Hungary Warehousing and Storage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

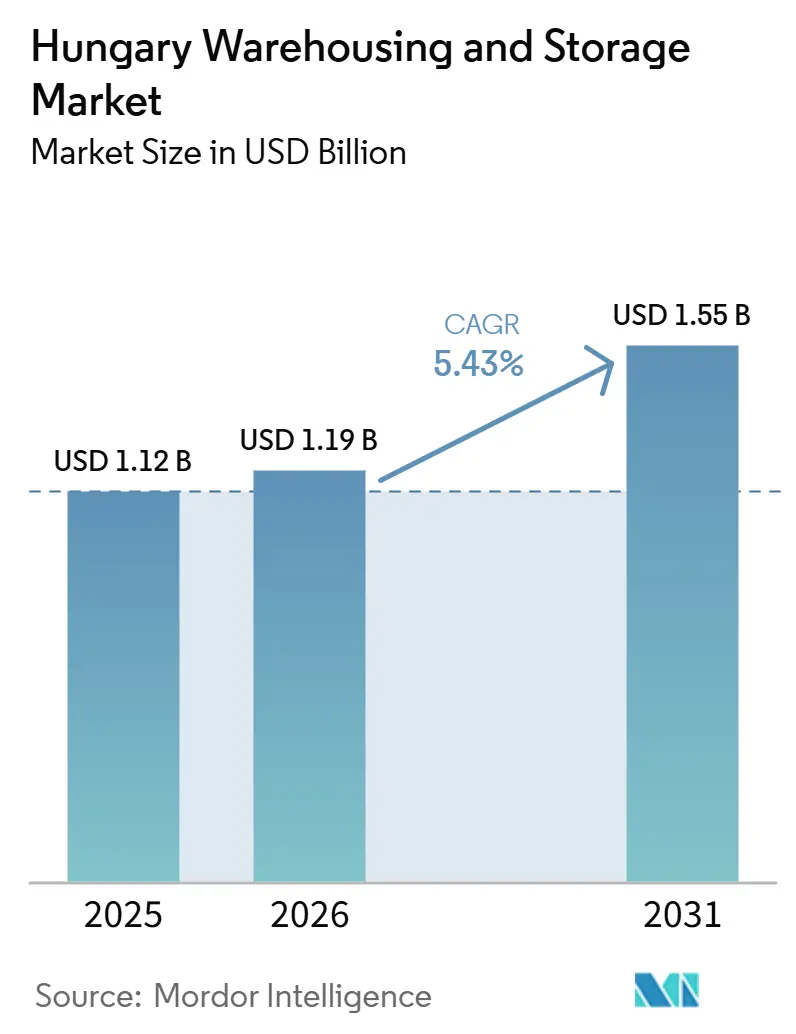

| Base Year Market Size (2025) | USD 1.12 Billion |

| Market Size (2026) | USD 1.19 Billion |

| Market Size (2031) | USD 1.55 Billion |

| Growth Rate (2026 - 2031) | 5.43% CAGR |

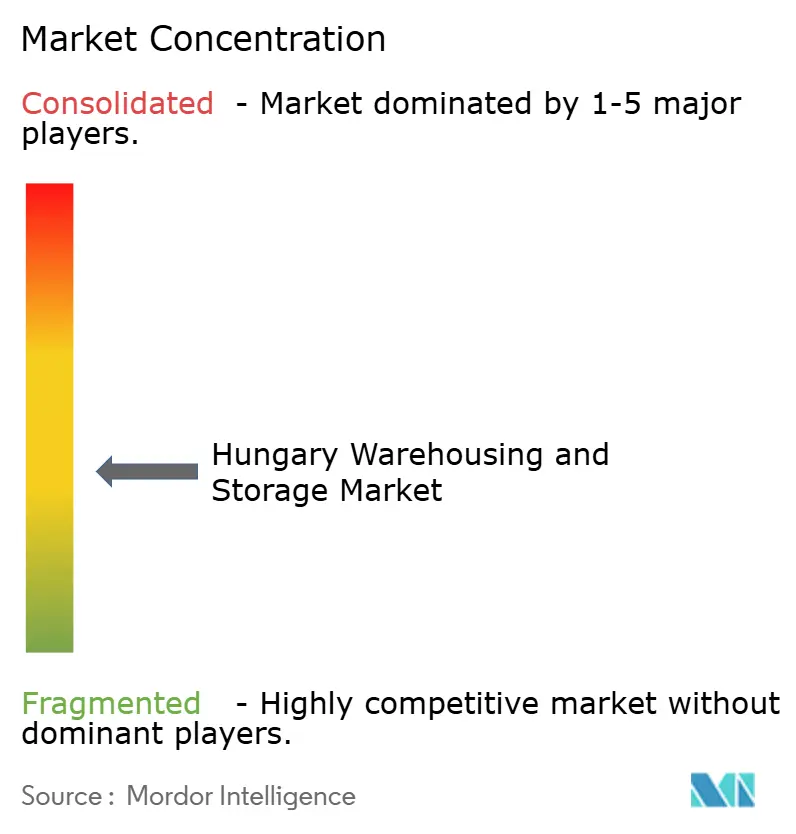

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hungary Warehousing and Storage Market Analysis by Mordor Intelligence

The Hungary warehousing and storage market size was valued at USD 1.12 billion in 2025 and is projected to expand to USD 1.19 billion in 2026 and to USD 1.55 billion by 2031, registering a CAGR of 5.43% between 2026 and 2031.

The current expansion is propelled by institutional capital inflows that fund speculative logistics projects, rapid adoption of automation that cuts unit-handling costs, and infrastructure upgrades that shorten cross-border transit times. Foreign pension funds now underwrite close to one-fifth of annual development activity, lured by net initial yields of 6% or more that outstrip Western European returns. At the same time, the commissioning of the Budapest-Belgrade rail corridor in 2025 positions Hungarian distribution centers as preferred transshipment nodes for Balkan and Western European freight.

Key Report Takeaways

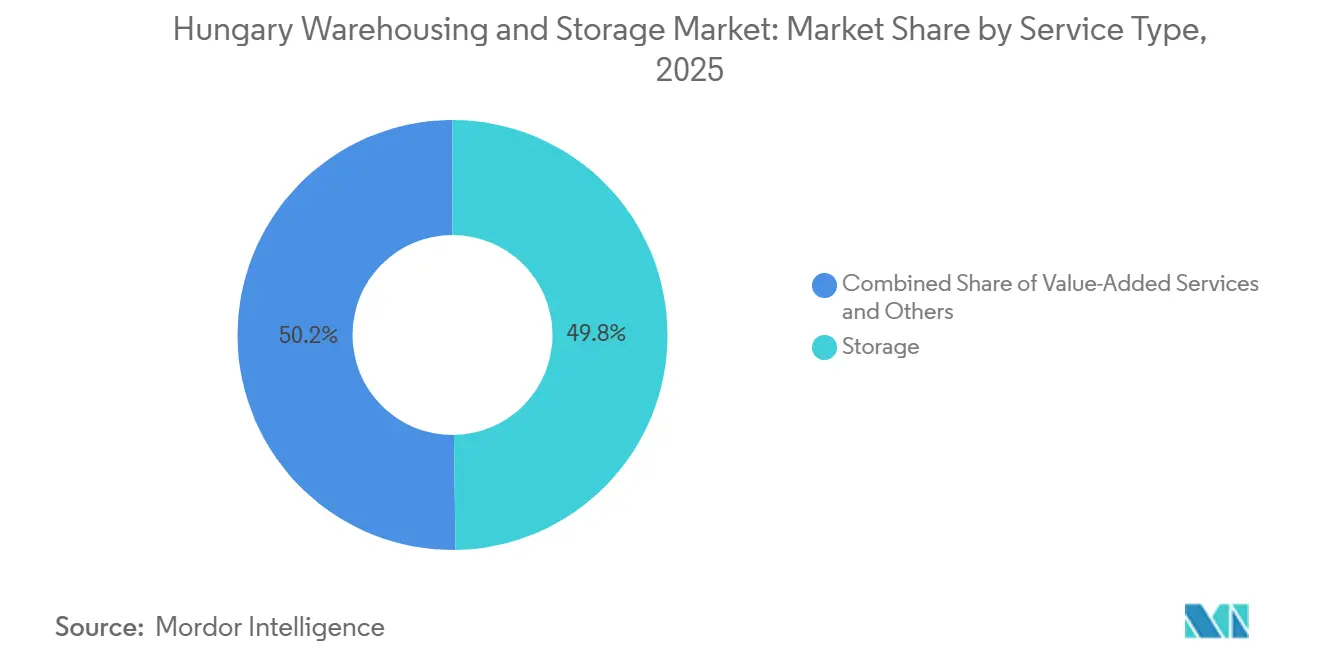

- By service type, storage accounted for 49.77% of the Hungary warehousing and storage market size in 2025, while value-added services and others are forecast to expand at a 8.64% CAGR through 2031.

- By warehouse type, general shared or multi-client facilities held 52.26% of the Hungary warehousing and storage market share in 2025, while bonded warehousing is projected to grow at 7.88% CAGR through 2031.

- By temperature control, non-temperature-controlled facilities accounted for 78.01% of the Hungary warehousing and storage market size in 2025, while temperature-controlled storage is projected to grow at 9.41% CAGR through 2031.

- By technology adoption, manual operations led with 54.69% of the Hungary warehousing and storage market share in 2025, while fully automated facilities are forecast to expand at 11.25% CAGR through 2031.

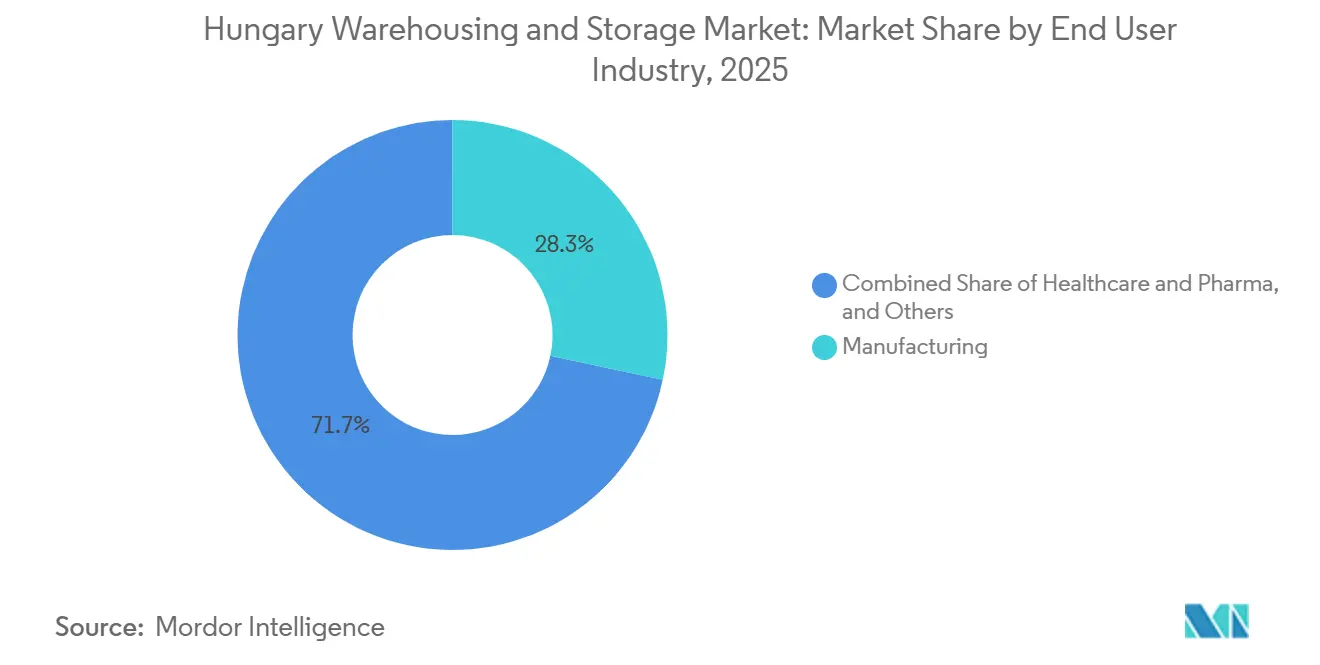

- By end user industry, manufacturing held 28.33% of the Hungary warehousing and storage market size in 2025, while healthcare and pharma is projected to grow at 10.17% CAGR through 2031.

- By geography, Central Hungary accounted for 56.87% of the Hungary warehousing and storage market share in 2025, while the Northern Great Plain is forecast to grow at 8.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Hungary Warehousing and Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Expansion of third-party grocery delivery platforms is spurring temperature-flexible fulfillment hubs | +1.3% | Budapest metropolitan area, Debrecen, Szeged, Győr | Short term (≤ 2 years) |

| EU sustainability incentives accelerating uptake of energy-positive, BREEAM-certified warehouses | +0.9% | National, concentrated in greenfield developments | Medium term (2-4 years) |

| Commissioning of the Budapest–Belgrade high-speed rail corridor, opening new south-eastern transit flows | +0.7% | Southern Hungary, particularly the Kecskemét-Szeged corridor | Long term (≥ 4 years) |

| Rapid adoption of autonomous mobile robots (AMRs) and high-bay AS/RS systems is reducing unit handling costs | +1.1% | National, with early adoption in the automotive and pharma sectors | Medium term (2-4 years) |

| Growth of urban micro-fulfillment centres inside the M0 ring to meet two-hour delivery expectations | +0.8% | Budapest within the M0 motorway ring | Short term (≤ 2 years) |

| Influx of foreign pension-fund capital is boosting speculative logistics real-estate supply | +0.6% | National, concentrated in Budapest, Győr, and Debrecen industrial zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Third-Party Grocery Delivery Platforms Spurring Temperature-Flex Fulfillment Hubs

The rapid growth of delivery platforms such as Wolt, Foodpanda, and Bolt Food is driving demand for advanced urban warehouses in Hungary, particularly multi-temperature facilities combining frozen, chilled, and ambient storage. These temperature-controlled warehouses command premium rents and benefit from energy-efficient climate systems, but high EU compliance costs create strong entry barriers. At the same time, overlapping grocery and pharmaceutical cold-chain needs improve year-round utilization. Rising expectations for fast delivery in cities like Budapest are further accelerating the development of near-city fulfillment centers[1]Statista, “Online Food Delivery – Grocery Delivery – Hungary,” statista.com.

EU Sustainability Incentives Accelerating Uptake of Energy-Positive, BREEAM-Certified Warehouses

Sustainability is increasingly shaping Hungary’s warehousing market, supported by the European Investment Bank's preferential financing for highly rated green buildings. While features like solar panels, water recycling, and EV charging raise upfront costs, they significantly reduce long-term operating expenses. Projects such as CTPark Budapest West highlight the efficiency gains of sustainable design. With national renewable energy targets and growing tenant demand for green facilities, sustainability is becoming a standard requirement, reinforcing premium valuations in the market.

Commissioning of the Budapest–Belgrade High-Speed Rail Corridor: Opening New South-Eastern Transit Flows

The development of the Budapest-Belgrade railway corridor is transforming Hungary’s logistics landscape by strengthening connectivity with South-Eastern Europe and elevating the importance of secondary cities such as Kecskemet and Kiskunfélegyhaza as cost-effective logistics hubs. Lower land costs and improved transport links are encouraging the formation of warehousing clusters near industrial bases, as seen with Mercedes-Benz’s major production facility in Kecskemet. This alignment of infrastructure and manufacturing is driving demand for cross-docking and transshipment facilities, positioning Hungary as a key gateway for trade flows between Western Europe and the Balkans.[2]European Investment Bank, “Climate Bank,” eib.org

Rapid Adoption of Autonomous Mobile Robots and High-Bay AS/RS Systems Reducing Unit Handling Costs

Automation is rapidly reshaping Hungary’s warehousing sector, driven by rising labor costs and faster returns on investment in robotic solutions. The adoption of autonomous mobile robots (AMRs) and high-bay automated storage and retrieval systems (AS/RS) enables warehouses to achieve greater vertical capacity, faster pallet movement, and significantly higher storage density than traditional racking. Facilities like DHL’s Hatvan site demonstrate the tangible benefits, including substantial reductions in labor hours and near-perfect inventory accuracy. Large third-party logistics providers can spread these investments across multiple sites, amplifying productivity advantages over smaller operators and reinforcing the role of automation in creating scale-driven efficiencies in the Hungarian logistics market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Grid-connection bottlenecks are delaying photovoltaic and EV-ready warehouse projects | -0.6% | National, acute in peri-urban zones outside Budapest, Győr, and Debrecen | Medium term (2-4 years) |

| Escalating municipal property taxes on logistics facilities located outside designated industrial zones | -0.4% | Municipalities surrounding Budapest, Győr, and Szeged | Short term (≤ 2 years) |

| Scarcity of SEVESO-compliant brownfield sites for chemical and hazardous-goods storage | -0.3% | National, particularly affecting Budapest and the Danube corridor | Long term (≥ 4 years) |

| Rising ESG reporting and certification costs are squeezing the margins of domestically-owned 3PL SMEs | -0.5% | National, disproportionately affecting operators with | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid-Connection Bottlenecks Delaying Photovoltaic and EV-Ready Warehouse Projects

Electricity grid constraints increasingly shape Hungary’s warehousing market, as developers face long wait times for high-capacity connections due to a backlog of applications, with logistics projects representing a significant share. Required contributions for grid reinforcement and mandatory EV-charging infrastructure add substantial upfront costs, putting pressure on thin-margin projects. To maintain operations, some developers rely on interim solutions such as diesel generators or phased solar installations, but these measures raise carrying costs and delay rental income. Together, these challenges are moderating the pace of new warehouse additions, highlighting the growing importance of energy planning in the country’s logistics sector.[3]Hungarian Energy and Public Utility Regulatory Authority, “Grid Connection Regulations,” mekh.hu

Escalating Municipal Property Taxes on Logistics Facilities Located Outside Designated Industrial Zones

Hungary’s warehouse development landscape is increasingly influenced by local tax policies, with municipalities imposing higher annual levies on properties outside designated industrial parks. In Budapest, this creates a significant cost differential between urban districts and zoned estates, driving competition for limited industrial land and inflating acquisition prices. As a result, speculative development on fringe plots has slowed, with new supply now concentrated within predictable, compliant zones. Operators established in these industrial parks benefit from a strengthened competitive position, but the fiscal pressures on developers temper overall growth in the warehousing market.[4]Hungarian Tax Authority, “Property Tax Regulations,” nav.gov.hu

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Value-Added Services Redefining Revenue Mix

Storage remained the largest service category, accounting for 49.77% of the Hungary warehousing and storage market size in 2025. That position reflected the heavy flow of general merchandise, automotive parts, and fast-moving consumer goods through the country’s main logistics parks. Distribution and inventory management remained in the middle of the mix because wholesale, retail, and manufacturing networks still needed high-volume stock to be positioned close to Budapest and the main motorway corridors. Value-added services and others are set to grow at a 8.64% CAGR through 2031, the fastest rate within this segmentation. That growth is tied to the rising use of kitting, labeling, co-packing, cross-docking, and returns processing inside multi-client fulfillment operations.

The revenue mix is changing because customers want more than pallet storage from their logistics partners. Large shippers now expect batch-level traceability, order integration, clearer carbon-related operating data, and basic handling. This creates a more durable client relationship than standard storage contracts and makes service bundles harder to replace. The Hungarian warehousing and storage industry is therefore shifting toward higher-value activities, where operators can defend margins through process depth rather than space alone.

By Warehouse Type: Bonded Facilities Emerge as Strategic Assets

General shared or multi-client warehousing, held 52.26% of the Hungary warehousing and storage market share in 2025. Shared facilities remained the largest format because many small and mid-sized shippers preferred variable-cost access to labor, racking, and transport links inside established parks. Dedicated contract warehousing continued to serve automotive and pharmaceutical clients that needed tailored layouts, controlled environments, and stable labor teams. Bonded warehousing will be the fastest-growing type with a 7.88% CAGR through 2031, even though it started from a smaller base. That growth reflects the rising customs and transit needs linked to the Budapest-Belgrade corridor and broader cross-border freight activity.

The segment also faces a high barrier to expansion because specialized compliance requirements are difficult to replicate across new sites. ADR Logistics’ SEVESO III upper-threshold bonded facility demonstrated the kind of hazardous goods and regulated storage capabilities that remain scarce in Hungary. As rail-linked transit and customs complexity increase, certified bonded capacity should become more valuable than general space. The Hungary warehousing and storage industry is therefore likely to see a wider gap between standard warehouse supply and highly regulated storage infrastructure.

By Temperature Control: Cold Chain Investment Expands Beyond Food

Non-temperature-controlled facilities accounted for 78.01% of the Hungary warehousing and storage market size in 2025, as most Hungarian warehouse stock still serves general cargo and standard industrial demand. Temperature-controlled storage is projected to grow at a 9.41% CAGR through 2031, making it one of the strongest expansion pockets in the market. Pharmaceutical GDP obligations, online grocery delivery, and tighter food traceability rules are all supporting that shift. HAVI Logistics commissioned a distribution center of nearly 18,500 m² at Alsonemedi in December 2025, including more than 3,600 m² of frozen space and a gas-free energy design. Dachser Hungary then added a 600 m² temperature-controlled food cross-dock at Kecskemét in June 2026 to improve daily service to Southern Hungary’s retail network.

Cold chain growth is expanding beyond food into pharmaceutical handling and healthcare distribution. These operations require continuous monitoring, stronger documentation, and more careful onboarding than standard dry storage. That raises the operating threshold for new entrants and gives experienced operators a stronger moat. In practice, the segment is growing not only because demand is rising, but also because the service standard is becoming increasingly difficult to meet.

By Technology Adoption: Automation Gap Creates Margin Divergence

Manual operations accounted for 54.69% of the Hungary warehousing and storage market share in 2025. Semi-automated facilities occupied the middle band and often relied on conveyors, basic warehouse management systems, and limited process digitization. Fully automated facilities are projected to expand at a 11.25% CAGR through 2031, the highest growth rate across all segmentation types. Gebruder Weiss reached full operational capacity at its autonomous Páty warehouse by July 2025, demonstrating that automated throughput can already operate at scale in Hungary. Jungheinrich also expanded an automated mobile robot system for Magyar Gomba in Demjen in March 2026, demonstrating that adoption was spreading into regional food production logistics and was no longer limited to Budapest-area hubs.

The gap between automated and manual assets is widening because productivity, labor intensity, and error rates now differ more clearly across facility types. Premium e-commerce, healthcare, and time-sensitive tenants are moving toward operators that can offer stable throughput and better traceability. Traditional clients in manufacturing and consumer goods still use manual or semi-automated space, but that base is becoming more price-sensitive. The Hungary warehousing and storage market is therefore splitting into a higher-margin automated tier and a lower-margin conventional tier.

By End User Industry: Pharma Growth Outpaces All Peers

Manufacturing accounted for 28.33% of the Hungary warehousing and storage market size in 2025 and remained the core anchor. Hungary’s automotive and electronics base continued to generate large sequencing, parts-handling, and finished-goods flows around production centers. Consumer goods, food, and beverages also accounted for a large share because national retail chains and their service providers maintained significant warehouse footprints along the main road network. Healthcare and pharma are the fastest-growing end-user segments with a 10.17% CAGR through 2031. Kuehne+Nagel opened a 2,000 m² GDP-compliant healthcare cross-dock in Budapest in January 2025 to strengthen its Central European LTL network for pharmaceutical logistics.

Growth in healthcare and pharma is being supported by supply chain reshoring, stricter storage rules, and rising demand for compliant cross-border distribution. Retail and e-commerce, even when smaller in site count, continue to push higher warehouse velocity and greater value-added service intensity. Other end-user groups, such as chemicals, energy, and construction materials, remain constrained by the scarcity of SEVESO sites and higher compliance costs. That keeps manufacturing in the lead today, but pharma is gaining ground faster than any other customer group in the Hungary warehousing and storage market.

Geography Analysis

Central Hungary accounted for 56.87% of the Hungary warehousing and storage market share in 2025. The region remained the country’s main warehouse cluster because the Greater Budapest corridor and the M0 orbital route concentrated most speculative supply and the highest-quality logistics parks. Annual gross take-up in Greater Budapest reached 667,490 m² in 2025, up 9% year over year, indicating that leasing demand continued even as more stock entered the market. The vacancy rate rose to 12.8% by Q4 2025, but net absorption of 155,150 m² in Q4 alone showed that users were still taking space and becoming more selective about quality. In practical terms, Central Hungary remains the control point for modern capacity, tenant choice, and certified building supply in the Hungary warehousing and storage market.

Western Transdanubia and Central Transdanubia formed the second logistics belt due to their access to the Austrian and Slovak borders and their links to the automotive bases in Gyor and Kecskemet. These regions attracted built-to-suit demand from automotive suppliers that needed sequencing, just-in-time flow management, and closer plant-side operations. Panattoni’s Mosonmagyarovar project captured this shift through a sustainability-led design featuring electric truck charging and a strong pre-leasing target before construction. Southern Transdanubia remained less developed, but CTP’s launch of a built-to-suit park in Pécs in 2026 showed that developers were beginning to test new regional footprints as Budapest-area land costs rose.

The Northern Great Plain will be the fastest-growing region with an 8.11% CAGR through 2031, supported by the Debrecen and Nyiregyhaza industrial cluster. BMW, CATL, and Samsung SDI related activity is raising demand for warehousing, sequencing, and in-plant logistics support across the region. Raben Group expanded its Debrecen site with a modern A-category facility in October 2025 that added food-grade, racked, and high-bay capability for the growing SME base. In the Southern Great Plain, Metrans selected Szeged for its next intermodal hub in February 2026, which reflected the freight value of Corridor X and rail connectivity toward Belgrade. Northern Hungary still served industrial warehousing linked to chemicals and basic materials, but limited SEVESO-compliant sites continued to restrict growth in hazardous goods capacity.

Competitive Landscape

The top five operators control about 38% of national capacity, placing the Hungary warehousing and storage industry in moderate-fragmented territory. Waberer’s 62.5% purchase of GySEV Cargo in 2025 broadened its rail-road integration and lowered customer logistics spend by up to 22% through intermodal routing. DHL, CEVA, and Raben deploy AMRs and high-bay automation, achieving labor-productivity uplifts above 40% that support 8%-12% rental premiums.

Institutional capital Blackstone, CTP, and HelloParks, among others, drove speculative completions to 340,000 m² in 2024, momentarily upping Budapest’s western-corridor vacancy to 8.2% but also furnishing high-spec stock that modern occupiers demand.

SEVESO-compliant hazardous-goods space remains a supply-constrained niche where incumbents Raben and Waberer’s extract 15%-22% premiums thanks to EUR 2-3.5 million (USD 2.34-4.10 million) up-front safety systems. SME 3PLs grapple with EUR 50,000-150,000 (USD 58,500-175,500) recurring ESG-compliance costs, creating acquisition targets for global providers seeking local footprints.

Hungary Warehousing and Storage Industry Leaders

Waberer’s Group

Raben Group

Prologis

CTP

DSV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: DSV Solutions Slovakia has renewed its lease for approximately 20,000 m² of modern warehouse space at Prologis Park Bratislava, reaffirming its continued presence at the site.

- December 2025: Weberer’s Group completed its first build-to-own warehouse development, a parcel logistics center covering approximately 25,000 square meters, for Magyar Posta.

- December 2025: Prologis entered into a physical Power Purchase Agreement (PPA) with ENGIE Zielona Energia, part of the ENGIE Group. Under the agreement, Prologis procured renewable electricity generated by ENGIE’s wind farms to power its logistics and industrial parks across Poland.

- November 2025: Dachser Hungary launched a direct Kecskemet-Sofia freight route. The company introduced a weekly direct groupage service from Kecskemet to Sofia, Bulgaria. This marked its second new direct route launched in 2025, following the Pilisvorosvar-Padova route in January, after Romania and Bulgaria joined the Schengen Area.

Hungary Warehousing and Storage Market Report Scope

| Storage |

| Distribution and Inventory Management |

| Value-Added Services and Others (Kitting, Labelling) |

| General Shared / Multi-client Warehousing |

| Dedicated Contract Warehousing |

| Bonded Warehousing |

| Non-Temperature Controlled |

| Temperature Controlled |

| Manual |

| Semi-automated |

| Fully Automated |

| Manufacturing |

| Consumer Goods |

| Food and Beverage |

| Retail and E-commerce |

| Healthcare and Pharma |

| Other End-user Industries |

| Central Hungary |

| Central Transdanubia |

| Western Transdanubia |

| Southern Transdanubia |

| Northern Hungary |

| Northern Great Plain |

| Southern Great Plain |

| By Service Type | Storage |

| Distribution and Inventory Management | |

| Value-Added Services and Others (Kitting, Labelling) | |

| By Warehouse Type | General Shared / Multi-client Warehousing |

| Dedicated Contract Warehousing | |

| Bonded Warehousing | |

| By Temperature Control | Non-Temperature Controlled |

| Temperature Controlled | |

| By Technology Adoption | Manual |

| Semi-automated | |

| Fully Automated | |

| By End User Industry | Manufacturing |

| Consumer Goods | |

| Food and Beverage | |

| Retail and E-commerce | |

| Healthcare and Pharma | |

| Other End-user Industries | |

| By Region | Central Hungary |

| Central Transdanubia | |

| Western Transdanubia | |

| Southern Transdanubia | |

| Northern Hungary | |

| Northern Great Plain | |

| Southern Great Plain |

Key Questions Answered in the Report

What is the size of warehousing and storage in Hungary in 2026?

The Hungary warehousing and storage market is estimated at USD 1.19 billion in 2026 and is projected to reach USD 1.55 billion by 2031 at a 5.43% CAGR.

Which service category leads revenue in Hungary?

Storage was the largest service type in 2025 with 49.77% of revenue, reflecting the country’s role in general merchandise, automotive, and FMCG flows.

Which warehouse format is growing the fastest?

Bonded warehousing is the fastest-growing warehouse type with a 7.88% CAGR through 2031, supported by rising customs complexity and corridor traffic.

Why is Central Hungary so important for warehouse demand?

Central Hungary held 56.87% of revenue in 2025 because Greater Budapest and the M0 corridor concentrate modern stock, tenant demand, and transport connectivity.

What is driving automation in Hungarian warehouse operations?

Fully automated facilities are projected to grow at 11.25% CAGR through 2031 because operators are seeking better throughput, lower handling costs, and more reliable service levels.

Which customer group is expanding the fastest?

Healthcare and pharma is the fastest-growing end-user segment with a 10.17% CAGR through 2031, driven by GDP-compliant storage needs and stronger regional pharmaceutical logistics demand.

Page last updated on: