Hollow-Core Fiber Backbone Network Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.72 Billion |

| Market Size (2031) | USD 3.60 Billion |

| Growth Rate (2026 - 2031) | 37.97% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hollow-Core Fiber Backbone Network Market Analysis by Mordor Intelligence

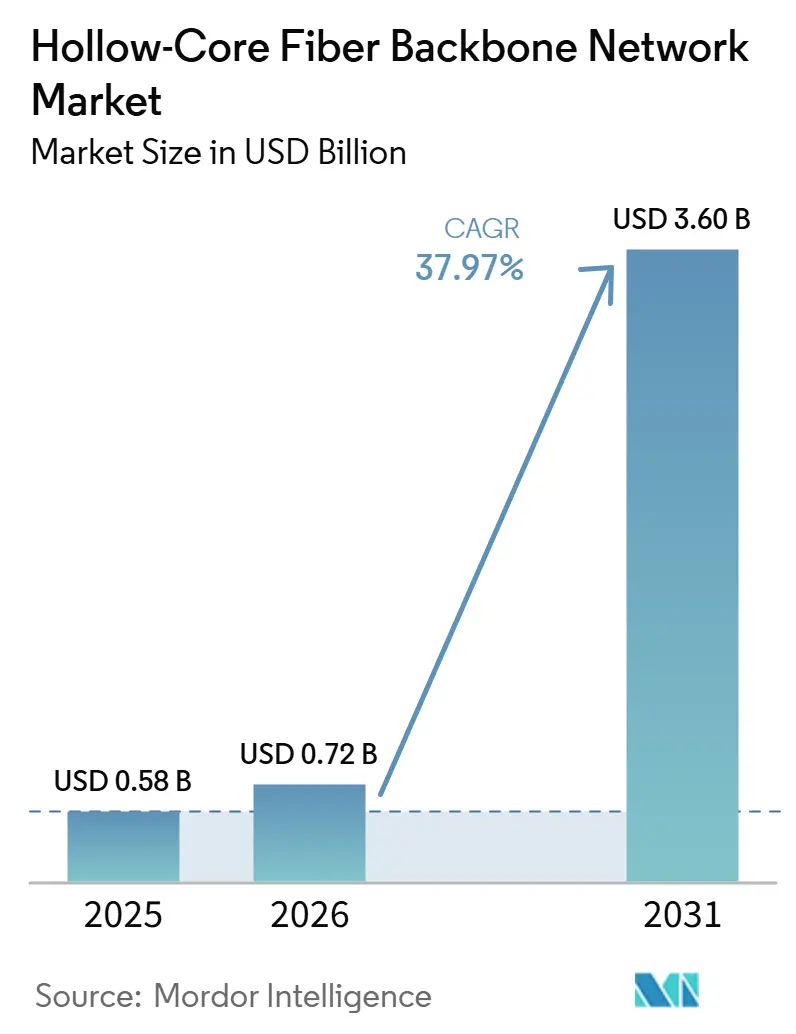

The Hollow-Core Fiber Backbone Network Market size is expected to increase from USD 0.58 billion in 2025 to USD 0.72 billion in 2026 and reach USD 3.60 billion by 2031, growing at a CAGR of 37.97% over 2026-2031. The hollow-core fiber backbone network market is moving into commercial deployment as cloud operators shift the technology from controlled trials to live backbone and inter-data-center networks. Demand is being shaped by the need for lower latency, more stable signal behavior, and wider transmission performance in AI-focused network architectures. Manufacturing partnerships are becoming a core competitive tool because access to production capacity now matters as much as fiber design quality in the hollow-core fiber backbone network market. The hollow-core fiber backbone network market is also benefiting from overlap among telecom transport, AI infrastructure, and quantum networking programs, widening the set of buyers beyond conventional optical network operators. This setup leaves the hollow-core fiber backbone network market with strong upside, but near-term growth still depends on how quickly supply, field deployment capability, and technical standardization improve.

Key Report Takeaways

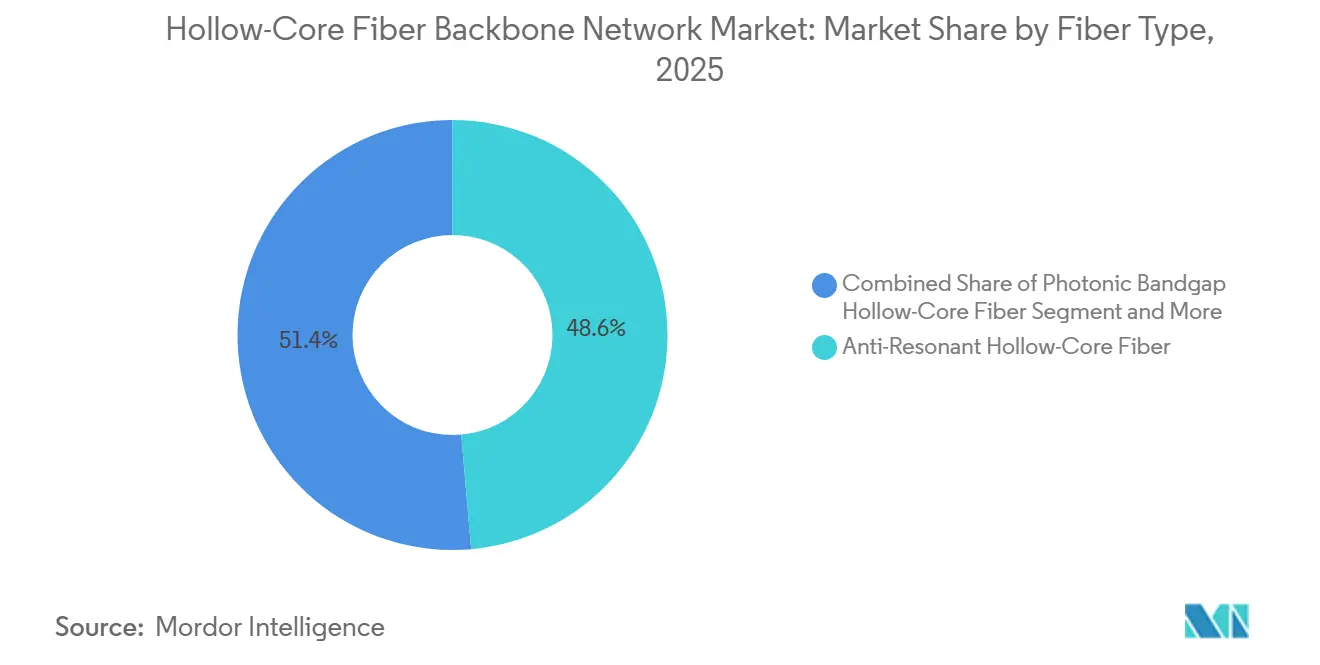

- By fiber type, anti-resonant hollow-core fiber held 48.61% revenue share in the hollow-core fiber backbone network market in 2025, while nested anti-resonant hollow-core fiber is projected to expand at a 42.31% CAGR through 2031.

- By application, telecom backbone networks accounted for 39.12% of revenue share in the hollow-core fiber backbone network market in 2025, while 5G and 6G transport networks are projected to expand at a 37.19% CAGR through 2031.

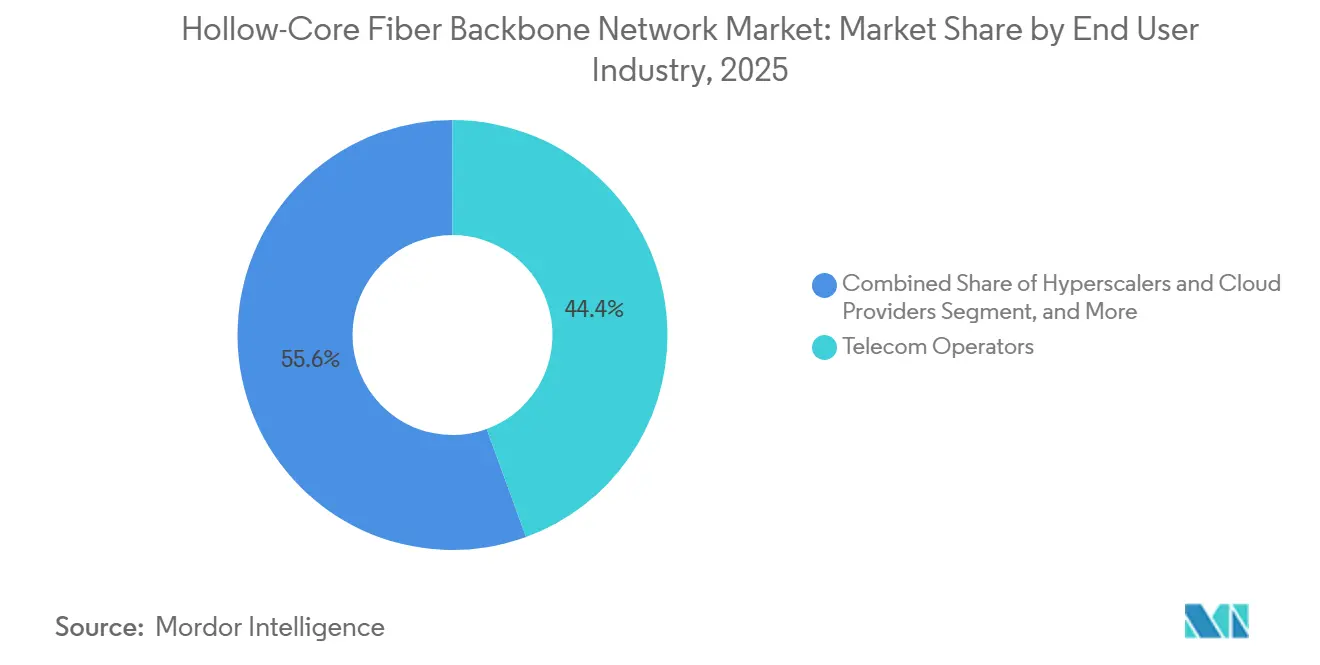

- By end user industry, telecom operators held 44.44% revenue share in the hollow-core fiber backbone network market in 2025, while hyperscalers and cloud providers are projected to expand at a 41.10% CAGR through 2031.

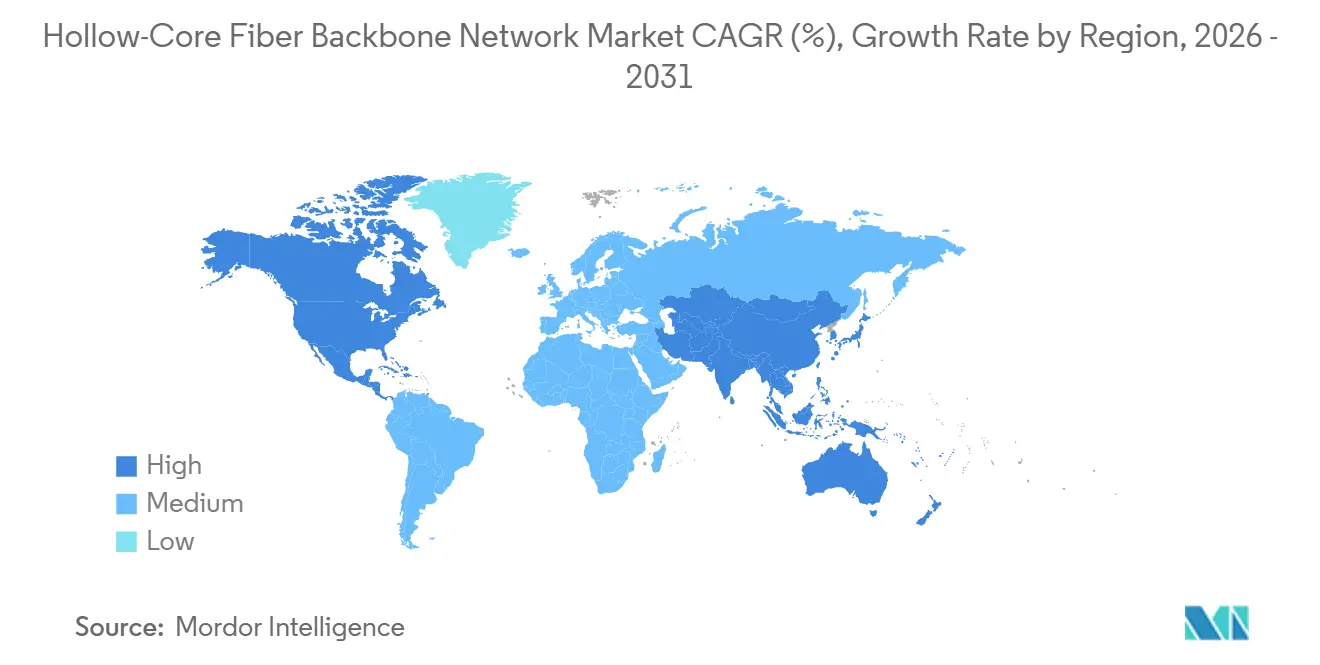

- By geography, North America held 35.50% revenue share in the hollow-core fiber backbone network market in 2025, while Asia-Pacific is projected to advance at a 38.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hollow-Core Fiber Backbone Network Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-Low Latency Demand in Backbone and Inter-Data-Center Links | +8.5% | Global, with highest intensity in North America and Asia-Pacific | Short term (≤ 2 years) |

| AI Training Clusters Need Deterministic Fiber Delay | +7.2% | Global, led by North America, with spill-over to Asia-Pacific and Europe | Short term (≤ 2 years) |

| 5G and 6G Transport Upgrade Cycles | +5.8% | Asia-Pacific core, spill-over to Europe and North America | Medium term (2-4 years) |

| Carrier and Hyperscaler Move to Vertical Integration | +4.9% | North America and Europe, with growing Asia-Pacific participation | Medium term (2-4 years) |

| Quantum Networking Readiness for Metro and Backbone Trials | +3.5% | Europe, North America, East Asia, including Japan and China | Medium term (2-4 years) |

| Rising Demand for Deterministic Network Performance in Industrial Automation and Edge Computing | +2.8% | Global, with early adoption in Germany, Japan, and South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ultra-Low Latency Demand in Backbone and Inter-Data-Center Links

Ultra-low latency remains the clearest near-term trigger for adoption in the hollow-core fiber backbone network market. Hollow-core fiber guides light through air rather than solid glass, reducing propagation delay and improving timing performance compared to standard single-mode fiber. Peer-reviewed work published in 2025 confirmed delay reductions in the 28-33% range relative to conventional fiber under transmission conditions relevant to modern optical networks. Commercial intent also became harder to ignore after Microsoft scaled live deployments and outlined a 15,000-km Azure expansion, following more than 1,280 km already carrying customer traffic between metro data center pairs. As latency becomes a priced service attribute rather than a background network metric, the hollow-core fiber backbone market is gaining traction on backbone routes, where even small timing gains can support premium workloads.

AI Training Clusters Need Deterministic Fiber Delay

The hollow-core fiber backbone network market is also being pulled forward by the way distributed AI training depends on highly stable delay across large accelerator clusters. Journal work published in 2025 showed that hollow-core transmission avoids many of the nonlinear limits that affect high-power, multi-wavelength transport in silica fiber, which supports more predictable signal behavior under demanding operating conditions. A second milestone came when Microsoft documented attenuation below 0.1 dB/km across record-wide bandwidth, which improves the case for longer spans without repeated optical amplification. That performance matters because AI network operators are now optimizing for synchronization efficiency rather than just raw bandwidth growth. In the hollow-core fiber backbone network market, this is pushing buyers to treat fiber design, manufacturing access, and deployment timing as part of a broader AI infrastructure strategy rather than as a routine cabling decision.

5G and 6G Transport Upgrade Cycles

Mobile transport upgrades are creating another path for the hollow-core fiber backbone network market, especially where fronthaul and midhaul networks need more latency headroom. A 2026 Optics Letters demonstration demonstrated 16.7 Tb/s full-duplex DWDM mobile fronthaul over a 10-km anti-resonant hollow-core fiber link in the C-band, directly supporting the case for advanced radio transport architectures.[1]Optica Editorial Team, “High-Throughput Full-Duplex DWDM IM-DD Mobile Fronthaul Based On Anti-Resonant Hollow-Core Fiber,” Optics Letters, opg.optica.org This result reduces a key qualification barrier by moving the discussion from theoretical suitability to proven transmission behavior in a relevant telecom setting. IEEE research also showed that the selective use of hollow-core fiber in latency-critical parts of a metro network can reduce the edge data center count by 29%, strengthening the case for hybrid deployment models rather than full network replacement. As carriers look at 5G evolution and early 6G transport planning, the hollow-core fiber backbone network market is likely to benefit most where operators choose targeted insertion on the most delay-sensitive routes.

Carrier and Hyperscaler Move to Vertical Integration

Vertical integration is reshaping how value is captured in the hollow-core fiber backbone network market. Microsoft has already tied advanced fiber design, manufacturing scale-up, and internal deployment more closely together through collaborations with Corning and Heraeus Covantics, which moved a major part of supply into a more controlled operating structure.[2]Corning Incorporated, “Corning Collaborates With Microsoft To Advance Performance And Reliability Of AI Networks,” Corning Incorporated, corning.com Prysmian and Relativity Networks then created an open-market counterweight through a long-term production agreement in Eindhoven, followed by Prysmian’s equity investment in 2025.[3]Prysmian Team, “Relativity Networks And Prysmian Partner For High-Volume Production Of Next-Generation Fiber-Optic Cable For Data Centers,” Prysmian, na.prysmian.com This pattern matters because buyers without captive supply need reliable alternatives if they want to scale beyond pilot routes. In practice, the hollow-core fiber backbone network market is separating into tightly controlled hyperscaler supply chains and a smaller open market that telecom carriers and other buyers still depend on.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Hollow-Core Fiber Manufacturing and Cabling | -3.8% | Global, most acute in emerging markets and Asia-Pacific | Short term (≤ 2 years) |

| Limited Splicing, Connectorization, and Field-Service Ecosystem | -2.9% | Global, most constraining outside North America and Europe | Short term (≤ 2 years) |

| Low Installed Base, Slower Standards Convergence, and Procurement Caution | -2.4% | Global, particularly constraining in South America, Middle East and Africa, and South Asia | Medium term (2-4 years) |

| Lack of Standardized Interoperability Between Hollow-Core Fiber, Optical Transceivers, and Existing Backbone | -1.8% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Hollow-Core Fiber Manufacturing and Cabling

High manufacturing cost remains the most visible barrier to broader adoption in the hollow-core fiber backbone network market. Recent scientific reviews showed that hollow-core production still faces a difficult mix of precision-geometry requirements, defect sensitivity, and yield variability, all of which keep usable output below what mainstream fiber-manufacturing economics would require. The same review noted that progress on low attenuation has been meaningful, but consistency across commercial draw runs still matters as much as best-case record performance. This cost burden limits adoption to links where low latency or signal quality carries direct economic value, such as AI interconnects, select backbone routes, and high-priority research networks. Until manufacturing yields improve and scale becomes more routine, the hollow-core fiber backbone network market is likely to remain concentrated in premium applications rather than spread evenly across standard carrier builds.

Limited Splicing, Connectorization, and Field-Service Ecosystem

The hollow-core fiber backbone network market also faces a deployment bottleneck at the installation layer. IEEE conference work published in 2025 showed that the interface between a hollow-core fiber and a standard single-mode fiber still introduces significant splice loss, even as laboratory methods improved performance to 0.97 dB through better arc settings and tapering approaches. This means field execution remains more specialized than in conventional optical cabling, thereby increasing installation time, training requirements, and project risk. Connectorization and maintenance practices are improving, but the service ecosystem is not yet broad enough to support uniform rollout across all regions. In the hollow-core fiber backbone network market, adoption is strongest in areas where specialist technical support and early-adopter network operators are already present.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fiber Type: Anti-Resonant Design Anchors Market, Nested Variant Accelerates

Anti-resonant hollow-core fiber held 48.61% of the hollow-core fiber backbone network market share in 2025, reflecting its greater manufacturing maturity and wider commercial availability. It has become the default option for many early deployments because buyers are balancing performance gains with supply reliability and installation confidence. The design’s position was reinforced by sub-0.1 dB/km attenuation milestones that were documented by Microsoft and echoed by commercial progress across the broader supply chain. In the hollow-core fiber backbone network industry, this has made anti-resonant fiber the practical first choice for data center interconnect and telecom backbone programs that need proven performance and stable sourcing.

The nested anti-resonant hollow-core fiber is projected to post the fastest growth in the hollow-core fiber backbone network market, with a 42.31% CAGR through 2031, supported by its stronger control of intermodal interference. That feature matters most in routes where signal purity is critical and mixed-traffic environments are expected to grow. Research published in npj Quantum Information showed that a nested anti-resonant hollow-core fiber supported three simultaneous entanglement-based quantum channels alongside 200 Gbps classical DWDM traffic, highlighting why this design is attracting attention in advanced network use cases. The photonic bandgap hollow-core fiber remained a niche, but 2025 conference work from Keio University confirmed stable underground campus performance over a full year, supporting its role in constrained deployments. Other designs were still in early development, and the lack of globally harmonized technical specifications continued to slow broader carrier procurement in the hollow-core fiber backbone network market.

By Application: Backbone Networks Lead While 5G and 6G Transport Segments Advance Fastest

Telecom backbone networks accounted for 39.12% of the hollow-core fiber backbone network market size in 2025, making them the largest application area. This lead reflects where carriers and cloud operators can justify a higher-performance fiber on routes that serve valuable, delay-sensitive traffic. Large-scale cloud deployments also supported this application layer, with Microsoft already carrying live customer traffic over more than 1,280 km of hollow-core routes and outlining much broader rollout plans. As a result, backbone use has moved ahead because it combines technical value, visible demand, and clearer network economics than less mature application categories.

5G and 6G transport networks are projected to expand at a 37.19% CAGR through 2031, which makes them the fastest-growing application segment. The strongest support for this came from the 2026 demonstration of 16.7 Tb/s full-duplex DWDM mobile fronthaul over anti-resonant hollow-core fiber, which directly addressed a core telecom qualification question. Data center interconnect applications are also expanding as hyperscalers move from controlled validation into production deployment, supported by fiber performance and manufacturing scale-up efforts. Quantum networks form a distinct application stream because the same fiber can support both secure quantum channels and high-speed classical traffic, broadening the buyer base beyond conventional telecom programs. Other applications were adopted earlier, but their presence showed that the hollow-core fiber backbone network market is not tied to a single demand path.

By End User Industry: Telecom Operators Command Share As Hyperscalers Drive Growth

Telecom operators held a 44.44% share of the hollow-core fiber backbone network market in 2025, reflecting their role as owners and buyers of backbone transport infrastructure. Their leadership was rooted in network control, existing route footprints, and the ability to place hollow-core fiber on select premium corridors rather than across entire systems at once. The 2025 NPS, Nokia, and Etisalat validation at 153 Tb/s on a live network segment showed that carrier-grade use is moving beyond theory and into structured operational evaluation. Even so, operator buying cycles remained more deliberate because cost, field standards, and the depth of the service ecosystem still mattered in investment decisions.

Hyperscalers and cloud providers are projected to grow at the fastest CAGR, 41.10% through 2031, which shows how directly AI infrastructure buildout is influencing the hollow-core fiber backbone network market. These buyers are treating hollow-core fiber as a strategic asset rather than as a standard line item, and that is why production partnerships and captive supply are becoming central to competition. Research and defense organizations are also becoming more relevant because hollow-core fiber supports both quantum key distribution and classical high-speed traffic on the same plant. Enterprises and financial institutions remained more selective, but their interest is meaningful in routes where lower latency has a direct operating or revenue impact. In the hollow-core fiber backbone network industry, this creates a demand mix in which large buyers drive early scale, while smaller, specialized users expand the range of viable applications over time.

Geography Analysis

North America held 35.50% of the hollow-core fiber backbone network market in 2025, making it the leading regional contributor. The region remained the commercial center in 2026 because Microsoft’s Lumenisity-based platform, large hyperscaler campus density, and Corning’s North Carolina manufacturing support were all concentrated there. Microsoft’s live traffic deployment and its 15,000-km expansion plan also showed that the region was moving beyond test environments into production networks. Canada and Mexico remained secondary within the region, with a larger role in cross-border traffic support than in independent fiber platform leadership.

Asia-Pacific is projected to record the fastest growth in hollow-core fiber backbone network market share, at a 38.43% CAGR through 2031. The region’s pace is being supported by a combination of state-backed research, domestic fiber manufacturing capability, and telecom upgrade programs. YOFC reported commercial-scale production below 0.1 dB/km and described more than 10 live hollow-core fiber projects across Asia, Europe, and the Americas at MWC Barcelona 2026, which underlined the region’s strong execution capacity. Japan added another layer of strength when Lightera Japan, OKI Electric Industry, and Keio University completed the first single-fiber bidirectional wideband WDM transmission demonstration on hollow-core fiber in May 2026. This left Asia-Pacific positioned as the main growth engine of the hollow-core fiber backbone network market, with China and Japan setting the tone for both commercial and research progress.

Europe remained strategically important in the hollow-core fiber backbone network market because it hosted major production and research assets, even though it did not lead in the 2025 share. Prysmian’s Eindhoven agreement with Relativity Networks, followed by its equity investment, gave the region a critical role in building open-market supply outside captive hyperscaler structures. South America was earlier in adoption, but Lightera, Scala Data Centers, and Nokia completed the first hollow-core fiber proof of concept in Brazil in 2025, demonstrating that the deployment case is extending into new hyperscale regions. Middle East markets were beginning to absorb the technology through sovereign AI and advanced infrastructure programs, although public disclosure remained limited. Africa still lagged because hyperscaler density and cost tolerance remained lower, but niche use around key terrestrial backhaul routes could emerge later in the forecast period.

Competitive Landscape

The hollow-core fiber backbone network market is moderately concentrated, with competition defined more by supply-chain position than by broad price competition. Microsoft sat at the center of the most integrated model through its control of Lumenisity-origin technology and its production ties with Corning and Heraeus Covantics, which kept a large share of advanced supply aligned with Azure deployment plans. That strategy gave Microsoft an advantage in timing, deployment control, and access to scarce manufacturing capacity. It also raised the importance of alternative supply chains for buyers that cannot depend on captive hyperscaler ecosystems.

The open-market side of the hollow-core fiber backbone network market was led by YOFC and Prysmian, with Relativity Networks and Lightera. YOFC pushed one of the most aggressive expansion strategies by combining commercial project rollout, a June 2026 long-haul transmission record, and a broad ecosystem push around HollowBand at MWC Barcelona 2026. Prysmian took a different route by pairing its production infrastructure in Eindhoven with an equity stake in Relativity Networks, positioning it as a critical supplier for buyers seeking non-captive capacity. Lightera’s work in Japan and Brazil showed that regional proof points also matter, especially when suppliers need to prove installation readiness in live environments. These moves show that competitive strength in the hollow-core fiber backbone network market is now tied to who can secure production, validate deployment, and stay close to hyperscaler and carrier buying programs.

A second layer of competition is forming around service capability, interoperability, and route-specific deployment expertise. The hollow-core fiber backbone network market still lacks a broad field-service ecosystem, meaning installation, splicing, and operational support remain significant bottlenecks rather than routine activities. Companies that can combine manufacturing access with reliable deployment support are likely to build buyer trust faster than firms that publish only technical performance records. This leaves the hollow-core fiber backbone network market in a position where scale will depend not only on better fiber, but also on who can make the full deployment model repeatable across regions.

Hollow-Core Fiber Backbone Network Industry Leaders

Microsoft Corporation

Corning Incorporated

Prysmian S.p.A.

Nokia Corporation

Relativity Networks, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: YOFC set a new world record for long-haul HCF transmission, demonstrating 51.3 Tb/s over 206.5 km of hollow-core fiber in the first field trial of a system capable of 1.2 Tb/s per wavelength without intermediate signal regeneration, validating backbone-scale HCF capacity on a live commercial cable.

- May 2026: Lightera Japan, OKI Electric Industry, and Keio University completed the world's first demonstration of single-fiber bidirectional wideband WDM transmission, 1.26-1.58 μm, using HCF under Japan's Ministry of Internal Affairs and Communications research program, unlocking a pathway toward power-efficient all-photonic network architectures.

- April 2026: Microsoft Azure and HUBER+SUHNER strengthened their collaboration, with HUBER+SUHNER committing to expanded HCF cable and connector manufacturing volumes at its Herisau, Switzerland, facility to support Microsoft's rolling deployment of HCF across additional Azure regions globally.

Global Hollow-Core Fiber Backbone Network Market Report Scope

The hollow-core fiber backbone network market's revenue comes from fiber cables, networking solutions, deployment and integration, design and installation, testing and maintenance, and infrastructure implementation for telecom operators, hyperscalers, data centers, research and defense organizations, financial institutions, and enterprises across telecom, cloud, 5G/6G, quantum networking, and data center interconnect applications. The hollow-core fiber backbone network market report is segmented by fiber type (anti-resonant hollow-core fiber, photonic bandgap hollow-core fiber, nested anti-resonant hollow-core fiber, and other hollow-core fiber types), application (telecom backbone networks, data center interconnect, 5G and 6G transport networks, quantum networks, and other applications), end user industry (telecom operators, hyperscalers and cloud providers, research and defense organizations, enterprises and financial institutions, and other end user industries), and geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in value (USD).

| Anti-Resonant Hollow-Core Fiber |

| Photonic Bandgap Hollow-Core Fiber |

| Nested Anti-Resonant Hollow-Core Fiber |

| Other Hollow-Core Fiber Types |

| Telecom Backbone Networks |

| Data Center Interconnect |

| 5G and 6G Transport Networks |

| Quantum Networks |

| Other Applications |

| Telecom Operators |

| Hyperscalers and Cloud Providers |

| Research and Defense Organizations |

| Enterprises and Financial Institutions |

| Other End User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of the Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Fiber Type | Anti-Resonant Hollow-Core Fiber | |

| Photonic Bandgap Hollow-Core Fiber | ||

| Nested Anti-Resonant Hollow-Core Fiber | ||

| Other Hollow-Core Fiber Types | ||

| By Application | Telecom Backbone Networks | |

| Data Center Interconnect | ||

| 5G and 6G Transport Networks | ||

| Quantum Networks | ||

| Other Applications | ||

| By End User Industry | Telecom Operators | |

| Hyperscalers and Cloud Providers | ||

| Research and Defense Organizations | ||

| Enterprises and Financial Institutions | ||

| Other End User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the hollow-core fiber backbone network market?

The hollow-core fiber backbone network market was valued at USD 0.58 billion in 2025, was estimated at USD 0.72 billion in 2026, and is forecast to reach USD 3.6 billion by 2031 at a CAGR of 37.97%.

Which fiber type leads adoption today?

Anti-resonant hollow-core fiber led with 48.61% share in 2025 because it had the strongest commercial maturity and the broadest manufacturing base.

Which application is growing the fastest?

5G and 6G transport networks are projected to grow the fastest at a 37.19% CAGR through 2031, supported by rising demand for lower-latency mobile transport.

Which end users are shaping demand the most?

Telecom operators held the largest 2025 share at 44.44%, while hyperscalers and cloud providers are projected to grow the fastest at 41.10% through 2031.

Which region offers the strongest expansion outlook?

Asia-Pacific is projected to post the fastest regional CAGR at 38.43% through 2031, supported by commercial rollout activity in China and advanced research progress in Japan.

What is the main barrier to wider deployment?

The biggest hurdle remains cost and deployment readiness, because manufacturing yield, splicing complexity, and field-service capability still limit broader rollout beyond premium routes.

Page last updated on: