India Bulk Transport Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

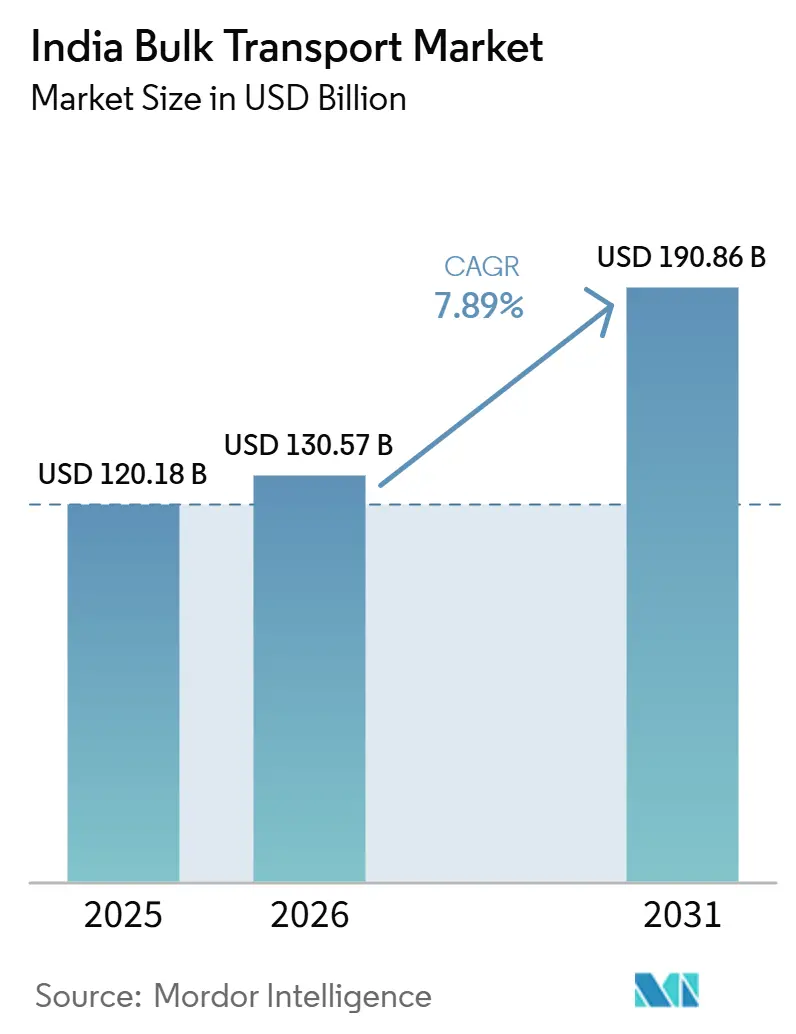

| Base Year Market Size (2025) | USD 120.18 Billion |

| Market Size (2026) | USD 130.57 Billion |

| Market Size (2031) | USD 190.86 Billion |

| Growth Rate (2026 - 2031) | 7.89% CAGR |

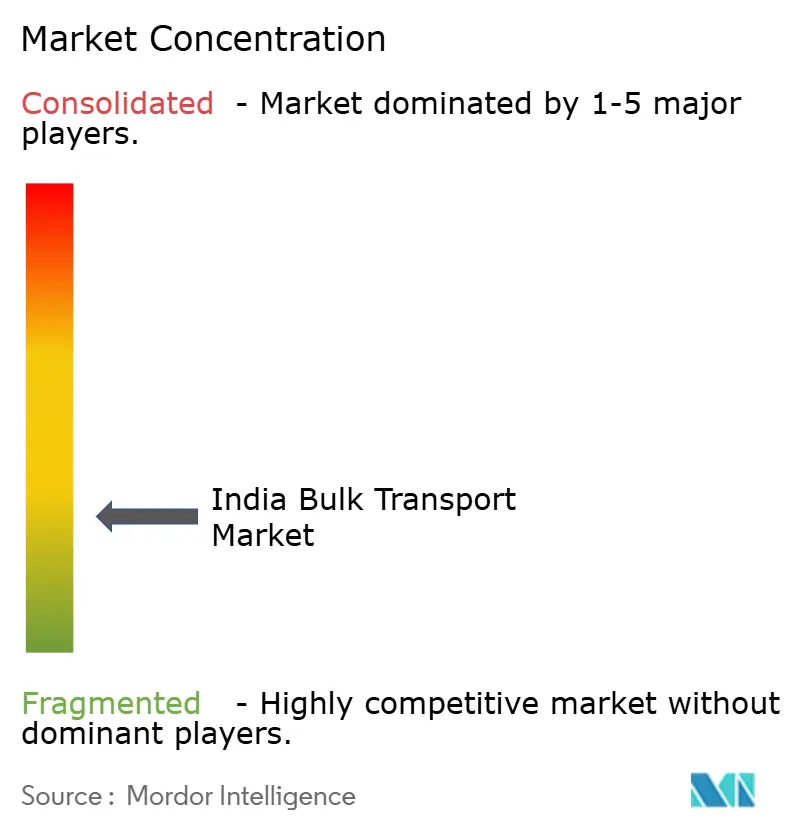

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Bulk Transport Market Analysis by Mordor Intelligence

The India bulk transport market size is expected to increase from USD 120.18 billion in 2025 to USD 130.57 billion in 2026 and reach USD 190.86 billion by 2031, growing at a CAGR of 7.89% over 2026-2031.

Public investment remains the backbone of this expansion, with FY27 capital expenditure raised to INR 12.2 lakh crore (USD 145.70 billion), keeping road, rail, port, and industrial projects active across the country. The completed Eastern and Western Dedicated Freight Corridors remove a long-standing bottleneck for rail-based bulk movement, especially on dense industrial lanes where speed and turnaround have historically limited scale. Private capital is reinforcing the same pattern, as investment rose 67% to INR 7.7 lakh crore (USD 91.96 billion) in the first half of FY26, led by metals, automobiles, and chemicals that generate steady raw material and finished input flows. Bulk freight demand is also supported by higher steel and cement output, tying transport growth to real production and infrastructure activity rather than to short-term inventory movements. The India bulk transport market therefore enters the forecast period with stronger physical infrastructure, deeper industrial demand, and a competitive structure that is still fragmented at the operator level but is consolidating around integrated logistics assets.

Key Report Takeaways

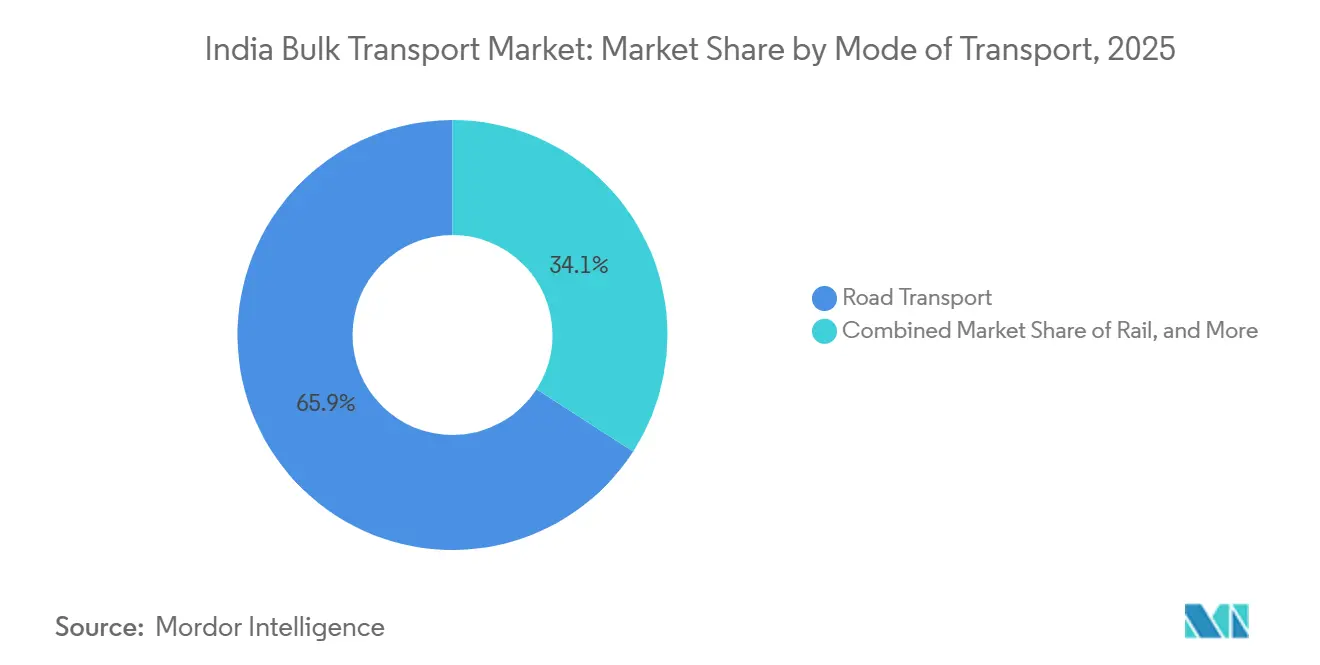

- By mode of transport, road freight held 65.88% of the India bulk transport market share in 2025, while waterways are projected to expand at a 9.57% CAGR through 2031.

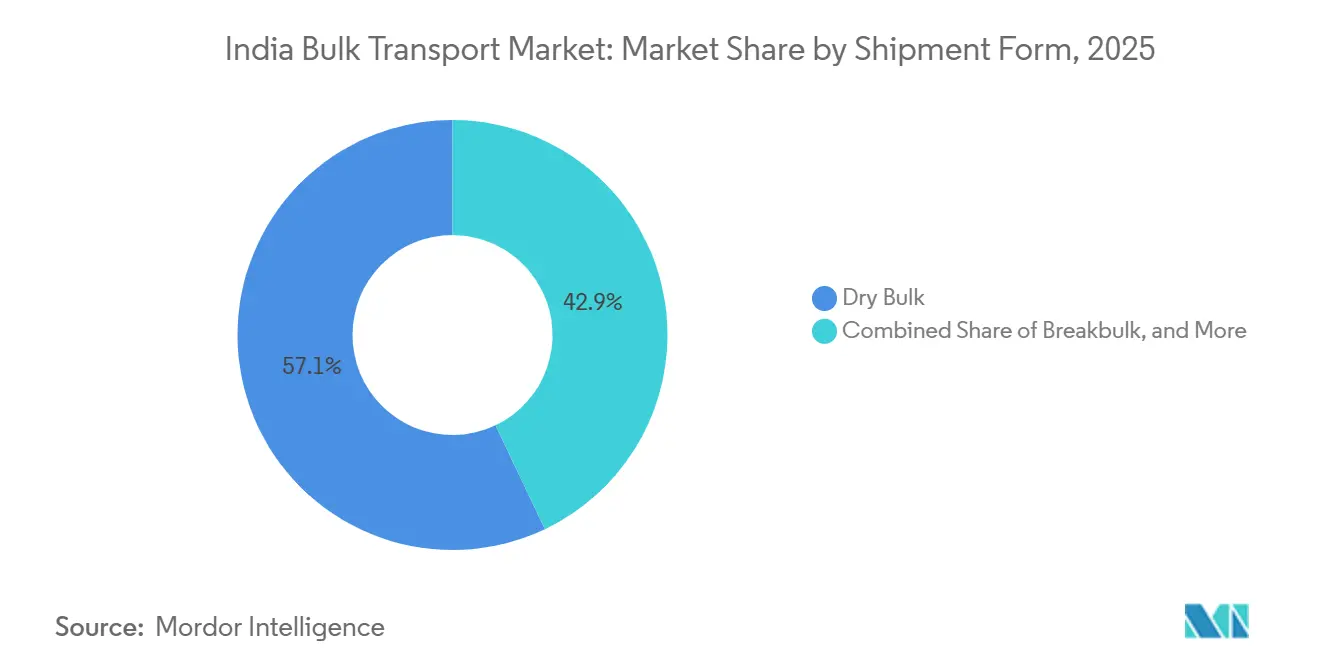

- By shipment form, dry bulk accounted for 57.07% of the India bulk transport market size in 2025, while liquid and gaseous bulk is forecast to grow at an 8.17% CAGR through 2031.

- By end user industry, energy commodities held 41.48% of the India bulk transport market in 2025, while construction aggregates and cement are projected to advance at an 8.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Bulk Transport Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industrial capex and infrastructure-material flows | +2.2% | National, concentrated in Delhi-Mumbai Industrial Corridor, Odisha steel belt, and Gujarat manufacturing clusters | Medium term (2-4 years) |

| Dedicated freight corridors and multimodal park rollout | +1.8% | National, immediate gains along EDFC and WDFC corridors | Short term (≤ 2 years) |

| National logistics policy, PM Gati Shakti, and ULIP integration | +1.5% | National, early gains in 28 Aspirational Districts using Gati Shakti District Master Plans | Medium term (2-4 years) |

| Inland waterways and coastal-shipping promotion | +0.8% | Eastern seaboard and western coastal states, with early-mover gains in Odisha, Maharashtra, and Goa | Long term (≥ 4 years) |

| Sectoral logistics blueprints for coal, cement, steel, and fertilizers | +1.2% | Coal in East India, cement across India, steel in Odisha, Jharkhand, and Maharashtra, fertilizers in Gujarat and Andhra Pradesh | Medium term (2-4 years) |

| Digital freight matching and organized freight procurement | +0.6% | National, Northern and western industrial belts matter most, especially around Delhi-NCR, Mumbai, Gujarat, and the broader west–north corridor | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Industrial Capex and Infrastructure-Material Flows

India's public and private investment cycle remains the deepest structural support for bulk freight demand in the India bulk transport market. The Union Budget 2026-27 raised public capital expenditure to INR 12.2 lakh crore (USD 145.70 billion), which preserved multi-year momentum in highways, railways, ports, and allied industrial infrastructure[1]“Union Budget 2026-27: Infra Stays King as Capex Scaled Up to ₹12.2 Lakh Crore,” Press Information Bureau, pib.gov.in. Steel and cement production, which are the 2 largest construction-linked commodity generators in this space, grew by 9.10% and 8.60% through FY26, keeping demand for iron ore, coking coal, aggregates, and clinker high. Private sector capital expenditure also rose 67% to INR 7.7 lakh crore (USD 91.96 billion) in the first half of FY26, led by metals, automobiles, and chemicals, which broadened the freight base beyond public works alone. As new facilities begin production, the weak point quickly shifts from demand creation to plant-gate connectivity, especially where rail sidings and high-quality feeder roads are missing. That shift gives third-party logistics operators and corridor specialists a larger role because many shippers now need integrated port, rail, and road execution rather than a single transport leg.

Dedicated Freight Corridors and Multimodal Park Rollout

The completed DFC network changes the economics of long-haul bulk movement in the India bulk transport market. The Eastern DFC was already operational, and the final Western DFC section completed its successful trial run on March 31, 2026, which closes a major infrastructure gap on one of India's most important freight systems. On commissioned sections, freight trains averaged 2.44 hours per 100 km against 5.25 hours on conventional mixed-use routes, which materially improves rail's value proposition for dense bulk flows on longer corridors. Planned Gati Shakti Multi-Modal Cargo Terminals along these corridors should make the benefits more durable, as faster trunk movement becomes more useful when aggregation and interchange points are available near production and consumption centers. The new Dankuni-Surat DFC also extends this logic into mineral-rich territory, which matters because the east-to-west industrial arc accounts for a large share of ore, coal, steel inputs, and heavy industrial loads. As more cargo is drawn into corridor-linked networks, the market should see a gradual shift from standalone road hauling toward planned multimodal chains[2]"DFCCIL Completes Construction Work on Dedicated Freight Corridor Project (Western Corridor)", Indian Infrastructure, indianinfrastructure.com.

National Logistics Policy, PM Gati Shakti, and ULIP Integration

Policy coordination has become a stronger operational force in the India bulk transport market than it was a few years ago. PM GatiShakti aligns physical planning across infrastructure projects, while the National Logistics Policy keeps attention on turnaround time, process simplification, and corridor efficiency. ULIP adds a digital layer to that system by connecting cargo, asset, and document visibility across transport modes, which reduces the information gaps that used to slow dispatch decisions and inflate coordination costs. This matters for bulk freight because heavy cargo depends on tighter sequencing between mines, plants, ports, terminals, and line-haul assets than parcel freight does. The result is not only lower friction for large organized shippers, but also better compliance visibility and more consistent service execution for institutional operators. As states and local logistics systems align with this structure, the India bulk transport market should become easier to manage across multi-state and multi-mode movements.

Inland Waterways and Coastal-Shipping Promotion

Water-based freight is moving from a marginal role to a more credible growth channel in the India bulk transport market. National waterways cargo reached 145.84 MMT in FY25 and 198.00 MMT through February 2026, which shows that policy support is now beginning to translate into actual cargo movement at scale. The Coastal Cargo Promotion Scheme and the push to operationalize 20 new National Waterways strengthen this shift, especially for mineral, fertilizer, cement, and petroleum flows on corridors close to ports and river systems. Odisha's NW-5 is strategically important because it connects the Talcher-Angul mineral belt with Paradip and Dhamra, giving coal and iron ore shippers another routing option beyond road and rail. Waterways also remain cost-competitive for heavy bulk once cargo is on the water, which gives them a clear role for dense loads where speed is less critical than unit economics. Over time, this should add pricing discipline to coastal corridors and reduce pressure on already busy road networks along the eastern and western seaboards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented truck fleet and driver shortage | -1.8% | National, most acute in northern and eastern states with high bulk commodity flows | Short term (≤ 2 years) |

| Rail siding and plant-gate first/last-mile gaps | -1.4% | National, concentrated at port hinterlands, mining clusters in Odisha and Jharkhand, and cement production belts | Medium term (2-4 years) |

| Hazardous-cargo and axle-load compliance pressure | -0.8% | National, most acute on NH-44 and NH-48 corridors and at state border checkpoints | Short term (≤ 2 years) |

| Fuel price volatility and cost pass-through constraints | -0.6% | National, most accurate, especially corridors linking Delhi-NCR, Punjab-Haryana, Rajasthan, Gujarat, and Maharashtra | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Truck Fleet and Driver Shortage

Road freight still carries the largest volume base, but its structure also creates one of the clearest limits on the India bulk transport market. Around 75-77% of truck operators own fewer than 5 vehicles, which keeps the sector price-led, weakly capitalized, and uneven in technology adoption. India had nearly 6 million trucks on the road but only around 3.6 million active drivers, meaning 25-30% of fleet capacity sat idle on a typical day and directly constrained throughput at. This shortage matters most for construction materials, agricultural cargo, and industrial chemicals, because these lanes often depend on spot market trucking across semi-urban and regional routes. When demand rises suddenly, small operators usually respond through price increases rather than through disciplined redeployment of spare assets. The result is higher rate volatility, weaker service quality, and a hard ceiling on how much incremental industrial output road freight can absorb without rising cost pressure.

Rail Siding and Plant-Gate First/Last-Mile Gaps

The DFC network improves line-haul economics, but plant-gate connectivity still limits how much of that benefit reaches the broader India bulk transport market. Many industrial sites still lack rail sidings or efficient feeder links, which forces cargo back onto roads even when rail would be cheaper and more reliable on the main haul. This also raises wagon idle time and reduces effective corridor productivity because the issue is no longer only train speed, but also how quickly cargo can enter and leave the network. Maruti Suzuki's in-plant siding at Manesar illustrates what good connectivity can do, as the INR 452.00 crore project (USD 53.98 million) dispatched 100,000 vehicles within 9 months and reduced emissions through rail-based movement. Most mid-scale industrial operators cannot fund dedicated links on that scale, which means the infrastructure gap remains system-wide rather than site-specific. Until siding access, feeder roads, and interchange planning improve in a coordinated way, a meaningful share of bulk traffic will keep moving by road because of access constraints rather than because of superior economics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Transport: Rail and Waterways Erode Road's Structural Lead

Road freight held 65.88% of the India bulk transport market share in 2025, reflecting its unmatched end-point reach and ability to serve sites without rail or water access. That lead remains important because bulk cargo still depends heavily on flexible pickup and delivery across mines, plants, storage yards, and construction sites. The logistics cost assessment cited in the source draft found that heavy-duty trailers weighing more than 55 tonnes operated at INR 1.51 (USD 0.016) per tonne-km for bulk movement, thereby keeping the road attractive where transfer points were limited. Indian Railways loaded a record 1,670.00 MT in FY26, with fertilizer up 13.49% and pig iron and finished steel up 13.11%, which showed that rail demand was strengthening in core industrial categories. These numbers show that the road remains essential, but they also indicate that the balance is beginning to shift, with freight density and corridor quality supporting rail substitution[3]"How India's Dedicated Freight Corridors Are Redrawing the Logistics Map." ITLN, itln.in.

Waterways is projected to expand at a 9.57% CAGR, making it the fastest-growing slice of the India bulk transport market through 2031. National waterways cargo reached 198.00 MMT through February 2026, which confirms that the traffic base is becoming meaningful rather than experimental. The government also wants inland water transport and coastal freight to take a larger share of heavy cargo, which supports longer-term rebalancing across modes. Other modes, including multimodal service bundles, matter beyond their current volume because organized operators are now packaging road, rail, and coastal shipping into unified contracts. That trend should steadily narrow road's structural lead and deepen the role of planned network design in the India bulk transport industry.

By Shipment Form: Dry Bulk Anchors Volume, Liquid and Gaseous Bulk Leads Value Growth

Dry bulk held 57.07% of the India bulk transport market size in 2025, which kept it as the main base for freight volumes across rail, road, and port systems. Coal remained the single most important anchor cargo and accounted for nearly 50% of Indian Railways' loading in FY26, which shows how closely bulk transport still tracks energy and heavy industry demand. Steel and cement output also rose through FY26, which kept ore, coal, clinker, limestone, and aggregate movements active across industrial corridors. Breakbulk is becoming more visible as project cargo, wind components, machinery, and non-containerized industrial loads increase in line with manufacturing expansion. This means shipment diversity is rising even though dry bulk continues to dominate the tonnage base[4]"India's National Waterways Support 145.84 MMT Cargo Transport in FY26; Passenger Traffic Jumps Nearly 6-Fold.", The Hawk, thehawk.in.

Liquid and gaseous bulk is forecast to grow at an 8.17% CAGR through 2026-2031, supported by LNG import infrastructure, refinery throughput, petrochemical chains, and coastal LPG movement. This part of the business grows faster in value because it needs specialized terminals, stricter handling practices, and tighter turnaround coordination than dry bulk does. Aegis Logistics approved a greenfield LPG and liquid terminal project at JNPA worth INR 502.50 crore (USD 60.01 million), with 77,286 MT of LPG storage and 318,100 cbm of liquid products capacity, which shows how private capital is targeting specialized bulk infrastructure. LNG bunkering and chemical logistics are also appearing more often in port development plans, which broadens the future demand base beyond traditional fuels. As these assets scale up, liquid handling should take a larger operational role in the India bulk transport market while dry bulk continues to anchor system throughput.

By End User Industry: Energy Stays Dominant, Construction Drives the Fastest Growth

Energy commodities accounted for 41.48% of the India bulk transport market in 2025 and remained the largest end-user base for line-haul and terminal activity. Coal still dominated the railway freight basket in FY26 even after a slight year-on-year dip, which confirms that the power and steel systems continue to shape freight patterns more than any other end market. Imported coking coal is adding to long-haul port-to-plant demand as new blast furnace and steelmaking capacity comes on stream at major producers. Fertilizer loading also rose 13.49% in FY26, which supports more scheduled movement across agricultural supply chains and industrial input networks. Together, these cargoes provide a stable demand base that supports capacity utilization across road fleets, rail assets, ports, and inland terminals.

Construction aggregates and cement are projected to grow at an 8.66% CAGR, giving this category the fastest expansion path in the India bulk transport market through 2031. The driver is straightforward because budget-backed infrastructure programs and urban expansion keep cement, stone, fly ash, and related construction inputs moving across regions. Cement production rose 8.60% in FY26, and rail cement transport surged after the November 2024 logistics reform, showing that pricing and equipment changes can redirect cargo flows at scale. Mineral and metal ores also remain important, especially on eastern corridors where rail links and port evacuation systems continue to deepen. The overall end-user mix therefore remains energy-led, but growth is broadening toward construction-intensive freight that benefits directly from infrastructure spending.

Geography Analysis

The India bulk transport market is most active across North and West India because these regions combine major industrial clusters, dense freight demand, and direct access to the Western DFC. The JNPT to Delhi NCR connection has sharply improved the movement of industrial inputs and export-linked cargo between ports and inland production centers. The western port cluster, including Mundra, JNPT, Pipavav, and Hazira, remains central for liquid cargo, containers, and multimodal bulk distribution. Mundra is already running near full capacity and forms part of Adani Ports' INR 90,000.00 crore to INR 100,000.00 crore investment plan (USD 10.75 billion to USD 11.94 billion), which underlines how strongly integrated infrastructure players are backing this corridor. In the north, the Delhi-Mumbai Industrial Corridor and the Haryana manufacturing belt generate sustained outbound flows in fertilizers, steel, and auto-linked cargo. Maruti Suzuki's Manesar siding, commissioned in June 2025 and reaching 100,000 vehicle dispatches within 9 months, shows how plant-level rail integration is starting to scale in corridor-linked industrial zones. The INR 10,000.00 crores (USD 1.19 billion) container manufacturing scheme also reinforces the western belt's position as an infrastructure and logistics investment center.

East India is the highest bulk-intensity zone in the India bulk transport market because coal mines, iron ore reserves, steel plants, and fertilizer capacity are concentrated across Odisha, Jharkhand, West Bengal, and Chhattisgarh. The Eastern DFC already improves access from this mineral-heavy belt to northern consumption centers, and the planned Dankuni-Surat DFC would add another major trunk connection through the same geography. The government's focus on NW-5 also strengthens East India's role by linking Talcher-Angul with Paradip and Dhamra, which adds a water-based option to a freight system that has long depended on road and rail. This combination makes the east the country's most strategically important mineral and industrial bulk corridor over the medium term.

South India is becoming a stronger growth zone for the India bulk transport market, especially in liquid bulk, chemicals, fertilizers, and construction-linked freight. Vizhinjam port, commissioned in 2025 and operated by APSEZ, is already at full utilization and is moving into further expansion, which improves South India's role in coastal and international cargo flows. DP World's 49% stake in the Mappedu Multimodal Logistics Park near Chennai also shows that foreign capital now sees the south as an inland logistics destination, not only as a port gateway. As coastal incentives improve the economics of short-sea movement, peninsular bulk corridors should become more competitive for shippers serving domestic and export-oriented industrial clusters.

Competitive Landscape

The India bulk transport market remains moderately fragmented at the operator level, but the ownership of critical infrastructure is becoming more concentrated around integrated platforms. Adani Ports and Special Economic Zone, Container Corporation of India, and DP World are the clearest examples of this shift because each is building combinations of terminals, rail links, inland assets, and digital capabilities. APSEZ is expanding Mundra, Vizhinjam, and Dhamra under a multi-year capital program, which strengthens its ability to keep cargo within its own ecosystem from port entry to inland movement. By contrast, the road freight layer is still dominated by very small fleets, and that price-led structure limits investment in digital tracking, asset optimization, and multimodal execution. This gap creates space for organized mid-tier providers to win share from fragmented operators by offering better schedule reliability, cleaner documentation, and more transport options within a single contract.

The clearest strategic move across the India bulk transport market is the push toward multimodal positioning. Gateway Distriparks plans to expand to 11 rail terminals along the Western DFC by the end of 2026, which should deepen its corridor relevance and improve its access to bulk-linked inland traffic. TCI plans an INR 200.00 crore to INR 250.00 crore vessel acquisition program in FY27, equivalent to USD 23.89 million to USD 29.86 million, to build out its coastal shipping exposure and capture higher-margin freight lanes. CONCOR is also strengthening DFC connectivity between NCR and JNPT while exploring broader rail-sea integration opportunities, which shows that line-haul operators now see maritime linkage as part of core strategy rather than as an adjacent service.

Technology and compliance are becoming more important competitive filters in the India bulk transport market. Organized players can absorb axle-load rules, hazardous cargo controls, and digital process requirements more easily because they spread those costs over larger volumes and broader networks. DP World's role in the Chennai Global Logistics Park, along with its wider inland and rail-linked ambitions, shows that foreign logistics capital is backing integrated domestic freight assets rather than only stand-alone terminal projects. That leaves the service layer open to many operators, but it raises the threshold for companies that want national scale, stronger margins, and durable customer retention.

India Bulk Transport Industry Leaders

-

AllCargo Logistics Pvt. Ltd.

-

Container Corporation of India, Ltd. (CCI)

-

Mahindra Logistics, Ltd.

-

ADANI Group

-

Transport Corporation of India, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Container Corporation of India enhanced its DFC connectivity between NCR and JNPT, effective June 1, 2026, to improve efficiency and reduce transit time on the Western Dedicated Freight Corridor. The development strengthens CONCOR's multimodal positioning as it simultaneously advances the Bharat Container Shipping Line initiative to extend its freight network to international maritime operations.

- May 2026: A.P. Moller–Maersk launched the FI2, a new dedicated weekly ocean service connecting Southern and Eastern China to India's western ports, Shanghai-Ningbo-Nansha-Tanjung Pelepas-JNPT-Pipavav, deployed with 6 vessels of 4,500 TEU capacity each. The service integrates with the Western DFC via Pipavav port for multimodal cargo connectivity to Delhi NCR, Gurugram, and Noida, reducing transit times for automotive, chemical, retail, and technology sector cargo flows.

- May 2026: Container Corporation of India and PSA Mumbai, Bharat Mumbai Container Terminals Pvt. Ltd., signed a strategic MoU to optimize rail container movement from JNPA, leveraging PSA Mumbai's 2.4 million TEU annual capacity to improve EXIM evacuation efficiency and reduce transit times.

- February 2026: Transport Corporation of India formalized a strategic collaboration with FLYING WHALES and FLYING WHALES SERVICES during the France-India summit to deploy the LCA60T cargo airship, 60-tonne payload, for heavy-lift logistics in remote, defense, infrastructure, and disaster relief applications. TCI simultaneously added a 1.5 lakh sq. ft. cold chain warehouse in Gurugram through its JV with Mitsui & Co.

India Bulk Transport Market Report Scope

| Road |

| Rail |

| Waterways |

| Other Modes of Transport, including Multimodal |

| Dry Bulk |

| Liquid and Gaseous Bulk |

| Breakbulk |

| Agricultural Bulk |

| Mineral and Metal Ores |

| Energy Commodities (Crude/LNG/Refined) |

| Construction Aggregates and Cement |

| Industrial Chemicals and Fertilizers |

| Others |

| By Mode of Transport | Road |

| Rail | |

| Waterways | |

| Other Modes of Transport, including Multimodal | |

| By Shipment Form | Dry Bulk |

| Liquid and Gaseous Bulk | |

| Breakbulk | |

| By End User Industry | Agricultural Bulk |

| Mineral and Metal Ores | |

| Energy Commodities (Crude/LNG/Refined) | |

| Construction Aggregates and Cement | |

| Industrial Chemicals and Fertilizers | |

| Others |

Key Questions Answered in the Report

What is the 2026 value of India bulk transport activities and how large can it become by 2031?

The India bulk transport market stood at USD 130.57 billion in 2026 and is projected to reach USD 190.86 billion by 2031 at a 7.89% CAGR, supported by public capex, industrial output, and corridor upgrades.

Which transport mode still carries the largest share of bulk cargo in India?

Road freight remained the largest mode in 2025 with a 65.88% share because it still offers the widest origin and destination coverage across industrial, mining, and construction networks.

Which mode is expected to grow the fastest through 2031?

Waterways is expected to record the fastest growth at a 9.57% CAGR as coastal incentives, new waterways, and port-linked mineral and energy flows gain traction.

Which shipment type grows fastest even though dry bulk leads the volume base?

Dry bulk held 57.07% share in 2025, but liquid and gaseous bulk is forecast to grow faster at an 8.17% CAGR because of LNG, LPG, refinery, and chemical logistics expansion.

Which end-user group contributes the most demand today and which one is rising fastest?

Energy commodities led with a 41.48% share in 2025, while construction aggregates and cement is projected to grow the fastest at an 8.66% CAGR as infrastructure and urban projects continue.

What is the main operational challenge that could slow freight efficiency over the next 5 years?

The largest near-term drag is the combination of a fragmented truck fleet and a driver shortage, with 25-30% of truck capacity idle on a typical day and many operators owning fewer than 5 vehicles.

Page last updated on: