India Construction Ornamental Stone Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

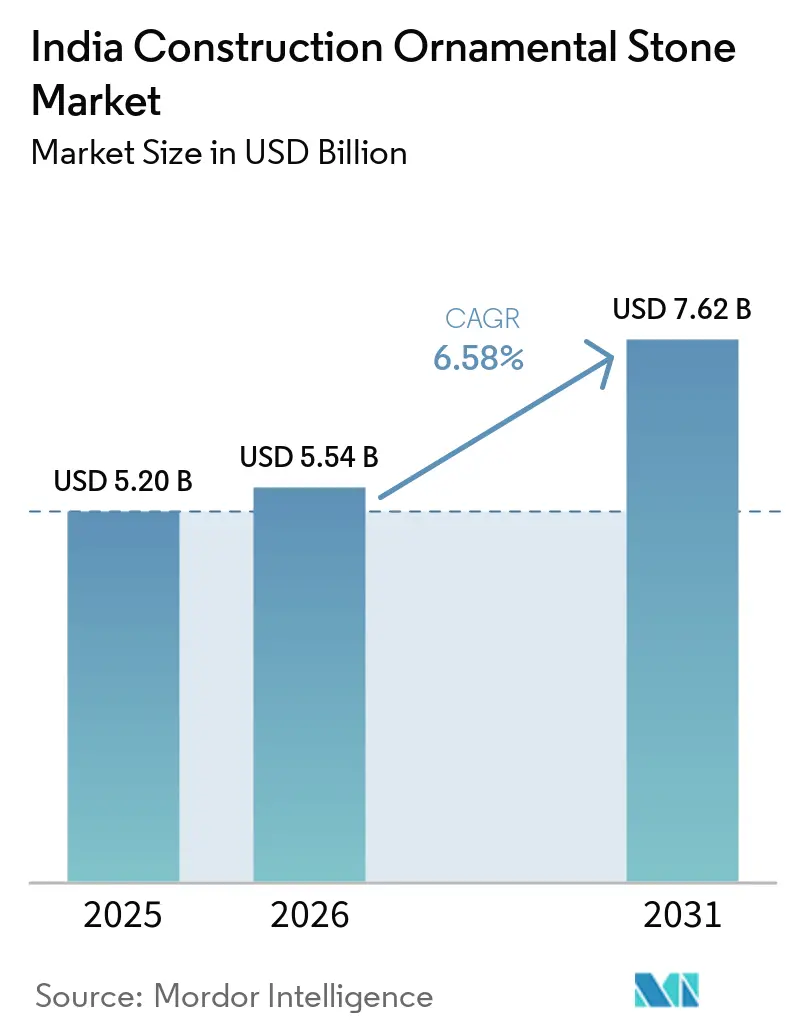

| Base Year Market Size (2025) | USD 5.20 Billion |

| Market Size (2026) | USD 5.54 Billion |

| Market Size (2031) | USD 7.62 Billion |

| Growth Rate (2026 - 2031) | 6.58% CAGR |

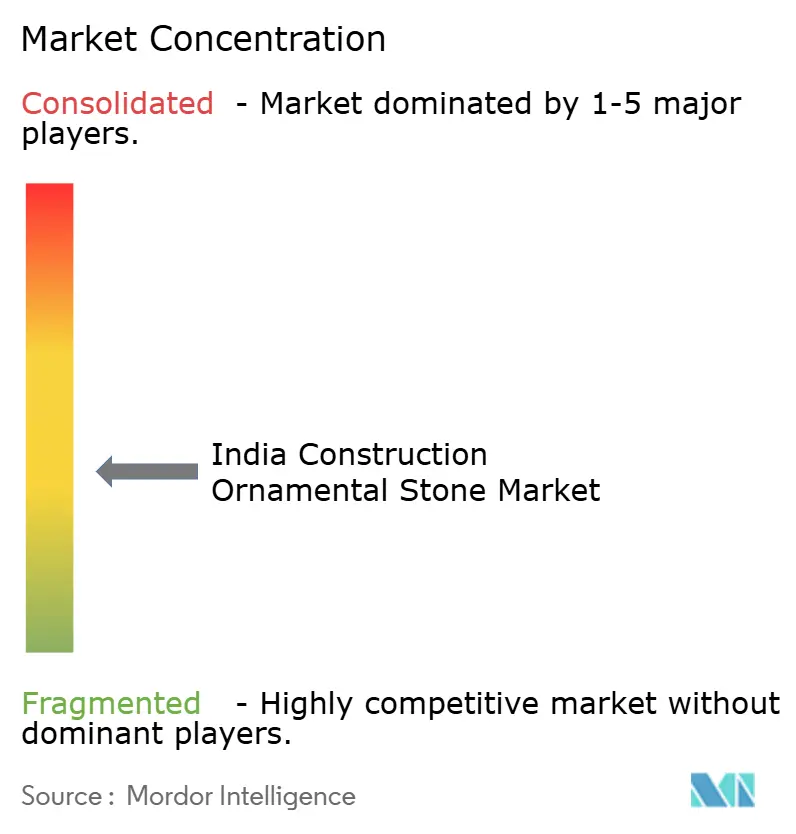

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Construction Ornamental Stone Market Analysis by Mordor Intelligence

The India construction ornamental stone market size is expected to grow from USD 5.20 billion in 2025 to USD 5.54 billion in 2026 and is forecast to reach USD 7.62 billion by 2031 at 6.58% CAGR over 2026-2031. Rising demand from luxury housing, the Smart Cities Mission, and metro-rail infrastructure is expanding addressable volumes even as the 28% goods and services tax (GST) on polished stone suppresses mid-tier residential uptake. Engineered quartz is closing the price gap with mid-grade granite after tariff relief and domestic joint ventures, while dry-cladding systems that cut installation times by up to 40% are accelerating adoption in high-rise projects. Stricter quarrying norms in Rajasthan and Karnataka are increasing compliance costs, but they are also lifting product quality by forcing modernization of extraction techniques. Collectively, these dynamics support steady value growth in the India construction ornamental stone market despite pricing pressures at the mass end.

Key Report Takeaways

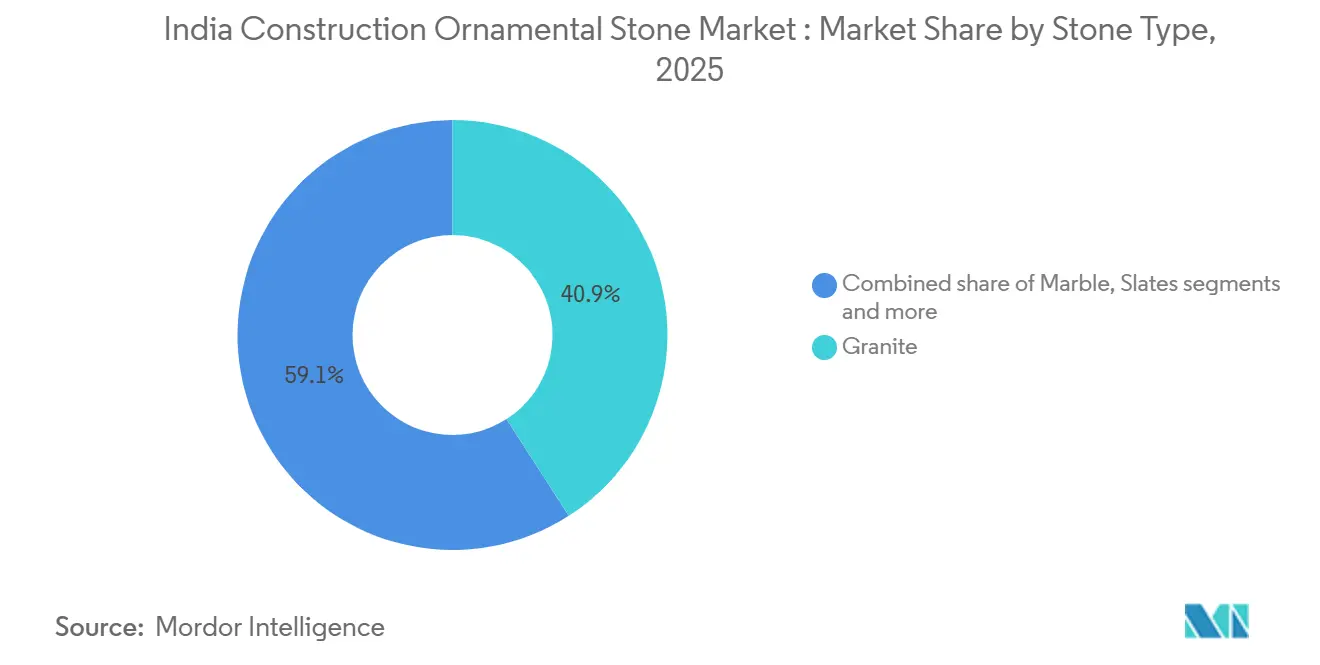

- By stone type, granite accounted for 40.9% of revenue in 2025, while quartzite and slate continued to gain visibility in premium façade and hospitality work in the India construction ornamental stone market.

- By manufacturing type, raw and unpolished stone accounted for 80.6% of revenue in 2025, while polished slabs are forecast to grow at 7.8% CAGR through 2031 in the India construction ornamental stone market.

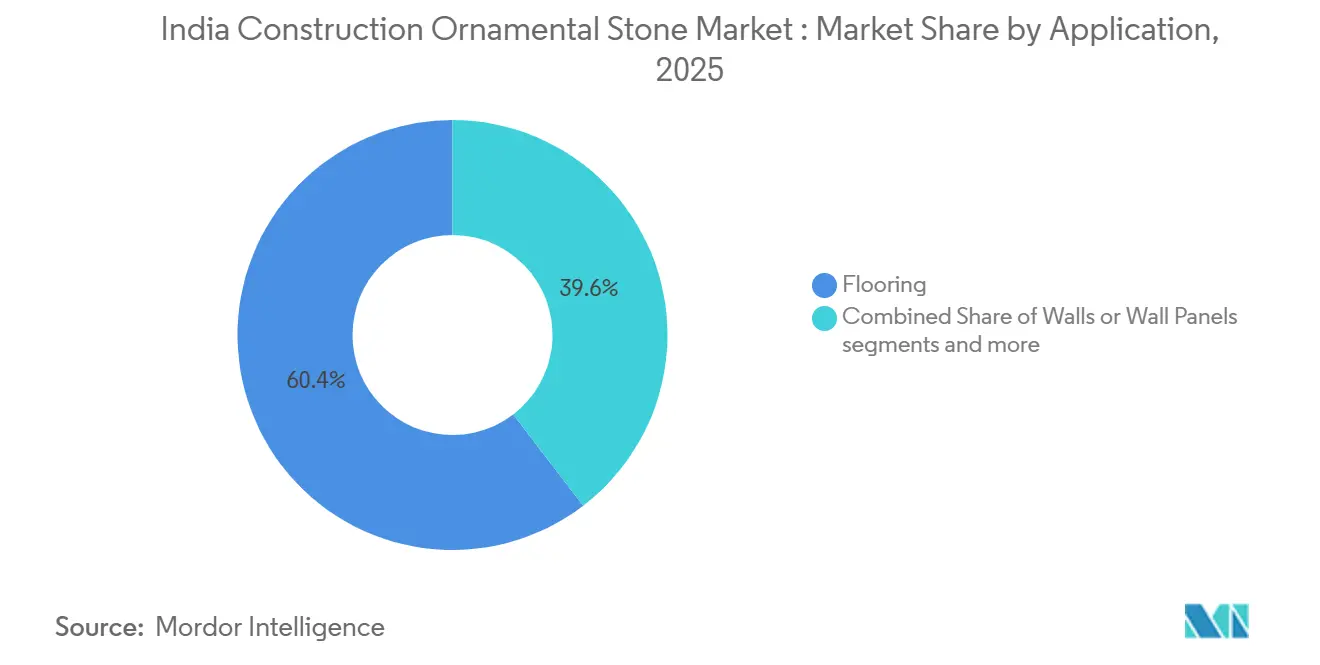

- By application, flooring accounted for 60.4% share of the India ornamental stone market size in 2025, while wall panels continued to gain traction in commercial façade work.

- By end user, residential accounted for 64.1% of India's ornamental stone market share in 2025, while commercial demand remained supported by office upgrades and hospitality renovation projects.

- By distribution channel, dealers and fabricators remained the main route to market, while this channel is forecast to grow at 6.8% CAGR through 2031 in the India ornamental stone market.

- By geography, North India is forecast to expand at 7.1% CAGR through 2031, while South and West India remain the core production base for the India construction ornamental stone market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with India representing one among them. The global report on construction ornamental stone market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

India Construction Ornamental Stone Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium Housing Demand in Tier-I and Tier-II Cities | +1.8% | National, with stronger gains in Mumbai, Delhi-NCR, Bengaluru, Panchkula, Mohali, and Raipur | Short term (≤ 2 years) |

| Smart Cities and Urban Landscaping Spend | +0.9% | Across Smart Cities Mission locations and AMRUT 2.0 cities | Medium term (2-4 years) |

| Commercial Real Estate Renovation Cycle | +0.8% | Top 7 cities, especially Bengaluru, Delhi NCR, Mumbai, and Hyderabad | Medium term (2-4 years) |

| Dry-Cladding Façade Adoption in Premium Projects | +0.7% | National, with early adoption in Maharashtra, Karnataka, and Tamil Nadu | Medium term (2-4 years) |

| Engineered Quartz Capacity Expansion and Import Mix | +0.5% | Telangana, Gujarat, and Tamil Nadu processing clusters | Long term (≥ 4 years) |

| CNC, Wire Saw, and Digital Fabrication Adoption | +0.6% | Tamil Nadu, Andhra Pradesh, Telangana, and Rajasthan processing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium Housing Demand in Tier-I and Tier-II Cities

In India, the luxury real estate market is experiencing a surge in demand for high-end apartments and premium bungalows. This trend is accompanied by an increased use of premium products in residential construction. Natural stones, once used sparingly, are now widely incorporated into construction projects. The cost of construction and investment in luxury projects has doubled, aligning with increased consumer spending capacity. Italian marble and large-sized premium tiles, including imported brands, are in higher demand. Brazilian products are popular due to their recognized premium quality, though high prices remain a challenge. Premium residential construction is changing stone demand in the India ornamental stone market at the project level, not only at the national level. Homes priced above INR 1 crore made up 50% of total housing sales in 2025, compared with 44% in 2024, which shows how quickly sales have shifted toward higher-value formats[1]Knight Frank, “India Real Estate Residential Report 2025,” knightfrank.co.in.

Smart Cities and Urban Landscaping Spend

Public works remain a second strong support for the India ornamental stone market because they create demand outside private housing cycles. As of mid-2025, the Smart Cities Mission had completed 94% of its 8,067 projects, with total investment reaching INR 1.64 lakh crore across 100 cities[2]Source: Press Information Bureau, “Smart Cities Mission – Project Completion Status,” Press Information Bureau, pib.gov.in. Budget 2026 also raised capital expenditure to INR 12.2 lakh crore and introduced City Economic Regions, which keeps the pipeline active for paving, plaza work, heritage-zone flooring, and other public-space uses where stone remains a preferred material AMRUT 2.0 widens this demand to more cities and expands the geographic reach of the India ornamental stone market beyond the main metro clusters. Government procurement also tends to favor domestic sandstone, kota stone, and granite, which protects demand for local quarrying and processing clusters that do not rely on luxury housing alone..

Commercial Real Estate Renovation Cycle

Office and institutional upgrades are giving the India ornamental stone market a useful demand stream that is less dependent on new launches. JLL estimated that retrofitting India’s existing Grade A office stock represented an INR 45,000 crore opportunity, or USD 5.3 billion, and that 62% of 530.8 million sq ft required upgrades to meet sustainability and occupier standards. These projects tend to favor premium finishes because upgraded assets can command rental premiums in strong submarkets, which keeps granite lobby cladding and marble flooring relevant in redevelopment budgets. Bengaluru, Delhi NCR, Mumbai, and Hyderabad account for 81% of this renovation spending pool, which places demand in the same regions where higher-specification stone already earns better realizations. For the India ornamental stone market, this means supply can still find demand even when mainstream residential construction slows.

CNC, Wire Saw, and Digital Fabrication Adoption

Processing upgrades are changing how value is captured in the India ornamental stone market. Multi-wire cutting systems now allow parallel slab production from granite blocks and improve throughput compared with older sawing methods, which supports better yield and shorter processing time. 5-axis CNC bridge saws also allow tighter dimensional control for countertops, cladding profiles, and custom architectural pieces, which helps organized processors compete on finish quality rather than only on raw material cost[3]Source: JB Engineers India, “Wire Saw Machine for Marble and Granite Cutting Industries,” JB Engineers India, jbengineers52.wordpress.com. This matters because the India ornamental stone market is moving toward polished and cut-to-size output, where fabrication quality directly affects pricing power. Smaller fabricators that cannot fund these upgrades are losing ground to processors that can offer higher precision, shorter lead times, and broader installation support.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GST and Compliance Cost Burden | -0.8% | National, with stronger effects on small and mid-size quarry and fabrication operators | Short term (≤ 2 years) |

| Quarry Supply Diversion Toward Export Grades | -0.7% | Telangana, Karnataka, and Rajasthan quarrying belts | Medium term (2-4 years) |

| Ceramic and Sintered Surface Substitution | -0.9% | National, strongest in mid-market housing and commercial interiors | Medium term (2-4 years) |

| Mining Permission and Environmental Clearance Delays | -0.8% | Tamil Nadu, Jharkhand, Odisha, and Karnataka | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ceramic and Sintered Surface Substitution

Large-format porcelain and sintered surfaces are becoming the clearest substitute threat to parts of the India ornamental stone market. Sintered products offer low porosity, full UV resistance, and high hardness, while larger slab sizes reduce visible joints and make the final surface look closer to natural stone. This challenge is strongest in kitchen countertops and bathroom wall panels, where mid-market home buyers compare installed cost, upkeep, and visual finish more directly than in flooring or civic applications. The pressure is most visible in the INR 50 lakh to INR 1 crore housing bracket, where design aspirations remain high but price sensitivity is tighter. As Morbi-based ceramic producers expand sintered capabilities, the substitute risk is moving lower across price bands and affecting application areas that once carried better margins for natural stone.

Mining Permission and Environmental Clearance Delays

Permit delays and quarry compliance actions also limit supply growth in the India ornamental stone market. In May 2026, Tamil Nadu suspended operations at 67 stone quarries after inspections across 431 quarries found violations at 155 locations, tightening supply from an important commercial granite source base. The Supreme Court’s November 2025 decision to restore post-facto environmental clearance provided some short-term relief to projects that had already started. Still, it did not remove the clearance backlog faced at the state level. This means processors can invest in cutting, polishing, and fabrication capacity without fully solving raw block availability. Quarry operators in Tamil Nadu, Rajasthan, and Karnataka, therefore, face a business climate in which compliance and permitting can delay the transition from lease to actual supply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Stone Type: Granite Leads Scale While Quartzite Builds Premium Position

Granite held 40.9% of the Indian ornamental stone market share in 2025, maintaining its leading revenue position among stone types. Its strength comes from dependable domestic block supply in Telangana, Karnataka, and Andhra Pradesh, as well as broad use in institutional flooring, luxury residences, and commercial interiors. In the India ornamental stone industry, granite remains the most practical material for projects that need both visual consistency and easier procurement across large floor areas. This combination of supply depth and familiarity with specifications gives granite a broader base than other stones.

Marble remained the second-largest category and stayed concentrated in high-end residential lobbies, hospitality interiors, and temple construction. Rajasthan’s Makrana and Kishangarh belts continued to anchor premium marble supply for projects in Delhi NCR and Mumbai, where white and decorative grades remain closely tied to luxury specifications. Quartzite and slate occupied a smaller share, but they benefited from designer preference for textured and honed surfaces in premium façade and hospitality work. Limestone, sandstone, and Kota stone served public-space, temple, and restoration uses, giving the Indian ornamental stone market a set of demand pockets that face weaker substitute pressure than kitchen and bathroom applications.

By Manufacturing Type: Polished Slabs Shift Value Toward Processing

Raw and unpolished stone accounted for 80.6% share of the India ornamental stone market size in 2025, which shows how large the basic supply layer still is. Even so, polished slabs are forecast to expand at 7.8% CAGR through 2031, which makes them the fastest-growing manufacturing format in the India ornamental stone market. The direction of value is therefore moving toward higher-finish processing even though raw material trade still holds the biggest revenue base. This shift is being driven by premium housing, commercial upgrades, and export demand for better-finished surfaces.

India has long supplied raw blocks to processors in China, the Middle East, and Europe, so the large share of unpolished material reflects that established trade pattern. However, that structure is changing as domestic processors in Tamil Nadu and Gujarat compete more actively in polished slab categories such as leathered granite, honed marble, and brushed quartzite. These finishes allow Indian suppliers to defend margins through workmanship and finish quality rather than only through raw stone availability. In the India ornamental stone industry, this is widening the gap between operators that process for value and those that still depend mainly on block trading.

By Application: Flooring Keeps the Base While Wall Uses Gain Ground

Flooring accounted for 60.4% of the ornamental stone market in India in 2025, making it the largest application by a wide margin. This lead reflects stone’s continued use in residential common areas, hotel lobbies, airport terminals, commercial atriums, and large institutional corridors. In these spaces, stone still carries weight because durability, acoustic comfort, and thermal performance matter as much as appearance. Flooring, therefore, remains the volume anchor for the ornamental stone market in India. Its strength is also reinforced by renovation demand in hospitals, government buildings, metro stations, and office properties that need resurfacing rather than new structural work. When these projects are upgraded, flooring is often one of the first visible finishes to be replaced or improved. That helps keep demand active even in periods when private new-build activity slows. It also explains why flooring has held its lead despite wider discussion around engineered surface substitution.

Walls and wall panels accounted for the second-largest application tier and continued to benefit from the adoption of dry cladding in commercial façades. This area is still smaller than flooring, but it is becoming more important as premium projects seek cleaner elevations and more controlled installation outcomes. In the India ornamental stone market, this supports demand for fabrication quality, panel calibration, and profile accuracy rather than just raw material supply. It also gives organized processors more room to differentiate.

By End-User: Residential Demand Stays Largest but Moves Further Upmarket

Residential end-users accounted for 64.1% of revenue in 2025, which made them the largest source of demand in the Indian ornamental stone market. The more important shift was inside this category, because premium and luxury housing gained share while lower-value housing weakened. Commercial end-users accounted for 35.9% of revenue in 2025 and remained important in hotel lobbies, flagship retail, office atriums, and institutional buildings. JLL’s estimated INR 45,000 crore office upgrade opportunity translates directly into fresh demand for granite flooring and marble cladding across a large installed base of aging Grade A stock.

Commercial demand also tends to favor higher-surface-value work because it is tied to brand image, visitor experience, and asset positioning. That creates room for book-matched marble, premium granite, and quartzite in settings where owners want visible upgrades. Indian processors are increasingly relevant in these jobs because better fabrication quality lets them compete with imported finished stone on more than price. This keeps the India ornamental stone market connected to premium build quality across both residential and commercial end-users.

By Distribution Channel: Dealers and Fabricators Gain Influence Through Service Depth

Dealers and fabricators are forecast to grow at 6.8% CAGR through 2031, making them the fastest-growing distribution route in the India ornamental stone market. Their role is shifting from simple product resale to full-service execution, including site measurement, custom cutting, sealing, delivery, and installation support. That change matters because developers and architects increasingly want a single accountable partner rather than multiple suppliers. It gives the dealer-fabricator layer more control over both customer relationships and realized pricing.

Direct manufacturer-to-customer sales remain present among larger organized suppliers such as Pokarna Limited and R K Marble, which have the brand reach and logistics structure to serve institutional and export orders directly. Even so, the market still depends heavily on fabricator networks because many projects need local design adaptation and installation management. This keeps channel power close to the point of specification and execution. It also means channel consolidation can reshape the structure of the India ornamental stone market faster than quarry ownership changes alone.

Geography Analysis

North India is the largest and fastest-growing regional market in the Indian ornamental stone market, projected to expand at a 7.1% CAGR through 2031. Delhi NCR luxury housing, infrastructure work in Uttar Pradesh, and premium residential growth in Haryana and Punjab are the main demand supports. JLL reported that premium apartments above INR 10 million increased their share of launches from 64% in 2024 to 70% in 2025 in key North Indian metros, thereby widening the premium stone specification pool.

South and West India are the main production bases of the Indian ornamental stone market. South India supplies much of the commercially traded granite used in domestic fabrication and export, with Tamil Nadu, Karnataka, and Andhra Pradesh remaining key quarrying clusters. These states support widely used grades such as Absolute Black, Rosy Pink, and TAN Brown, which are used across both residential and institutional projects.

East and North-East India remain the smallest regional segment by revenue, but metro rail and public infrastructure projects are creating incremental institutional demand. This part of the India ornamental stone market is less driven by premium housing and more by transport, civic, and public building applications. Prefabricated stone panels for metro interiors and transit infrastructure could become more relevant here, as dimensional accuracy matters and project volumes can be standardized. Supply conditions remain less predictable in eastern states because quarry clearance and environmental oversight remain more complex than in the more established western and southern stone belts.

Competitive Landscape

The India ornamental stone market remains fragmented, with no single company holding a dominant national position. The leading organized group includes Pokarna Limited, R K Marble, Classic Marble Company, Aro Granite Industries, and Madhav Marbles and Granites. However, each player is still rooted in specific quarry or processing geographies rather than a fully national control model. This keeps competition distributed across product categories, stone grades, and regional project networks.

In the India ornamental stone market, operators that combine captive quarries with in-house processing hold a clear operating edge because they can manage raw block availability, processing quality, and delivery schedules more tightly. That advantage becomes more valuable when quarry compliance actions or freight issues disrupt open-market sourcing.

A meaningful white space remains in architectural fabrication, especially in complex cladding systems, bespoke countertop profiles, and pre-cut temple stone components. Smaller CNC-equipped fabricators in Tier-2 cities are starting to address this space, which gives them a path into architect-led work that was once served mainly by metro importers or foreign suppliers. Asian Granito’s corporate restructuring and expansion into warehouse and showroom operations in Dubai and the United Kingdom illustrate how mid-tier Indian players are pairing organizational changes with market expansion to pursue higher-margin specification business. This raises the competitive standard in the Indian ornamental stone market without changing its overall fragmented structure.

India Construction Ornamental Stone Industry Leaders

Pokarna Limited

Aro Granite Industries Ltd

R K Marble

Classic Marble Company (KalingaStone)

Stonex India Pvt Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Asian Granito India Limited received NCLT approval for a corporate restructuring scheme involving demerger, slump sale, and amalgamation. The company also established warehouse and showroom operations in Dubai and the United Kingdom as part of its international market expansion.

- October 2024: Pokarna Limited commissioned a 1.2 million m² quartz plant in Telangana to supply UV-resistant slabs for premium kitchens.

India Construction Ornamental Stone Market Report Scope

| Granite |

| Marble |

| Quartzites |

| Slates |

| Other Natural Stones, Limestone, Sandstone, Etc. |

| Raw/Unpolished |

| Polished Slabs |

| Cut-to-Size |

| Flooring |

| Walls or Wall Panels |

| Countertops, Both Kitchen and Bathroom |

| Other Applications, Temples, Monuments, Furniture |

| Residential |

| Commercial |

| Directly from the Manufacturers |

| Dealers and Fabricators |

| North India |

| South India |

| West India |

| East & North-East India |

| By Stone Type | Granite |

| Marble | |

| Quartzites | |

| Slates | |

| Other Natural Stones, Limestone, Sandstone, Etc. | |

| By Manufacturing Type | Raw/Unpolished |

| Polished Slabs | |

| Cut-to-Size | |

| By Application | Flooring |

| Walls or Wall Panels | |

| Countertops, Both Kitchen and Bathroom | |

| Other Applications, Temples, Monuments, Furniture | |

| By End-User | Residential |

| Commercial | |

| By Distribution Channel | Directly from the Manufacturers |

| Dealers and Fabricators | |

| By Region | North India |

| South India | |

| West India | |

| East & North-East India |

Key Questions Answered in the Report

What is the 2031 outlook for ornamental stone demand in India construction projects?

The India ornamental stone market is projected to reach USD 7,622.4 million by 2031 from USD 5,543 million in 2026, at a 6.6% CAGR. Premium housing and public works remain the main demand supports.

Which product category leads current revenue in India ornamental stone use?

Granite led stone type revenue with a 40.9% share in 2025 because it combines reliable domestic supply with broad use across flooring, interiors, and institutional projects.

Why is flooring still the largest use case for ornamental stone in India?

Flooring held 60.4% of revenue in 2025 because it remains standard in residential common areas, hospitality lobbies, airport terminals, and large institutional spaces.

Which end-user group matters most for revenue growth?

Residential remained the largest end-user with 64.1% revenue share in 2025, but growth is increasingly coming from premium and luxury housing rather than mass housing.

Which region is expanding fastest in India?

North India is the fastest-growing region, with a projected 7.1% CAGR through 2031, supported by Delhi NCR luxury housing, Uttar Pradesh infrastructure work, and demand across Haryana and Punjab.

Page last updated on: