India Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.31 Billion |

| Market Size (2026) | USD 0.41 Billion |

| Market Size (2031) | USD 1.87 Billion |

| Growth Rate (2026 - 2031) | 35.46% CAGR |

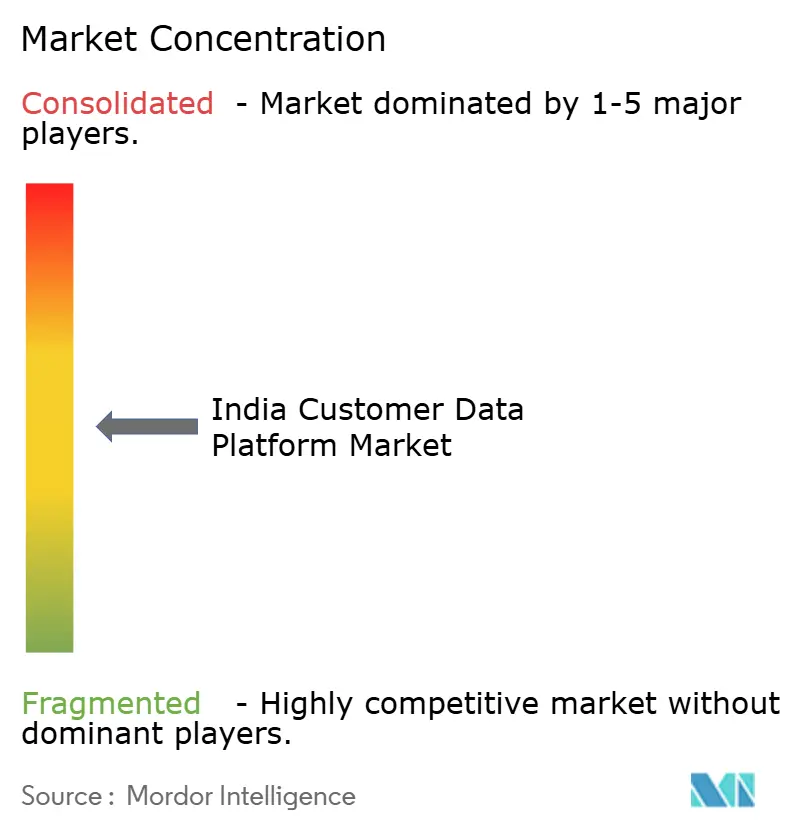

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Customer Data Platform Market Analysis by Mordor Intelligence

The India customer data platform market size is expected to increase from USD 0.31 billion in 2025 to USD 0.41 billion in 2026 and reach USD 1.87 billion by 2031, growing at a CAGR of 35.5% over 2026-2031. The shift toward first-party data, tighter consent handling requirements, and broader use of AI in customer engagement are supporting growth. The Digital Personal Data Protection Rules, notified in November 2025, have accelerated buying decisions because enterprises now need systems that can capture, store, and honor consent across channels. The India customer data platform market is also moving beyond campaign execution, as companies link customer data programs to governance, retention, service quality, and operating control. Competition is intensifying between global platform vendors and India-native providers, keeping product design focused on faster integration, greater compliance readiness, and local pricing flexibility. The main opportunity now sits in large implementation programs and mid-market adoption, while the main constraint remains limited specialist talent for identity resolution, consent architecture, and real-time data pipelines.

Key Report Takeaways

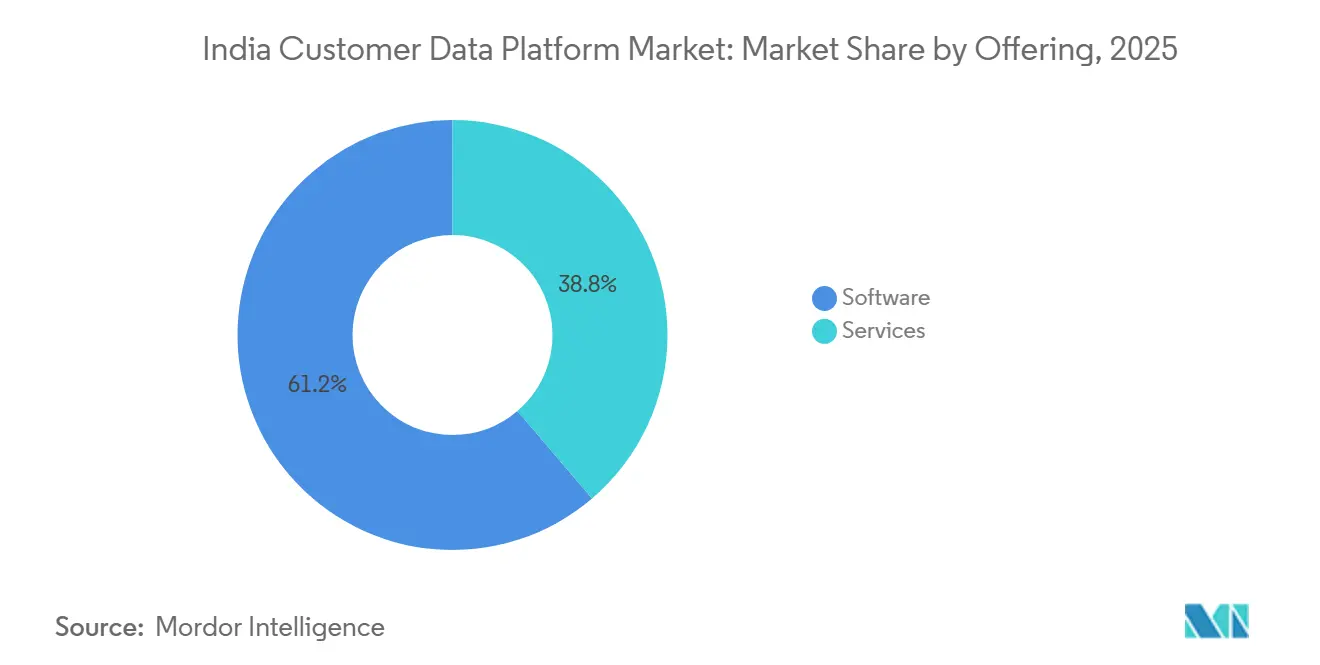

- By offering, software held 61.24% revenue share in the India customer data platform market in 2025, while services are projected to record the fastest growth at 38.73% CAGR through 2031.

- By deployment mode, cloud accounted for 68.47% of the market in 2025, while hybrid is forecast to expand at a 41.29% CAGR through 2031.

- By organization size, large enterprises accounted for 54.83% of the market in 2025, while SMEs are expected to grow fastest at a 39.16% CAGR through 2031.

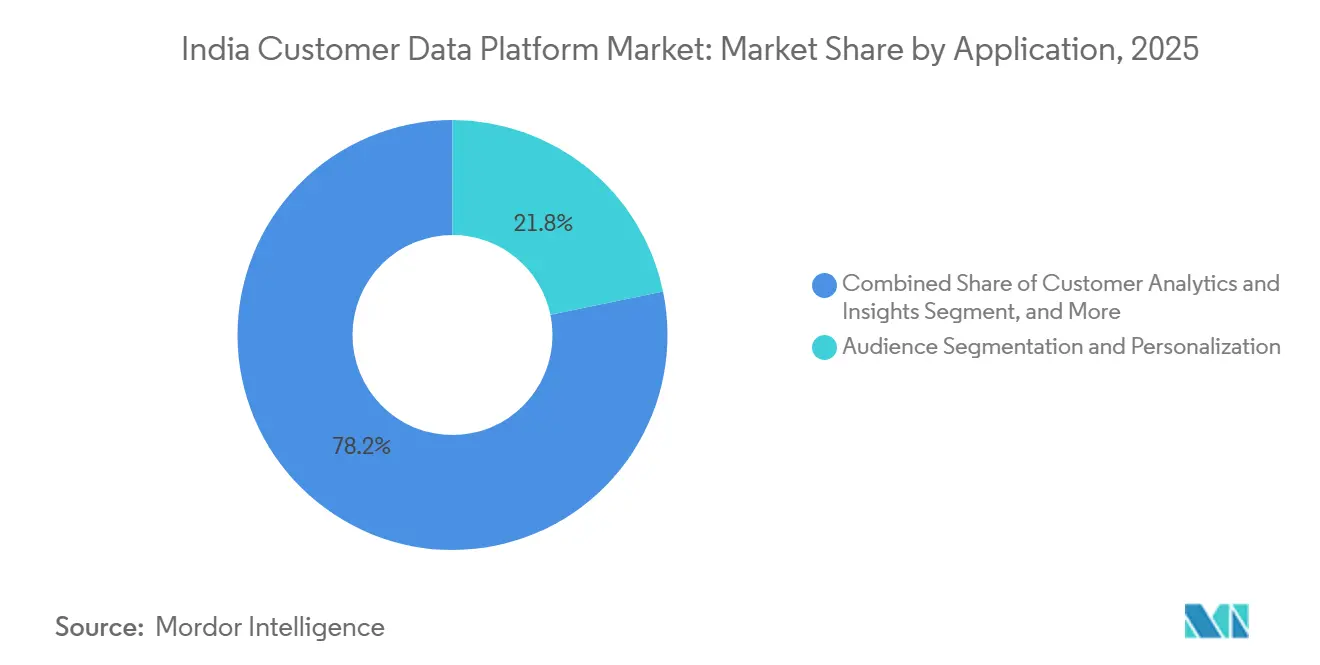

- By application, audience segmentation and personalization held a 21.76% share in 2025, while customer analytics and insights are projected to grow at a 42.81% CAGR through 2031.

- By end-user industry, retail and e-commerce accounted for 23.91% of the market share in 2025, while media and entertainment is forecast to grow fastest at a 37.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unified Customer Profile Demand | +5.8% | National, concentrated in Mumbai, Bengaluru, NCR, Hyderabad | Short term (≤ 2 years) |

| Omnichannel Personalization Expansion | +5.2% | National, with early gains in metro retail corridors and D2C hubs | Short term (≤ 2 years) |

| Cloud-Native Stack Migration | +4.6% | National, linked to hyperscaler zones in major enterprise corridors | Medium term (2-4 years) |

| DPDP-Led Privacy Architecture Investment | +4.1% | National, with pressure highest in BFSI, healthcare, and telecom | Medium term (2-4 years) |

| Real-Time Journey Orchestration Demand | +3.3% | National, led by consumer internet, fintech, and quick commerce | Medium term (2-4 years) |

| AI-Led Segmentation and Propensity Modeling | +2.9% | National, with early scaling in Bengaluru and Hyderabad engineering centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Need for Unified Customer Profiles

The India customer data platform market is being driven by a fundamental operating problem: fragmented customer information across too many systems. Customer activity now spans apps, websites, WhatsApp, stores, and service channels within the same buying cycle, so a single customer record often sits in multiple incomplete versions. This leaves marketing, service, and analytics teams working with inconsistent identifiers, duplicated records, and poor visibility into the full customer journey. As a result, many personalization programs underperform even when the business has strong campaign tools and solid spending capacity. The commercial value of a cleaner identity layer has become easier for enterprises to see because retention, conversion, and suppression logic work better once duplicate and stale records are removed. The India customer data platform market, therefore, benefits when enterprises stop treating profile unification as a campaign feature and start treating it as a base layer for customer operations.

Expansion of Omnichannel Personalization Use Cases

The India customer data platform market is also gaining from the steady spread of omnichannel engagement models across consumer-facing sectors. Mobile-led traffic patterns in India create strong pressure for fast message timing, coordinated suppression, and consistent treatment across push, app, browser, and messaging channels. This is moving platform demand beyond simple segmentation toward always-on orchestration, where customer context must be updated in real time. Enterprises are also buying with a broader operational goal in mind, seeking data systems that can support automated decisioning as AI use rises. That keeps the focus on platforms that can move from profile storage to activation without large handoffs across disconnected tools. The India customer data platform market is therefore expanding not only because brands want more personalization, but also because they need one system to coordinate many forms of personalization at the same time.

Faster Migration to Cloud Native Marketing Stacks

The India customer data platform market is being supported by broader migration toward cloud-native enterprise architectures. When companies modernize CRM, commerce, ERP, and analytics systems, they often reopen the question of how customer data should be stitched, governed, and activated. Older on-premises environments are harder to extend to real-time streaming and AI-linked workflows, so CDP evaluations are increasingly tied to larger modernization programs. This pattern is visible in greenfield, and large transformation builds where cloud design choices are made early in the stack. Birla Opus Paints was built on a full SAP cloud stack from inception, demonstrating how cloud-based data and application design are already shaping new enterprise environments in India.[1]SAP India News Center, “From Inception to Scale, Birla Opus Paints Build a Future-Ready Paints Enterprise With SAP Cloud Transformation,” SAP India News Center, news.sap.com The India customer data platform market benefits from this because CDP deployment becomes easier to justify when the surrounding architecture is already being rebuilt for speed, integration, and scale.

Privacy-First Data Architecture Investment Under DPDP Compliance

The India customer data platform market is receiving a strong push from privacy and consent requirements under the Digital Personal Data Protection framework. Once consent handling becomes a compliance issue rather than a marketing preference, enterprises need a system that can log permissions, propagate revocations, and maintain audit readiness across downstream tools. This changes the buying logic because the platform is now judged not only on campaign outcomes but also on governance reliability. It also raises the value of data models that can separate identity, consent status, and activation logic without breaking customer experience flows. Companies that adopt privacy-led architecture early are likely to avoid costly retrofits later as enforcement expectations become clearer. The India customer data platform market is therefore benefiting from regulation, not because regulation creates demand by itself, but because it makes it harder to postpone customer data discipline.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy CRM and Commerce Integration Complexity | -2.8% | National, concentrated in manufacturing, retail, and BFSI enterprises with long legacy stacks | Medium term (2-4 years) |

| Shortage of CDP and Governance Talent | -2.4% | National, most acute outside Bengaluru, Hyderabad, and NCR | Long term (≥ 4 years) |

| Consent and Audit Readiness Costs | -2.0% | National, with elevated burden in BFSI, healthcare, and telecom | Medium term (2-4 years) |

| MarTech Budget Preference for Short-Term Tools | -1.7% | National, concentrated in mid-market and SME segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Integration Complexity Across Legacy CRM and Commerce Systems

The India customer data platform market still faces a serious execution barrier: legacy integration complexity. Many large enterprises continue to run older CRM systems, loyalty systems, branch platforms, on-premises ERP environments, and channel tools that were not designed to exchange customer records in real time. This means that even when a company is ready to buy a CDP, the work needed to connect source systems can slow the rollout for many months. The problem is not only technical because data fields, customer identifiers, and process ownership are often inconsistent across business units. That pushes more cost into services, testing, and change management, which can delay the realization of value. The India customer data platform market, therefore, grows fastest where enterprises already have cleaner source systems or where leadership is prepared to properly fund the integration layer.

Shortage of CDP Implementation and Data Governance Talent

The India customer data platform market is also constrained by a limited pool of specialists capable of executing these programs effectively. Identity resolution, event streaming, consent design, profile modeling, and downstream activation each need different skills, and those skills do not always sit in the same team. The talent gap widens when a project also requires regulatory familiarity, security discipline, and sector-specific data-handling standards. This is one reason why adoption remains concentrated in major technology corridors, where experienced engineers and platform specialists are easier to find. It also explains why some mid-market firms choose lighter engagement tools instead of deeper data platforms, even when the long-term data case favors the CDP route. The India customer data platform market will continue to attract demand, but implementation speed will remain uneven until the delivery talent base becomes broader across cities and company sizes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Incumbency Gives Way to Services-Led Delivery

Software held 61.24% of the India customer data platform market share in 2025, indicating that early buyers focused on core platform licensing. Enterprises first spent on ingestion, identity resolution, and profile unification because those elements had to be in place before activation models could scale. This pattern fits the early phase of the India customer data platform market, where buyers focused on building the system foundation before committing to more extensive managed support. Many first-generation deployments were therefore structured around product ownership, internal control, and architecture selection. Software also remained the clearest starting point for enterprises that were still defining governance, consent, and channel coordination models.

The picture is now changing because services are projected to grow at a 38.73% CAGR through 2031, reflecting the rising complexity of implementation, integration, and ongoing tuning. Buyers are learning that value comes less from installation and more from data mapping, workflow design, and model refinement after go-live. Tealium reported that 84% of CDP users said their platform simplifies AI projects when the data foundation is properly built, which supports the case for deeper services engagement around architecture and readiness.[2]Tealium, “2025 Future of Customer Data Report,” Tealium, tealium.com This is why the India customer data platform industry is shifting toward delivery models in which implementation partners, internal data teams, and vendors remain involved longer after deployment. The India customer data platform market is likely to keep this tilt because reimplementation work, real-time upgrades, and consent redesign add recurring service demand on top of initial product revenue.

By Deployment Mode: Hybrid Becomes the Architecture of Choice

Cloud accounted for 68.47% of the India customer data platform market in 2025, confirming that most new buyers favored scalable, easier-to-update deployment models. Cloud environments fit well with enterprises that want faster rollout cycles, easier connector management, and better alignment with modern analytics and AI layers. The India customer data platform market also benefits from the fact that many enterprise software stacks are already being redesigned around cloud-centered operations. This gives CDP vendors a more familiar deployment environment and reduces friction in data exchange with surrounding applications. Cloud, therefore, remains the default for many new programs, especially where speed and operational flexibility matter more than full in-house control of infrastructure.

At the same time, hybrid is forecast to grow at a 41.29% CAGR through 2031, as regulated enterprises seek a balance between local control and scalable processing. Hybrid design allows sensitive records and consent data to remain under tighter internal control while compute-intensive activation and analytics tasks move to cloud environments. This has become more relevant in sectors where governance expectations are strict, and the cost of mishandling customer records is high. The India customer data platform market is seeing hybrid become a practical compromise rather than a temporary step, especially in banking, insurance, and other policy-driven settings. The rising interest in certification filters and a stronger governance architecture also supports this shift, as hybrid deployments often align better with internal audit preferences and regulated operating models.

By Organization Size: SMEs Close the Gap as Composable CDPs Democratize Entry

Large enterprises represented 54.83% of the India customer data platform market share in 2025, reflecting their earlier ability to fund enterprise-grade customer data programs. These buyers had the scale, channel complexity, and internal digital maturity to justify major investments before the broader field reached its current level of adoption. Large retailers, telecom operators, financial institutions, and consumer-facing groups were among the first to face pressure to unify customer records across multiple touchpoints. That gave them a head start in architecture building, vendor evaluation, and internal operating model changes. The India customer data platform market, therefore, still draws a large portion of current revenue from organizations that entered early and now need to deepen or refresh existing deployments.

SMEs are projected to expand at a 39.16% CAGR through 2031, indicating that the next growth wave is moving into smaller, more modular buying environments. This shift is being helped by API-first product design, narrower deployment packages, and pricing that is easier to fit into local budgeting cycles. The India customer data platform market is becoming more reachable for this group because companies no longer need a full enterprise stack to begin consolidating profiles and using customer signals more effectively. India-native vendors also lower entry barriers by offering modular activation paths and channel support tailored to local commerce and messaging habits. The India customer data platform industry is therefore broadening from an enterprise-led base to a more distributed market, although the speed of SME adoption will still depend on implementation support and clear proof of value.

By Application: Personalization Anchors Revenue, Analytics Drives the Next Wave

Audience segmentation and personalization accounted for 21.76% of the market share in 2025, confirming that most early CDP purchases were justified by more effective targeting and lower campaign waste. Enterprises could explain these investments internally because better segmentation directly affects conversion logic, suppression efficiency, and customer relevance. This meant the first application focus of the India customer data platform market stayed close to revenue-facing use cases that marketing teams could operationalize quickly. It also met the needs of businesses seeking to move away from broad campaign blasts toward more selective, cohort-based engagement. Personalization, therefore, anchored near-term value because it was the easiest application area to connect to visible performance outcomes.

Customer analytics and insights are projected to grow at a 42.81% CAGR through 2031, signaling that enterprises now want a stronger interpretation of customer behavior, not just better list creation. Customer Analytics and Insights is set to post the fastest growth in the India customer data platform market, with a 42.81% CAGR through 2031, as buyers place greater value on understanding why a customer behaves a certain way and what action should follow. That underscores the importance of propensity models, churn signals, and decision-support tools that rely on cleaner, more current profile data. The India customer data platform market is therefore moving from profile assembly toward analytical usefulness, which is a natural step once basic unification has already been funded. Consent and preference management also becomes relevant in this application mix because analytics, activation, and governance now need to operate within the same profile and permission framework.

By End-User Industry: Retail Dominates, but Media and Entertainment Rewrites the Growth Story

Retail and e-commerce accounted for a 23.91% share in 2025, making it the largest end-user segment in the India customer data platform market. This leadership is tied to the scale, frequency, and data intensity of online and omnichannel retail interactions, where product discovery, cart behavior, repeat purchase patterns, and promotion response generate large volumes of usable signals. Retail buyers also tend to feel customer experience gaps more quickly because fragmented data can weaken personalization, attribution, and service continuity in visible ways. That is why the India customer data platform market has found a strong anchor in retail and e-commerce, where the case for a unified customer record is easier to make across teams. BFSI, IT and telecom, and healthcare and life sciences also represent active adoption areas, though each brings a different mix of governance pressure, infrastructure readiness, and integration depth.

Media and entertainment is forecast to grow at a 37.54% CAGR through 2031, making it the fastest-growing end-user segment in the India customer data platform market. High user volumes, fast session changes, and content recommendation needs create a strong requirement for real-time profile resolution and quick decisioning. This makes the sector an important growth story, as the customer record must remain up to date while the user remains active on the platform. The India customer data platform market is therefore benefiting from streaming-led demand for fast identity and content relevance, while government and public administration and industrial manufacturing remain earlier in the adoption cycle. That gap across sectors suggests that near-term growth will continue to come first from data-rich consumer environments and then move outward into slower-to-modernize operating contexts.

Geography Analysis

The India customer data platform market remains geographically concentrated rather than evenly distributed nationwide. South India, especially Bengaluru and Hyderabad, serves as a major implementation base because it brings together technology enterprises, product engineering teams, global capability centers, and India-native MarTech vendors within the same operating corridor. This concentration helps the India customer data platform market by making data engineering talent, vendor support, and implementation experience easier to access in these cities. It also shortens execution cycles for enterprises that need complex identity resolution, event streaming, and channel orchestration work.

Maharashtra, led by the Mumbai metropolitan region, remains central to the India customer data platform market because it anchors a large share of the country’s BFSI activity. Banks, insurers, and financial service firms in this corridor face simultaneous pressure from localization expectations, privacy compliance, and digital competition, which keeps customer data modernization high on the agenda. This produces a different buying pattern from the technology corridor because many projects here are upgrade or replacement programs rather than first-time greenfield builds. The National Capital Region has also become an important center for the Indian customer data platform market, as large consumer brands, retail groups, and public-facing enterprises are placing greater emphasis on controlling first-party data. The region’s role is strengthened by the presence of large corporate headquarters and broader digital transformation budgets, which make it easier to sponsor multi-team customer data programs.

Tier-2 cities such as Pune, Ahmedabad, Chennai, and Kochi are still smaller in terms of installed base, but they represent a growing opportunity for the India customer data platform market. Growth in these cities is being helped by D2C expansion, regional fintech activity, and wider digital business adoption. Multilingual consent handling is becoming more important in these markets because customer acquisition and service journeys often extend beyond English-only environments. The India customer data platform market is therefore likely to widen geographically as vendors offer modular deployment, local pricing, and features that fit regional operating needs.

Competitive Landscape

The India customer data platform market has split into a few clear competitive layers, but the boundaries between them are becoming harder to maintain. At the enterprise level, Adobe, Salesforce, Oracle, and SAP continue to benefit from existing CRM and ERP relationships, which give them a strong starting point with large accounts. Their advantage comes from installed software footprints, broader suite integration, and the ability to position CDP functions within a larger enterprise transformation agenda. This means the India customer data platform market still gives global vendors a durable path into complex accounts where governance, scale, and multi-system integration matter most. SAP’s work with Asian Paints shows how incumbent enterprise vendors are using broader transformation programs to deepen control over data unification and adjacent customer workflows.[3]SAP, “A Brighter Shade of Innovation, Asian Paints Transforms Their Business With SAP,” SAP, sap.com

A second layer in the India customer data platform market is formed by India-native or India-focused players such as FirstHive, Lemnisk, and MoEngage, as well as composable providers that compete on flexibility, execution speed, and local operating fit. These vendors are often more competitive in regulated or mid-market accounts where pricing structure, faster turnaround, and local support matter heavily. Their position improves when buyers want data residency awareness, easier WhatsApp-linked activation, or deployment patterns that fit local budget cycles. Lemnisk’s November 2025 secondary transaction, led by Bajaj Financial Securities, reflects rising interest in India-built customer data infrastructure for enterprise use cases, especially in financial-regulated sectors. The India customer data platform market is therefore not moving toward a simple global-versus-local split, because many accounts now evaluate vendors on execution model and sector fit rather than on brand scale alone.

A third theme in the India customer data platform market is the amount of open space that still exists in government programs, healthcare data unification, and the SME base. These areas remain less penetrated because standards, budgets, and implementation readiness are still uneven across buyers. Newer entrants can still gain ground if they bring differentiated data models or a better fit with emerging digital rails. Ignosis raised USD 4 million to build customer data intelligence on the Account Aggregator rail, which shows that domain-linked data enrichment can create an alternative path into the market. Zeta’s partnership with Palantir to rebuild Zeta’s Data Cloud on Palantir Foundry also shows how vendors are trying to anchor future competition around governed AI infrastructure rather than campaign execution alone. Zeta’s Open Semantic Interchange move with Snowflake aligns with this trend, as interoperability is becoming part of the competitive offer in AI-linked data systems. The India customer data platform market is likely to remain contested, as buyers are still deciding whether long-term value comes more from suite depth, local execution strength, or architecture openness.[4]Zeta Global Investors, “Palantir and Zeta Global Announce Strategic Partnership to Build a Unified Data and AI Infrastructure for the Future of Marketing With Athena by Zeta at the Center,” Zeta Global Investors, investors.zetaglobal.com

India Customer Data Platform Industry Leaders

Salesforce, Inc.,

Adobe Inc.

Oracle Corporation

Tealium, Inc

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Zeta Global Corp. (NYSE: ZETA) announced a strategic partnership with Palantir Technologies on June 23, 2026, to rebuild Zeta's Data Cloud on Palantir Foundry as an enterprise AI infrastructure layer. The seven-year agreement, announced at Cannes Lions, integrates Zeta's Athena AI decisioning layer with Palantir's operational ontology, targeting enterprise clients requiring auditable, governed marketing AI at scale.

- June 2026: MoEngage launched Merlin AI Custom Agents on June 3, 2026, enabling lifecycle marketers and CRM teams to build custom workflow agents on top of MoEngage data with marketer-defined guardrails and an open Model Context Protocol (MCP) architecture compatible with Claude and ChatGPT.

- June 2026: Zeta Global joined the Open Semantic Interchange (OSI) initiative with Snowflake on May 15, 2026, to establish a vendor-neutral universal data standard for AI-powered marketing. OSI membership ensures Zeta's Zeta Marketing Platform data and insights interoperate with enterprise data stacks without custom integration work.

- April 2026: Twilio Inc. was named a Leader in the 2026 IDC MarketScape for Worldwide Communications Engagement Platforms and the 2026 Omdia Universe for Customer Engagement Platforms on April 22, 2026. In 2025, Twilio powered more than 2.5 trillion customer interactions for more than 402,000 active customer accounts.

India Customer Data Platform Market Report Scope

The India customer data platform (CDP) market refers to the ecosystem of software and associated services that enable organizations in India to collect, unify, and manage customer data from multiple touchpoints into a single, persistent database. These platforms are designed to break down data silos, creating comprehensive customer profiles that can be leveraged for advanced audience segmentation, personalized marketing campaigns, customer journey orchestration, and predictive analytics. The market encompasses cloud, on-premises, and hybrid deployment models tailored to the operational needs of large and small and medium enterprises across sectors such as retail, BFSI, healthcare, and IT. By integrating consent and preference management capabilities, CDPs help Indian businesses comply with evolving local data protection regulations (such as the Digital Personal Data Protection Act) while enhancing customer experience, driving brand loyalty, and improving overall marketing return on investment.

The India Customer Data Platform Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), and End-User Industry (Retail and E-Commerce, BFSI, Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| BFSI | |

| Healthcare and Life Sciences | |

| IT and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the forecast value of the India customer data platform space by 2031?

It is projected to reach USD 1.87 billion by 2031 from USD 0.41 billion in 2026, growing at 35.5% CAGR over 2026-2031.

What is driving adoption of customer data platforms in India right now?

The main drivers are first-party data needs, omnichannel personalization, privacy and consent requirements under DPDP, and the move toward AI-enabled customer engagement.

Which deployment model leads in 2025 and which one is growing fastest?

Cloud led with 68.47% share in 2025, while hybrid is forecast to grow fastest at 41.29% CAGR through 2031.

Why are services growing faster than software in this space?

Services is growing faster because integration, configuration, governance, and ongoing model tuning now determine whether enterprises can realize value from CDP deployments.

Which application is expanding fastest through 2031?

Customer analytics and insights is the fastest-growing application, with a projected 42.81% CAGR through 2031, ahead of other use cases.

Which end-user group currently leads demand in India?

Retail and e-commerce led in 2025 with 23.91% share, while media and entertainment is expected to post the fastest growth at 37.54% CAGR through 2031.

Page last updated on: