Hydraulics Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

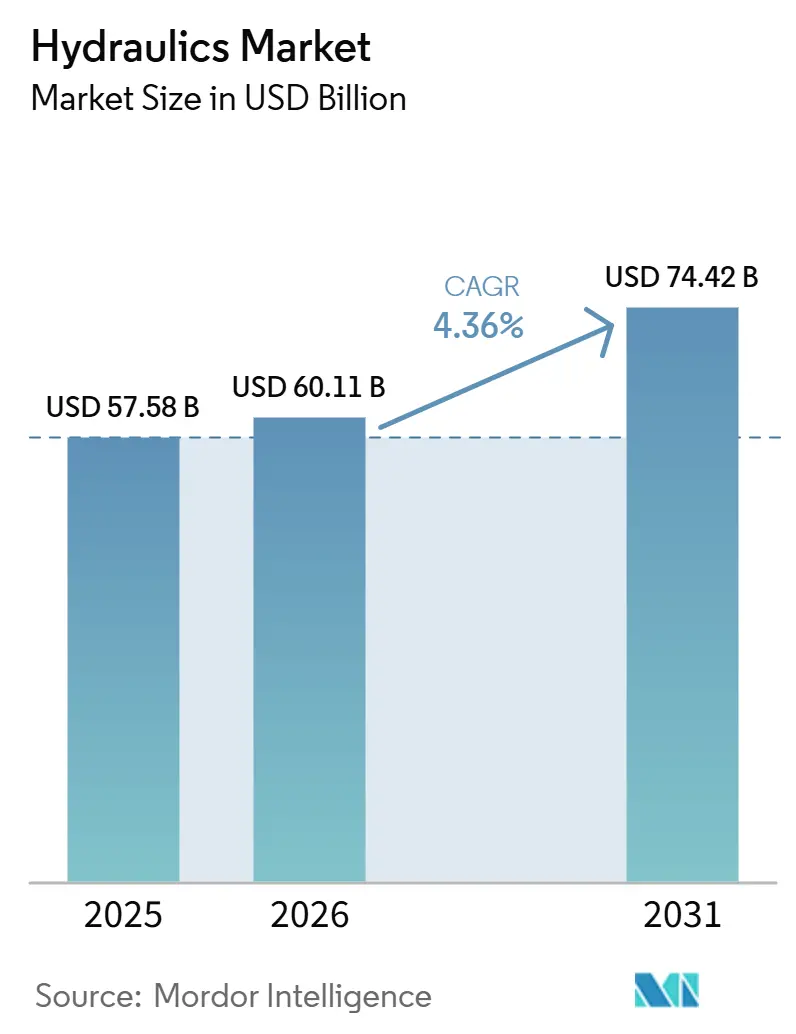

| Market Size (2026) | USD 60.11 Billion |

| Market Size (2031) | USD 74.42 Billion |

| Growth Rate (2026 - 2031) | 4.36% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hydraulics Market Analysis by Mordor Intelligence

The Hydraulics Market size is projected to expand from USD 57.58 billion in 2025 and USD 60.11 billion in 2026 to USD 74.42 billion by 2031, and is expected to register a CAGR of 4.36% between 2026 and 2031. The hydraulics market continues to benefit from demand in applications where high force density, long service life, and reliable power transmission remain more important than a complete shift to electromechanical systems. Infrastructure spending across Asia-Pacific and the Middle East, combined with replacement demand from aging mobile equipment fleets in North America and Europe, continues to support the market. Research expected in 2025 indicates that electro-hydraulic actuators can reduce energy use by up to 54% compared with conventional hydraulic systems, supporting investment in advanced hydraulic architectures rather than full substitution. The hydraulics market also continues to attract interest as digital controls, predictive maintenance tools, and sensor integration improve system efficiency and equipment uptime. Competitive pressure remains active across the market, while labor shortages and material cost pressures continue to constrain margin expansion in parts of the value chain.

Key Report Takeaways

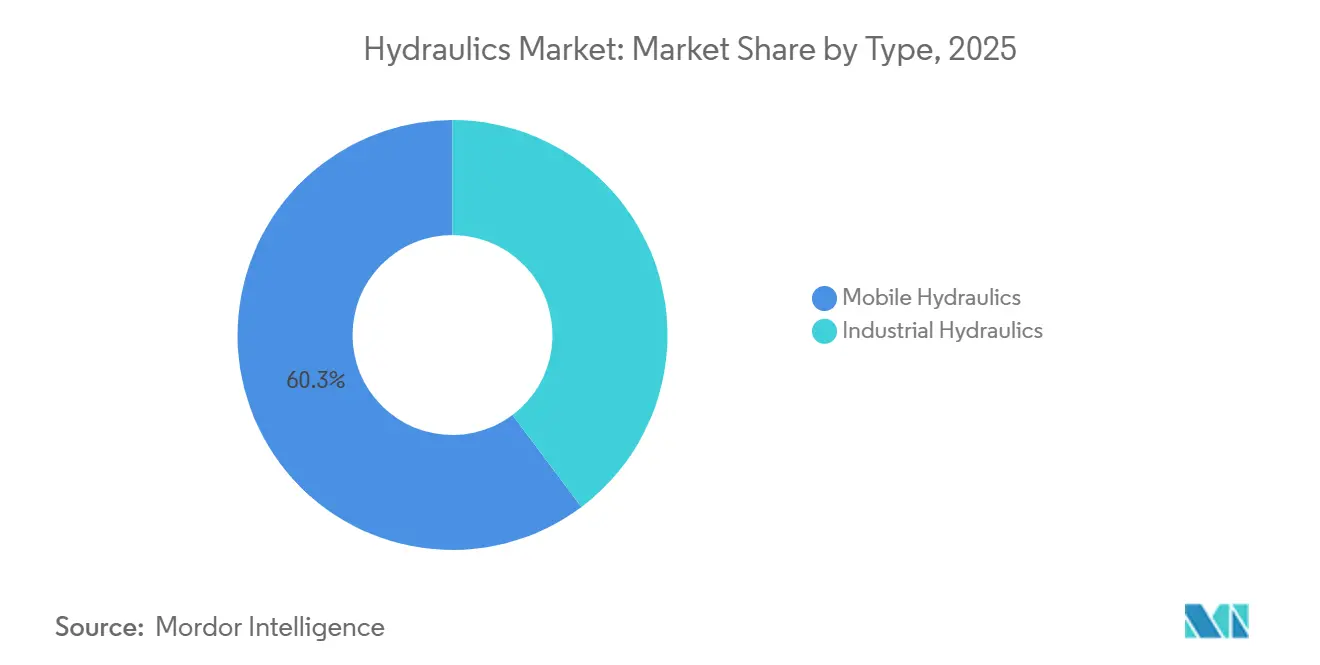

- By type, mobile hydraulics led with a 60.25% share in 2025, while industrial hydraulics is projected to expand at a 4.85% CAGR through 2031.

- By component, pumps accounted for a 25.85% share in 2025, while valves recorded the highest projected CAGR at 5.76% through 2031.

- By sensor, pressure sensors held a 30.62% share in 2025, while flow sensors are forecast to grow at a 5.33% CAGR through 2031.

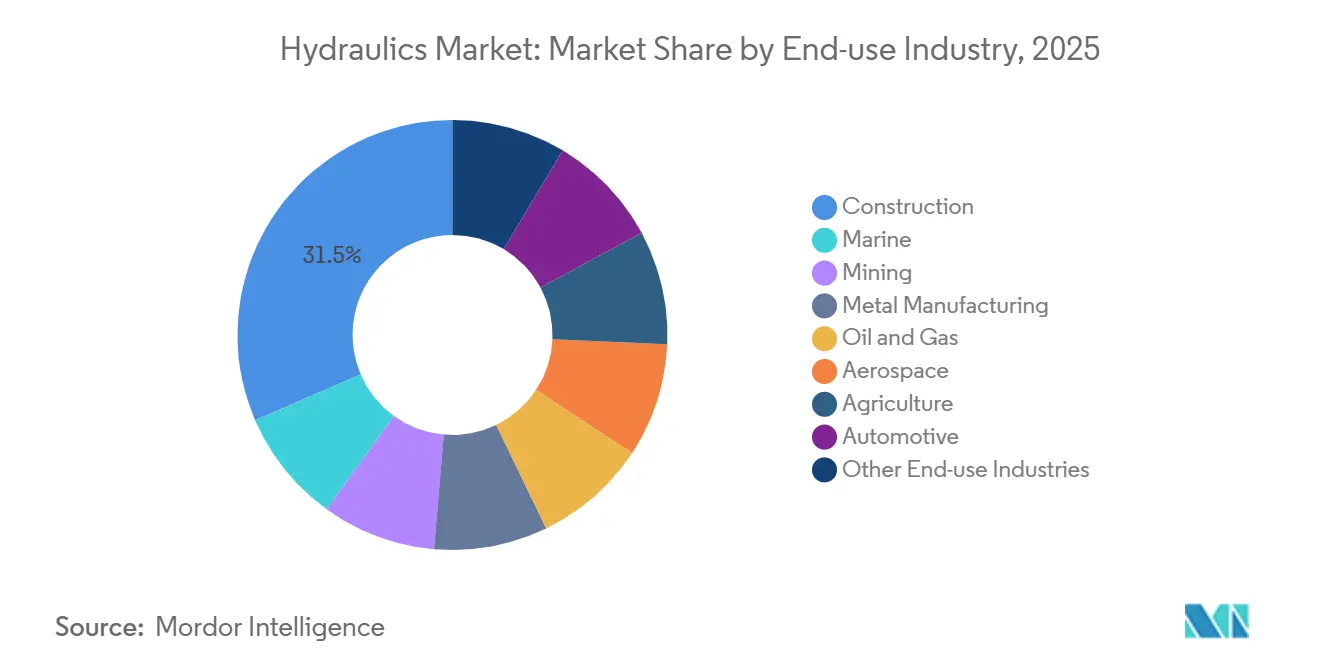

- By end-use industry, construction held a 31.48% share in 2025, while mining is expected to advance at a 5.27% CAGR through 2031.

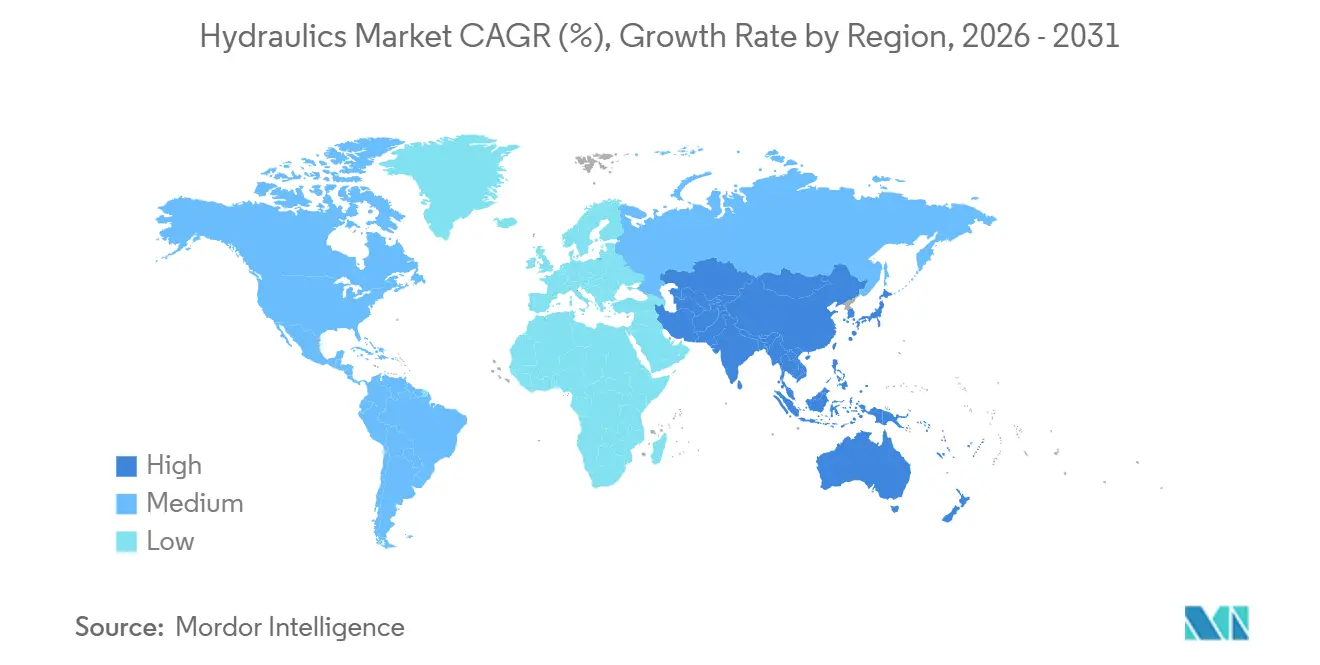

- By geography, Asia-Pacific held a 39.65% share in 2025 and is expected to be the fastest-growing regional segment, with a 4.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hydraulics Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Warehouse and Industrial Automation | +1.2% | Global | Medium term (2-4 years) |

| Shift Toward Electro-Hydraulics and Energy-Efficient Architectures | +1.0% | Global | Medium term (2-4 years) |

| Precision Agriculture Machinery Demand | +0.8% | Asia-Pacific, North America, EU | Medium term (2-4 years) |

| Electrification of Off-Highway Vehicles | +0.7% | North America and the EU, with spill-over to APAC | Long term (≥ 4 years) |

| Sensor-Embedded Hydraulics and Predictive Maintenance | +0.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift Toward Electro-Hydraulics and Energy-Efficient Architectures

Electro-hydraulic systems are replacing fixed-displacement circuits in construction, agriculture, and industrial press applications across the hydraulics market. Users are prioritizing lower energy consumption while maintaining the force output and duty performance that hydraulic systems provide. A 2025 study reports that a load-prediction-based variable-supply-pressure strategy delivered 70% hydraulic energy savings in robotic two-axis arm applications compared with fixed-supply-pressure systems. The same study reported energy savings of 62.5% in standard harmonic tests and 90% in multi-step reference tests for electro-hydraulic servo system control strategies. This data supports continued investment across the hydraulics market, as electrified machine architectures still require advanced valves, controls, and sensors to manage variable-speed power inputs.

Sensor-Embedded Hydraulics and Predictive Maintenance

Pressure, flow, temperature, and position sensing are shifting the hydraulics market from a hardware-led model to a more data-driven one. Embedded sensing enables hydraulic systems to move beyond closed analog loops and report condition, performance, and failure risk in real time. A peer-reviewed framework published in May 2026 showed that fractional factorial sensor designs combined with neural networks can detect hydraulic anomalies in real time with limited data requirements. This is relevant for the hydraulics market because fleet operators can run machines closer to target performance without increasing the risk of major breakdowns. It also strengthens the service side of the hydraulics market, as predictive maintenance tools support remote diagnostics, planned replacement cycles, and improved uptime management.

Precision Agriculture Machinery Demand

Precision agriculture is increasing hydraulic demand in the hydraulics market through greater system complexity and faster replacement cycles. Hydraulic systems continue to support power take-off, steering, and implement control across most agricultural machinery. As a result, advanced farming practices typically increase hydraulic content rather than reduce it. Danfoss launched the X1P piston pump family in April 2025 for medium-power mobile machinery and stated that the design reduces hysteresis by up to 80% and hydraulic noise by up to 3 dBA at 2,200 rpm[1]Danfoss A/S, “Danfoss Power Solutions Launches X1P Family, The First Step in the Evolution of Its Open-Circuit Piston Pump Portfolio,” Danfoss Newsroom, danfoss.com. ISO 11783 (ISOBUS)-based equipment integration is also increasing the number of independently managed hydraulic functions on a single machine in the hydraulics market. South Asia and Southeast Asia remain important to the hydraulics market because mechanization levels continue to rise across several crop systems.

Electrification of Off-Highway Vehicles

Electrification is changing hydraulic specifications across the hydraulics market, but it is not eliminating the need for hydraulic power. Electric excavators and loaders still require hydraulic systems, although these systems must now perform efficiently under intermittent duty cycles and variable-speed pump inputs. This design shift increases the need for precise metering, improved controls, and higher sensor content in each hydraulic circuit within the hydraulics market. As a result, the value mix in the hydraulics market is shifting toward smarter components rather than simple volume replacement. This trend keeps the hydraulics market relevant in off-highway equipment programs focused on battery efficiency, system responsiveness, and control precision.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hydraulic Fluid Leakage and Environmental Compliance Costs | -0.4% | Global, concentrated in EU, North America, and Australia | Short term (≤ 2 years) |

| Skilled Labor Scarcity in Hydraulics Maintenance and Engineering | -0.3% | North America and the EU, spillover to mining hubs in APAC | Medium term (2-4 years) |

| Raw-Material and Commodity Pricing Pressures | -0.5% | Global, acute in the US, South America, and import-dependent MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hydraulic Fluid Leakage and Environmental Compliance

Hydraulic fluid leakage remains a key issue across the hydraulics market, affecting operating efficiency and regulatory compliance. ISO 15380:2024 defines four biodegradable fluid categories-HETG, HEPG, HEES, and HEPR-and sets performance requirements for environmentally acceptable hydraulic fluids[2]Slovenian Institute for Standardization, “SIST ISO 15380:2024, Specifications for Environmentally Acceptable Hydraulic Fluids,” SIST, standards.iteh.ai. These requirements are changing the cost structure in parts of the hydraulics market, as fluids, seals, and fittings increasingly need to comply with environmental standards. They are also changing design priorities, as leakage can create procurement and compliance requirements beyond maintenance. As a result, the hydraulics market faces a higher engineering threshold for new systems, while suppliers with leak-control capabilities have a clearer path to differentiation.

Skilled Labor Scarcity in Hydraulics Engineering and Maintenance

The hydraulics market also faces a specialized labor challenge. Hydraulic service work increasingly requires technicians who understand fluid dynamics, precision calibration, and sensor-based diagnostics. TechForce Foundation reported 241,842 annual technician openings across the industrial machinery sector in 2026, compared with only 101,743 training program graduates, representing a 58% supply gap and USD 7.42 billion in wage-based output loss. This shortage affects the hydraulics market by slowing commissioning, field service, and advanced troubleshooting across mobile and industrial settings. It also strengthens the position of suppliers in the hydraulics market that offer remote diagnostics, predictive maintenance, and service contracts, thereby reducing dependence on limited field specialists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Mobile Applications Anchor Volume as Industrial Demand Builds

Mobile hydraulics are expected to hold 60.25% of the hydraulics market in 2025, reflecting the high hydraulic content used in construction, agriculture, mining, and lifting equipment. A single excavator or loader can use several simultaneous circuits for boom, arm, bucket, swing, and propel functions, keeping the value per machine high in the hydraulics market. This equipment profile explains why mobile applications continue to anchor volume across the hydraulics market, even as end-user requirements become more digital. The installed base also supports the hydraulics market, as wear parts, seals, and replacement components generate ongoing aftermarket demand over long equipment life cycles. Software-enabled control layers are becoming more common in these machines, but the core hydraulic architecture remains central to power delivery and work output.

Industrial hydraulics is projected to be the faster-growing type segment, registering a 4.85% CAGR through 2031, which keeps it important to the hydraulics industry despite its smaller base. Press automation, injection molding, metal forming, and process machinery upgrades are supporting demand across the hydraulics market. Danfoss is expected to introduce the Vickers PVMX axial piston pump in December 2025 for injection molding, rubber molding, and metal forming applications, with the design aimed at high dynamic performance, lower energy use, and advanced control. Reindustrialization also supports the hydraulics market, as semiconductor plants, battery factories, and aerospace facilities still require hydraulic press and actuation systems with long service lives. Verband Deutscher Maschinen- und Anlagenbau (VDMA) projected 3% nominal revenue growth for European fluid power manufacturers in 2026, indicating stabilization in customer industries, although trade and policy pressures continue to limit a faster recovery.

By Component: Pumps Lead Revenue While Valves Post the Fastest Growth

Pumps are expected to account for 25.85% of the hydraulics market size in 2025 because every hydraulic circuit depends on a power conversion stage. Piston pumps, especially variable-displacement axial piston designs, remain important in higher-pressure industrial and mobile applications across the hydraulics market. Gear pumps continue to serve lower-cost and less complex applications, keeping them relevant in simpler equipment platforms. The rest of the hydraulics market includes cylinders, motors, valves, filters, accumulators, transmissions, and other supporting components, each playing a distinct role in force generation, movement control, cleanliness, or energy management. Valves are projected to grow at a 5.76% CAGR through 2031, reflecting the rising adoption of proportional controls and advanced flow management across the hydraulics market.

This valve growth is tied to increasing system complexity in the hydraulics market, as electrified and automated machines require more accurate flow control at the function level. Proportional directional valves, load-sensing valves, and electronically managed manifolds are becoming more common in mid-range equipment, rather than remaining limited to premium systems. Filters and accumulators, while smaller in revenue terms, still shape performance across the hydraulics market by supporting cleanliness control, longer component life, and energy recovery. Peer-reviewed work expected to be published in 2025 showed that hydraulic hybrid machines can achieve fuel savings of 17% to 48% through accumulator-based energy regeneration. Procurement standards tied to safety, contamination control, and reliability are also pushing the hydraulics market toward higher average specification levels across component categories.

By Sensor: Pressure Sensors Lead While Flow Sensors Expand the Fastest

Pressure sensors are expected to hold a 30.62% share in 2025 within the hydraulics market's sensor segment, as they are essential for monitoring circuit integrity, system load, and component condition. Manufacturers use pressure sensors across a wide range of mobile and industrial systems, giving them the broadest installed base in the hydraulics market. Position, tilt, temperature, and level sensing also remain important, but their use depends more directly on machine function and operating conditions. Flow sensors are forecast to grow at a 5.33% CAGR through 2031, reflecting the need for real-time control in predictive maintenance and electro-hydraulic systems across the hydraulics market. Research expected to be published in 2026 showed that data-efficient neural network frameworks can detect anomalies in hydraulic networks in real time, lowering the practical barrier to wider sensor deployment.

Temperature sensing is gaining importance in the hydraulics market where thermal stability affects fluid viscosity, seal life, and cycle consistency, especially in metal forming and injection molding. Tilt sensors support safety functions in mobile cranes and aerial work platforms, where angle data is tied to operating limits and load control. Position sensing remains central to the hydraulics market because machine tools, mobile booms, and precision actuation systems require repeatable movement. A broader shift is also emerging in the hydraulics market, as manufacturers group multiple sensor types within advanced cylinder and actuator designs. This integration supports higher-value platforms because customers increasingly want pressure, position, temperature, and fault visibility from a single hydraulic assembly.

By End-Use Industry: Construction Leads While Mining Grows the Fastest

Construction is expected to hold 31.48% of the hydraulics market share in 2025, while mining is projected to grow at a 5.27% CAGR through 2031. Construction remains the largest end-use base in the hydraulics market because infrastructure programs and urban development require large fleets of excavators, loaders, cranes, and road-building machinery. Agriculture follows as another major source of demand, supported by mechanization and the shift toward more precise machine control. Mining is smaller in absolute terms, but it is the fastest-growing end-use in the hydraulics market, as autonomous haulage programs and electrified equipment require more advanced control architectures. A large installed base of aging mine equipment also supports the hydraulics market through replacement demand for pumps, cylinders, seals, hoses, and service work.

Other end-use segments remain important to the hydraulics market because they require specialized designs and often carry higher technical barriers. Aerospace applications demand high reliability and low failure tolerance, keeping that part of the hydraulics market relevant despite lower unit volumes. Parker Hannifin announced in May 2026 that it had entered a definitive agreement to acquire CIRCOR International's Commercial and Defense Aerospace business for USD 2.55 billion, underscoring its continued interest in motion and flow control applications. Oil and gas equipment continues to support the hydraulics market through high-pressure control systems used in specialized field conditions. Automotive and metal manufacturing also remain relevant because stamping, forming, bonding, and process equipment still rely on hydraulic actuation as production systems continue to evolve.

Geography Analysis

Asia-Pacific is expected to hold 39.65% of the hydraulics market share in 2025 and is projected to grow at a CAGR of 4.42% through 2031. This makes Asia-Pacific the largest and fastest-growing regional market for hydraulics. The region benefits from infrastructure development, agricultural mechanization, and demand for precision manufacturing. China remains a key hydraulics market, as construction equipment activity increases demand for mobile hydraulic systems and replacement parts. India supports the hydraulics market through infrastructure programs, equipment fleet upgrades, and broader financing access for farm and construction machinery.

Japan contributes to the hydraulics market through demand linked to automation, machine tools, and precision industrial systems. North America remains the second-largest regional market for hydraulics, supported by infrastructure programs, fleet replacement, farm equipment demand, and oil and gas activity in Canada. A large installed base of mid-life equipment supports the hydraulics market in North America, as replacement cycles for pumps, cylinders, seals, and hoses remain active even when new machine purchases slow. This provides distributors and service providers in the hydraulics market with aftermarket demand across construction, agriculture, and industrial users.

Europe shows a mixed trend in the hydraulics market, as Germany supports premium demand while slower investment in other parts of the region weighs on broader momentum. VDMA projects 3% nominal revenue growth for European fluid power manufacturers in 2026, indicating a cautious recovery rather than a sharp acceleration. Wind energy supports the hydraulics market in Europe, as pitch control, yaw drives, and braking systems continue to rely on hydraulic actuation. South America and the Middle East and Africa contribute smaller but meaningful demand to the hydraulics market through Brazil’s agri-machinery needs, Gulf construction and oil and gas projects, and mining replacement demand in South Africa.

Competitive Landscape

The hydraulics market is moderately fragmented among leading players and significantly more fragmented below that tier. Bosch Rexroth, Danfoss, Parker Hannifin, and Eaton maintain notable positions in the hydraulics market due to their broad product portfolios, system integration capabilities, and service reach. Competition is shifting from stand-alone hardware toward bundled solutions that include controls, sensing, and power management. According to the forward-looking information provided, Parker Hannifin stated in its 2025 annual report that it completed the acquisition of Curtis Instruments for USD 1 billion, adding motor controllers and power converters for electric and hybrid mobile equipment. Parker also announced in May 2026 that it had entered a definitive agreement to acquire CIRCOR International's Commercial and Defense Aerospace business for USD 2.55 billion, expanding its position in higher-margin flow and motion-control applications.

According to the forward-looking information provided, Eaton reported USD 27.4 billion in FY2025 revenue, a 10% year-over-year increase, and stated in July 2026 that it had invested USD 2.1 billion in research and development since 2020. These investments align with hydraulics market trends, as customers focus more on efficiency, asset productivity, and safety. Mid-tier participants face pressure from global-scale companies at the top and cost-focused competitors in more standardized product categories. This dynamic creates opportunities for specialists that can compete through faster customization, application engineering, and post-installation support.

Suppliers that combine hydraulic hardware with sensors, software, and service tools are increasingly gaining notable positions in the hydraulics market. This shift matters because customers want lower energy consumption, higher uptime, and easier diagnostics from the same installed system. Regional specialists still have opportunities, especially where machine requirements are specific and response time matters more than portfolio breadth. However, standardized parts of the hydraulics market remain exposed to price competition unless suppliers demonstrate clear value through integration, reliability, or lifecycle support.

Hydraulics Industry Leaders

Bosch Rexroth AG

PARKER HANNIFIN CORP

Danfoss A/S

HYDAC International GmbH

Eaton

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Parker Hannifin entered into a definitive agreement to acquire CIRCOR International's Commercial and Defense Aerospace business for USD 2.55 billion. The transaction is expected to close in the second half of 2026 and focuses on flight-critical motion and flow control products for commercial and defense aircraft platforms.

- March 2026: Bosch Rexroth and Kawasaki Heavy Industries announced a planned strategic partnership to jointly develop intelligent off-highway machine concepts. The collaboration combines Bosch Rexroth's electronics, software, and electrification portfolio with Kawasaki's precision hydraulic hardware and excavator system expertise. It targets autonomous operation, hydrogen propulsion, and advanced worksite safety.

Global Hydraulics Market Report Scope

Hydraulics refers to the science of transmitting energy and force through pressurized liquids. Based on Pascal’s Law, force applied to a confined fluid transfers pressure equally throughout the fluid, increasing force at the other end.

The hydraulics market is segmented by type, component, sensor, end-use industry, and geography. By type, the market is segmented into mobile hydraulics and industrial hydraulics. By component, the market is segmented into cylinders, pumps, motors, valves, filters, accumulators, transmissions, and other components. By sensor type, the market is segmented into tilt sensors, position sensors, pressure sensors, temperature sensors, level sensors, and flow sensors. By end-use industry, the market is segmented into aerospace, agriculture, automotive, construction, marine, mining, metal manufacturing, oil and gas, and other end-use industries. The report also covers market size and forecasts for hydraulics across 16 countries in major regions. The market sizes and forecasts are provided in terms of value (USD).

| Mobile Hydraulics |

| Industrial Hydraulics |

| Cylinders |

| Pumps |

| Motors |

| Valves |

| Filters |

| Accumulators |

| Transmissions |

| Other Components |

| Tilt Sensors |

| Position Sensors |

| Pressure Sensors |

| Temperature Sensors |

| Level Sensors |

| Flow Sensors |

| Aerospace |

| Agriculture |

| Automotive |

| Construction |

| Marine |

| Mining |

| Metal Manufacturing |

| Oil and Gas |

| Other End-use Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Mobile Hydraulics | |

| Industrial Hydraulics | ||

| By Component | Cylinders | |

| Pumps | ||

| Motors | ||

| Valves | ||

| Filters | ||

| Accumulators | ||

| Transmissions | ||

| Other Components | ||

| By Sensor | Tilt Sensors | |

| Position Sensors | ||

| Pressure Sensors | ||

| Temperature Sensors | ||

| Level Sensors | ||

| Flow Sensors | ||

| By End-use Industry | Aerospace | |

| Agriculture | ||

| Automotive | ||

| Construction | ||

| Marine | ||

| Mining | ||

| Metal Manufacturing | ||

| Oil and Gas | ||

| Other End-use Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Hydraulics Market?

The Hydraulics Market size is projected to expand from USD 57.58 billion in 2025 and USD 60.11 billion in 2026 to USD 74.42 billion by 2031, and is expected to register a CAGR of 4.36% between 2026 and 2031.

Which region leads to global demand for hydraulic systems?

Asia-Pacific led with 39.65% share in 2025 and is also the fastest-growing region, with a 4.42% CAGR through 2031.

Which type of hydraulic application is the largest today?

Mobile hydraulics was the largest segment in 2025, with a 60.25% share, supported by demand for construction, agriculture, mining, and lifting equipment.

Which component category is growing the fastest?

Valves are the fastest-growing component segment, with a projected 5.76% CAGR through 2031, as system control becomes more precise and increasingly managed electronically.

Page last updated on: