Hypersensitivity Pneumonitis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

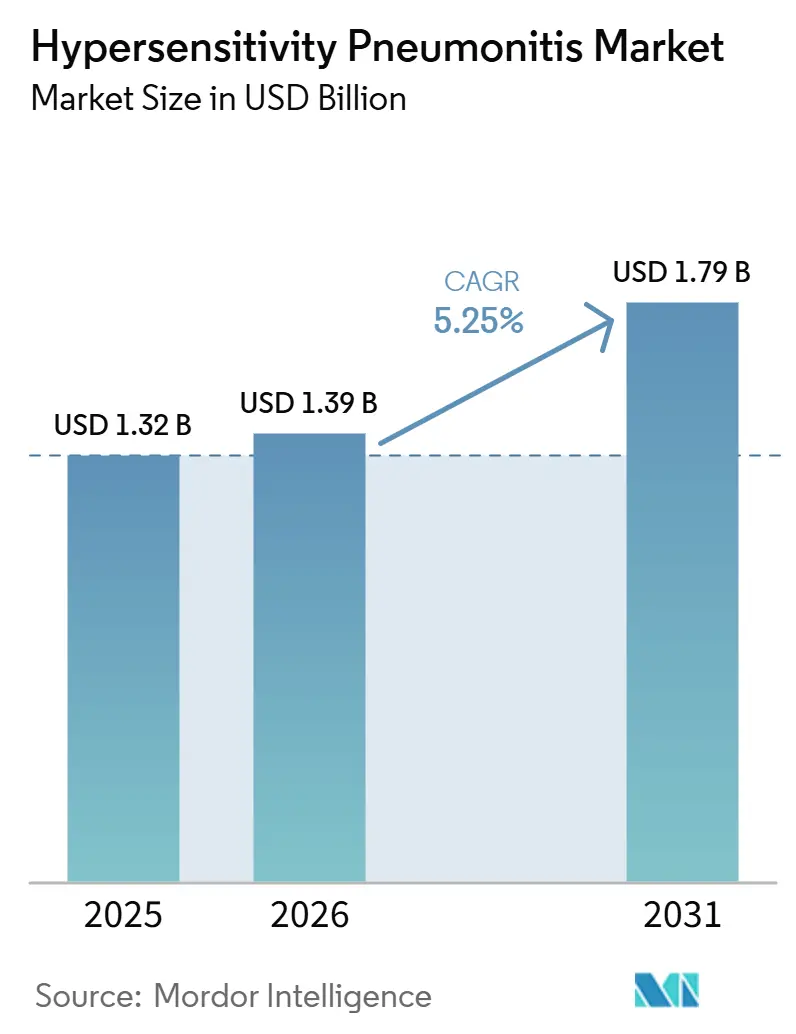

| Market Size (2026) | USD 1.39 Billion |

| Market Size (2031) | USD 1.79 Billion |

| Growth Rate (2026 - 2031) | 5.25% CAGR |

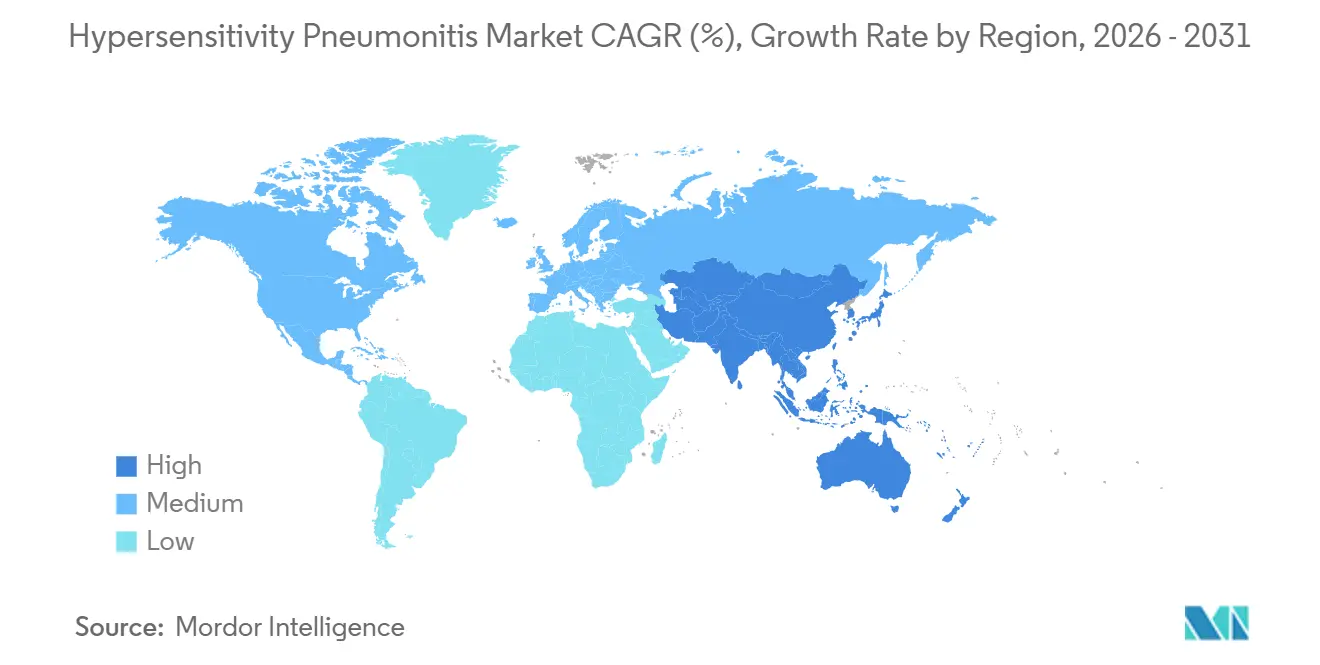

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

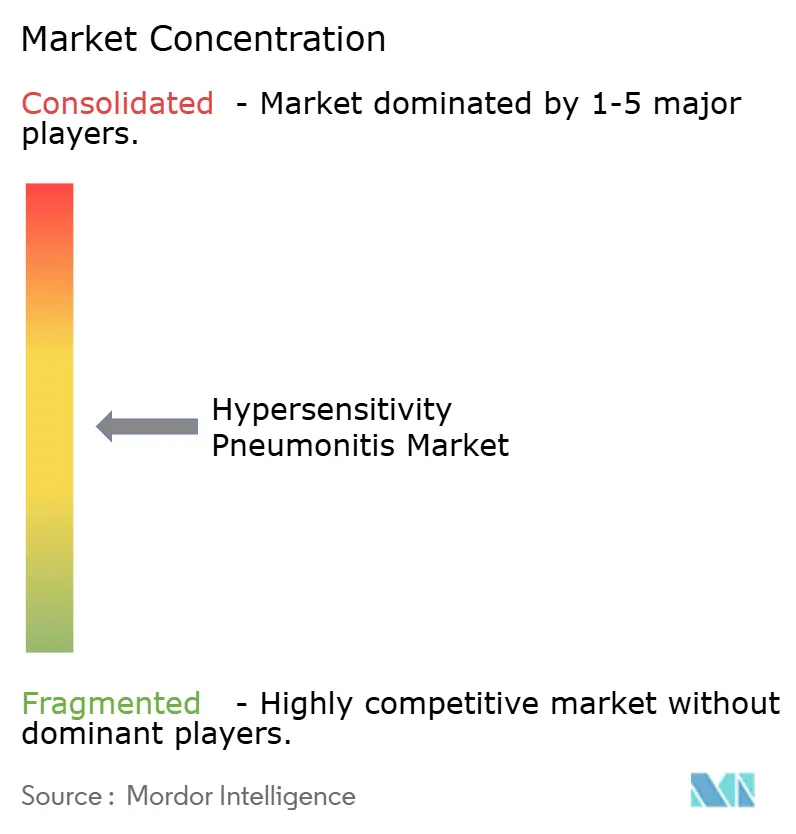

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hypersensitivity Pneumonitis Market Analysis by Mordor Intelligence

The Hypersensitivity Pneumonitis Market size was valued at USD 1.32 billion in 2025 and is estimated to grow from USD 1.39 billion in 2026 to reach USD 1.79 billion by 2031, at a CAGR of 5.25% during the forecast period (2026-2031).

Clearer differentiation between fibrotic and non-fibrotic disease under ATS, JRS, and ALAT diagnostic practices is supporting growth in the hypersensitivity pneumonitis market by improving patient identification and treatment decisions. The market is also benefiting from wider antifibrotic therapy use in progressive pulmonary fibrosis, with hypersensitivity pneumonitis-related fibrosis now included in treatment pathways across major markets. Structured surveillance across farming, bird exposure, humidifier use, and indoor mold settings is expanding formal diagnosis and the treated population. However, weak antigen identification rates, uneven reimbursement, and the lack of a single diagnostic gold standard continue to slow the conversion of clinical demand into treatment revenue.

Key Report Takeaways

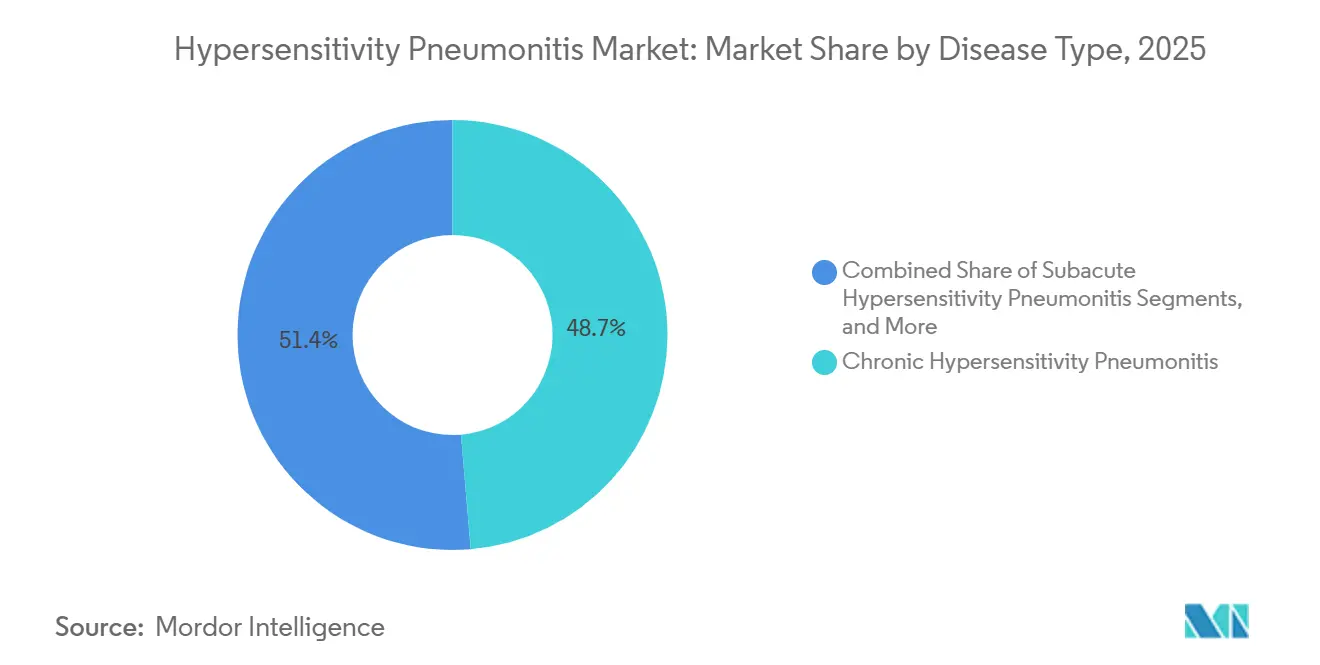

- By disease type, chronic hypersensitivity pneumonitis led with 48.65% share in 2025, while acute hypersensitivity pneumonitis is projected to expand at a 6.93% CAGR through 2031.

- By diagnosis, imaging held 57.23% of the hypersensitivity pneumonitis market size in 2025, while laboratory testing is projected to grow at an 8.67% CAGR through 2031.

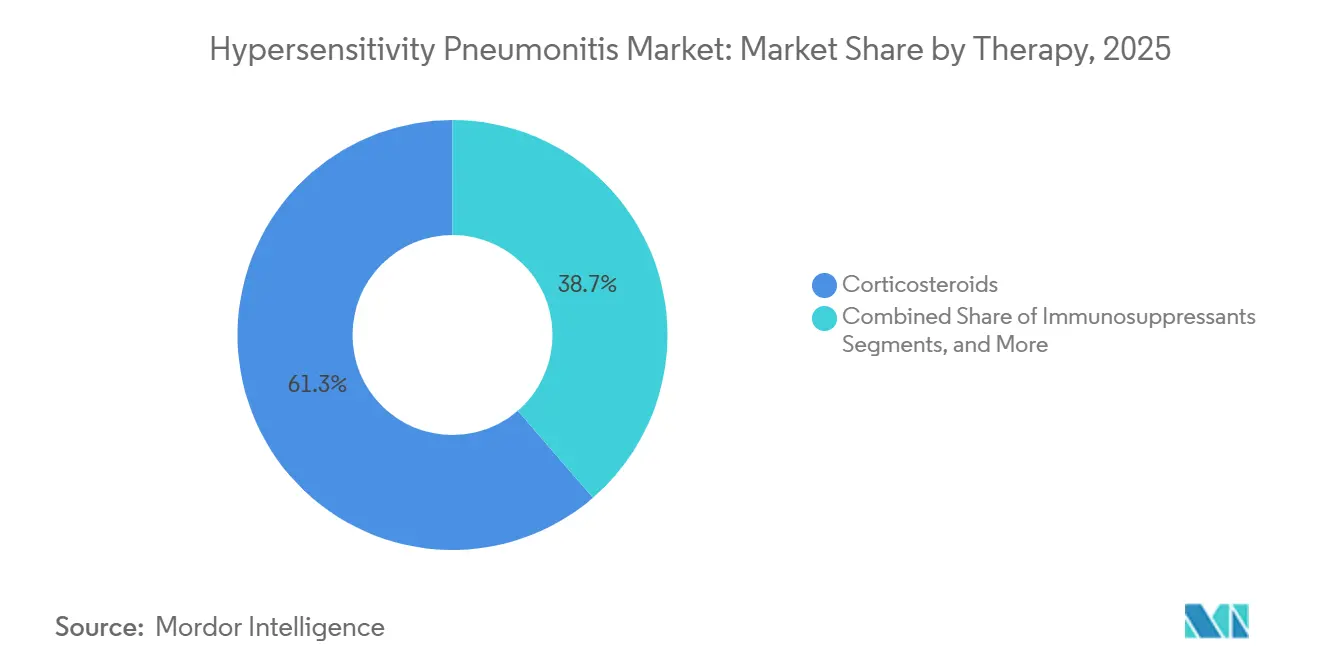

- By therapy, corticosteroids accounted for 61.34% share in 2025, while antifibrotics are expected to advance at an 8.35% CAGR through 2031.

- By route of administration, oral therapies held 62.88% share in 2025, while injectables are projected to grow at a 7.78% CAGR through 2031.

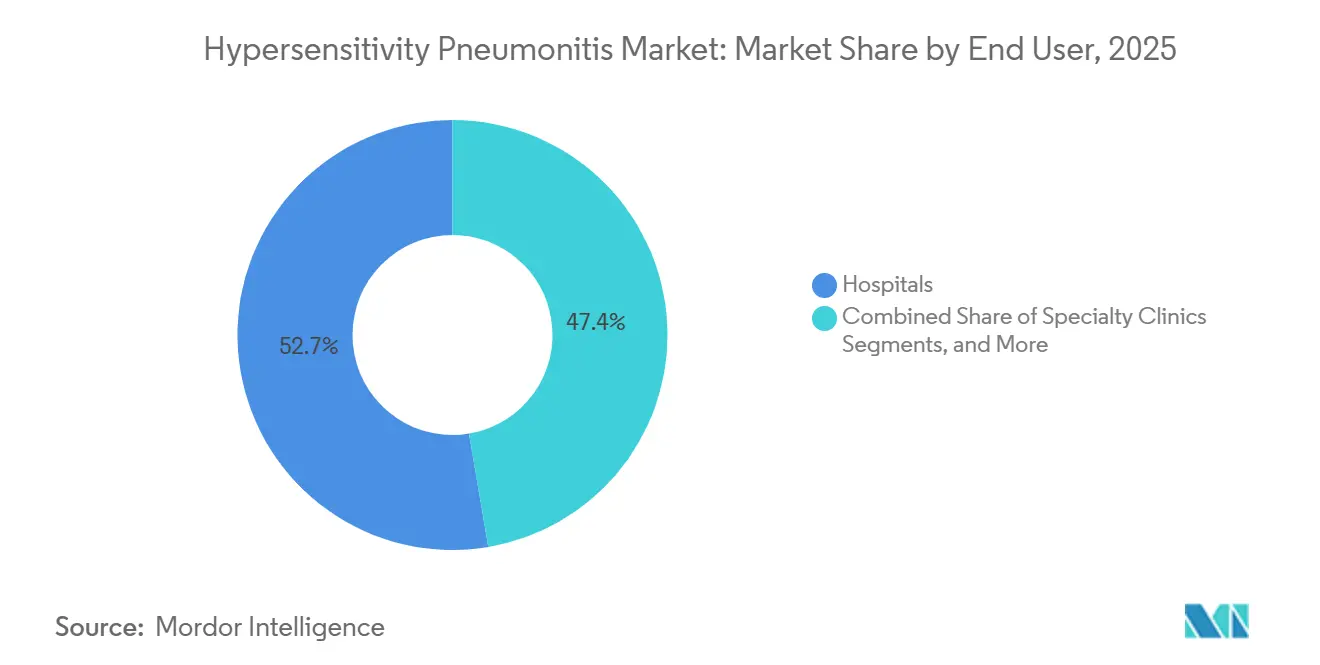

- By end user, hospitals captured 52.65% share in 2025, while specialty clinics are projected to record the highest CAGR of 8.76% through 2031.

- By geography, North America held 41.56% of the hypersensitivity pneumonitis market share in 2025, while Asia-Pacific is projected to expand at a 9.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hypersensitivity Pneumonitis Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Fibrotic hypersensitivity pneumonitis expands long-term treatment need | +1.2% | Global, strongest in North America and Asia-Pacific | Long term (≥ 4 years) |

| Progressive fibrosing ILD treatment spillover broadens the market | +1.0% | North America and Europe primary, Asia-Pacific secondary | Medium term (2-4 years) |

| High diagnostic uncertainty sustains multidisciplinary decision-making | +0.8% | Global, elevated in North America and Europe | Medium term (2-4 years) |

| Occupational surveillance in farming and bird-related settings | +0.6% | Europe, North America, and Asia-Pacific, with spillover to South America | Medium term (2-4 years) |

| Indoor mold, humidifier, and HVAC exposure screening | +0.5% | Asia-Pacific core, especially Japan and China, with relevance in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fibrotic Hypersensitivity Pneumonitis Expands Long-Term Treatment Need

Fibrotic hypersensitivity pneumonitis is expanding long-term treatment need in the hypersensitivity pneumonitis market, as clinicians now manage it as a distinct disease course with a different prognosis and treatment pathway. Hypersensitivity pneumonitis represented 26% of the INBUILD population for progressive fibrosing interstitial lung disease, highlighting its significant treatment resource requirement within the broader care setting. In Japan’s two-year nintedanib post-marketing surveillance, hypersensitivity pneumonitis accounted for 10.05% of the PF-ILD cohort, and 73.17% of these patients experienced adverse drug reactions, indicating an active and closely monitored treatment group. Germany’s 2025 S2k guideline endorsed antifibrotic therapy for progressive fibrotic hypersensitivity pneumonitis and added structured workplace exposure surveillance, raising prescribing standards in that market and potentially influencing nearby European countries.

Progressive Fibrosing ILD Treatment Spillover Broadens the Hypersensitivity Pneumonitis Market

The hypersensitivity pneumonitis market is widening because drugs initially developed for idiopathic pulmonary fibrosis are now used under the broader progressive pulmonary fibrosis label, where hypersensitivity pneumonitis is an explicit underlying diagnosis. Boehringer Ingelheim’s nerandomilast received FDA approval in December 2025 for progressive pulmonary fibrosis, marking a major step for antifibrotic therapy in this treatment space. The FIBRONEER-ILD trial showed that nerandomilast 9 mg delivered an 83 mL advantage over placebo in FVC preservation at week 52, with a consistent treatment effect in the hypersensitivity pneumonitis subgroup. The same product received a positive CHMP opinion in May 2026 and UK MHRA approval in July 2026, creating a multi-region regulatory pathway within a single year. Each new progressive pulmonary fibrosis trial that includes hypersensitivity pneumonitis as a subgroup strengthens payer arguments and supports higher-value therapy adoption across the hypersensitivity pneumonitis market.[1]Medicines & Healthcare products Regulatory Agency, “Nerandomilast (Jascayd) Approved to Treat Adult Patients with Idiopathic Pulmonary Fibrosis and Progressive Pulmonary Fibrosis,” GOV.UK, gov.uk

High Diagnostic Uncertainty Sustains Multidisciplinary Decision-Making

Diagnostic uncertainty remains high in the hypersensitivity pneumonitis market and continues to drive resource use, as patients often undergo repeat imaging, laboratory work, bronchoscopy, and specialist review before treatment begins. A 2025 management review stated that clinicians identify no causative antigen in 50% of confirmed cases, making multidisciplinary discussion central to confident diagnosis. HRCT remains critical, and a 2024 multicenter imaging study showed that the ATS, JRS, and ALAT system delivered stronger specificity than the ACCP approach in low-prevalence settings, influencing referral-center imaging review.[2] Koschel D., “Diagnosis and Treatment of Hypersensitivity Pneumonitis, S2k Guideline of the German Respiratory Society and the German Society for Allergology and Clinical Immunology,” PMC, pmc.ncbi.nlm.nih.gov A 2025 narrative review also noted that AI-based HRCT analysis and plasma proteomic panels may predict short-term fibrotic progression with high sensitivity, shifting diagnosis toward ongoing surveillance rather than a one-time event.[3]Ferrara G., “Current Concepts in the Diagnosis and Treatment of Hypersensitivity Pneumonitis, A Narrative Review,” Brazilian Journal of Pulmonology, doi.org The coexistence of several guideline systems across countries keeps referral chains active and supports commercial activity across the hypersensitivity pneumonitis market.

Occupational Surveillance in Farming and Bird-Related Settings

Occupational surveillance in agriculture, poultry handling, and avian exposure settings remains a major route through which new patients enter the hypersensitivity pneumonitis market. Data from the UK SWORD scheme for 2016-2022 estimated occupational hypersensitivity pneumonitis incidence at 1.77 cases per million workers, with fungi and molds, metalworking fluids, and avian proteins as the leading exposure groups. In Germany, statutory accident insurance bodies recorded an average of 112 suspected occupational cases per year between 1999 and 2022, but formally recognized only a limited share as occupational disease, indicating a remaining pool of unaddressed cases. A nationwide cohort analysis in Japan found that early antigen identification was associated with slower FVC decline, showing that better surveillance can translate into earlier and longer treatment episodes. A 2025 study in the Journal of Occupational Health also noted that coordinated environmental surveys involving occupational physicians, industrial hygienists, and antigen testing remain the most reliable way to detect mold-related disease early, supporting continued case finding in the hypersensitivity pneumonitis market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| No single diagnostic gold standard slows treatment initiation | -0.5% | Global | Long term (≥ 4 years) |

| Antigen identification failure limits etiology-directed therapy | -0.4% | Global, more pronounced in Asia-Pacific and South America | Long term (≥ 4 years) |

| Reimbursement pressure favors low-cost steroid regimens | -0.4% | Europe, Middle East and Africa, and South America | Medium term (2-4 years) |

| Weak prospective evidence base constrains therapy selection | -0.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

No Single Diagnostic Gold Standard Slows Treatment Initiation

The absence of a widely accepted diagnostic gold standard slows treatment initiation in the hypersensitivity pneumonitis market, as clinicians often reclassify patients across different diagnostic systems before finalizing care plans. The 2020 ATS, JRS, and ALAT criteria, the ACCP framework, and the 2025 Korean guideline differ in sensitivity and specificity, creating variation across centers, particularly in lower-resource settings. Clinicians often require bronchoscopy and bronchoalveolar lavage for high-confidence diagnosis, but these invasive procedures are not consistently available outside tertiary interstitial lung disease centers. Inconsistent serological testing, driven by non-standardized ELISA and chemiluminescence methods and geography-specific antigen panels, further extends referral timelines, delays specialist engagement, and slows movement into guideline-based treatment.

Reimbursement Pressure Favors Low-Cost Steroid Regimens

Reimbursement pressure continues to favor low-cost steroid regimens, limiting the expansion of higher-value segments of the hypersensitivity pneumonitis market despite evolving clinical practice. A 2024 pharmacoeconomic study confirmed that prednisolone and methylprednisolone remain the lowest-cost treatment options, supporting payer preference when head-to-head evidence in hypersensitivity pneumonitis remains limited. In Chile, public procurement channels continued to restrict access to antifibrotic therapy for fibrotic hypersensitivity pneumonitis, even though studies had already documented clinical benefit. Injectable biologics in development face closer scrutiny, as many payers are likely to wait for positive randomized evidence before review, creating commercial delays for premium therapies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Type: Chronic Forms Anchor Revenue While Acute Subtypes Capture Rising Case Volume

Chronic hypersensitivity pneumonitis held 48.65% of the disease-type segment in 2025, giving it the leading position in the hypersensitivity pneumonitis market. Its lead came from longer care episodes and higher use of imaging, follow-up, antigen avoidance counseling, corticosteroids, immunosuppressants, and antifibrotics. Acute and subacute disease also remained important, as they continued to generate diagnostic work and monitored follow-up despite better reversibility than chronic fibrotic cases. A 2025 PLOS ONE study showed that home mold exposure was often missed outside Japan, indicating that some subacute and chronic cases were not identified until clinicians reviewed environmental history in more detail.

Acute hypersensitivity pneumonitis is projected to grow at a 6.93% CAGR through 2031, making it the fastest-expanding disease subtype in the hypersensitivity pneumonitis market. More structured occupational screening is identifying mild and moderate acute cases that were previously treated as viral illness or short-term respiratory irritation. A nationwide Japanese study found that humidifier lung, mainly acute and subacute in phenotype, showed a rising trend during 2011-2021, with a notable increase during the COVID-19 period as indoor time and humidifier use increased. Japan’s first national prevalence estimates for fibrotic and non-fibrotic hypersensitivity pneumonitis also gave the hypersensitivity pneumonitis market a stronger base for planning case volume and treatment demand in the region.

By Diagnosis: Imaging Commands the Segment While Laboratory Biomarkers Gain Ground

Imaging accounted for 57.23% of the hypersensitivity pneumonitis market size within diagnosis in 2025, making it the largest diagnostic segment. HRCT remained the first-line tool across major guidelines because it was central to separating fibrotic from non-fibrotic patterns and narrowing the differential diagnosis. A 2025 study in Diagnostics found that expiratory HRCT, especially air trapping assessment, was one of the strongest single radiologic signals supporting a multidisciplinary diagnosis of hypersensitivity pneumonitis. Bronchoscopy and bronchoalveolar lavage remained important when imaging was inconclusive, while lung biopsy remained limited to selected cases requiring granuloma identification.

Laboratory testing is forecast to grow at an 8.67% CAGR through 2031, making it the fastest-growing diagnostic sub-segment in the hypersensitivity pneumonitis market. Growth is being driven by serum-specific IgG panels, KL-6 testing, and broader proteomic approaches that support less invasive diagnosis. A 2025 Respiratory Research study reported that a combined exosomal KL-6, CAPN2, and SP-B model achieved an AUC of 0.987 in interstitial lung disease subtyping, setting a strong benchmark for future hypersensitivity pneumonitis-focused assays. A 2026 preprint also identified two blood-based immune-metabolic endotypes in fibrotic hypersensitivity pneumonitis with different clinical trajectories, suggesting that laboratory tools will move from broad screening toward more precise disease phenotyping in the hypersensitivity pneumonitis market.

By Therapy: Corticosteroids Hold the Base While Antifibrotics Expand the Ceiling

Corticosteroids held 61.34% share of the therapy segment in 2025, keeping them at the center of the hypersensitivity pneumonitis market. Their position reflected long-established first-line use, wide generic availability, and continued use across non-fibrotic forms of disease. Immunosuppressants such as mycophenolate mofetil, azathioprine, and rituximab followed steroids and were being used more often in moderate and severe fibrotic cases, especially when clinicians needed steroid-sparing options. Supportive care, including oxygen therapy, pulmonary rehabilitation, and transplantation workup, remained important but was concentrated in advanced hospital-based care settings.

Antifibrotics are projected to grow at an 8.35% CAGR through 2031, making them the fastest-growing therapy class in the hypersensitivity pneumonitis market. This rise follows the December 2025 FDA approval of nerandomilast for progressive pulmonary fibrosis and the continued use of nintedanib in progressive fibrotic hypersensitivity pneumonitis. An ACR 2025 subgroup analysis showed that nerandomilast slowed FVC decline consistently in the autoimmune-ILD and hypersensitivity pneumonitis populations, strengthening confidence in disease-specific use.

By Route of Administration: Oral Therapy Leads While Injectables Build a Niche

Oral therapies held 62.88% share in 2025, giving this route the largest position in the hypersensitivity pneumonitis market. This lead reflected the dominance of oral corticosteroids and the oral formulations of nintedanib and nerandomilast in routine practice. The 2024 FDA label update for OFEV reaffirmed its use across chronic fibrosing interstitial lung diseases with a progressive phenotype, supporting oral antifibrotic uptake in eligible hypersensitivity pneumonitis patients. Oral immunosuppressants such as mycophenolate mofetil and azathioprine added further volume because clinicians used them as steroid-sparing agents in fibrotic disease.

Injectables are forecast to grow at a 7.78% CAGR through 2031, making them the fastest-growing route in the hypersensitivity pneumonitis market. This growth is tied to biologic use in refractory populations where standard antigen avoidance and immunosuppressive approaches do not deliver stable disease control. A phase 2 study of intravenous rituximab in treatment-refractory hypersensitivity pneumonitis reported FVC stabilization at six months, providing the first peer-reviewed real-world efficacy signal for a biologic in this setting.

By End User: Hospitals Lead Complex Care While Specialty Clinics Gain Momentum

Hospitals held 52.65% share in 2025, keeping them as the largest end-user segment in the hypersensitivity pneumonitis market. Their role was strongest in HRCT imaging, bronchoscopy, bronchoalveolar lavage, acute exacerbation management, and advanced transplantation workup for progressive fibrotic disease. Large academic centers with dedicated interstitial lung disease programs continued to generate the highest-value treatment episodes by combining imaging, serology, and multidrug management in one setting. Diagnostic laboratories and academic institutes also contributed a growing part of the value chain as serology and biomarker development increasingly moved outside the hospital floor.

Specialty clinics are projected to grow at an 8.76% CAGR through 2031, making them the fastest-growing end-user category in the hypersensitivity pneumonitis market. These clinics are taking a larger share of chronic and stable fibrotic cases that need pulmonary function monitoring, antifibrotic management, and periodic imaging without full hospital admission. A nationwide South Korean study found that newly incident hypersensitivity pneumonitis cases had a mean age of 52 years and were distributed almost equally by sex, supporting a long-term outpatient specialist care model. This shift is important because it turns each stable patient into a longer-duration follow-up opportunity for the hypersensitivity pneumonitis market.

Geography Analysis

North America held a 41.56% share in 2025, making it the largest regional block in the hypersensitivity pneumonitis market. The region benefited from strong interstitial lung disease infrastructure, high specialist access, and reimbursement pathways that supported advanced therapies more effectively than many public systems. The United States remained the largest national market in the region, with reported incidence ranging from 1.28 to 1.94 new cases per 100,000 persons annually. In addition, 50% of U.S. cases still had an unidentified antigen, supporting repeat referrals, imaging, and specialist reviews. Nerandomilast’s U.S. approval in December 2025 also positioned North America at the forefront of the antifibrotic shift in the hypersensitivity pneumonitis market.

Europe formed the second-largest regional cluster in the hypersensitivity pneumonitis market, led by Germany, the United Kingdom, and France. Germany’s S2k guideline in January 2025 formalized antifibrotic use in progressive fibrotic hypersensitivity pneumonitis and reinforced workplace exposure surveillance, which may influence prescribing standards across nearby countries. In the United Kingdom, MHRA approval for nerandomilast in July 2026 created a formal treatment path for idiopathic pulmonary fibrosis and progressive pulmonary fibrosis, including hypersensitivity pneumonitis-related fibrosis. Spain’s REGINHA registry also helped define local outcomes, supporting prescribing practice and later formulary negotiations.

Asia-Pacific is forecast to grow at a 9.56% CAGR through 2031, making it the fastest-growing geography in the hypersensitivity pneumonitis market. Japan remains a key driver, as its first national epidemiological survey estimated fibrotic hypersensitivity pneumonitis prevalence at 6.3 per 100,000 and non-fibrotic prevalence at 3.6 per 100,000, with notable southern clustering linked to mold and bird exposure. Japan’s 2026 post-marketing surveillance results also confirmed real-world nintedanib use in progressive fibrosing disease programs that included hypersensitivity pneumonitis. South Korea reported incidence rates of 1.14 to 2.16 per 100,000 persons between 2011 and 2020, and its 2025 guideline added conditional support for antifibrotics in fibrotic disease. The Middle East and Africa and South America will remain longer-term opportunities, as specialist access, reimbursement depth, and occupational monitoring remain uneven across many countries.

Competitive Landscape

The hypersensitivity pneumonitis market is moderately concentrated and shaped by two linked groups: pharmaceutical companies on the therapy side and imaging and laboratory suppliers on the diagnostic side. Boehringer Ingelheim held the clearest strategic position, as nerandomilast represented the only new-mechanism therapy in this space with a recent multi-region regulatory pathway across the United States, Europe, and the United Kingdom. This sequence shifted the market away from a therapy mix led mainly by generic steroids and toward a more differentiated antifibrotic segment. Clinical evidence in progressive pulmonary fibrosis further supported the company’s position, as it directly related to hypersensitivity pneumonitis-associated fibrosis.

Competition also built around refractory disease, where biologics may drive the next wave of treatment change in the hypersensitivity pneumonitis market. A 2025 Scientific Reports study indicated that intravenous rituximab stabilized FVC in treatment-refractory hypersensitivity pneumonitis, giving larger immunology-focused companies a clearer development signal. aTyr Pharma also remained active in adjacent granulomatous interstitial lung disease, with topline Phase 3 efzofitimod results in September 2025 and an IND filing in June 2026 for a new Phase 3 study in pulmonary sarcoidosis. Although these programs did not represent hypersensitivity pneumonitis approvals, stakeholders continued to monitor them due to overlap with granulomatous and restrictive lung disease management.

On the diagnostic side, Siemens Healthineers, Thermo Fisher Scientific, Abbott Laboratories, and Sysmex Corporation held important positions across HRCT, immunoassay, and bronchoalveolar lavage testing workflows in the hypersensitivity pneumonitis market. Imaging remained commercially central because HRCT was required early in the workup and continued to support fibrotic versus non-fibrotic classification across most care pathways. Laboratory platforms gained importance as serum IgG testing, KL-6 measurement, and future proteomic panels became more relevant for repeat assessment. As a result, competition gradually shifted from stand-alone diagnosis toward disease monitoring and refined phenotyping.

Hypersensitivity Pneumonitis Industry Leaders

Boehringer Ingelheim International GmbH

F. Hoffmann-La Roche Ltd.

AstraZeneca plc

Pfizer Inc.

Novartis AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Boehringer Ingelheim’s nerandomilast (Jascayd) received UK MHRA approval for IPF and PPF, including HP-related fibrosis, making it available to NHS patients.

- May 2026: The EU CHMP adopted a positive opinion for nerandomilast (Jascayd) in IPF and PPF, including progressive fibrosing interstitial lung diseases such as hypersensitivity pneumonitis.

- December 2025: The FDA approved Boehringer Ingelheim’s nerandomilast (JASCAYD) for progressive pulmonary fibrosis in adults, including hypersensitivity pneumonitis.

Global Hypersensitivity Pneumonitis Market Report Scope

As per the scope of the report, hypersensitivity pneumonitis (HP) is an immune system disorder where the lungs become inflamed after repeated inhalation of environmental allergens, such as molds, bacteria, or animal proteins. Also known as extrinsic allergic alveolitis, it can cause flu-like symptoms or, over time, lead to irreversible lung scarring (pulmonary fibrosis).

The hypersensitivity pneumonitis market is segmented by disease type, diagnosis, therapy, route of administration, end user, and geography. By disease type, the market is segmented into acute hypersensitivity pneumonitis, subacute hypersensitivity pneumonitis, and chronic hypersensitivity pneumonitis. By diagnosis, the market includes imaging, laboratory testing, bronchoscopy and bronchoalveolar lavage, and lung biopsy. By therapy, the market is segmented into corticosteroids, immunosuppressants, antifibrotics, and supportive care. By route of administration, the market is categorized into oral, injectable, and inhaled. By end user, the market is segmented into hospitals, specialty clinics, diagnostic laboratories, and academic and research institutes. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Acute Hypersensitivity Pneumonitis |

| Subacute Hypersensitivity Pneumonitis |

| Chronic Hypersensitivity Pneumonitis |

| Imaging |

| Laboratory Testing |

| Bronchoscopy and Bronchoalveolar Lavage |

| Lung Biopsy |

| Corticosteroids |

| Immunosuppressants |

| Antifibrotics |

| Supportive Care |

| Oral |

| Injectable |

| Inhaled |

| Hospitals |

| Specialty Clinics |

| Diagnostic Laboratories |

| Academic and Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disease Type | Acute Hypersensitivity Pneumonitis | |

| Subacute Hypersensitivity Pneumonitis | ||

| Chronic Hypersensitivity Pneumonitis | ||

| By Diagnosis | Imaging | |

| Laboratory Testing | ||

| Bronchoscopy and Bronchoalveolar Lavage | ||

| Lung Biopsy | ||

| By Therapy | Corticosteroids | |

| Immunosuppressants | ||

| Antifibrotics | ||

| Supportive Care | ||

| By Route of Administration | Oral | |

| Injectable | ||

| Inhaled | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Diagnostic Laboratories | ||

| Academic and Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value of hypersensitivity pneumonitis worldwide?

The hypersensitivity pneumonitis market size is USD 1.39 million in 2026 and is forecast to reach USD 1.79 million by 2031 at a 5.25% CAGR.

Which region leads current demand for hypersensitivity pneumonitis treatment?

North America led with 41.56% share in 2025, supported by stronger interstitial lung disease infrastructure, specialist access, and broader treatment reimbursement.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is projected to grow at a 9.56% CAGR through 2031, driven by stronger case detection, national epidemiology data, and rising antifibrotic adoption in countries such as Japan and South Korea.

Which therapy category is expanding the quickest?

Antifibrotics are the fastest-growing therapy class with an 8.35% CAGR, supported by nerandomilast approval in progressive pulmonary fibrosis and continued nintedanib use in progressive fibrotic disease.

Why do hospitals still account for the largest end-user share?

Hospitals held 52.65% share in 2025 because they remain central for HRCT, bronchoscopy, bronchoalveolar lavage, acute exacerbation care, and transplantation workup.

What is the main challenge slowing wider treatment adoption?

The biggest barriers are the absence of one diagnostic gold standard, frequent failure to identify the causative antigen, and reimbursement systems that still favor low-cost corticosteroids over newer therapies.

Page last updated on: