India Cold Storage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

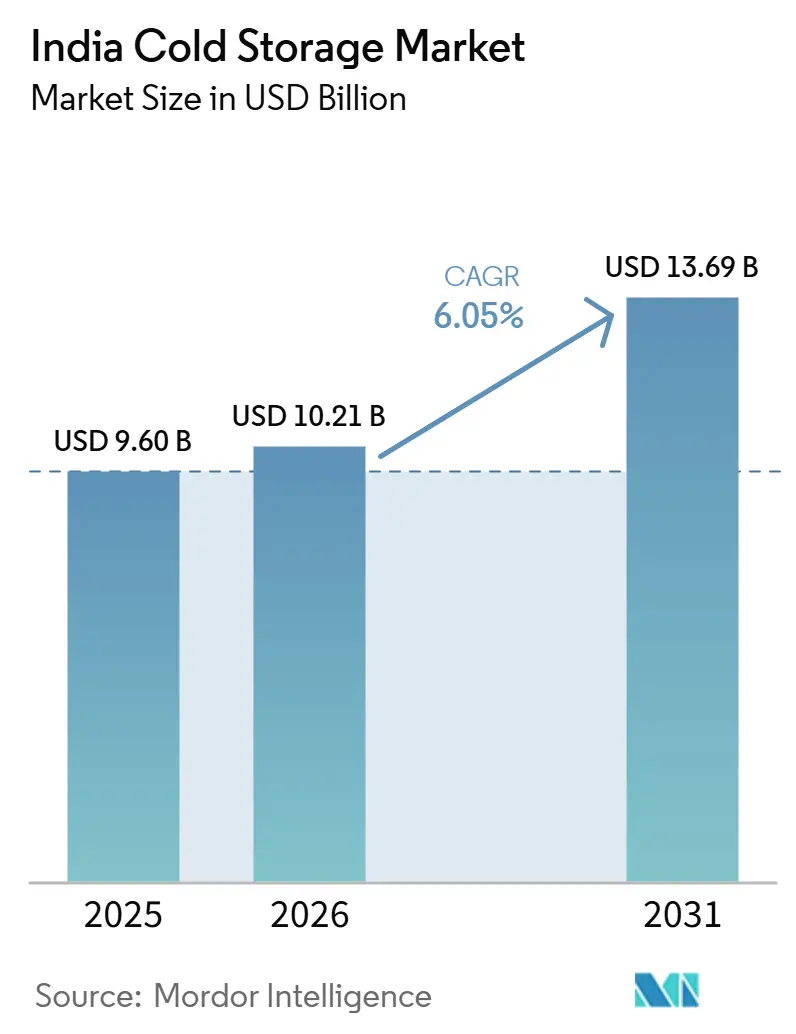

| Base Year Market Size (2025) | USD 9.60 Billion |

| Market Size (2026) | USD 10.21 Billion |

| Market Size (2031) | USD 13.69 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

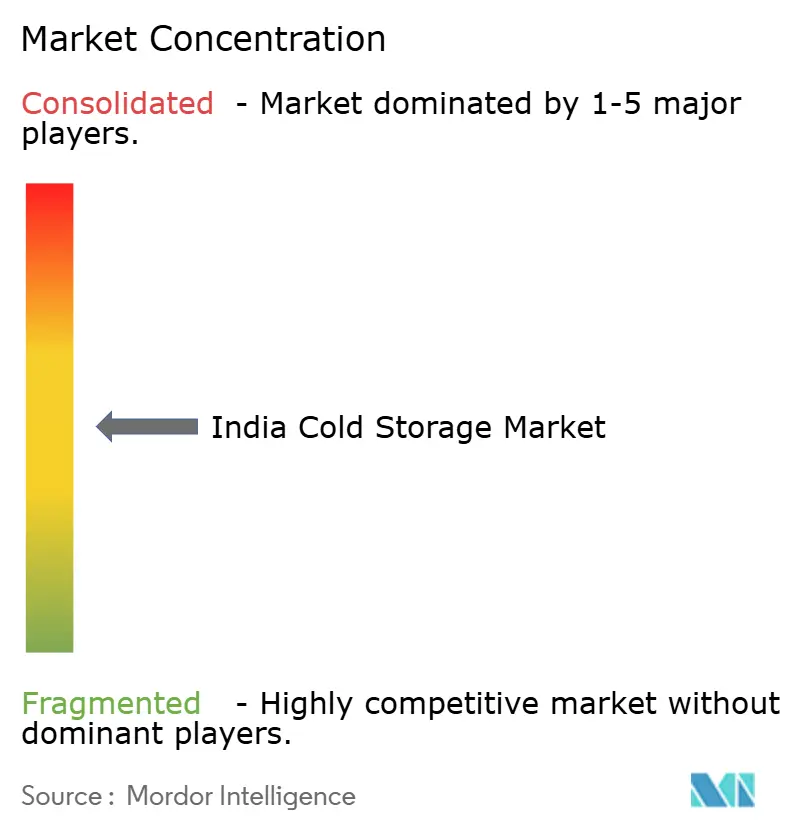

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Cold Storage Market Analysis by Mordor Intelligence

The India cold storage market size is expected to increase from USD 9.60 billion in 2025 to USD 10.21 billion in 2026 and reach USD 13.69 billion by 2031, growing at a CAGR of 6.05% over 2026-2031.

The India cold storage market is being shaped by 3 demand streams that now move in parallel, food retail modernization, pharmaceutical cold chain expansion, and the spread of quick commerce dark stores. That mix is changing the type of infrastructure operators need to build, because large single-commodity warehouses no longer match the storage pattern required by urban food retail and regulated healthcare logistics. The India cold storage market is also seeing investment shift toward facilities that can manage multiple temperature bands, achieve faster inventory turns, and strengthen compliance controls. The opportunity is becoming more visible in tier-2 and tier-3 cities, where supply remains limited even as consumption and organized distribution continue to widen. Competitive activity in the India cold storage market remains moderate, with listed logistics firms, global supply chain operators, and automation-led specialists all expanding through built-to-suit capacity, compliance upgrades, and targeted regional projects.

Key Report Takeaways

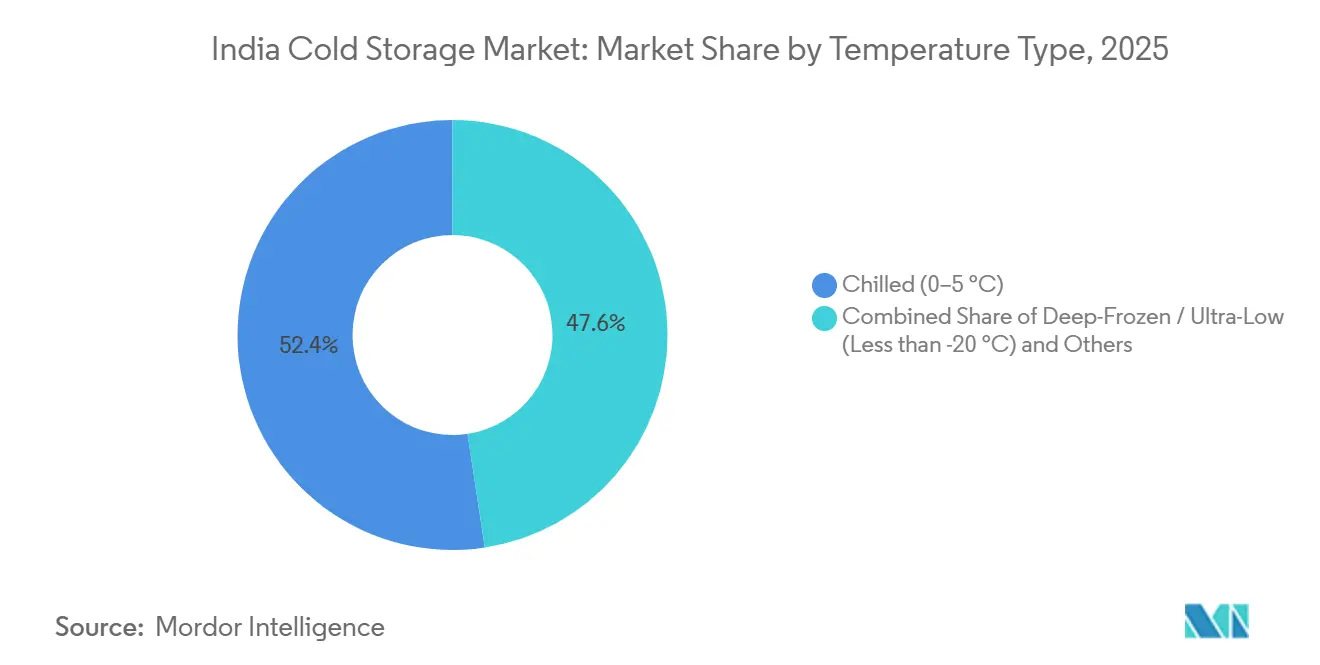

- By temperature type, chilled (0-5 °C) held 52.40% of India cold storage market size in 2025, while deep-frozen / ultra-low (less than -20 °C) is projected to grow at 11.31% CAGR through 2031.

- By automation level, conventional facilities held 84.31% of the India cold storage market share in 2025, while automated cold stores are forecast to expand at 14.04% CAGR through 2031.

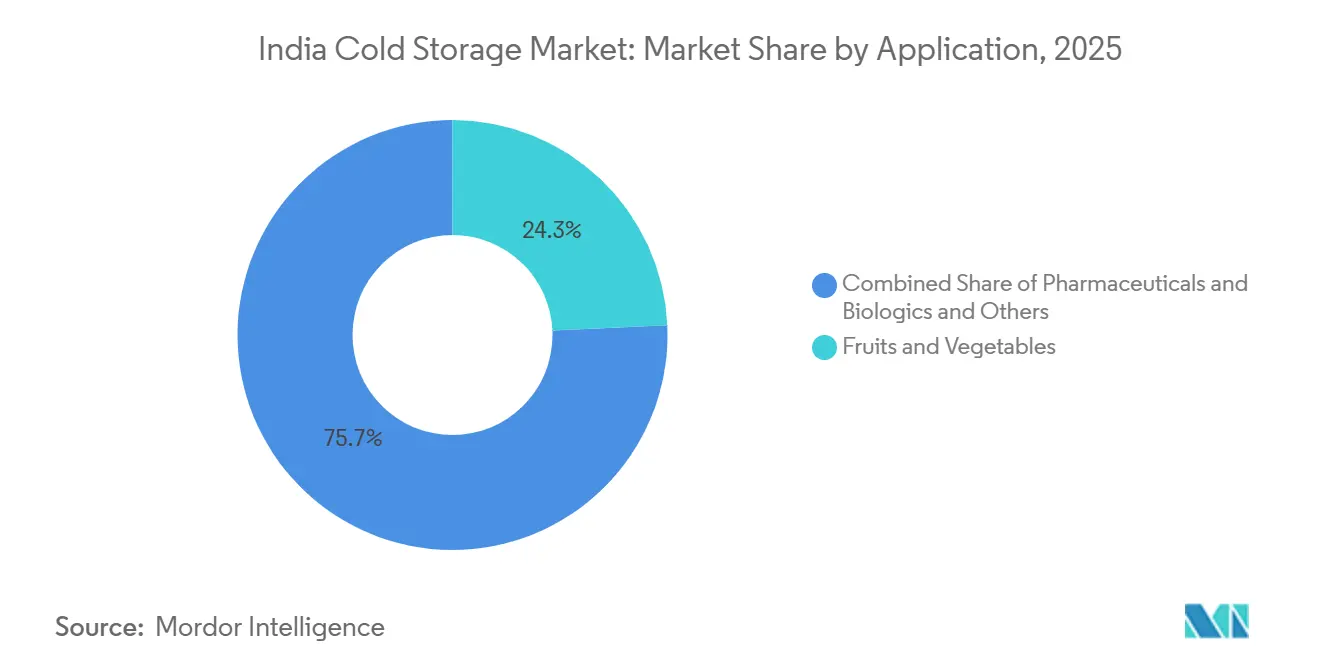

- By application, fruits & vegetables accounted for 24.28% of India cold storage market size in 2025, while pharmaceuticals & biologics are advancing at 14.37% CAGR through 2031.

- By region, North India held 31% of India cold storage market share in 2025, while the South region is projected to grow at 10.37% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Cold Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Multi-Temperature Warehousing | +1.2% | Pan-India, particularly North, West, and South | Medium term (2-4 years) |

| Expansion of Organized Food Retail and Quick Commerce | +1.5% | Urban metros and Tier-1 cities, spill-over to Tier-2 | Short term (≤ 2 years) |

| Rising Pharma, Vaccine, and Biologics Cold Chain Needs | +1.1% | South, West, spill-over to North | Medium term (2-4 years) |

| Energy Resilience Through On-Site Renewable Backup | +0.5% | Gujarat, Rajasthan, Andhra Pradesh, Maharashtra | Long term (≥ 4 years) |

| Digital Temperature Traceability for Export Compliance | +0.4% | Export hubs including Mumbai, Chennai, JNPT corridor, Hyderabad | Medium term (2-4 years) |

| Cluster-Level Capacity Buildout Near Processing Hubs | +0.7% | West, South, East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Multi-Temperature Warehousing

Demand in the India cold storage market is no longer centered on a single temperature band. Retail chains, quick-service restaurants, and pharmaceutical companies increasingly need chilled, frozen, and ambient zones on the same site. That change is pushing operators to rethink warehouse design, as facilities built for a single commodity or temperature cannot easily accommodate mixed inventory. Quick commerce platforms recorded a 30% rise in summer demand for frozen and chilled products in 2025, further increasing pressure on dark-store operators to manage multiple cold zones within tight delivery windows. In the India cold storage market, this design mismatch is extending the investment cycle beyond new builds alone, because retrofitting older sites is often as important as building fresh capacity. The result is a longer modernization runway, especially in cities where consumption is broadening faster than infrastructure quality.

Expansion of Organized Food Retail and Quick Commerce

Organized food retail and quick commerce are changing the operating logic of the India cold storage market. India’s quick commerce gross merchandise value reached USD 11.3 billion in 2025, and Zepto alone earmarked INR 1,629 crores (USD 190 million) for dark-store expansion across FY 27-FY 30. Blinkit has also stated plans to expand its dark-store network to 3,000 stores by March 2027, adding to the density of cold-sensitive urban inventory. Perishables now account for a large share of orders on these platforms, so demand is shifting from long-dwell repository storage to fast-turn micro-fulfillment capacity near residential clusters. This is why the India cold storage market is seeing stronger demand for urban multi-zone sites rather than only large rural or peri-urban bulk facilities. The supply gap remains wide in most major metros, making near-city cold infrastructure one of the clearest expansion pockets.

Rising Pharma, Vaccine, and Biologics Cold Chain Needs

The India cold storage market is also being pulled upward by a sharper rise in pharmaceutical and biologics handling requirements. Drug makers and exporters need more 2° C to 8 °C storage, as well as more ultra-low-temperature capacity, to support newer therapies that move beyond the traditional generics model. This changes the revenue mix because pharmaceutical throughput requires stronger compliance and delivers higher value per pallet than agricultural storage. The shift is especially important in 2026, as more exporters prepare for larger flows of biologics and biosimilars across regulated trade lanes. That need is already visible in infrastructure decisions, as CONCOR and Maersk launched the Aushadhi Express reefer rail service from Hyderabad to Jawaharlal Nehru Port on May 2, 2026, creating a dedicated temperature-controlled pharma export corridor[1]Source: Maersk Newsroom, “Pharmaceutical Exporters to Benefit from Maersk's First Dedicated Reefer Rail Service from Hyderabad to Mumbai,” Maersk, maersk.com. In the Indian cold storage market, this means future growth will come not only from increased capacity but also from specialized capacity that meets regulated healthcare service standards.

Energy Resilience Through On-Site Renewable Backup

Power quality remains a basic operating issue in the India cold storage market, which is why energy resilience is moving closer to the center of facility design. Cold stores cannot afford temperature excursions, and operators in weaker grid corridors face both direct spoilage risk and higher diesel dependence. That makes on-site power support more than a cost issue, because reliability is now tied to contract quality and customer confidence. TCI Cold Chain Solutions commissioned its Gurugram facility in December 2025, featuring a 500 kW rooftop solar system and SCADA-based refrigeration monitoring, demonstrating how leading operators are combining energy backup with advanced control systems[2]Source: Economic Times, “TCI Expands Cold Chain Warehousing Capacity with 1.5 Lakh Sq Ft Facility in Gurugram,” The Economic Times, economictimes.indiatimes.com. In the Indian cold storage market, sites with stronger power resilience are better placed to win food and pharma accounts that cannot tolerate temperature instability. This is likely to widen the operating gap between organized networks and smaller independent facilities over time.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Intensity for Modern Cold Chain Facilities | -1.0% | Pan-India, most acute in tier-2 and tier-3 cities | Long term (≥ 4 years) |

| Power Reliability and Operating Cost Pressure | -0.8% | North, Central, East India, rural corridors | Medium term (2-4 years) |

| Shortage of Skilled Refrigeration and Automation Technicians | -0.5% | Pan-India, most acute where AS/RS is being deployed | Long term (≥ 4 years) |

| Fragmented Demand Reduces Asset Utilization | -0.6% | Tier-2 and tier-3 markets, agricultural hinterland | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Intensity for Modern Cold Chain Facilities

High project cost remains one of the clearest limits on the pace of the India cold storage market. Construction costs for frozen cold storage range from INR 3,200 to INR 4,000 (USD 33.80 to USD 43.60 ) per ft², while pharmaceutical-grade cold rooms cost INR 25,000-40,000 (USD 267 to USD 462) per metric ton of capacity. Multi-temperature layouts, automation systems, warehouse management software, and backup power all further increase the required investment. This stretches payback periods, especially for operators that cannot offset capex with long-term anchor clients or subsidy support. In the Indian cold storage market, this is creating a split: larger, organized players are expanding faster, while smaller operators struggle to finance upgrades that customers increasingly expect. The pressure is not only financial, because rising compliance expectations in food and healthcare also reduce the room for low-spec capacity to remain competitive.

Power Reliability and Operating Cost Pressure

Power reliability remains a practical operating restraint across many parts of the Indian cold storage market. Facilities in agricultural belts and smaller cities often experience repeated interruptions, creating both spoilage risk and a heavier reliance on diesel backup. The burden becomes even more serious in frozen and deep-frozen applications, where short temperature breaks can quickly damage inventory. This means cost pressure is uneven across the market, because better urban locations with stronger grids and integrated power systems operate under a different risk profile than rural belts. In the India cold storage market, weaker power reliability can reduce utilization incentives, delay new investment, and keep modern service formats from spreading as fast as demand would otherwise support. The result is that infrastructure growth does not move at the same speed across regions, even when end demand is present.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Temperature Type: Deep-Frozen Segment Disrupting Legacy Temperature Mix

Chilled (0-5 °C) accounted for 52.40% of the India cold storage market share in 2025, reflecting the continued dominance of fruits, vegetables, and dairy in total throughput. Frozen and ambient formats still play important roles across processed foods, confectionery, and dry pharmaceuticals. The fastest shift, however, is in deep-freeze / ultra-low storage, which is projected to grow at a 11.31% CAGR through 2031. That growth rate shows how the India cold storage market is moving beyond its older focus on conventional produce storage and into more specialized temperature bands. The need for handling at -20 °C to -80 °C is rising as pharmaceutical use cases broaden from standard products to biologics, vaccines, and other temperature-sensitive therapies.

That shift is now visible in project execution. Indicold deployed India’s first fully automated high-bay frozen ASRS warehouse in Dholasan, Gujarat, in 2024, and followed it with a second Detroj facility in April 2025 with more than 10,000 pallet capacity at -25 °C[3]Source: Indicold Team, “After Pioneering India's First Frozen ASRS, Indicold Scales Up with a Second Fully Automated Facility,” Indicold, indicold.com. The India cold storage industry is therefore moving through a staggered capex cycle, where chilled capacity remains the installed base, frozen capacity is being scaled for organized food distribution, and ultra-low infrastructure is entering commercial relevance. Operators serving quick commerce also need better frozen continuity between the central warehouse, the micro-fulfillment point, and the final delivery. That is why temperature segmentation in the India cold storage market is no longer just a technical classification; it is becoming a direct indicator of where new capital is being deployed.

By Automation Level (Storage): Conventional Facilities Losing Share to Automation-Led Operators

Conventional facilities held 84.31% of India cold storage market size in 2025, while automated cold stores are forecast to grow at 14.04% CAGR through 2031. That contrast shows that the installed base of the India cold storage market still reflects legacy construction, even though the direction of fresh investment is clearly shifting toward automation. Labor efficiency, throughput speed, and tighter handling discipline are all strengthening the case for AS/RS and robotics in new projects. The value of automation is greater in facilities serving retail, quick-service restaurants, and pharma, where order intensity and compliance needs are both higher. In practice, the automation story is less about replacing labor everywhere and more about reducing error, improving pallet movement, and supporting better process control.

That move is already supported by market activity. Daifuku reported that warehousing leasing in India exceeded 9 million ft² in Q1 2025, while Grade A warehouse demand rose 33% year over year. Indicold’s Detroit project uses a Four-Way Shuttle system at -25 °C, supports stacker crane speeds of 180 pallets per hour, removes routine human entry, and integrates oxygen-reduction fire prevention with warehouse software. The India cold storage industry is therefore developing a wider capability gap between the top organized operators and the long tail of manual sites. Over time, the India cold storage market is likely to treat automation less as a premium differentiator and more as a baseline requirement for higher-value customer contracts.

By Application: Pharmaceuticals Overtaking Agri-Commodities in Value Intensity

Fruits & vegetables accounted for 24.28% of the India cold storage market size in 2025, keeping agriculture as the largest application by volume and the broadest usage. Meat and poultry, fish and seafood, dairy and frozen desserts, bakery, confectionery, and ready-to-eat meals all remain important demand pockets as consumption patterns diversify across urban and peri-urban India. The fastest application growth is coming from pharmaceuticals & biologics, which is projected to expand at 14.37% CAGR through 2031. This matters because application growth in the India cold storage market is no longer driven solely by tonnage, but also by the revenue density of each pallet and the compliance level associated with it. Pharmaceutical storage earns much higher rental rates than potato and onion storage, so even a smaller volume base can reshape the revenue mix.

That value-intensity shift is already influencing where organized operators place capital. The Hyderabad pharmaceutical cluster has become one of the clearest examples, as Kuehne+Nagel, DHL, and CONCOR have all commissioned or supported pharma-oriented cold infrastructure in the city and its export network during 2025 and 2026. At the same time, the Indian cold storage market still relies on food-linked applications for broad adoption, which means the next phase will not replace agri-storage but layer higher-value use cases onto the same regional network. FSSAI and pharmaceutical audit requirements are also raising the investment floor across applications, which favors operators that can manage documentation, traceability, and multi-zone operations. This is why the India cold storage market is seeing application demand change not only by category, but also by the quality threshold required to serve each category.

Geography Analysis

North India held a 31% share in 2025, making it the largest regional base in the India cold storage market. Uttar Pradesh, Punjab, and Haryana continue to anchor this position through their concentration of potato and grain-linked cold storage. That base provides the region with dependable use, but it also keeps a large share of capacity tied to lower-value single-commodity formats. Organized operators are expanding their product mix, as Snowman opened new temperature-controlled warehouses in Kolkata and Krishnapatnam in June 2025 to deepen access across the eastern and coastal corridors[4]Source: India Seatrade News, “Snowman Opens New Temp-Controlled Warehouses in Kolkata, Krishnapatnam,” India Seatrade News, indiaseatradenews.com.

The South region is projected to grow at a 10.37% CAGR through 2031, making it the fastest-growing geography in the India cold storage market. Its growth is centered less on bulk food storage and more on pharmaceutical export logistics. Hyderabad remains the clearest anchor because its manufacturing and export ecosystem needs stronger GDP-compliant, GxP-aligned handling across air, road, and rail. Kuehne+Nagel strengthened this corridor with its Bengaluru HealthChain-certified Cool Zone in December 2025 and its Hyderabad temperature-controlled facility in May 2026. CONCOR and Maersk also launched the Aushadhi Express service in May 2026, adding a dedicated reefer rail connection from Hyderabad to JNPT and Mumbai for pharmaceutical exports. Together, these moves show that regional growth in the India cold storage market is increasingly linked to export reliability and compliance capability, not only warehouse count.

The West region remains central to technology-led investment in the India cold storage market, with Maharashtra and Gujarat supporting both multi-temperature food infrastructure and automated frozen capacity. Pune has attracted fresh warehouse additions serving food processing and quick-turn urban demand, while Gujarat has emerged as the main base for automated frozen storage rollouts. Indicold’s twin ASRS projects in Dholasan and Detroj show how the western corridor is setting the pace for more advanced cold infrastructure. Central India remains underpenetrated relative to agricultural output, leaving the India cold storage market with a later-stage, inland opportunity once project economics improve, and organized networks move further away from coastal and metro-adjacent locations.

Competitive Landscape

The India cold storage market remains moderately fragmented, because a long tail of single-commodity facilities still controls a large share of installed capacity even as organized operators gain ground in higher-value categories. This creates a two-layer structure in which traditional agri-storage remains widespread, while modern multi-zone, compliance-led facilities are concentrated among a smaller group of companies. The leading organized names in the Indian cold storage market include Snowman Logistics, TCI Cold Chain Solutions, ColdEX Logistics, DHL Supply Chain India, and Indicold. Their advantage comes less from simple scale and more from the type of capacity they are adding, the clients they are targeting, and the service standards they can maintain. The competitive center of gravity is moving toward operators that can combine location, compliance, automation, and customer-specific facility design.

Several strategic moves illustrate that shift. Snowman expanded its network with new facilities in Kolkata and Krishnapatnam in June 2025, which raised its owned cold chain presence across more cities and trade corridors. TCI Cold Chain Solutions opened a 150,000 ft² multi-temperature warehouse in Gurugram in December 2025 under a flexible pay-as-you-use model, aimed at quick commerce, pharmaceutical, dairy, and life sciences demand in the National Capital Region. Kuehne+Nagel added healthcare-focused facilities in Bengaluru and Hyderabad, strengthening its regulated cold chain position in the South.

Technology-led challengers are also changing the tone of competition in the India cold storage market. Indicold has positioned itself around fully automated frozen ASRS infrastructure, integrated warehouse management, and low-human-entry operations that are suitable for both food and pharmaceutical handling. That model allows a newer operator to compete on both efficiency and service quality, rather than only on footprint. The whitespace remains strongest in tier-2 cities, inland multimodal corridors, and ultra-low pharmaceutical storage, where capacity is still short relative to likely demand. This is why the India cold storage market is competitive but not yet consolidated: the next winners will be defined by specialization and execution quality rather than broad national presence alone.

India Cold Storage Industry Leaders

Snowman Logistics Ltd.

ColdEX Logistics Pvt. Ltd.

Allcargo Gati

Allcargo Gati Mahindra Logistics Limited

TCI Cold Chain Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: CONCOR and Maersk launched India's first dedicated pharmaceutical reefer rail service, "Aushadhi Express," on May 2, 2026, connecting ICD Sanathnagar, Hyderabad, to Jawaharlal Nehru Port, Mumbai. The weekly service uses 40-foot refrigerated containers and is expected to reduce greenhouse gas emissions by 3,000 tons annually versus road transport, while improving transit predictability for pharma exporters.

- May 2026: Kuehne+Nagel opened a HealthChain-certified airfreight cross-dock pharma facility in Hyderabad under a GxP-compliant service model for pharmaceutical and medical device exporters. The 248 m² facility operates at +2 °C to +8 °C and +15 °C to +25 °C zones, following the Bengaluru HealthChain Cool Zone, commissioned in December 2025.

- May 2026: Snowman Logistics reported the commissioning of four facilities in Kolkata, Krishnapatnam, Kundli, and Jaipur during FY 26, adding approximately 17,000 pallet positions. The company now operates 45 warehouses across 21 cities with approximately 1.55 lakh pallets. An additional 13,000 pallet positions across Pune and Patna are under active development.

- December 2025: TCI Cold Chain Solutions (a JV between TCI, holding 80%, and Mitsui & Co. Japan, holding 20%) commenced operations at its new 1.5 lakh ft² multi-temperature warehouse in Gurugram under a flexible pay-as-you-use storage contract model. The facility targets quick commerce, pharmaceutical, dairy, and life sciences operators across the National Capital Region.

India Cold Storage Market Report Scope

| Chilled (0–5 °C) |

| Frozen (-18–0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (Less than -20 °C) |

| Conventional Facilities |

| Automated Cold Stores (AS/RS, Robotics) |

| Fruits & Vegetables |

| Meat & Poultry |

| Fish & Seafood |

| Dairy & Frozen Desserts |

| Bakery & Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals & Biologics |

| Vaccines & Clinical Trial Materials |

| Chemicals & Specialty Materials |

| Other Perishables |

| North |

| Central |

| West |

| East |

| South |

| By Temperature Type | Chilled (0–5 °C) |

| Frozen (-18–0 °C) | |

| Ambient | |

| Deep-Frozen / Ultra-Low (Less than -20 °C) | |

| By Automation Level (Storage) | Conventional Facilities |

| Automated Cold Stores (AS/RS, Robotics) | |

| By Application | Fruits & Vegetables |

| Meat & Poultry | |

| Fish & Seafood | |

| Dairy & Frozen Desserts | |

| Bakery & Confectionery | |

| Ready-to-Eat Meals | |

| Pharmaceuticals & Biologics | |

| Vaccines & Clinical Trial Materials | |

| Chemicals & Specialty Materials | |

| Other Perishables | |

| By Region | North |

| Central | |

| West | |

| East | |

| South |

Key Questions Answered in the Report

What is the current value outlook for cold storage in India through 2031?

The India cold storage market size is expected to rise from USD 10.21 billion in 2026 to USD 13.69 billion by 2031 at a 6.05% CAGR.

Which temperature category leads demand in India?

Chilled storage leads, with a 52.40% share in 2025, because fruits, vegetables, and dairy still drive a large share of total throughput.

Which part of the business is growing the fastest?

Automated cold stores are the fastest-growing format by automation level, with a 14.04% CAGR through 2031, while pharmaceuticals & biologics is the fastest-growing application, with a 14.37% CAGR.

Why is South India growing faster than other regions?

The South region is projected to grow at a 10.37% CAGR, driven by Hyderabad, Bengaluru, and Chennai strengthening as pharmaceutical and biotech cold chain corridors.

How is quick commerce affecting storage demand in Indian cities?

Quick commerce is pushing demand toward urban multi-temperature facilities and dark-store-linked micro-fulfillment capacity, rather than solely large bulk warehouses.

Which companies are shaping the competitive environment?

Snowman Logistics, TCI Cold Chain Solutions, DHL Supply Chain India, Kuehne+Nagel, and Indicold are among the most visible players through expansion, automation, and compliance-led projects.

Page last updated on: