HR Chatbot And Virtual Assistant Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

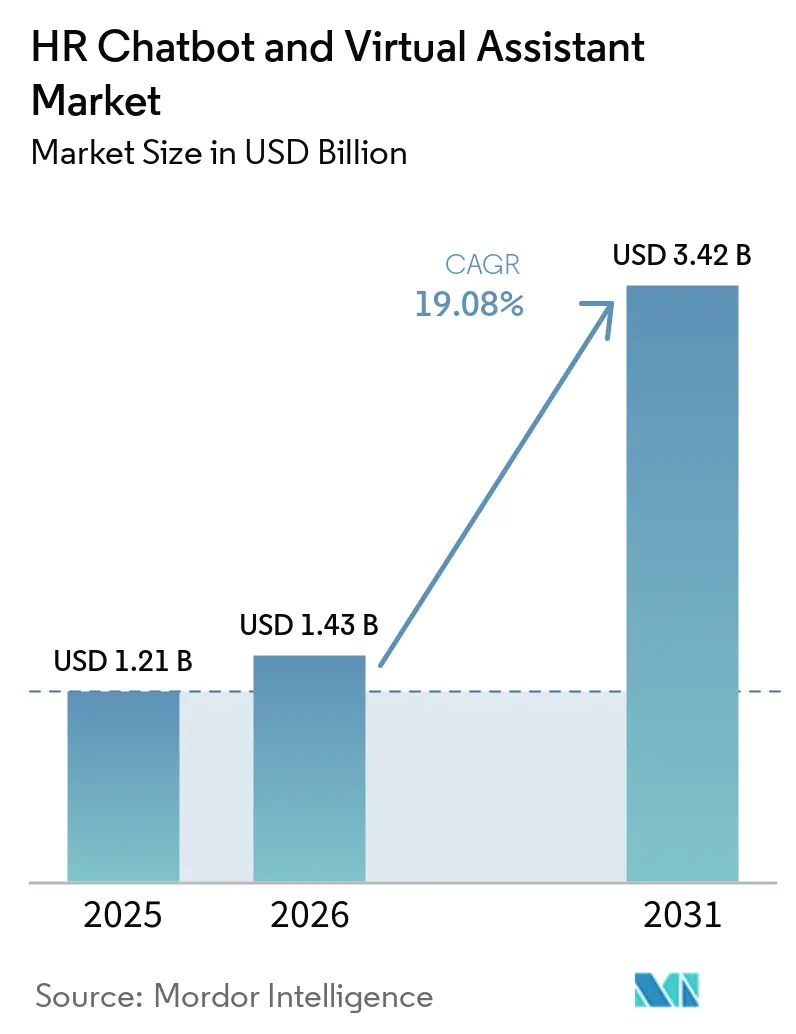

| Market Size (2026) | USD 1.43 Billion |

| Market Size (2031) | USD 3.42 Billion |

| Growth Rate (2026 - 2031) | 19.08% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HR Chatbot And Virtual Assistant Market Analysis by Mordor Intelligence

The HR Chatbot and Virtual Assistant market size is expected to increase from USD 1.21 billion in 2025 to USD 1.43 billion in 2026 and reach USD 3.42 billion by 2031, growing at a CAGR of 19.08% over 2026-2031. This expansion reflects employers’ shift toward conversational AI that now screens applicants, answers benefits queries, and conducts wellness check-ins that once consumed 70% of HR staff hours. Consolidation among enterprise software giants, such as Workday and ServiceNow, is accelerating adoption because buyers trust deeply integrated tools. Demand is reinforced by strict bias-audit rules in the United States and the European Union that require auditable logs, encouraging enterprises to favor chatbots with built-in compliance controls. At the same time, multilingual capabilities are unlocking untapped labor pools across Asia-Pacific and the Middle East, solidifying the technology’s role in global talent strategies.

Key Report Takeaways

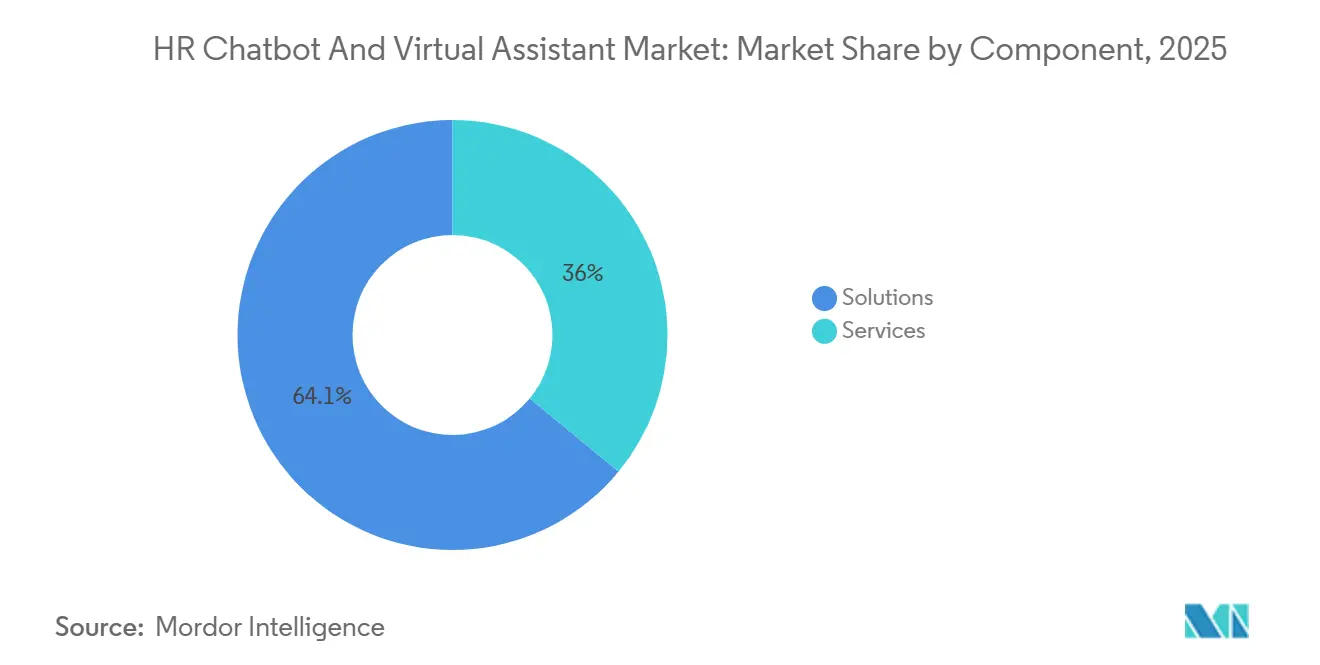

- By component, solutions led with a 64.05% revenue share in the HR Chatbot and Virtual Assistant market in 2025, while services are expanding at a 21.85% CAGR through 2031.

- By application, recruitment and onboarding captured 43.21% of 2025 revenue, whereas workforce engagement and wellness is rising the fastest at a 20.43% CAGR through 2031.

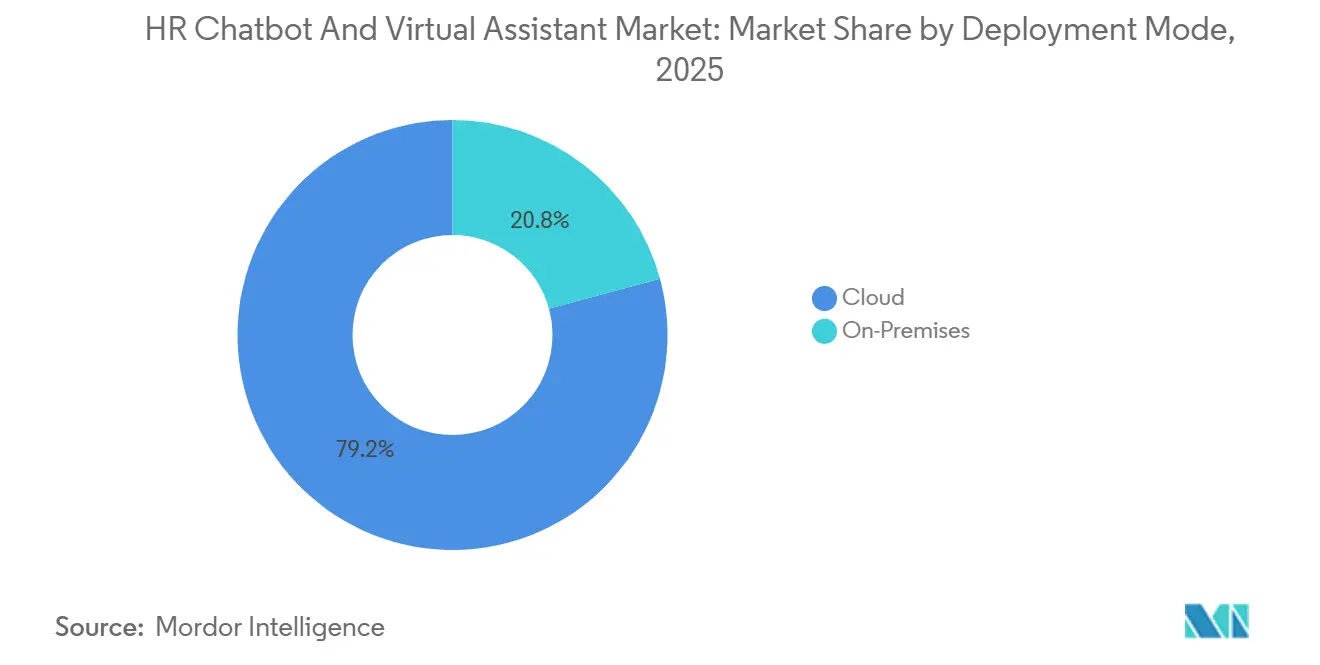

- By deployment mode, cloud accounted for 79.22% of 2025 revenue and is set to expand at a 22.01% CAGR to 2031.

- By organization size, small and medium-sized enterprises represented 38.55% of 2025 revenue and are projected to grow at 21.56% through 2031.

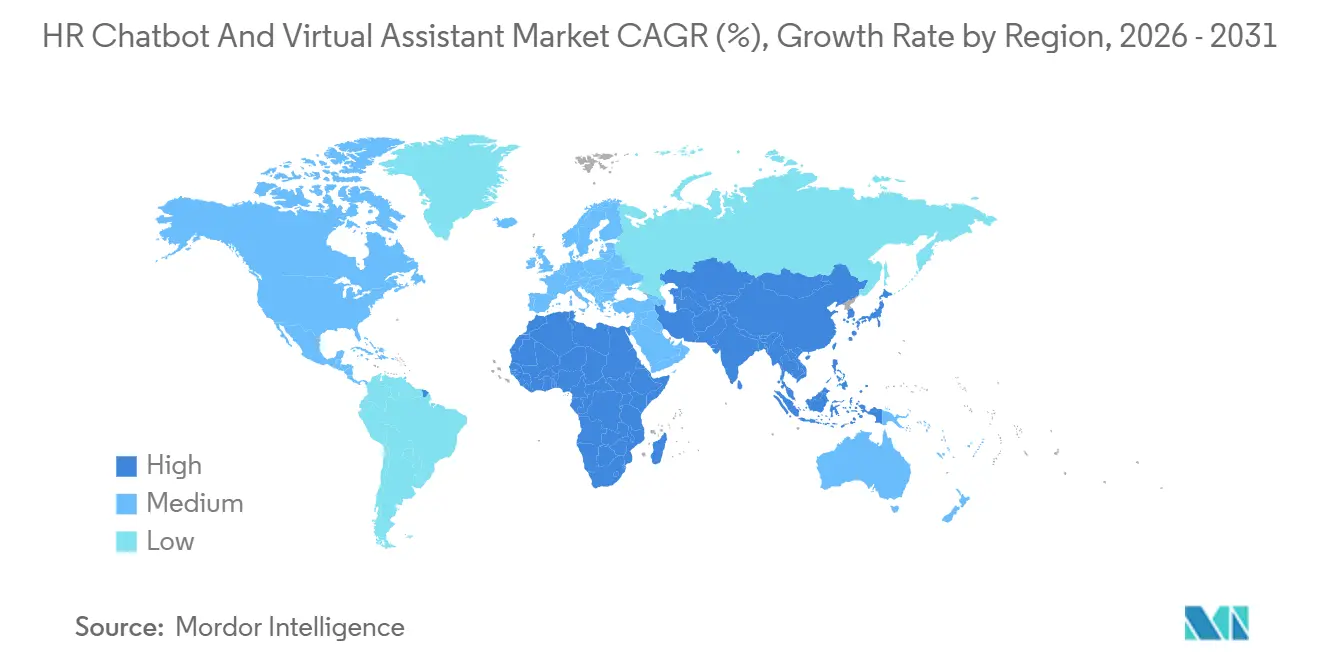

- By geography, North America held 37.00% of 2025 revenue yet Asia-Pacific is advancing at a 20.90% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HR Chatbot And Virtual Assistant Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating AI-Driven Recruitment Automation | +4.8% | Global, early concentration in North America and Asia-Pacific | Short term (≤ 2 years) |

| Rising Demand for Always-On Candidate Engagement | +3.9% | Global, acute in Asia-Pacific labor markets with sub-3% unemployment | Medium term (2-4 years) |

| Growth of Remote and Hybrid Work Models | +3.2% | North America and Europe with spillover to South America and Middle East | Medium term (2-4 years) |

| Seamless Integration With HRIS and ATS Platforms | +2.6% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Emergence of Multilingual Generative AI Chatbots | +2.1% | Asia-Pacific core, Middle East, and South America | Medium term (2-4 years) |

| Pressure for ESG-Aligned Fair-Hiring Practices | +1.5% | Europe and North America, emerging in Middle East sovereign portfolios | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating AI-Driven Recruitment Automation

Large language models now parse résumés, rank applicants, and draft outreach messages in seconds, shrinking screening cycles from weeks to hours. Workday’s planned integration of Paradox into its human capital platform will expose AI scheduling and pre-qualification workflows to more than 10,000 enterprise customers, encouraging rapid mainstream adoption.[1]Workday Investor Relations, “Workday to Acquire Paradox,” workday.com Buyers also perceive lower integration risk when automation resides inside their system of record. Competitive pressure forces standalone applicant-tracking vendors to match this speed or face displacement. Audit-ready logs required by ISO/IEC 27001 have become a non-negotiable feature, cementing recruitment automation as a default capability rather than an optional add-on.

Rising Demand for Always-On Candidate Engagement

Persistent talent shortages push passive candidates to expect instant answers on compensation, remote-work policies, and career paths. Chatbots that respond within a minute satisfy this expectation, especially in Asia-Pacific where 76% of Singaporean firms deployed AI HR tools by late 2025. JobTalk AI supports 23 languages with natural speech, letting recruiters address applicants in Tokyo, Mumbai, and São Paulo simultaneously. Enterprises report reclaiming more than 800 recruiter hours each year, redirecting effort toward finalist engagement and hiring-manager collaboration. As response times fall, candidate expectations climb, creating a virtuous adoption cycle.

Growth of Remote and Hybrid Work Models

Distributed teams generate continuous HR queries spanning visas, equipment, and local labor rules. Chatbots with jurisdiction-specific knowledge bases triage up to 80% of requests, preventing backlogs that lower employee satisfaction. Leena AI’s Colleague Studio lets HR partners design localized workflows without code, reflecting the fragmentation of HR processes in borderless workforces. The April 2025 partnership embedding Colleague Studio into UKG’s suite illustrates how vendors simplify deployment by bundling conversational AI with existing systems. Data-residency rules reinforce demand for chatbots that store answers and logs inside compliant clouds.

Seamless Integration With HRIS and ATS Platforms

Enterprises invested millions in Workday, SAP SuccessFactors, Oracle HCM Cloud, and ADP Workforce Now resist chatbots that cannot read or write core records. Vendors offering certified connectors cut roll-out time from quarters to weeks. Paylocity’s April 2026 acquisition of Grayscale created a chatbot that retrieves year-to-date earnings and adjusts tax withholdings directly inside Paylocity’s payroll engine. Tight coupling also reduces data-breach risk, meeting GDPR Article 30 record-keeping rules. As a result, integration depth has become a decisive purchase criterion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Data-Privacy and Bias Regulations | -2.2% | Europe and North America, expanding to Asia-Pacific finance hubs | Short term (≤ 2 years) |

| Limited Contextual Understanding in Complex Queries | -1.6% | Global, acute in regulated verticals such as healthcare and finance | Medium term (2-4 years) |

| Integration Complexity With Legacy Systems | -1.2% | North America and Europe where HRIS pre-date 2015 | Long term (≥ 4 years) |

| Rising Risk of Anti-AI Hiring Legislation | -0.8% | North America and Europe with early signals in Australia and Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Data-Privacy and Bias Regulations

The European Union AI Act mandates third-party conformity assessments, transparency notices, and human-oversight controls for recruitment chatbots, adding up to 18 months to product cycles and raising compliance costs. New York City Local Law 144 imposes annual bias audits with penalties up to USD 1,500 per violation. Smaller vendors struggle to afford these audits, shifting market share toward providers with dedicated compliance teams. Regional rules in Illinois and Colorado layer additional requirements, prompting platforms to support jurisdiction-specific configurations. Procurement offices increasingly request ISO/IEC 42001 certification, reinforcing the restraint.

Limited Contextual Understanding in Complex Queries

Chatbots excel at factual answers yet falter on multi-step scenarios involving exceptions or conflicting rules. In healthcare and financial services, misinterpreting leave statutes or whistle-blower protections exposes employers to liability. Escalation to human agents mitigates risk but erodes cost savings when rates exceed 25-30%. The core challenge lies in language models predicting tokens rather than reasoning, so minor phrasing changes produce divergent answers. Enterprises respond by narrowing chatbot scope or adding guardrails, slowing full automation in high-risk use cases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Momentum as Compliance Tightens

Solutions generated 64.05% of 2025 revenue through license and subscription fees. Services, however, are expanding at 21.85% CAGR because enterprises need prompt engineering, bias audits, and model tuning to stay compliant with evolving laws. Paradox’s February 2025 purchase of Eqtble reflects the pivot toward bundled compliance services.[2]Paradox Press Release, “Paradox Acquires Eqtble,” paradox.ai This reflects the increasing demand for integrated solutions that address regulatory challenges effectively.

Solutions remain vital for recurring revenue and lock-in effects. Yet the European Union AI Act’s 2026 deadline forced many organizations to seek external experts, lifting demand for managed services. Vendors offering one-stop compliance and tuning are set to outpace pure software sellers.

By Application: Wellness Chatbots Outpace Hiring Tools

Recruitment and onboarding held 43.21% of 2025 revenue as firms chased faster time-to-hire. Workforce engagement and wellness is growing quickest at a 20.43% CAGR, fueled by M42 and TELUS Health’s employee assistance program that triages mental health inquiries in Arabic and English. The HR Chatbot and Virtual Assistant market size attached to wellness tools is expanding as retention proves cheaper than recruitment.

Self-service portals rank second, covering password resets and benefits enrollment, with 74% of Malaysian and Singaporean staff expecting such portals by 2025. Training and development bots are emerging as they recommend personalized learning paths, while HR helpdesk chatbots automate payroll and tax queries.

By Deployment Mode: Cloud Dominance Reflects SME Demand

Cloud captured 79.22% of 2025 spending and is accelerating at 22.01% CAGR. Small and medium-sized enterprises migrate to subscription models that cut capital outlays, explaining why the HR Chatbot and Virtual Assistant market share linked to cloud keeps rising. Frequent model updates and security patches arrive automatically, a strong advantage for lean IT teams.

In sectors like finance, defense, and healthcare, on-premises solutions remain dominant, ensuring sensitive data stays within corporate firewalls. While hybrid models merge cloud front-ends with on-premises data stores, they grapple with latency challenges that vendors are actively working to refine. These challenges highlight the ongoing need for innovation in hybrid infrastructure solutions.

By Organization Size: SMEs Close the Adoption Gap

Large enterprises supplied 61.45% of 2025 revenue, but SMEs are growing faster at 21.56% CAGR, mirroring the services segment. Tiered pricing below USD 100 per month makes entry affordable, and TurboHire’s USD 6 million Series A funds expansion into India’s tier-two cities to serve this cohort.

Tight labor markets propelled Asia-Pacific SMEs to embrace conversational AI at double the rate of their North American counterparts. While large enterprises continue to outpace rivals in spending, there is still ample opportunity for disruptors focusing on SMEs. This trend highlights the growing importance of tailored solutions for smaller businesses in the region.

Geography Analysis

North America produced 37.00% of 2025 revenue, buoyed by technology, healthcare, and retail adopters. Bias-audit mandates under Local Law 144 forced vendors to build audit logs that set global compliance benchmarks. Consolidation, including Paychex’s USD 4.1 billion Paycor deal and Paylocity’s Grayscale purchase, demonstrates how incumbents add chatbots to defend payroll and HCM franchises.

Asia-Pacific is expanding at a 20.90% CAGR, the fastest worldwide. Unemployment for skilled roles in Singapore and urban China stayed under 3% in 2025, spurring adoption of multilingual chatbots like MapRecruit.ai’s ReA (105 languages) and Hire-Match.ai’s Clara (50 languages). Funding rounds for TurboHire and other regional players show investors’ confidence in sustained double-digit growth.

Europe grows steadily, though compliance complexity under the EU AI Act slows deployments that lack built-in audit trails. Germany, the United Kingdom, and France adopt fastest, focusing on privacy-ready platforms. The Middle East gains momentum through wellness initiatives such as the M42 and TELUS Health program in the UAE. South America lags due to lower cloud penetration yet sees rising interest in Brazil and Argentina, while Africa remains nascent with early pilots in South Africa and Kenya.

Competitive Landscape

Top five vendors controlled under 40% of 2025 revenue, marking a moderately fragmented field. Workday’s planned Paradox acquisition and its USD 1.1 billion Sana purchase underscore the suite vendors’ drive to own conversational interfaces. ServiceNow’s USD 2.85 billion Moveworks deal stretches chatbots across IT, HR, and facilities requests.[3]ServiceNow Investor Relations, “ServiceNow to Acquire Moveworks,” servicenow.com This trend reflects the increasing demand for automation and efficiency in enterprise operations.

Pure-play innovators such as HireVue, Eightfold AI, and Leena AI accelerate generative-model deployment to stay ahead, yet face buyer preference for integrated suites. White-space opportunities lie in high-turnover sectors like hospitality and logistics, and in emerging SME markets that need low-cost multilingual bots. ISO/IEC 42001 compliance and pre-built ERP connectors increasingly decide competitive wins.

As the market evolves, partnerships and collaborations are expected to play a critical role in driving innovation and expanding market reach. Vendors that can effectively integrate advanced technologies while addressing specific industry needs are likely to gain a competitive advantage during the forecast period. Furthermore, the adoption of AI-driven analytics and predictive tools is anticipated to enhance decision-making processes.

HR Chatbot And Virtual Assistant Industry Leaders

Paradox, Inc.

HireVue, Inc.

Eightfold AI, Inc.

Leena AI, Inc.

TurboHire Technologies Private Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Paylocity completed the Grayscale acquisition, embedding conversational payroll support directly into its HCM suite.

- February 2026: M42 and TELUS Health launched an Arabic-English AI employee assistance program in the UAE.

- October 2025: Leena AI unveiled Colleague Studio, enabling no-code HR workflow design.

- September 2025: Workday bought Sana for USD 1.1 billion to add learning content discovery to its chatbot portfolio.

Global HR Chatbot And Virtual Assistant Market Report Scope

The HR Chatbot and Virtual Assistant market encompasses AI-driven tools that automate employee queries, HR transactions, and routine support tasks. Leveraging natural language processing, these solutions deliver real-time answers on topics like leave, policies, onboarding, payroll, and system navigation. By offering 24/7 assistance, HR chatbots not only speed up service delivery but also reduce support volumes and elevate the overall employee experience. The market's expansion is being propelled by the increasing adoption of generative AI technologies and the growing need to support a remote workforce.

The HR Chatbot and Virtual Assistant Market Report is Segmented by Component (Solutions, and Services), Application (Recruitment and Onboarding, Employee Self-Service, Training and Development, HR Helpdesk and Case Management, and Workforce Engagement and Wellness), Deployment Mode (Cloud, and On-Premises), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions |

| Services |

| Recruitment and Onboarding |

| Employee Self-Service |

| Training and Development |

| HR Helpdesk and Case Management |

| Workforce Engagement and Wellness |

| Cloud |

| On-Premises |

| Large Enterprises |

| Small and Medium-Sized Enterprises (SMEs) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Component | Solutions | |

| Services | ||

| By Application | Recruitment and Onboarding | |

| Employee Self-Service | ||

| Training and Development | ||

| HR Helpdesk and Case Management | ||

| Workforce Engagement and Wellness | ||

| By Deployment Mode | Cloud | |

| On-Premises | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-Sized Enterprises (SMEs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and projected size of the HR Chatbot and Virtual Assistant market?

The market stands at USD 1.43 billion in 2026 and is forecast to reach USD 3.42 billion by 2031, reflecting a 19.08% CAGR, according to Mordor Intelligence.

Which segment is growing faster, solutions or services?

Services are outpacing solutions at a 21.85% CAGR through 2031 as firms require bias audits and model tuning.

Why are Asia-Pacific companies adopting HR chatbots so rapidly?

Tight labor markets and high multilingual needs drive Asia-Pacific enterprises to deploy conversational AI at twice the North American rate.

How do privacy regulations affect HR chatbot adoption?

The EU AI Act and New York City Local Law 144 add audit and transparency obligations that favor vendors with built-in compliance features.

Which deployment model dominates the market?

Cloud deployment commands 79.22% of revenue and grows fastest at 22.01% CAGR because it lowers upfront costs for SMEs.

Page last updated on: