Hormonal Implants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.91 Billion |

| Market Size (2031) | USD 1.25 Billion |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hormonal Implants Market Analysis by Mordor Intelligence

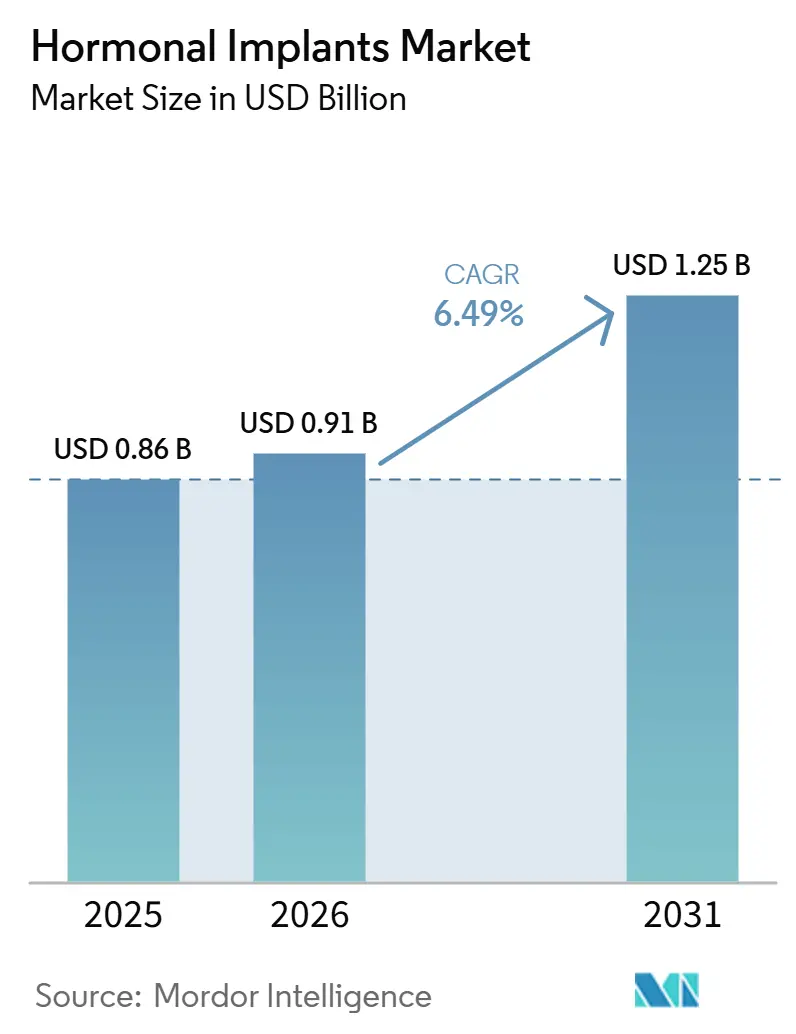

The Hormonal Implants Market size is expected to grow from USD 0.86 billion in 2025 to USD 0.91 billion in 2026 and is forecast to reach USD 1.25 billion by 2031 at 6.49% CAGR over 2026-2031.

The hormonal implants market is advancing as long-acting reversible contraception gains broader clinical support, product labels cover longer use periods, and public procurement programs expand across Africa and Asia. In January 2026, the FDA extended NEXPLANON use from three years to five years after an extended-use trial reported a Pearl Index of 0.0 pregnancies per 100 woman-years, strengthening the cost-per-year case for implants and supporting payer interest. Demand fundamentals remained strong, with the CDC reporting in 2025 that implants and IUDs accounted for 10.5% of all current contraceptive use among women aged 15 to 49 in the United States, rising to 13.8% among women aged 20 to 29. Competitive activity also indicated category confidence, as Apollo Global Management invested EUR 3 billion (USD 3.4 billion) for a minority stake in Bayer’s LARC business in July 2026, while UNFPA reported USD 57.5 million in national allocations across 54 partner countries in 2024. However, the hormonal implants market faces a more complex operating environment, as reimbursement systems may take time to align with the new five-year label, while biodegradable implant development could eventually change removal-related service economics for clinics and providers.

Key Report Takeaways

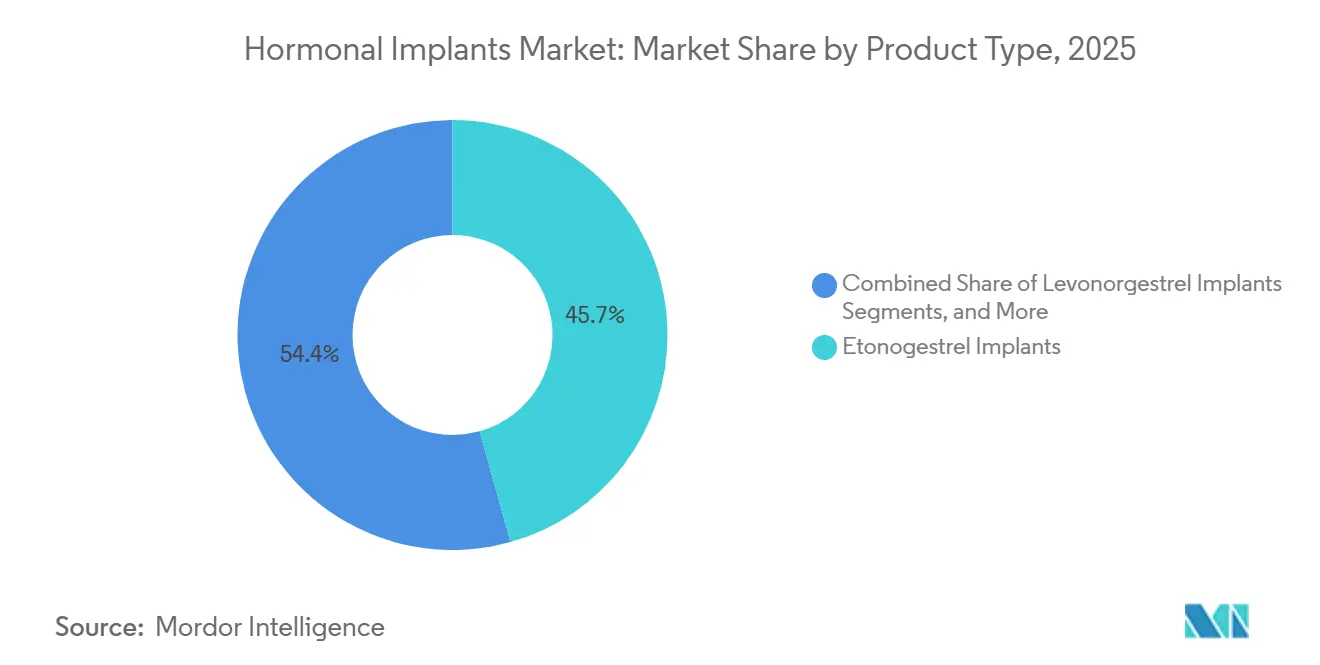

- By product type, etonogestrel implants led with 45.65% revenue share in 2025, while levonorgestrel implants are projected to expand at 8.93% CAGR through 2031.

- By application, contraception accounted for 38.23% revenue share in 2025, while hormone replacement therapy is projected to grow at 9.67% CAGR through 2031.

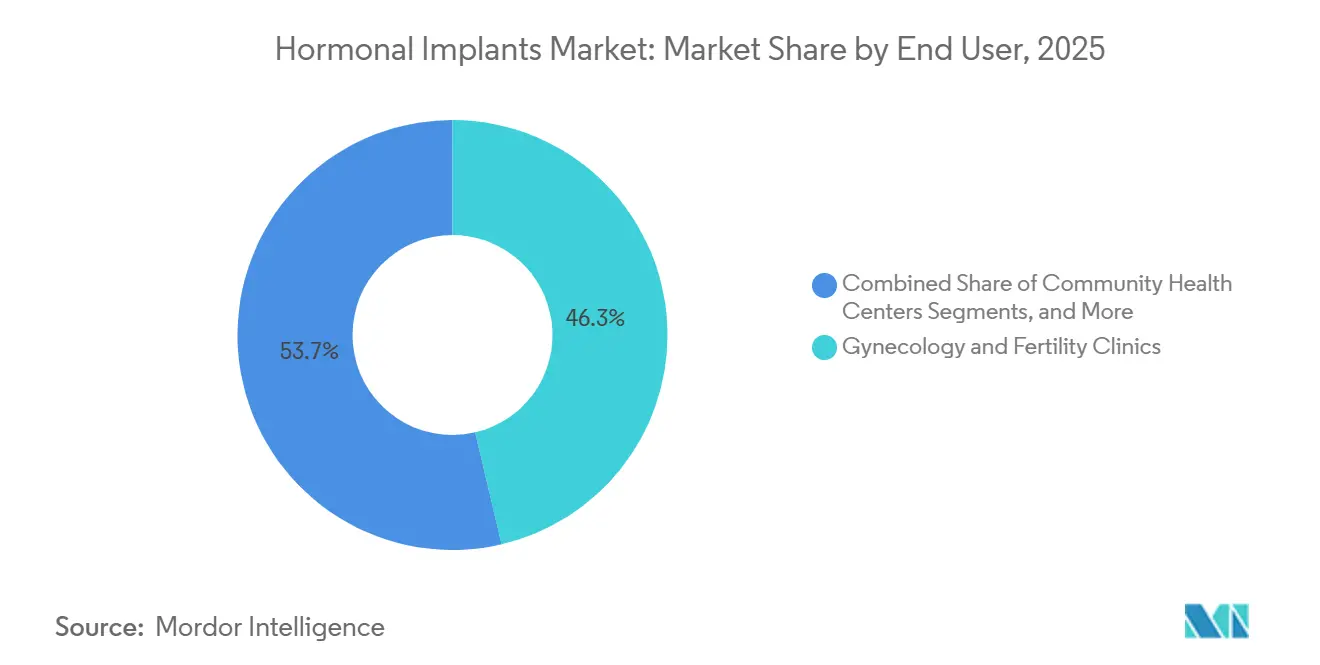

- By end user, gynecology and fertility clinics held 46.34% of the hormonal implants market share in 2025, while community health centers projected a CAGR at 8.35% through 2031.

- By distribution channel, public procurement captured 58.88% revenue share in 2025 and is also projected to grow at 9.78% CAGR through 2031.

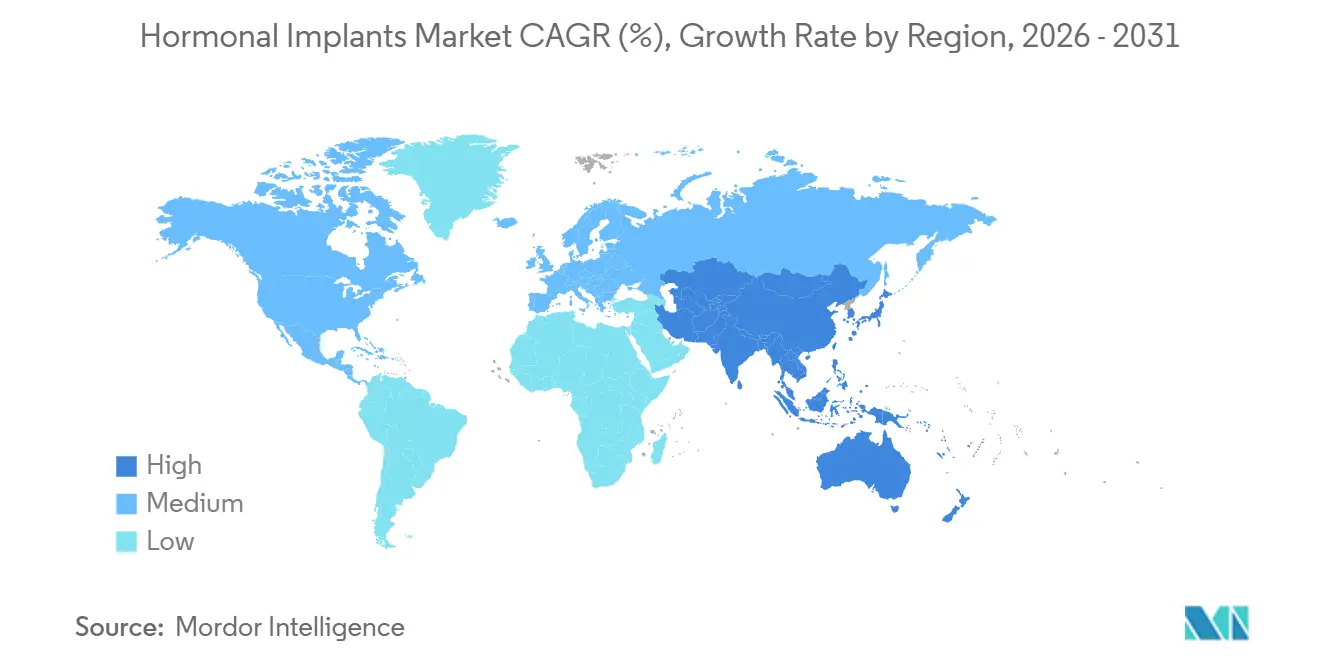

- By geography, North America held 38.56% share in 2025, while Asia-Pacific is projected to expand at 8.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hormonal Implants Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising preference for long-acting reversible contraception | +1.8% | Global | Short term (≤ 2 years) |

| Expansion of postpartum and post-abortion family planning programs | +1.0% | Sub-Saharan Africa, South Asia, Latin America | Medium term (2-4 years) |

| Wider access through public procurement and donor-funded supply chains | +0.8% | Sub-Saharan Africa, APAC core, spill-over to MEA | Medium term (2-4 years) |

| Improved clinical convenience versus daily or short-cycle methods | +0.7% | Global, especially North America & EU | Short term (≤ 2 years) |

| Extended product duration and label updates supporting replacement cycles | +0.5% | North America & EU primary, Global secondary | Short term (≤ 2 years) |

| Growing demand for hormone delivery options beyond contraception | +0.4% | North America, Europe, East Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Preference for Long-Acting Reversible Contraception

The hormonal implants market benefits from a strong clinical value proposition, as implants provide high real-world effectiveness and remove the adherence burden linked to daily methods. The CDC reported in 2025 that implants and IUDs together accounted for 10.5% of contraceptive use among U.S. women aged 15 to 49, with adoption highest among women aged 20 to 29 at 13.8%.[1]Centers for Disease Control and Prevention, “Contraceptive Use Among Women Aged 15–49 in the United States,” CDC National Center for Health Statistics, cdc.gov

FP2030 reported in 2025 that implants were the most common contraceptive method in 13 countries and the second most common method in 17 others, indicating broader adoption across public health systems. A 2025 article available through PMC also highlighted a sustained rise in LARC uptake across surveyed populations, reinforcing the market’s long-term demand potential.[2]Organon & Co., “Organon Announces US Food and Drug Administration Approval of Supplemental New Drug Application Extending Duration of Use of NEXPLANON® (Etonogestrel Implant) 68 Mg Radiopaque,” Organon, organon.com

Expansion of Postpartum and Post-Abortion Family Planning Programs

The hormonal implants market is gaining momentum as healthcare systems integrate contraceptive access into delivery and post-procedure care pathways. A 2025 study published through PMC found that structured hospital-based postpartum family planning programs increased postpartum LARC insertions within 60 days of delivery by 11.7 percentage points in early-adopting sites.[3]Apollo Global Management, “Bayer Secures 3.0 Billion Euros to Improve Capital Structure,” Apollo Global Management, apollo.com UNFPA reported that postpartum family planning indicators were embedded into national health information systems across 54 countries in 2024, enabling governments to monitor uptake and support continued funding. These pathways improve completion rates for implant insertion and expand access to clinically suitable patients beyond standalone outpatient visits.

Extended Product Duration and Label Updates Supporting Replacement Cycles

The hormonal implants market received an important product and policy boost when the FDA approved a longer NEXPLANON use period in January 2026. Organon reported that the supplemental approval extended the device’s use from 3 years to 5 years, and the supporting trial recorded zero pregnancies during years 4 and 5, with no new safety signals across a wide BMI range. This update improves value per insertion and strengthens the market’s position in systems that assess the total cost of ownership across contraceptive options. However, longer duration reduces replacement frequency, requiring suppliers to expand first-time user adoption while the new REMS requirement increases the importance of provider training.

Wider Access Through Public Procurement and Donor-Funded Supply Chains

The hormonal implants market relies heavily on procurement systems in Africa and Asia, where governments and multilateral agencies shape access more directly than retail channels. UNFPA reported that its Supplies Partnership procured USD 141 million in reproductive health commodities in 2024, enabled 25 million women to access services, delivered 43 million couple-years of protection, and recorded implants at 19% of the method mix across partner countries. The market also faced a funding shock in 2025, but CHAI noted that some countries increased domestic reproductive health allocations. This shift could reduce exposure to donor cycle volatility and improve tender visibility for commercial suppliers.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Provider training requirements for insertion and removal | -1.2% | Global, highest in APAC & MEA | Short term (≤ 2 years) |

| Adverse event perception and discontinuation concerns | -0.9% | Global, highest in North America & Europe | Short term (≤ 2 years) |

| Dependence on reimbursement, procurement, and policy coverage | -1.3% | Sub-Saharan Africa, APAC, MEA | Medium term (2-4 years) |

| Substitution pressure from intrauterine devices and injectable contraceptives | -1.0% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Dependence on Reimbursement, Procurement, and Policy Coverage

The hormonal implants market remains sensitive to financing decisions, as product access often depends on reimbursement rules, public tenders, and policy continuity. CHAI reported that Zambia experienced a major supply disruption in March 2025, with Jadelle availability declining to 34% facility availability in Lusaka Province after USAID withdrew funding. Such disruptions are significant because, in many low-income settings, the hormonal implants market cannot quickly replace donor-supported supply through private distribution. In the United States, the transition to the NEXPLANON REMS program also created a temporary access risk, as clinics that did not complete certification could not order or dispense the device after the compliance deadline. Smaller suppliers also face a higher compliance burden when reimbursement and regulatory standards change simultaneously. As a result, the hormonal implants market can grow on strong demand fundamentals while still facing interruptions when funding or policy mechanisms shift too quickly.

Provider Training Requirements for Insertion and Removal

The hormonal implants market faces limitations because insertion and removal require trained providers rather than routine self-administration. Implant placement is a minor procedure, but removal can become more difficult when the device migrates or is positioned incorrectly, making clinical skill central to safe use. Organon stated in 2026 that the FDA required formal REMS certification for NEXPLANON providers, indicating that training quality remained an active issue even in mature parts of the hormonal implants market. CHAI also reported that disruptions in provider capacity building affected 6 of 11 surveyed countries in 2025, meaning supply expansion did not always align with clinical readiness in the hormonal implants market. FOGSI addressed this issue in April 2025 through a position statement that standardized guidance on subdermal implant training, offering a practical model for the hormonal implants market in other countries.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Five-Year Label Drives Etonogestrel Consolidation

Etonogestrel implants accounted for 45.65% of the hormonal implants market size in 2025, keeping them in the lead across product categories. Their single-rod format reduced insertion complexity by requiring only one placement site and a preloaded applicator. This simpler procedure supported provider efficiency in consultations and insertions, with less room for technique variation than older multi-rod systems. The January 2026 FDA label extension for NEXPLANON from three years to five years further strengthened this position by improving the cost per protected year and supporting payer confidence.

Levonorgestrel implants were the fastest-growing product segment, with an 8.93% CAGR through 2031, supported by strong public sector demand and wider use in cost-sensitive tenders. The July 2026 Apollo investment in Bayer’s LARC business, which includes Jadelle, and the portfolio’s 12.5% growth in 2025 reinforced confidence in this segment of the hormonal implants market. Competition in this tier also broadened, as WHO-prequalified two-rod products were well-positioned in large-volume procurement programs.

By Application: HRT Demand Reshapes the Non-Contraceptive Pipeline

Contraception held 38.23% of revenue in 2025, making it the largest application base in the hormonal implants market. This position reflected its established use in both reimbursed private systems and donor-supported public programs. UNFPA reported that implants represented 19% of the contraceptive method mix across 54 partner countries in 2024, while FP2030 reported in 2025 that implants were the leading method in 13 countries. This broad base gave the hormonal implants market a stable volume foundation, even when replacement timing changed.

Menstrual regulation and other therapeutic uses also became more visible, as clinicians increasingly recognized hormonal effects that could reduce bleeding in selected users. Hormone replacement therapy was the fastest-growing application in the hormonal implants market, with a projected 9.67% CAGR through 2031. This segment gained interest because subcutaneous estradiol pellets could provide steadier hormone levels over several months and avoid first-pass liver metabolism, strengthening the clinical case for selected patients.

By End User: Clinics Lead but Community Health Integration Accelerates

Gynecology and fertility clinics held 46.34% of the hormonal implants market share in 2025, making them the leading end-user setting. These clinics led because they already had trained staff, insertion equipment, and established reproductive health workflows. The hormonal implants market continued to rely heavily on these capabilities because specialist clinics naturally supported provider certification, patient counseling, and follow-up care. Hospitals ranked behind clinics but remained important because they captured postpartum and post-abortion insertions that later outpatient visits might otherwise miss.

In India, Implanon NXT expanded to 16 states by 2024 through the national family planning program, while community-based delivery through auxiliary nurse midwife networks became a key part of scale-up in the hormonal implants market. In Washington State, a government report covering 2024 to 2025 found that same-day LARC insertion rates at federally qualified health centers rose by 111% when stock and trained staff were available together. This showed that service design directly affected access. The pattern suggested that the hormonal implants market could expand beyond specialist care if stakeholders integrated training and product availability into routine primary care delivery.

By Distribution Channel: Public Procurement Dominates Volume and Momentum

Public procurement represented 58.88% of the hormonal implants market size in 2025, making it the dominant distribution route by a wide margin. This reflected the role of governments and multilateral agencies as the main buyers across several high-volume countries. The hormonal implants market depended on these channels because tender systems shaped pricing, product eligibility, and long-term planning more strongly than retail sales. UNFPA’s 2024 procurement activity and country program support showed how central this model remained to the hormonal implants market in partner countries.

WHO prequalification and similar compliance filters also kept distribution concentrated among suppliers that could meet strict quality and tender requirements. Public procurement was also the fastest-growing channel in the hormonal implants market, with a projected 9.78% CAGR through 2031. This momentum was tied to domestic budget expansion, procurement formalization, and the need to stabilize supply after donor-related disruptions in 2025.

Geography Analysis

North America held 38.56% of the hormonal implants market share in 2025, keeping it ahead of every other region by revenue. The United States supported this position through higher per-unit pricing, broad reimbursement, and a large provider base experienced in implant counseling and insertion. The January 2026 NEXPLANON label extension strengthened product value in North America, although the REMS transition may have temporarily limited ordering at clinics that did not complete certification on time. Europe remained the second-largest regional block, supported by reimbursement systems in Germany, France, and the United Kingdom, while the United Kingdom’s 2026 approval of a 5-year NEXPLANON duration supported cost-effectiveness and improved value per patient.

The Asia-Pacific hormonal implants market size is projected to expand at an 8.56% CAGR through 2031, making it the fastest-growing regional market. India illustrated the regional growth pattern, as the national family planning scale-up broadened the delivery footprint for Implanon NXT and linked growth to public health access programs. In Indonesia, the REACH project launched in June 2026 through UNFPA, Organon, and public sector partners to support more equitable family planning access and stronger domestic financing foundations. Higher-income Asian markets, such as Japan, South Korea, China, and Australia, also added a second layer of opportunity as HRT and other non-contraceptive uses started gaining attention in the hormonal implants market.

The Middle East and Africa and South America were smaller than North America and Europe by revenue in 2025, but they remained important volume growth corridors in the hormonal implants market. Sub-Saharan Africa remained especially important, as large public procurement programs drove method uptake, although tighter pricing and supply interruptions had a stronger effect on access. CHAI’s 2025 findings from Zambia showed how quickly availability could decline when donor-backed supply weakened, highlighting the need for dual sourcing and stronger national buffers. South America stood out as Brazil’s public system sharply expanded implant access, creating a clear example of large-scale national procurement and service rollout.

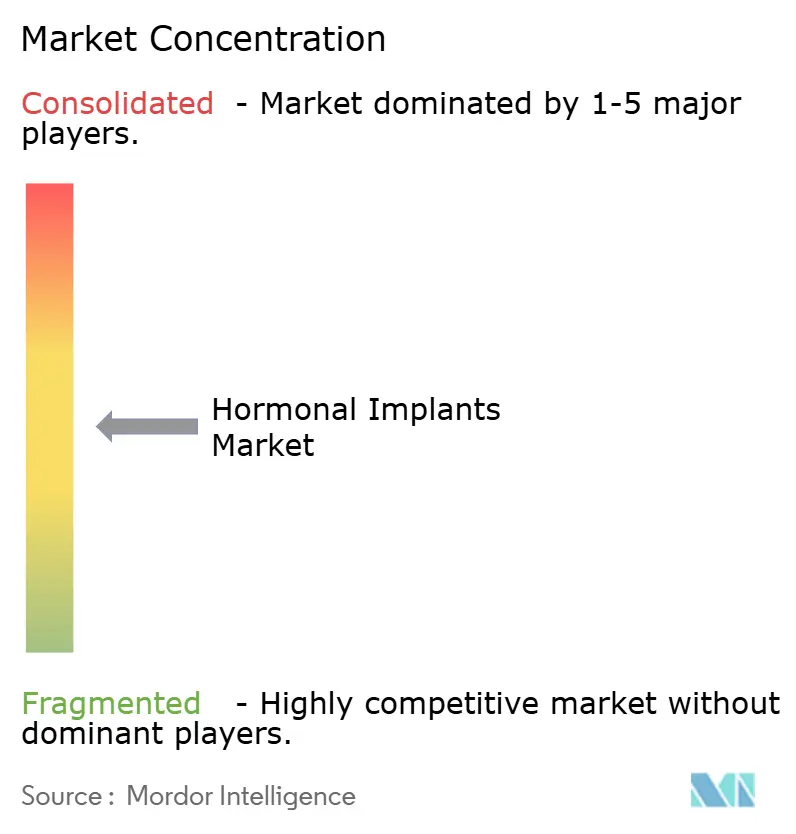

Competitive Landscape

The hormonal implants market showed moderate concentration in branded products and broader fragmentation in access-focused supply. Organon and Bayer remained the two most visible branded players, supported by strong clinical recognition for NEXPLANON, Implanon NXT, and Jadelle, established provider training programs, and deep ties to public sector or reimbursed channels. However, regional control varied, with Organon stronger in North America and parts of Asia, while Bayer held a firmer position in sub-Saharan Africa and selected public programs in Latin America. Organon’s 2025 annual filing showed that worldwide NEXPLANON sales declined by 4% in 2025, while Bayer’s LARC portfolio posted 12.5% growth in the same year, indicating that performance increasingly depended on channel mix and geography rather than brand strength alone.

Strategic moves in 2026 clarified the competitive direction of the hormonal implants market. Organon secured FDA approval to extend NEXPLANON use to five years and moved into a REMS-based provider certification model, linking product access more closely to training infrastructure and compliance management. Bayer separated part of its LARC value into a new entity and attracted EUR 3 billion, or USD 3.4 billion, from Apollo, underscoring confidence in the market’s cash flow resilience. At the next tier, Aspen Pharmacare, Gedeon Richter, Amneal Pharmaceuticals, and Cadila Healthcare competed through regional distribution or generic pathways, while DKT International and Population Council influenced access-focused deployment in lower-income settings.

Biodegradable platforms also emerged as a disruptive pathway in the hormonal implants market. FHI 360’s Phase I work on Casea S was important because it could eliminate the need for device extraction and reduce a key service barrier to adoption. WHO prequalification remained a major competitive filter, as qualified suppliers were better positioned to win multilateral tenders and scale through public procurement systems. Digital training and remote provider education gained relevance as regulatory requirements made certification speed and provider reach key competitive factors.

Hormonal Implants Industry Leaders

Bayer AG

Merck & Co., Inc.

AbbVie Inc.

Pfizer Inc.

Teva Pharmaceutical Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Bayer AG secured EUR 3 billion (USD 3.4 billion) from Apollo Global Management for a minority, non-controlling stake in a new entity holding its LARC business, including Jadelle, Mirena, Kyleena, and Jaydess.

- June 2026: UNFPA Indonesia launched the REACH project with the Indonesian Ministries of Population and Health, supported by Organon’s 2026 Her Health Grant, to improve family planning access and financing sustainability.

- May 2026: The United Kingdom approved a 5-year labeled duration for NEXPLANON in women of reproductive potential, supported by trial data showing zero pregnancies during extended use.

- January 2026: The FDA approved Organon’s supplemental application for NEXPLANON, extending approved use from 3 years to 5 years, and introduced a REMS program for certified US providers.

Global Hormonal Implants Market Report Scope

As per the scope of the report, a hormonal implant (also known as a contraceptive implant) is a small, flexible rod about the size of a matchstick. A healthcare provider inserts it just beneath the skin of the upper arm. It slowly releases a hormone to prevent pregnancy for up to 3 to 5 years.

The hormonal implants market is segmented by product type, application, end user, distribution channel, and geography. By product type, the market includes etonogestrel implants, levonorgestrel implants, and other hormonal implants. By application, the market is segmented into contraception, hormone replacement therapy, menstrual regulation, and other therapeutic applications. By end user, the market is segmented into hospitals, gynecology and fertility clinics, community health centers, ambulatory surgical centers, and other end users. By distribution channel, the market is segmented into public procurement, private healthcare procurement, and retail and pharmacy channels. By geography, the market is analyzed across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Etonogestrel Implants |

| Levonorgestrel Implants |

| Other Hormonal Implants |

| Contraception |

| Hormone Replacement Therapy |

| Menstrual Regulation |

| Other Therapeutic Applications |

| Hospitals |

| Gynecology and Fertility Clinics |

| Community Health Centers |

| Ambulatory Surgical Centers |

| Other End Users |

| Public Procurement |

| Private Healthcare Procurement |

| Retail and Pharmacy Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Etonogestrel Implants | |

| Levonorgestrel Implants | ||

| Other Hormonal Implants | ||

| By Application | Contraception | |

| Hormone Replacement Therapy | ||

| Menstrual Regulation | ||

| Other Therapeutic Applications | ||

| By End User | Hospitals | |

| Gynecology and Fertility Clinics | ||

| Community Health Centers | ||

| Ambulatory Surgical Centers | ||

| Other End Users | ||

| By Distribution Channel | Public Procurement | |

| Private Healthcare Procurement | ||

| Retail and Pharmacy Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the hormonal implants sector in 2026?

The hormonal implants market size is USD 0.91 billion in 2026 and is forecast to reach USD 1.25 billion by 2031 at a 6.49% CAGR.

Which product category leads revenue generation?

Etonogestrel implants led product revenue with a 45.65% share in 2025, supported by easier insertion and stronger branded positioning.

Which application is growing the fastest through 2031?

Hormone replacement therapy is the fastest growing application, with a projected 9.67% CAGR through 2031.

Why does public procurement matter so much for this space?

Public procurement held 58.88% revenue share in 2025 and is also the fastest growing distribution channel at 9.78% CAGR, making government and donor linked purchasing central to demand.

Which region shows the strongest growth outlook?

Asia-Pacific is the fastest growing regional market, with an expected 8.56% CAGR through 2031, supported by family planning scale up in countries such as India and Indonesia.

What are the main risks that could slow adoption?

The main risks are provider training requirements, reimbursement and procurement dependence, and supply disruptions when policy or donor funding changes too quickly.

Page last updated on: