Hot-Melt Self-Adhesive Labels Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

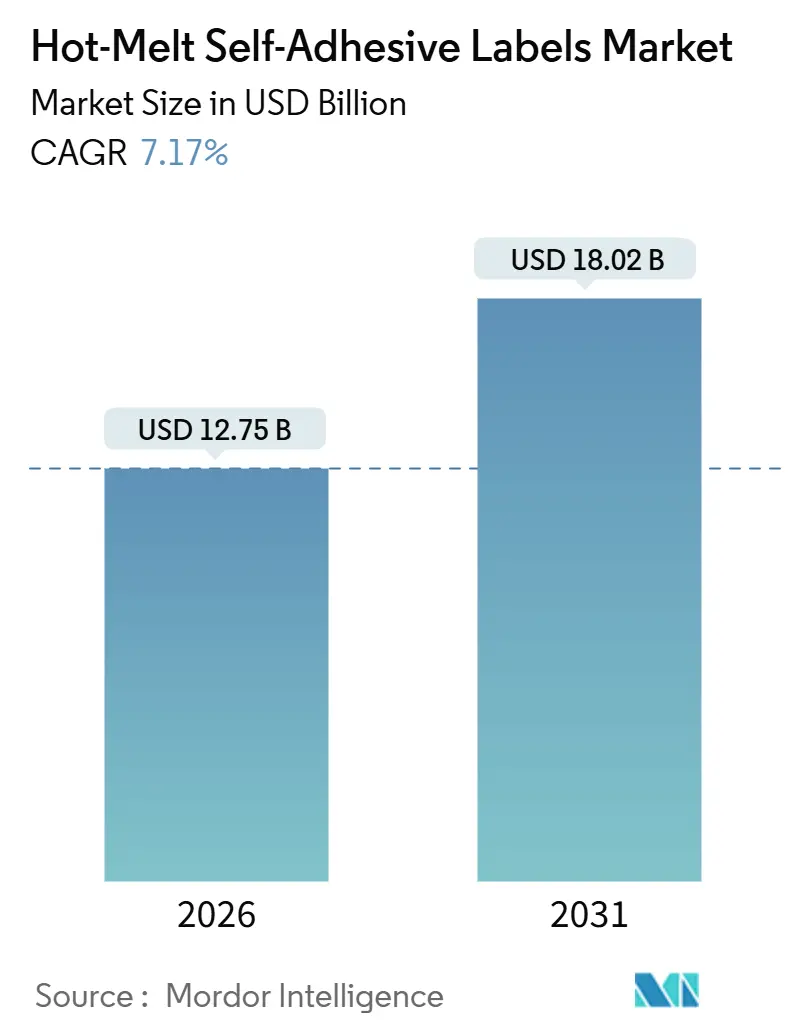

| Market Size (2026) | USD 12.75 Billion |

| Market Size (2031) | USD 18.02 Billion |

| Growth Rate (2026 - 2031) | 7.17% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

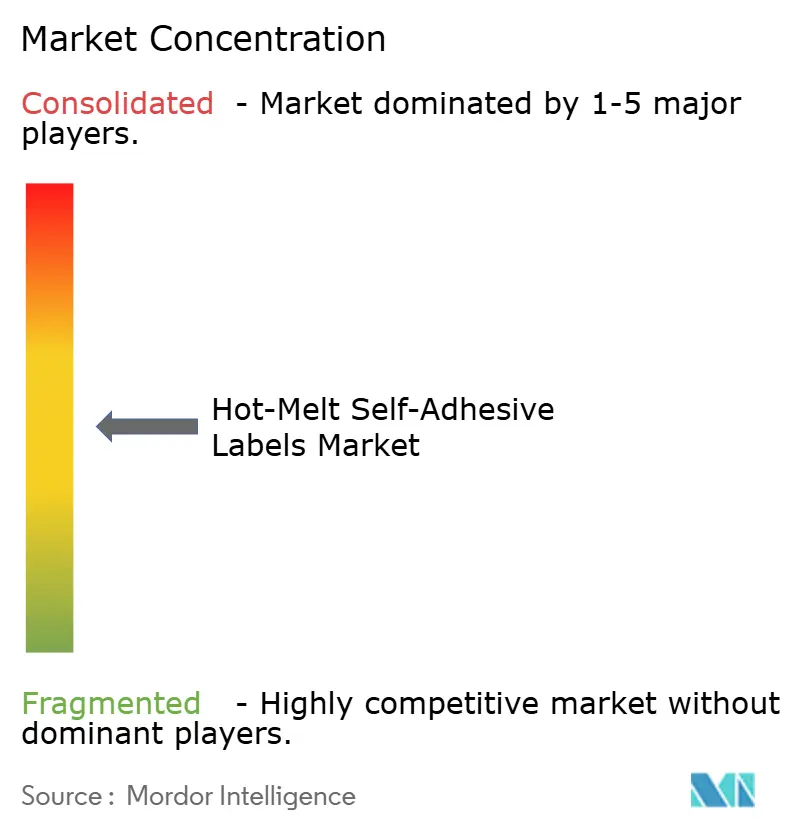

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hot-Melt Self-Adhesive Labels Market Analysis by Mordor Intelligence

The Hot-Melt Self-Adhesive Labels Market size is estimated at USD 12.75 billion in 2026, and is expected to reach USD 18.02 billion by 2031, at a CAGR of 7.17% during the forecast period (2026-2031). Intensifying parcel movements within e-commerce, rising serialization in pharmaceuticals, and the regulatory pivot toward solvent-free chemistries are the primary forces behind this expansion. In Q3 2025, online retail sales in the United States experienced a year-over-year increase, which translates directly into heightened logistics-label volumes. In parallel, the European Union’s Regulation 2025/40 restricts per- and polyfluoroalkyl substances effective August 2026, pushing brands to validate hot-melt formulations that pair low toxicity with freezer-to-microwave durability. Printer-converter adoption of high-speed rotary lines, FDA serialization compliance, and Asia-Pacific packaged-food growth are further compounding demand, while material suppliers race to engineer wash-off adhesives compatible with PET and HDPE recycling streams.

Key Report Takeaways

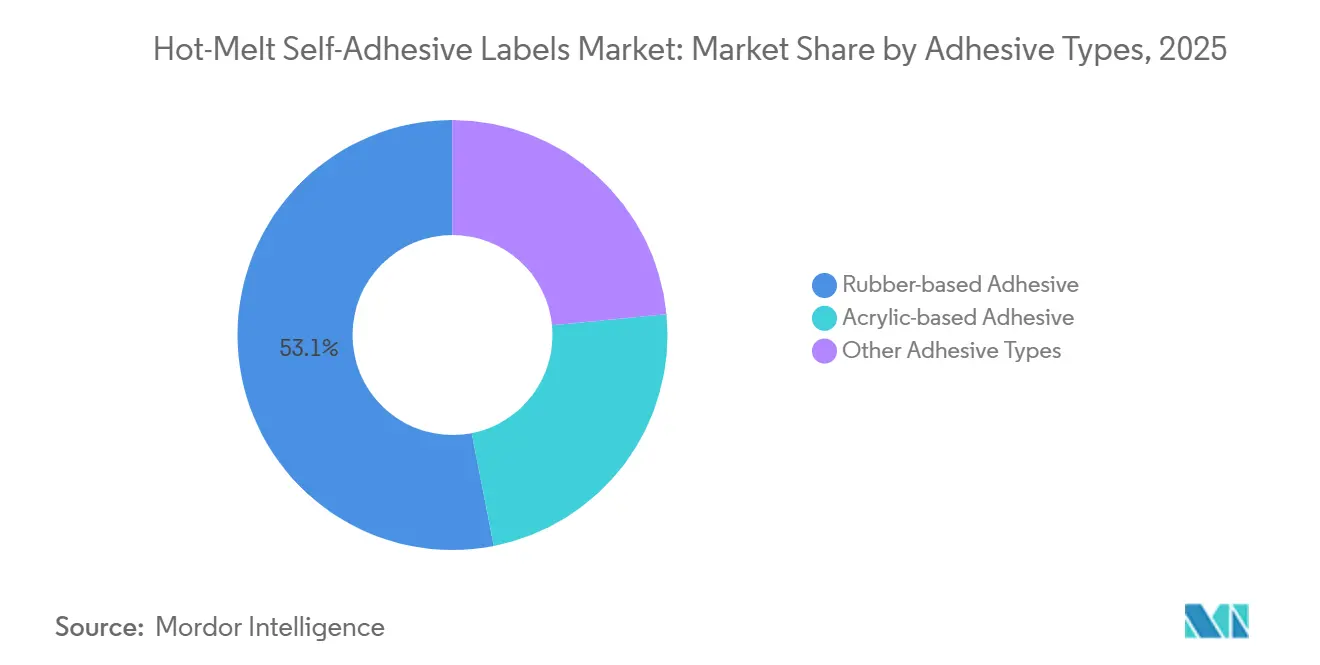

- By adhesive type, rubber-based formulations captured 53.08% of the hot-melt self-adhesive labels market share in 2025 and are projected to register a 7.81% CAGR by 2031.

- By release liner, silicone liners led with 89.82% revenue share in 2025, while film and sheet liners are forecast to post a 7.65% CAGR to 2031.

- By surface substrate, paper commanded 65.19% share of the hot-melt self-adhesive labels market size in 2025 and is projected to register a 7.23% CAGR by 2031.

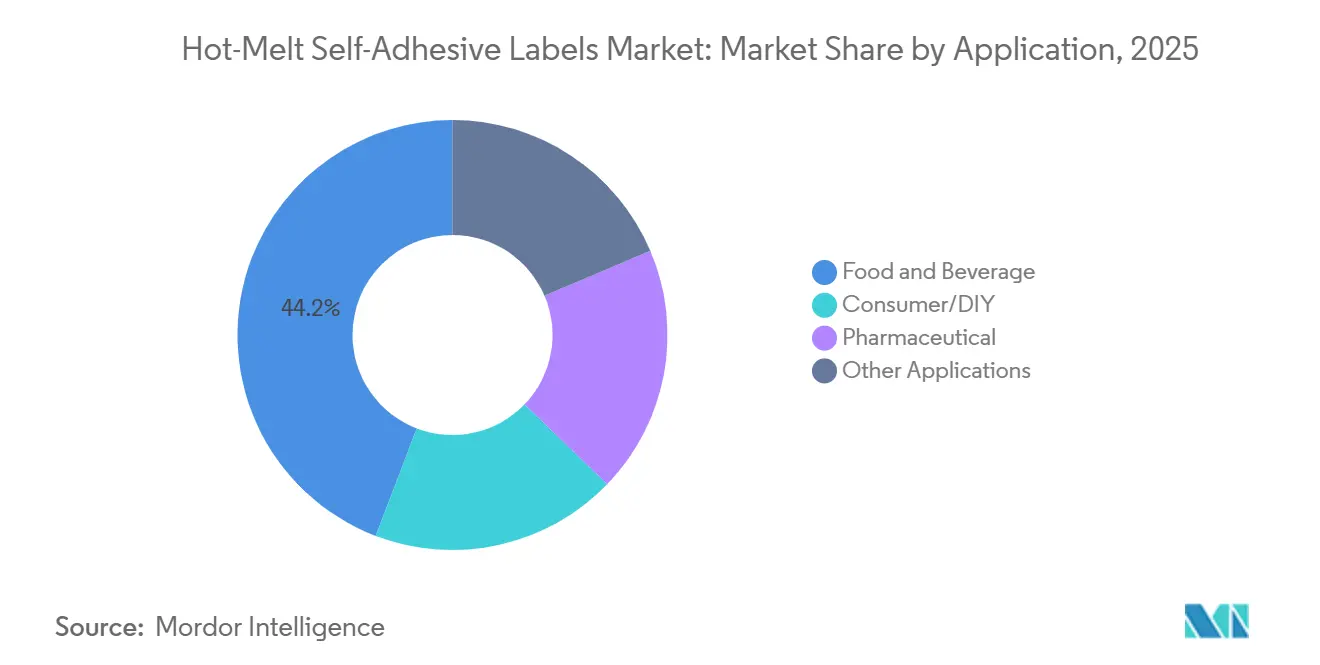

- By application, food and beverage held a 44.20% share in 2025, whereas pharmaceutical labels are advancing at an 8.11% CAGR through 2031.

- By geography, Asia-Pacific commanded 40.95% of 2025 consumption and records the fastest regional growth at an 8.51% CAGR till 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hot-Melt Self-Adhesive Labels Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce parcel volume surge fueling logistics label demand | +1.8% | Global, with peak intensity in North America and Asia-Pacific | Short term (≤ 2 years) |

| Expansion of packaged food and beverage production in emerging Asia | +1.5% | Asia-Pacific core, spill-over to Middle-East and Africa | Medium term (2–4 years) |

| Converter shift to high-speed automated hot-melt labeling lines | +1.2% | North America and Europe, early adoption in China | Medium term (2–4 years) |

| Regulatory preference for solvent-free adhesives in consumer packaging | +1.4% | Europe and North America, cascading to Asia-Pacific | Long term (≥ 4 years) |

| Rapid uptake of microwave-safe hot-melt labels for ready-meal trays | +1.0% | Europe and North America, emerging in urban Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-commerce Parcel Volume Surge Fueling Logistics Label Demand

As consumers increasingly opt for direct-to-consumer fulfillment, the number of parcels per order has surged, leading to a faster rise in label requirements compared to overall revenue growth. This uptick is largely attributed to shoppers strategically splitting their purchases to qualify for free shipping. Hot-melt pressure-sensitive labels have become the go-to choice in this scenario, as applicators can operate at speeds exceeding 200 meters per minute without the need for solvent flash-off. In Asia, third-party logistics providers (3PLs) are innovating by combining rotary die-cutting with variable-data inkjet heads, enabling real-time address modifications. This adoption is further bolstered by barcode regulations, which mandate that substrates maintain a contrast ratio above 1.5, even under abrasion. Together, these dynamics are propelling the hot-melt self-adhesive labels market on a steep upward trajectory.

Expansion of Packaged Food and Beverage Production in Emerging Asia

In 2024, China's food-manufacturing output surged, driven by strong demand in the dairy, bakery, and frozen-meal sectors. In India, the harmonization of the Goods and Services Tax (GST) has redirected packaging investments towards larger hubs. These hubs now predominantly favor hot-melt lines, which operate without the need for UV ovens. In Japan, the circulation of label backing paper highlights a consumption baseline in this mature economy. If China and India were to adopt a per-capita usage similar to Japan's, it would result in increased demand for facestock and adhesive volumes by 2031. This burgeoning demand is propelling the market for hot-melt self-adhesive labels across the Asia-Pacific region.

Converter Shift to High-Speed Automated Hot-Melt Labeling Lines

Digital-flexo hybrid presses with inline inspection reduce changeovers from hours to minutes. Konica Minolta’s 2024 market note highlighted Japan’s rapid migration toward short-run, variable-data work[1]Konica Minolta, “Digital Label Printing Market Analysis Japan 2024,” konicaminolta.com. Hot-melt chemistry fits because it needs no drying tunnel, trimming energy draw, or footprint. Avery Dennison’s UV-acrylic hot-melt S8035 survives 150 °C autoclave cycles, illustrating how suppliers engineer specialty performance. Machine-learning platforms such as LINTEC’s HVT model predict peel strength from polymer glass-transition temperature, accelerating recipes and giving converters a commercial edge. Automation, therefore, magnifies throughput and underpins stable demand across the hot-melt self-adhesive labels market.

Regulatory Preference for Solvent-Free Adhesives in Consumer Packaging

EU Regulation 2025/351 sets a cap on overall migration for food-contact components. 100%-solids hot-melt systems can easily meet this limit. In the U.S., 21 CFR 175.125 aligns with these extractables standards, emphasizing a unified approach across regions. RecyClass's wash-off testing mandates that paper labels achieve a high level of adhesive releasability, while film constructions need to demonstrate strong performance. As a result, brands are gravitating towards hot-melt products that boast these certifications. Additionally, being solvent-less significantly reduces VOC emissions, aiding converters in meeting stringent air-quality permits at the plant level. Such regulatory endorsements ensure a sustained growth trajectory for the hot-melt self-adhesive labels market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recycling challenges from adhesive and facestock contamination | -1.1% | Europe and North America, emerging in Asia-Pacific | Medium term (2–4 years) |

| Competitive threat from linerless label technologies | -0.8% | Global, with early adoption in logistics and retail | Long term (≥ 4 years) |

| Oxidative discoloration of rubber-based hot-melt labels in premium cosmetics | -0.5% | Europe and North America luxury segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Recycling Challenges from Adhesive and Facestock Contamination

FEICA's 2024 guidance on paper recycling highlights that pressure-sensitive adhesives should either wash off completely or disperse without visibility. However, residues from hot melts can clump together, leading to a decrease in the brightness of PET flakes. RecyClass imposes a limit, capping the residual adhesive at a few weight percentages and mandating a release rate of at least 95% for paper constructions. Meanwhile, EU Regulation 2025/40 has introduced a ban on specific fluorinated substances. This regulation pushes formulators towards low-molecular-weight tackifiers, which, unfortunately, weaken adhesion on rough glass surfaces. These compliance costs may hinder the speed of specification changes, thereby moderating the growth of the hot-melt self-adhesive labels market.

Competitive Threat from Linerless Label Technologies

By coating the facestock back with linerless rolls, shippers eliminate silicone liners, reducing material costs. This method also reduces waste, offering a notable sustainability advantage. The Association of Plastic Recyclers permits up to three wt% adhesive, a benchmark that's more attainable for thinner linerless coatings[2]Federation of European Adhesive & Sealant Industry, “Adhesives in Paper and Board Recycling,” feica.eu. Yet, the need for specialized printers and dispensers poses a challenge, leading retailers to be cautious about revamping their existing fleets. Nonetheless, a swift adoption of parcel hubs could divert business from traditional methods, potentially curbing the growth of the hot-melt self-adhesive labels market in the future.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Adhesive Type: Rubber Systems Maintain Volume Leadership

Rubber-based hot-melts accounted for 53.08% of 2025 revenue within the hot-melt self-adhesive labels market. At this level, the segment controlled more than half of all shipments, confirming near-term preference for high tack at low cost. Rubber grades are forecast to expand at 7.81% through 2031, slightly above the overall CAGR. The hot-melt self-adhesive labels market size for rubber chemistries is consequently on track to rise sharply, driven by beverage bottlers and frozen-food handlers that need adhesion on wet glass. Acrylic-based systems hold a smaller slice yet will gain points in cosmetics and outdoor goods because their higher UV resilience offsets premium resin pricing. Machine-learning formulation tools, highlighted by LINTEC’s HVT platform, cut development cycles and help fine-tune antioxidant dosing.

Rubber remains dominant even as discoloration concerns linger. Food-contact laws in the United States and European Union impose extractables caps that both rubber and acrylic systems can meet with food-grade tackifiers. This regulatory clearance keeps rubber cost-competitive for short lifecycle labels. Meanwhile, niche UV-curable hot-melts serve electronics and automotive harnesses where zero residual tack after cure is vital. Such specialization widens the portfolio and sustains volume in the broader hot-melt self-adhesive labels market.

By Release Liner Type: Silicone Dominates but Film Liners Accelerate

Silicone-coated liners delivered 89.82% of 2025 sales. Despite high silicone cost, converters value consistent release forces that prevent adhesive pick-up on high-speed presses. Film liners, especially polyester, post the fastest 7.65% CAGR. They combine low moisture absorption with tight dimensional control, essential for serialized 2D barcodes under the U.S. Drug Supply Chain Security Act. Film-liner adoption therefore lifts the hot-melt self-adhesive labels market size at the premium end.

Glassine liners still rule commodity label rolls due to price, yet they swell under humidity and distort the register. Non-silicone release chemistries, often fluoropolymer-based, undercut silicone cost. Early trials show stable release across multiple rewind cycles, but mass rollout waits on proof of recyclability. Over the outlook, silicone will keep a large majority, though incremental shifts to film will diversify supply and sustain healthy competition within the hot-melt self-adhesive labels market.

By Surface Substrate: Paper Favored for Circularity, Film Wins on Durability

Paper substrates made up 65.19% of 2025 shipments and post the fastest 7.23% CAGR, underscoring brand commitments to fiber-based packaging. RecyClass requires greater than 95% label release during repulping, a threshold easier for paper to meet than film. Consequently, the paper continues to anchor large-volume food and logistics runs. The hot-melt self-adhesive labels market size for film labels, however, is rising fastest where moisture and abrasion resistance matter. Clear polypropylene enables showcase windows on cosmetics, while PET facestock survives refrigeration. Japan’s biomass adhesive labels from AIM Group cut Scope 3 emissions, aligning film offerings with sustainability metrics.

Future regulation also guides material splits. EU Regulation 2025/40 states that labels must not hinder primary-package recyclability. Adhesive suppliers therefore deliver wash-off systems like Avery Dennison CleanFlake that fragment in caustic baths. Such innovation lets film labels coexist with PET bottle recycling, keeping both substrate families relevant inside the hot-melt self-adhesive labels market.

By Application: Pharmaceuticals Post Highest Growth Under Serialization Rules

Food and beverage retained a 44.20% share in 2025 on sheer volume, yet pharmaceuticals are the quickest riser at 8.11% CAGR. Package-level 2D barcodes became mandatory under the FDA’s DSCSA in November 2023. The hot-melt self-adhesive labels market size attributed to drug packaging will therefore swell as global track-and-trace regimes converge. Labels must deliver low-reflectivity surfaces for reliable scanning long after production. Serialized barcodes also drive film-liner preference to avoid dimensional drift.

Beyond healthcare, consumer DIY brands exploit hot-melt adhesion on low-surface-energy HDPE bottles. Logistics providers layer RFID into facestock to manage parcels in real time. Stora Enso’s paper RFID label, certified plastic-free, shows that smart functionality can align with fiber-based recycling. Each niche builds incremental revenue and strengthens overall momentum within the hot-melt self-adhesive labels market.

Geography Analysis

Asia-Pacific held 40.95% of global revenue in 2025 and is tracking an 8.51% CAGR to 2031. This growth is bolstered by capacity expansions in China's Yangtze River Delta, Gujarat corridor in India, and northern provinces of Vietnam. In a move to streamline operations, UPM Adhesive Materials inaugurated a terminal close to Hanoi in October 2025, aiming to reduce lead times for specialty grades. As chilled-food production rises and the cold-chain network expands, there's an increasing demand for freezer-grade labels that can operate at minus 50 °C. Additionally, packaging harmonization driven by GST is promoting the establishment of centralized high-speed converting hubs across India.

North America and Europe are witnessing steady growth. Investments in automation are curbing make-ready waste, and brands are adapting to EU Regulation 2025/40, which mandates trials with PFAS-free adhesives. In August 2025, Avery Dennison bolstered its Materials Group by acquiring Meridian's flooring-adhesive unit, enhancing its specialty expertise. Meanwhile, CCL Industries reported an increase in label revenue in Q3 2024, driven by balanced demand in home care, pharmaceuticals, and security labeling.

While South America and the Middle-East and Africa are still modest players, they're on the rise. Brazil's regulations on Portuguese labeling secure its domestic print volume, and Saudi Arabia's Vision 2030 is spurring the establishment of pharmaceutical factories that necessitate serialized codes. Due to high ambient temperatures, there's a shift towards acrylic grades for UV stability in adhesives, yet budget constraints keep rubber variants in demand. Together, these regions may offer only marginal gains, but they expand the customer base for the hot-melt self-adhesive labels market.

Competitive Landscape

The hot-melt self-adhesive labels market is moderately fragmented. Leader companies leverage global coating lines, proprietary chemistries, and field engineers to secure specifications. Regional converters in Southeast Asia and Latin America chip away at share by offering short lead times and local language support. Many focus on microwave-safe ready-meal trays, a niche first targeted by Stora Enso’s ECO RFID paper label. Technology investment is a clear trend. Inline inspection cameras verify ISO/IEC 15415 barcode grades in real time, while digital print engines enable seasonal SKUs without overstock risk. Sustainability also steers competition. Longer term, bio-based tackifiers, linerless formats, and smart packaging offer white-space opportunities. Suppliers that balance circularity, regulatory compliance, and cost will outpace rivals, shaping the next growth phase for the hot-melt self-adhesive labels market.

Hot-Melt Self-Adhesive Labels Industry Leaders

Avery Dennison Corporation

CCL Industries

UPM

LINTEC Corporation

AKO GROUP

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: BioBond Adhesives unveiled BioMelt plant-based pressure-sensitive adhesives for labels and tapes, with sampling available from Q4 2025.

- August 2025: Henkel introduced Technomelt EM 335 RE, a PET-labeling hot-melt designed to enable cleaner flake separation and support EU recycled-content quotas.

Global Hot-Melt Self-Adhesive Labels Market Report Scope

Hot-melt self-adhesive labels feature a thermoplastic adhesive that remains solid at room temperature but melts upon heating, turning tacky for application. These labels provide high initial tack and quick bonding, making them perfect for swift, automated labeling on diverse surfaces, even those that are challenging, non-smooth, or irregular.

The hot-melt self-adhesive labels market is segmented by adhesive type, release liner type, surface substrate, and application. By adhesive type, the market is segmented into acrylic-based adhesives, rubber-based adhesives, and other adhesive types. By release liner type, the market is segmented into silicone and non-silicone liners. By surface substrate, the market is segmented into paper-based and film-based surfaces. By application, the market is segmented into food and beverage, consumer/DIY, pharmaceutical, and other applications. The report also covers the market size and forecasts in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

| Acrylic-based Adhesive |

| Rubber-based Adhesive |

| Other Adhesive Types |

| Silicone |

| Non-silicone |

| Paper-based |

| Film-based |

| Food and Beverage |

| Consumer/DIY |

| Pharmaceutical |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Adhesive Types | Acrylic-based Adhesive | |

| Rubber-based Adhesive | ||

| Other Adhesive Types | ||

| By Release Liner Type | Silicone | |

| Non-silicone | ||

| By Surface Substrate | Paper-based | |

| Film-based | ||

| By Application | Food and Beverage | |

| Consumer/DIY | ||

| Pharmaceutical | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the hot-melt self-adhesive labels market in 2026?

The market stands at USD 12.75 billion in 2026 and is forecast to reach USD 18.02 billion by 2031, registering a 7.17% CAGR.

What is driving the fastest growth within label applications?

Pharmaceutical serialization mandates under regulations such as the U.S. DSCSA are propelling an 8.11% CAGR for drug-package labels.

Which region leads demand for hot-melt self-adhesive labels?

Asia-Pacific accounts for 40.95% of global revenue thanks to capacity expansion in China, India, and Southeast Asia.

Why are silicone release liners still dominant?

Silicone liners offer consistent low release force at high press speeds, maintaining 89.82% share despite higher material cost.

How are recyclability requirements influencing adhesive formulations?

European and U.S. protocols demand higher than 90–95% wash-off performance, prompting suppliers to develop clean-flake hot-melt grades certified by RecyClass.

What competitive moves stand out among leading suppliers?

Avery Dennison’s acquisition of Meridian’s flooring-adhesive assets and Henkel’s Technomelt EM 335 RE launch highlight strategic expansion into specialty and sustainable products.

Page last updated on: