India Automotive Reed Sensors Switches Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

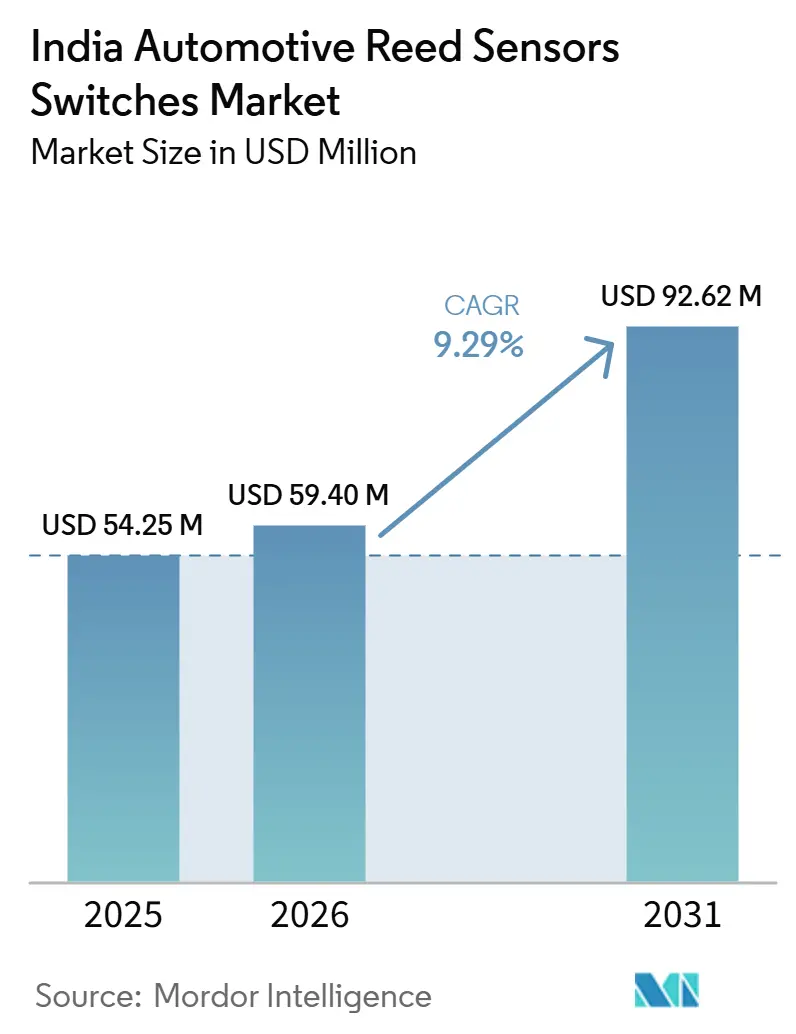

| Base Year Market Size (2025) | USD 54.25 Million |

| Market Size (2026) | USD 59.40 Million |

| Market Size (2031) | USD 92.62 Million |

| Growth Rate (2026 - 2031) | 9.29% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Automotive Reed Sensors Switches Market Analysis by Mordor Intelligence

The automotive reed sensors and switches market in India is expected to grow from USD 54.35 million in 2025 to USD 59.40 million in 2026, and is forecast to reach USD 92.62 million by 2031, at a CAGR of 9.3% over 2026-2031. The market is expanding faster than the broader regional trend, as vehicle programs in the country are adding more sensing points driven by electrification and increasing feature intensity. Electric vehicle sales in India crossed 2.45 million units in FY2025-26, supporting a wider installed base for battery management, charging, and safety interlock functions that use reed components. The market is also benefiting from a broader shift in vehicle design, where electronics-rich architectures, stronger localization plans, and supplier qualification requirements are directing more value toward component families that can meet cost, durability, and compliance needs simultaneously. In this environment, the market is drawing opportunity from both new EV platforms and mainstream passenger vehicle programs that continue to add convenience, access, and safety functions without a significant increase in component cost. Competitive dynamics remain shaped by a limited set of qualified global suppliers, rising domestic-content expectations, and ongoing pressure to defend reed technology against solid-state substitutes in lower-voltage body-electronics applications.

Key Report Takeaways

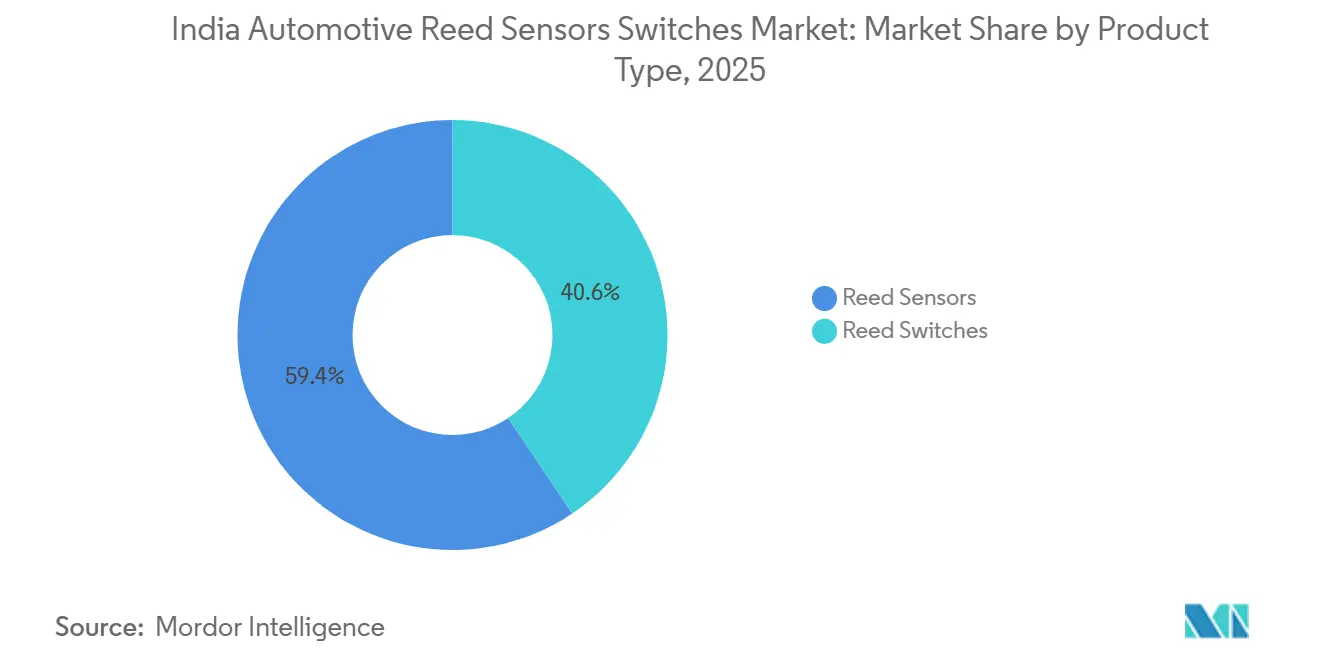

- By product type, reed switches held 59.41% revenue share in 2025, while reed sensors are forecast to expand at an 11.42% CAGR through 2031.

- By application, body electronics accounted for 31.08% of revenue in 2025, while battery and charging systems are projected to grow at a 14.42% CAGR through 2031.

- By sales channel, OEMs held 80.42% revenue share in 2025 and also recorded the highest projected CAGR at 10.12% through 2031. .722% CAGR through 2031.

- By sales channel, OEMs held 80.42% revenue share in 2025 and also recorded the highest projected CAGR at 10.1% through 2031.

- By propulsion type, ICE vehicles held 65.80% revenue share in 2025, while battery electric vehicles are projected to grow at a 16.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Automotive Reed Sensors Switches Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Adoption and Incentives | +3.5% | National (High In Metro States) | Short term (≤ 2 years) |

| Public Charging Rollout | +2.0% | Metro Cities + Highway Corridors | Medium term (2-4 years) |

| Passenger Car Electronics Content | +1.2% | National (PV-Dominant) | Medium term (2-4 years) |

| Body Electronics Replacement Cycle | +1.0% | Pan-India | Medium term (2-4 years) |

| OEM Localization and Scale | +0.8% | Key Auto Clusters | Medium term (2-4 years) |

| Compact Module Miniaturization | +0.4% | OEM/Tier Programs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Electrification-Driven Growth in Battery and Charging Sensing Points

The automotive reed sensor switches market in India is seeing its strongest demand from the rise in high-voltage sensing points inside EV battery packs and onboard chargers. Reed relays placed between the high-voltage battery bus and low-voltage measurement electronics offer breakdown voltages from 400 VDC to 1,500 VDC, keeping them relevant in applications where isolation and package efficiency are both required. India has recorded significant EV sales growth in recent years, with electric car sales expanding substantially on a year-on-year basis, indicating that the number of platforms requiring these functions is rising rapidly. Each new EV architecture adds several reed-based isolation and connector detection points, so volume growth in vehicles also multiplies component demand within each platform. As a result, battery and charging systems are growing faster than the rest of the automotive reed sensor switches market in India, even though they still represent a narrower application base than body electronics today[1]"EV sales in India surpass 2.45 million units in FY2026", Autocar, autocarpro.in.

Increasing Electronics Content in Body Modules and Comfort/Access Features

Body electronics represents the largest application segment by value. Growth is supported by rising penetration of electronic closures and access systems, including door, hood, and trunk status monitoring, latch modules, and actuator position detection. OEMs continue to introduce additional comfort and safety features even in cost-sensitive vehicle categories, resulting in a steady increase in the number of state-detection points.

Reed switches remain a practical solution in these applications due to predictable switching behavior, proven durability, and ease of integration into established module designs.

Preference for Sealed, Reliable Switching Solutions in Harsh Automotive Environments

Reed-based technologies maintain relevance in applications where long service life and stable performance are required under harsh operating conditions. These include exposure to heat, vibration, moisture, and contamination. Modules located near vehicle exteriors or within exposed housings often prioritize sealed switching solutions to reduce failure risk.

The inherent sealing and contact isolation characteristics of reed components support continued adoption in such environments, particularly where functional requirements remain binary.

OEM Localization and Scale-Up of Supply

Localization is becoming a structural demand driver for the Automotive reed sensors switches market in India because major automakers are raising domestic content expectations across advanced components and associated electronics. Hyundai Motor India disclosed 92% localization across 1,238 key components in January 2025. It began local battery pack assembly at its Chennai plant through Mobis India, which shows how vehicle programs are tying more electronics value to local qualification [2]“HMIL Commits to Atmanirbhar Bharat by Localizing Over 1,200 Key Components and EV Battery-Packs,” Hyundai Motor India Limited, hyundai.com.

The broader Indian automotive industry has planned significant investment to deepen localization of advanced components, and the PLI auto scheme has reported substantial sales figures, indicating visible commercial traction. This environment puts pressure on foreign suppliers to establish local inventory, local assembly, or reliable domestic partnerships before the next platform sourcing cycle. It also raises the barrier for low-cost entrants that cannot support qualification, supply continuity, or localized customer service at the standard expected by Indian OEMs and Tier-1 suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Solid-State Sensor Substitution | -1.1% | National | Medium term (2-4 years) |

| Incentive and Policy Uncertainty | -0.8% | National | Short term (≤ 2 years) |

| Price Sensitivity in Mass Market | -0.6% | Tier-2/3 + Value Segments | Medium term (2-4 years) |

| OEM Qualification Lead-Time Delays | -0.4% | OEM/Tier Programs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Substitution by Solid-State Alternatives

Competition from solid-state sensing technologies remains a key restraint. In certain magnetic or proximity sensing applications, OEMs may prefer semiconductor-based solutions to align with IC-driven architectures or enable additional diagnostics. While this trend does not eliminate the use of reed technologies, it can limit penetration in subsystems where continuous sensing or complex signal processing is required.

Cost-Down Pressure and Design-to-Cost

India’s automotive market remains highly cost-competitive. OEMs continuously pursue bill-of-material optimization, which may lead to consolidation of sensing points or alternative design approaches. Even when reed components meet technical requirements, program-level cost targets can influence final selection decisions, particularly in high-volume vehicle platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Reed Switches Lead Today; Reed Sensors Expand Faster

Reed switches accounted for 59.41% of revenue in 2025, keeping them the largest product category within the Automotive reed sensor switches market in India. Their scale is tied to broad use across door-latch position detection, trunk release mechanisms, seat-position functions, and fluid-level sensing arrays that together cover more than 25 application points in a typical production vehicle. This installed base gives reed switches a durable position because a design already qualified for a vehicle platform is not easily replaced mid-platform life. Reed sensors remain the fastest-growing category, projected to grow at a 11.42% CAGR through 2031 as EV battery systems and charging circuits use them for isolation measurement and connector detection. This means the product mix is shifting even though the current Automotive reed sensors switches market share still sits with conventional switches.

Miniaturization is reinforcing this transition, as newer vehicle modules require smaller packages that fit more tightly within board layouts without compromising reliability. Standex Electronics launched the MK33 SMD series, a bare-glass, surface-mount reed switch designed for space-constrained PCB layouts. This product direction is relevant to the automotive reed sensors and switches market, as Indian OEMs and Tier-1 suppliers are integrating more functions into consolidated modules and require direct PCB compatibility. The same trend applies to reed sensors, where compact, diagnostics-friendly formats are easier to incorporate into EV and comfort electronics modules without a significant footprint penalty.

By Application: Body Electronics Anchor Demand; Battery and Charging Systems Lead Growth

Body electronics accounted for 31.08% of the automotive reed sensor switches market in India in 2025, making it the largest application segment by revenue. This position is driven by India's SUV-heavy product mix, where climate systems, access modules, soft-close functions, and roof mechanisms all require sensing positions that reed components can serve. Battery and charging systems are projected to grow at a 14.42% CAGR through 2031, materially faster than the overall market, reflecting additional isolation, pre-charge, and connector-engagement positions created by each new BEV program.

The application mix is shifting from body-heavy demand toward a broader distribution that gives EV-related functions greater weight over time. Safety and security, infotainment and comfort systems, and transmission and braking systems continue to provide stable supporting demand. Safety-oriented adoption is further supported by growing consumer focus on protective features in mainstream passenger vehicles, keeping cost-competitive switching elements relevant in seatbelt, airbag, and access-linked functions. Engine and powertrain demand remains limited, as Hall-effect alternatives rather than reed products already serve many core ICE sensing functions.

By Vehicle Type: Passenger Cars Dominate; Commercial Vehicles Grow Faster

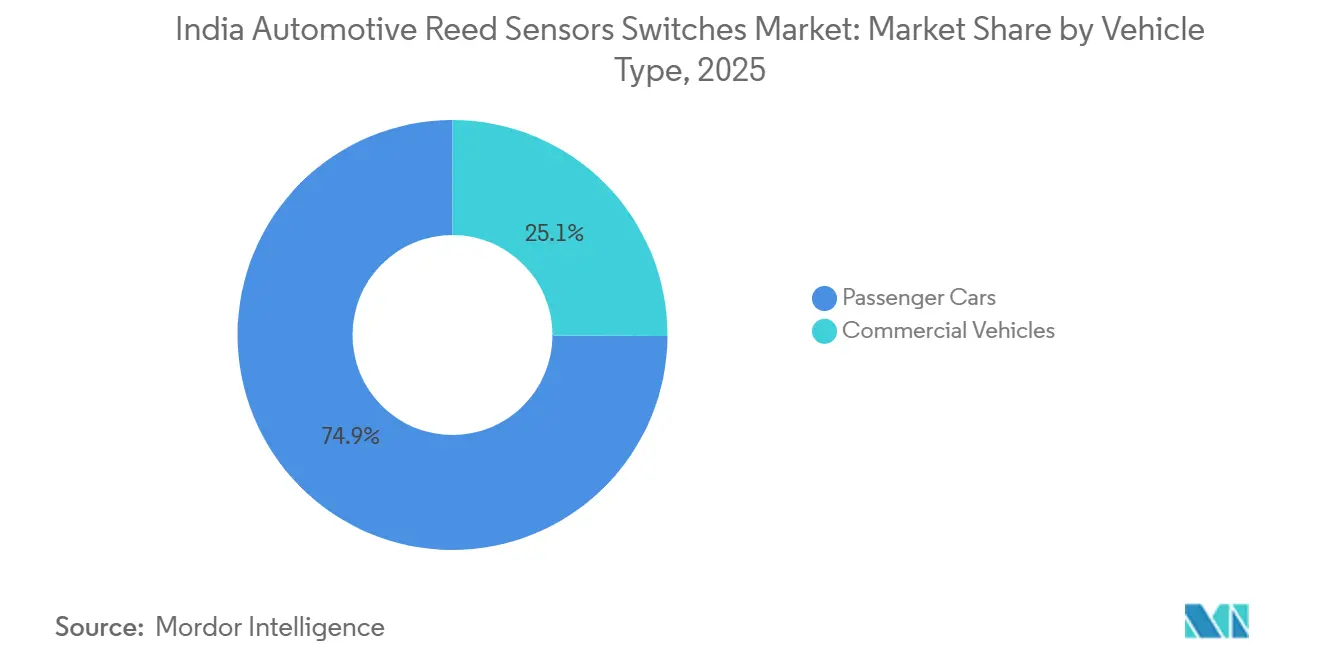

Passenger cars held a 74.92% revenue share in 2025, making them the clear volume anchor for the Automotive reed sensors switches market in India. India’s domestic passenger car sales reached 4.64 million units in FY2025-26, and this scale keeps demand high for everyday body, access, and convenience sensing functions across hatchbacks, sedans, and utility vehicles. The segment also benefits from rising feature density, since powered tailgates, proximity functions, and cabin electronics all increase the number of potential switch locations per vehicle. Commercial vehicles are smaller in current value terms, but they are projected to grow at 10.72% CAGR through 2031 and are becoming more important as fleet electrification moves into procurement-led deployment. This gives the automotive reed sensors switches market in India a second demand engine beyond conventional passenger vehicle volumes.

The commercial case is relevant because electric buses and trucks carry larger battery packs and require more high-voltage management positions than a typical passenger EV. Tata Motors has disclosed a substantial electric commercial vehicle order book, indicating that demand for electrified fleets is moving beyond pilot use. This increases the component value per vehicle for suppliers serving battery isolation, pre-charge, and related safety functions. Passenger cars remain the revenue base of the automotive reed sensors switches market, while commercial vehicle electrification is adding a more specialized, higher-function demand layer.

By Sales Channel: OEMs Dominate and Remain the Primary Growth Engine

OEMs accounted for 80.42% of the automotive reed sensor switches market in 2025 and are projected to grow at a 10.11% CAGR through 2031. Demand is increasingly driven by platform design decisions rather than aftermarket replacement demand. Major OEMs and Tier-1 suppliers are engaging component suppliers earlier in development cycles, giving approved reed switch families an extended supply runway once a platform enters production. A component that fails to qualify can remain embedded throughout the full production life of a vehicle line.

The aftermarket accounted for the remaining 19.58% of revenue and faces greater commoditization pressure from unbranded imports and lower barriers to entry. Longer OEM warranty coverage and stronger authorized service networks are limiting the pace of replacement demand growth in the early years of vehicle ownership. This environment favors suppliers that offer integrated sensor modules, connector assemblies, or other validated subassemblies that are more difficult to displace on price alone. As a result, the OEM channel remains the most direct route to scale and stability in the automotive reed sensor switches market in India.

By Propulsion Type: ICE Leads Current Volume; BEVs Expand the Fastest

Internal combustion engine vehicles account for the largest share of demand, with a 65.80% revenue share in 2025. This reflects the current production mix and the large installed base of ICE vehicles in India. Reed sensors and switches remain widely deployed in ICE platforms for body electronics and basic safety-related sensing functions.

Battery electric vehicles are projected to grow at the fastest rate, registering a CAGR of 16.42% during the forecast period. Growth is supported by policy momentum, rising EV adoption, and the continued expansion of charging infrastructure. BEV platforms introduce additional battery and charging-related sensing requirements, which increase sensing density per vehicle and support faster growth for reed-based solutions.

Geography Analysis

Within India, demand for automotive reed sensors and switches is closely linked to the geographic distribution of OEM and Tier-1 manufacturing clusters. States with a high concentration of vehicle and module production facilities account for a significant share of demand, as reed components are primarily sourced through OEM-led supply chains. These regions benefit from higher vehicle output, deeper Tier-1 integration, and faster adoption of electronics-intensive modules, particularly in passenger vehicles.

Tamil Nadu and Maharashtra remain the primary centers for vehicle assembly and the supporting supplier ecosystem. Hyundai's Chennai operations anchor the south, with local battery pack assembly reinforcing Tamil Nadu's role in the EV-linked electronics supply chain. Maharashtra remains significant through its concentration of OEM and Tier-1 activity around Pune. Assam is also notable, where Tata Electronics and Qualcomm Technologies plan to manufacture automotive modules at Tata's OSAT facility in Jagiroad, which is expected to generate downstream demand for electromechanical sensing components.

India has recorded strong EV sales growth in recent years, with electric car sales rising steadily and expanding demand for battery and charging system components that are more reed-intensive than standard ICE applications. EV-linked procurement is sensitive to product rollouts, platform timing, and infrastructure buildout, creating quarter-to-quarter demand variability. Suppliers with regional inventory, local customer support, and qualification depth are better positioned to capture this demand.

Competitive Landscape

The automotive reed sensor switches market in India has a medium concentration profile, led by a small group of established global specialists. Standex Electronics, Littelfuse, and TE Connectivity are the most prominent players, supporting OEM-grade validation, broad product catalogs, and engineering engagement with Tier-1 module suppliers. Their advantage lies in packaging reed elements into qualified assemblies that are difficult to evaluate on a unit-price basis alone, thereby keeping entry barriers high even in a cost-sensitive market like India.

Recent company actions illustrate how competition is evolving. In January 2026, Standex Electronics launched the KS01 reed technology key switch, an IP67-rated, hermetically sealed solution for harsh environments. Littelfuse introduced the 59177 Series ultra-miniature overmolded reed switch, targeting space-constrained automotive and EV designs. TE Connectivity has focused on margin defense and deeper platform integration through greater materials control and broader participation in sensor modules. The market is rewarding suppliers that combine scale, reliability, and application engineering over those competing on commodity pricing alone.

Competition also comes from Asian price challengers and adjacent solid-state sensor suppliers, with domestic participation remaining limited. Hall-effect alternatives continue to improve in body electronics and latch-related functions, meaning incumbents must differentiate around isolation, sealing, and high-voltage use cases where reed switches retain a practical advantage. The competitive focus is shifting from basic switch supply toward solution depth, validation records, and relevance to EV architectures.

India Automotive Reed Sensors Switches Industry Leaders

-

Littelfuse, Inc.

-

Standex Electronics

-

Coto Technology, Inc.

-

PIC GmbH

-

Aleph

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: JSW MG Motor India unveiled ADAPT, India's first multi-powertrain new energy vehicle platform supporting EV, PHEV, strong hybrid, and range-extender configurations. The company committed INR 3,000-4,000 crore over the next few years, with capacity expanding from 120,000 to 160,000 units annually by March 2027. Each new powertrain variant under ADAPT resets reed sensor specifications for battery isolation, connector engagement, and body electronics modules.

- January 2025: Hyundai Motor India disclosed 92% localization across 1,238 key components and commenced local battery pack assembly at its Chennai plant through Mobis India, the first model equipped being the CRETA Electric. The initiative reduced foreign exchange exposure and directly increased India-based demand for locally qualified reed sensors in body and battery electronics applications.

India Automotive Reed Sensors Switches Market Report Scope

Automotive reed switches are magnetically actuated electromechanical components that open or close in the presence of a magnetic field. Automotive reed sensors typically refer to reed-switch-based sensing assemblies that are packaged, sealed, or overmolded and integrated into housings. These solutions are used for position, proximity, closure, and safety interlock sensing across various vehicle systems.

The scope of the market includes segmentation by product type (reed switches and reed sensors), application (body electronics, battery and charging systems, and others), vehicle type (passenger cars and commercial vehicles), sales channel (OEMs and aftermarket), and propulsion type (internal combustion engine vehicles, battery electric vehicles, and others). Market sizing and forecasts are provided in USD terms.

| Reed Sensors |

| Reed Switches |

| Engine and Powertrain Systems |

| Body Electronics |

| Safety and Security Systems |

| Infotainment and Comfort Systems |

| Transmission and Braking Systems |

| Battery and Charging Systems |

| Other Applications |

| Passenger Cars |

| Commercial Vehicles |

| OEMs |

| Aftermarket |

| Internal Combustion Engine (ICE) Vehicles |

| Hybrid Electric Vehicles (HEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Battery Electric Vehicles (BEV) |

| Fuel Cell Electric Vehicles (FCEV) |

| Segmentation by Product Type (Value, USD) | Reed Sensors |

| Reed Switches | |

| Segmentation by Application (Value, USD) | Engine and Powertrain Systems |

| Body Electronics | |

| Safety and Security Systems | |

| Infotainment and Comfort Systems | |

| Transmission and Braking Systems | |

| Battery and Charging Systems | |

| Other Applications | |

| Segmentation by Vehicle Type (Value, USD) | Passenger Cars |

| Commercial Vehicles | |

| Segmentation by Sales Channel (Value, USD) | OEMs |

| Aftermarket | |

| Segmentation by Propulsion Type (Value, USD) | Internal Combustion Engine (ICE) Vehicles |

| Hybrid Electric Vehicles (HEV) | |

| Plug-in Hybrid Electric Vehicle (PHEV) | |

| Battery Electric Vehicles (BEV) | |

| Fuel Cell Electric Vehicles (FCEV) |

Key Questions Answered in the Report

What is the current and forecast value of automotive reed sensors switches in India?

The Automotive reed sensors switches market in India was valued at USD 54.35 million in 2025, stands at USD 59.40 million in 2026, and is forecast to reach USD 92.62 million by 2031 at a 9.29% CAGR.

Which product category leads demand in India?

Reed switches led with 59.41% revenue share in 2025 because they remain widely used across body, access, seat, and fluid-level functions in mainstream vehicle platforms.

Which application is growing the fastest?

Battery and charging systems are expanding at a 14.42% CAGR through 2031 because EV platforms need more isolation, pre-charge, and connector detection points than many traditional applications.

How important are EVs to future demand?

EVs are becoming central to future expansion because battery electric vehicles are projected to grow at a 16.42% CAGR and each electrified platform adds several new reed-based sensing points.

What is the main competitive threat to reed technology in vehicles?

The clearest challenge comes from solid-state Hall-effect devices in body electronics, but reed products still retain an advantage in high-voltage isolation, hermetic sealing, and certain safety-critical functions.

Page last updated on: