India Enterprise Content Management (ECM) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

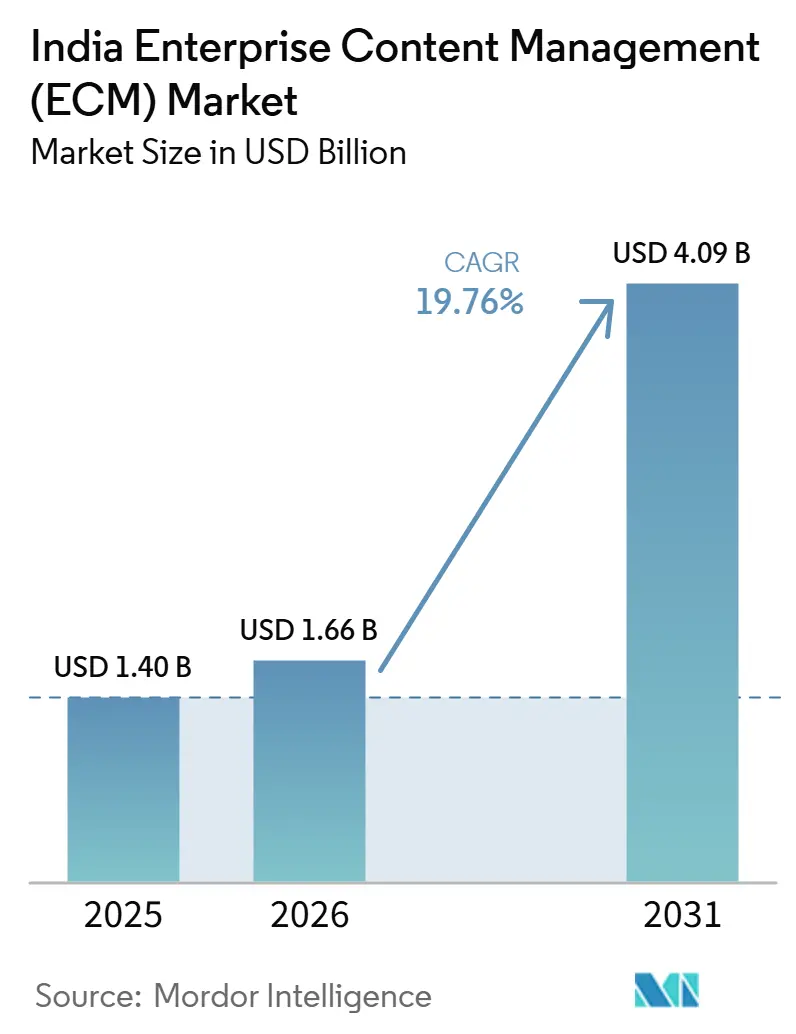

| Base Year Market Size (2025) | USD 1.40 Billion |

| Market Size (2026) | USD 1.66 Billion |

| Market Size (2031) | USD 4.09 Billion |

| Growth Rate (2026 - 2031) | 19.76% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Enterprise Content Management (ECM) Market Analysis by Mordor Intelligence

The India Enterprise Content Management (ECM) market size is expected to increase from USD 1.40 billion in 2025 to USD 1.66 billion in 2026 and reach USD 4.09 billion by 2031, growing at a CAGR of 19.76% over 2026-2031. The growth path reflects a broader shift toward digital records, cloud-based application delivery, and greater control over unstructured enterprise content. Regulatory requirements for audit trails, retention, access logs, and defensible recordkeeping are pushing content governance into core operating processes across many organizations. Vendors are also strengthening their India presence, which supports local deployment, customer support, and data residency needs for regulated buyers. Buyers are increasingly looking for platforms that connect document control with workflow execution, search, and automation, rather than treating content systems solely as storage tools. Integration with older enterprise systems still slows projects in some accounts, but demand remains broad and sustained across the India Enterprise Content Management (ECM) market.

Key Report Takeaways

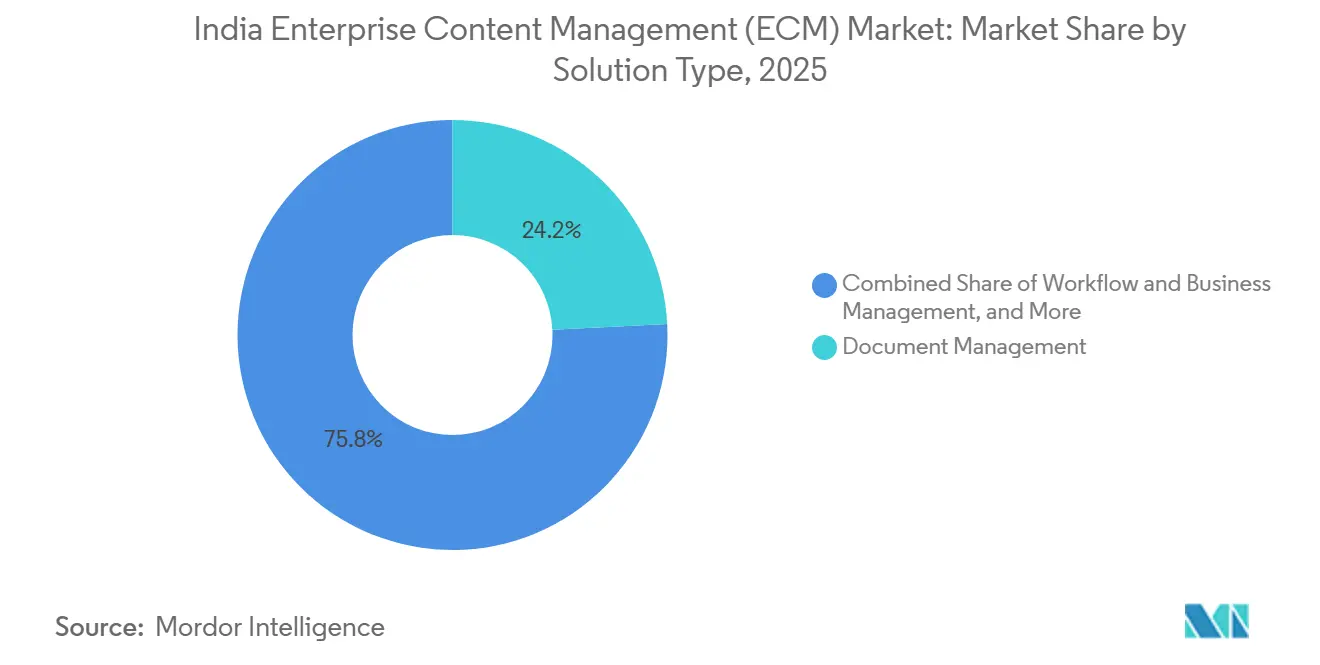

- By solution type, document management accounted for 24.18% of revenue share in 2025, while workflow and business process management is projected to expand at a 22.41% CAGR through 2031.

- By deployment mode, cloud held a 75.62% share of the India Enterprise Content Management (ECM) market in 2025, and is also projected to grow at a 21.84% CAGR through 2031.

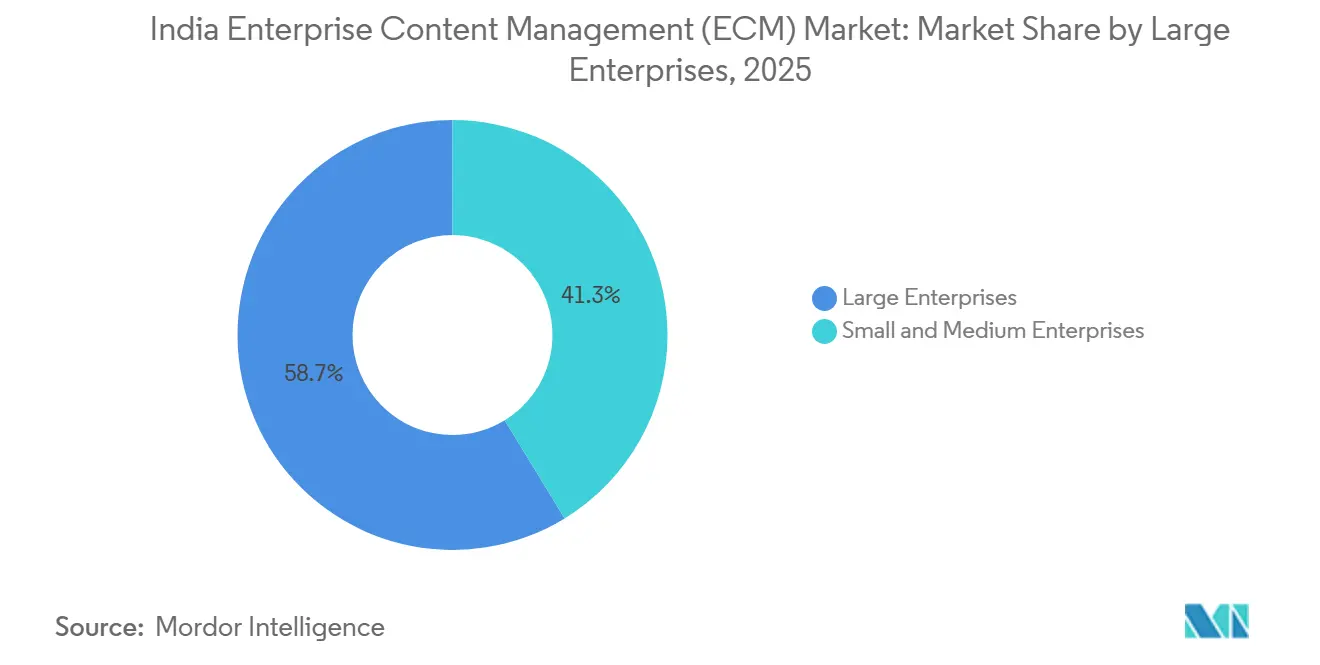

- By enterprise size, large enterprises held 58.74% share in 2025, while SMEs are projected to expand at 22.16% CAGR through 2031.

- By end-user industry, BFSI held 22.36% share of the India Enterprise Content Management (ECM) market in 2025, while healthcare is projected to grow at 23.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Enterprise Content Management (ECM) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Digital Transformation Across Indian Enterprises | +4.2% | National, with early gains in Bengaluru, Mumbai, Delhi, Hyderabad, and Pune technology corridors | Medium term (2-4 years) |

| Compliance-Driven Demand for Audit-Ready Content Control | +3.8% | National, concentrated in regulated centers including Mumbai, Delhi, and Chennai | Short term (≤ 2 years) |

| Shift Toward Cloud-Enabled Workflow Automation | +3.5% | National, with strong expansion into tier-2 cities | Medium term (2-4 years) |

| SME Adoption of Packaged ECM Platforms | +3.1% | National, with emerging gains in Jaipur, Coimbatore, Ahmedabad, and Surat | Long term (≥ 4 years) |

| AI-Assisted Metadata Classification and Search | +2.4% | National, with India as a major R&D base | Long term (≥ 4 years) |

| Multilingual Content Processing Requirements in India | +1.5% | National, especially in state governments and regional enterprise clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Digital Transformation Across Indian Enterprises

The India Enterprise Content Management (ECM) market is benefiting from a wider enterprise move toward digitized workflows and governed digital records. As organizations refresh ERP environments and extend cloud-based software across departments, they need a controlled layer for contracts, invoices, scanned forms, and email records that sit outside structured databases. That requirement is moving ECM from a back-office repository into a system that supports daily operating decisions. The role of content repositories is also changing, as classified and tagged documents now support search, retrieval, and AI-assisted knowledge access, rather than just simple storage. Government-backed language technology programs are adding relevance because enterprises increasingly need systems that can organize multilingual content at scale. This broader shift gives the India Enterprise Content Management (ECM) market a wider demand base across both large organizations and smaller firms.[1]Securities and Exchange Board of India, “Cybersecurity and Cyber Resilience Framework (CSCRF) for SEBI Regulated Entities,” SEBI

Compliance-Driven Demand for Audit-Ready Content Control

Tighter audit, retention, and access control requirements across regulated sectors are also shaping the India Enterprise Content Management (ECM) market. SEBI issued its Cybersecurity and Cyber Resilience Framework in August 2024, which increased the need for stronger audit-trail discipline, recoverability, and documented controls among regulated entities.[2]Digital India BHASHINI Division, “National Hub for Language Technologies Powers End-to-End AI at Population Scale,” Digital India Corporation This turns content governance into an ongoing operating requirement rather than a one-time compliance project. Banks, financial institutions, and capital market participants increasingly need content systems that can show who accessed a record, when it changed, and how it was retained. Newgen positioned its ECM offering around AML, KYC, Basel III, FATCA, and DPDP-related governance needs, reflecting buyer demand for compliance controls built into the platform. That pattern continues to support procurement across BFSI, government, and other regulated workflows in the India Enterprise Content Management (ECM) market.[3]Newgen Software Technologies Limited, “Enabling Compliance and Risk Management With ECM in Banking,” Newgen Software

Shift Toward Cloud-Enabled Workflow Automation

The India Enterprise Content Management (ECM) market is moving steadily toward cloud-enabled workflow automation, as buyers seek faster setup, simpler upgrades, and less infrastructure management. Cloud delivery shortens pilot cycles and makes it easier for organizations to test document workflows before expanding them across departments. It also allows vendors to package low-code workflow tools with records control, search, and collaboration features in a single subscription model. In regulated sectors, this does not always mean full public cloud adoption because many buyers still prefer hybrid or dedicated India-based environments for sensitive content. Hyland’s June 2026 collaboration with Microsoft to bring the Content Innovation Cloud to Azure shows how vendors are aligning ECM platforms with the cloud environments that Indian enterprises already use. As a result, the India Enterprise Content Management (ECM) market is seeing workflow automation become a central buying criterion rather than an optional add-on.[4]Hyland, “Hyland Collaborates With Microsoft to Power the Agentic Enterprise With the Content Innovation Cloud on Microsoft Azure,” PR Newswire

SME Adoption of Packaged ECM Platforms

The India Enterprise Content Management (ECM) market is seeing a new layer of demand from SMEs as subscription-based products lower adoption costs. Packaged deployments reduce the need for dedicated IT teams and shorten implementation timelines for businesses that want document control without large customization projects. This matters in India because smaller firms increasingly want systems that can handle lending files, supplier records, clinical forms, invoices, and compliance documentation in a structured way. Vendors are responding with vertical packages that combine records handling with pre-built workflows for sectors such as lending, insurance, healthcare, and manufacturing. The India Enterprise Content Management (ECM) market is therefore expanding through first-time adoption, as well as replacement spending by larger enterprises. This shift also creates room for smaller providers that can deliver focused modules faster than broader enterprise suites.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity With Legacy Enterprise Systems | -3.8% | National, with the sharpest pressure in manufacturing corridors and the public sector | Short term (≤ 2 years) |

| Data Sovereignty And Privacy Concerns For Cloud Deployment | -2.8% | National, with higher sensitivity in BFSI, government, and healthcare | Medium term (2-4 years) |

| Change Management And User Adoption Challenges | -1.8% | National, with stronger pressure in tier-2 and tier-3 cities | Long term (≥ 4 years) |

| Implementation Cost Pressure For Mid-Market Buyers | -0.9% | National, concentrated among mid-size manufacturers and regional healthcare providers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity with Legacy Enterprise Systems

A major restraint in the India Enterprise Content Management (ECM) market is the difficulty of connecting modern platforms with older enterprise systems. Many large organizations still operate a mix of legacy ERP tools, older document repositories, custom forms applications, and paper-heavy workflows that were built long before API-led integration became standard. That creates a fragmented content environment where files are stored in different formats and governed under inconsistent metadata rules. Migration is often slow because content must be reclassified before it can move into a modern system with search, retention, and workflow controls. Even when vendors use AI-assisted classification during ingestion, the project still demands specialist skills and careful mapping across business units. This complexity can delay decisions, stretch implementation timelines, and reduce initial deal size in the India Enterprise Content Management (ECM) market.

Data Sovereignty And Privacy Concerns for Cloud Deployment

Data sovereignty is another restraint because regulated buyers need stronger assurance on where content is stored, how it is accessed, and what controls apply to cloud-hosted records. This issue is especially visible in BFSI, government, and healthcare, where buyers often prefer hybrid or localized deployment patterns for sensitive information. SEBI’s framework has added pressure for stronger controls, resilience, and traceability, raising the bar for vendors serving regulated workflows. Vendors must also demonstrate that security controls, access policies, and retention settings align with India-specific expectations rather than relying on generic global templates. Hyland’s Azure partnership and the continued focus on local deployment support demonstrate how suppliers are addressing these concerns with region-specific delivery models. Until buyer confidence improves further, this issue will keep some workloads on hybrid or on-premises architectures within the India Enterprise Content Management (ECM) market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Workflow Automation Becomes The Fastest Revenue Engine

Document management accounted for 24.18% of the India Enterprise Content Management (ECM) market size in 2025, while workflow and business process management is projected to expand at 22.41% CAGR through 2031. This pairing shows that the category remains anchored in core document control, but new spending is moving toward process-linked use cases. Many Indian organizations still need to digitize paper-based records, standardize file storage, and improve retrieval across dispersed offices. That keeps document management large because it remains the starting point for regulated record keeping and searchable digital archives. At the same time, buyers increasingly want content systems that can trigger approvals, route forms, manage exceptions, and close business tasks without switching between several tools.

That shift is lifting workflow and business process management because enterprises are trying to reduce cycle time, manual review effort, and process fragmentation. Records management is also gaining relevance where retention rules and disposal controls matter, especially in government and regulated services. Case management is particularly relevant in healthcare and public service processes, where files move through several steps and users need context at each stage. Digital asset management is becoming increasingly important in retail, media, and e-commerce environments that handle growing volumes of content and brand assets. Web content management remains smaller, but it is being shaped by the need for more consistent publishing and controlled updates across institutional websites in the India Enterprise Content Management (ECM) industry.

By Deployment Mode: Cloud Leads While Hybrid Use Deepens

projected to grow at 21.84% CAGR through 2031. This lead reflects the ease of subscription buying, faster setup, and lower infrastructure burden for many organizations. It also reflects wider comfort with SaaS delivery for content-centric processes that do not require heavy local hardware investment. Even so, the cloud picture in India is more layered than the headline share suggests because many regulated deployments combine local data handling with cloud-based workflow and collaboration features. That is why hybrid architecture continues to matter in sectors that need both flexibility and tighter control over sensitive records.

On-premises deployments remain relevant in certain public-sector, defense-adjacent, and highly controlled enterprise settings, even as that share narrows over time. The cloud model is also the clearest path for SMEs that want a usable system without large implementation teams or dedicated infrastructure. Vendors are responding with pre-configured bundles for industries such as lending, healthcare, and document-heavy service operations. Hyland reinforced this direction by expanding its India footprint with a Hyderabad office in June 2025 and later extending its Azure-based cloud positioning through its Microsoft partnership in June 2026. As a result, deployment choice in the India Enterprise Content Management (ECM) market is no longer a simple cloud-versus-on-premises decision, but a fit question shaped by regulation, workload sensitivity, and internal IT capacity.

By Enterprise Size: SME Digitization Opens A New Demand Layer

Large enterprises accounted for 58.74% of the India Enterprise Content Management (ECM) market in 2025, while SMEs are projected to expand at a 22.16% CAGR through 2031. Large organizations still command the bigger share because they invested earlier in first-generation content systems and now have the budgets to refresh them. These buyers often need broader workflow orchestration, stronger compliance controls, and integration with ERP, CRM, and industry-specific platforms. Their decisions also tend to involve wider rollout plans across departments, business units, and branch networks. That keeps the large-enterprise segment central to total revenue even as growth shifts toward smaller firms.

SMEs are growing faster because cloud-based products reduce upfront cost and remove much of the infrastructure burden that once limited adoption. Within the India Enterprise Content Management (ECM) industry, SME demand is increasingly vertical rather than horizontal, as smaller firms typically seek a ready-made solution for a specific, regulated workflow. A lender wants loan file control, a hospital wants clinical document handling, and an exporter wants structured archival for invoices and related records. This creates an opportunity for vendors to deliver compliance-ready workflows with minimal setup time. Meanwhile, larger accounts still matter deeply for incumbents because expansion within existing customers remains an important revenue path in the India Enterprise Content Management (ECM) market.

By End-User Industry: BFSI Anchors Demand While Healthcare Expands Fastest

BFSI held 22.36% of the India Enterprise Content Management (ECM) market share in 2025, while healthcare is projected to grow at 23.08% CAGR through 2031. BFSI led because banks, insurers, lenders, and related institutions depend on content-intensive workflows such as KYC documentation, loan files, audit support, and compliance archiving. These use cases require strict retention, access control, version tracking, and retrieval discipline, which fit well with ECM capabilities. The segment also benefits from persistent regulatory pressure, which makes content governance part of operating risk management rather than a discretionary IT spend. This keeps BFSI at the center of the India Enterprise Content Management (ECM) market even as other verticals expand.

Healthcare is growing faster because digital health records, facility digitization, and interoperability needs are widening the use case for governed content systems. The Ayushman Bharat Digital Mission had linked more than 105 crore digital health records by July 2026, and more than 2.72 lakh healthcare facilities had adopted ABDM-enabled software. Government and public-sector demand remains important because digital file movement, record retention, and standardized publishing still require robust document control. IT and telecommunications, manufacturing, retail, and media and entertainment also sustain demand through contracts, quality records, supplier content, and digital assets. Education, energy, and utilities hold smaller shares, but structured records management is gradually becoming more relevant there as digitization and compliance requirements deepen.

Geography Analysis

India is projected to record 17.94% CAGR through 2031 within the Asia-Pacific ECM space, making it the fastest-growing national market in the region. The India Enterprise Content Management (ECM) market is concentrated first in the Mumbai-Pune corridor, where BFSI, insurance, and pharmaceutical operations create sustained demand for controlled records and audit-ready workflows. Delhi and the NCR region remain central for government and public sector deployments because ministries and national institutions continue to digitize file movement and publishing systems. Bengaluru and Hyderabad support both demand and supply because they house large IT services operations and major product engineering teams. This concentration gives large vendors a strong base in metro clusters before they extend deeper into regional markets.

Tier-2 cities are becoming an important growth layer for the India Enterprise Content Management (ECM) market as SMEs adopt cloud-based document and workflow tools. Cities such as Jaipur, Ahmedabad, Coimbatore, Indore, and Nagpur are moving from basic digitization toward more structured content handling in daily operations. Regional business clusters are therefore becoming increasingly relevant for first-time deployments, especially in finance, healthcare, manufacturing, and trade, where document control is tied to these sectors. State-level digitization programs are also widening the addressable base beyond the largest metros. That broader spread supports a more balanced demand map over the forecast period.

Geography within India also matters because regulated sectors, export manufacturing, and IT services each concentrate in different business clusters. Financial services demand remains strongest in western India, public sector demand is centered in Delhi, and technology-led adoption is strongest in the south. Vendor expansion reflects the same pattern, with Hyland opening a Hyderabad office in 2025 to support customer success, engineering, and regional operations in the country. As a result, the India Enterprise Content Management (ECM) market is likely to continue scaling from metro-led demand into broader state- and regional-level adoption through 2031.

Competitive Landscape

The India Enterprise Content Management (ECM) market remains moderately fragmented, with global platform vendors, specialist providers, and India-based players all competing for enterprise budgets. Newgen has a structural advantage in regulated accounts because its platform combines content services, low-code process automation, and intelligent document processing into a single stack designed for local compliance needs. Global vendors such as OpenText, IBM, Microsoft, Oracle, and SAP compete through broader enterprise relationships and integration depth. This keeps replacement cycles competitive because buyers often compare platform breadth against local regulatory fit. The result is a market where incumbency matters, but specialist differentiation still wins deals in BFSI, government, healthcare, and mid-market workflows.

Strategic moves show that vendors are trying to expand relevance rather than compete only on storage features. Hyland announced a partnership with Microsoft in June 2026 to bring the Content Innovation Cloud to Microsoft Azure, which strengthens its reach among enterprises already standardized on Azure and Microsoft 365. M-Files said in January 2026 that its FY2025 product cycle delivered more than 240 innovations, with deeper Microsoft 365 integration and stronger governance controls built into the platform. Hyland also expanded its India presence with a new Hyderabad office in June 2025, which shows that local customer support and engineering investment still matter in vendor selection. These moves show that product depth, Microsoft ecosystem fit, and country-level execution are shaping vendor positioning across the India Enterprise Content Management (ECM) market.

Another competitive theme is verticalization, with vendors tailoring their offerings for banking, insurance, public sector, and healthcare workflows rather than selling a single horizontal suite to every buyer. There is also room for multilingual content handling, as enterprises increasingly need classification and retrieval across Indian languages and mixed document types, and government language technology programs are beginning to support that foundation. This leaves space for differentiation even when larger platforms hold deep enterprise relationships. That mix of platform scale, local execution, and workflow specialization should keep competition active through the forecast period.

India Enterprise Content Management (ECM) Industry Leaders

Newgen Software Technologies Limited

Open Text Corporation

Hyland Software, Inc.

Microsoft Corporation

Box, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Hyland announced a strategic partnership with Microsoft to bring the Hyland Content Innovation Cloud to Microsoft Azure, enabling customers to deploy governed enterprise content management across Azure regions while maintaining local data residency and compliance requirements. The agreement expanded Hyland's cloud reach for India-based Azure customers and positioned it as an agentic enterprise content platform for Microsoft 365 environments.

- April 2026: Newgen Software Technologies reported FY2026 full-year consolidated revenue of INR 1,574 crore (USD 189 million), a 6% year-on-year increase, with subscription revenues growing 24% and SaaS revenue growing 36% year-on-year. The company grew its large customer base, clients with annual billing exceeding INR 5 crore, from 87 in FY2025 to 101 in FY2026, reflecting deeper wallet-share expansion within BFSI, government, and insurance segments.

- January 2026: M-Files announced that its FY2025 product cycle delivered over 240 new innovations, including context-first AI experiences, enterprise-grade governance controls, and native integration within Microsoft 365 applications including Teams, Word, PowerPoint, and Excel. The platform now holds almost 2 petabytes of data in its memory context, enabling AI-assisted decision-making at enterprise scale.

- September 2025: OpenText expanded its Bengaluru Center of Excellence with a new 70,000 sq ft facility housing 700 employees, following 194% workforce growth in Bengaluru over 2 years. The company indicated that 70% of its global R&D would be driven from India, with over 6,000 of its 9,000 engineers based in India across Bengaluru, Hyderabad, and Chennai.

India Enterprise Content Management (ECM) Market Report Scope

The India enterprise content management (ECM) market refers to the ecosystem of software solutions and services designed to systematically capture, manage, store, preserve, and deliver an organization's unstructured and structured content and documents within the country. This includes technologies such as document management, records management, workflow, business process management, case management, digital asset management, and web content management. Deployed on-premises, in the cloud, or in hybrid models, these solutions cater to organizations of all sizes across diverse industries in India, including BFSI, government, healthcare, IT, and manufacturing. Driven by the government's "Digital India" initiative, rapid digital transformation across sectors, and the growing need to comply with evolving data protection regulations (such as the Digital Personal Data Protection Act), ECM solutions enable Indian businesses to streamline complex administrative workflows, enhance cross-departmental collaboration, ensure robust information governance, and transition from legacy paper-based systems to highly efficient, digitized operations.

The India Enterprise Content Management (ECM) Market Report is Segmented by Solution Type (Document Management, Records Management, Workflow and Business Process Management, Case Management, Digital Asset Management, Web Content Management, and Other Solutions), Deployment Mode (On-Premises, Cloud, and Hybrid), Enterprise Size (Small and Medium Enterprises, and Large Enterprises), and End-User Industry (BFSI, Government and Public Sector, Healthcare, IT and Telecommunications, Manufacturing, Retail, Media and Entertainment, Education, Energy and Utilities, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Document Management |

| Records Management |

| Workflow and Business Process Management |

| Case Management |

| Digital Asset Management |

| Web Content Management |

| Other Solutions |

| On-Premises |

| Cloud |

| Hybrid |

| Small and Medium Enterprises |

| Large Enterprises |

| BFSI |

| Government and Public Sector |

| Healthcare |

| IT and Telecommunications |

| Manufacturing |

| Retail |

| Media and Entertainment |

| Education |

| Energy and Utilities |

| Other End-User Industries |

| By Solution Type | Document Management |

| Records Management | |

| Workflow and Business Process Management | |

| Case Management | |

| Digital Asset Management | |

| Web Content Management | |

| Other Solutions | |

| By Deployment Mode | On-Premises |

| Cloud | |

| Hybrid | |

| By Enterprise Size | Small and Medium Enterprises |

| Large Enterprises | |

| By End-User Industry | BFSI |

| Government and Public Sector | |

| Healthcare | |

| IT and Telecommunications | |

| Manufacturing | |

| Retail | |

| Media and Entertainment | |

| Education | |

| Energy and Utilities | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the size outlook for enterprise content management in India?

The India Enterprise Content Management (ECM) market is expected to rise from USD 1.66 billion in 2026 to USD 4.09 billion by 2031, at a CAGR of 19.76% over 2026-2031.

Which deployment model leads adoption in India?

Cloud led with 75.62% share in 2025 and is also projected to grow at 21.84% CAGR through 2031, supported by faster rollout and lower infrastructure burden.

Which solution category is growing the fastest?

Workflow and business process management is the fastest-growing solution type, with a projected 22.41% CAGR through 2031, as buyers link content control more closely with process execution.

Why does BFSI remain the largest end-user segment?

BFSI led with 22.36% share in 2025 because it relies heavily on KYC files, loan records, audit trails, and compliance archiving that require strong control and retrieval.

Why is healthcare expanding faster than other verticals?

Healthcare is projected to grow at 23.08% CAGR through 2031, supported by the expansion of digital health records and wider use of ABDM-enabled software across facilities.

What is driving SME adoption in this space?

SMEs are projected to grow at 22.16% CAGR through 2031 because subscription-based platforms, packaged workflows, and lighter deployment needs have lowered adoption barriers.

Page last updated on: