others Industry Vertical |

Key Questions Answered in the Report

How large will the India enterprise resource planning market be by 2031?

It is forecast to reach USD 2.62 billion by 2031, expanding at a 16.08% CAGR from 2026-2031.

Which segment accounts for the highest India enterprise resource planning market share today?

Cloud-native suites held 53.77% share in 2025, making them the leading type segment.

Why are SMEs adopting ERP solutions faster than large enterprises?

Subsidies, low-entry cloud pricing, and credit programs tied to real-time ERP data drive a 19.2% CAGR for SME installations.

What is the main regulatory catalyst for ERP adoption?

Mandatory e-invoicing above INR 5 crore and stricter continuous-audit trail rules have turned ERP into a statutory requirement.

Page last updated on: