Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

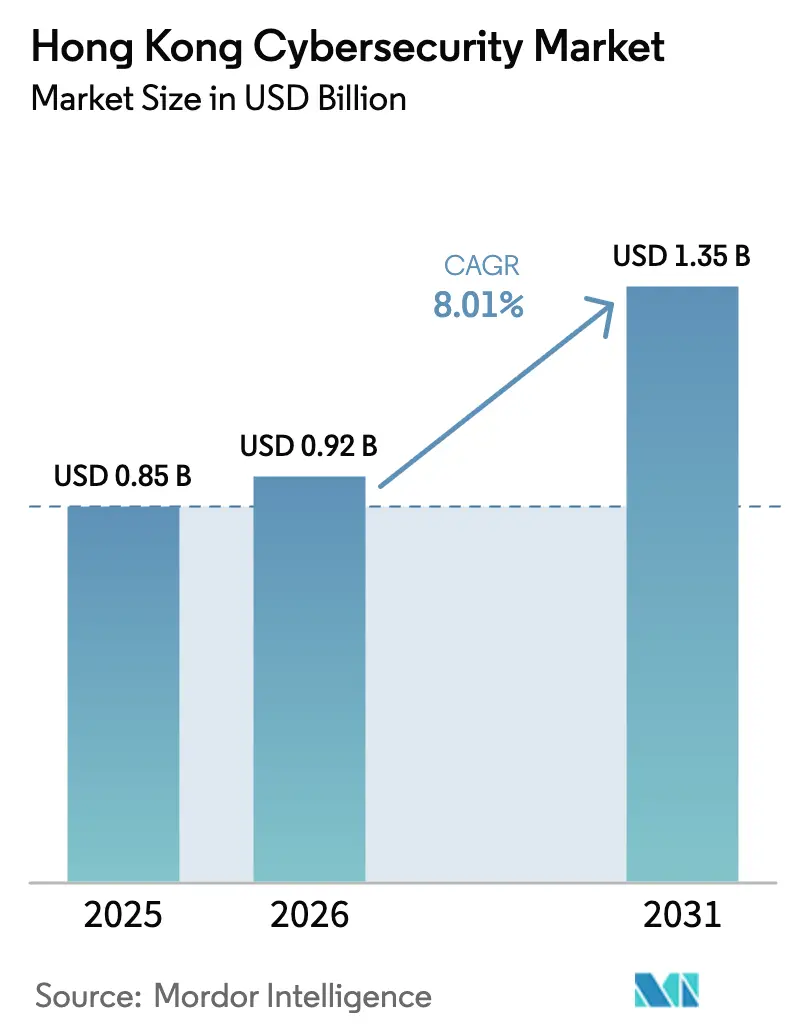

| Base Year Market Size (2025) | USD 0.85 Billion |

| Market Size (2026) | USD 0.92 Billion |

| Market Size (2031) | USD 1.35 Billion |

| Growth Rate (2026 - 2031) | 8.01% CAGR |

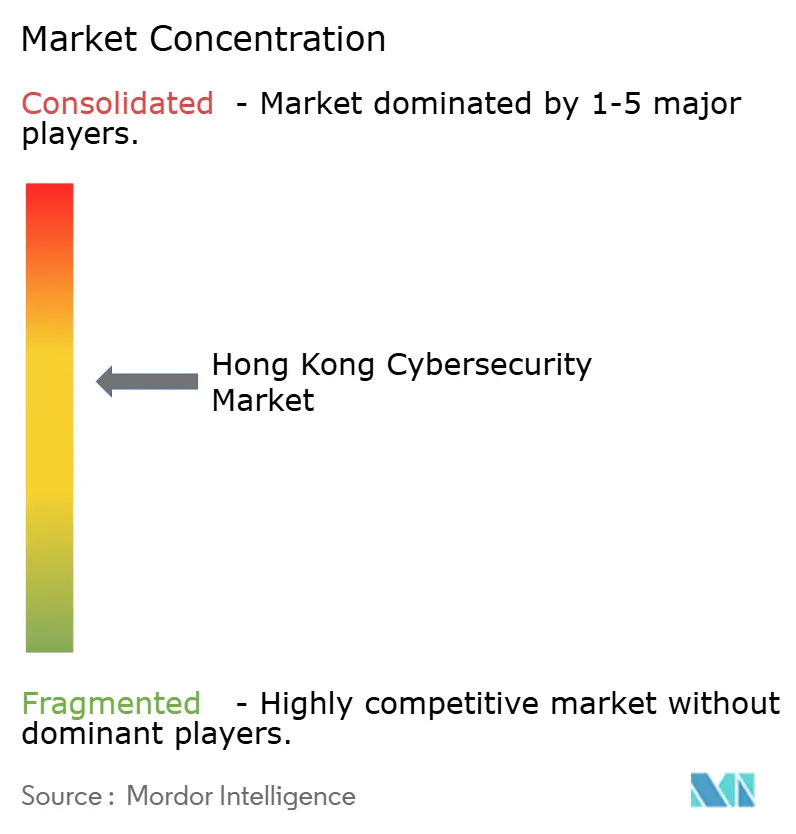

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hong Kong Cybersecurity Market Analysis by Mordor Intelligence

Hong Kong cybersecurity market size in 2026 is estimated at USD 0.92 billion, growing from 2025 value of USD 0.85 billion with 2031 projections showing USD 1.35 billion, growing at 8.01% CAGR over 2026-2031. Heightened regulatory scrutiny, especially the Protection of Critical Infrastructures (Computer Systems) Ordinance enacted in March 2025, is pivoting budget allocations from discretionary tools to mandated risk-assessment and incident-response capabilities. Escalating attack volumes, exemplified by 12,536 incidents logged by HKCERT in 2024, keep threat visibility top of mind while cross-border data-flow pressures encourage demand for data-loss-prevention platforms [1]Hong Kong Computer Emergency Response Team, “Cyber Security Outlook 2025,” hkcert.org. Enterprises that once favored single-purpose appliances now seek integrated platforms to rein in tool sprawl, and capital-efficient SMEs accelerate adoption of managed detection services that offset bilingual talent shortages. Strategic public funding of USD 24 billion for the technology economy, paired with more than 4,200 active startups, strengthens local innovation pipelines and fosters partnerships between global vendors and territorial specialists.

Key Report Takeaways

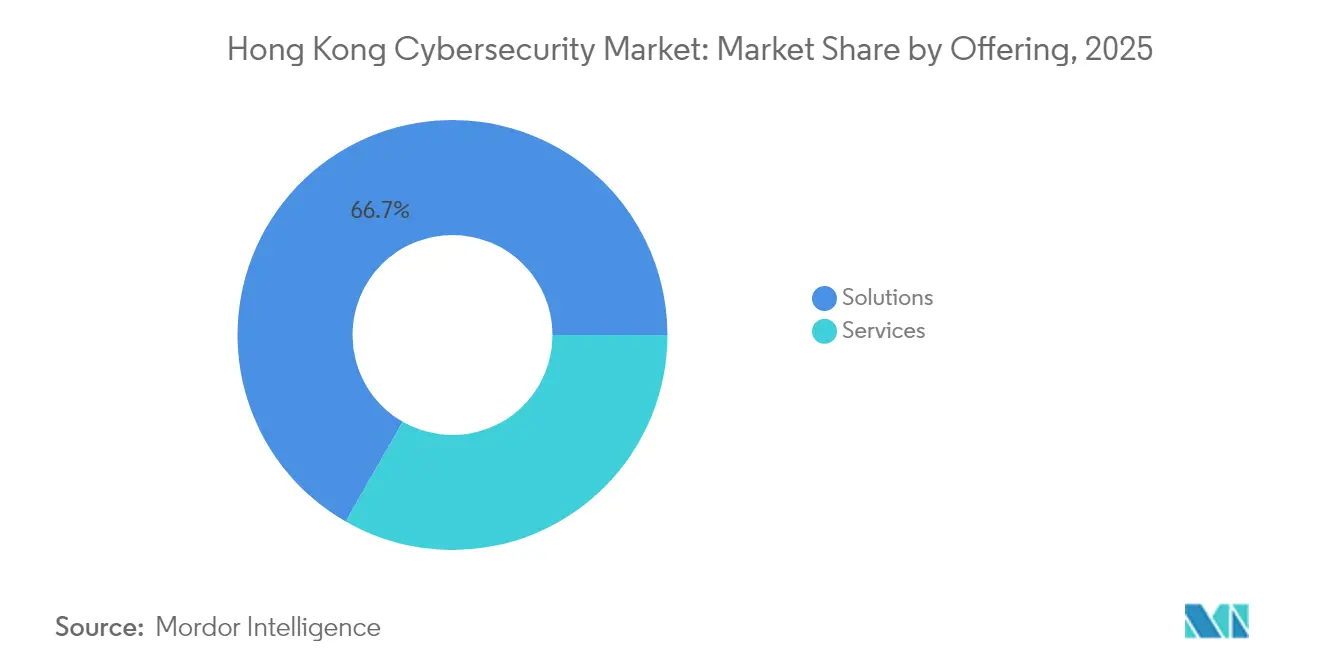

- By offering, Solutions led with 66.72% Hong Kong cybersecurity market share in 2025, whereas Managed Services is forecast to advance at an 11.02% CAGR through 2031.

- By deployment mode, On-Premise implementations accounted for 73.92% of the Hong Kong cybersecurity market size in 2025; cloud-delivered security is expanding at a 12.14% CAGR.

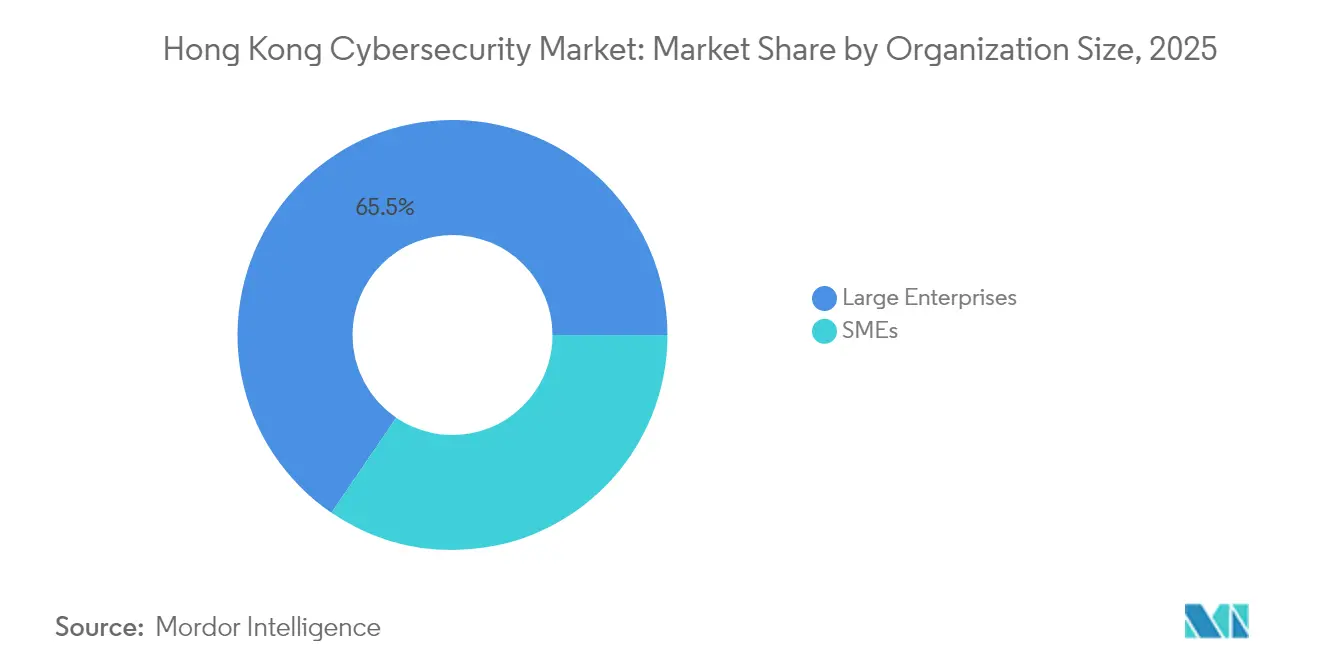

- By organization size, Large Enterprises held 65.48% revenue share in 2025, while SMEs record the fastest 12.93% CAGR to 2031.

- By end-user vertical, BFSI captured 28.12% revenue in 2025; Healthcare is projected to grow the quickest at 14.12% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Hong Kong Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compliance with PDPO amendments and critical-infrastructure law | +2.1% | Hong Kong, Greater Bay Area | Short term (≤ 2 years) |

| Smart City Blueprint 2.0 investment | +1.8% | Hong Kong, New Territories | Medium term (2-4 years) |

| Virtual banking and FinTech surge | +1.6% | Hong Kong, ASEAN corridors | Short term (≤ 2 years) |

| Hybrid and multi-cloud adoption | +1.4% | Hong Kong with mainland integration | Medium term (2-4 years) |

| Cross-border data-transfer scrutiny | +1.2% | Hong Kong–mainland corridor | Long term (≥ 4 years) |

| Government USD 24 billion tech-economy investment | +1.0% | Hong Kong | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory Compliance with Hong Kong PDPO Amendments and Sector-specific Regulations Accelerating Security Spend

The 2025 Critical Infrastructures Ordinance imposes statutory obligations that cover risk assessments, incident disclosure, and formation of security management units. Non-compliance can jeopardize operating licences, which pushes boards to approve accelerated procurement cycles for governance-driven solutions. Vendors that demonstrate audit-ready reporting functions and bilingual support gain preferred-bidder status. Large enterprises re-evaluate fragmented tool stacks in favour of platforms that integrate vulnerability, asset, and compliance dashboards. The law also stimulates professional-services demand as organizations seek external validation of control maturity. Perceived regulatory leadership differentiates the Hong Kong cybersecurity market from regional peers, making compliance posture a competitive advantage in foreign-direct-investment decisions.

Hong Kong Smart City Blueprint 2.0 Driving Critical-Infrastructure Cybersecurity Investments

The USD 24 billion technology allocation earmarks funds for IoT-centric public services such as smart lampposts, e-mobility charging stations, and intelligent traffic control. Each new sensor node enlarges the attack surface, prompting utilities to procure operational-technology (OT) security gateways and real-time anomaly-detection software. Public tenders now require secure-by-design credentials, pushing integrators to embed encryption at chip level. Multi-vendor ecosystems demand centralized visibility to reconcile disparate device protocols, fostering uptake of AI-driven security orchestration platforms. The initiative ties vendor performance metrics to citizen-data protection benchmarks, thereby raising the bar for privacy-enhancing technologies. Blueprint deadlines through 2030 ensure sustained demand for life-cycle services ranging from threat-modelling to penetration testing [2]Alex Yi, “Smart City Blueprint 2.0 Funding Details,” hkcert.org.

Rapid Surge in FinTech and Virtual Banking Requiring Robust Security Architectures

Eight virtual banks serve a digitally native clientele, processing high-volume micro-transactions via API ecosystems. Continuous KYC verification and behavioural fraud analytics become critical because regulatory sandboxes still require real-time oversight. Cloud-native architectures bring agility but expose misconfiguration risks, so banks deploy continuous compliance scanners tailored to HKMA guidelines. Payment tokens traversing multiple jurisdictions heighten cryptographic-key management complexity, accelerating demand for hardware security modules delivered as service. FinTech scale-up cycles favour modular security components that adapt without re-engineering underlying apps. Established vendors bundle threat-intelligence feeds tuned to financial malware trends, creating cross-sell synergies into insurance and wealth-management sub-segments.

Hybrid/Multi-Cloud Adoption Boosting Demand for Cloud-Native Security Platforms

Pandemic-era remote-work policies normalised SaaS usage, but data-residency clauses compel enterprises to juggle international and mainland-hosted clouds. Configuration-drift across providers causes visibility gaps that legacy firewalls cannot bridge, fuelling interest in cloud-security-posture-management (CSPM) suites. CISOs pivot from tool counts to coverage metrics, favouring platforms able to unify identity, workload, and data-classification telemetry. Automated policy enforcement reduces manual review cycles and mitigates bilingual talent shortages. Large retailers extend zero-trust policies to branch stores via secure-access service edge (SASE) nodes for consistent user experience. Continuous encryption-key management across sovereign clouds positions the Hong Kong cybersecurity industry for specialist service growth.

Cross-Border Data-Transfer Scrutiny Fueling Data-Loss-Prevention Solutions

Data transfers between Hong Kong and mainland partners must satisfy PRC residency rules while preserving international client confidentiality. Enterprises implement granular content-inspection engines that auto-classify records by jurisdictional sensitivity. Inline tokenisation protects customer identifiers during analytics workflows hosted outside the territory. Legal teams demand audit trails that map every cross-border packet to policy outcomes, improving dispute-resolution readiness. Vendors partner with telcos to embed DLP at network edge elements, reducing latency for financial transactions. The resulting controls create replicable blueprints for other Greater Bay Area jurisdictions, bolstering export prospects for Hong Kong-engineered compliance tools.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bilingual cybersecurity talent shortage | -1.3% | Hong Kong, regional competition | Long term (≥ 4 years) |

| Legacy systems within public sector | -0.9% | Hong Kong government agencies | Medium term (2-4 years) |

| High cost of threat-intelligence services for SMEs | -0.7% | Hong Kong SMEs | Short term (≤ 2 years) |

| Fragmented OT security guidance | -0.5% | Critical-infrastructure operators | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Severe Shortage of Bilingual Cybersecurity Talent

Fluency in Cantonese, Mandarin, and English is prerequisite for many security roles because compliance documentation, vendor consoles, and regulatory submissions span these languages. Scarcity inflates salaries by more than 30% over regional averages, straining mid-tier enterprise budgets. University programmes graduate fewer than 400 cybersecurity majors yearly, far below estimated demand. Visa processing delays make it hard to import foreign specialists, so firms outsource monitoring to managed security service providers (MSSPs). Dependence on external SOCs raises vendor-lock risks and limits bespoke policy tuning. Government upskilling grants alleviate entry-level gaps yet do not bridge senior-architect shortages, prolonging project timelines.

Persistent Legacy Systems Within Public Sector Hindering Modernisation

Mainframe-based workflows inside tax, immigration, and transport agencies resist integration with modern endpoint telemetry. Middleware customization inflates project overhead and introduces uncatchable code paths that attackers exploit. Procurement rules prioritize proven suppliers, hampering pilot adoption of innovative zero-trust fabric. Downtime tolerance is low due to citizen-service mandates, so agencies favour incremental patching over transformative re-platforming. Budget cycles tied to legislative approval add another layer of delay. These factors collectively curb large-scale upgrades, postponing realization of full-spectrum cyber resilience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Solutions Dominance Drives Market Foundation

Solutions generated USD 567.12 million in 2025, equal to 66.72% Hong Kong cybersecurity market share, as enterprises sought unified control planes covering network, endpoint, and application domains. Application-security toolkits gain favour among FinTech platforms that run continuous deployment pipelines, while cloud-security gateways underpin SaaS adoption in professional-services firms. Endpoint detection and response adoption increases after HKCERT traced 45% of last year’s incidents to compromised laptops and smartphones. Data-security suites that combine tokenization with format-preserving encryption see heightened demand within healthcare providers following widely publicized breaches.

Managed Services is forecast to record an 11.02% CAGR to 2031, raising its revenue from USD 314.06 million in 2026 to more than USD 529.66 million by the end of the decade. MSSPs bundle threat hunting, incident response, and compliance reporting to offset end-user talent shortages, especially among SMEs. Large banks co-source security operations to gain 24/7 coverage without incurring additional headcount, while cloud-native MSSPs use automation to keep margins healthy. Professional services revenue grows steadily as new regulations require third-party audits of risk postures. Vendors that combine advisory, solution resale, and managed services position themselves as one-stop shops, securing multi-year contracts that dampen churn.

By Deployment Mode: On-Premises Preference Meets Cloud Acceleration

On-Premises deployments contributed 73.92% revenue in 2025 because financial institutions remain wary of sensitive-data exfiltration and prefer direct hardware control aligned with regional data-residency statutes. Banks invest in high-density next-generation firewalls and on-prem key-management appliances to meet intraday settlement latency targets. Costly real-estate and power-density constraints motivate appliance consolidation, spurring interest in unified threat-management devices that combine firewall, IPS, and DDoS mitigation functions.

Cloud-delivered protections are poised for a 12.14% CAGR, expanding from USD 248.6 million in 2026 to almost USD 441.2 million by 2031. SMEs gravitate toward SaaS security because operating-expense models avoid upfront capital investments. Continuous feature updates allow quick alignment with evolving PDPO clauses, which is critical as regulators may issue guidelines with short compliance windows. Hybrid architectures gain traction inside conglomerates that offload non-customer-identifiable workloads to public clouds while retaining crown-jewel data on private clouds housed in local co-location facilities. This blend drives procurement of CASB, CSPM, and container-security modules that secure workloads irrespective of hosting venue.

By Organization Size: Enterprise Leadership Faces SME Disruption

Large Enterprises commanded 65.48% revenue in 2025, equivalent to almost USD 556.58 million within the Hong Kong cybersecurity market. Their global connectivity mandates premium threat feeds, sandboxing, and red-team exercises. Multinational insurers integrate security-scorecard outputs into vendor-risk programmes, expanding demand for third party-risk monitoring tools. Enterprise footprints extend into mainland subsidiaries, requiring bilingual dashboards that reconcile PRC and Hong Kong compliance artefacts. Budget resilience allows experimentation with AI-driven detection engines, accelerating proof-of-concept cycles.

SMEs will see the briskest 12.93% CAGR, enlarging their collective spending from USD 331.32 million in 2026 to beyond USD 608.5 million in 2031. Government subsidies such as Cyberport’s Digital Transformation Support Pilot reimburse up to 50% of eligible cybersecurity spend, lowering adoption barriers. Vendor product teams strip back feature saturation to offer simplified consoles that busy SMB owners can master in days. Bundled endpoint, email, and backup protection delivered via subscription resonates with retailers and micro-exporters that lack dedicated IT staff. Channel partners that pair cybersecurity with managed infrastructure win share because SMEs prefer single invoices for all technology services.

By End-User Vertical: BFSI Dominance Meets Healthcare Innovation

The BFSI community generated 28.12% of overall revenue, translating to USD 239.02 million in 2025, underscoring its centrality to the Hong Kong cybersecurity market size. Trading houses deploy ultra-low-latency packet inspection appliances to protect algorithmic strategies, while insurers focus on identity-proofing technologies that reduce synthetic-identity fraud. The Hong Kong Monetary Authority’s virtual-banking framework obliges continuous security-posture reporting, which fuels demand for automated compliance dashboards. FinTech firms embed runtime-application-self-protection (RASP) inside mobile apps to guard against overlay attacks that bypass two-factor authentication.

Healthcare spending is forecast to rise at 14.12% CAGR, elevating its outlay from USD 63.91 million in 2026 to nearly USD 123.7 million by 2031. Hospitals digitise radiology workflows and telehealth portals, increasing exposure of personally identifiable patient data. After several high-profile breaches, the Department of Health mandates encryption of data at rest and in transit, making tokenisation platforms standard. Connected medical devices demand network segmentation along clinical engineering corridors, introducing opportunities for OT-oriented micro-segmentation vendors. Research labs handling genomic data adopt privacy-preserving computation to enable cross-institution collaboration without revealing raw datasets.

Geography Analysis

Hong Kong is both a demand centre and an export springboard, making the Hong Kong cybersecurity market a regional bellwether for Greater Bay security innovation. The city’s dense fibre footprint enables MSSPs to operate latency-sensitive SOC services, which attract multinational corporations seeking consistent regional coverage. Integration with Shenzhen supply-chain partners forces enterprises to adopt policy engines capable of distinguishing data flows subject to PRC Cybersecurity Law from those governed by PDPO standards, thereby elevating DLP and encryption spending.

Physical constraints drive operators to vertical data-centre designs, which in turn heighten emphasis on airflow-aware rack-level fire-suppression and environmental monitoring as part of holistic security postures. Proximity to regional subsea cable landing stations bolsters Hong Kong’s appeal for global cloud providers, which strengthens the case for sovereignty-aligned cloud-security controls. Time-zone overlap with Tokyo and Singapore allows security teams to leverage follow-the-sun monitoring models that reduce incident-response gaps.

Cross-border collaboration directives within the Greater Bay Area elevate adoption of secure-collaboration SaaS that embeds data classification at object level. Government negotiations on mutual recognition of e-signatures introduce new demand for cryptographic interoperability testing. Investors view Hong Kong’s predictable common-law framework as risk mitigating compared with mainland markets, which encourages long-term cyber-infrastructure bets. The resulting capital inflow supports local RandD hubs focused on post-quantum encryption and AI-based anomaly detection.

Competitive Landscape

The vendor ecosystem is moderately fragmented, with the top five providers accounting for roughly 42% of the Hong Kong cybersecurity market. Global leaders such as Palo Alto Networks and Fortinet bundle subscriptions spanning firewall, SD-WAN, and cloud-security modules, winning large-enterprise renewals through platform breadth. Local champion HKT Trust differentiates with bilingual SOC analysts and tight integration with its fixed-line and 5G networks, securing municipal and SME contracts.

Strategic alliances emerge as vendors race to add regulatory functions. CITIC Telecom CPC launched its ICT-MiiND framework that layers AI pentesting over managed connectivity, appealing to manufacturers that want single-supplier simplicity. Meanwhile, Blackpanda focuses on incident-response retainers, and its USD 6.7 million Series A financing underwrites expansion of digital-forensics capacity that complements preventive-control vendors[3]Blackpanda Pte Ltd, “Series A Funding Press Release,” blackpanda.com . Cloud-security start-ups capitalize on niche opportunities such as container hardening for DevSecOps pipelines, but consolidation looms as customers demand broader coverage.

Pricing power tilts toward vendors offering integrated suites because buyers value tool-chain reduction. However, compliance specialization creates a viable lane for boutique consultancies that translate legislation into control frameworks. Channel partners encompassing telcos, global integrators, and value-added resellers negotiate revenue-sharing deals tied to recurring licenses. Market entry barriers remain moderate given open procurement in the private sector, yet public-sector certification requirements advantage incumbents with proven track records.

Hong Kong Cybersecurity Industry Leaders

IBM Corporation

Digitpol

Rackspace Technology

Maximus

Edvance International Holdings Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Hong Kong Legislative Council passed the Protection of Critical Infrastructures (Computer Systems) Ordinance, instituting statutory cybersecurity duties across eight sectors.

- January 2025: HKCERT released “Hong Kong Cyber Security Outlook 2025,” reporting 12,536 incidents in 2024 and spotlighting phishing as the fastest-growing threat vector.

- September 2024: Blackpanda secured USD 6.7 million in Series A funding to expand cyber emergency-response services across Asia.

- July 2024: HKT launched the HKT POS mobile application with embedded security features for SME electronic payments.

Hong Kong Cybersecurity Market Report Scope

Cybersecurity solutions help an organization monitor, detect, report, and counter cyber threats that are internet-based attempts to damage or disrupt information systems and hack critical information using spyware and malware, and phishing, to maintain data confidentiality. The study is structured to track the revenues accrued by cybersecurity vendors through sales of various solutions and allied services.

Hong Kong cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security Equipment | |

| Endpoint Security | |

| Other Solutions | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| On-Premise |

| Cloud |

By Organization Size

| SMEs |

| Large Enterprises |

By End-User Vertical

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Retail |

| Energy and Utilities |

| Manufacturing |

| Others |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security Equipment | ||

| Endpoint Security | ||

| Other Solutions | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premise | |

| Cloud | ||

| By Organization Size | SMEs | |

| Large Enterprises | ||

| By End-User Vertical | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Retail | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

Key Questions Answered in the Report

What is the current size of the Hong Kong cybersecurity market?

The Hong Kong cybersecurity market size is USD 0.92 billion in 2026 and is forecast to grow at an 8.01% CAGR to USD 1.35 billion by 2031.

Which offering category leads spending in Hong Kong?

Solutions account for 66.72% market share in 2025, driven by demand for integrated platforms that simplify compliance and threat management.

Why are managed security services growing quickly?

A shortage of bilingual cybersecurity professionals pushes organizations, especially SMEs, to outsource monitoring and incident response, propelling managed services at an 11.02% CAGR.

How does new regulation influence cybersecurity investment?

The Critical Infrastructures Ordinance mandates risk assessments and incident reporting, compelling companies to accelerate purchase of governance-ready security tools.

Which vertical will grow the fastest through 2031?

Healthcare is projected to expand at 14.12% CAGR as hospitals digitize records and comply with stricter patient-data protection requirements.

What deployment approach is gaining traction among SMEs?

Cloud-delivered security is rising at a 12.14% CAGR because subscription models lower upfront costs and simplify management for resource-constrained firms.

Page last updated on: