Idiopathic Short Stature Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

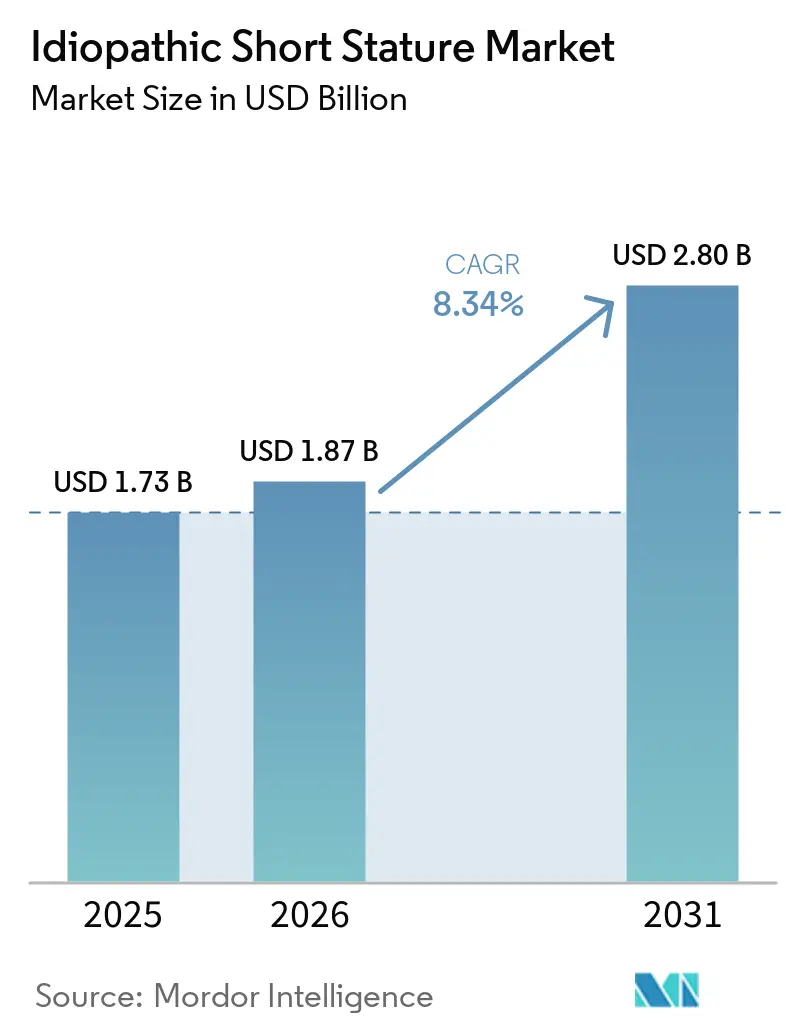

| Market Size (2026) | USD 1.87 Billion |

| Market Size (2031) | USD 2.80 Billion |

| Growth Rate (2026 - 2031) | 8.34% CAGR |

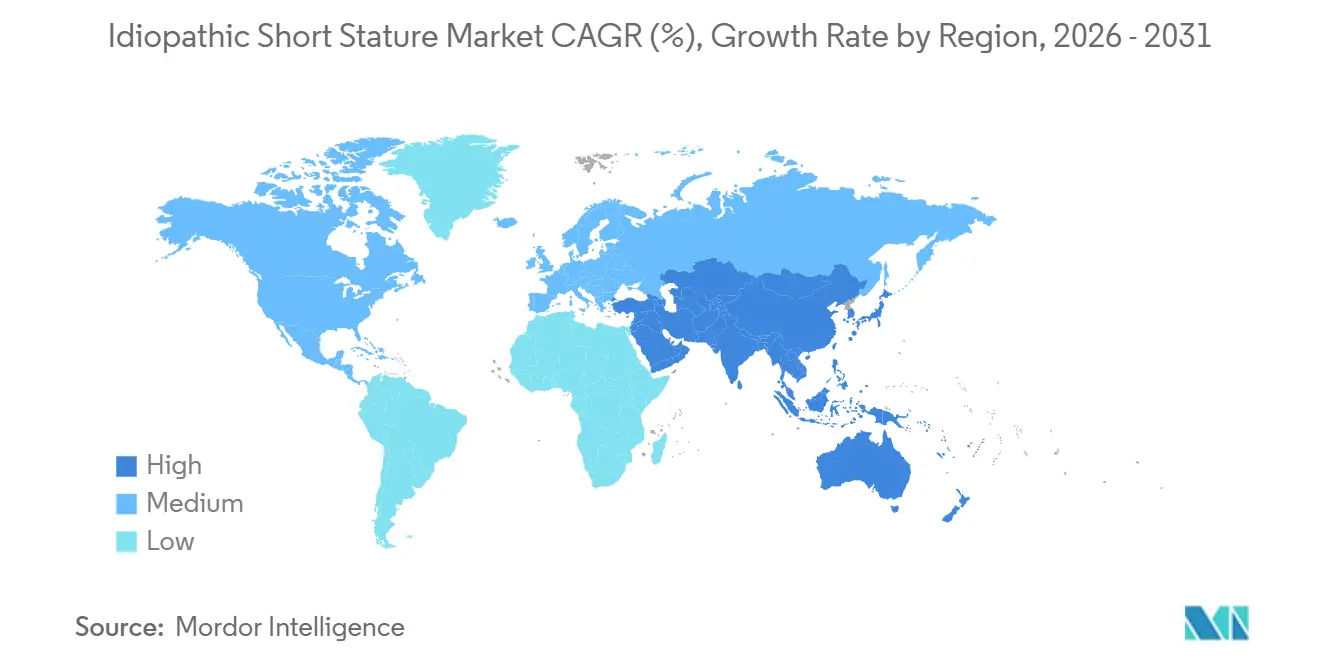

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Idiopathic Short Stature Market Analysis by Mordor Intelligence

The Idiopathic Short Stature Market size is expected to grow from USD 1.73 billion in 2025 to USD 1.87 billion in 2026 and is forecast to reach USD 2.80 billion by 2031 at 8.34% CAGR over 2026-2031.

Steady uptake of recombinant human growth hormone (rhGH) therapy, widening genomic screening programs, and the regulatory green light for once-weekly analogs are broadening the treated population and lifting revenue, even as payer scrutiny remains intense. Weekly injections that cut the annual needle burden from 365 to 52 doses are driving adherence gains, tipping physician preference toward long-acting options. Biosimilar competition is compressing prices in Asia-Pacific, while connected auto-injectors are shifting care from hospitals to homes and supporting real-time adherence monitoring. Cold-chain innovations, including formulations that remain stable for six months at room temperature, are expanding access in regions with weak logistics infrastructure.

Key Report Takeaways

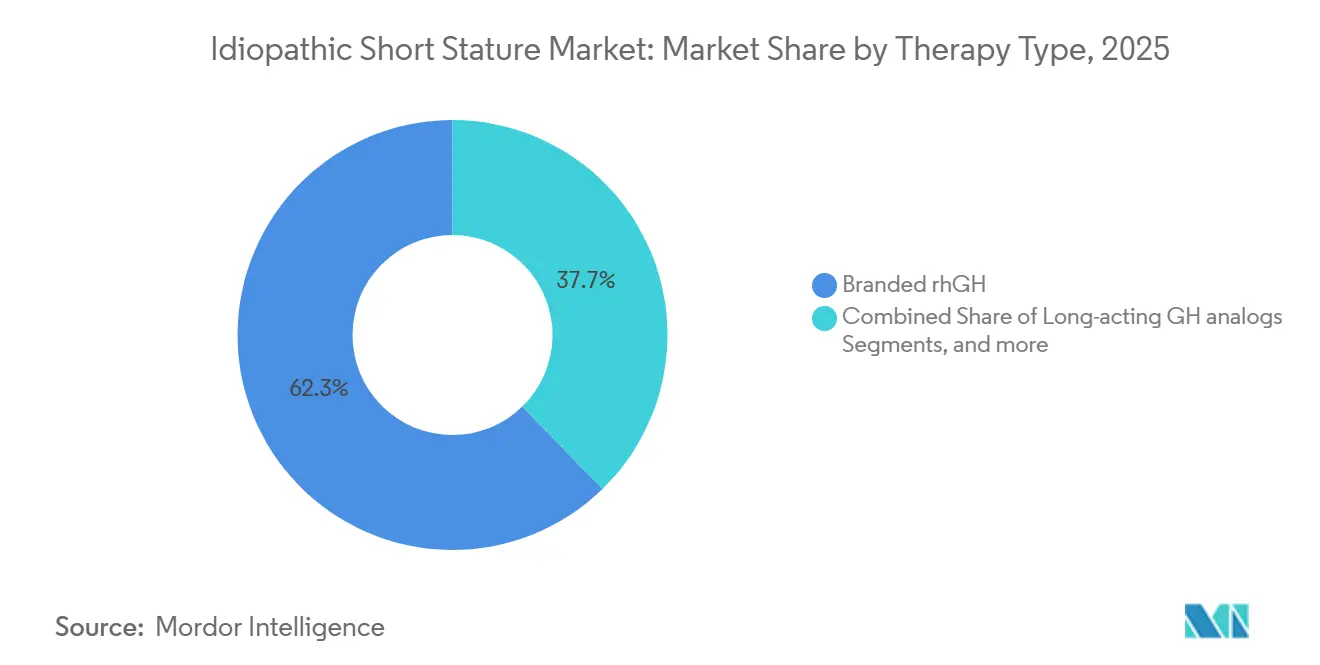

- By therapy type, branded rhGH formulations led with 62.20% of the idiopathic short stature market share in 2025. Long-acting growth hormone analogs are forecast to post the fastest segment growth at 9.32% CAGR through 2031.

- By age group, pre-pubertal children accounted for 65.05% of the idiopathic short stature market size in 2025. The same cohort is projected to expand at 9.55% CAGR between 2026 and 2031.

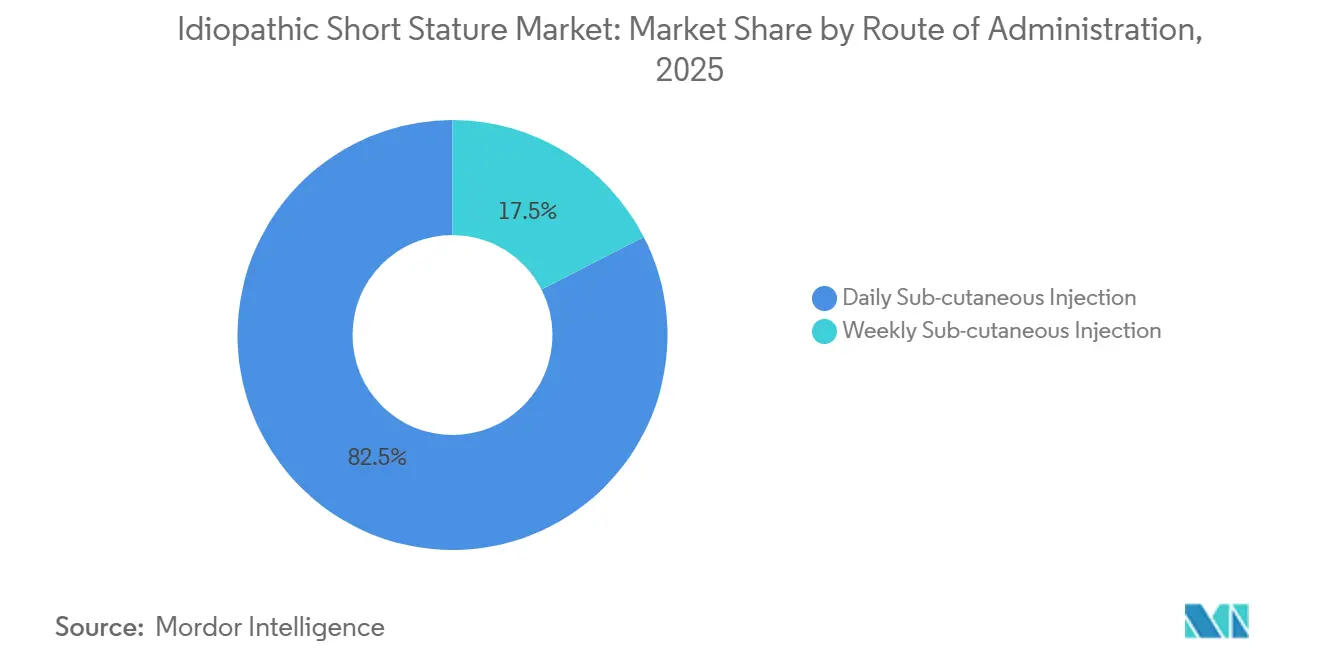

- By route of administration, daily subcutaneous injections held 82.54% share in 2025. Weekly formulations are expected to advance at 10.02% CAGR to 2031

- By end user, hospitals retained 42.89% revenue share in 2025. Home-care settings are expected to rise at 9.20% CAGR through 2031.

- By geography, North America accounted 38.13% of the share in 2025, and Asia-Pacific is expected to grow at a CAGR of 9.33% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Idiopathic Short Stature Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising prevalence of ISS diagnosis | +1.8% | Global, with acceleration in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Growing adoption of rhGH biosimilars | +1.5% | Asia-Pacific core, spillover to Middle East & Africa | Short term (≤ 2 years) |

| Expanded insurance reimbursement | +1.2% | North America & Europe, selective APAC markets | Medium term (2-4 years) |

| Long-acting GH formulations pipeline | +2.1% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Genomic screening for early detection | +0.9% | North America, Europe, urban APAC centers | Long term (≥ 4 years) |

| Medical tourism for pediatric endocrinology | +0.6% | Latin America (Mexico, Costa Rica), Southeast Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of ISS Diagnosis

Next-generation sequencing has reduced the cost and turnaround time for genetic evaluations, enabling clinicians to exclude monogenic causes such as SHOX deficiency and reclassify children into the idiopathic short stature market treatment pool. An October 2025 guideline recommends multiplex ligation-dependent probe amplification for all children below -2.5 standard deviations, which standardizes referrals. In Abu Dhabi, idiopathic short stature accounted for 34.8% of all rhGH prescriptions from 2011 to 2022, surpassing growth hormone deficiency.[1]Sara Salem Al Jneibi et al., “Recombinant growth hormone therapy in children with short stature in Abu Dhabi,” Frontiers in Pediatrics, frontiersin.org Although the diagnostic yield of sequencing remains 14.9%, the significant increase in screened children is driving demand. As more hospitals implement electronic growth charts, deviations prompt earlier specialist referrals, increasing volume in North America and the Gulf.

Growing Adoption of rhGH Biosimilars

Price-competitive biosimilars are transforming the idiopathic short stature market in China and India, where domestic manufacturers obtained National Reimbursement Drug List coverage in January 2026, reducing annual therapy costs by more than 50%. Intas Pharmaceuticals’ fermentation-to-fill pipeline provides a cost advantage once Indian state payers finalize reimbursement rules. In Latin America, mandatory coverage in Argentina is hindered by administrative bottlenecks that disrupt supply and negatively impact clinical outcomes. Europe and North America lag behind as physicians remain loyal to originator brands and regulatory requirements for immunogenicity data extend approval timelines.

Expanded Insurance Reimbursement

Insurance coverage is the most significant factor influencing market access. The FDA’s 2003 decision forms the basis for most U.S. private-payer policies, yet a seven-year review revealed only a 15% approval rate, highlighting stringent prior-authorization challenges. Argentina’s Plan Médico Obligatorio technically covers idiopathic short stature, but delays and expiring authorizations frequently interrupt therapy. Abu Dhabi’s inclusive insurance policies allow idiopathic short stature to account for a third of growth hormone prescriptions, demonstrating how reimbursement alignment can drive demand.

Long-Acting GH Formulations Pipeline

Weekly injections address adherence challenges by reducing dose frequency to 52 per year, eliminating the penalty of 52 missed days when children skip one daily shot each week. Ascendis Pharma’s SKYTROFA achieved EUR 206.2 million (USD 220 million) in 2025 revenue and captured a 6.5% U.S. market share following its pediatric launch, supported by a rechargeable smart injector with a 94% ease-of-use rating.[2]Infobae Health Desk, “Estudio muestra brecha de género en acceso al tratamiento,” infobae.com Novo Nordisk’s Sogroya became the first once-weekly analog explicitly approved for idiopathic short stature in February 2026, with 78.6% of patients preferring its pen over competitor devices. Japan’s JCR initiated phase III trials for JR-142 in December 2024, reflecting increased regional research and development investment. Pfizer’s NGENLA received approval in Argentina in 2023 but remains restricted by payers.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent regulatory scrutiny & high therapy cost | -1.4% | Global, acute in Europe and select U.S. payers | Medium term (2-4 years) |

| Low awareness / delayed diagnosis in LICs | -0.8% | Sub-Saharan Africa, South Asia, rural Latin America | Long term (≥ 4 years) |

| Ethical concerns over non-medical height use | -0.6% | Europe, selective North America payers | Long term (≥ 4 years) |

| Cold-chain constraints for biologics | -0.7% | Sub-Saharan Africa, Southeast Asia, rural South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Scrutiny & High Therapy Cost

The EMA’s 2007 refusal to approve idiopathic short stature contrasts with FDA acceptance and establishes a two-tier access structure, as European payers cite ethical concerns when rejecting claims. U.S. annual therapy costs of USD 20,000-50,000 push insurers toward strict prior-authorization, while pediatric endocrine societies advise caution, reinforcing payer denials. Long-acting analogs face additional safety checks because continuous GH exposure increased edema rates in trials. Argentine private insurers systematically defer coverage for premium analogs despite local approval, framing high cost as the primary barrier.

Low Awareness / Delayed Diagnosis in Low-Income Countries

Primary-care under-recognition delays treatment initiation beyond the optimal pre-pubertal window in South Asia, Latin America, and Africa. A 2025 review of 12 Latin American nations found the median initiation age exceeded 10 years, significantly reducing growth potential. Cultural norms often attribute short stature to hereditary factors, particularly for girls, leading to gender-skewed treatment ratios as high as 80% male in Costa Rica.[3]Primera Edición Staff, “ANMAT aprobó una hormona de crecimiento semanal,” primeraedicion.com.ar Limited specialist clinics, long travel distances, and out-of-pocket costs create additional challenges, shrinking the addressable idiopathic short stature market despite evident biological need.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Type: Biosimilars Challenge Branded Dominance

In 2025, branded rhGH held a 62.20% market share. However, long-acting analogs are set to outpace the market, growing at a projected 9.32% CAGR through 2031, making them the fastest-growing segment in the idiopathic short stature market. Ascendis Pharma’s SKYTROFA, within just 18 months, secured a notable 6.5% share in the U.S. market. This demonstrates that premium pricing can coexist with payer acceptance, especially when adherence benefits are evident. Conversely, in China, biosimilar approvals reduced therapy costs by 75%, broadening the idiopathic short stature market's accessibility to middle-income families. While Western companies strengthen their market share with connected devices and expanded labels, regional players effectively leverage government tenders to secure volume contracts, particularly in county-level hospitals.

By Age Group: Pre-Pubertal Focus Fuels Volume Surge

In 2025, children aged 10 and under constituted 65.05% of treated patients. This segment is projected to grow at a robust 9.55% CAGR through 2031, driven by earlier detection of growth deficits through genomic screening. Initiating therapy pre-puberty can secure an annualized growth velocity often surpassing 11 cm. While adolescents still represent a significant portion of the idiopathic short stature market, their growth is tempered due to the diminishing efficacy post growth-plate closure. Health campaigns are now proactively targeting primary schools with height-monitoring initiatives, streamlining referrals to pediatric endocrine clinics.

By Route of Administration: Weekly Injections on the Rise

Daily injections commanded an 82.54% market share in 2025, highlighting established prescribing patterns and the widespread presence of biosimilars. Yet, weekly formulations are poised for a surge, projected to grow at a 10.02% CAGR through 2031, marking the steepest ascent among administration routes. This shift is largely attributed to a growing emphasis on convenience among physicians. Clinical trials indicate that both daily and weekly injections yield comparable growth velocities, addressing and neutralizing prior clinical reservations.

By End User: Home-Care Expands with Enhanced Monitoring

In 2025, hospitals accounted for a 42.89% market share, primarily due to the need for specialist oversight during diagnosis and treatment initiation. However, the home-care segment is on an upward trajectory, expanding at a 9.20% CAGR through 2031. This growth is supported by the advent of connected devices that relay adherence logs. For instance, Merck’s easypod demonstrated a notable clinical advantage, lifting height SDS by 0.23 over four years compared to non-connected alternatives. Payers are incentivizing this trend, offering broader coverage for auto-injectors in recognition of reduced outpatient visits, while families are drawn to the convenience of at-home care.

Geography Analysis

In 2025, North America accounted for 38.13% of global revenue, supported by strong insurance frameworks and high per-capita drug spending. However, only 15% of prior-authorization requests for idiopathic short stature succeed, reflecting ongoing concerns about cost-effectiveness. Despite premium pricing, Skytrofa achieved a 6.5% share in the US market within 18 months, demonstrating physicians' preference for its weekly regimen. Access to treatments in Canada varies by province; some provinces provide reimbursements through exceptional drug programs, while others restrict funding to classical deficiencies, resulting in uneven national uptake.

Asia-Pacific is set to lead with a projected 9.33% CAGR through 2031. In January 2026, China's inclusion in the NRDL reduced patient co-pays by more than half, driving increased demand among urban middle-income families. Genescience dominates the market, holding over 70% of China's rhGH sales and leveraging its scale to deter new entrants. Meanwhile, Indian biosimilar firms are targeting export opportunities in Southeast Asia once the WHO pre-qualification is secured. South Korea and Japan are advancing their domestic pipelines with innovative long-acting analog options.

Europe grapples with the EMA's 2007 decision, leaving many patients reliant on off-label prescriptions. In Germany, funding for idiopathic short stature is tightly regulated, based on criteria such as genetic potential disparity. The UK's NHS rarely approves treatments, typically doing so only on compassionate grounds. Southern European countries rely on regional health authorities, leading to disparities and hindering the market's growth for idiopathic short stature. While Western Europe has adequate cold-chain stability, Eastern Europe continues to face logistical challenges, particularly in rural areas.

Competitive Landscape

The idiopathic short stature market exhibits moderate concentration. Novo Nordisk, Pfizer, and Ascendis Pharma lead the long-acting category, while Chinese and Indian biosimilar manufacturers compete on price in densely populated emerging economies. Novo Nordisk’s February 2026 U.S. approval of Sogroya for idiopathic short stature provides a first-mover advantage among weekly analogs. Ascendis differentiates itself with a smart rechargeable injector offering six-month room-temperature stability, a feature particularly beneficial in regions with unreliable refrigeration. Pfizer leverages its global distribution capabilities but faces challenges from payer resistance to Somatrogon’s premium pricing.

Device innovation has become a key strategic focus. LG Chem’s April 2026 EcoPen 48, developed in partnership with Ypsomed, emphasizes sustainability and user convenience, a strategy expected to influence tender evaluations. Merck’s easypod connectivity data supports value-based contracts that link reimbursement to adherence metrics, a model gaining traction among insurers. Research and development pipelines are also exploring oral GH secretagogues. If these prove to have efficacy comparable to injectables, they could disrupt the market, although commercialization is unlikely before the late 2030s.

Regional manufacturers are pursuing distinct strategies. GeneScience is investing in thermostable formulations to address China’s long-distance cold-chain challenges, while Intas Pharmaceuticals is preparing a U.S. filing for its biosimilar to enter the lucrative but heavily regulated Western markets. In Latin America, despite ANMAT approval, NGENLA faces payer resistance, illustrating that regulatory approval alone does not guarantee market adoption when budget constraints are a factor.

Idiopathic Short Stature Industry Leaders

Eli Lilly and Company

Novartis AG

Pfizer Inc.

Merck KGaA

F-Hoffmann-La Roche Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: LG Chem introduced the cartridge-replaceable Utropin EcoPen 48 in partnership with Ypsomed, emphasizing convenience and reduced plastic waste.

- March 2026: Novo Nordisk secured FDA approval for Sogroya in Noonan syndrome, adding to its February 2026 Idiopathic Short Stature label expansion.

- March 2026: BioMarin paused dosing in Voxzogo trials for Turner, SHOX-, and ACAN-deficiencies after hip-related safety signals.

- January 2026: Ascendis Pharma gained China NMPA clearance for SKYTROFA in pediatric growth hormone deficiency, its first entry into the world’s second-largest GH market.

- July 2025: Ascendis won FDA approval for SKYTROFA in adult growth hormone deficiency, widening its revenue base.

Global Idiopathic Short Stature Market Report Scope

As oer scope of the report, idiopathic short stature (ISS) is a diagnostic term used to describe children who are significantly shorter than their peers without any identifiable medical, genetic, or environmental cause.

The idiopathic short stature (ISS) market is segmented by therapy type, age group, route of administration, and end-user. By therapy type, the market includes branded rhGH, biosimilar rhGH, long-acting GH analogs, and GH secretagogues (oral, pipeline). By age group, the market is segmented into pre-pubertal children (≤10 yrs) and pubertal adolescents (11-18 yrs). By route of administration, the market is segmented into daily sub-cutaneous injection, weekly sub-cutaneous injection, and oral formulations (pipeline). By end-user, the market is segmented into hospitals, specialty endocrine clinics, and home-care settings. By Geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Branded rhGH |

| Biosimilar rhGH |

| Long-acting GH analogs |

| GH secretagogues (oral, pipeline) |

| Pre-pubertal Children (?10 yrs) |

| Pubertal Adolescents (11-18 yrs) |

| Daily sub-cutaneous injection |

| Weekly sub-cutaneous injection |

| Oral formulations (Pipeline) |

| Hospitals |

| Specialty Endocrine Clinics |

| Home-care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy Type | Branded rhGH | |

| Biosimilar rhGH | ||

| Long-acting GH analogs | ||

| GH secretagogues (oral, pipeline) | ||

| By Age Group | Pre-pubertal Children (?10 yrs) | |

| Pubertal Adolescents (11-18 yrs) | ||

| By Route of Administration | Daily sub-cutaneous injection | |

| Weekly sub-cutaneous injection | ||

| Oral formulations (Pipeline) | ||

| By End User | Hospitals | |

| Specialty Endocrine Clinics | ||

| Home-care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Idiopathic Short Stature market in 2026 and what is its growth outlook?

The Idiopathic Short Stature market size was USD 1.87 billion in 2026 and is projected to reach USD 2.80 billion by 2031, expanding at an 8.34% CAGR according to Mordor Intelligence.

Which therapy type holds the largest share of spending?

Branded recombinant human growth hormone dominated with a 62.20% share in 2025, ahead of biosimilars and long-acting analogs, as reported by Mordor Intelligence.

What segment is growing the fastest?

Long-acting growth hormone analogs are forecast to grow at 9.32% CAGR through 2031, outpacing all other segments.

Which region will lead growth to 2031?

Asia-Pacific is expected to post the highest regional CAGR at 9.33% on the back of China's reimbursement expansion and local biosimilar launches.

How significant is the adherence benefit of weekly injections?

Missing a single weekly dose equals 52 lost treatment days per year, whereas skipping one daily shot weekly translates to the same loss; shifting to once-weekly dosing therefore minimizes cumulative missed-dose days and improves growth outcomes.

Who are the main competitors in long-acting products?

Novo Nordisk, Ascendis Pharma, and Pfizer head the category, with newcomers such as LG Chem and JCR Pharmaceuticals advancing pipeline candidates.

Page last updated on: