Hyaluronic Acid Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

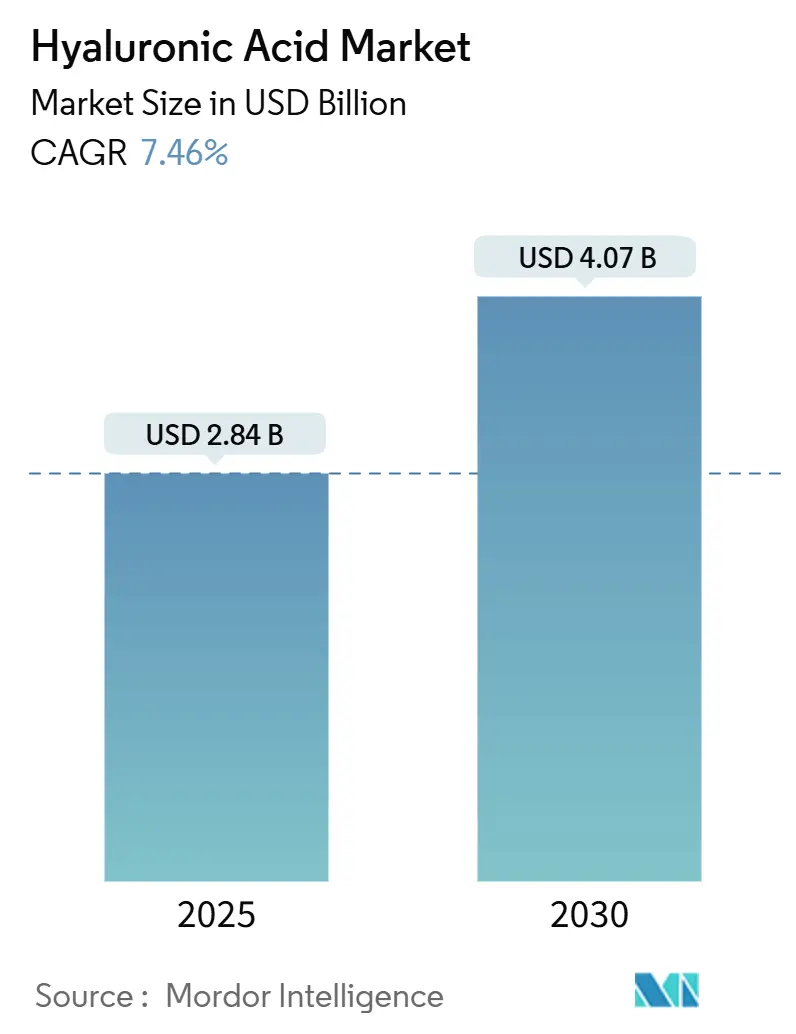

| Market Size (2025) | USD 2.84 Billion |

| Market Size (2030) | USD 4.07 Billion |

| Growth Rate (2025 - 2030) | 7.46% CAGR |

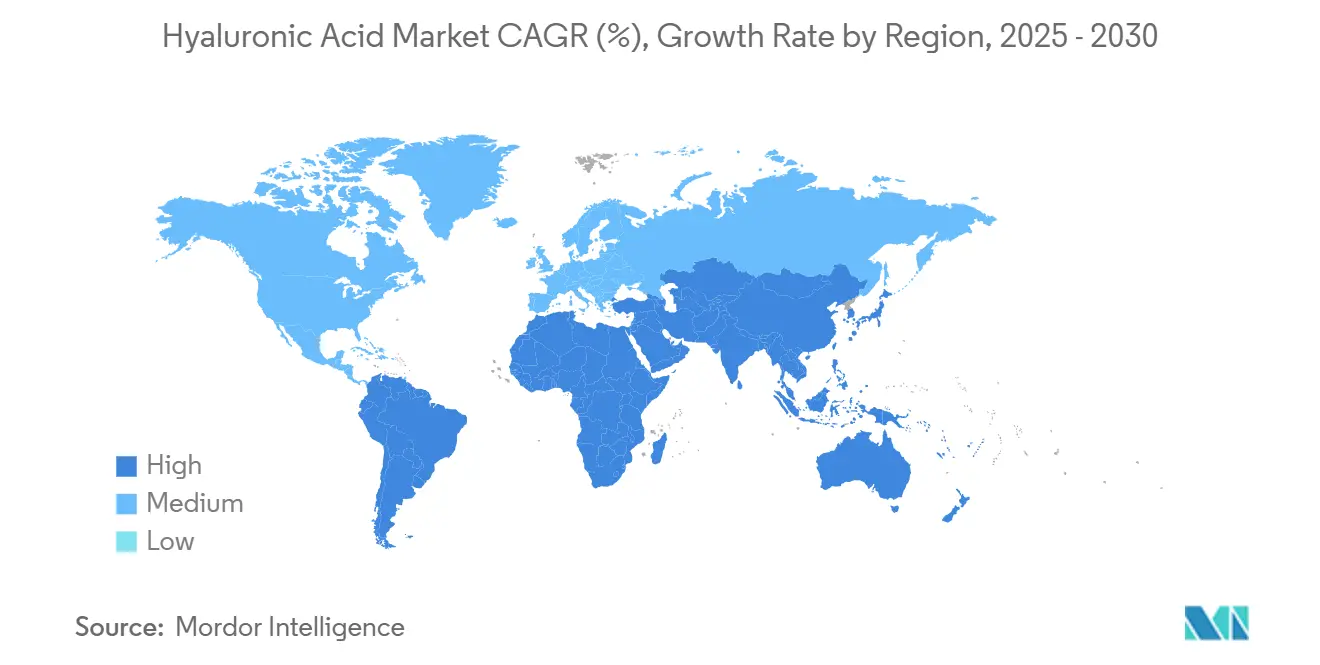

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Hyaluronic Acid Market Analysis by Mordor Intelligence

The hyaluronic acid products market size reached USD 2.84 billion in 2025 and is projected to attain USD 4.07 billion by 2030, translating to a 7.46% CAGR. This upward trajectory is driven by the increasing integration of aesthetic medicine with therapeutic applications, a steady influx of regulatory approvals for advanced formulations, and a shift in production technologies favoring non-animal fermentation methods. Industry players are strategically aligning cosmetic and medical applications to diversify and expand their revenue streams. Simultaneously, healthcare professionals are increasingly adopting multi-molecular-weight hyaluronic acid products, which are recognized for their enhanced ability to penetrate deeper skin layers and provide extended tissue retention. Strategic collaborations, such as L’Oréal’s acquisition of a 10% stake in Galderma, highlight the intensifying competition among market participants to secure innovative assets and maintain a competitive edge. The Asia-Pacific region emerges as a key growth driver, leveraging its large-scale manufacturing capabilities and the rising demand from urban populations. Furthermore, regulatory authorities in the region have accelerated their review and approval processes, effectively reducing the time required for product commercialization and enabling faster market entry.

Key Report Takeaways

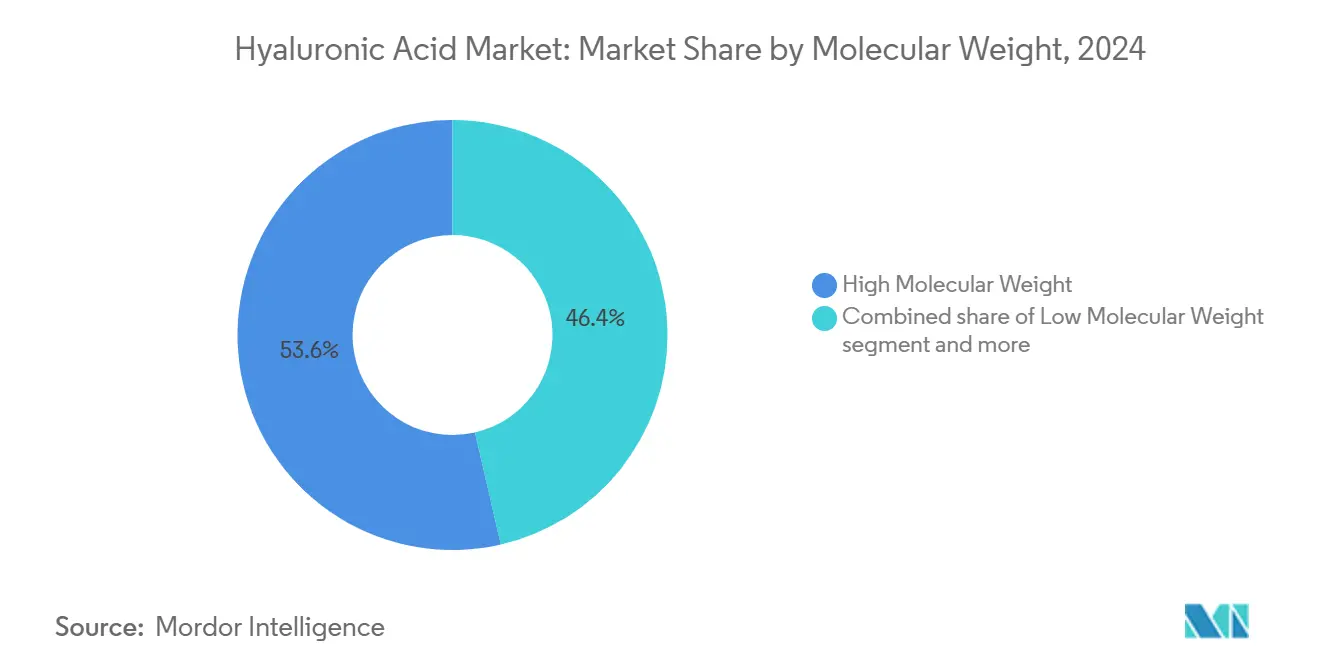

- By molecular weight, high-molecular products led with 46.44% of hyaluronic acid products market share in 2024, while ultra-low molecular variants are forecast to grow at 8.45% CAGR to 2030.

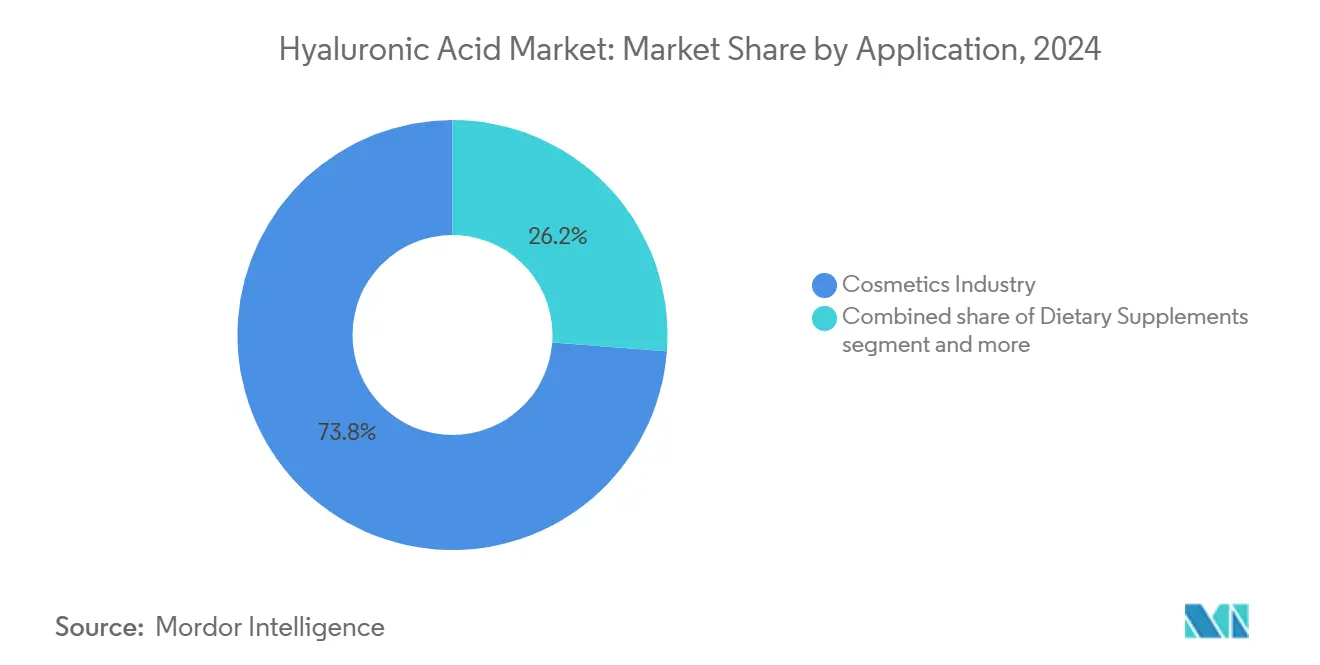

- By application, cosmetics retained 73.81% revenue share of the hyaluronic acid products market in 2024; the pharmaceutical segment is expanding at an 8.70% CAGR through 2030.

- By geography, Asia-Pacific held 46.08% of the hyaluronic acid products market in 2024 and is expected to register the fastest regional CAGR at 8.19% through 2030.

Global Hyaluronic Acid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for anti-aging solutions in skincare | +1.8% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Growing use in aesthetic dermatology and cosmetic injections | +2.1% | Global, led by Asia-Pacific urban centers | Short term (≤ 2 years) |

| Expansion in orthopedic applications | +1.2% | North America and Europe | Long term (≥ 4 years) |

| Oral hyaluronic acid supplements are gaining popularity for joint and skin health | +0.9% | Asia-Pacific core, expanding to North America | Medium term (2-4 years) |

| Demand for non-animal and vegan sources of hyaluronic acid | +0.7% | Global, early adoption in Europe | Long term (≥ 4 years) |

| Adoption in advanced drug delivery systems | +0.8% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for anti-aging solutions in skincare

Clinical studies have demonstrated that cross-linked hyaluronic acid injections effectively sustain fibroblast activation and collagen synthesis for up to a year, driving the market for scientifically validated anti-aging solutions. Shifting demographics are influencing demand trends, moving beyond traditional metrics of population aging. As of January 2024, the European Union reported a population of 449.3 million, with over 21.6% aged 65 and above[1]Source: European Commission, "Population structure and ageing" ec.europa.eu. Key suppliers, such as DSM-Firmenich, have launched trinary molecular-weight product lines designed to target specific dermal depths, enabling premium pricing strategies. Growing consumer preference for minimally invasive treatments has led companies to invest in multi-weight serums that complement in-clinic injectable procedures. Radiofrequency-enhanced endogenous HA stimulation has achieved a 67.69% increase in natural HA levels within three months, positioning device-cosmetic hybrids as a lucrative growth opportunity. Furthermore, rising disposable incomes in emerging markets are driving demand for high-performance anti-aging solutions.

Growing use in aesthetic dermatology and cosmetic injections

The aesthetic dermatology market is transitioning toward precision medicine, emphasizing advanced molecular engineering and clinical applications of hyaluronic acid fillers. The hyaluronic acid products market is experiencing growth, driven by FDA approvals for temple hollowing fillers and RHA technologies that replicate natural facial movements. Product development now focuses on rheological properties, such as G-prime strength and cohesivity, to ensure long-lasting structural support. Galderma’s Restylane SHAYPE exemplifies how next-generation gels meet these stringent performance criteria. Combination treatment protocols, with an 89% patient satisfaction rate, integrate multiple fillers in a single session to optimize aesthetic outcomes. These bundled services not only enhance practitioner revenue per visit but also increase product demand, accelerating market growth.

Expansion in orthopedic applications

The growing prevalence of osteoarthritis, particularly among the aging global population, is driving increased demand for hyaluronic acid in orthopedic applications. According to the Population Reference Bureau, in 2024, Japan and Monaco led the world in the percentage of their populations aged 65 and above, with Japan at 29% and Monaco at 36%[2]Source: Population Reference Bureau, "World Population Data Sheet 2024", prb.org. Aesthetic dermatology is shifting toward precision medicine, with greater emphasis on advanced molecular engineering and clinical applications of hyaluronic acid fillers. The hyaluronic acid products market is expanding, supported by FDA approvals for temple hollowing fillers and RHA technologies designed to replicate natural facial movements. Product innovation is now centered on rheological properties, such as G-prime strength and cohesivity, to deliver long-lasting structural support. Galderma’s Restylane SHAYPE exemplifies how next-generation gels are meeting these rigorous performance standards. Additionally, combination treatment protocols, achieving an 89% patient satisfaction rate, integrate multiple fillers in a single session to maximize aesthetic outcomes. These bundled services not only enhance practitioner revenue per visit but also drive product demand, accelerating market growth.

Demand for non-animal and vegan sources of hyaluronic acid

Non-animal fermentation methods effectively address both ethical concerns and contamination risks, offering a sustainable and innovative solution for the industry. Novozymes has introduced a Bacillus subtilis platform that eliminates the reliance on animal-derived ingredients and organic solvents. This advancement not only ensures cleaner product labeling but also streamlines the regulatory approval process, making it more efficient. In the European market, there is a growing consumer preference for vegan formulations, which has driven companies to reformulate their legacy product lines to align with this demand. As fermentation processes become more efficient, they generate significant cost savings, enabling price competitiveness with traditional extraction techniques. Additionally, the reduction in carbon emissions aligns with corporate sustainability goals, further increasing procurement interest from leading global cosmetics companies seeking environmentally responsible solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Allergic reactions and inflammation from consumption | -0.4% | Global, higher sensitivity in developed economies | Short term (≤ 2 years) |

| Regulatory challenges for oral HA supplements and claims | -0.6% | North America and Europe | Medium term (2-4 years) |

| Storage sensitivity and risk of microbial contamination | -0.4% | Global | Short term (≤ 2 years) |

| Challenges in combining with certain active ingredients | -0.5% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Allergic reactions and inflammation from consumption

A meta-analysis of 16 trials identified limited pain relief from intra-articular HA and highlighted systemic inflammatory markers, prompting healthcare providers to optimize patient selection strategies. FDA warnings regarding fillers contaminated with undisclosed diclofenac emphasized the critical need for enhanced supply chain oversight. In response, manufacturers like Contipro have invested in advanced endotoxin-removal filtration technologies to improve product purity. Additionally, personalized dosing algorithms are being developed to optimize efficacy and safety, supported by digital monitoring tools that track post-injection swelling and bruising. As surveillance systems evolve, real-world evidence will provide deeper insights into the actual incidence of adverse events, enabling data-driven evaluations of risk-benefit profiles to inform formulary decisions.

Regulatory challenges for oral HA supplements and claims

Fragmented regulations hinder cross-border scalability. The European Medical Devices Regulation requires extended post-market follow-up, increasing compliance costs for smaller innovators. In the U.S., delays in the GRAS pathway for sodium hyaluronate create uncertainty for food-grade applications. Inconsistent bioavailability testing standards complicate claim validation, pushing brands to adopt region-specific marketing strategies. To adapt, some companies are bundling HA with vitamins to position themselves in the nutraceutical market rather than focusing solely on therapeutic applications. While harmonization efforts may reduce these barriers in the long term, businesses planning near-term launches must prepare for diverse evidence requirements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Molecular Weight: Ultra-Low Variants Drive Innovation

In 2024, high-molecular products accounted for 46.44% of the hyaluronic acid market revenue, driven by their well-established applications in viscosupplementation and fillers. Meanwhile, ultra-low variants are gaining traction with an 8.45% CAGR, attributed to their superior dermal penetration and compatibility with nanoparticle carriers. Hybrid formulations, such as IBSA’s NAHYCO-based complexes, combine high and low molecular weights to restore facial volume while maintaining effective spreadability. Crosslink chemistries now enable post-production weight adjustments, providing manufacturers with flexible tools to optimize viscosity and degradation rates. The competitive landscape is increasingly focused on patent portfolios that protect proprietary depolymerization and crosslinking technologies.

Emerging clinical data is shaping product selection strategies. Studies indicate that polymer concentration and crosslink type significantly influence injectability force, impacting physician preferences. Regulatory authorities are now requiring rheology data in technical submissions, adding complexity to compliance processes. Companies offering multi-weight kits empower practitioners to customize treatments on-site, improving inventory efficiency and reducing patient chair time. As low-weight products continue to penetrate drug delivery pipelines, molecular-weight segmentation is expected to converge across therapeutic and cosmetic applications, unlocking broader revenue opportunities.

By Application: Pharmaceutical Segment Emerges as Growth Leader

In 2024, the cosmetics sector accounted for nearly 74.81% of the hyaluronic acid products market, primarily due to strong demand for daily-use serums and dermal fillers. Meanwhile, the pharmaceutical segment is set to grow significantly, with an 8.70% compound annual growth rate projected from 2025 to 2030. This growth is driven by expanding applications in areas such as orthopedics, dermatology, and oncology. Recent treatment approvals for conditions such as temple hollowing and cervical dystonia demonstrate a solid evidence-based approach, opening up opportunities for premium reimbursement. Additionally, advances in drug-delivery methods are utilizing hyaluronic acid as a carrier for cytotoxic drugs aimed at CD44-positive tumors, offering lucrative licensing opportunities.

Product innovation is also blurring traditional market boundaries. For instance, SkinMedica’s HA5 Hydra Collagen combines five types of hyaluronic acid with peptides, allowing it to be marketed in both cosmetic and clinical spaces. Although dietary supplements represent a smaller market segment, they are growing, especially in joint health, as alternatives like glucosamine see declining demand. Improvements in encapsulation technology that protect the active ingredients from stomach acid are increasing absorption, which supports health claims under dietary supplement regulations. This broad range of applications helps diversify the hyaluronic acid market and reduces dependency on any single sector.

Geography Analysis

In 2024, the Asia-Pacific region accounted for 46.08% of global revenue and is projected to grow at a CAGR of 8.19% from 2025 to 2030. This growth is driven by cost-efficient fermentation capabilities and the rapid urban adoption of injectable aesthetics. China, serving as a manufacturing hub, leads in hyaluronic acid production for cosmetics. According to China Customs, the export value of personal care and cosmetic products from China reached USD 7.2 billion in 2024[3]Source: China Customs, "Major Export Commodities in Quantity and Value", customs.gov.cn. Regional governments are supporting this growth through biotechnology incentives. For instance, South Korea increased its biomedical research and development funding by 15% for 2025, aiming to commercialize advanced HA derivatives. Bloomage Biotech exemplifies the region's shift from contract manufacturing to intellectual property-driven value creation, with over 520 patents and a supply network spanning more than 4,000 global brands. The competitive landscape is becoming more intense, as public disputes over labeling accuracy highlight stricter local regulatory oversight.

North America and Europe prioritize premium formulations supported by extensive clinical evidence. Regulatory changes, such as the FDA's drug reclassification proposal, create both challenges and opportunities for companies capable of managing lengthy trial processes. Products like Galderma's Restylane SHAYPE and AbbVie's JUVÉDERM VOLUMA XC Temple demonstrate region-specific innovations designed to address unique anatomical needs. Strategic partnerships, such as the Galderma-L'Oréal collaboration, enable co-marketing and shared technological advancements. While compliance costs under Europe's Medical Devices Regulation pose barriers for smaller firms, those that remain in the market benefit from reduced competition.

Emerging regions, including South America and the Middle East and Africa, are experiencing double-digit growth in procedures, although infrastructure constraints limit immediate volume expansion. LG Chem's launch of VITARAN in Thailand reflects a broader trend of multinational companies adapting their portfolios to local markets. These firms are also establishing regional depots to reduce lead times and navigate tariff complexities. As regulatory frameworks in these regions mature, the market is expected to transition from heavy import reliance to selective local manufacturing partnerships, further diversifying the global hyaluronic acid products market.

Competitive Landscape

The hyaluronic acid products market is moderately fragmented, characterized by the presence of established players like AbbVie Inc., Anika Therapeutics, Inc., Contipro a.s., Ferring B.V., and Galderma S.A., leading the industry through continuous innovation and strategic expansion. Companies are increasingly focusing on developing sustainable production methods, with white biotechnology and cell-free enzymatic technology emerging as key trends in manufacturing processes. The industry has witnessed a surge in product launches featuring multi-molecular hyaluronic acid formulations, particularly targeting the skincare and cosmetics segments.

Market leaders are strengthening their positions through vertical integration, from raw material sourcing to end-product manufacturing, while simultaneously expanding their geographical presence through strategic partnerships and facility establishments. Research and development investments have intensified, particularly in areas of ingredient purity, efficacy, and sustainable production methods.

Patent filings, targeting crosslink agents and molecular-weight manipulation, are establishing strong competitive barriers for innovators. With conglomerates aiming to address pipeline gaps, strategic mergers and acquisitions are anticipated. The evolving competitive landscape points to increasing entry barriers, favoring companies that effectively integrate manufacturing capabilities, intellectual property strength, and regulatory expertise.

Hyaluronic Acid Industry Leaders

-

AbbVie Inc.

-

Anika Therapeutics, Inc.

-

Contipro a.s.

-

Ferring B.V.

-

Galderma S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: Bloomage introduced its new product, MitoPQQ™, and highlighted its latest advancements in hyaluronic acid research at the 2024 IFT FIRST expo, a leading global event for food science professionals.

- May 2024: Galderma has launched Restylane VOLYME in China, leveraging its proprietary OBT gel technology. This product introduction focuses on mid-face contouring and volumization, targeting one of the fastest-growing aesthetics markets globally.

Global Hyaluronic Acid Market Report Scope

Hyaluronic acid, also known as hyaluronan (HA), is an organic compound that belongs to the branch of carbohydrates and polysaccharides. Hyaluronic acid plays a crucial role in retaining moisture, promoting tissue hydration, and lubricating joints. It also plays a crucial role in wound healing by controlling inflammation and redirecting blood flow to damaged tissue.

The Hyaluronic Acid market is segmented by Application into dietary supplements, pharmaceutical industry, and cosmetics industry, and by Geography it is segmented into North America, Europe, Asia-Pacific, and the Rest of the World. The market sizing has been done in value terms in USD for all the abovementioned segments.

| High Molecular Weight |

| Low Molecular Weight |

| Ultra Low Molecular Weight |

| Dietary Supplements |

| Pharmaceutical Industry |

| Cosmetics Industry |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Poland | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Molecular Weight | High Molecular Weight | |

| Low Molecular Weight | ||

| Ultra Low Molecular Weight | ||

| By Application | Dietary Supplements | |

| Pharmaceutical Industry | ||

| Cosmetics Industry | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Poland | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected value of the hyaluronic acid products market by 2030?

The market is forecast to reach USD 4.07 billion by 2030, reflecting a 7.46% CAGR.

Which region currently leads the hyaluronic acid products market?

Asia-Pacific leads with 46.08% revenue share thanks to robust manufacturing capacity and high procedure uptake.

Which segment is growing fastest within the market?

Pharmaceutical applications are advancing at an 8.70% CAGR because new therapeutic indications are winning regulatory approval.

Why are ultra-low molecular weight variants in high demand?

They offer superior dermal penetration and are integral to emerging drug-delivery systems, driving an 8.45% CAGR for the sub-segment.

Page last updated on: