Home Sleep Screening Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.49 Billion |

| Market Size (2031) | USD 6.11 Billion |

| Growth Rate (2026 - 2031) | 6.36% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Home Sleep Screening Devices Market Analysis by Mordor Intelligence

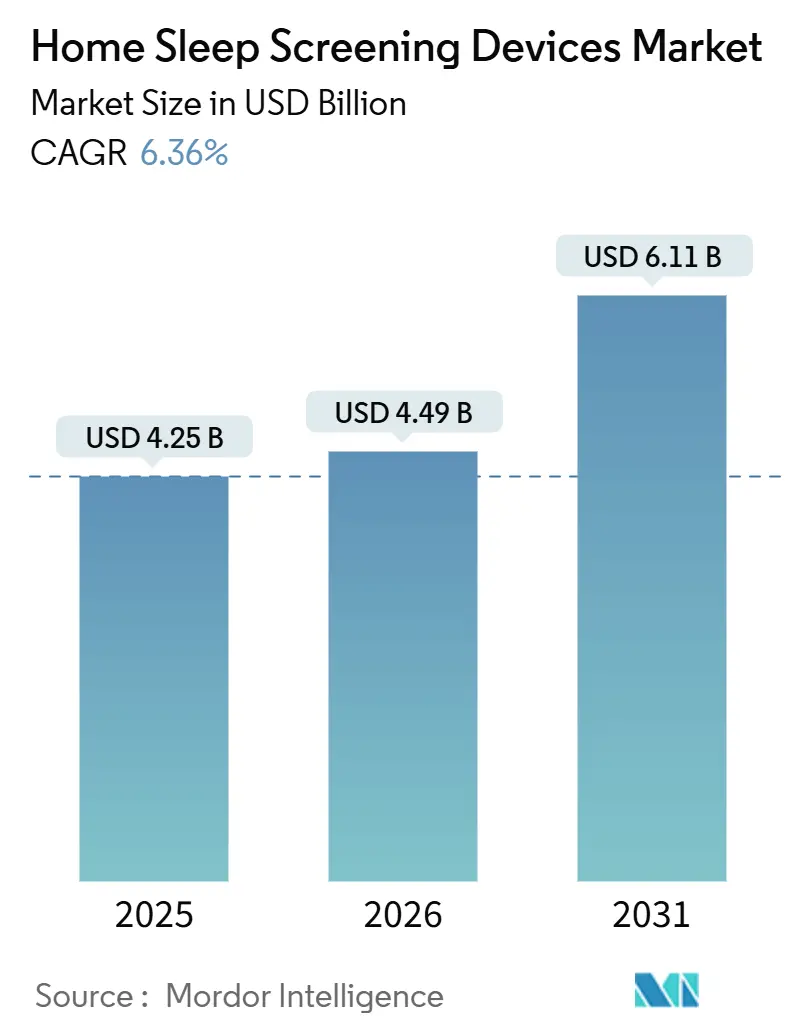

The Home Sleep Screening Devices Market size is expected to grow from USD 4.25 billion in 2025 to USD 4.49 billion in 2026 and is forecast to reach USD 6.11 billion by 2031 at 6.36% CAGR over 2026-2031.

Uptake is being propelled by payer-aligned reimbursement, telemedicine infrastructure, and AI-assisted scoring that let primary-care teams order tests once confined to sleep laboratories [1]Centers for Medicare & Medicaid Services, “2025 Physician Fee Schedule Final Rule,” CMS.gov. At the same time, the market’s growth ceiling reflects clinical limits, as home devices are approved only for uncomplicated adults, and every study still requires manual review, which slows throughput. A regulatory split has also emerged: the March 2023 CMS ban on derived or virtual channels has forced manufacturers to choose between reusable PAT platforms that comply with the rule and single-use disposables that optimize patient convenience. Competitive intensity is rising as respiratory-care incumbents defend share against patch-based startups and AI-native scoring platforms that decouple hardware from interpretation software.

Key Report Takeaways

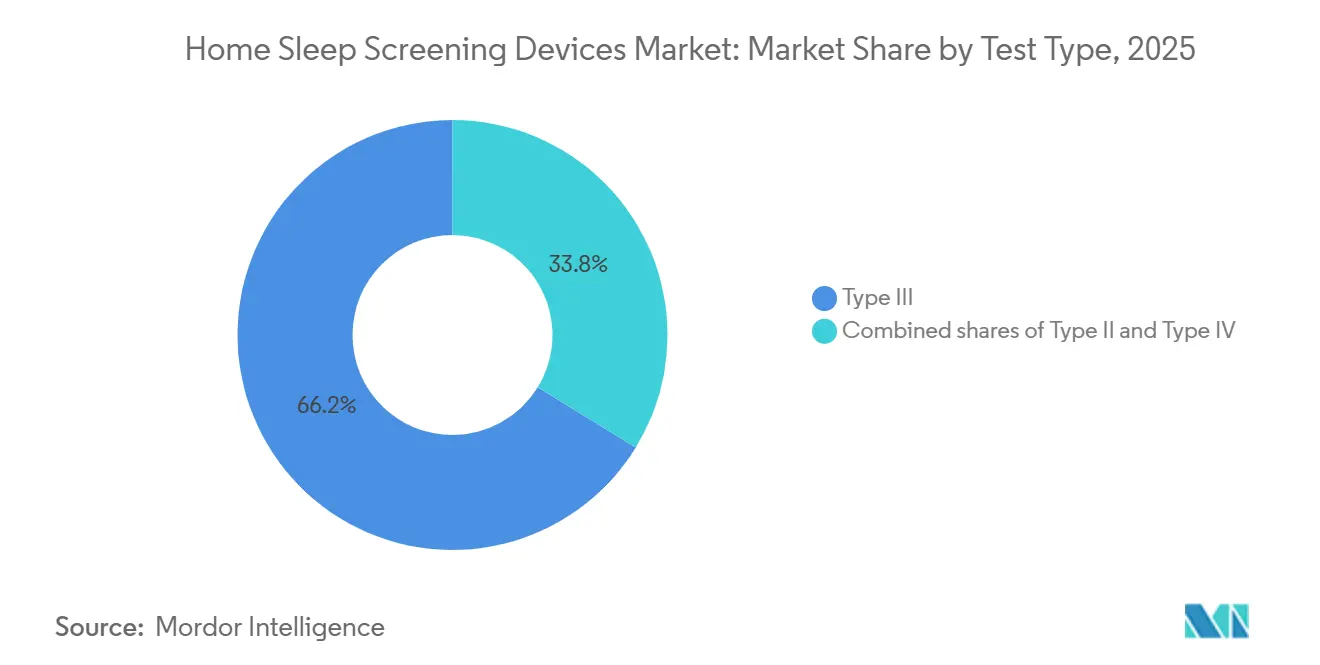

- By test type, Type III devices held 66.23% of the Home Sleep Screening Devices market share in 2025 and Type IV is projected to expand at a 9.21% CAGR through 2031.

- By distribution channel, offline outlets led with 70.12% revenue share in 2025, while online channels are forecast to grow at an 8.56% CAGR to 2031.

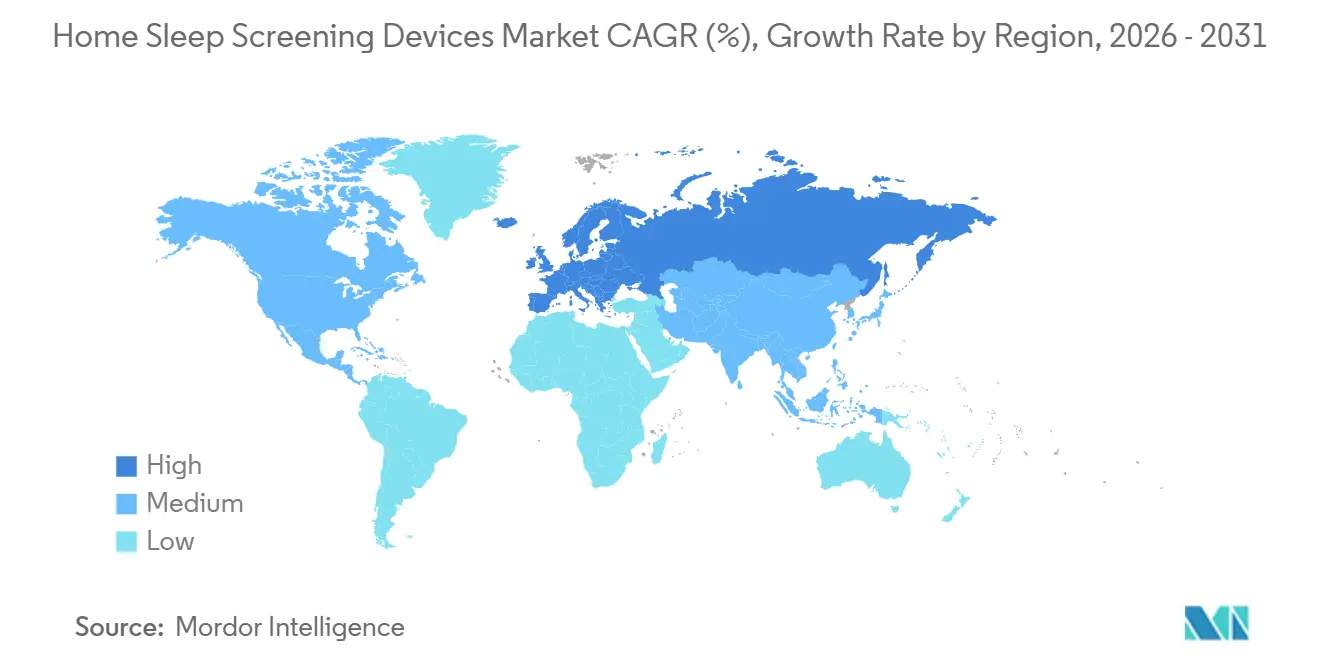

- By geography, North America contributed 49.34% of 2025 revenue, yet Europe is set to record an 8.09% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Home Sleep Screening Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Payer-Aligned HSAT Coverage and Coding in Key Markets | +1.8% | North America, Western Europe | Medium term (2-4 years) |

| Shift To Home Diagnostics for Cost and Convenience | +1.5% | Global with early gains in US, UK | Short term (≤2 years) |

| Advancements In Wearable/Patch Sensors And PAT/PPG Platforms | +1.2% | Global with spill-over to APAC | Medium term (2-4 years) |

| Telemedicine Workflow And AI-Assisted Scoring Integration | +0.9% | North America, EU, APAC core | Long term (≥4 years) |

| AI-Derived Total Sleep Time Enabling Higher Reimbursements Were Permitted | +0.5% | US (select payers), Germany (DiGA) | Long term (≥4 years) |

| New De Novo and Pediatric-Clearances Expand Eligible Populations | +0.5% | US, EU with gradual APAC adoption | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Payer-Aligned HSAT Coverage and Coding in Key Markets

Medicare’s LCD L33405 and CPT 95800/95801/95806 have standardized payment for unattended studies, but the 2025 Physician Fee Schedule trimmed certain codes and barred devices that rely only on derived channels. The rule favors four-channel Type III systems that collect nasal flow and respiratory effort data, tilting purchasing toward established DME suppliers. Private insurers, led by UnitedHealthcare, mirror Medicare’s stance and require manual technologist scoring, further entrenching incumbent workflows[2]UnitedHealthcare, “Home Sleep Testing for Obstructive Sleep Apnea,” UHC.com. Startups therefore steer disposable wearables to cash-pay and employer programs where coverage rules are looser. These dynamics will keep the Home Sleep Screening Devices market anchored to rule-compliant hardware, even as consumer interest in low-sensor wearables continues to rise.

Shift to Home Diagnostics for Cost and Convenience

HSAT costs range from USD 150 to USD 600 per study, compared with USD 1,000–10,000 for in-lab polysomnography, creating an immediate economic appeal for providers[3]Department of Veterans Affairs, “Cost Analysis of Home Sleep Apnea Testing,” VA.gov. A 2024 VA analysis showed that HSAT generated USD 1,211 in revenue per operational day, compared with USD 902 for PSG, accelerating hospital adoption of home pathways. Disposable solutions such as ResMed’s NightOwl, cleared for ten-night use, strengthen the cost-benefit equation with richer longitudinal data. Direct-to-consumer platforms, including GEM SLEEP, ship mail-order kits for as little as USD 189 and target the 20 million undiagnosed Americans with moderate-to-severe OSA.

However, at-home data loss lifts per-test cost by 15-20%, and 13.5% of studies remain inconclusive, prompting costly follow-up PSG. Even so, the convenience premium is shifting purchase decisions toward home models, supporting steady gains for the Home Sleep Screening Devices market.

Advancements in Wearable and Patch Sensors

Patch-based systems such as Onera Health’s Sleep Test System achieved 0.98 concordance with PSG for AHI in a 206-patient multicenter trial, while the majority of users rated the form factor as completely satisfactory. Huxley Medical’s SANSA chest patch, cleared in December 2025, reported 100% sensitivity and 99% specificity for central sleep apnea across 340 subjects. ZOLL Itamar’s WatchPAT platform shows a 98% study success rate and now carries pediatric labeling for ages 12 and above. Despite these strides, a Swiss cohort reported 30% night-to-night variability in PAT-derived AHI, prompting manufacturers to adopt multi-night protocols. These sensor advances, paired with cloud telemetry that meets ISO 27001 standards, are broadening patient groups and driving the Home Sleep Screening Devices market toward form factors that promise higher comfort and richer datasets.

Telemedicine Workflow and AI-Assisted Scoring Integration

EnsoData’s AI engine trims manual technologist time by as much as 70% and supported 90.9% sensitivity in a 2026 validation of 225 at-risk adults. China’s Hang Hao Meng agent, deployed on Alipay, screened more than 3 million users and flagged 90,100 cases of sleep disorders, with 78.7% diagnostic concordance. Stanford’s SleepFM model, trained on 600,000 hours of PSG, foreshadows AI tools that predict multi-dimensional sleep phenotypes, yet CMS still mandates a qualified technologist to overread for payment. This regulatory throttle limits throughput gains but sets the stage for gradual task shifting once evidence and policy converge. The convergence of telehealth consultations, AI triage, and home testing underpins long-term expansion of the Home Sleep Screening Devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clinical Limitations and Manual Overread; Restricted to Uncomplicated Adults | −1.1% | Global | Short term (≤2 years) |

| Uneven Reimbursement and Procurement Hurdles in Developing Markets | −0.8% | APAC ex-Japan, MEA, South America | Medium term (2-4 years) |

| CMS Prohibition on Derived/Virtual Channels Limits Some Novel Devices | −0.6% | United States | Long term (≥4 years) |

| At-Home Data Loss/Retests and Logistics Increase Per-Test Cost | −0.4% | Global with higher rural impact | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Clinical Limits and Manual Overread

AASM guidelines restrict HSAT to adults with high pretest probability and no major comorbidities. A 2026 Spanish multicenter study of 329 patients found autoscoring matched PSG for severe OSA in 96.2% of cases, but agreement fell to 41.6% across all severities, underscoring the need for specialist review. Manual overread adds 15–30 minutes per study and dulls the labor-saving edge of automation. Lower therapy adherence in primary-care pathways 13% below sleep-specialist cohorts—exposes long-term outcome risks. These barriers temper the growth velocity of the Home Sleep Screening Devices market.

Uneven Reimbursement and Procurement Hurdles in Developing Markets

China counts 176 million adults with AHI for more than 5 years, yet HSAT coverage differs by province, and rural patients face out-of-pocket hurdles despite higher prevalence. India lacks standardized codes under Ayushman Bharat, so most consumers pay out of pocket or skip testing, while Brazil’s public system funds PSG but not HSAT, splitting the market along income lines. Import tariffs, volatile currencies, and 12–24-month approval times further raise entry costs. These obstacles limit regional contribution to the Home Sleep Screening Devices market over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Type IV Devices Capture Multi-Night and Wellness Segments

Type III systems controlled 66.23% of the market in 2025 because Medicare and most private insurers view them as adequate for straightforward obstructive sleep apnea cases. Even so, Type IV devices are on track to grow the fastest—9.21% a year through 2031—due to lower prices, direct-to-consumer sales, and AI that can interpret single-channel data. These one- or two-channel products (often pulse oximetry, actigraphy, or single-lead ECG) have never met CMS’s four-channel rule for reimbursed diagnosis, yet their advantages are hard to ignore.

A test costs about USD 150–300, the sensors are more comfortable, and patients can wear them for a week or longer without the hassle of nasal cannulas or chest belts. That combination makes them popular for cash-pay wellness checks, employer programs, and ongoing monitoring. Samsung’s Galaxy Watch, cleared in early 2024, shows how consumer wearables are moving into this space, while SleepImage uses single-lead ECG to generate a Sleep Quality Index and now has clearance for children as young as two. ResMed’s NightOwl—a disposable PAT device approved for ten-night studies—sits on the borderline between Type III and Type IV, aiming squarely at the multi-night niche where single-use economics beat rental logistics.

Type II devices, which include EEG and chin EMG for full sleep staging, stay niche because they cost more and take longer to set up, but they shine in complex cases—an area Huxley Medical’s SANSA patch now addresses with 100% sensitivity and 99% specificity for central sleep apnea.

By Distribution Channel: Digital Pathways Accelerate

Offline distributors, such as DME suppliers, hospital sleep centers, and physician offices, controlled 70.12% of revenue in 2025, yet online platforms will expand at an 8.56% CAGR through 2031. This acceleration means online outlets will account for an increasing share of the Home Sleep Screening Devices market over the forecast period. Telehealth partners embed HSAT ordering in virtual visits, while employer wellness programs subsidize screening to cut absenteeism. ResMed’s 2025 purchase of VirtuOx shows incumbents pivoting into service delivery to defend territory.

Even so, reimbursement guards remain up. UnitedHealthcare requires a physician order and technologist scoring, blocking fully automated DTC models from insurance payments. Europe’s DiGA framework offers a reimbursement template for AI-scored tools, and China’s Alipay deployment proves digital reach at a population scale. Data privacy rules—GDPR in Europe and HIPAA in the United States—add compliance costs but also build trust. Net gains will favor online expansion, lifting the total Home Sleep Screening Devices market as platform models harvest latent demand among undiagnosed users.

Geography Analysis

North America generated 49.34% of 2025 revenue, helped by Medicare’s uniform HSAT codes (95800/95801/95806) and large health systems eager to clear lab backlogs. The United States drives most of this value, with about 54 million adults living with mild-to-severe OSA and more than 20 million of them still undiagnosed. Recent fee-schedule cuts and the 2023 ban on derived channels have squeezed prices and slowed uptake of single-channel wearables. A 2026 Mayo Clinic review showed that primary-care HSAT pathways trimmed the median wait for treatment from 113 to 28 days, but specialist-managed patients logged 13% better nightly PAP adherence, highlighting a trade-off between speed and long-term outcomes. Canada’s coverage varies by province—Ontario and British Columbia lead—while Mexico’s fragmented private insurance keeps adoption low outside major cities. With high-probability adults now widely tested, companies are turning to underdiagnosed groups such as women, minority communities, and children. FDA clearances for WatchPAT (12 years and older) and SleepImage (down to age 2) open these segments, although payer policies are still catching up.

Europe is on track for an 8.09% CAGR through 2031 as the Medical Device Regulation (MDR) aligns standards, digital-health programs expand reimbursement, and the Philips Respironics consent decree pushes customers toward new suppliers. Germany’s DiGA framework already reimburses AI-scored sleep apps, while France’s PECAN pathway and NICE guidance in the UK support HSAT use in primary care. Funding, however, is uneven: Germany, France, and the UK provide solid public support, whereas much of Southern and Eastern Europe rely on out-of-pocket spending or private cover. MDR’s tougher evidence rules raise hurdles for small entrants but reward firms with strong clinical data. Investor interest remains high; Onera Health’s EUR 30 million Series C round in 2024 and its seven-site German validation study underscore confidence in patch-based platforms.

Asia-Pacific combines a heavy disease burden with patchy market access. China’s adult OSA prevalence jumped from 8.1% to 26.9% over two decades—about 176 million people—yet provincial insurance coverage is inconsistent and rural patients often pay cash despite higher prevalence rates. Alipay’s Hang Hao Meng AI tool has already screened more than 3 million users and flagged 90,100 potential cases, but without a national reimbursement policy, many never move to diagnostic testing. Japan’s mature sleep-medicine network supports steady HSAT use, though its national insurance still favors lab studies. India remains limited by an urban concentration of specialists and no unified HSAT payment under Ayushman Bharat. Elsewhere, the Middle East & Africa and South America are still early-stage markets. Adoption there centers on private clinics in the GCC, South Africa, Brazil, and Argentina. Import duties, complex approvals, and absent public funding hold back growth, though pilot projects in Brazil’s SUS and South Africa’s NHI could widen access if they scale. Compliance with local certifications and environmental rules adds further cost for global manufacturers looking to enter these regions.

Competitive Landscape

The Home Sleep Screening Devices market shows moderate concentration. ResMed, Philips, and ZOLL Itamar anchor Type III and PAT segments, while startups such as Onera Health, Huxley Medical, and EnsoData pursue patch form factors and AI scoring. ResMed’s 2025 VirtuOx acquisition signals a move from pure hardware toward revenue diversified across testing, scoring, and therapy optimization. Philips continues recovery efforts post-recall and, in March 2026, teamed with Medtronic to pool oximetry and capnography assets, defending hospital accounts.

Venture funding fuels challengers; Onera closed a EUR 30 million Series C in early 2024 to fund patch-based PSG expansion. Huxley’s SANSA patch targets central sleep apnea and received FDA clearance in 2025. AI specialists such as EnsoData license algorithms that run across rival devices, hinting at hardware commoditization. Strategic vectors cluster around three levers: smaller, disposable sensors that lift adherence; AI that slashes scoring labor; and omnichannel distribution that captures untapped demand. Yet CMS mandates for manual overread and four-channel recordings preserve a moat around incumbent platforms. Conformity to FDA 510(k), ISO 13485, and ISO 27001 remains essential for payer and enterprise adoption across the Home Sleep Screening Devices market.

Home Sleep Screening Devices Industry Leaders

ResMed Inc.

Koninklijke Philips

ZOLL Itamar

Onera Health

Natus Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Sleepal introduced its AI-powered smart sleep system, functioning as both a tracker and a guide. This advanced solution allows users to monitor and optimize their sleep and bedroom environment without relying on wearables or physical contact, while seamlessly integrating into any interior design.

- December 2025: Huxley Medical gained FDA clearance for central sleep apnea detection with SANSA, posting 100% sensitivity and 99% specificity.

- April 2025: ResMed NightOwl widely available across the U.S., this small, FDA-cleared sensor fits on the finger and provides a simplified way for providers to diagnose Obstructive Sleep Apnea (OSA).

Global Home Sleep Screening Devices Market Report Scope

As per the scope of the report, home sleep screening devices are portable, prescription-based diagnostic tools designed to monitor breathing and oxygen levels in a patient's natural sleep environment.

The home sleep screening devices market is segmented by test type, distribution channel, and geography. Based on test type, the market is segmented into Type II, Type III, and Type IV. By distribution channel, the market is segmented into offline and online. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Type II |

| Type III |

| Type IV |

| Online |

| Offline |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Test Type | Type II | |

| Type III | ||

| Type IV | ||

| By Distribution Channel | Online | |

| Offline | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and growth forecast for the Home Sleep Screening Devices Market?

The Home Sleep Screening Devices Market reached USD 4.49 billion in 2026 and is projected to grow to USD 6.11 billion by 2031, registering a 6.36% CAGR during the forecast period.

Which test type dominates the market and why?

Type III devices commanded 66.23% market share in 2025, and Type IV is forecast to grow at 9.21% CAGR through 2031.

What is driving the shift from offline to online distribution channels?

Offline channels held 70.12% market share in 2025, yet online channels are forecast to expand at 8.56% CAGR through 2031, propelled by direct-to-consumer models, telehealth partnerships, and employer-sponsored wellness programs that bypass traditional durable medical equipment suppliers

Which geographic region offers the highest growth potential?

Europe is forecast to grow at 8.09% CAGR through 2031.

Page last updated on: