Hydrogel Dressing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.95 Billion |

| Market Size (2031) | USD 1.27 Billion |

| Growth Rate (2026 - 2031) | 5.98% CAGR |

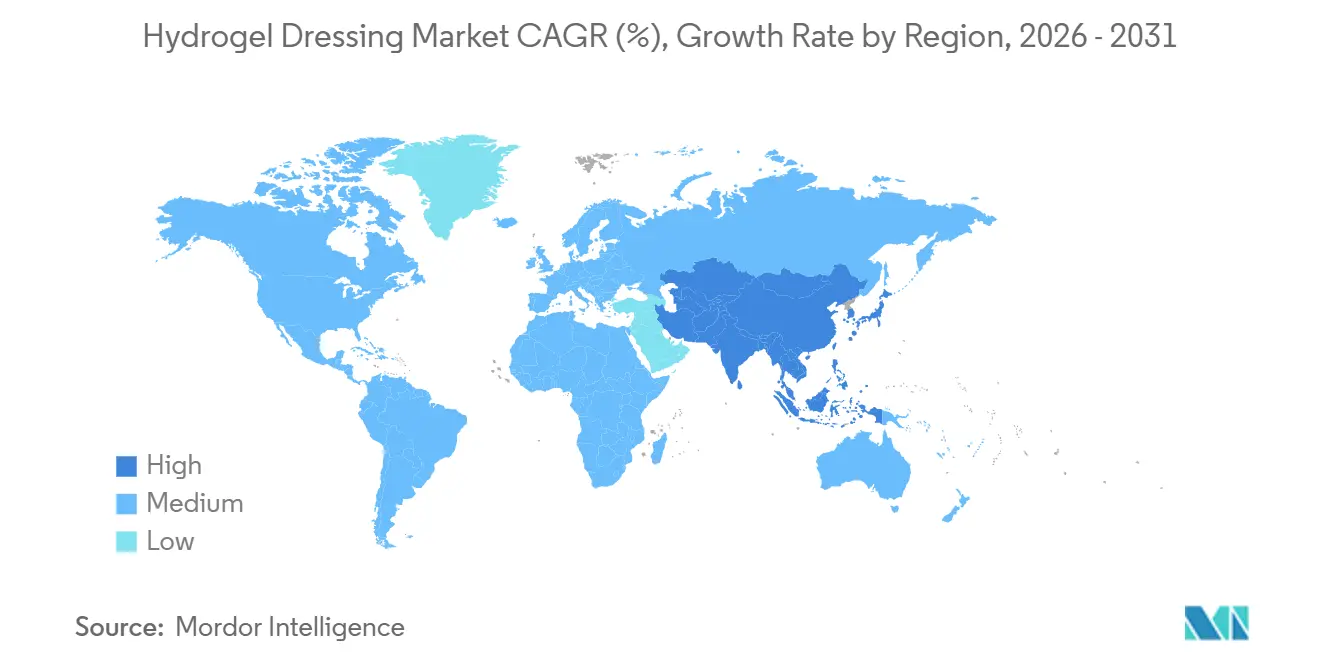

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

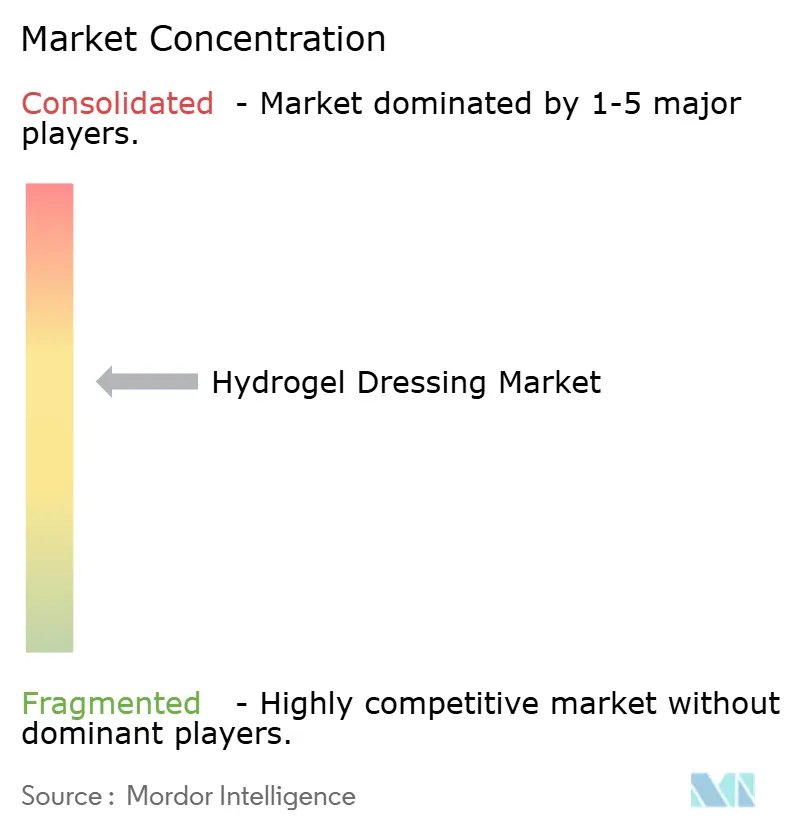

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hydrogel Dressing Market Analysis by Mordor Intelligence

The Hydrogel Dressing Market size is expected to increase from USD 0.89 billion in 2025 to USD 0.95 billion in 2026 and reach USD 1.27 billion by 2031, growing at a CAGR of 5.98% over 2026-2031.

Wider use of evidence-based dressings, tighter antimicrobial-resistance rules, and payment models that reward shorter nursing time are steering procurement away from gauze toward advanced products, including sensor-ready formats. Hospitals now bundle dressing costs into episode payments, so purchasers favor options that reduce readmissions and nurse visits[1]Centers for Medicare & Medicaid Services, “Physician Fee Schedule,” CMS.gov . Manufacturers are also reallocating R&D toward hybrid polymers that balance mechanical strength with bioactivity, while navigating the proposed FDA reclassification that would move antimicrobial hydrogels from Class I to Class III devices. This shift raises the bar for clinical evidence. North America leads current revenue due to reimbursement depth, yet Asia-Pacific is the foremost growth frontier as China and India scale surgical capacity and diabetic prevalence climbs. Strategic exits such as Smith & Nephew’s April 2024 sale of its Advanced Wound Bioactives unit signal that top players are concentrating on higher-margin negative-pressure systems while leaving room for data-enabled hydrogel challengers.

Key Report Takeaways

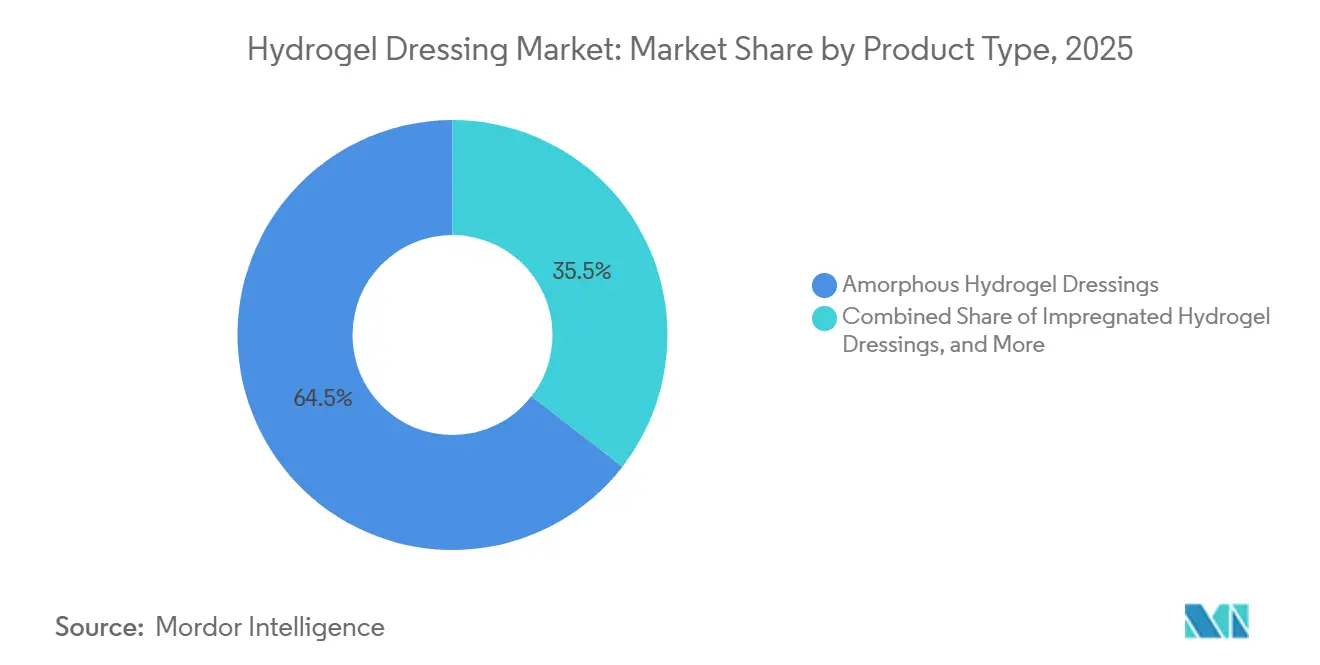

- By product type, amorphous formulations led with 64.55% of the hydrogel dressing market share in 2025, whereas sheet formats are set to expand at an 8.25% CAGR through 2031.

- By raw material, synthetic polymers accounted for 60.53% of the hydrogel dressing market size in 2025, while hybrid compositions show the fastest 8.85% CAGR to 2031.

- By application, chronic wounds captured 61.63% share of the hydrogel dressing market size in 2025, yet acute wounds are advancing at an 8.12% CAGR through 2031.

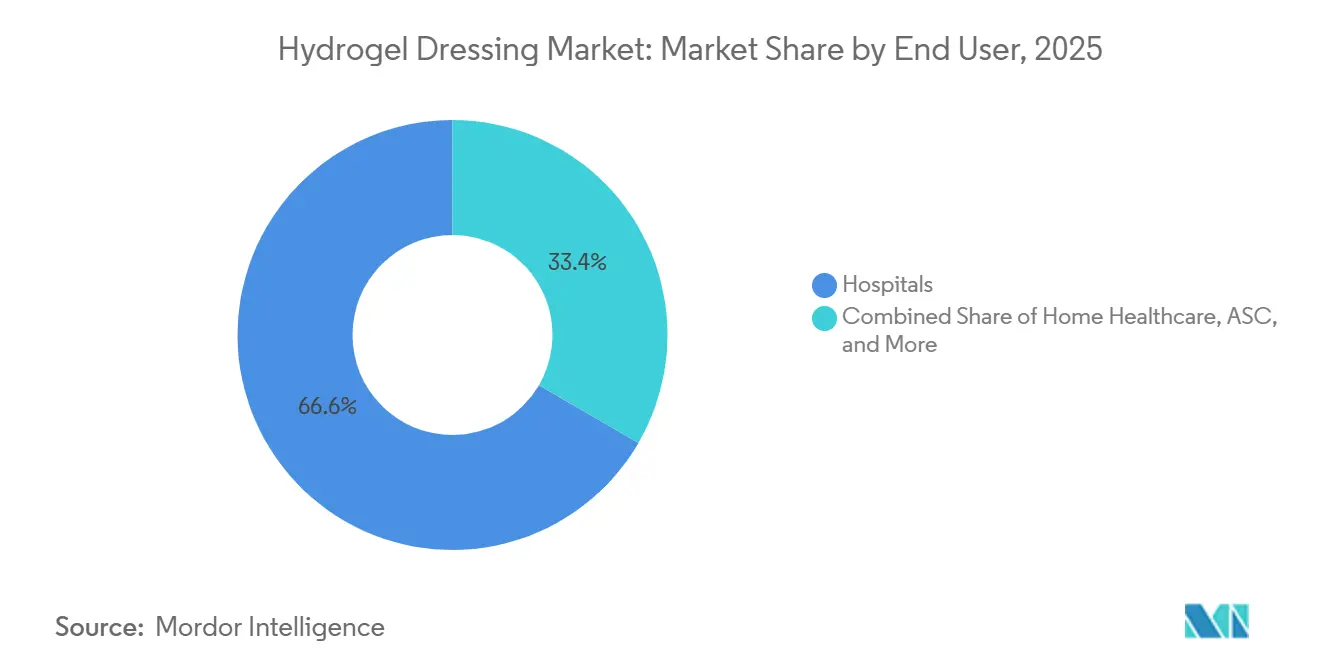

- By end user, hospitals accounted for 66.63% of revenue share in 2025, whereas home healthcare is growing at an 8.27% CAGR through 2031.

- By geography, North America contributed 40.13% of the hydrogel dressing market size in 2025; Asia-Pacific is progressing at a 9.51% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hydrogel Dressing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Chronic Wounds | +1.2% | Global, highest in North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Shift From Gauze to Evidence-Based Dressings | +1.0% | North America and Western Europe lead; Asia-Pacific and Latin America follow | Medium term (2-4 years) |

| Innovation in Antimicrobial & Smart Hydrogels | +0.9% | North America, Europe, East Asia | Medium term (2-4 years) |

| Growing Surgical & Burn Caseloads | +0.8% | Global, rapid growth in India, China, Brazil | Short term (≤ 2 years) |

| Outpatient Payment Reforms | +0.7% | United States, Germany, United Kingdom, Australia | Short term (≤ 2 years) |

| Sensor-Integrated Tele-Wound Dressings | +0.6% | North America and select European markets; pilots in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Wounds

Diabetic foot ulcers, pressure ulcers, and venous leg ulcers now affect more than 40 million people worldwide, and United States treatment costs exceed USD 50 billion annually[2]Centers for Disease Control and Prevention, “National Diabetes Statistics Report,” cdc.gov. The International Working Group on the Diabetic Foot noted in 2024 that 1-year mortality after a diabetic foot ulcer diagnosis matches some cancers. Yet, fewer than half of high-risk patients receive moisture-balanced dressings[3]International Working Group on the Diabetic Foot, “IWGDF Guidelines,” iwgdfguidelines.org. Hydrogels maintain moist environments that accelerate autolytic debridement and lower nursing frequency from daily changes to three-day intervals. Skilled-nursing facilities experience labor reductions when hydrogel replaces gauze, supporting its adoption in capitated payment systems. These factors collectively raise baseline demand in the hydrogel dressing market

Shift from Gauze to Evidence-Based Advanced Dressings

Guidelines from NICE and the Wound Healing Society emphasize moist healing and faster epithelialization, but cost sensitivity slows uptake in some hospitals[4]National Institute for Health and Care Excellence, “Pressure Ulcers: Prevention and Management (CG179),” nice.org.uk. Bundled payments fold dressing costs into procedure codes, prompting procurement to favor options that shorten stays and cut readmissions. Hydrogels prove particularly valuable in low-to-moderate exudate wounds, though high-exudate ulcers still require absorbent foams. These reimbursement shifts add momentum to the hydrogel dressing market across developed regions.

Innovation in Antimicrobial & Stimuli-Responsive Hydrogels

University labs have moved color-changing and pH-responsive hydrogels from prototypes to pilot deployments. Tufts researchers showed a silk-fibroin variant that detects Pseudomonas within 24 hours. FDA combination-product rules increase approval costs, pushing larger firms to fund evidence packages while leaving opportunities for start-ups that design drug-free sensor variants. The resulting pipeline ensures a steady flow of next-generation offerings that can lift average selling prices in the hydrogel dressing market.

Growing Surgical & Burn Caseloads

Elective surgeries rose 7.3% year-on-year through mid-2025 as pandemic backlogs cleared. Burn injuries, about 11 million annually, disproportionately drive hydrogel demand because non-adherent, cooling sheets relieve pain and prevent tissue trauma. Sheet hydrogels can reduce pain scores by roughly 2 points on a 10-point scale, a compelling benefit for trauma centers. Rising caseloads in India and Brazil further underpin market volumes for hydrogel dressings.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Unit and Manufacturing Cost | –0.8% | Global; most acute in India, Southeast Asia, Latin America | Medium term (2-4 years) |

| Limited Absorption for Heavy-Exudate Wounds | –0.6% | Global where venous ulcers and high-drain wounds dominate | Short term (≤ 2 years) |

| Supply-Chain Volatility for Specialty Polymers | –0.5% | China and petrochemical hubs worldwide | Short term (≤ 2 years) |

| Extra Regulatory Hurdles for Combo Products | –0.4% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Unit and Manufacturing Cost Versus Conventional Dressings

Hydrogels retail at USD 3–15 per unit, far above the USD 0.10–0.50 for gauze, causing sticker shock in low-income settings. Specialty polymers like medical-grade hyaluronic acid cost up to USD 500 per kilogram, making materials the most significant expense driver. Sterile packaging adds another USD 0.50–2.00 per unit, and these costs compound across high-volume chronic-wound regimens. A 2024 Journal of Wound Care study still showed an 18% lower total episode cost than gauze, because fewer changes and infections offset the material premium. Yet price remains a barrier in India and Southeast Asia, limiting penetration of the hydrogel dressing market outside urban hospitals.

Limited Absorption for Heavy-Exudate Wounds

Hydrogels donate moisture rather than absorb fluid, making them unsuitable for wounds producing more than about 10 mL of drainage daily. A 2025 Wound Repair and Regeneration review excluded hydrogels from venous leg ulcer comparisons because absorption capacity was insufficient. Clinicians instead select hydrofiber foams that achieve 65–72% healing rates. Hybrid designs that layer hydrogels over absorbent cores are emerging, but reimbursement codes lag, complicating the narrative of the hydrogel dressing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Amorphous Versatility And Sheet Momentum

Amorphous formulations held 64.55% of the hydrogel dressing market share in 2025, reflecting their ability to fill irregular cavities and tunnel wounds. Sheet variants, however, are growing at 8.25% CAGR because burn units prefer pre-formed pads that cool tissue and reduce nursing time. Amorphous gels require secondary retention, which increases labor, but they permit clinicians to pack undermined tissue with precise moisture control. Sheet hydrogels deliver a uniform thickness and adhere gently, reducing dressing changes by up to 2 per week and improving patient comfort.

Regulatory compliance is strict across formats: ISO 10993 testing adds up to USD 100,000 per formulation. The FDA cleared a sheep-collagen sheet hydrogel in 2025, confirming that novel biomaterials can pass through the 510(k) pathway when equivalence is demonstrated. Sheet hydrogels face competition from silicone foams with better exudate handling, yet remain favored where autolytic debridement is required, keeping both formats integral to the hydrogel dressing market.

By Raw Material: Synthetic Strength And Hybrid Bioactivity

Synthetic polymers accounted for 60.53% of the hydrogel dressing market in 2025, as polyethylene glycol and polyacrylamide offer reproducible mechanical properties and sterilization compatibility. Hybrid blends of synthetic backbones with bioactive chitosan or hyaluronic acid are advancing at an 8.85% CAGR. Natural components improve cell signaling and growth-factor retention, leading to faster healing in early studies. Batch variability and higher costs still constrain pure natural gels, yet hybrids mitigate these issues by keeping synthetic durability.

Supply-chain risks shape strategy. China’s dominance in hyaluronic acid exposes producers to geopolitical swings, prompting multisource procurement. ISO 13485 audits add overhead yet prevent recalls from contaminated lots. The resulting emphasis on resilience and bioactivity will likely expand hybrid revenue share within the hydrogel dressing market.

By Application: Chronic Wounds Anchor Demand While Acute Wounds Accelerate

Chronic wounds accounted for 61.63% of the hydrogel dressing market in 2025, driven by diabetic foot ulcers, pressure ulcers, and venous leg ulcers. Hydrogels excel in low-exudate diabetic wounds because they encourage autolytic debridement without painful scrubs. Acute wounds—burns and surgical sites are growing at 8.12% CAGR as elective surgeries rebound and burn centers adopt evidence-based protocols.

Trauma indications receive an indirect lift from the FDA’s expansion of RECELL spray-on skin to acute injuries, because clinicians need moisture-retentive coverings post-application. Pressure ulcer incidence dropped 25% in U.S. hospitals, tempering chronic-segment growth but not offsetting gains from diabetes prevalence. Both chronic and acute niches, therefore, remain critical to the hydrogel dressing market.

By End User: Hospital Dominance And Home Care Upswing

Hospitals retained 66.63% of revenue share in 2025, as inpatient wound-care teams and burn units followed protocolized dressing regimens. Multi-product contracts with established brands secure discounts and simplify inventory. Home healthcare, however, is expanding at 8.27% CAGR, fueled by bundled payments that penalize readmissions and by remote monitoring codes that reimburse connected dressings.

Ambulatory surgical centers and long-term care facilities add diversified demand. ASCs favor kit-packaged hydrogels that minimize the number of stock-keeping units. Long-term care homes value extended-wear sheets that reduce nurse visits from daily to every 3 to 5 days. These dynamics collectively shift volume distribution within the hydrogel dressing market without displacing hospital leadership.

Geography Analysis

North America accounted for 40.13% of the hydrogel dressing market in 2025, driven by robust reimbursement and early smart-dressing pilots. Medicare codes still cover hydrogels, yet bundled payments pass cost pressure to providers, prompting data-backed purchasing. Canada’s provincial formularies vary; Ontario funds hydrogels in home care, whereas Alberta requires prior authorization, creating uneven uptake. Mexico benefits from medical tourism and expanding social-insurance coverage, boosting imports from United States suppliers.

Europe remains sizable but governed by strict Medical Device Regulation 2017/745 processes. Germany reimburses listed dressings through the Hilfsmittelverzeichnis, while unlisted products need case approvals. The United Kingdom purchases centrally through NHS Supply Chain, and NICE’s 2024 review found insufficient evidence to prefer hydrogels, which has slowed adoption. France’s LPPR process can take up to 18 months, delaying full reimbursement. Southern Europe shows slower uptake due to tighter budgets.

Asia-Pacific posts the highest CAGR of 9.51%, driven by China, India, Japan, Australia, and South Korea. China reduced Class II approval timelines to about 12–15 months, letting domestic leaders such as Winner Medical raise exports 12.6% year-on-year. India’s Class B registration system welcomes multinationals without mandated clinical trials, while Japan’s PMDA allows Class II notifications through a Marketing Authorization Holder structure. Australia’s high per-capita wound-care spend and South Korea’s accelerating approvals make both countries attractive launch pads for premium offerings, reinforcing the hydrogel dressing market’s pivot eastward.

Gulf states import premium dressings for private hospitals serving medical tourists, yet public tenders remain gauze-heavy. South Africa’s dual public-private system creates a split market, while Brazil’s ANVISA fast-tracks low-risk devices yet budget constraints limit nationwide roll-out. Currency volatility in Argentina and price controls elsewhere keep penetration uneven, but rising diabetes rates still add incremental volumes to the hydrogel dressing market.

Competitive Landscape

The hydrogel dressing market is moderately fragmented: the top five players, Smith & Nephew, ConvaTec, Molnlycke, Solventum, and Coloplast, jointly command a sizable but not dominant share. Smith & Nephew’s USD 115 million divestiture of its Advanced Wound Bioactives arm in April 2024 reallocates resources to high-margin PICO and RENASYS GO negative-pressure systems. ConvaTec integrates its Convatec.me platform to capture outcomes data and strengthen payer negotiations. Molnlycke bought Sentry Medical for USD 160 million in February 2024 to expand drape capacity and bundle infection-prevention kits for value-analysis committees.

Emerging challengers exploit pricing gaps and digital overlays. Chinese firms Winner Medical and Zhende Medical undercut Western pricing while meeting ISO 13485 standards, accelerating export share. Integra LifeSciences’ Flowable Wound Matrix commands USD 1,507 per cubic centimeter under Medicare, demonstrating premium pricing when outcomes justify it. Sensor-focused start-ups, such as the iSAFE consortium, target telehealth budgets but must still navigate reimbursement and data-security hurdles. Regulatory headwinds, notably the FDA’s planned Class III shift for antimicrobial hydrogels, favor well-capitalized incumbents yet leave technological white space for nimble innovators within the hydrogel dressing market.

Hydrogel Dressing Industry Leaders

Solventum Corporation

Coloplast A/S

Molnlycke Health Care AB

ConvaTec Group PLC

Smith & Nephew plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: University of Bayreuth researchers reported a self-healing hydrogel that combines strength and flexibility, published in Nature Materials.

- February 2025: Canada-based Biomiq introduced PureGel, a nano-hydrogel that delivers stable hypochlorous acid for extended antimicrobial activity.

Global Hydrogel Dressing Market Report Scope

As per the report's scope, a hydrogel dressing is a type of wound dressing mainly made of water (up to 90%) embedded in a gel matrix. It provides a moist environment that promotes wound healing, soothes pain, and facilitates autolytic debridement. Hydrogel dressings are non-adherent, flexible, and cooling, making them suitable for burns, ulcers, pressure sores, and dry or necrotic wounds. They also help in absorbing small amounts of exudate while maintaining moisture balance for optimal tissue repair.

The hydrogel dressing market segmentation includes product type, raw material, application, end user, and geography. By product type, the market is segmented into amorphous hydrogel dressings, impregnated hydrogel dressings, and sheet hydrogel dressings. By raw material, the market is segmented into synthetic, natural, and semi-synthetic/hybrid hydrogels. By application, the market is segmented into chronic wounds and acute wounds. By end user, the market is segmented into hospitals, home healthcare, ambulatory surgical centers, and other end users. By geography, the global market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Amorphous Hydrogel Dressings |

| Impregnated Hydrogel Dressings |

| Sheet Hydrogel Dressings |

| Synthetic Hydrogels |

| Natural Hydrogels |

| Semi-synthetic / Hybrid Hydrogels |

| Chronic Wounds | Diabetic Foot Ulcers |

| Pressure Ulcers | |

| Venous Leg Ulcers | |

| Acute Wounds | Burns |

| Surgical & Traumatic Wounds |

| Hospitals |

| Home Healthcare |

| Ambulatory Surgical Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Amorphous Hydrogel Dressings | |

| Impregnated Hydrogel Dressings | ||

| Sheet Hydrogel Dressings | ||

| By Raw Material | Synthetic Hydrogels | |

| Natural Hydrogels | ||

| Semi-synthetic / Hybrid Hydrogels | ||

| By Application | Chronic Wounds | Diabetic Foot Ulcers |

| Pressure Ulcers | ||

| Venous Leg Ulcers | ||

| Acute Wounds | Burns | |

| Surgical & Traumatic Wounds | ||

| By End User | Hospitals | |

| Home Healthcare | ||

| Ambulatory Surgical Centers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the hydrogel dressing market?

The hydrogel dressing market size is USD 0.95 billion in 2026.

How fast is the hydrogel dressing market projected to grow?

It is forecast to expand at a 5.98% CAGR between 2026 and 2031.

Which product type is gaining the most momentum?

Sheet hydrogels are accelerating with an 8.25% CAGR through 2031.

Why is Asia-Pacific attracting attention from manufacturers?

Rising surgical volumes, diabetic prevalence, and streamlined approvals give the region a 9.51% CAGR outlook.

How are payment reforms influencing adoption patterns?

Bundled and remote-monitoring reimbursements reward dressings that reduce nurse time and readmissions, boosting smart hydrogel uptake.

Which companies currently lead sales?

Smith & Nephew, ConvaTec, Molnlycke, Solventum, and Coloplast collectively hold the largest revenue share.

Page last updated on: