High-Speed And Low-Loss Printed Circuit Board Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

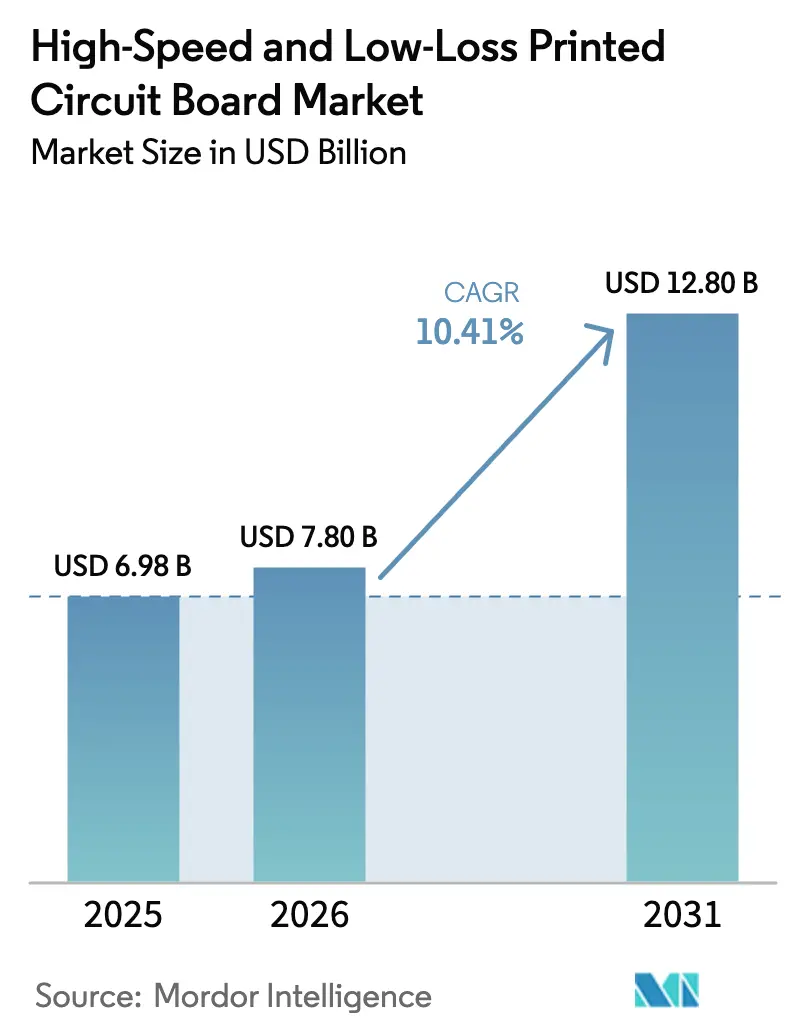

| Market Size (2026) | USD 7.80 Billion |

| Market Size (2031) | USD 12.80 Billion |

| Growth Rate (2026 - 2031) | 10.41% CAGR |

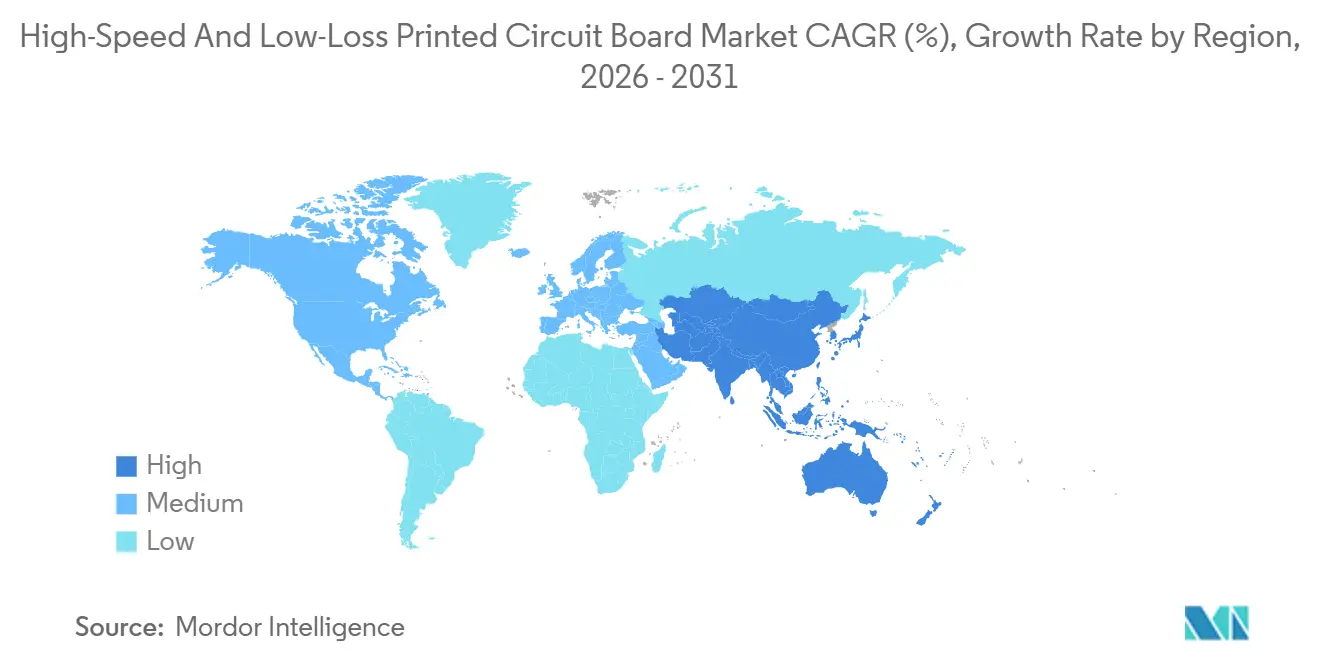

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

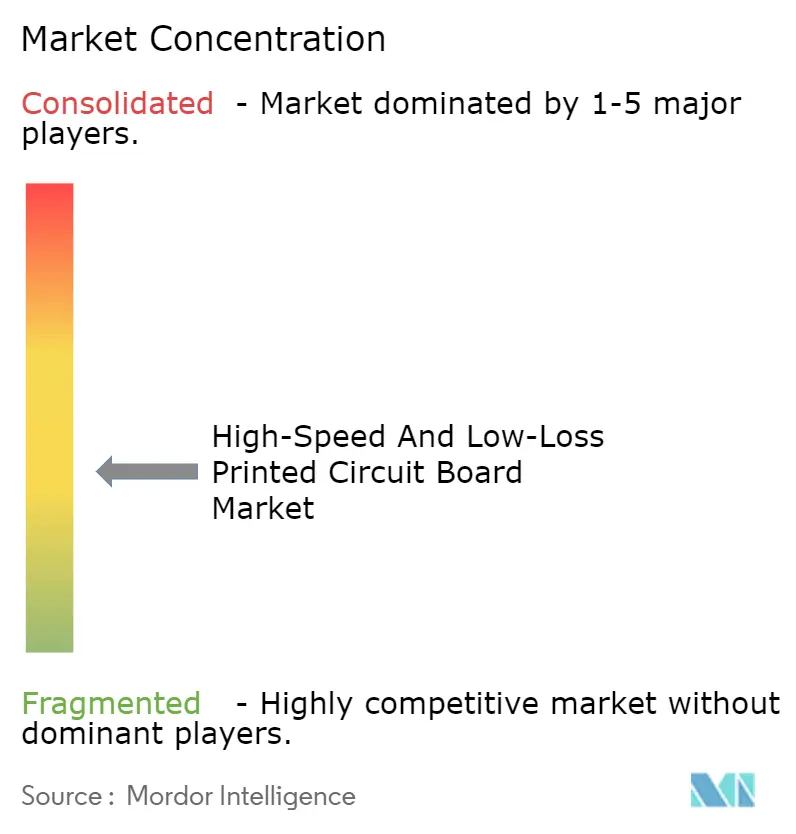

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High-Speed And Low-Loss Printed Circuit Board Market Analysis by Mordor Intelligence

The High-Speed And Low-Loss Printed Circuit Board Market size is projected to expand from USD 6.98 billion in 2025 and USD 7.80 billion in 2026 to USD 12.80 billion by 2031, registering a CAGR of 10.41% between 2026 to 2031. Surging demand for 112 G SerDes lanes, PCIe 7.0 backplanes, and 77 GHz automotive radar boards is accelerating substrate innovation. Material vendors are reformulating epoxy blends with polyphenylene oxide and liquid crystal polymer to meet dielectric-loss budgets below 1 dB per inch at 56 GHz, while board fabricators invest in sequential lamination presses that enable 30-plus layer counts. Hyperscale data-center operators are co-designing switch fabrics with PCB suppliers to tighten skew tolerances to sub-50 ps, and automotive OEMs are embracing zonal architectures that push multilayer rigid-flex demand. At the same time, copper-foil cost inflation and shortages of ultra-low-Dk/Df resins are squeezing margins and tilting the competitive edge toward vertically integrated players.

Key Report Takeaways

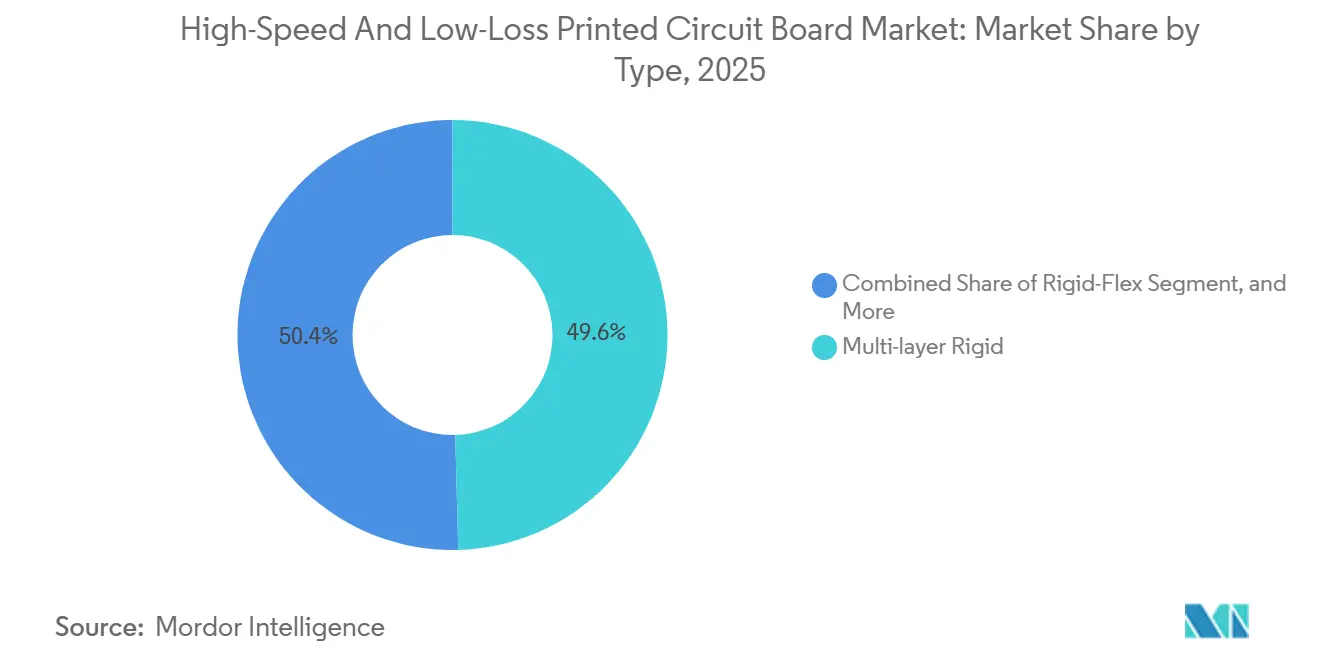

- By pcb type, multilayer rigid boards captured 49.57% of the high-speed and low-loss printed circuit board market share in 2025; rigid-flex boards are forecast to expand at an 11.27% CAGR to 2031.

- By material, modified-epoxy/PPE/PPO blends accounted for 38.29% share of the high-speed and low-loss PCB market size in 2025, whereas liquid-crystal-polymer substrates are projected to grow at an 11.59% CAGR.

- By performance tier, high-speed digital (10–25 Gbps) accounted for 41.29% of the revenue share, while ultra-high-speed digital (above 25 Gbps) is projected to register the fastest growth at an 11.12% CAGR.

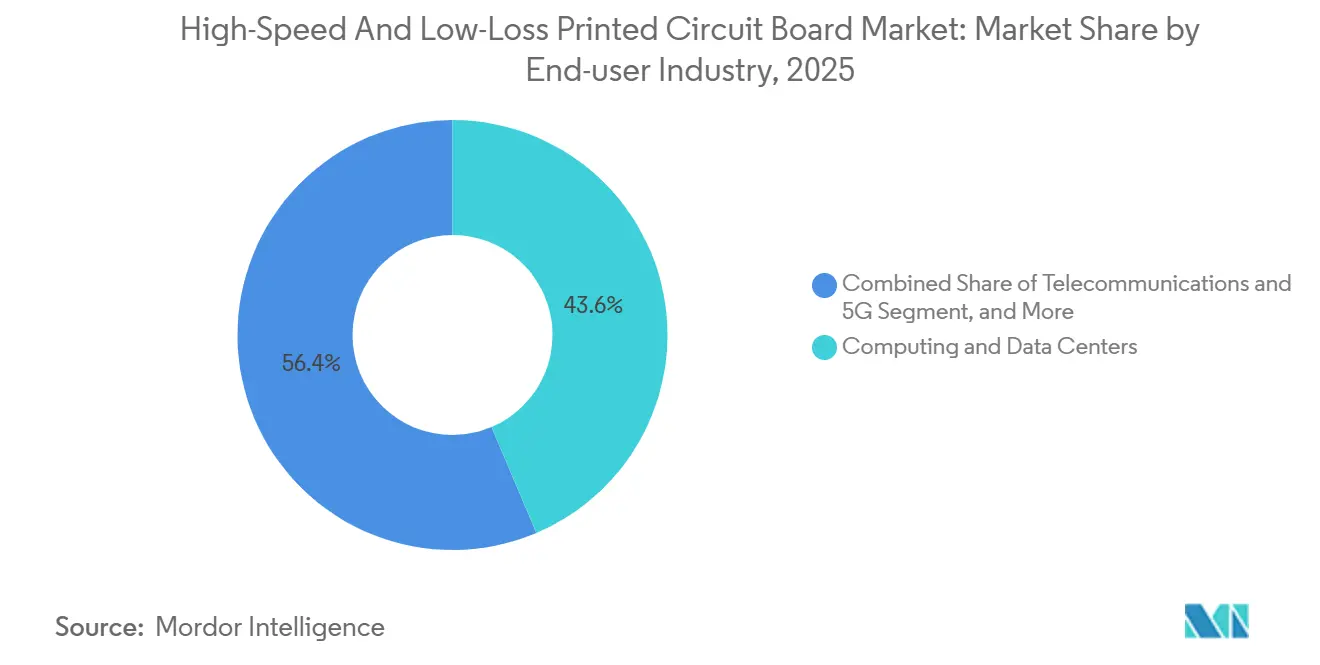

- By end user, computing and data centers held 43.61% of the revenue share in 2025; telecommunications and 5G infrastructure are expected to exhibit the highest CAGR at 11.78% through 2031.

- By geography, Asia-Pacific led with 53.87% revenue share in 2025, while North America recorded the fastest CAGR at 11.52% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global High-Speed And Low-Loss Printed Circuit Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of 112G SerDes and PCIe 7.0 Interfaces | +2.10% | North America, Asia-Pacific (Taiwan, China, South Korea) | Medium term (2-4 years) |

| Rapid Adoption of AI Accelerators in Hyperscale Data Centers | +2.30% | Global, with concentration in North America and Asia-Pacific | Short term (≤ 2 years) |

| 5G-Advanced Infrastructure Requiring Low-Loss Boards | +1.80% | Asia-Pacific, Europe, North America | Medium term (2-4 years) |

| Automotive Radar and High-Bandwidth In-Vehicle Networking | +1.60% | Europe, Asia-Pacific (China, Japan, South Korea), North America | Long term (≥ 4 years) |

| Space-Constrained mmWave Satellite Terminals for LEO Constellations | +1.20% | Global, with early adoption in North America and Europe | Long term (≥ 4 years) |

| Government Incentives for Local Laminate Manufacturing in Asia-Pacific | +1.40% | Asia-Pacific (China, Taiwan, South Korea, India) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of 112 G SerDes and PCIe 7.0 Interfaces

The PCI-SIG ratified PCIe 7.0 in 2025, doubling data rates to 128 GT/s and shrinking eye diagrams, so insertion loss budgets now sit below 1 dB per inch at 56 GHz.[1]PCI-SIG, “PCI Express 7.0 Specification,” pcisig.com Laminate makers are shifting to finer ceramic fillers and reverse-treated copper with sub-2 µm roughness to preserve signal integrity. OEMs demand sub-50 ps skew across 1 m backplanes, concentrating spend with a handful of board houses that master sequential via-stub back-drilling. The rapid rollout is compressing design cycles, favouring suppliers that offer simulation-to-fabrication services and guarantee lead times under 10 weeks.

Rapid Adoption of AI Accelerators in Hyperscale Data Centers

NVIDIA’s 1.8 Tbps NVLink interconnect on its 2025 Blackwell GPU pushes dielectric constants below 3.2 and mandates Tg above 180 °C to survive liquid-cooled chassis environments.[2]NVIDIA Corporation, “Fiscal 2025 Annual Report,” investor.nvidia.com Hyperscale’s in the United States and China are locking multi-year laminate contracts, straining global resin capacity. Lead times for ultra-low-loss cores exceeded 20 weeks in early 2026, prompting EU and Indian governments to subsidize domestic PCB lines. Board shops able to validate 30-plus layers at 50 °C ambient win a premium, while smaller fabricators migrate back to sub-25 Gbps work.

5G-Advanced Infrastructure Requiring Low-Loss Boards

Release 18 adds radar-like sensing, forcing co-located RF and digital processing on single substrates. Operators specify fluoropolymer or ceramic-filled laminates to hold loss under 0.5 dB per inch at 28 GHz. China deployed 3.6 million 5G sites by 2025, with 12% in mmWave bands.[3]3GPP, “Release 18 Specifications,” 3gpp.org Regional price sensitivity creates a split market: urban macros use PTFE-based boards, while rural rollouts rely on modified-epoxy blends. Suppliers able to tier their portfolios capture volume without margin erosion.

Automotive Radar and High-Bandwidth In-Vehicle Networking

Regulators now allow higher EIRP at 77-81 GHz, extending detection range and tightening phase coherence needs. Ceramic-filled laminates with Dk 3.0-3.5 balance RF loss and mechanical rigidity through -40 to 125 °C cycles. The shift toward zonal architectures links radar, lidar, and domain controllers over IEEE 802.3ch multigigabit Ethernet, creating pull for rigid-flex boards that cut harness weight by 30%. Cost pressures curb adoption outside premium models, but long qualification timelines lock in suppliers once design-wins occur.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of Ultra-Low Dk/Df Resin Formulations | -1.40% | Global, with acute shortages in North America and Europe | Short term (≤ 2 years) |

| Yield Challenges in Sequential Lamination of HDI Stack-Ups | -1.10% | Asia-Pacific (Taiwan, China, South Korea), North America | Medium term (2-4 years) |

| Rising Copper Foil Prices Tightening PCB Margins | -0.90% | Global | Short term (≤ 2 years) |

| Limited Skilled Workforce for RF Material Processing | -0.70% | North America, Europe, select Asia-Pacific facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Ultra-Low Dk/Df Resin Formulations

Polyphenylene oxide and liquid crystal polymer output is concentrated with a few chemical majors running above 90% capacity, leaving little flex for AI-driven surges. Capital needs exceed USD 200 million for a 5 ktpa plant, discouraging new entrants. Laminate vendors resort to hybrid epoxy-ceramic recipes that lower Dk marginally but raise CTE, complicating automotive reliability tests. Shortages have extended laminate lead times and tempered the high-speed and low-loss printed circuit board market growth in North America and Europe.

Yield Challenges in Sequential Lamination of HDI Stack-Ups

Boards over 20 layers see yields dip below 80% as inner layers endure multiple press cycles. AT&S lifted IC-substrate yields to 82% by late-2025 yet scrap costs for ultra-high-speed panels still top USD 500 per sheet. Smaller firms exit the segment, pushing customers toward vertically integrated giants that can amortize process tweaks, thus restraining competitive diversity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By PCB Type: Rigid-Flex Gains on Miniaturization Demand

Multilayer rigid boards generated the largest slice of the high-speed and low-loss printed circuit board market revenue in 2025. Computing backplanes, telecom routers, and industrial drives favour their flat form factors and mature process economics. The segment will keep incremental growth as PCIe 6.0 and 7.0 systems proliferate. Rigid-flex formats, however, deliver the strongest momentum. Satellite terminals, foldable consumer devices, and surgical wearables need boards that bend in three axes without compromising impedance. Lockheed Martin’s next-gen fighter program will triple rigid-flex assemblies per airframe, underscoring uptake in aerospace applications.

Rigid-flex expansion is helped by process advances such as laser-drilled stacked microvias and embedded passives that shrink bend radii under 1 mm. Nippon Mektron prototypes that exceed 12 layers while meeting sub-50 µm via diameters signal maturing yields. Yet a 2-to-3× cost premium limits penetration to premium SKUs. As equipment amortizes and yields climb, rigid flex could erode rigid share in high-volume consumer electronics beyond 2028.

By Material: LCP Surges for mmWave Antennas

Modified epoxy/PPE/PPO blends retained the highest revenue share in 2025, serving digital lanes up to 25 Gbps. The materials integrate smoothly with FR-4 processes and cure at standard profiles, keeping total cost low. Liquid crystal polymer substrates, however, post double-digit growth as mmWave radios and satellite phased arrays proliferate. LCP’s 0.04% moisture uptake and CTE under 17 ppm/°C sustain layer registration through orbital thermal swings. Rogers RO3003G2’s commercial success with base-station antenna OEMs highlights the shift.

Fluoropolymer laminates like PTFE preserve sub-0.3 dB per inch loss at 40 GHz, locking them into defense radars and aerospace payloads, though high price restricts mainstream telecom use. Ceramic-filled boards bridge the gap, balancing RF loss and mechanical stability for automotive radar and power amplifiers. As hyperscalers specify higher lane speeds, more digital workloads migrate to next-generation modified-epoxy lines such as Isola Astra MT77, which offers insertion loss under 1.2 dB per inch at 56 GHz while retaining standard process flows.

By End-User Industry: Telecom Surges with Standalone 5G

In the high-speed and low-loss printed circuit board market, computing and data centers anchored demand in 2025 at 43.61%, powered by GPU-rich racks and edge inferencing nodes. Telecom moves fastest, buoyed by Release 18 small-cell rollouts and 1.6 Tbps Ethernet links. Ericsson shipped 28% more radios year over year in 2025, with mmWave units rising to 18% of mix.

Automotive applications grow steadily as OEMs pivot to zonal control networks and 79 GHz radar. Defense retains reliable, low-volume demand, bolstered by domestic sourcing mandates such as DFARS 252.225-7009. Medical, test-and-measurement, and broadcast niches round out consumption, benefiting from telehealth adoption and SDR migration.

By Performance Tier: Ultra-High-Speed Digital Accelerates

High-speed digital 10-25 Gbps boards remain workhorses for enterprise servers, SANs, and 100 GbE routers. Yet ultra-high-speed digital boards above 25 Gbps are outpacing legacy growth, with a 10.88% CAGR, supported by PCIe 6.0/7.0 adoption in AI clusters. The tighter noise margins of PAM-4 signaling drive designers toward differential-pair impedance windows of ±5% and via stubs below 10 mils. Simulation suites embed machine-learning optimizers, but full-wave solvers remain compute-intensive, leading OEMs to selectively apply them on critical nets.

Radio-frequency sub-6 GHz boards continue steady demand as carriers densify 4G and 5G macros. Millimeter-wave and satellite boards, while the smallest slice, are registering the fastest revenue growth due to LEO constellations. SpaceX’s second-generation terminal specification illustrates the pivot to LCP substrates for beam-steering arrays.

Geography Analysis

Asia-Pacific high-speed and low-loss printed circuit board market dominated revenue at 53.87% in 2025, driven by integrated supply chains encompassing resin, laminate, and board fabrication. Taiwan’s Unimicron and Nan Ya PCB coordinate closely with TSMC and OSAT houses, shortening prototype cycles. China’s CNY 15 billion (USD 2.1 billion) subsidy program accelerates ultra-low-loss laminate lines, targeting import substitution. South Korea’s giants are expanding IC-substrate capacity in Busan to back captive chip and display units. Japanese vendors still lead fluoropolymer and LCP chemistries but face price competition from Chinese newcomers.

North America contributed 22% of 2025 sales, buoyed by hyperscale data-center expansion and defense offset programs. The CHIPS and Science Act granted USD 285 million in 2025 for PCB lines in Arizona and Texas. TTM Technologies is investing USD 150 million to equip its Syracuse plant with 30-layer sequential presses. Canada services automotive and telecom niches from Ontario and Quebec, whereas Mexican maquiladoras attract Asian board makers seeking near-shore capacity for U.S. customers.

Europe held about 15% share, with Austria-based AT&S scaling Leoben for IC substrates and Germany’s automotive tier-ones driving radar demand. The EU Chips Act earmarks EUR 3.3 billion (USD 3.6 billion) for advanced packaging, yet higher energy and labour costs hamper competitiveness. Brazil leads South America’s sub-5% slice, supplying telecom gear but remains reliant on imported laminates.

Competitive Landscape

High-Speed and Low-Loss printed circuit board Market Top 10 laminate suppliers capture roughly 60% of global revenue, while the leading 20 board fabricators hold about 45% of volume. Vertically integrated players lower risk by owning resin, copper foil, and press lamination. Shengyi’s 2025 acquisition of a PPO line cut raw-material costs 12% and sliced lead time by three weeks. Rogers expanded its Arizona LCP facility by 40,000 ft² in January 2026 to serve 5G and satellite customers. Isola and Taiwan Union Technology are co-developing PCIe 7.0-ready modified epoxies due Q3 2026.

White space lies in co-packaged optics substrates, where only a handful of shops can embed waveguides and dissipate 500 W/in². Chinese challengers Kingboard and Nanya Plastics undercut incumbents in sub-25 Gbps boards, yet aerospace and defense remain locked to Japanese and U.S. sources due to qualification hurdles. AI-assisted board design and additive manufacturing open doors for niche prototypes, but high-volume economics still favour large footprints equipped with laser direct imaging and plasma desmear. IPC-6012DS Class 3/A has become table-stakes for telecom bids, raising compliance costs for late entrants.

High-Speed And Low-Loss Printed Circuit Board Industry Leaders

Rogers Corporation

Isola Group

Panasonic Holdings Corporation

Taiwan Union Technology Corporation (TUC)

ITEQ Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Rogers Corporation completed a USD 120 million expansion in Chandler, Arizona, adding LCP laminate capacity for mmWave 5G and satellite boards.

- December 2025: Isola Group and Taiwan Union Technology formed a joint program to release PCIe 7.0-optimized modified-epoxy laminates by Q3 2026.

- November 2025: Unimicron pledged TWD 8 billion (USD 256 million) for a new IC-substrate plant in Taoyuan, Taiwan, with 1.2 million m² annual output set for Q1 2027.

- October 2025: DuPont introduced Pyralux TK laminate for rigid-flex circuits, featuring Df 0.0025 at 10 GHz and Dk 3.2.

Global High-Speed And Low-Loss Printed Circuit Board Market Report Scope

The High-Speed and Low-Loss PCB Market Report is Segmented by Type (Multi-Layer Rigid, High-Density Interconnect, Rigid-Flex, Other Types), Material Type (Fluoropolymer-Based, Modified Epoxy/PPE/PPO Blends, Ceramic-Filled Laminates, Liquid Crystal Polymer, Other Advanced Substrates), Performance Tier (High-Speed Digital 10-25 Gbps, Ultra-High-Speed Digital Above 25 Gbps, Radio Frequency Sub-6 GHz, Millimeter-Wave and Satellite Above 24 GHz), End-User Industry (Computing and Data Centers, Telecommunications and 5G, Automotive and EV, Aerospace and Defense, Healthcare/Medical, Other End-User Industries), and Geography (North America, Europe, Asia-Pacific, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Multi-Layer Rigid |

| High-Density Interconnect (HDI) |

| Rigid-Flex |

| Other PCB Types |

| Fluoropolymer-Based (PTFE) |

| Modified Epoxy/PPE/PPO Blends |

| Ceramic-Filled Laminates |

| Liquid Crystal Polymer (LCP) |

| Other Advanced Substrates |

| High-Speed Digital (HSD 10-25 Gbps) |

| Ultra-High-Speed Digital (Above 25 Gbps) |

| Radio Frequency (RF) - Low/Mid Band (Sub-6 GHz) |

| Millimeter-Wave (mmWave) and Satellite (Above 24 GHz) |

| Computing and Data Centers |

| Telecommunications and 5G |

| Automotive and EV |

| Aerospace and Defense |

| Healthcare / Medical |

| Other End-User Industries |

| North America | United States |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Taiwan | |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Rest of World |

| By PCB Type | Multi-Layer Rigid | |

| High-Density Interconnect (HDI) | ||

| Rigid-Flex | ||

| Other PCB Types | ||

| By Material Type | Fluoropolymer-Based (PTFE) | |

| Modified Epoxy/PPE/PPO Blends | ||

| Ceramic-Filled Laminates | ||

| Liquid Crystal Polymer (LCP) | ||

| Other Advanced Substrates | ||

| By Performance Tier | High-Speed Digital (HSD 10-25 Gbps) | |

| Ultra-High-Speed Digital (Above 25 Gbps) | ||

| Radio Frequency (RF) - Low/Mid Band (Sub-6 GHz) | ||

| Millimeter-Wave (mmWave) and Satellite (Above 24 GHz) | ||

| By End-User Industry | Computing and Data Centers | |

| Telecommunications and 5G | ||

| Automotive and EV | ||

| Aerospace and Defense | ||

| Healthcare / Medical | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Taiwan | ||

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Rest of World | ||

Key Questions Answered in the Report

What is the current value of the high-speed and low-loss PCB market?

The market is valued at USD 7.8 billion in 2026.

How fast is the market expected to grow?

It is forecast to post a 10.41% CAGR and reach USD 12.80 billion by 2031.

Which region accounts for the largest revenue share?

Asia-Pacific led with 53.87% of global revenue in 2025.

Which board type is growing the fastest?

Rigid-flex constructions are projected to grow at an 11.27% CAGR through 2031.

What material shows the highest future growth?

Liquid crystal polymer substrates are set to advance at an 11.59% CAGR because of mmWave and satellite demand.

Which end-user sector will expand the quickest?

Telecommunications and 5G infrastructure is expected to grow at 11.78% CAGR as Release 18 networks roll out.

Page last updated on: