Hybrid CRO Models And Tech-Enabled CRO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 17.82 Billion |

| Market Size (2031) | USD 28.56 Billion |

| Growth Rate (2026 - 2031) | 9.89% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hybrid CRO Models And Tech-Enabled CRO Market Analysis by Mordor Intelligence

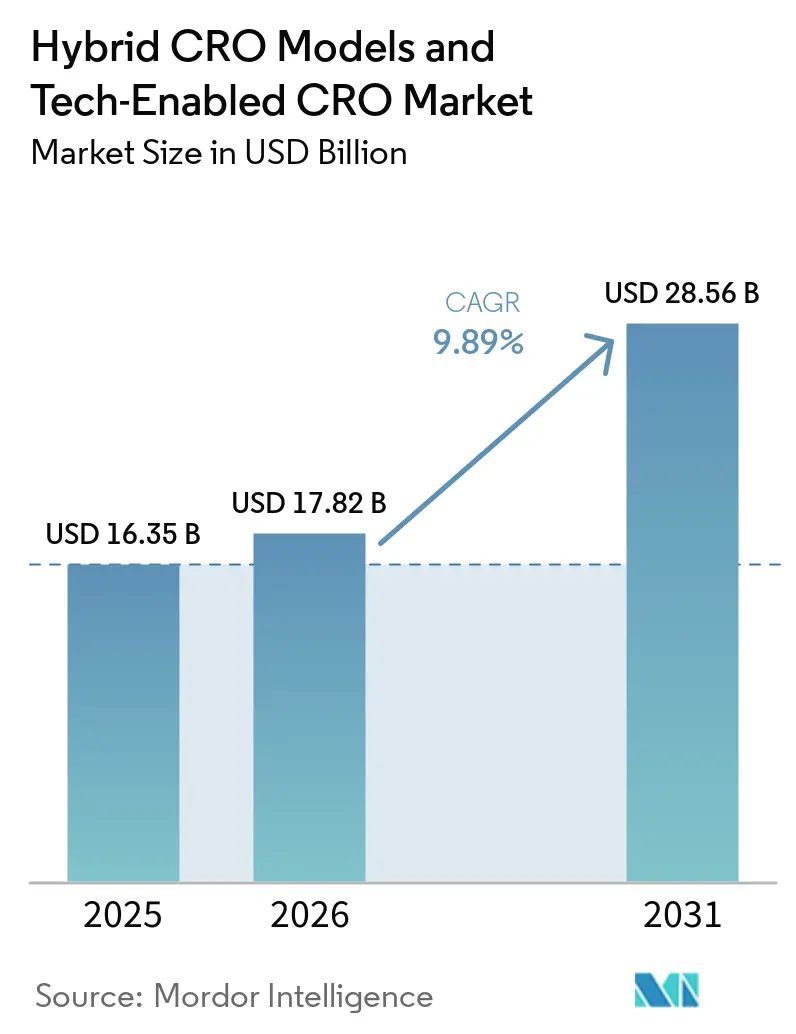

The Hybrid CRO Models And Tech-Enabled CRO Market size is projected to be USD 16.35 billion in 2025, USD 17.82 billion in 2026, and reach USD 28.56 billion by 2031, growing at a CAGR of 9.89% from 2026 to 2031.

Hybrid operating models that blend traditional site-based monitoring with decentralized infrastructure have shifted from optional pilots to the default approach, especially for orphan-drug trials where patients live on multiple continents and recruitment windows last longer than 18 months [1]H.R.6283, “Orphan Biologics and Biosimilars Bill Act of 2025,” Congress.gov, congress.gov. Tech-enabled platforms deliver artificial-intelligence patient matching, wearable sensors for continuous endpoint capture, and cloud-native data integration that supports adaptive protocols capable of shortening Phase I dose-escalation by up to 40%. The Orphan Biologics and Biosimilars Bill eliminated United States price-negotiation risk, reviving 14 stalled Phase III programs and driving sponsors toward hybrid contracts that reduce per-patient costs through at-home nursing and telemedicine. Asia-Pacific is emerging as the fastest-growing geography after China tripled its priority-review-voucher pipeline in early 2025, prompting CROs to open hybrid trial units in Shanghai and Beijing. Mid-tier specialists are winning share by offering vector-manufacturing oversight, long-term registry maintenance, and AI-powered data lakes that reconcile privacy rules across regions, reinforcing the Hybrid CRO Models & Tech-Enabled CRO market’s transition from labor-intensive service work to data-centric platforms.

Key Report Takeaways

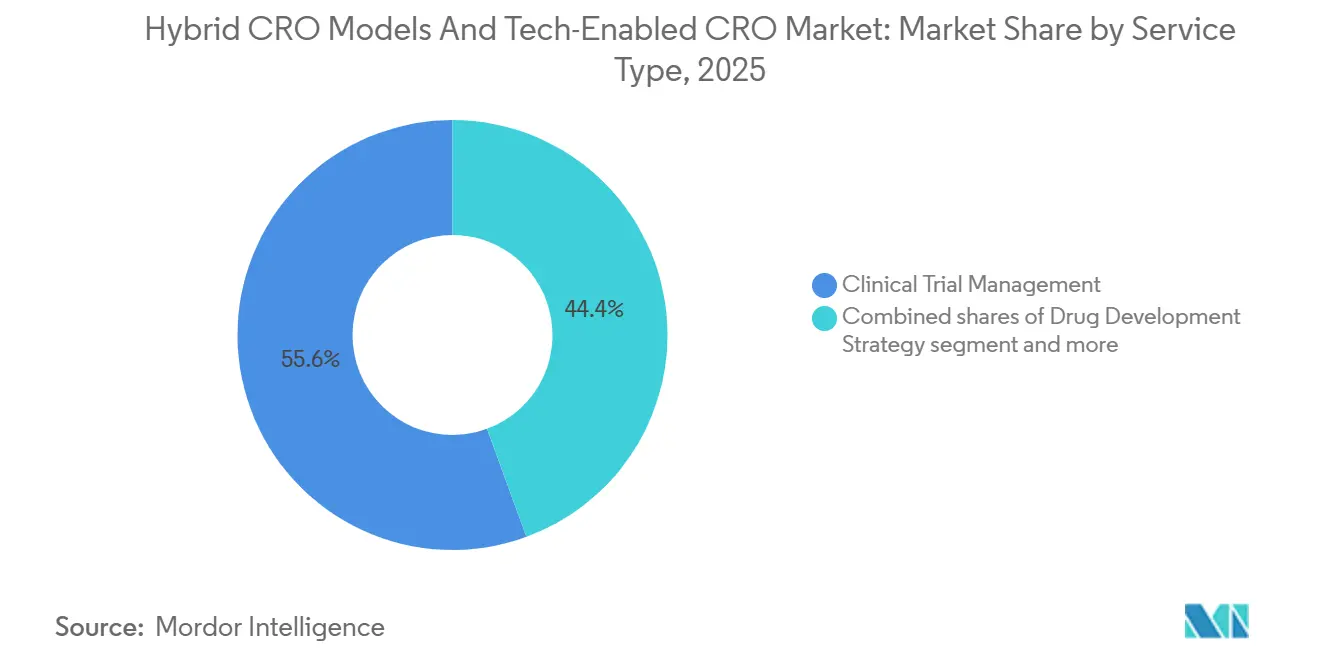

- By service type, Clinical Trial Management led with 55.6% of the Hybrid CRO Models & Tech-Enabled CRO market share in 2025, whereas Data Management & Biostatistics is advancing at a 10.50% CAGR through 2031.

- By therapeutic area, Oncology accounted for 35.2% of the Hybrid CRO Models & Tech-Enabled CRO market size in 2025; Neuroscience is projected to expand at a 10.38% CAGR to 2031.

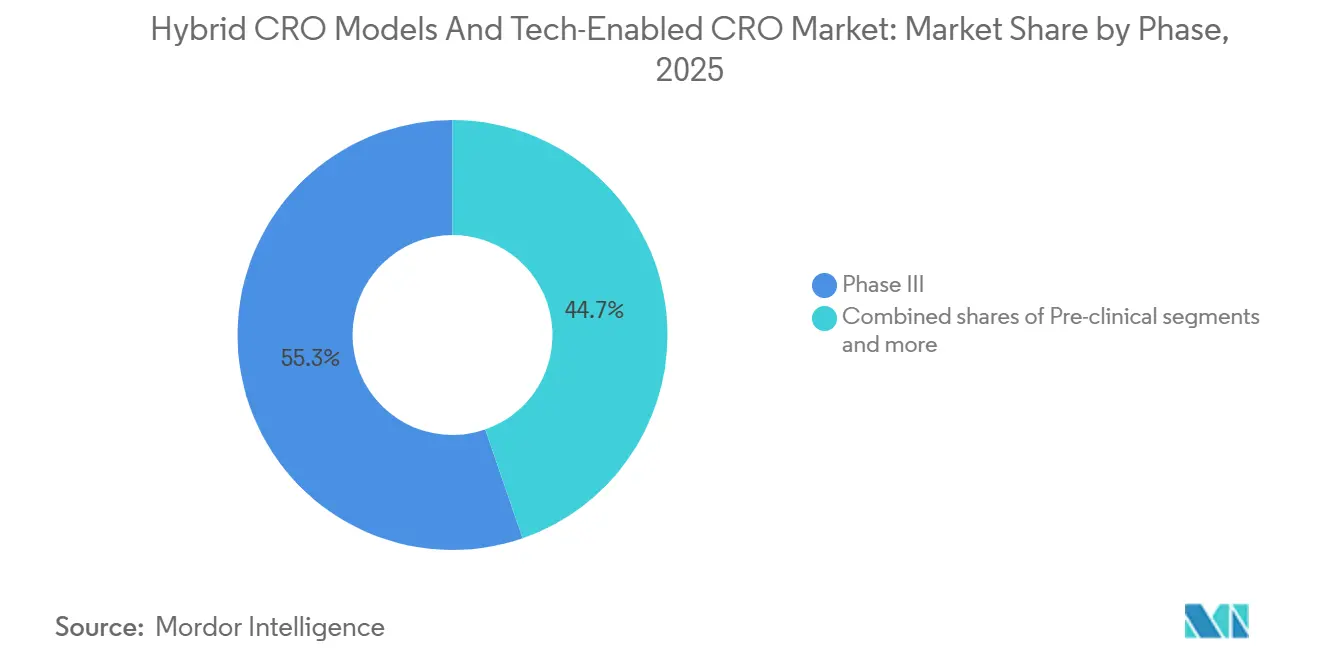

- By phase, Phase III dominated with 55.3% share in 2025, while Phase I is growing at an 10.33% CAGR through 2031.

- By end-user, Pharma & Biotech companies held 72.1% of 2025 spending, yet Non-profit & Government sponsors posted the highest 10.48% CAGR to 2031.

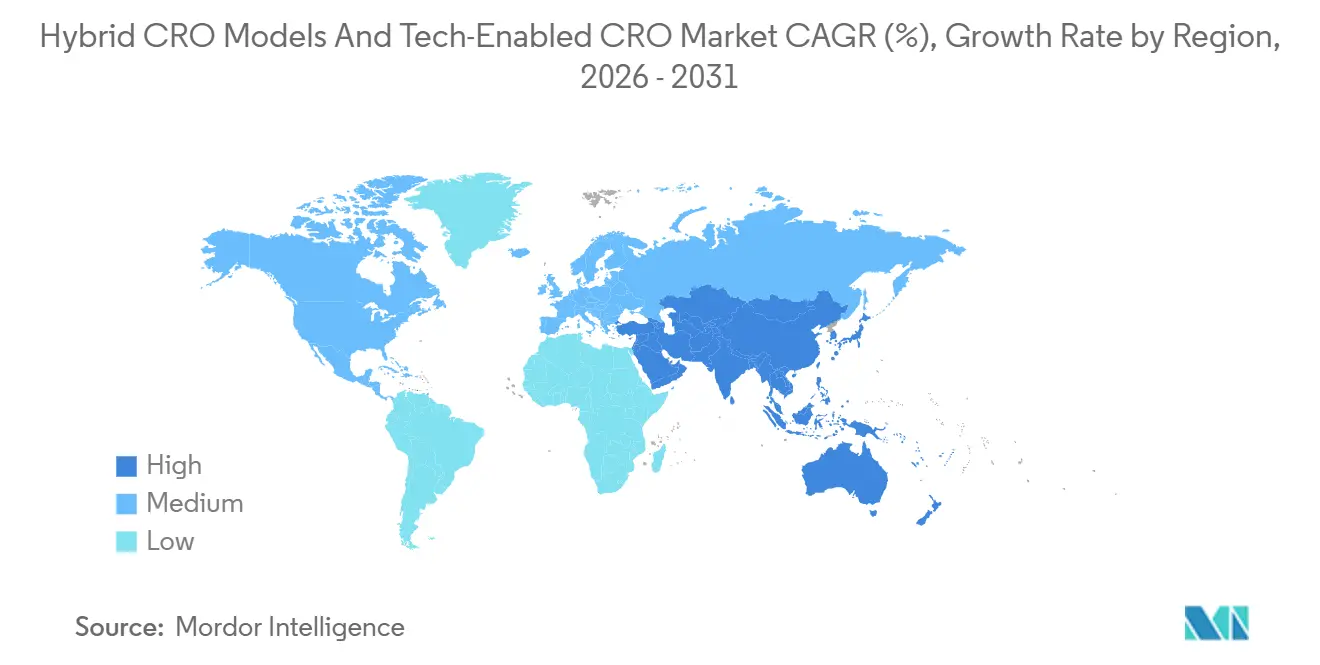

- By geography, North America accounted for 47.4% of the 2025 revenue, while Asia-Pacific is projected to grow at 10.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hybrid CRO Models And Tech-Enabled CRO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence & awareness of rare diseases | +1.8% | Global, strongest in North America and Europe | Medium term (2–4 years) |

| Regulatory incentives under Orphan-Drug statutes | +2.1% | North America and Europe, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Surge in gene- and cell-therapy pipelines | +2.4% | Global, led by North America | Medium term (2–4 years) |

| Rising outsourcing of complex orphan trials | +1.6% | Global | Long term (≥ 4 years) |

| AI-driven patient-matching registries | +1.2% | North America and Europe, early Asia-Pacific uptake | Medium term (2–4 years) |

| IRA-exemption expansion via OBBB Act | +0.7% | United States | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence & Awareness of Rare Diseases

Whole-genome sequencing costs have fallen below USD 600, enabling pediatric geneticists to detect ultra-rare disorders earlier and in greater numbers. The European Reference Networks diagnosed 47,000 new patients in 2025, up 22% from 2024, creating natural-history-study demand that hybrid CROs monetize through turnkey registry design [2]“European Reference Networks for Rare Diseases,” European Commission, europa.eu. The National Organization for Rare Disorders licenses digital phenotype databases to CROs, shrinking recruitment timelines from 14 to 8 months for indications with under 5,000 patients. Early diagnosis prompts sponsors to file investigational new-drug applications sooner, and AI engines that screen social-media references to undiagnosed symptoms are emerging, although EU privacy law confines deployment to anonymized data.

Regulatory Incentives under Orphan-Drug Statutes

The European Medicines Agency’s 2025 waiver of pediatric investigation plans for gene therapies shaved 18 months from development and validated simultaneous adult-and-pediatric decentralized enrollment. Japan expanded the Sakigake pathway to indications affecting fewer than 50,000 people, granting conditional approval to three gene therapies based on Phase II data and spurring telemedicine-based bridging studies. The FDA’s Complex Innovative Trial Designs pilot lets sponsors modify endpoints mid-study, but the privilege requires continuous cloud integration that only tech-enabled CROs provide.

Surge in Gene- & Cell-Therapy Pipelines

The FDA cleared 12 orphan-designated gene therapies in 2025, each subject to 15-year post-treatment surveillance that transforms registries into annuity revenue. Sponsors lack in-house vector-manufacturing quality control, so CROs now oversee GMP audits via IoT sensors that flag batch drift in real time. Chimeric antigen receptor T-cell trials require orchestration of apheresis, transduction, and cryopreservation across borders, tasks that classic site-centric models cannot handle without cloud supply-chain tracking.

Rising Outsourcing of Complex Orphan Trials

Sixty-eight percent of orphan studies were outsourced in 2025, up from 61% in 2023. Adaptive protocols demand rapid interim reading and real-time data fusion, capabilities that favor hybrid CROs with modular tech stacks. ICON’s hybrid offering, born of its PRA Health Sciences acquisition, won three gene-therapy contracts in 2025 by pairing in-hospital vector infusions with at-home wearable monitoring.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patient-recruitment scarcity & dispersion | -1.4% | Global, acute in rural North America and parts of Asia-Pacific | Long term (≥ 4 years) |

| High cost of multi-regional micro-cohort trials | -1.1% | Global, most severe in North America and Europe | Medium term (2–4 years) |

| Stringent ESG compliance for suppliers | -0.6% | Europe core, spreading to North America | Medium term (2–4 years) |

| Cross-border genomic-data privacy barriers | -0.8% | Europe and North America, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Patient-Recruitment Scarcity & Dispersion

Orphan trials average 87 enrollees worldwide and often need sites in 15 countries. Hybrid CROs cut median travel distance to 35 kilometers by deploying mobile nurses but still face in-person-baseline mandates in Germany and France, which dilute cost savings. AI validation of advocacy-registry entries halves screen-failure rates but adds six weeks of data cleaning.

High Cost of Multi-Regional Micro-Cohort Trials

Site activation runs USD 25,000–60,000 and small-cohort revenue fails to cover overhead; 40% of planned sites never enroll a patient. Hybrid CROs cluster infusions at academic hubs and move follow-up to virtual visits, slicing per-patient expense by 25%. China’s rule that 20% of participants be Chinese nationals pushes sponsors into tier-2 cities, forcing CROs to work with local tele-health firms to stabilize logistics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Biostatistics Automation Drives Fastest Growth

Data Management & Biostatistics grows at a 10.50% CAGR, the fastest in the Hybrid CRO Models & Tech-Enabled CRO market, because adaptive studies need continuous Bayesian re-estimation and dropout prediction. Clinical Trial Management still commands 55.6% of 2025 revenue, yet sponsors increasingly buy data-only or regulatory-only modules. Regulatory & Consulting uptake rises as companies navigate decentralized-trial guidance. Other Specialist Services thrive on FDA-mandated 15-year gene-therapy surveillance, locking CROs into decades-long registries.

Tech investment is shifting the margin from human monitoring to analytics. Mid-tier rivals embed machine-learning quality checks that spot protocol deviations in uploaded site videos, cutting on-site monitoring trips by 60% and bolstering the Hybrid CRO Models & Tech-Enabled CRO market’s scalability.

By Therapeutic Area: Neuroscience Gene Therapies Fuel Tech Adoption

Neuroscience posts a 10.38% CAGR on the back of spinal muscular atrophy, Duchenne, and Huntington gene-therapies entering pivotal studies and demanding 15-year wearable-enabled registries. Oncology still leads spending at 35.2% share, but CAR-T logistics drive decentralization and data-integration investments. Ophthalmology relies on smartphone acuity tests validated against clinic metrics, enabling remote follow-up for inherited retinal dystrophies. Cardiovascular and Metabolic segments grow steadily, aided by RNA-i therapies and NIH-funded micro-cohort grants. Each therapeutic domain feeds data-hungry workflows, reinforcing platform adoption throughout the Hybrid CRO Models & Tech-Enabled CRO market.

By Phase: Adaptive Phase I Designs Accelerate Platform Demand

Phase I advances at an 10.33% CAGR because seamless adaptive designs merge early-safety and dose-finding tasks. Phase III maintains 55.3% 2025 share but is shifting to hybrid follow-up visits that trim monthly site trips. FDA guidance allows endpoint changes mid-study, making cloud-native biostatistics non-negotiable. Post-marketing registries (Phase IV) rise as EMA conditional approvals require five-year real-world evidence, turning CRO platforms into lifecycle partners rather than episodic vendors.

By End-Users: Non-Profits Propel Hybrid Adoption

Non-profit & Government sponsors register an 10.48% CAGR, fueled by NIH grants that require CRO engagement for data-management and regulatory files. Academic institutions and advocacy foundations seek modular, sub-USD 5 million packages that hybrid CROs deliver. Pharma & Biotech firms still make up 72.1% of 2025 spend but are migrating to risk-sharing contracts tied to recruitment speed and data quality, reshaping revenue mechanics across the Hybrid CRO Models & Tech-Enabled CRO market.

Geography Analysis

Asia-Pacific is the fastest-growing region, advancing at a 10.62% CAGR and expected to lift its Hybrid CRO Models & Tech-Enabled CRO market share sharply by 2031. Growth stems from China’s 2025 decision to extend rare-disease priority-review vouchers to indications affecting fewer than 140,000 residents, which tripled the local orphan-drug pipeline and encouraged CROs to open tech-enabled units in Shanghai and Beijing. Japan’s Sakigake pathway, granting conditional approval on Phase II data, drew 18 multinational sponsors in 2025 and favors decentralized bridging studies that enroll patients through telemedicine, trimming per-patient costs by 30%. South Korea’s national registry of 62,000 rare-disease cases is now a recruitment engine for CROs that screen candidates remotely before activating physical sites. Australia’s fast-track orphan route accepts 70% foreign clinical evidence, making Sydney and Melbourne attractive hubs for sponsors seeking ethnic-diversity data ahead of U.S. filings.

North America retained 47.4% of 2025 revenue, giving the region the largest Hybrid CRO Models & Tech-Enabled CRO market size, yet sponsors are quickly shifting to decentralized methods after the FDA’s 2025 guidance formalized remote consent and telemedicine, provided video-verified exams prove equivalence. Canada’s streamlined orphan pathway cut approval times to 14 months and spurred 12 hybrid trials in Toronto and Montreal that rely on bilingual AI tools to screen French and English health records. Mexico granted nine orphan designations in 2025, and CROs now use mobile phlebotomy vans in Guadalajara and Monterrey while housing data teams in Houston and San Diego. The U.S. National Institutes of Health increased rare-disease grants to USD 180 million in 2025, each requiring a hybrid CRO partner for data and regulatory work.

Europe remains crucial because a single EMA filing opens 27 markets, but uneven reimbursement pushes CROs to connect trial data with insurance claims to guide launch plans. Germany’s 12-month fast-track review is concentrating trials in Munich and Berlin where registries already exist. The United Kingdom’s conditional-approval route prompted seven gene-therapy sponsors to run hybrid bridging studies that pair clinic-based vector infusions with at-home wearable monitoring. France still mandates one baseline site visit, so CROs toggle between on-site and virtual modes to preserve cost savings. Italy and Spain offer 30% lower investigator fees yet lag in diagnosis rates, pushing providers to mine prescription and genetic-testing databases for candidates. Brazil’s 14 new orphan designations in 2025 hint at rising sophistication, and local CROs in São Paulo and Rio are partnering with tele-health firms to install decentralized capabilities.

Competitive Landscape

The Hybrid CRO Models & Tech-Enabled CRO market is moderately concentrated: IQVIA, ICON, Parexel, Syneos Health, and Thermo Fisher PPD held significant market share. Each bolsters AI patient-matching, decentralized consent, and wearable integration to defend territory. IQVIA’s algorithm shaved 35% off recruitment in a 12-system pilot and now sells for USD 15,000 per enrolled patient. ICON’s USD 120 million Duchenne contract spans 45 sites and layers wearable gait sensors on top of site infusions [3]ICON Investor Relations, iconplc.com. Thermo Fisher PPD purchased 14 European registries to strengthen long-term surveillance.

Mid-tier innovators close gaps through vertical integration. Precision for Medicine monitors vector potency with ML models trained on 240 prior trials, reducing batch failure 22%, and Fortrea’s Japanese vector facility underpins Sakigake submissions. Vial raised USD 32 million to automate protocol-deviation detection via computer vision, cutting monitoring travel 60%. Post-marketing surveillance remains under-served; fewer than 10 CROs can sustain 15-year gene-therapy registries, leaving a lucrative niche for early movers.

Hybrid CRO Models And Tech-Enabled CRO Industry Leaders

IQVIA

ICON

Parexel

Syneos Health

Thermo Fisher PPD

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: IQVIA added at-home gene-therapy infusions for ultra-rare metabolic disorders through six U.S. nursing networks, pairing wearable vital-sign monitoring with remote physician oversight.

- December 2025: Thermo Fisher PPD acquired a European registry firm covering 85,000 lysosomal-disorder patients to offer wearable-enabled natural-history studies.

- November 2025: Fortrea partnered with a Japanese manufacturer for end-to-end gene-therapy trials and 15-year cloud registries targeting Sakigake approvals.

Global Hybrid CRO Models And Tech-Enabled CRO Market Report Scope

As per the scope of the report, hybrid CRO models blend the traditional site-based approach with decentralized elements, allowing sponsors to choose which services to outsource to a Contract Research Organization (CRO) and which to manage through specialized vendors. This approach often combines in-person visits for complex procedures with remote monitoring, telemedicine, and home-based data collection to reduce patient burden. Tech-Enabled CROs leverage advanced eClinical platforms, AI-driven analytics, and automated workflows to streamline trial management. These organizations replace manual, paper-based processes with digital tools like Electronic Data Capture (EDC), eConsent, and wearable devices for real-time monitoring.

The Hybrid CRO Models & Tech-Enabled CRO Market is segmented by service type, therapeutic area, phase, end-users, and geography. By service type, the market is categorized into drug development strategy, clinical trial management, data management & biostatistics, regulatory & consulting, and other specialist services. By therapeutic area, the market is divided into cardiovascular, neuroscience, ophthalmology, oncology, metabolic and other. By clinical phase, it is segmented into Pre-clinical, Phase I, Phase II, Phase III, and Phase IV and post marketing. By end-users, the segmentation includes pharma & biotech companies, non-profit & gov’t sponsors, academic & research institutes, and others. Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Drug Development Strategy |

| Clinical Trial Management |

| Data Managemet & Biostatistics |

| Regulatory & Consulting |

| Other Specialist Services |

| Cardiovascular |

| Neuroscience |

| Ophthalmology |

| Oncology |

| Metabolic & Other |

| Pre-clinical |

| Phase I |

| Phase II |

| Phase III |

| Phase IV & Post-marketing |

| Pharma & Biotech Companies |

| Non-profit & Gov’t Sponsors |

| Academic & Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Drug Development Strategy | |

| Clinical Trial Management | ||

| Data Managemet & Biostatistics | ||

| Regulatory & Consulting | ||

| Other Specialist Services | ||

| By Therapeutic Area | Cardiovascular | |

| Neuroscience | ||

| Ophthalmology | ||

| Oncology | ||

| Metabolic & Other | ||

| By Phase | Pre-clinical | |

| Phase I | ||

| Phase II | ||

| Phase III | ||

| Phase IV & Post-marketing | ||

| By End-Users | Pharma & Biotech Companies | |

| Non-profit & Gov’t Sponsors | ||

| Academic & Research Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Hybrid CRO Models & Tech-Enabled CRO market in 2026?

The Hybrid CRO Models & Tech-Enabled CRO market size is estimated to reach USD 17.82 billion in 2026, rising toward USD 28.56 billion by 2031.

Which service category is growing fastest?

Data Management & Biostatistics posts the quickest 10.50% CAGR through 2031 because adaptive studies need continuous analytics.

Why is Asia-Pacific growth outpacing other regions?

China’s expanded voucher program and Japan’s Sakigake pathway are spurring launches, driving a 10.62% CAGR in Asia-Pacific through 2031.

How does the OBBB Act influence hybrid CRO demand?

By extending price-negotiation exemptions, the Act reactivated dormant Phase III trials and boosted demand for cost-saving hybrid contracts.

What differentiates leading tech-enabled CROs?

AI patient-matching, wearable-sensor integration, and cloud registries that satisfy 15-year gene-therapy follow-up obligations are key.

Page last updated on: