Size and Share of High-Purity Chemicals Market For DRAM Wet Processing

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

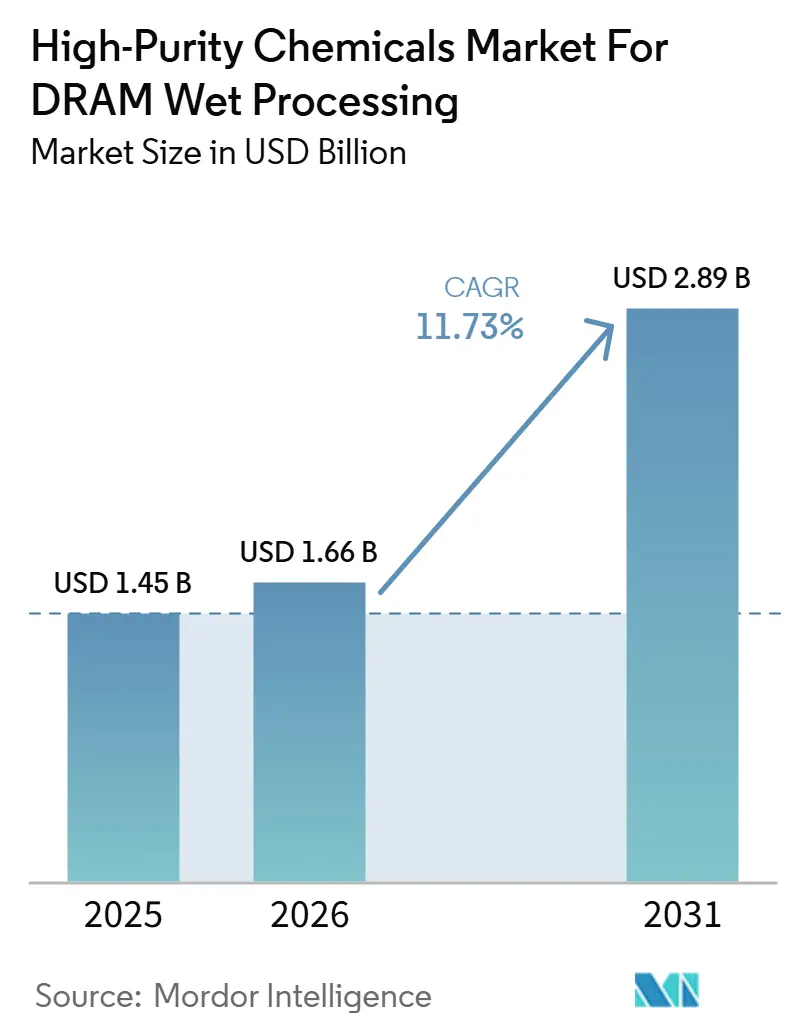

| Market Size (2026) | USD 1.66 Billion |

| Market Size (2031) | USD 2.89 Billion |

| Growth Rate (2026 - 2031) | 11.73% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of High-Purity Chemicals Market For DRAM Wet Processing by Mordor Intelligence

The high-purity chemicals market for DRAM wet processing size is expected to increase from USD 1.45 billion in 2025 to USD 1.66 billion in 2026 and reach USD 2.89 billion by 2031, growing at a CAGR of 11.73% over 2026-2031. Growth remains closely tied to AI-led memory demand, as DRAM manufacturers continue to expand advanced capacity and push deeper into more chemically intensive process generations. Wet processing plays a central role in DRAM fabrication because node migration adds more cleaning, etch, strip, and surface conditioning steps per wafer, rather than simply tightening existing specifications. This makes demand more resilient than in several other semiconductor materials categories, since qualified chemicals are consumed through recurring production flows and not only during fab build cycles. Supplier strength, therefore, depends on consistent ultra-high purity execution, secure access to critical feedstocks, and the ability to support customers through localized purification and packaging footprints. The result is a market where advanced grades maintain stronger pricing discipline, while commodity categories face greater pressure from regional competition and input volatility.

Key Report Takeaways

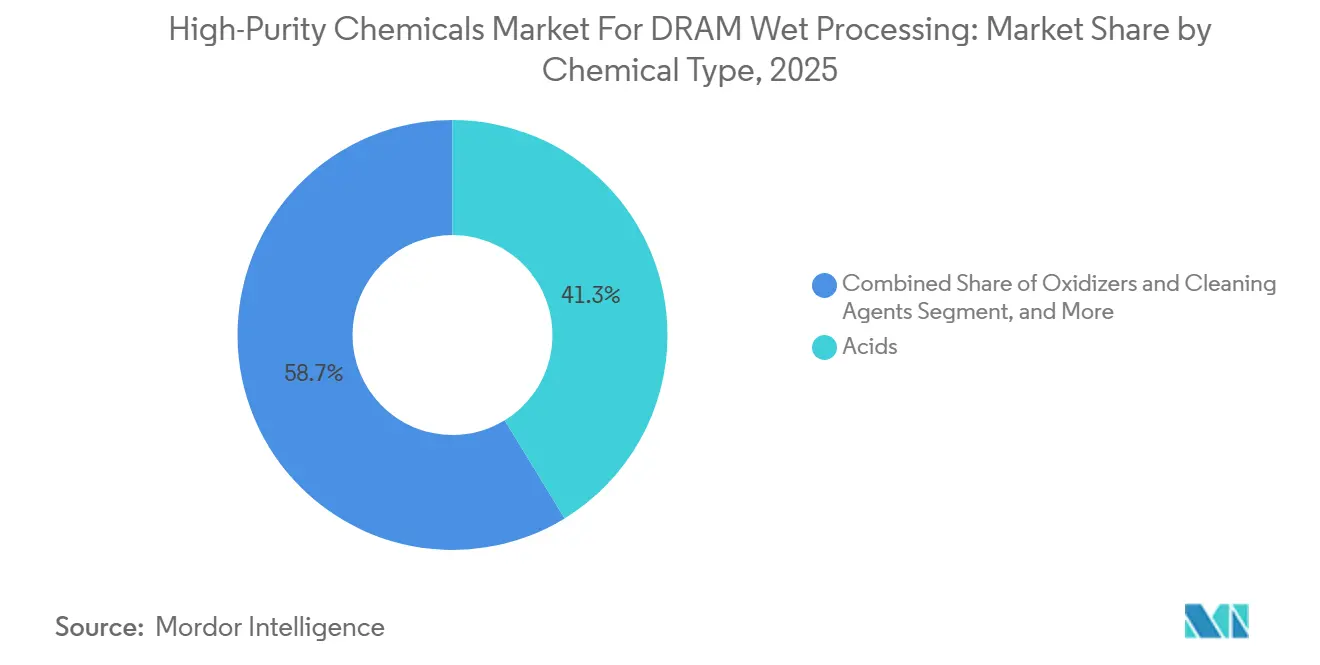

- By chemical type, acids accounted for 41.26% of the high-purity chemicals market for DRAM wet processing in 2025, while oxidizers and cleaning agents are projected to grow at a 12.64% CAGR through 2031.

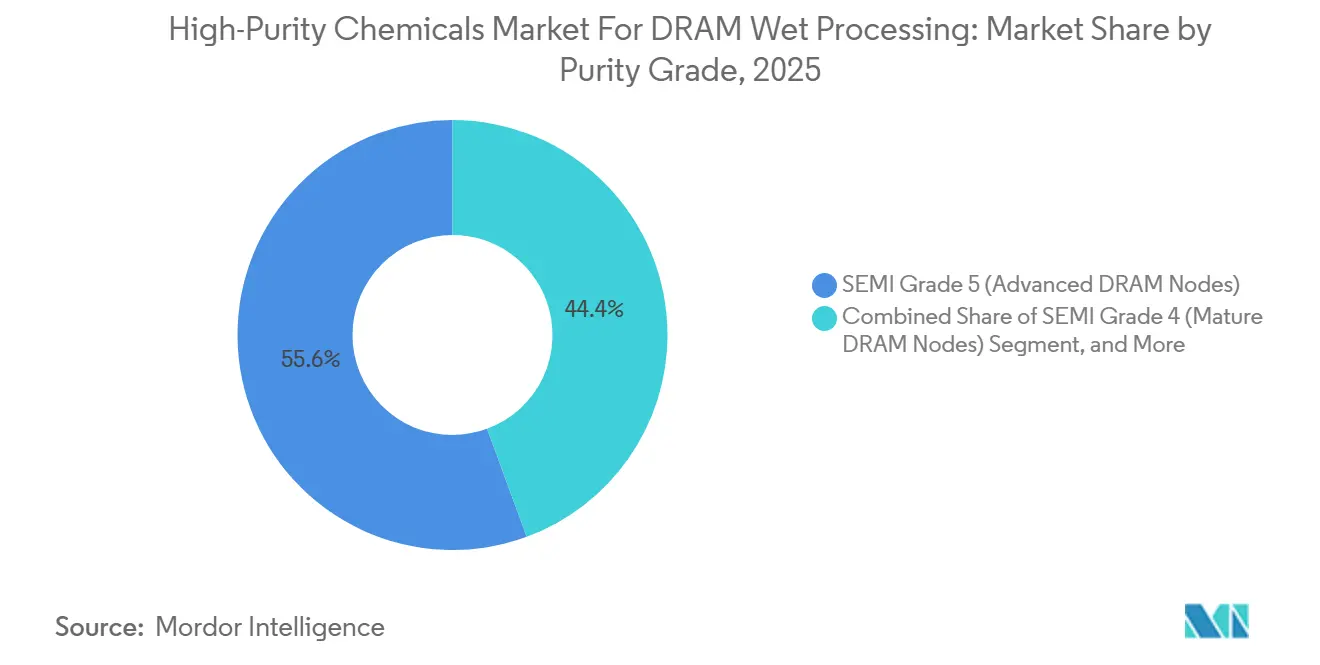

- By purity grade, SEMI grade 5 (advanced DRAM nodes) accounted for 55.61% of revenue in 2025, while emerging ultra-high purity and customized grades are projected to expand at a 12.31% CAGR through 2031.

- By DRAM product type, DDR5 DRAM held 32.46% of revenue in 2025, while HBM is projected to grow at a 12.86% CAGR through 2031.

- By process application, wafer cleaning accounted for 48.72% of the high-purity chemicals market for DRAM wet processing in 2025, while photoresist stripping is projected to expand at a 12.78% CAGR through 2031.

- By geography, Asia-Pacific held 87.53% of revenue in 2025, while North America is projected to expand at a 12.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Insights and Trends of High-Purity Chemicals Market For DRAM Wet Processing

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising DRAM Node Shrinks Increasing Wet Clean Intensity | +3.2% | Global, concentrated in South Korea, Taiwan, and Japan advanced-node fabs | Short term (≤ 2 years) |

| High Bandwidth Memory Expansion Driving Advanced Surface Preparation Demand | +2.8% | South Korea, Taiwan, with spill-over to North America, Indiana and Texas | Short term (≤ 2 years) |

| Tight Contamination Limits at Sub-PPTrillion Levels Raising Chemical Consumption Per Wafer | +2.1% | Global, highest impact at leading-edge nodes in South Korea and Taiwan | Medium term (2-4 years) |

| Fab Localization Incentives Expanding Qualified Chemical Buying Across New Capacity | +1.8% | North America and Europe core, spill-over to Japan | Medium term (2-4 years) |

| Dual Sourcing Requirements Favoring Suppliers with Multi-Region Purification Assets | +0.9% | Global, most acute in North America and Europe where local supply is nascent | Long term (≥ 4 years) |

| On-Site Chemical Blending and Packaging Integration Lowering Defect Risk in Wet Processing | +0.7% | Asia-Pacific core, with early gains in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising DRAM Node Shrinks Increasing Wet Clean Intensity

Each new DRAM node shrink adds more wet clean steps per wafer, not just tighter purity targets, which keeps recurring chemical demand rising in the high-purity chemicals market for DRAM wet processing. Research covering process nodes from N90 to A14 showed that wet processing accounted for 35-59% of total chemical consumption across a full technology flow, and it remained the dominant chemical-use block even at advanced geometries. That pattern means chemical demand can keep rising even when wafer start growth is moderate, because more chemistry is needed to process each wafer through the full sequence. The move to 1-beta and 1-gamma structures also adds deposition, selective etch, and residue-removal steps, increasing the number of required clean cycles. Suppliers that already meet the analytical framework used for liquid chemical qualification under SEMI C1 are better placed to defend incumbency as customers requalify chemicals generation by generation. This keeps the high-purity chemicals market for DRAM wet processing tied to technology migration and yield control, rather than just unit output.

High Bandwidth Memory Expansion Driving Advanced Surface Preparation Demand

HBM is one of the most chemically intensive DRAM formats because TSV formation, layer bonding, and post-etch cleaning require tighter surface control than conventional planar memory flows. Applied Materials said HBM output has been growing at roughly a 50% CAGR in recent years, a pace that is supporting healthy demand for advanced DRAM wafer processing and related materials capabilities. As TSV dimensions shrink and aspect ratios rise, residue removal becomes more sensitive, and the tolerance for particles and trace contaminants narrows. That raises both grade requirements and unit chemical consumption per wafer, especially in post-TSV and bonding surface preparation steps. In the high-purity chemicals market for DRAM wet processing, HBM matters not only because it is growing quickly, but also because it shifts revenue toward higher-value formulations. Suppliers with dedicated chemistries for hybrid bonding and advanced surface conditioning, therefore, stand to capture more value than suppliers focused only on conventional DDR flows.

Tight Contamination Limits at Sub-PPTrillion Levels Raising Chemical Consumption Per Wafer

Sub-10nm DRAM processing requires metallic impurity control at single-digit parts-per-trillion levels for some steps, turning chemical-grade selection into a yield decision in the high-purity chemicals market for DRAM wet processing. SEMI F115 defines a test method for determining the presence of metallic elements on wetted surfaces in ultra-high-purity chemical delivery systems and components, reinforcing that purity must be controlled throughout the full delivery path, not just in the liquid itself.[1]SEMI International Standards, “C00100 - SEMI C1: Guide for the Analysis of Liquid Chemicals,” SEMI Store, store-us.semi.org The practical effect is a broader contamination-control burden, since the container, line, dispensing system, and process tool must all remain within extremely tight limits. As tolerance windows narrow, fabs add more rinse cycles, more analytical checks, and more frequent requalification work to protect defect density and yield. This increases chemical consumption per wafer and strengthens suppliers with proven purification, packaging, and metrology infrastructure. The high-purity chemicals market for DRAM wet processing, therefore, benefits from a structural purity trend that is difficult to reverse at more advanced geometries.

Fab Localization Incentives Expanding Qualified Chemical Buying across New Capacity

Manufacturing incentives are expanding the qualified buyer base outside Asia, broadening the long-term opportunity set for the high-purity chemicals market for DRAM wet processing. NIST said the CHIPS Program Office included USD 39 billion in support for semiconductor manufacturing facilities, helping pull advanced capacity and supply-chain investment into the United States. New fabs do not provide instant supplier access, as wet chemicals still have to complete the full process and purity qualification before commercial use. That favors suppliers that can replicate purification, blending, packaging, and delivery standards across multiple regions without changing analytical consistency. BASF's 2025 decision to build semiconductor-grade H₂SO₄ and electronic-grade NH₄OH capacity in Ludwigshafen shows that suppliers are already positioning assets near expected demand growth nodes. Over time, this localization trend should reduce single-region supply exposure while adding new revenue pools to the high-purity chemicals market for DRAM wet processing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-High Purity Qualification Cycles Slowing New Supplier Entry | -1.2% | Global, most acute in North America and Europe, where new entrants lack fab-proximity track records | Long term (≥ 4 years) |

| High Cost of Electronic-Grade Purification, Packaging, And Analytical Control | -0.9% | Global, constraining capacity expansion among second-tier Asian suppliers | Medium term (2-4 years) |

| Regional Feedstock Concentration for Fluorinated and Oxidizing Inputs | -0.7% | South Korea and Japan, with spill-over to North America through precursor routes | Short term (≤ 2 years) |

| Water, Waste, And Emissions Compliance Burden on Wet Chemical Producers | -0.5% | Europe and South Korea, with early-stage pressure in the United States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ultra-High Purity Qualification Cycles Slowing New Supplier Entry

Ultra-high-purity qualification cycles are slowing new supplier entry into the high-purity chemicals market for DRAM wet processing, even as end demand remains strong. At leading-edge DRAM fabs, analytical verification, process compatibility testing, and yield-impact review can stretch qualification to 12-18 months for electronic-grade liquids and longer for new formulations. SEMI F115 extends this burden beyond the liquid itself, as wetted surfaces across delivery systems and components must also meet the metallic contamination requirements. Once a supplier is approved at a specific process step, switching costs become high because any change can disturb yield, tool performance, or long-cycle production stability. This helps incumbents defend their positions through multiple node generations and makes sole-source relationships more durable than in broader industrial chemical markets. The same barrier that protects margins also slows the pace at which new capacity translates into broader supplier choice inside the high-purity chemicals market for DRAM wet processing.

High Cost of Electronic-Grade Purification, Packaging, and Analytical Control

Electronic-grade purification, packaging, and analytical control keep the cost base of the high-purity chemicals market for DRAM wet processing well above commodity chemical benchmarks. SEMI Grade 5 production requires repeated purification, extremely low particle thresholds, and continuous batch release testing, which lifts both fixed and variable costs. BASF said in April 2025 that it was investing EUR 80 million (USD 87 million) in a new semiconductor-grade H₂SO₄ plant in Ludwigshafen, while also commencing construction of an electronic-grade NH₄OH facility at the same site. That scale of capital commitment is significant even for large chemical groups and is harder for second-tier suppliers to absorb without putting pressure on margins. Analytical failures also carry a high penalty because off-spec sub-ppt material cannot be easily redirected into other applications. As a result, capacity additions remain selective, and price competition at the highest-purity tiers remains more constrained than in the broader high-purity chemicals market for DRAM wet processing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Chemical Type: Acids Anchor the Volume Base, Oxidizers Gain with Node Complexity

Acids accounted for 41.26% of the high-purity chemicals market for DRAM wet processing share in 2025, confirming their central role across DRAM wet clean and etch sequences. Hydrofluoric acid, H₃PO₄, and H₂SO₄ remain basic inputs for native oxide removal, selective etch, and strip-related process steps that appear repeatedly across a wafer flow. This keeps acids at the core of the high-purity chemicals market for DRAM wet processing even as device architecture changes from one generation to the next. Their lead also reflects the cumulative nature of wet processing, as a wafer moves through many acid-dependent operations before reaching the final output. Feedstock tightness in fluorinated materials can therefore support growth in acid value even when supplier margins are under pressure.

Oxidizers and cleaning agents are projected to grow at a 12.64% CAGR through 2031, making them the fastest-rising chemical group in the high-purity chemicals market for DRAM wet processing. Advanced DRAM lines are using more sulfuric-peroxide mixtures, ozonated DI water, and high-purity hydrogen peroxide as residue sensitivity rises at smaller geometries. Solvay said its electronic-grade H₂O₂ business delivered double-digit volume growth, supported by a capacity doubling at its Zhenjiang facility completed in September 2025.[2]Solvay S.A., “Q1 2026 Earnings Roadshow Presentation,” Solvay, solvay.com Bases and solvents still matter, but solvents face more structural pressure where fabs move toward ozone-assisted or aqueous oxidant sequences for advanced stripping and surface preparation.

By Process Application: Wafer Cleaning Dominates, Photoresist Stripping Gains Speed

Wafer cleaning accounted for 48.72% of revenue in 2025, making it the largest application in the high-purity chemicals market for DRAM wet processing. Its scale reflects the cumulative weight of pre-gate, post-CMP, post-etch, and inter-level cleans that multiply as DRAM nodes become more complex. A peer-reviewed study found that wet processing remained the dominant chemical use across multiple node generations, supporting the large share of cleaning in total consumption. Front-end surface preparation and wet etching also maintained significant roles because advanced cell structures still depend on selective removal and defect-sensitive interfaces. This leaves the high-purity chemicals market for DRAM wet processing tilted toward contamination prevention rather than toward one-time process events.

Photoresist stripping is projected to expand at a 12.78% CAGR through 2031, the fastest pace among process applications in the high-purity chemicals market for DRAM wet processing. EUV-related patterning increases the number of resist-removal cycles per wafer, thereby increasing demand for acids, oxidizers, and specialized strip chemistries. Post-CMP cleaning and surface conditioning remain smaller in total volume, but they are technically differentiated because they must remove residue without damaging delicate dielectric layers. That gives proprietary formulations a premium role even when their volume stays below wafer cleaning inside the high-purity chemicals for DRAM wet processing industry.

By Purity Grade: SEMI Grade 5 Sets the Baseline, Customized UHP Grades Raise the Ceiling

SEMI Grade 5 formulations accounted for 55.61% of revenue in 2025, making them the dominant commercial tier for advanced DRAM process steps in the DRAM wet-processing high-purity chemicals market. SEMI C1 defines the analytical framework for assessing liquid chemical grades, and Grade 5 remains the reference point for leading-edge metallic impurity control. This matters because fabs evaluate not only nominal chemical composition but also trace metals, particles, and batch-to-batch repeatability under different delivery conditions. Grade 4 still serves mature DRAM markets, where contamination tolerance is looser, and price competition from regional suppliers is more pronounced. That leaves the purity ladder in the high-purity chemicals market for DRAM wet processing split between a broad mature-node base and a more protected advanced-node tier.

Higher emerging ultra-high-purity and customized grades are projected to grow at a 12.31% CAGR through 2031, the fastest rate in this segment of the high-purity chemicals for DRAM wet processing industry. Advanced nodes increasingly need tighter contamination control than standard off-the-shelf specifications can consistently provide in production conditions. Suppliers that add point-of-use purification, customer-specific blending, and inline analytical verification can capture higher-value positions as fabs move deeper into 1-gamma and later generations. This is pushing the high-purity chemicals market for DRAM wet processing toward more customized formulation supply and away from purely catalog-based selling.

By DRAM Product Type: DDR5 Leads Volume, HBM Raises Per-Wafer Chemical Intensity

DDR5 DRAM accounted for 32.46% of revenue in 2025, the largest product-type share in the DRAM wet-processing high-purity chemicals market. Its lead came from the shift in server and workstation memory demand toward AI infrastructure and higher-performance platforms. The chemistry profile for DDR5 still resembles mainstream advanced DRAM, but rising output keeps consumption strong across cleans, etch steps, and strip sequences. LPDDR5 and LPDDR5X continued to support a steady base in mobile and edge AI, while DDR4 remained relevant at mature nodes but lost momentum as platform transitions advanced. This kept the high-purity chemicals market for DRAM wet processing balanced between a large conventional base and a faster-changing performance memory mix.

HBM is projected to grow at a 12.86% CAGR through 2031, making it the fastest product subsegment in the high-purity chemicals for DRAM wet processing industry. Applied Materials said HBM's TSV and hybrid bonding steps require more advanced wet-chemical processes, which increase the chemistry content per wafer relative to conventional memory flows. That makes HBM important not only because it is growing quickly, but because it shifts value toward higher-grade surface preparation and post-etch formulations. As AI accelerators gain share, the high-purity chemicals market for DRAM wet processing is likely to carry a richer product mix than in earlier DRAM cycles.

Geography Analysis

Asia-Pacific accounted for 87.53% of revenue in 2025, thereby remaining the center of the high-purity chemicals market for DRAM wet processing. That concentration reflected the location of major DRAM production in South Korea, Taiwan, Japan, and China. South Korea remained the core demand base because Samsung Electronics and SK Hynix operated the highest concentration of advanced DRAM output. Taiwan added a secondary growth layer through NANYA Technology and Micron operations, while Japan served as both a consumption base and a supply base for specialty chemical exporters. As a result, the high-purity chemicals market for DRAM wet processing in Asia-Pacific combined fabs, purification infrastructure, and export capabilities into a tightly linked regional cluster.

North America is projected to grow at a 12.93% CAGR through 2031, making it the fastest-growing regional slice of the high-purity chemicals market for DRAM wet processing. NIST said CHIPS for America included USD 39 billion in support for semiconductor manufacturing facilities, helping attract upstream materials and supply-chain investment into the United States.[3]National Institute of Standards and Technology, “CHIPS for America,” NIST, nist.gov This does not reduce Asian dependence quickly, as each wet chemical still requires full purity and process qualification before high-volume use. Even so, new fab and packaging capacity in the United States is opening space for local purification, blending, and logistics support. Europe remained smaller in direct DRAM demand, but BASF's semiconductor-grade sulfuric acid and electronic-grade ammonium hydroxide investments in Ludwigshafen showed that local wet chemical supply capability was being built alongside broader semiconductor ambitions.

Rest of the World remained modest in absolute revenue within the high-purity chemicals market for DRAM wet processing. Southeast Asia was more relevant as a logistics, assembly, and distribution layer than as a leading-edge DRAM manufacturing base. The Middle East mattered strategically as a transit corridor for fluorinated feedstocks, which meant disruption there could ripple into global material availability. South America remained a negligible contributor during the forecast window because it lacked advanced memory fab infrastructure.

Competitive Landscape

The high-purity chemicals market for DRAM wet processing showed moderate concentration at the SEMI Grade 5 tier, where a small group of suppliers held durable qualified positions. Entegris, Merck KGaA, FUJIFILM Electronic Materials, and Stella Chemifa remained important because leading-edge fabs valued purity consistency, technical support, and switching-cost discipline. Below that ceiling, the high-purity chemicals market for DRAM wet processing was more fragmented, with regional Asian suppliers competing on mature-node acids, bases, and solvents. This created a two-layer structure, one shaped by qualification depth and one shaped by price. It also explained why advanced-grade products maintained stronger pricing discipline than more commoditized categories.

Merck said its Semiconductor Solutions business reached EUR 2.5 billion (USD 2.7 billion) in FY2025, supported by demand for advanced-node materials tied to AI chip systems. BASF announced in April 2025 that it was building a semiconductor-grade H₂SO₄ plant and an electronic-grade NH₄OH facility in Ludwigshafen, showing how the high-purity chemicals market for DRAM wet processing is drawing targeted capacity close to expected demand centers.[4]BASF SE, “BASF Invests in New Semiconductor-Grade Sulfuric Acid Plant in Ludwigshafen,” BASF News Release, basf.com Air Liquide inaugurated its first advanced materials manufacturing plant in Taiwan in March 2026, then signed a major June 2026 agreement linked to SK hynix in South Korea, extending its position across critical semiconductor inputs. These moves showed that location, purity control, and long-term contracts mattered as much as nominal product breadth. They also reinforced how customer proximity had become a competitive tool in the high-purity chemicals market for DRAM wet processing.

Entegris reported USD 1,799.1 million in FY2025 revenue from its Advanced Purity Solutions segment, highlighting the value of filtration, purification, and contamination-control capabilities alongside liquid chemicals. That left the clearest white space in post-Grade 5 customized formulations and in point-of-use purification models that can reduce transit-related contamination risk near the fab. In the high-purity chemicals market for DRAM wet processing, suppliers with mirrored purification networks across Asia and North America are better positioned to meet dual-source expectations without sacrificing analytical consistency. Competitive pressure is therefore likely to intensify around technical service, local packaging, and qualification support rather than only around headline volume.

Leaders of High-Purity Chemicals Market For DRAM Wet Processing

Entegris, Inc.

Stella Chemifa Corporation

Merck KGaA

FUJIFILM Corporation

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Air Liquide signed a major long-term contract with SK hynix, committing EUR 200 million (USD 232 million) to build and operate a nitrogen production unit at SK hynix's P&T7 advanced packaging facility in Cheongju, South Korea, dedicated to HBM chip production. The facility is scheduled to begin operations in late 2027 and significantly expands Air Liquide's footprint in the Korean semiconductor materials supply chain.

- April 2026: Air Liquide announced a EUR 200 million investment (USD 220 million) to build 2 industrial gas production units in Hiroshima, Japan, under a new long-term agreement with a leading global semiconductor manufacturer. The facilities will deliver ultra-pure N₂, O₂, and Ar and are scheduled to begin operations by end-2028.

- April 2026: FUJIFILM Corporation announced the development of the world's first fluorine-free negative ArF immersion photoresist, designed to be compatible with advanced nodes used in AI semiconductor manufacturing. The company began providing samples to customers in April 2026 and is targeting early commercialization following customer evaluations.

- March 2026: Air Liquide inaugurated its first large-scale Advanced Materials manufacturing plant in Taichung City, Taiwan, the first Air Liquide site in Taiwan dedicated to advanced deposition and etching materials. The move reinforced its supply-chain presence across 54 existing semiconductor industry facilities in the region.

Scope of Report on High-Purity Chemicals Market For DRAM Wet Processing

The high-purity chemicals for DRAM wet processing market covers the chemicals used in wet cleaning, etching, stripping, and surface preparation during dynamic random-access memory (DRAM) manufacturing. The scope includes ultra-high-purity acids, bases, solvents, and specialty formulations designed to meet stringent contamination control requirements in semiconductor fabrication.

The High-Purity Chemicals Market for DRAM Wet Processing Report is Segmented by Chemical Type (Acids, Bases, Solvents, and Oxidizers and Cleaning Agents), Process Application (Wafer Cleaning, Front-End Surface Preparation, Wet Etching, Photoresist Stripping, and Other Process Applications), Purity Grade (SEMI Grade 5 [Advanced DRAM nodes], SEMI Grade 4 [Mature DRAM nodes], and Higher Emerging UHP Grades/Customized Purity Formulations), DRAM Product Type (DDR5 DRAM, LPDDR5/LPDDR5X DRAM, HBM DRAM, DDR4 DRAM, and Specialty and Embedded DRAM), and Geography (North America, Europe, Asia-Pacific, and Rest of World). The Market Forecasts are Provided in Terms of Value (USD).

| Acids |

| Bases |

| Solvents |

| Oxidizers and Cleaning Agents |

| Wafer Cleaning |

| Front-End Surface Preparation |

| Wet Etching |

| Photoresist Stripping |

| Other Process Applications |

| SEMI Grade 5 (Advanced DRAM nodes) |

| SEMI Grade 4 (Mature DRAM nodes) |

| Higher Emerging UHP Grades / Customized Purity Formulations |

| DDR5 DRAM |

| LPDDR5 / LPDDR5X DRAM |

| HBM DRAM |

| DDR4 DRAM |

| Specialty and Embedded DRAM |

| North America | |

| Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Chemical Type | Acids | |

| Bases | ||

| Solvents | ||

| Oxidizers and Cleaning Agents | ||

| By Process Application | Wafer Cleaning | |

| Front-End Surface Preparation | ||

| Wet Etching | ||

| Photoresist Stripping | ||

| Other Process Applications | ||

| By Purity Grade | SEMI Grade 5 (Advanced DRAM nodes) | |

| SEMI Grade 4 (Mature DRAM nodes) | ||

| Higher Emerging UHP Grades / Customized Purity Formulations | ||

| By DRAM Product Type | DDR5 DRAM | |

| LPDDR5 / LPDDR5X DRAM | ||

| HBM DRAM | ||

| DDR4 DRAM | ||

| Specialty and Embedded DRAM | ||

| By Geography | North America | |

| Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

What is the size of the high-purity chemicals market for DRAM wet processing in 2026, and where is it heading by 2031?

The market is estimated at USD 1.66 billion in 2026 and is forecast to reach USD 2.89 billion by 2031, growing at a 11.73% CAGR over 2026-2031.

Which region leads demand for high-purity chemicals used in DRAM wet processing?

Asia-Pacific led with an 87.53% revenue share in 2025 because most global DRAM production remains concentrated in South Korea, Taiwan, Japan, and China.

Which chemical category holds the largest share in DRAM wet processing?

Acids led the mix with a 41.26% share in 2025, supported by the recurring use of hydrofluoric acid, H₃PO₄, and H₂SO₄ across clean and etch flows.

Which application is growing fastest across DRAM wet processing lines?

Photoresist stripping is projected to grow the fastest at a 12.78% CAGR through 2031, as advanced patterning increases strip cycles per wafer.

Why is HBM changing demand for wet processing chemicals?

HBM is projected to grow at a 12.86% CAGR through 2031, and its TSV and hybrid bonding steps require more advanced cleaning and surface preparation chemistries per wafer.

What is the main barrier for new suppliers trying to enter this space?

The biggest barrier is the long ultra-high purity qualification cycle, because fabs require extended analytical, compatibility, and yield validation before approving new chemical sources.

Page last updated on: