Hybrid OTT Monetization Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.89 Billion |

| Market Size (2031) | USD 22.39 Billion |

| Growth Rate (2026 - 2031) | 10.02% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hybrid OTT Monetization Market Analysis by Mordor Intelligence

The hybrid OTT monetization market size is expected to increase from USD 13.12 billion in 2025 to USD 13.89 billion in 2026 and reach USD 22.39 billion by 2031, growing at a CAGR of 10.02% over 2026-2031. The hybrid OTT monetization market is moving away from single-revenue streaming models toward a layered structure that combines subscription, advertising, free streaming, and transaction-based access within a single platform. This shift is supported by wider adoption of connected TV, stronger programmatic advertising tools, and device ecosystems that now treat ad inventory as a recurring revenue stream rather than a side feature. Consumer acceptance of lower-cost and free viewing options with advertising has improved enough to make ad-supported access a mainstream entry point rather than a secondary offer. The hybrid OTT monetization market is also gaining support from subscription fatigue in mature regions and price sensitivity in emerging regions, which makes mixed pricing and bundle strategies more durable than pure subscription plans. Larger platforms are responding by building broader data ecosystems, tighter bundling structures, and deeper monetization layers that can support growth even as content costs and measurement gaps remain difficult constraints.

Key Report Takeaways

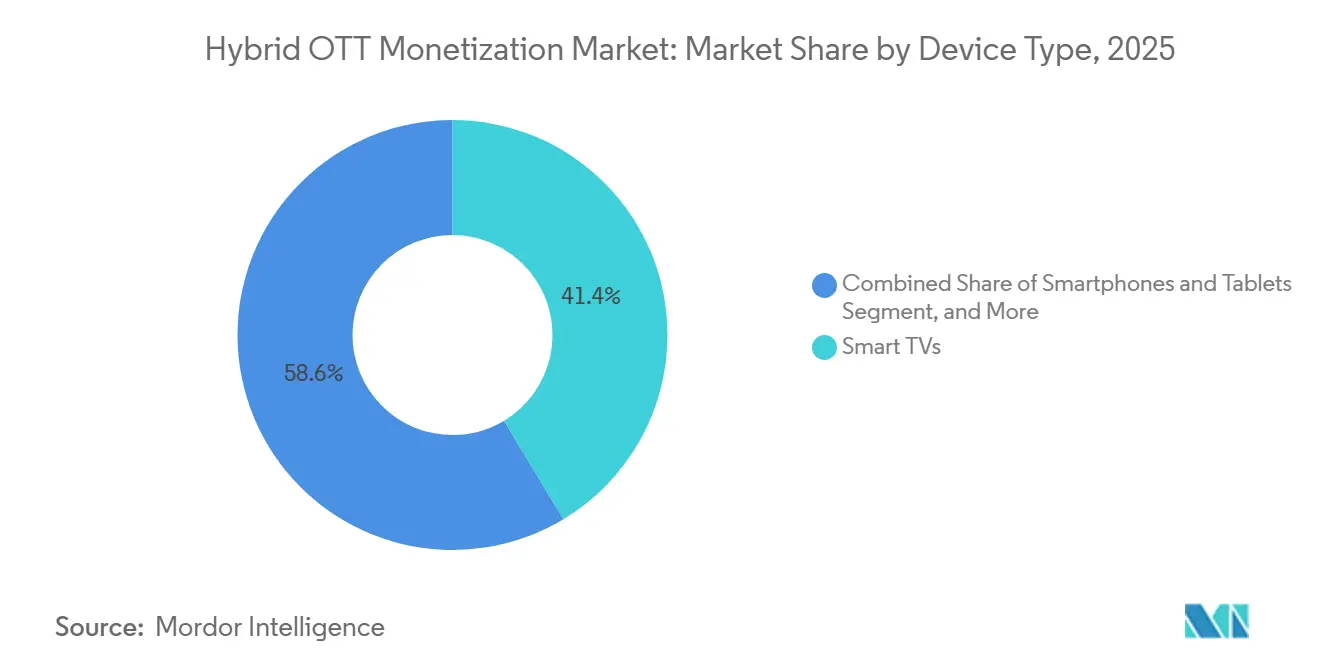

- By device type, smart TVs accounted for 41.37% of revenue in 2025 and remained the leading and fastest-expanding device category, with a CAGR of 11.32% in the hybrid OTT monetization market through the forecast period.

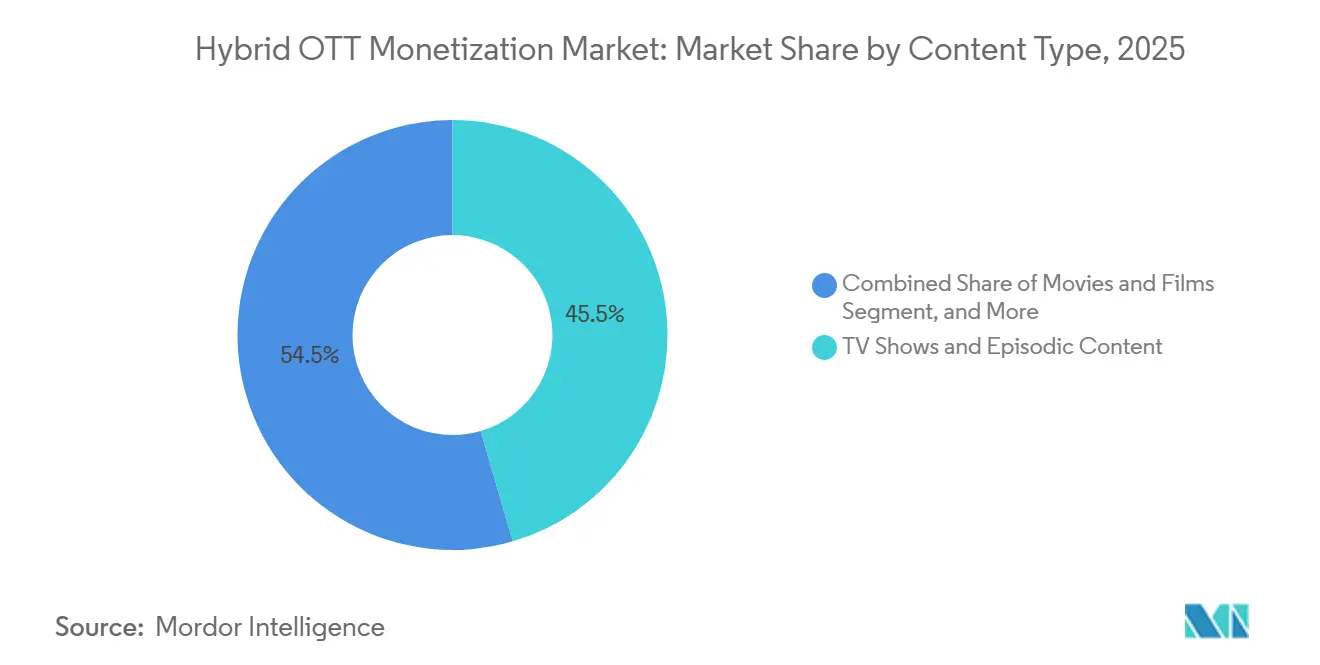

- By content type, TV shows and episodic content accounted for the largest revenue share in 2025, while documentaries are projected to expand at an 11.73% CAGR through 2031.

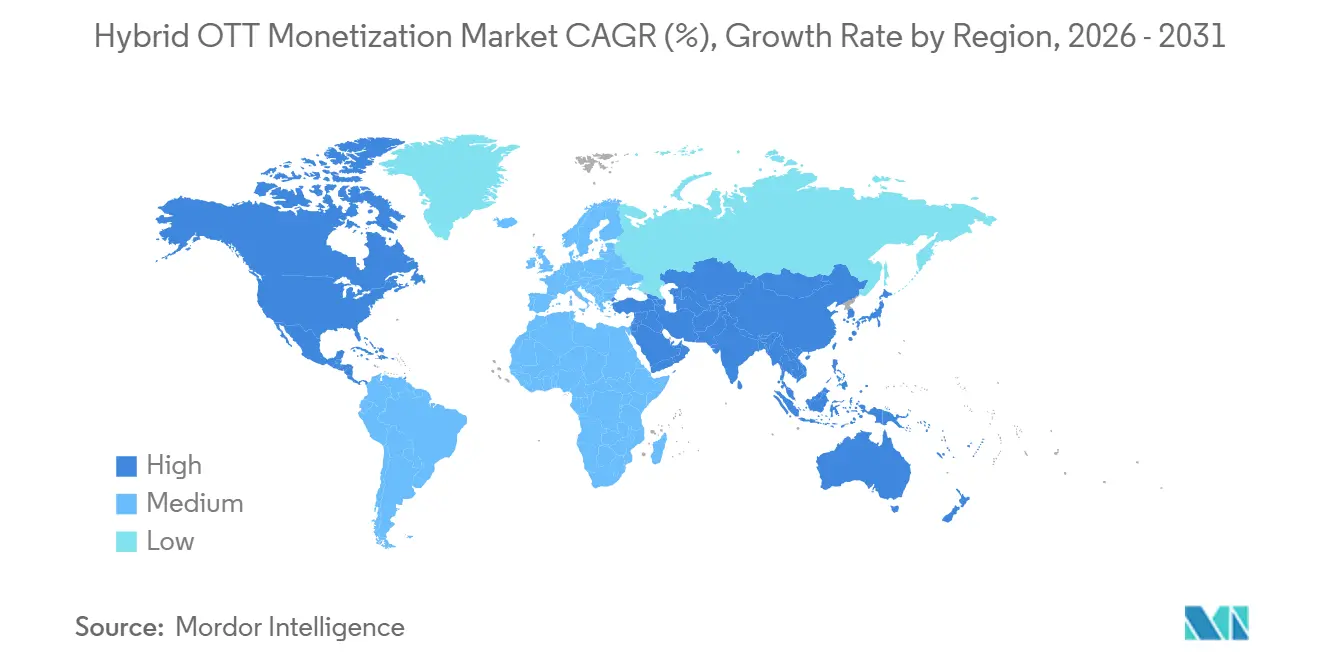

- By geography, North America accounted for 31.82% of global revenue in 2025, while Asia-Pacific is projected to grow at a 11.61% CAGR through 2031 for the hybrid over-the-top (OTT) monetization market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hybrid OTT Monetization Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Hybrid Tier Adoption Among SVOD Leaders | +2.8% | Global | Short term (≤ 2 years) |

| Rising FAST Monetization Through CTV OEM Ecosystems | +2.1% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Subscription Fatigue Accelerates Bundling and Freemium Conversion | +1.7% | North America, Europe | Medium term (2-4 years) |

| First-Party Viewing Data Improves Ad Yield Optimization | +1.4% | North America and Europe | Medium term (2-4 years) |

| Localized Content Monetization Gains in Asia-Pacific and South America | +1.0% | Asia-Pacific core, spill-over to South America | Medium term (2-4 years) |

| Live Sports and Event Windows Expand TVOD and Premium Ad Inventory | +0.7% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Hybrid Tier Adoption Among SVOD Leaders

The hybrid OTT monetization market is gaining momentum because major subscription streaming platforms now treat ad-supported tiers as a core part of platform design rather than a defensive pricing response. Netflix stated that its advertising business grew by more than 2.5 times in 2025, exceeding USD 1.5 billion, while total company revenue reached USD 45.2 billion.[1]Netflix, Inc., “Annual Report 2025 (Form 10-K),” Netflix Investor Relations, s22.q4cdn.com That scale matters because ad-tier users create household viewing data that ad-free subscriptions do not generate at the same depth, which improves audience targeting and supports stronger pricing in video advertising. The hybrid OTT monetization market is therefore seeing revenue per user become less dependent on subscription price increases and more dependent on the mix of access fees and ad yield per impression. Disney’s unified ad-buying stack across Disney+, Hulu, and ESPN+ shows that the leading platforms are not only adding lower-priced tiers but also building switching costs across broader portfolios.

Rising FAST Monetization Through CTV OEM Ecosystems

The hybrid OTT monetization market is also being driven by FAST growth across connected TV ecosystems, where device manufacturers, channel operators, and platforms now share a common monetization surface. Amagi’s AIRTIME findings for April to June 2026 showed a 55% year-on-year increase in global FAST viewing hours and a 53% increase in ad impressions. These numbers show that free streaming is no longer only a discovery layer, because it now supports habitual viewing across a growing connected TV base. The OEM layer matters more in the hybrid OTT monetization market because television makers are using home-screen inventory, FAST storefronts, and automatic content recognition data as repeatable revenue sources beyond hardware sales. Nexxen’s July 2025 update on the VIDAA and Vestel relationship also shows that data access and exclusive monetization rights are becoming strategic assets for connected TV advertising in Europe.

Subscription Fatigue Accelerates Bundling and Freemium Conversion

The hybrid OTT monetization market is benefiting from rising consumer fatigue with managing multiple full-price subscriptions in mature streaming regions. Antenna reported that the Disney+/Hulu/Max bundle achieved a 12-month subscriber survival rate of 59% for its 2024 cohort, which was 4 percentage points above standalone Netflix and 28 percentage points above the component services on average. By Q4 2025, bundles accounted for 27% of total premium SVOD subscriptions, up from 14% in Q4 2023, while bundle subscriptions grew 50% year on year and non-bundle subscriptions contracted 1%. This shows that bundles are no longer a side offer, because they now function as a primary retention tool and a more stable monetization structure for large platform groups. The hybrid over-the-top (OTT) monetization market is also benefiting, as bundled users create richer cross-service behavioral records, which improve audience segmentation and increase the value of ad inventory sold across multiple services.

First-Party Viewing Data Improves Ad Yield Optimization

The hybrid OTT monetization market is increasingly shaped by first-party viewing data, as advertisers seek stronger evidence that connected TV campaigns can be measured across screens and linked to outcomes. Comcast Advertising launched Outcomes+ in 2025, combining deterministic TV and streaming viewing data with Blockgraph On Demand for self-service advertiser data matching. IAB stated in October 2025 that 75% of advertisers already using conversion APIs were willing to reallocate budgets based on conversion performance, while 72% of publishers still cited technical complexity as a barrier to adoption. That gap creates a near-term advantage for large platforms that can fund server-to-server data pipelines, attribution engines, and identity systems before those tools become easier to standardize. The hybrid OTT monetization market is therefore moving toward a structure in which data quality has a greater influence on CPM performance than raw inventory volume alone. This is also widening the performance gap between operators that own premium supply and audience data and operators that still depend on fragmented external ad-tech stacks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Ad-Tech Stacks Limit Unified Yield Optimization | -1.8% | Global | Medium term (2-4 years) |

| Rising Content and Rights Costs Compress Hybrid Margins | -1.4% | Global | Long term (≥ 4 years) |

| Measurement Gaps Across Platforms Reduce Advertiser Confidence | -1.0% | North America and Europe | Medium term (2-4 years) |

| Closed Ecosystems and Privacy Rules Restrict Cross-Platform Targeting | -0.7% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Ad-Tech Stacks Limit Unified Yield Optimization

The hybrid OTT monetization market still faces a structural operational problem because platforms are trying to combine SVOD, AVOD, FAST, and TVOD on infrastructure that was not designed to cleanly share data. Separate entitlement engines, bid-request systems, and identity frameworks make each added monetization tier more expensive to run and harder to optimize at scale. CIMM and the 4As found that 43% of advertisers viewed cross-platform measurement as a major or severe barrier over the next 3 to 5 years, indicating that infrastructure issues continue to affect advertiser confidence. The same study found that 84% of advertisers viewed AI’s impact on measurement as the most consequential upcoming development, which suggests the industry expects a solution later rather than now. The hybrid OTT monetization market, therefore, remains uneven because large incumbents can fund proprietary yield systems while mid-tier operators absorb higher complexity with less pricing power.

Rising Content and Rights Costs Compress Hybrid Margins

The hybrid OTT monetization market also remains exposed to content inflation because mixed revenue models have not reduced the cost of premium libraries and live rights. Amazon disclosed total content spending of USD 22.4 billion for FY2025, a 10% year-on-year increase. Netflix’s content payment growth slowed to 4% in 2025, which shows that tighter spending discipline is possible, but it is much harder to replicate for smaller operators with weaker amortization efficiency.[2]Netflix, Inc., “Annual Report 2025 (Form 10-K),” Netflix Investor Relations, s22.q4cdn.com The pressure is especially strong in live sports, where multi-year contracts often include annual escalators regardless of advertising conditions or platform profitability. The hybrid OTT monetization market is therefore seeing a widening gap between the upside from premium event windows and the rising floor cost required to secure them across the forecast period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Smart TVs Anchor Hybrid Monetization At Scale

Smart TVs accounted for 41.37% of revenue in 2025, making them the leading device category in the hybrid OTT monetization market and the clearest center of monetization across FAST, SVOD apps, and ACR-powered advertising. The same segment also represented the fastest-growing device category, indicating that large-screen viewing is rising as monetization tools on connected televisions become more valuable. In the hybrid OTT monetization industry, this convergence is important because smart TV operating systems are no longer limited to app distribution; they are now monetizing home screens, channel rails, storefront placement, and first-party viewing data. That creates a second monetization layer above the content platform itself, which makes OEM distribution agreements more important than they were in the earlier phase of streaming. The hybrid OTT monetization market is therefore giving greater weight to operators that can secure living-room access, manage higher ad load tolerance, and convert audience behavior into premium connected TV inventory.

Smartphones and tablets remained the second-largest device segment, and they are especially important in Asia-Pacific and South America, where mobile viewing still accounts for a large share of OTT consumption. JioHotstar described IPL 2026 as a tool for shifting mobile-first viewers toward connected-TV behavior, showing how live sports can change device usage rather than just drive short-term traffic spikes. Laptops and desktops kept a smaller role because they support individual viewing moments but offer less scale and weaker ad-load tolerance than smart TVs. Other device types, such as gaming consoles and streaming sticks, still extend reach, but fragmented identity signals and limited monetization control keep them from becoming primary revenue surfaces in the hybrid OTT monetization market.

By Content Type: Serialized Formats Lead, Nonfiction Emerges As A Margin Play

TV shows and episodic content held the largest revenue share of 45.18% in 2025, and that leadership came from a format structure that fits the hybrid OTT monetization market especially well. Serialized viewing creates natural ad-pod insertion points, extends total session time, and generates completion signals that are useful for programmatic targeting and audience quality scoring. Documentaries are projected to expand at an 11.73% CAGR through 2031, making them the fastest-growing content type, as they combine lower production costs with a high-intent audience profile that supports attractive AVOD pricing. In the hybrid OTT monetization industry, that cost-yield balance makes nonfiction one of the few categories that can improve monetization efficiency without carrying the same title-level rights risk as premium scripted content. The hybrid OTT monetization market is therefore seeing documentaries move from a supporting catalog category into a meaningful margin-supporting content class.

Movies and films continued to generate hybrid revenue through TVOD for newer releases and AVOD for library titles after premium release windows ended. Amagi’s June 2026 AIRTIME findings also showed that kids' content recorded 191% growth in hours viewed and 118% growth in ad impressions across FAST channels between April and June 2026, which indicates stronger family-oriented monetization in free streaming environments. The broader other content type category includes live events, sports highlights, short-form vertical video, and user-generated content, and each of these formats carries a different monetization pattern depending on urgency, repeat viewing, and commerce integration. JioHotstar’s Tadka integration shows that short-form content can add another monetization layer within the hybrid over-the-top (OTT) monetization market without replacing long-form viewing behavior

Geography Analysis

North America held 31.82% of the hybrid OTT monetization market share in 2025, making it the largest revenue region globally. This lead came from advanced programmatic infrastructure, high TV household penetration, and stronger monetization efficiency in premium ad-supported streaming. The United States and Canada accounted for 74% of global FAST ad impressions and 54% of global FAST viewing hours, indicating a clear pricing and yield premium in the region. Live sports also strengthened the region’s position because streaming rights for the NFL, MLB, and other events support premium ad inventory and transaction-based viewing windows simultaneously. Mexico remained smaller within the broader regional mix, but hybrid AVOD models are expanding there as telecom-linked OTT access and lower-cost entry points reshape consumer acquisition.

Asia-Pacific is projected to expand at an 11.61% CAGR through 2031, making it the fastest-growing regional component of the hybrid OTT monetization market. The region is moving toward hybrid monetization faster than many Western markets because affordability remains a central factor in content access across India, Southeast Asia, and other emerging regions. Reliance Industries stated that JioStar averaged 451 million monthly active users during FY26 and generated INR 34,917 crore in revenue (USD 4.18 billion). That result confirms that scale-driven hybrid economics can work even when average user spending stays low, because large ad-supported audiences still create a viable commercial base. South Korea and Japan have a more mature SVOD foundation, while India and Southeast Asia continue to drive regional growth through a mix of subscription and advertising models.[3]Viaccess-Orca, “APAC Streaming Trends: Data and Analysis,” Viaccess-Orca, viaccess-orca.com

Europe remains a more complex operating environment because GDPR compliance limits some forms of cross-platform targeting and behavioral personalization used in AVOD yield optimization. Even so, the region is still expanding, and VAUNET projected that Germany’s 2026 TV, video streaming, and audio media advertising revenue would reach EUR 6.55 billion (USD 7.07 billion). That still shows that streaming is taking share from linear formats even within a stricter regulatory setting. The Middle East and Africa remain earlier in the monetization curve, with premium SVOD growth in Gulf markets and mobile-first AVOD adoption across South Africa, Egypt, and Nigeria supporting gradual expansion in the hybrid over-the-top (OTT) monetization market.

Competitive Landscape

The hybrid OTT monetization market remains moderately concentrated at the global platform tier, with Netflix, Amazon, and Alphabet’s YouTube holding strong positions through content scale, proprietary advertising technology, and broad distribution. The main competitive pattern is clear as the leading operators are trying to deepen first-party data ownership, expand bundle value, and keep more of the advertising stack within their own systems. Netflix’s amended USD 82.7 billion all-cash agreement for Warner Bros. Discovery showed how the largest players are still using library scale as a hedge against monetization pressure and content inflation. The same deal also preserved a 45-day theatrical window, showing that transaction revenue still matters within broader hybrid platform strategies. The hybrid over-the-top (OTT) monetization market is therefore favoring companies that can spread monetization across subscriptions, advertising, and selective premium release windows without relying on any single layer.

A second competitive layer is developing around OEM-native FAST systems and technology intermediaries that help smaller operators improve yield management. Device-linked platforms such as Roku, Samsung TV Plus, VIDAA, and Titan OS are building monetization positions that operate independently of the major content owners, enabling them to capture ad revenue from viewer activity across many streaming applications. Chalice AI and OpenX announced in June 2026 that advertisers would be able to deploy custom AI bidding models against premium video inventory through OpenX’s supply-side platform, which lowers the technical threshold for more advanced curation and pricing. The hybrid OTT monetization market is creating space for these infrastructure-focused players, as professional monetization tools are becoming as important as content ownership in determining revenue quality.

Regional operators are responding by leaning on localization, selective alliances, and shared rights structures rather than trying to match global incumbents on spending. PCCW’s Viu and iQIYI International announced a Southeast Asian bundle arrangement that reduced rights pressure while expanding the addressable AVOD audience, demonstrating how co-distribution can serve as a competitive tool outside the top global tier. JioHotstar’s ChatGPT-powered conversational discovery rollout in India also shows that product design can improve engagement and create richer intent signals for monetization at scale.[4]JioStar, “JioHotstar Launches ChatGPT-Branded Conversational Streaming in India,” JioStar, jiostar.com Taken together, these moves show that the hybrid OTT monetization market is not only a scale contest, because regional relevance, device access, and monetization tools still create durable positions even alongside larger global competitors.

Hybrid OTT Monetization Industry Leaders

Netflix, Inc.

The Walt Disney Company

Amazon.com, Inc.

Comcast Corporation

Paramount Skydance Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: DAZN reported FIFA World Cup 2026 ad revenue exceeding internal expectations across its streaming coverage, with the platform's hybrid TVOD and AVOD inventory structures monetizing live sports audiences across multiple access tiers. The outcome validates live sports event windows as a primary driver of premium ad inventory expansion in hybrid OTT platforms.

- June 2026: Omnicom announced expanded CTV partnerships with Disney, Roku, Amazon, and JioStar, creating integrated programmatic and direct-sold advertising pipelines spanning 4 of the largest hybrid OTT platforms globally, the collaboration is designed to provide brand advertisers with unified addressable CTV reach across multiple ecosystems without requiring separate platform-level negotiations, per Storyboard18 reporting.

- June 2026: Chalice AI and OpenX announced a partnership embedding AI-powered supply curation within OpenX's SSP infrastructure, enabling advertisers to deploy custom AI bidding models in real time against high-quality CTV video inventory, the integration reduces intermediary friction in premium CTV demand access and lowers the engineering threshold for mid-scale content operators to achieve professional yield management, per the companies' joint press release.

- May 2026: Viant Technology closed its acquisition of TVision, a television measurement provider specializing in quantifying viewer attention across CTV, linear TV, YouTube, and Prime Video content, per Viant's Q1 2026 earnings call transcript, the deal positions the company to connect ad exposure to verified eyes-on-screen data, addressing one of the hybrid OTT ecosystem's most persistent attribution gaps.

Global Hybrid OTT Monetization Market Report Scope

The Hybrid OTT Monetization market comprises over-the-top (OTT) video streaming services that generate revenue through a combination of monetization models, including subscription-based video-on-demand (SVOD), advertising-supported video-on-demand (AVOD), transactional video-on-demand (TVOD), pay-per-view (PPV), and freemium offerings. These platforms deliver digital video content over the internet across multiple connected devices, enabling users to access movies, television series, documentaries, and other video programming through one or more revenue models within a single service.

The Hybrid OTT Monetization Market Report is Segmented by Device Type (Smartphones and Tablets, Smart TVs, Laptops and Desktops, and Other Device Types), Content Type (Movies and Films, TV Shows and Episodic Content, Documentaries, and Other Content Types), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Smartphones and Tablets |

| Smart TVs |

| Laptops and Desktops |

| Other Device Types |

| Movies and Films |

| TV Shows and Episodic Content |

| Documentaries |

| Other Content Types |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Device Type | Smartphones and Tablets | |

| Smart TVs | ||

| Laptops and Desktops | ||

| Other Device Types | ||

| By Content Type | Movies and Films | |

| TV Shows and Episodic Content | ||

| Documentaries | ||

| Other Content Types | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2026 value and 2031 outlook for hybrid OTT monetization?

The hybrid OTT monetization market is estimated at USD 13.89 billion in 2026 and is projected to reach USD 22.39 billion by 2031 at a 10.02% CAGR.

Why are ad-supported and hybrid streaming models gaining ground so quickly?

Lower-cost access, subscription fatigue, and stronger connected TV ad tools are making mixed models more attractive for both consumers and platforms.

Which device category contributes the most revenue today?

Smart TVs led with 41.37% share in 2025, supported by strong living-room viewing time and better monetization on connected television screens.

Which content category is expanding the fastest through 2031?

Documentaries are projected to grow the fastest at an 11.73% CAGR because they pair lower production costs with strong advertiser interest.

Which region is growing the fastest in streaming monetization?

Asia-Pacific is the fastest-growing region with an 11.61% CAGR, helped by large ad-supported audiences and lower-price entry models.

What are the main challenges holding back stronger revenue expansion?

Fragmented ad-tech systems, uneven cross-platform measurement, and rising content and rights costs continue to limit monetization efficiency.

Page last updated on: