Human Platelet Lysate Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

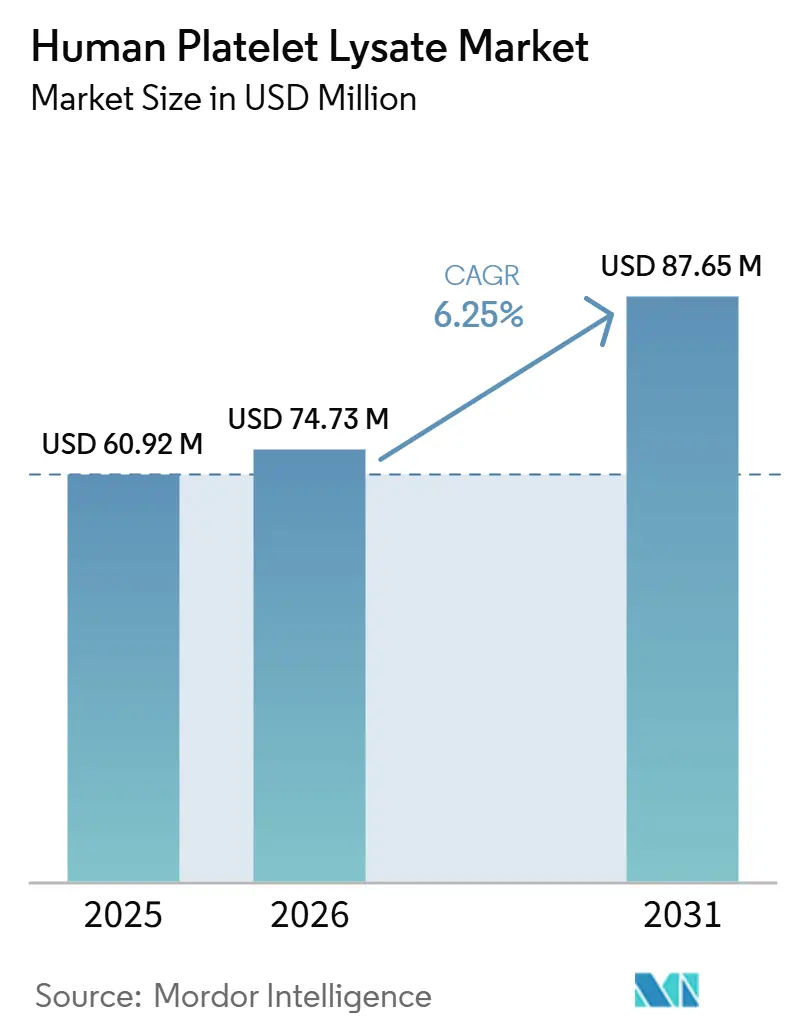

| Market Size (2026) | USD 74.73 Million |

| Market Size (2031) | USD 87.65 Million |

| Growth Rate (2026 - 2031) | 6.25% CAGR |

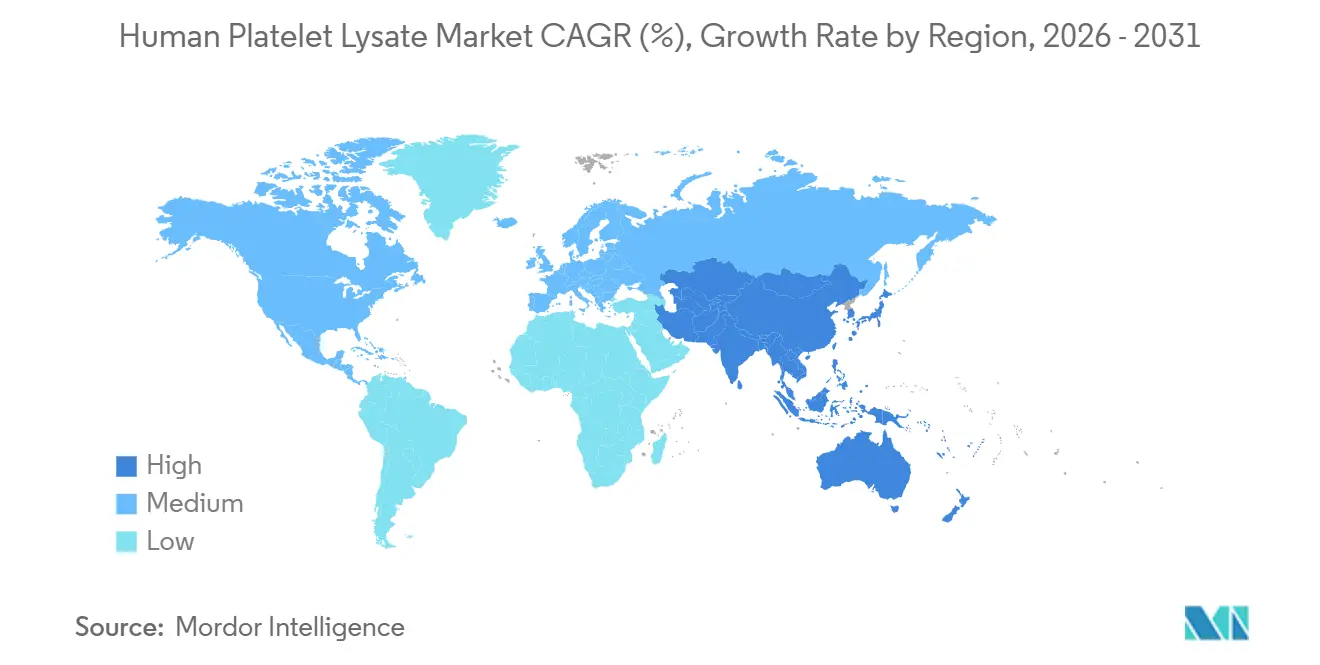

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

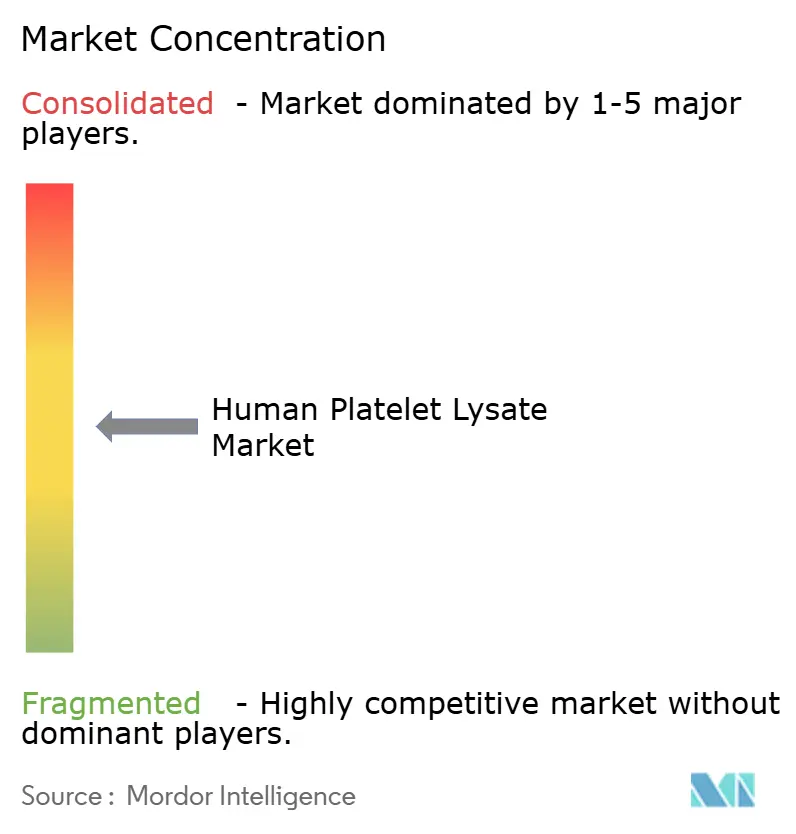

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Human Platelet Lysate Market Analysis by Mordor Intelligence

The Human Platelet Lysate Market size was valued at USD 60.92 million in 2025 and is estimated to grow from USD 74.73 million in 2026 to reach USD 87.65 million by 2031, at a CAGR of 6.25% during the forecast period (2026-2031).

The human platelet lysate market is advancing as clinical manufacturing teams shift away from fetal bovine serum and prioritize xeno-free materials aligned with regulatory expectations in advanced therapy production. Demand is rising as the gene, cell, and RNA therapy pipeline remains large, supporting the use of human-derived cell culture supplements across clinical and commercial manufacturing. The market is shifting toward controlled products with pathogen reduction, traceability, and stronger release documentation, giving established suppliers an advantage in regulated programs. Supply remains tight, but developments in leukoreduction filter recovery and lyophilized processing may ease raw material and logistics constraints over time.

Key Report Takeaways

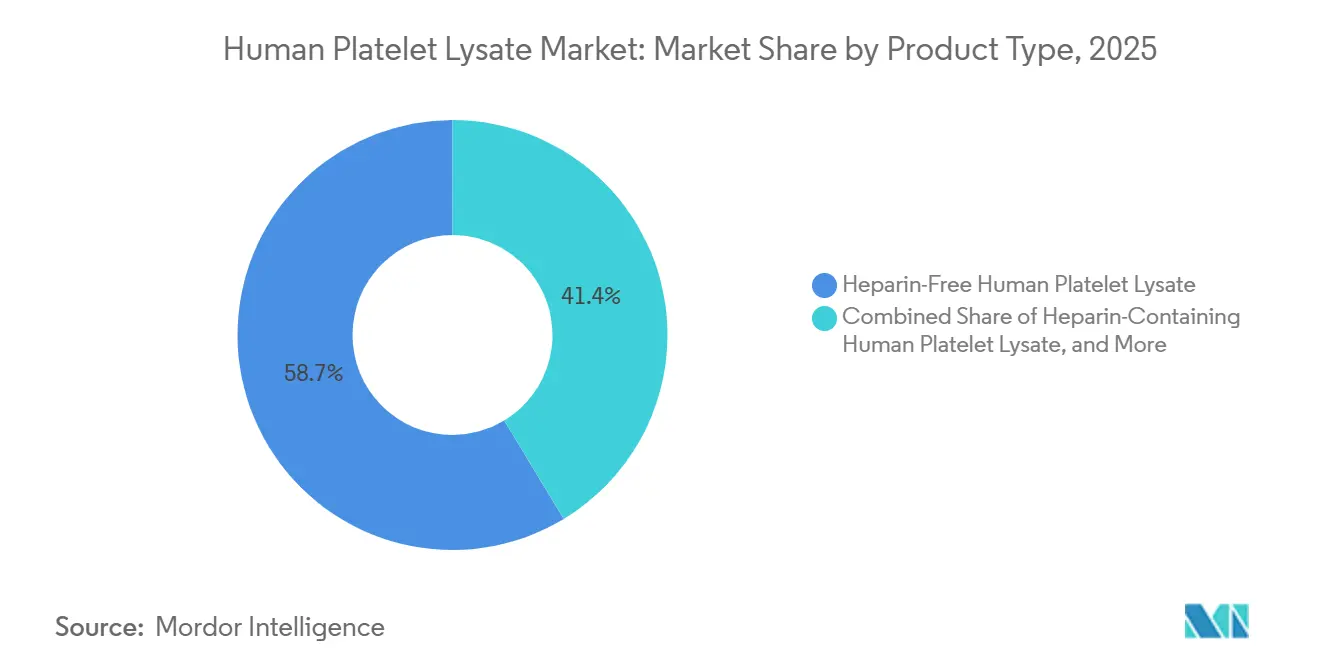

- By product type, heparin-free formulations led with 58.65% revenue share in 2025, while heparin-containing HPL is projected to expand at an 8.93% CAGR through 2031.

- By source, platelet-rich plasma captured 55.23% of revenue in 2025, while whole blood-derived platelets are projected to grow at a 9.67% CAGR through 2031.

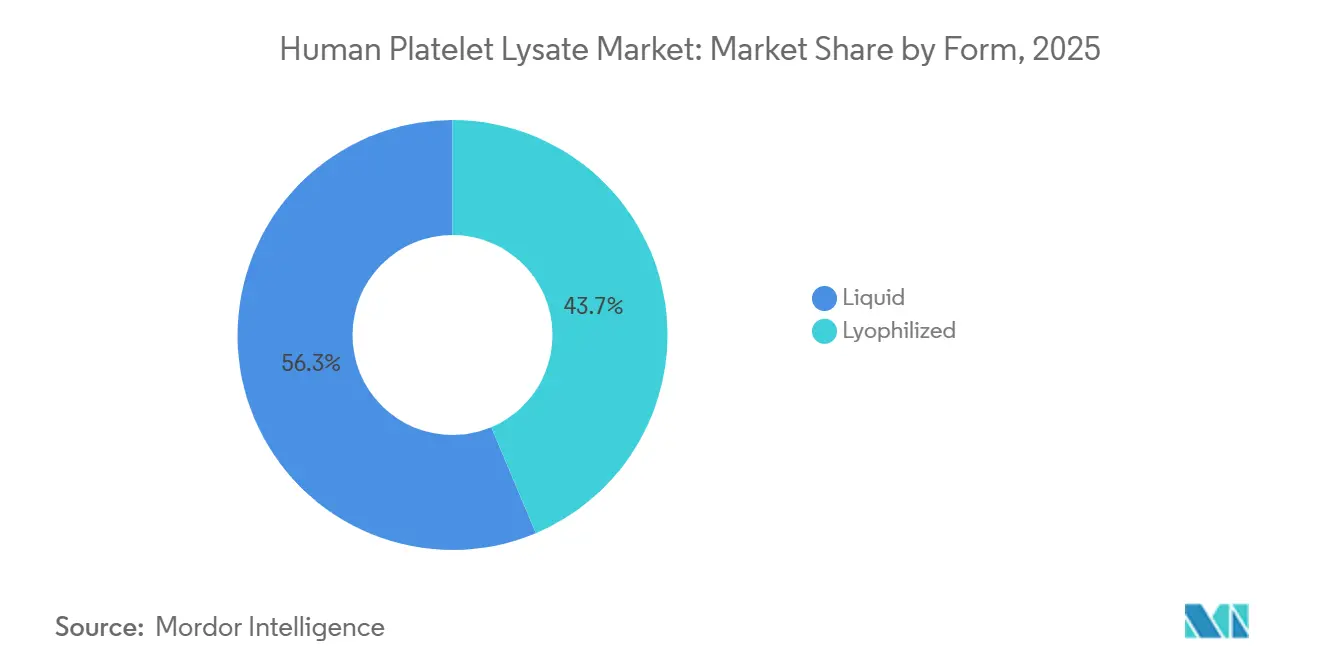

- By form, liquid HPL held 56.34% of revenue in 2025, while lyophilized HPL is expected to advance at an 8.35% CAGR through 2031.

- By application, cell and gene therapy manufacturing accounted for 42.88% of revenue in 2025, while tissue engineering is projected to record the fastest CAGR at 9.78% through 2031.

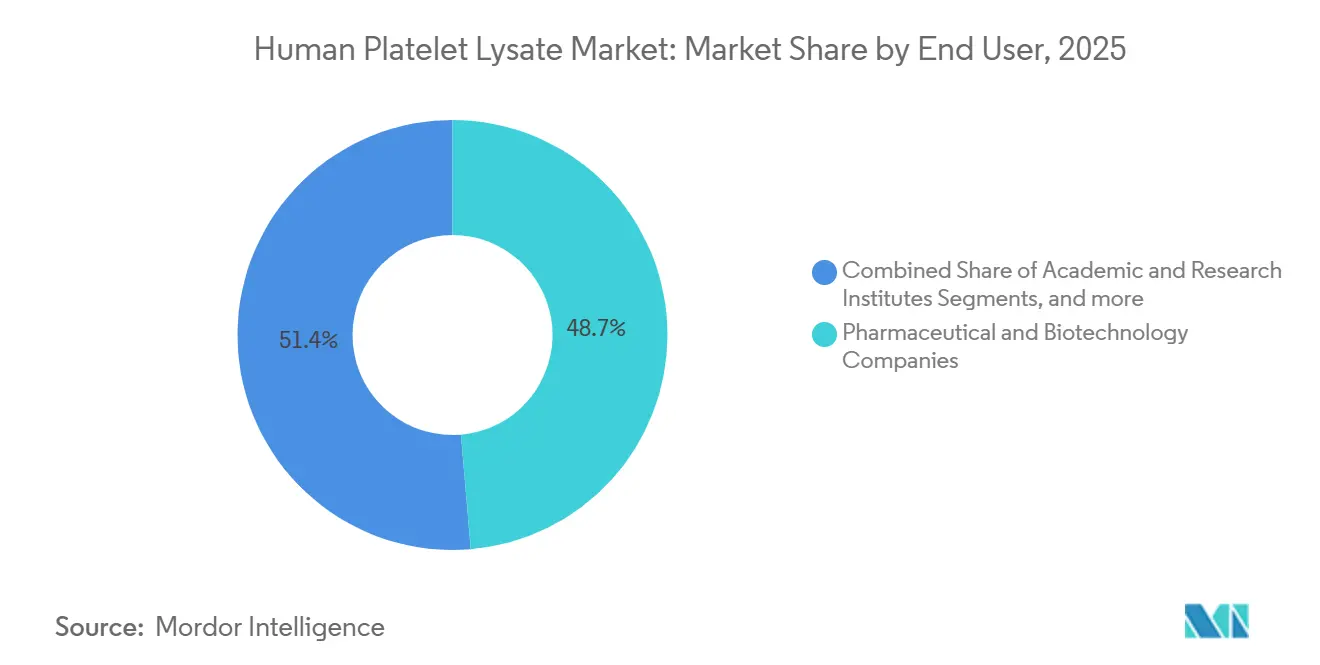

- By end user, pharmaceutical and biotechnology companies held 48.65% of revenue in 2025, while hospitals and cell therapy centers are expected to grow at an 8.76% CAGR through 2031.

- By geography, North America commanded 40.56% of revenue in 2025, while Asia-Pacific is projected to expand at an 8.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Human Platelet Lysate Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

| Rising shift from fetal bovine serum to xeno-free hPL | +1.8% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Growing cell and gene therapy manufacturing pipeline | +1.5% | North America, Asia-Pacific, and Europe | Medium term (2-4 years) |

| Expansion of GMP-grade, donor-traceable platelet lysate products | +1.2% | North America and Europe | Medium term (2-4 years) |

| Recycling of expired platelet units and leukoreduction filters | +0.8% | Global, with early adoption in Europe and Japan | Long term (≥ 4 years) |

| Decentralized cell therapy manufacturing increases demand for closed, standardized supplement supply | +1.2% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Shift From Fetal Bovine Serum to Xeno-Free Human Platelet Lysate

The human platelet lysate market gained support from the steady shift away from fetal bovine serum in clinical and regulated cell culture applications. Manufacturers faced increasing pressure to use human-derived supplements, as these materials aligned more closely with safety and traceability expectations for advanced therapy production. A 2026 review in Frontiers in Toxicology reported that more than 1,180 distinct cell lines had already been cultured under serum-free conditions by late 2025, showing that this transition was no longer limited to a narrow group of mesenchymal stem cell programs. This trend expanded demand beyond early HPL use cases.[1]ASGCT and Citeline, “Gene, Cell, & RNA Therapy Landscape Report Q4 2025,” American Society of Gene & Cell Therapy, asgct.org Manufacturers seeking approvals across multiple regions also benefited when starting materials aligned with xeno-free expectations, as this reduced documentation friction during regulatory review.

Growing Cell and Gene Therapy Manufacturing Pipeline

The scale of the gene, cell, and RNA therapy development pipeline also supported growth in the human platelet lysate market. The ASGCT and Citeline landscape report showed 4,164 gene, cell, and RNA therapies in development as of Q4 2025, keeping upstream media and supplement demand tied to a large active project base. As more programs advanced into Phase II and Phase III, manufacturers found it harder to change raw materials because later-stage manufacturing required tighter process control and more complete documentation. This trend supported suppliers that maintained Drug Master Files or similar regulatory packages, as customers could reference existing data instead of rebuilding support files.

Expansion of GMP-Grade, Donor-Traceable Platelet Lysate Products

The human platelet lysate market became more specification-driven as suppliers moved beyond simple pooled supplements and offered products with stronger GMP positioning. Pathogen reduction, gamma irradiation, donor traceability, and detailed release records became more important as buyers prioritized materials that integrated smoothly into clinical manufacturing files. PL BioScience launched ELAREM Ultimate-FD PLUS in April 2025 as a gamma-irradiated, GMP-grade HPL produced in Europe. The company positioned the product as xeno-free, fibrinogen-depleted, and anticoagulant-free for clinical cell manufacturing applications. These features reduced additional validation work for customers and shifted supplier selection from price comparisons toward total compliance cost, release confidence, and ease of regulatory integration. This also raised barriers for new entrants that offered lower prices but lacked comparable documentation depth or a clinical manufacturing track record.

Recycling of Expired Platelet Units and Leukoreduction Filters

The human platelet lysate market also benefited from initiatives that expanded the usable platelet input base beyond traditional expired platelet concentrates. Conventional HPL production relied on expired platelet units, creating a natural constraint as improved blood bank inventory control reduced the number of units that expired. Research published in Stem Cell Research and Therapy in 2025 showed that HPL produced from leukoreduction filter contents supported mesenchymal stem cell expansion at a clinically relevant scale using automated bioreactors, confirming discarded filter material as a useful secondary source.[2]H. Meng et al., “Exploring Ethical, Sustainable and Effective Foetal Bovine Serum Alternatives for In Vitro Mammalian Cell Culture,” Frontiers in Toxicology, frontiersin.org This expanded the effective raw material pool without requiring additional donor recruitment.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Batch-to-batch variability and donor heterogeneity | -0.6% | Global | Short term (≤ 2 years) |

| Limited supply of platelet starting material and compliance constraints | -0.5% | Global, most acute in Asia-Pacific emerging markets | Medium term (2-4 years) |

| Complex GMP release, documentation, and quality-control burden for blood-bank-derived inputs | -0.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Batch-to-Batch Variability and Donor Heterogeneity

The human platelet lysate market continues to face quality consistency challenges because donor platelet profiles vary across collections. Variations in growth factors, such as PDGF-AB, PDGF-BB, FGF, and VEGF, can create measurable lot-to-lot differences, complicating process development for customers that require stable media performance across clinical batches. A 2025 study reported that donor pools of 16 still showed meaningful growth factor variation and recommended larger pools of 20 to 24 donors to improve batch stability.[3]K. Wendland et al., “Lyophilized Human Platelet Lysate, Manufacturing, Quality Control, and Application,” Frontiers in Cell and Developmental Biology, doi.org This issue affects the human platelet lysate market because smaller manufacturers and academic groups may lack regular access to enough donations to achieve these pool sizes. It also increases the workload for product characterization, release testing, and customer qualification, especially for processed formats such as lyophilized HPL, where manufacturers must prove that reconstitution preserves expected biological performance with consistent results for regulated use.

Limited Supply of Platelet Starting Material and Compliance Constraints

The human platelet lysate market also remains constrained by the finite availability of its starting material, which depends closely on blood collection and blood bank handling practices. Improved blood inventory management reduces waste, but it can also reduce the supply of expired platelet concentrates that have traditionally supported HPL production. This creates a business challenge, as stronger blood banking systems can improve healthcare efficiency while tightening feedstock availability for HPL suppliers. The human platelet lysate market also faces constraints from varying release and documentation standards across major jurisdictions, including the FDA, the EMA framework, and Japan's PMDA-related requirements cited in supplier positioning materials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Heparin-Free Formulations Lead, Heparin-Containing Scales Fast

Heparin-free formulations held 58.65% of the human platelet lysate market share in 2025, showing strong buyer preference for products that support fully anticoagulant-free workflows in clinical settings. This leadership reflected rising demand for materials that aligned more clearly with xeno-free declarations and avoided complications associated with the downstream use of animal-derived heparin.

Heparin-containing HPL remained important in the human platelet lysate industry because many research groups and some manufacturing programs continued to use established protocols built around this format. This installed base explained why the segment remained commercially meaningful, even though heparin-free products led current revenue. At the same time, heparin-containing HPL is projected to expand at a CAGR of 8.93% during 2026-2031, showing that growth is not limited to the clinically preferred format. Some CDMOs and development programs continued to favor validated workflows over immediate reformulation, especially when heparin suppliers and media systems had already been qualified.

By Source: Platelet-Rich Plasma Leads, Whole Blood-Derived Gains Momentum

Platelet-rich plasma was the leading source in 2025 with 55.23% of segment revenue, supported by its ability to deliver high platelet concentration per collection unit. In the human platelet lysate market, this made PRP attractive because stronger platelet density could improve growth factor yield per liter and support efficient production economics at scale. PRP also fit well in regions with advanced automated apheresis systems and mature blood establishment controls, strengthening its position in advanced manufacturing networks. Single-donor traceability provided another practical advantage when buyers required clear documentation and easier linkage between the collected unit and the finished supplement batch.

Whole blood-derived platelets were the fastest-growing source category and are projected to expand at a CAGR of 9.67% through 2031, indicating a broader sourcing shift within the human platelet lysate market. Their momentum came from blood banking networks that improved buffy coat processing and used standard whole blood donations more effectively for downstream platelet recovery. This source route could lower per-unit collection costs because it used platelet fractions recovered from standard donation flows instead of relying only on dedicated apheresis sessions. The cross-border standardization study published in Stem Cell Research and Therapy in 2025 also supported the viability of pooled donor material across multiple institutions, strengthening the case for broader procurement models.

By Form: Liquid Dominates, Lyophilized Advances Across Logistics-Constrained Markets

Liquid HPL commanded 56.34% of the human platelet lysate market size in 2025, reflecting its long-standing use in validated cell expansion workflows. Buyers continued to prefer liquid products because their growth factor profile was familiar, and many clinical development files were originally built around liquid HPL specifications. In the human platelet lysate market, this created strong process inertia because changing the format often required compatibility testing, internal validation, and additional regulatory support. Liquid products also suited organizations with reliable cold-chain infrastructure, freezer capacity, and standard operating procedures for frozen or refrigerated handling.

Lyophilized HPL is projected to grow at a CAGR of 8.35% through 2031, reflecting strong demand for longer shelf life and easier logistics in the human platelet lysate market. Frontiers in Cell and Developmental Biology reported in 2025 that lyophilization preserved HPL quality across growth factor concentrations, mesenchymal stem cell proliferation behavior, and differentiation capacity, addressing a key technical concern around freeze-drying. This evidence supported wider use in settings where cold-chain costs, storage space, and shipment timing created barriers to liquid product adoption.

By Application: Cell Therapy Manufacturing Anchors Demand, Tissue Engineering Accelerates

Cell and gene therapy manufacturing accounted for 42.88% of the human platelet lysate market size in 2025, confirming its role as the main volume anchor for current demand. The segment held this position because manufacturers already used HPL in workflows tied to mesenchymal stem cells, CAR-T programs, and T-cell expansion under GMP-oriented manufacturing systems. In the human platelet lysate market, this created steady purchasing patterns because once a supplement became part of a regulated process, switching became difficult and usually occurred only when an alternative offered a clear technical or compliance benefit.

BioLife Solutions reported in Q1 2026 that its HPL products were embedded in four commercially approved CGT therapies and referenced in more than 35 active clinical trials, illustrating how deeply HPL was tied to production activity in this application area. This level of integration meant demand in this segment depended not only on research activity but also on late-stage manufacturing and commercial supply needs.

By End User: Pharma and Biotech Lead, Hospitals Post Fastest Growth

Pharmaceutical and biotechnology companies held 48.65% of the human platelet lysate market share in 2025, reflecting their central role in advanced therapy manufacturing and clinical development. These buyers typically treated HPL as a specification-linked raw material rather than a routine lab consumable, which changed how they made purchasing decisions. In the human platelet lysate market, suppliers that won this customer group often retained the relationship for long periods because switching could trigger new qualification work and add risk to production schedules.

Hospitals and cell therapy centers are projected to grow at a CAGR of 8.76% through 2031, indicating a gradual shift toward more decentralized treatment and manufacturing models. These settings became more important where point-of-care or hospital-linked therapy workflows were being developed in fields such as orthopedics, hematology, and oncology. Terumo Blood and Cell Technologies entered a strategic collaboration with Steminent Biotherapeutics in May 2026 to advance late-stage clinical manufacturing readiness for MSC-based therapies using automated expansion systems, supporting the operational model these end users needed.

Geography Analysis

North America accounted for 40.56% of the human platelet lysate market size in 2025, making it the largest regional contributor. The region led due to the United States’ strong base of commercially approved CGT products, specialized CDMOs, and GMP-oriented research institutions. Suppliers benefited from established ancillary material qualification and documentation practices within customer procurement systems. BioLife Solutions stated in Q1 2026 that it held more than a 70% share in U.S. commercially sponsored clinical trials and nearly 80% of more than 30 active Phase III programs, while Canada supported the region through academic medical center networks and Mexico remained at an earlier adoption stage.

Europe remained a key center for production innovation and supply standardization in the human platelet lysate market. In July 2025, PL BioScience opened its new GMP headquarters in Aachen, Germany, spanning more than 1,200 m² and capable of producing up to 20,000 liters of GMP-grade HPL annually. The United Kingdom, France, Belgium, and the Netherlands supported regional standardization through blood establishment networks. A 2025 multicenter study across Belgium, the Netherlands, and France showed that cross-border HPL standardization was practical when institutions aligned around shared methods.

Asia-Pacific is projected to grow at a CAGR of 8.56% through 2031, making it the fastest-growing regional segment of the human platelet lysate market. China’s biopharmaceutical expansion, South Korea’s organized CGT distribution structure, and India’s broader import diversification are supporting growth. In April 2026, ExcellaTherapeutics signed a distribution agreement with PL BioScience to supply ELAREM Ultimate-FD PLUS in South Korea, strengthening high-specification HPL distribution in North Asia. Japan adds a compliance-driven market layer, while South America and the Middle East and Africa remain at earlier adoption stages, with Brazil and GCC countries standing out as promising demand centers.

Competitive Landscape

The human platelet lysate market shows moderate concentration, with a small group of specialized suppliers controlling a large share of the clinical-grade revenue base. Dedicated HPL companies such as PL BioScience, BioLife Solutions, Mill Creek Life Sciences, AventaCell BioMedical, Compass Biomedical, and STEMCELL Technologies play central roles by competing on formulation quality, regulatory support, and application fit. Larger life science groups such as Sartorius through Biological Industries, Lonza, and Thermo Fisher Scientific also participate, but they compete mainly through distribution reach and workflow integration. Companies with regulatory filings, pathogen-reduced or gamma-irradiated product lines, and documented performance in GMP-relevant cell types hold the strongest positions, making it difficult for new entrants to move beyond research-grade products or small pilot demand.

Several strategic moves in 2025 and 2026 showed that competition in the human platelet lysate market shifted toward capacity, product differentiation, and supply control. PL BioScience launched ELAREM Ultimate-FD PLUS in April 2025 as a gamma-irradiated, GMP-grade HPL product with xeno-free and anticoagulant-free positioning, strengthening its high-specification product offering. The company announced a major site expansion in Aachen in July 2025, adding scale and supporting a two-source GMP supply strategy to improve resilience against production disruptions. PL BioScience also entered a patent license and assignment agreement with Macopharma in 2025, transferring Macopharma's HPL customer relationships into PL BioScience's supply network and accelerating installed base expansion.

The human platelet lysate market also has a clear innovation race around future supply models. PL BioScience and DewCell Biotherapeutics signed a Letter of Intent in May 2025 to jointly develop artificial human platelets for scalable animal-free HPL production, and the collaboration included a filed patent for the artificial HPL production process. If this approach reaches practical GMP use, it could ease the donation-linked supply constraints that still shape much of the human platelet lysate market. Incumbents still hold an advantage because buyers value regulatory files, quality records, and proven use in advanced therapy workflows.

Human Platelet Lysate Industry Leaders

Mill Creek Life Sciences LLC

Merck KGaA

STEMCELL Technologies Inc.

PL BioScience GmbH

Compass Biomedical, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: ExcellaTherapeutics signed a distribution agreement with PL BioScience to supply ELAREM Ultimate-FD PLUS GMP-grade HPL in South Korea, expanding PL BioScience’s presence in North Asia’s CGT market.

- July 2025: PL BioScience opened a 1,200+ m² GMP headquarters in Aachen, Germany, with capacity to produce up to 20,000 liters of GMP-grade HPL annually.

- May 2025: PL BioScience and DewCell Biotherapeutics signed a Letter of Intent to develop artificial human platelets for scalable, animal-free HPL production, building on an earlier Memorandum of Understanding.

- April 2025: PL BioScience launched ELAREM Ultimate-FD PLUS, a globally patented gamma-irradiated, GMP-grade HPL produced in Europe for clinical cell manufacturing and ATMP applications.

Global Human Platelet Lysate Market Report Scope

As per the scope of the report, Human Platelet Lysate (hPL) is a liquid solution made from human blood platelets. It is created by freezing and thawing platelets to break them open. This process releases growth factors, special proteins that signal cells to grow and repair tissue, making hPL a powerful tool in medicine and science.

The human platelet lysate market is segmented by product type, source, form, application, end user, and geography. By product type, the market includes heparin-free human platelet lysate, heparin-containing human platelet lysate, and pathogen-reduced human platelet lysate. By source, the market is segmented into apheresis platelets, whole blood-derived platelets, and platelet-rich plasma. By form, the market is segmented into liquid and lyophilized. By application, the market is categorized into cell and gene therapy manufacturing, regenerative medicine, research and drug discovery, tissue engineering, and vaccine development. By end user, the market is segmented into pharmaceutical and biotechnology companies, academic and research institutes, contract research organizations and CDMOs, and hospitals and cell therapy centers. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Heparin-Free Human Platelet Lysate |

| Heparin-Containing Human Platelet Lysate |

| Pathogen-Reduced Human Platelet Lysate |

| Apheresis Platelets |

| Whole Blood-Derived Platelets |

| Platelet-Rich Plasma |

| Liquid |

| Lyophilized |

| Cell and Gene Therapy Manufacturing |

| Regenerative Medicine |

| Research and Drug Discovery |

| Tissue Engineering |

| Vaccine Development |

| Pharmaceutical and Biotechnology Companies |

| Academic and Research Institutes |

| Contract Research Organizations and CDMOs |

| Hospitals and Cell Therapy Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Heparin-Free Human Platelet Lysate | |

| Heparin-Containing Human Platelet Lysate | ||

| Pathogen-Reduced Human Platelet Lysate | ||

| By Source | Apheresis Platelets | |

| Whole Blood-Derived Platelets | ||

| Platelet-Rich Plasma | ||

| By Form | Liquid | |

| Lyophilized | ||

| By Application | Cell and Gene Therapy Manufacturing | |

| Regenerative Medicine | ||

| Research and Drug Discovery | ||

| Tissue Engineering | ||

| Vaccine Development | ||

| By End User | Pharmaceutical and Biotechnology Companies | |

| Academic and Research Institutes | ||

| Contract Research Organizations and CDMOs | ||

| Hospitals and Cell Therapy Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving demand for human platelet lysate in advanced therapies?

Demand is being driven by the shift away from fetal bovine serum, a large pipeline of 4,164 gene, cell, and RNA therapies in development as of Q4 2025, and the need for xeno-free materials in regulated manufacturing.

How large is the human platelet lysate space by 2031?

The human platelet lysate market size stands at USD 74.73 million in 2026 and is projected to reach USD 87.65 million by 2031 at a CAGR of 6.25%.

Which product format leads current revenue?

Heparin-free formulations led product revenue with a 58.65% share in 2025, while liquid HPL led the form segment with 56.34% share in the same year.

Which application area is most important today?

Cell and gene therapy manufacturing held 42.88% of revenue in 2025, making it the main demand anchor for current purchasing and validation activity.

Which region offers the strongest near-term growth?

Asia-Pacific is projected to grow at an 8.56% CAGR through 2031, supported by biopharmaceutical expansion in China, South Korea, and India.

What is the biggest operational challenge for suppliers?

The main challenge remains the balance between limited platelet starting material, batch-to-batch variability, and the need to meet different regulatory documentation standards across key markets.

Page last updated on: