Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 29.23 Billion |

| Market Size (2031) | USD 41.12 Billion |

| Growth Rate (2026 - 2031) | 7.06% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

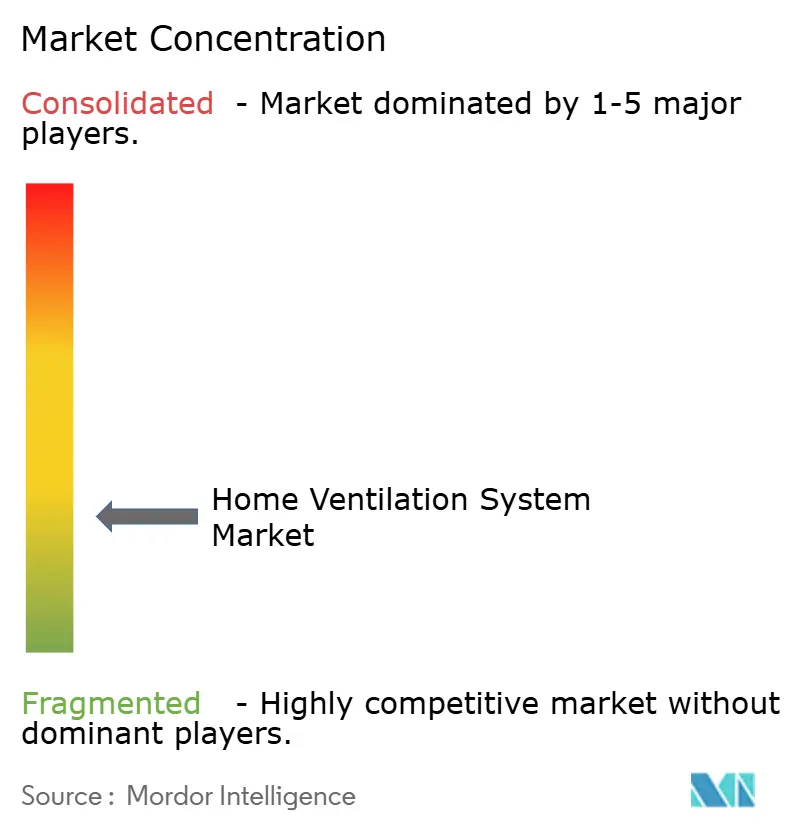

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Home Ventilation System Market Analysis by Mordor Intelligence

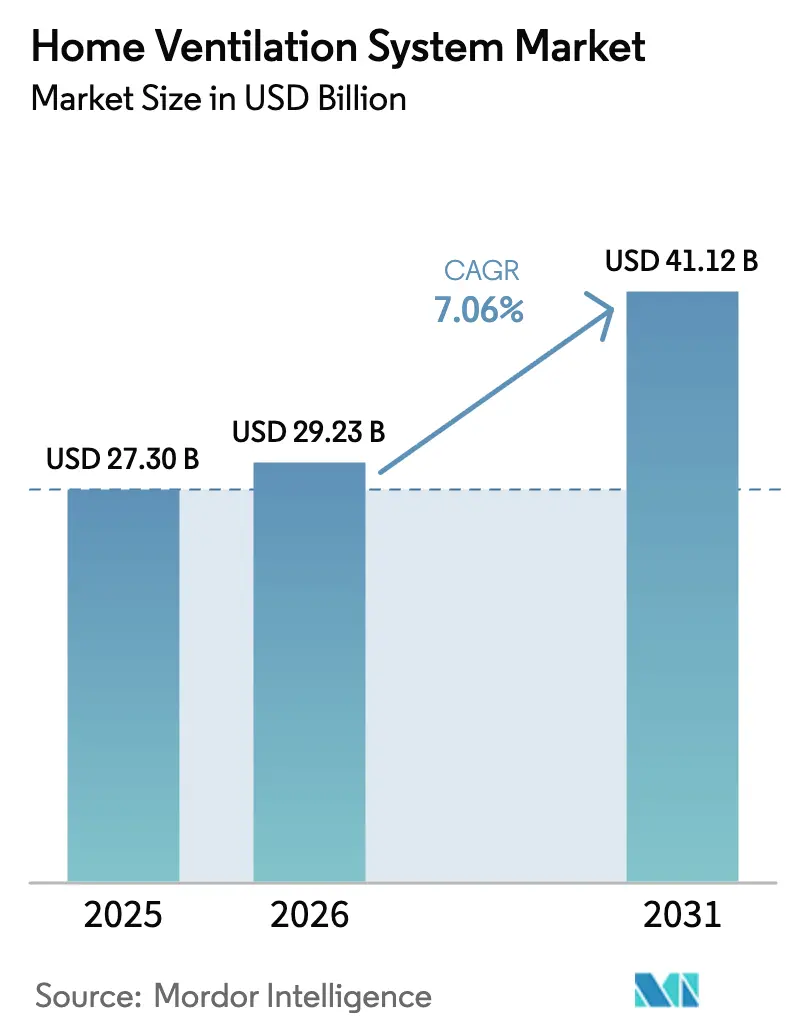

The home ventilation system market size is projected to expand from USD 27.30 billion in 2025 and USD 29.23 billion in 2026 to USD 41.12 billion by 2031, registering a CAGR of 7.06% between 2026 to 2031. Building codes are tightening airtightness thresholds, which makes mechanical ventilation a baseline requirement for compliance in both new homes and many renovations. The International Energy Conservation Code requires mechanical ventilation when dwellings meet prescriptive air-sealing requirements, and it tightens air leakage targets in colder climate zones, driving demand for balanced solutions with recovery capabilities. In Europe, the recast Energy Performance of Buildings Directive requires member states to transpose the directive by May 29, 2026, and sets a zero-emission requirement for new buildings by 2030, which implies tighter envelopes and mechanical ventilation strategies as standard practice[1]Source: European Commission, “Energy Performance of Buildings Directive,” European Commission, energy.ec.europa.eu. Jurisdictions like California have added specific balanced ventilation rules for multifamily applications when envelope leakage falls below set thresholds, reinforcing the adoption of HRV and ERV systems in both moderate and cold climates.

Key Report Takeaways

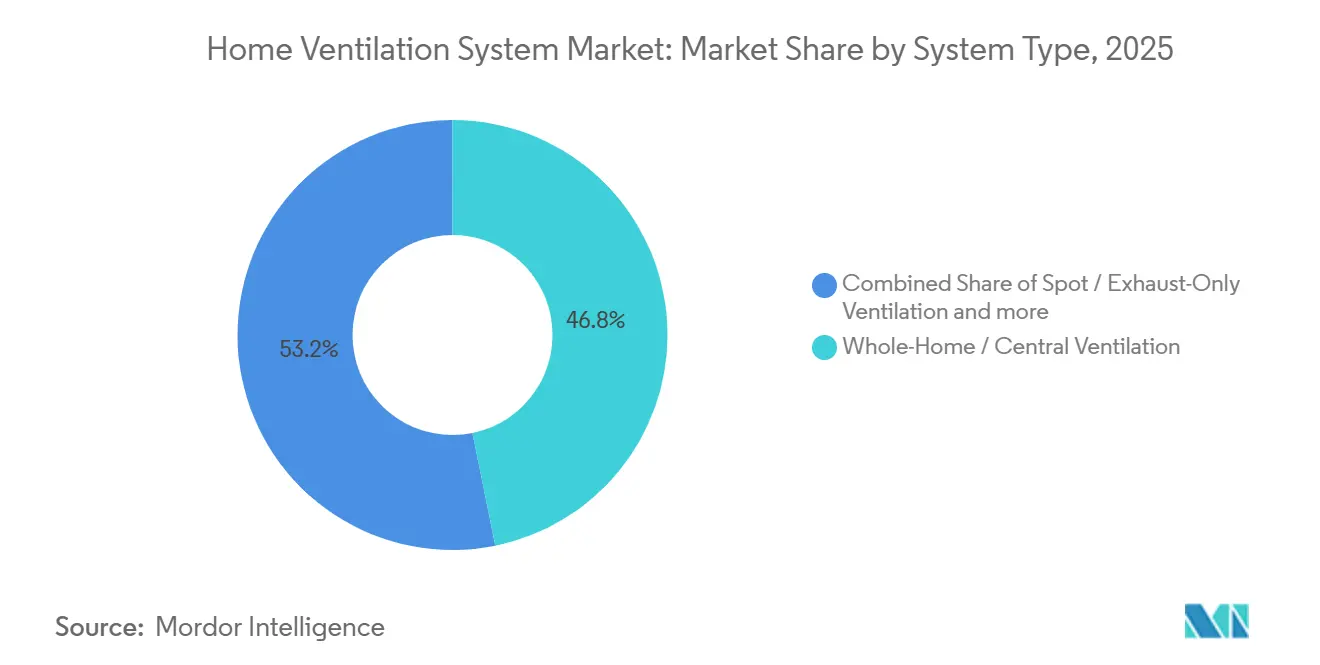

- By system type, whole-home or central ventilation led with 46.81% of the Home Ventilation System Market in 2025, while energy recovery ventilators are forecast to expand at a 7.72% CAGR through 2031.

- By product type, HVAC-integrated units held 41.62% of the Home Ventilation System Market in 2025, and standalone ventilators and fans are projected to lead growth at an 8.45% CAGR.

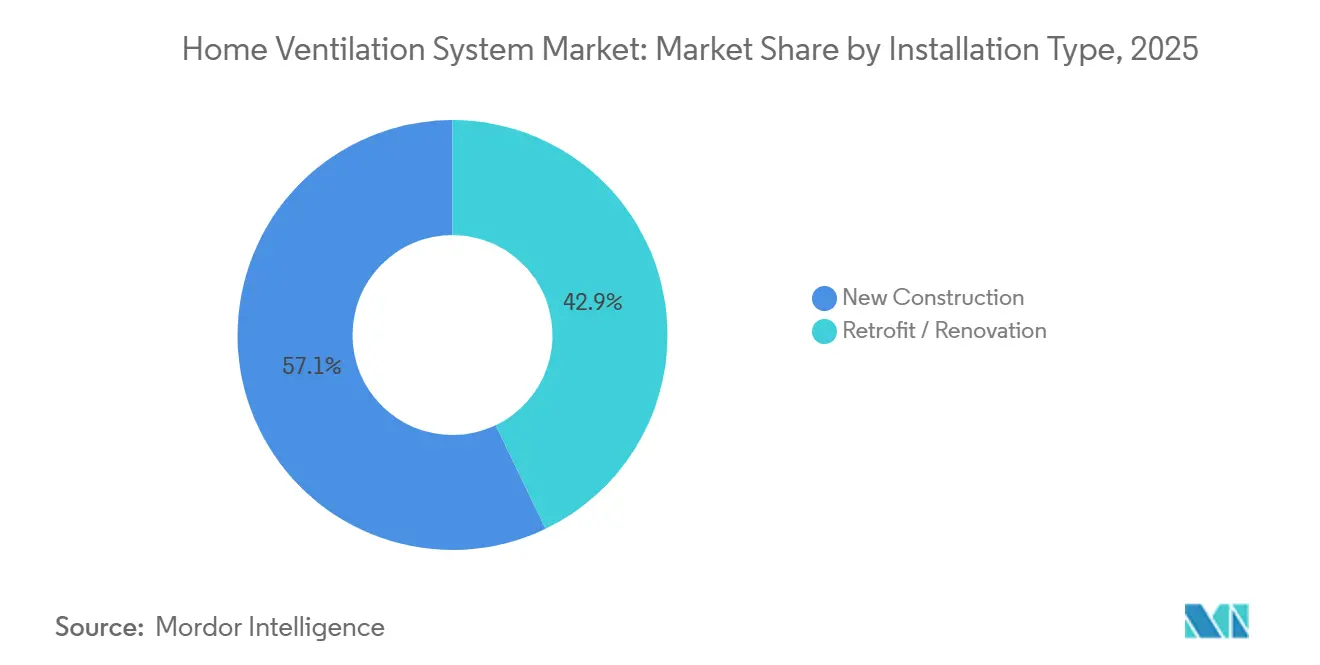

- By installation type, new construction captured 57.12% of the Home Ventilation System Market in 2025, while retrofit and renovation installations are forecast to grow at an 8.12% CAGR.

- By geography, Europe maintained the largest share at 31.73% of the Home Ventilation System Market in 2025, while Asia-Pacific is projected to grow the fastest at a 6.71% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Home Ventilation System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Indoor Air Quality Becoming a Core Residential Health Priority | +1.2% | Global, with early gains in North America, Western Europe, and urban Asia | Short term (≤ 2 years) |

| Smart Home Integration Accelerating Demand for Intelligent Ventilation | +0.8% | North America & EU core, spillover to APAC urban centers | Medium term (2-4 years) |

| Mandatory Ventilation Requirements in Energy-Efficient Building Codes | +1.8% | Global, particularly the EU (EPBD 2024), North America (IECC 2024), UK (Future Homes Standard) | Short to Medium term (2-4 years) |

| Renovation-Led Demand from Aging and Poorly Ventilated Housing Stock | +1.0% | North America, Western Europe, mature markets with a 40+ year median home age | Medium to Long term (2-4+ years) |

| Airtight Urban Housing Driving Mechanical Ventilation Adoption | +1.1% | APAC core (China, India urban clusters), EU, North America multifamily | Medium term (2-4 years) |

| Rising Penetration of Heat-Recovery & Energy-Efficient Systems | +1.2% | Cold climates (North America CZ 6-8, Nordic EU, Canada), expanding to moderate climates | Medium to Long term (2-4+ years) |

| Source: Mordor Intelligence | |||

Indoor Air Quality Becoming a Core Residential Health Priority

Indoor air quality has moved from an optional upgrade to a routine requirement in residential projects and mid-cycle retrofits, as awareness of airborne contaminants has persisted since 2024. Minimum ventilation rates are embedded across codes and standards with enforcement pathways that tie compliance to measurable continuous airflow, creating a compliance-driven floor for ventilation capacity in most new homes. In the European Union, the EPBD 2024 recast requires member states to establish national indoor air quality measures by May 29, 2026, and embeds monitoring in all new non-residential zero-emission buildings, which sets a tone for residential expectations as zero-emission buildings become the norm. Health-focused programs such as DOE Zero Energy Ready Home and associated labeling frameworks integrate ventilation as part of a broader performance package, which steers builders toward balanced systems with right-sized filtration in new construction now and through the 2030 horizon[2]Source: ENERGY STAR, “Stakeholder Comments, SFNH Version 3.3 and MFNC Version 1.3,” U.S. EPA ENERGY STAR, energystar.gov. As codes and voluntary labels converge, ERV adoption benefits from evidence that balanced ventilation can deliver steady airflow rates without relying on incidental infiltration, which makes the home ventilation system market a clear beneficiary of the shift toward health-centered residential design.

Smart Home Integration Accelerating Demand for Intelligent Ventilation

Residential HVAC platforms have integrated more software features since 2024, and ventilation is increasingly included in the control stack as part of energy optimization. Manufacturer disclosures underscore a focus on predictive maintenance, open connectivity, and AI-assisted control, and these features are being applied to ventilation scheduling and demand control alongside heating and cooling. Companies with building automation portfolios show a clear pivot to software-enabled differentiation, and this supports ventilation modules that respond to measured indoor conditions rather than static setpoints. Product ecosystems that consolidate thermostats, IAQ sensors, and ventilation boxes under a single app are gaining traction with installers and homeowners, which shortens commissioning and supports value propositions beyond air exchange alone. As intelligent features spread across mid-market price points, the home ventilation system market sees expanding use cases for demand-controlled ventilation, remote diagnostics, and performance verification that align with code compliance checks and utility program requirements. These capabilities reinforce ventilation’s role as a measurable, controllable element in a whole-home performance stack, improving the value capture for connected ERV and HRV systems across regions where smart device adoption is already mainstream.

Mandatory Ventilation Requirements in Energy-Efficient Building Codes

Code evolution has moved mechanical ventilation from a recommendation to a requirement as envelope tightness targets drop and as energy credits favor low-leakage assemblies. The 2024 IECC sets tighter air leakage thresholds, expands prescriptive and performance paths that reward tighter envelopes, and explicitly requires mechanical ventilation when the air-sealing requirements are met, which is a material catalyst for the home ventilation system market in colder zones. U.S. federal and state policy actions channel more projects under these modernized standards, while DOE analyses and implementation webinars provide clarity on the scope of change and the tradeoffs builders face when pursuing energy credits through high-performance envelopes. On the West Coast, Title 24 updates require balanced ventilation in multifamily homes when envelopes are tight, and code resources in California reinforce the need for dedicated outdoor air strategies, which increases ERV and HRV adoption in attached housing[3]Source: Energy Code Ace, “Section 160.2, Mandatory Requirements for Ventilation and IAQ,” Statewide Codes and Standards Program, energycodeace.com. In Europe, the EPBD 2024 recast sets a zero-emission mandate for new buildings by 2030 and accelerates the renovation trajectory, which practically points to balanced mechanical ventilation in both new builds and substantial retrofits as airtightness ratchets down. Certification pathways aligned with highly efficient envelopes, such as the Phius approach, create a strong linkage between airtightness limits and the use of mechanical ventilation with recovery, making compliance a direct demand channel for high-efficiency ventilation solutions [4]Source: Phius, “Phius Certification Guidebook v25.1.0,” Phius, phius.org.

Renovation-Led Demand from Aging and Poorly Ventilated Housing Stock

Aging housing stock across North America and Western Europe contains a large installed base that predates modern insulation and envelope practices. As codes converge around verified airtightness and as blower door testing becomes common in code enforcement, many leaky homes still face indoor air quality risks, moisture control issues, and comfort problems that ventilation can address when broader envelope upgrades are pursued. Evidence from building science communities and airtightness studies shows that legacy homes vary widely in leakage, and that upgrades that lower infiltration must be paired with mechanical ventilation to avoid under-ventilation and moisture accumulation. Utility and incentive programs in several states direct funds toward ventilation when linked to broader energy retrofits, which shortens payback timelines in colder climates where recovered heat substantially reduces the ventilation energy penalty. As regional retrofit markets stabilize and financing costs ease, balanced ventilation paired with filtration is poised to capture a larger share of residential upgrade budgets, with contractors bundling ERVs and HRVs alongside air sealing, heat pumps, and duct system improvements in whole-home packages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High System & Installation Costs Limiting Mass-Market Adoption | -1.5% | Global, particularly price-sensitive markets (APAC emerging, Latin America, Eastern Europe) | Short to Medium term (≤ 4 years) |

| Structural Constraints in Retrofitting Older Residential Buildings | -0.9% | North America, Western Europe (pre-1980 housing stock), and mature markets with legacy construction | Medium to Long term (2-4+ years) |

| Fragmented Regulations Across Countries and Building Standards | -0.8% | Global, especially regions with decentralized building codes (EU member states, North America, parts of APAC) | Medium term (2–4 years) |

| Perceived Maintenance Complexity and Long-Term Cost Concerns | -0.6% | Global; stronger impact in residential and small commercial segments | Short to Medium term (≤ 3 years) |

| Source: Mordor Intelligence | |||

High System & Installation Costs Limiting Mass-Market Adoption

Whole-house systems that deliver balanced airflow with heat or energy recovery involve both equipment and labor, which can be significant in homes without pre-planned duct runs. Installation complexity increases when existing HVAC systems cannot share ductwork or when additional penetrations and wiring are needed for a stand-alone ventilator, which adds to project budgets and lengthens payback periods in retrofit scenarios. Price trends have been influenced by component transitions such as low-GWP refrigerants, supply chain conditions, and upgraded control packages that reflect the market’s shift toward connected devices, all of which contribute to higher average selling prices reported by several manufacturers. While incentives reduce net costs in many programs, homeowners in price-sensitive regions still weigh upfront outlays against alternative upgrades, which can delay adoption of centrally ducted solutions in favor of incremental measures. In new construction, costs are more easily amortized into mortgages, and this helps sustain share for integrated systems in the home ventilation system market, where builders specify balanced ventilation as part of a comprehensive HVAC package.

Structural Constraints in Retrofitting Older Residential Buildings

Legacy homes with limited ceiling cavities, smaller chases, and preserved finishes present challenges to routing supply and exhaust ductwork for every habitable room. Multi-level houses often require vertical duct runs, additional penetrations, and structural coordination that add to labor time and affect interior finishes, all of which make comprehensive retrofits harder to sell. Historic properties and buildings with masonry or solid walls may face local preservation limits on exterior penetrations for intake and exhaust, which narrows options to decentralized or ductless units that come with different cost and performance tradeoffs. For older multifamily buildings, compartmentalization and leakage conditions vary widely, and achieving tightness targets can require significant air sealing that changes the ventilation strategy needed to maintain indoor air quality. These realities explain why integrated systems are prevalent in new builds and why decentralized or stand-alone units gain share in retrofits, creating a mixed product landscape within the home ventilation system market as housing stock conditions drive different specification paths.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: ERVs Propel Market Shift Toward Total Energy Recovery

Whole-home or central ventilation systems accounted for 46.81% in 2025, reflecting builder preferences for centralized ducted solutions that distribute fresh air across multiple zones as a standard practice in tighter envelopes. The category benefits from established installation workflows and compatibility with forced-air infrastructure in new construction, where ductwork and controls are coordinated at rough-in stages. Energy recovery ventilators are the fastest-growing segment at a 7.72% CAGR through 2031, as owners and builders value both sensible and latent energy transfer, which stabilizes indoor conditions across seasons; this differential supports adoption in mixed and cooling-dominant regions. Alongside efficiency gains, balanced systems align with codes that require mechanical ventilation for homes meeting prescriptive air-sealing, reinforcing ERV and HRV penetration in climates where the energy and comfort payoffs are most visible. These choices create a noticeable shift in the home ventilation system market where total energy recovery solutions are favored when envelopes are tight, multifamily projects require compartmentalization, and comfort goals include humidity control in summer conditions.

In the broader comparison of system types, spot or exhaust-only ventilation retains a base in moisture-prone rooms due to lower upfront costs and ease of installation. HRVs continue to serve cold climates with sensible heat recovery that reduces ventilation heat loss, adding measurable value where winter heating loads dominate. Embedded trends favor balanced systems across new construction because performance-based compliance and airtightness credits push projects toward lower leakage targets, which are harder to maintain with exhaust-only approaches; this context amplifies ERV growth in the home ventilation system industry. These patterns are reinforced by OEM product roadmaps and supported by code resources, labeling programs, and builder training that make balanced ventilation the default selection when targeting higher energy performance and healthy home credentials. As a result, ERVs and HRVs are positioned to capture a larger portion of system specifications over the forecast period, with ERVs addressed to regions where indoor humidity control and cooling are central considerations in the home ventilation system market.

By Product Type: HVAC Integration Dominates but Standalone Units Lead Growth

HVAC-integrated units held 41.62% in 2025, aided by builder adoption of single-vendor packages that coordinate heating, cooling, and ventilation controls, which reduces commissioning time and simplifies warranty management. This approach spreads ducting and labor across the whole HVAC scope in new homes and is broadly compatible with code pathways where verified tightness and continuous ventilation are intertwined performance targets under energy credits. Standalone ventilators and fans are projected to grow the fastest at an 8.45% CAGR through 2031, supported by retrofit use cases where existing HVAC systems or architecture do not accommodate additional ductwork or where owners want independent ventilation control. Inline fans and decentralized units broaden options for multi-room or room-by-room solutions, which expand addressable retrofit volume for contractors who can deliver airflow improvements without major tear-outs. This mix underscores how product choice maps to construction phases and constraints, which preserves integrated dominance in new builds while decentralization and stand-alone boxes lead growth in existing stock within the home ventilation system market.

The category’s evolution shows more ENERGY STAR-aligned features and connected controls migrating into stand-alone units, closing the perception gap with integrated systems on both performance and user experience. In jurisdictions with prescriptive outdoor air targets, retrofit-friendly accessories, including motorized dampers and control kits, help existing systems meet airflow requirements, which supports stand-alone growth inside the broader home ventilation system industry. As more programs verify delivered airflow and filtration, and as builders target higher performance labels, integrated products remain the default in new construction while stand-alone options add flexibility for constrained retrofits. This dual track strengthens the category’s overall outlook and ensures that both paths see continued investment in efficiency, acoustic performance, and connectivity as code enforcement and consumer expectations rise. These combined trends reinforce share stability for integrated products and share expansion for stand-alone solutions through 2031 in the home ventilation system market.

By Installation Type: Retrofit Gains Momentum on Aging Stock

New construction captured 57.12% in 2025, reflecting how builders preempt compliance risk by specifying balanced ventilation early in the design and installation process. Code verification methods, including blower door testing and commissioning checks, align with balanced systems that deliver predictable airflow at high levels of airtightness, which makes ventilation essential before occupancy in many jurisdictions. Retrofit and renovation installations are projected to expand at an 8.12% CAGR through 2031, leveraging decentralized solutions when ducted approaches are impractical and incentive support where programs tie ventilation upgrades to broader energy retrofits. As more existing homes undergo air sealing or HVAC replacement, owners and contractors increasingly pair these steps with balanced ventilation to stabilize indoor conditions and reduce moisture risks. The resulting upgrade path spreads adoption across attached and detached homes, supported by product portfolios tuned to constrained spaces, older assemblies, and room-by-room requirements in the home ventilation system market.

New residential supply cycles and interest rate movements affect near-term installation mix, but the structural drivers for ventilation in airtight homes remain. Incentive design in several states and provinces supports ventilation when integrated into whole-home improvements, which helps reduce payback timelines in colder zones. Over time, this supports a rising share for retrofits as aging stock is modernized, while new construction remains the larger base for code-driven installations in the home ventilation system market. Builders continue to standardize balanced ventilation on higher-performance tiers, and this consistency reduces variance in delivered airflow and quality outcomes at occupancy. The two channels reinforce each other as product advances for retrofits spill back into new-build offerings, and as integrated systems improve commissioning workflows, sustaining installations across both paths.

Geography Analysis

Europe’s leadership at 31.73% in 2025 rests on regulations that make mechanical ventilation a practical necessity for new builds and major renovations. The recast Energy Performance of Buildings Directive pushes zero-emission building standards and requires member states to implement indoor air quality measures, reinforcing the need for ventilation in increasingly airtight buildings. National renovation strategies focus on upgrading inefficient building stock, naturally linking ventilation upgrades with insulation and heating improvements. Germany and France serve as major demand hubs, while Northern European countries lead innovation in heat recovery and balanced ventilation suited to colder climates. In the United Kingdom, updated building regulations and overheating mitigation measures strongly position mechanical ventilation with heat recovery as a preferred compliance solution in new homes.

Asia-Pacific is smaller in its current share but grows the fastest at a 6.71% CAGR through 2031, shaped by urban density and greater reliance on mechanical conditioning in new construction. New construction in the region relies heavily on mechanical systems to manage indoor air quality and thermal comfort. Manufacturers are expanding local production and tailoring integrated ventilation and conditioning solutions to meet the needs of high-density housing. As building envelopes tighten and airflow verification becomes more common, balanced ventilation systems gain wider acceptance, often supported by connected controls and air quality monitoring. Energy efficiency programs and evolving national codes in select countries are steadily shifting ventilation from an optional feature to a standard requirement in residential projects.

North America represents a substantial portion of global demand and shows steady growth supported by evolving building codes and energy programs. Updated energy codes encourage mechanical ventilation as homes become more airtight, effectively embedding ventilation into new residential construction. Regional regulations, particularly in multifamily housing, promote the use of balanced systems such as heat and energy recovery ventilators. Wider adoption of updated codes and alignment with federal efficiency initiatives are expanding the installed base across diverse climate zones. Over time, consistent enforcement, builder education, and localized incentive programs are strengthening demand, especially in colder regions and attached housing, where mechanical ventilation is critical for performance and compliance.

Regulatory Landscape

Residential ventilation demand is anchored to building energy codes and IAQ standards that tighten airtightness and then mandate verified mechanical ventilation. In North America, the 2024 International Residential Code (IRC) sets whole-house mechanical ventilation requirements when tested air leakage is below 5 ACH50, while the 2025 California Building Energy Efficiency Standards (Title 24) require whole-house ventilation aligned with ASHRAE 62.2 and include performance provisions such as fan efficacy and sound limits. These requirements favor higher-efficiency fans and better-controlled balanced systems.

In Europe, ventilation-unit performance continues to be governed by EU Ecodesign rules such as Regulation (EU) 1253/2014 for ventilation units. Industry bodies including Eurovent engaged the European Commission in May 2025 with comments on draft revisions to the Ecodesign and labelling framework for residential ventilation units. Separately, the recast Energy Performance of Buildings Directive adds a near-term compliance milestone, with member states required to transpose the directive by May 29, 2026, reinforcing tighter envelopes and mechanical ventilation strategies within zero-emission building pathways.

Value Chain Analysis

The value chain runs from raw materials (steel and aluminum for cabinets and exchangers, plastics, copper, motors, sensors and semiconductors for controls, and filter media) into component manufacturing (impellers, casings, heat-exchanger cores), followed by final assembly of HRV/ERV units and fans. After that, certification and test regimes feed into distribution channels that reach builders, retailers, and HVAC wholesalers. Downstream value capture is concentrated with mechanical contractors and installers, who size, commission, and verify airflow, particularly where code compliance ties to delivered ventilation performance.

Standards and labeling influence specifications and purchasing decisions across the chain. ANSI/ASHRAE Standard 62.2-2025 is a central benchmark for residential mechanical ventilation, and it includes updates such as MERV 11 filtration requirements. Program pathways such as US EPA Indoor airPLUS Version 1 (Rev. 5), issued in December 2025, require whole-dwelling mechanical ventilation to meet ASHRAE 62.2-2010 or later. OEM product strategies increasingly embed controls, sensors, and timing functions to simplify compliance and reduce commissioning friction, including ERV product positioning around ASHRAE 62.2 and ENERGY STAR-aligned features.

Competitive Landscape

The home ventilation system market remains moderately fragmented, with leading manufacturers collectively holding a significant but not dominant share, alongside a wide base of regional specialists and diversified HVAC suppliers. Competition spans multiple product categories and sales channels, reflecting varied residential and light commercial needs. Strategic focus across the industry centers on software-enabled controls, integrated product portfolios, and selective acquisitions. These moves are aimed at expanding geographic presence and adding complementary capabilities. Overall, competitive positioning increasingly depends on technology differentiation rather than scale alone.

A key strategic shift occurred when Johnson Controls divested its residential and light commercial HVAC operations to Bosch, allowing it to sharpen its focus on commercial solutions and building automation. This transaction reshaped competitive dynamics while preserving Johnson Controls’ broader ventilation and control competencies. Major original equipment manufacturers continue to prioritize connected devices and advanced analytics within their HVAC and ventilation offerings. Corporate disclosures highlight investments in predictive maintenance, open connectivity, and energy optimization. These capabilities strengthen value propositions for balanced ventilation systems through improved commissioning support and verifiable performance under regulatory oversight.

International manufacturers are also expanding production capacity and forming regional partnerships to meet rising demand and local regulatory requirements. Systemair has reported investments in new and expanded facilities across Europe, along with deeper engagement in India and Southeast Asia through acquisitions and localized manufacturing. These efforts align supply chains with stricter building codes and growing residential ventilation adoption. Across the industry, product development emphasizes higher heat recovery efficiency, reduced noise levels, and seamless integration with home automation platforms. At the same time, refrigerant transitions toward low global warming potential alternatives are influencing product design, cost structures, and pricing for integrated HVAC and ventilation solutions.

Home Ventilation System Industry Leaders

Zehnder Group

Lennox International

Panasonic Corporation

Broan-NuTone LLC

Mitsubishi Electric

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Code-driven airtightness requirements create a clear opportunity for packaged, compliance-ready ventilation solutions that reduce installer time and verification risk. In the United States, whole-house ventilation triggers tied to low air leakage under the 2024 IRC, combined with performance-oriented requirements embedded in California Title 24 (2025 standards), support demand for higher-efficacy fans, quieter operation, and better-controlled outdoor air delivery. This expands the space for contractor-friendly kits that bundle controls, dampers, and verification support across new construction and renovation.

Tight-space and retrofit constraints also support growth for compact, decentralized, and auto-balancing balanced-ventilation formats, especially in multifamily projects and older housing where duct routing is difficult. Product evidence points in this direction, including Panasonic Eco Systems North America introducing the BalancedHome 210 ERV in June 2026 to target modern single-family applications with a compact form factor and higher recovery performance, and Zehnder launching the ultra-slim, Passivhaus-certified Zehnder EVO MVHR in July 2026 for confined installations. On the policy side, the UK published Approved Document F 2026 with updated ventilation performance guidance that takes effect in 2027, creating a defined compliance window for suppliers and installers to standardize MVHR specification and commissioning practices.

Recent Industry Developments

- June 2026: Panasonic Eco Systems North America launched the BalancedHome 210 energy recovery ventilator aimed at single-family new construction and light commercial applications. The release emphasizes compact installation and higher-performance energy recovery, supporting code-aligned ventilation strategies in tighter envelopes.

- September 2025: Panasonic launched its Intelli-Balance Elite and Elite Plus+ series of energy recovery ventilators positioned for year-round comfort across more extreme climate conditions and alignment with modern building standards. The rollout broadened Panasonic’s ERV lineup in a segment where compliance and recovery performance increasingly drive specifications.

- August 2024: Lennox International and Samsung announced the establishment of Samsung Lennox HVAC North America, a joint venture focused on ductless and variable refrigerant flow offerings. Expanding ductless and connected HVAC platforms strengthens bundled IAQ and ventilation propositions for contractors and distributors selling whole-home systems.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the home ventilation system market covers equipment used to exchange indoor and outdoor air in residential buildings, including mechanical supply, exhaust, balanced ventilation, and energy recovery based systems, along with typical related control and airflow components sold with the system.

Scope exclusions: We exclude non-residential ventilation, large industrial air handling setups, and building services that are not part of a defined home ventilation system sale.

Segmentation Overview

- By System Type

- Whole-Home / Central Ventilation

- Spot / Exhaust-Only Ventilation

- Energy Recovery Ventilators (ERV)

- Heat Recovery Ventilators (HRV)

- By Product Type

- HVAC-Integrated Units

- Standalone Ventilators & Fans

- Inline Duct Fans & Accessories

- By Installation Type

- New Construction

- Retrofit / Renovation

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East And Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries and build a reference base of indicators before modeling. We relied on public and official sources such as US Census Bureau construction and housing indicators, Eurostat housing and renovation statistics, International Energy Agency updates on building energy efficiency, and standards and guidance notes published by ASHRAE and national building code agencies.

To keep the demand narrative grounded, we also reviewed company annual reports, investor presentations, and reputable press coverage on residential HVAC and indoor air quality upgrades. Patent databases were checked to understand technology direction in energy recovery ventilation and controls, and we used paid subscriptions for company financials and news to confirm timelines and revenue mix statements when disclosures were limited. These examples are illustrative, and other public and paid sources were also consulted for data collection, cross-checks, and clarification during interviews.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with manufacturers, distributors, HVAC installers, building services consultants, and selected residential developers, since each group sees a different part of the buying cycle. We used these discussions to validate pricing bands, typical system mixes by climate, and how energy codes and retrofit programs are translating into actual orders across major regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 16% | APAC: 43% |

| Mid tier: 46% | Functional/Unit leaders: 35% | EMEA: 31% |

| Smaller Players: 16% | Managers: 49% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where residential construction activity and renovation intensity are translated into an addressable home stock, which is then filtered by mechanical ventilation penetration and replacement cycles. Once the demand pool is defined, value is derived using region-level average selling prices that reflect common system configurations, installation context (new build versus retrofit), and the split between standard exhaust systems and higher-priced HRV or ERV options.

To keep results realistic, we corroborated totals using selective bottom-up checks, such as supplier revenue direction, channel feedback on unit movement, and sampled ASP multiplied by estimated volumes in a few representative markets. When gaps appear in smaller countries or in retrofit-heavy areas, we use proxy assumptions based on nearby markets with similar climate, code stringency, and housing types, then test those proxies in follow-up calls.

For forecasting, scenario analysis was used because residential ventilation demand is sensitive to housing starts, retrofit incentives, and energy code enforcement that can shift quickly. The forward view was anchored on inputs such as housing completions, renovation spending trends, indoor air quality awareness signals, energy efficiency code updates, and expected price progression for energy recovery systems and smart controls, and then reviewed with industry participants before finalizing the curve.

Data Validation & Update Cycle

Model outputs were checked against independent signals such as residential HVAC shipment direction, building permit momentum, and the observed mix shift toward energy recovery units in colder climates. If a region showed an unusual jump in value without a matching change in construction activity or the pricing logic, the assumptions were re-tested, and respondents were re-contacted to confirm whether the change was real or timing related.

Before sign-off, the work is reviewed in steps, starting with internal consistency checks, followed by peer review on inputs, and then final analyst validation of the output tables and narrative. Reports are refreshed annually, and interim updates are made when material events occur, such as major code changes, sharp currency moves, or a clear pricing reset. Right before delivery, a final review pass is completed so clients receive the most current view available.

Mordor Intelligence's Home Ventilation System Market Size Compared With Other Published Estimates

Published market sizes for home ventilation systems can look far apart, even when the topic sounds identical, because the underlying calculations often use different time cutoffs and pricing treatments. Differences also show up when sources do not align to the same residential boundary, or when they combine equipment value with broader HVAC spending.

In practice, the spread usually comes from how unit prices are updated through the year, which exchange rate window is used for regional conversion, and whether the model checks results against housing activity and replacement cycles before finalizing totals. A refresh-led approach that re-tests ASP bands and currency timing close to publication, then verifies the outcome with installer and channel feedback, is the main reason the 2025 value lands at USD 27.30 B in Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 27.30 B (2025) | |

| Trade Journal A | USD 27.75 B (2025) | Often aligned to broader ventilation systems coverage that can include non-home end users, and pricing can be based on a single-year average without explicit checks against residential replacement cycles. |

| Regional Consultancy B | USD 7.64 B (2024) | May treat the market as a narrower set of residential ventilation products, with limited inclusion of whole-home energy recovery systems and uneven currency conversion timing across regions. |

The table shows that year selection and scope boundaries explain most of the gap, and then the rest comes from how pricing and currency are handled in the model. When the market is rebuilt from housing-linked demand signals and then stress-tested with channel validation, the result stays more traceable to clear inputs and can be repeated with the same steps in the next refresh cycle.

Key Questions Answered in the Report

What is the current size and growth outlook for the home ventilation system market?

The home ventilation system market size is USD 29.23 billion in 2026 and is projected to reach USD 41.12 billion by 2031 at a 7.06% CAGR.

Which regions lead and which are growing fastest?

Europe holds the largest share at 31.73% in 2025, while Asia-Pacific is forecast to grow the fastest at a 6.71% CAGR through 2031.

Which system type is growing fastest and why?

Energy recovery ventilators are projected to grow at a 7.72% CAGR through 2031 due to benefits in both heating and cooling seasons and alignment with tight-envelope code requirements.

How do codes influence the adoption of residential ventilation?

The 2024 IECC requires mechanical ventilation in sealed homes, EPBD 2024 mandates zero-emission buildings by 2030, and Title 24 sets balanced ventilation triggers in multifamily dwellings, all of which drive ERV and HRV adoption.

What installation channel will expand the most through 2031?

Retrofit and renovation installations are projected to grow at an 8.12% CAGR as aging stock is upgraded and balanced ventilation is paired with energy retrofits.

Which product approach gains the most in retrofits?

Standalone ventilators and fans lead growth at an 8.45% CAGR, serving homes where integrated ducted solutions are impractical or where owners want independent ventilation control.

Page last updated on: