High Performance IMU Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 28.22 Billion |

| Market Size (2030) | USD 38.46 Billion |

| Growth Rate (2025 - 2030) | 6.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High Performance IMU Market Analysis by Mordor Intelligence

The High Performance IMU market size is expected to reach USD 28.22 billion by 2025 and is projected to grow to USD 38.46 billion by 2030, advancing at a 6.39% CAGR. Momentum stems from overlapping defense modernization agendas, expanding commercial space launches, and rising autonomy levels across automotive and industrial robotics. Navigation-grade and tactical-grade sensors are now indispensable whenever GPS denial, harsh environments, or sub-meter positioning accuracy significantly impact mission outcomes, ensuring procurement pipelines remain resilient despite macroeconomic fluctuations. System integrators are prioritizing turnkey inertial solutions that compress qualification timelines, while suppliers invest in vertically integrated optical fiber and ASIC capacity to protect margins. Export-control regimes continue to fragment global supply chains, nudging Asia-Pacific and Europe toward indigenous production and parallel technology ecosystems.

Key Report Takeaways

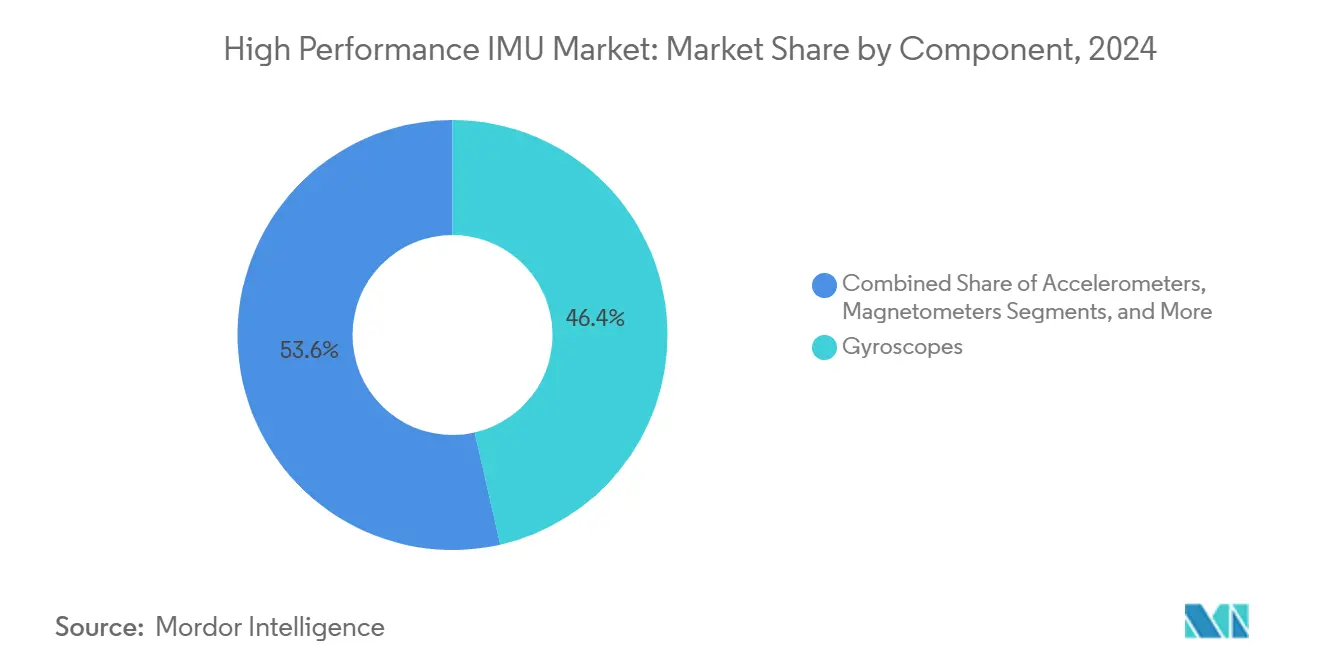

- By component, gyroscopes led with 46.44% revenue share in 2024, whereas magnetometers are forecast to expand at a 7.29% CAGR to 2030.

- By technology, the fiber optic gyro accounted for 32.39% of revenue in 2024, while the hemispherical resonator gyro is expected to post the fastest growth rate of 6.88% through 2030.

- By grade, navigation sensors captured 41.74% of sales in 2024; however, tactical sensors are projected to grow at a 7.63% CAGR through 2030.

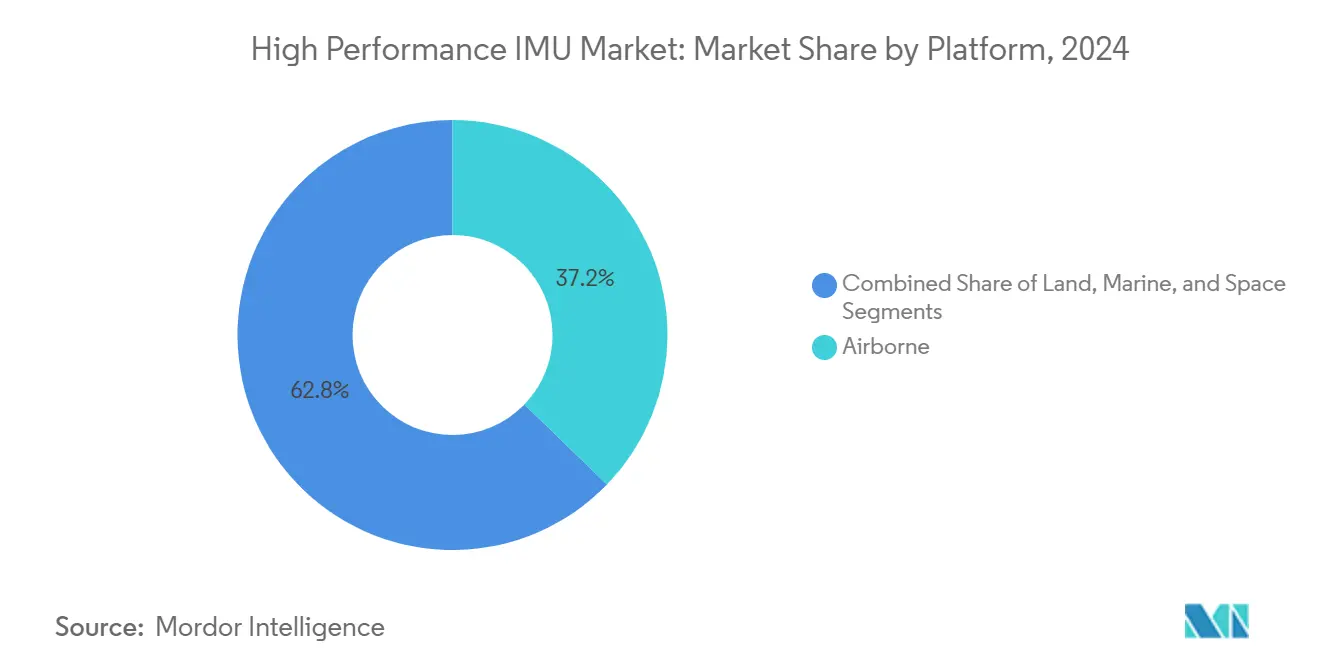

- By platform, airborne assets accounted for 37.23% of 2024 turnover, whereas space applications are expected to grow at a 7.19% CAGR during the forecast period.

- By end-user industry, the aerospace and defense sector contributed 44.61% of 2024 demand, while the automotive sector is on track for an 8.10% CAGR to 2030.

- By geography, North America commanded a 38.49% revenue share in 2024; however, the Asia-Pacific region is expected to accelerate at a 7.80% CAGR through 2030.

Global High Performance IMU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for navigation-grade IMUs in commercial spacecraft | +1.2% | Global, concentrated in North America and Asia-Pacific | Medium term (2–4 years) |

| Accelerated defense modernization programs worldwide | +1.4% | Global, led by North America, Asia-Pacific and Europe | Short term (≤ 2 years) |

| Increased autonomy requirements in industrial robotics | +0.9% | Asia-Pacific core, spillover to Europe and North America | Medium term (2–4 years) |

| Growing adoption of HRG technology for precision oil and gas drilling | +0.7% | Global, emphasis on Middle East, North America offshore | Long term (≥ 4 years) |

| Emergence of swarm-drone concepts requiring miniature high-end IMUs | +0.6% | North America and Europe defense, Asia-Pacific commercial | Medium term (2–4 years) |

| Advent of quantum-enhanced IMUs offering GPS-denied navigation | +0.4% | North America and Europe research hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Navigation-Grade IMUs in Commercial Spacecraft

Commercial launch providers are fielding thousands of satellites annually, and each payload requires multiple inertial units for attitude control and orbit maintenance. Starlink missions alone consume high volumes of navigation-grade sensors with sub-arcsecond bias stability, compelling suppliers to adopt automotive-style production throughput. Miniaturization efforts on vehicles, such as Rocket Lab’s Electron, free up avionics mass for payloads, further elevating IMU demand.[1]Rocket Lab, “Launch Vehicle Data Sheet,” rocketlabusa.com Redundant inertial suites on Blue Origin’s New Glenn reflect rising human-rating requirements, confirming that robust sensors remain mandatory even in an era of proliferated LEO constellations. The shift from bespoke, small-lot manufacturing to scaled production compresses qualification timelines and places pressure on cost structures, yet it simultaneously enlarges the total accessible market for High Performance IMU market suppliers.

Accelerated Defense Modernization Programs Worldwide

Defense ministries accelerated investment in hypersonic glide vehicles, collaborative combat aircraft, and autonomous ground systems that must operate in GPS-contested theaters. The United States FY 2025 budget sets aside USD 1.8 billion for Next Generation Air Dominance, embedding tactical-grade IMUs into unmanned wingmen. China’s People’s Liberation Army is scaling HRG-equipped glide weapons at production rates above 50 units per year, while India’s Atmanirbhar Bharat initiative pushes domestically produced ring laser gyros into the Tejas Mk2 fighter. European response to the Ukraine conflict drives urgent orders for loitering munitions, lifting inertial sensor backlogs at Thales and Safran. Consequently, the High Performance IMU market experiences sustained near-term pull from defense modernization efforts.

Increased Autonomy Requirements in Industrial Robotics

Collaborative robots operating in unstructured environments require centimeter-level pose accuracy, which is not readily available from consumer-grade MEMS. Amazon Robotics deployed more than 750,000 mobile robots by 2024, each equipped with IMUs to maintain localization when vision or lidar fails. Precision manufacturing for aerospace composites or semiconductor wafers similarly relies on gyroscopes with bias instability of less than 1 degree per hour. ISO 8373 and ISO 10218 mandate redundant sensing in safety-critical motions, embedding IMU performance directly into compliance. These specifications translate into a clear volume opportunity for tactical-grade suppliers striving to balance cost with accuracy, reinforcing growth for the High Performance IMU market.

Growing Adoption of HRG Technology for Precision Oil and Gas Drilling

Directional drilling operators favor HRG sensors for their low power draw, vibration tolerance, and azimuth accuracy near 0.1 degree in hostile downhole environments. Schlumberger reported 12% less non-productive time after fielding HRG-equipped tools in the North Sea.[2]Schlumberger Limited, “Annual Report 2024,” slb.com Immunity to magnetic interference is decisive in multilateral wells where magnetic survey tools lose integrity. Halliburton and Baker Hughes expanded HRG capacity to meet Middle Eastern demand for enhanced oil recovery projects. The oilfield’s high daily rig-rate economics support premium price points, giving HRG suppliers profitable beachheads even as they pursue space and defense use cases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply chain bottlenecks in specialty optical fibers | -0.8% | Global, acute in Asia-Pacific and Europe | Short term (≤ 2 years) |

| High calibration and testing costs limiting mass adoption | -0.6% | Global, pronounced in cost-sensitive automotive and industrial segments | Medium term (2–4 years) |

| Export-control regulations on tactical-grade sensors | -0.5% | Global, fragmenting North America, Europe and Asia-Pacific supply chains | Long term (≥ 4 years) |

| Thermal drift challenges in MEMS-based high-end IMUs | -0.4% | Global, constraining automotive and industrial robotics adoption | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Bottlenecks in Specialty Optical Fibers

Fiber optic gyro production relies on polarization-maintaining fiber, which is produced at fewer than ten plants worldwide, creating single-point failures that surfaced in 2024 as demand from commercial space and defense peaked. Lead times doubled to 26 weeks when Corning and Fujikura faced capacity ceilings.[3]Corning Incorporated, “Specialty Materials Overview,” corning.com Defense customers then insisted on reshoring fiber draws to meet domestic content rules, a transition that temporarily reduces output and raises costs. Given the dominance of FOG technology in navigation-grade systems, any fiber disruption ripples across airborne, marine, and space programs, capping upside for the High Performance IMU market until new draw towers come online.

High Calibration and Testing Costs Limiting Mass Adoption

Each navigation-grade unit requires multi-axis rate-table runs and thermal cycling, which can total 40 hours of machine time, tying up USD 2 million worth of capital test stands. In low-volume automotive pilots, calibration alone can exceed USD 500 per sensor, clashing with automakers’ target bill-of-material ceilings. Without firm volume commitments, sensor makers hesitate to invest in automated test cells that could amortize costs. The resulting stalemate hinders the penetration of tactical-grade devices into cost-sensitive sectors, thereby constraining near-term growth for the High Performance IMU market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Gyroscopes Continue to Provide the Core Reference

Gyroscopes generated 46.44% of 2024 revenue, underscoring their pivotal role as the backbone of angular rate in aviation, maritime, and missile guidance. The Magnetometers are expanding at a 7.29% CAGR. Ring laser gyros dominate agile aircraft needing rapid spin-up, while fiber optic gyros underpin naval vessels that value long-term bias stability. Accelerometers complement these devices by measuring specific force for dead reckoning, and magnetometers are fast becoming a standard in automotive sensor fusion frameworks destined for Level 4 autonomy. Ancillary temperature and pressure elements, though minor in bill-of-material share, improve drift compensation and help suppliers meet ASIL-D requirements.

Emerging hybrid assemblies blend MEMS gyroscopes for cost efficiency with optical gyroscopes for precision, a pathway Analog Devices demonstrated in 2024 prototypes for Tier 1 automotive clients. Honeywell’s 22% year-over-year increase in commercial aviation gyro shipments demonstrates that line-fit and retrofit programs continue to require large lot sizes, even as suppliers target new industrial buyers. These trends keep the High Performance IMU market integral to both legacy and next-generation motion platforms.

By Technology: HRG Gains Ground in Power-Sensitive Missions

Fiber optic gyro technology retained a 32.39% share in 2024 due to its maturity; however, the hemispherical resonator gyro is expanding at a 6.88% CAGR, as spacecraft builders and oilfield engineers prioritize low power draw and superior vibration resilience. Ring laser gyros remain critical for fast-maneuver missiles, despite their sensitivity to acoustic noise, whereas MEMS gyros satisfy price-driven industrial buyers where sub-degree accuracy is sufficient. Research funding in quantum rotation sensors signals long-term disruption possibilities, yet commercial deployments remain several years away.

Safran’s FOG units guide NASA’s Artemis lunar missions, highlighting FOG’s unmatched bias stability for deep-space voyages. By contrast, Northrop Grumman reduced power consumption by 60% by fielding an HRG-based unit for cubesats, making HRG a strong contender for proliferated LEO networks. This multifaceted landscape ensures that no single technology captures the entire high performance IMU market, sustaining healthy competition and specialization across various use cases.

By Grade: Tactical Sensors Multiply Across Unmanned Fleets

Navigation-grade devices secured 41.74% revenue in 2024, thanks to stringent accuracy demands in commercial aviation and naval fleets. Tactical-grade units, however, are projected to grow at 7.63% as armed forces increasingly utilize loitering munitions, small UAS, and unmanned ground vehicles that require sub-degree stability for missions lasting hours, not days. Industrial-grade sensors are designed for factory automation and logistics robots, whose localization cycles span minutes, whereas commercial-grade sensors are primarily used in consumer electronics.

The U.S. Marine Corps Organic Precision Fires-Mounted program and Israel Aerospace Industries Harop drone both illustrate how tactical-grade performance can meet accuracy benchmarks without imposing navigation-grade costs. Uptake within industrial AGVs further evidences spillover into civilian domains, fortifying the high performance IMU market as tactical specifications converge with price-sensitive adoption.

By Platform: Space Deployments Accelerate on Constellation Wave

Airborne systems accounted for 37.23% of the 2024 turnover, reflecting the extensive global fleet of fixed-wing, rotary, and unmanned aircraft. Yet, space platforms will advance at a 7.19% CAGR, propelled by mega-constellations, lunar surface missions, and the proliferation of small satellites. Land vehicles and industrial robots rely on ruggedized IMUs to withstand shock and temperature swings, while marine vessels mandate long-term bias stability to sustain submerged operations.

SpaceX launches that loft sixty-plus satellites per mission epitomize how constellation economics convert into large inertial procurement volumes. Honeywell supplies navigation-grade IMUs for OneWeb, and NASA’s Orion capsule further validates space as a premium use case.[4]Honeywell International, “Aerospace Investor Presentation 2024,” honeywell.com These developments solidify orbital demand as a key driver of growth for the high performance IMU market.

By End-User Industry: Automotive Autonomy Becomes the Fastest Adopter

Aerospace and defense maintained a 44.61% share in 2024, while automotive led growth with an 8.10% CAGR as Level 3 and Level 4 pilot programs transitioned toward series production. ISO 26262 functional safety enforces redundant sensing, pushing automakers to integrate tactical-grade devices for fail-operational navigation when GNSS is unavailable. Industrial automation, marine exploration, and oil and gas drilling round out additional niches, each valuing specific performance envelopes that premium sensors can satisfy.

Tesla’s Full Self-Driving and General Motors' Ultra Cruise both utilize high-precision inertial data to maintain sub-meter lateral accuracy, demonstrating that vehicle autonomy has become a credible and scalable demand node. As production ramps up, this sector will diversify revenue streams for suppliers historically reliant on defense, elevating the long-term opportunity in the high performance IMU market.

Geography Analysis

North America retains its technological leadership with a 38.49% market share in 2024. Robust federal defense budgets, commercial space launch cadence surpassing 100 missions, and a vibrant advanced air-mobility ecosystem together translate into steady procurement of navigation-grade and tactical-grade units. Canada adds naval and aerospace projects, while Mexico’s automotive assembly plants embed cost-optimized IMUs into ADAS platforms. Federal Aviation Administration certification pathways for eVTOL vehicles require redundant inertial suites, creating a new domestic opportunity in the high performance IMU market.

Asia-Pacific is poised for the fastest 7.80% CAGR. China expands autonomous underwater and hypersonic glide programs, while India’s indigenization mandates funnel business toward domestic gyro makers. Japan’s factory automation giants install tactical-grade units in collaborative robots, and South Korea’s Hyundai accelerates Level 3 rollouts that need centimeter-level localization. Australia’s AUKUS submarine commitments embed navigation-grade sensors into regional procurement pipelines, reinforcing the region’s demand momentum.

Europe balances defense urgency with industrial prowess. Ongoing conflict on the continent spurs fresh orders for loitering munitions and armored vehicle upgrades that specify tactical-grade IMUs. The European Union’s Galileo independence strategy propels sensor integration capable of multi-constellation fusion. In the Middle East, Saudi Arabia and the United Arab Emirates import tactical-grade devices for unmanned aerial systems, leveraging offset deals to gain local assembly know-how. South America is experiencing a resurgence in aviation deliveries from Embraer, resulting in modest but growing demand for navigation-grade units. Collectively, these regional storylines diversify the growth trajectory for the high performance IMU market and mitigate single-region risk.

Competitive Landscape

Moderate concentration defines the supplier matrix. Honeywell, Northrop Grumman, and Collins Aerospace anchor navigation-grade channels through vertically integrated fiber draws, ASIC lines, and field-proven calibration. Mid-sized competitors Safran, Thales, and KVH Industries cater to tactical and industrial niches, while newcomers Advanced Navigation and VectorNav leverage MEMS innovation to underprice legacy vendors in the swarm drone and small satellite markets.

Strategic moves focus on supply-chain security and adjacent areas. Northrop Grumman’s 2024 in-house fiber acquisition sliced FOG cost by 18%, demonstrating margin leverage. Honeywell’s push into the automotive sector aims for USD 500 million in inertial revenue by 2028, signaling its cross-vertical aspirations. Safran partnered with Exail to blend FOG and HRG portfolios tailored to European defense offsets. Start-ups hunt whitespace in quantum-enhanced and ultra-miniature designs, yet certification hurdles and ITAR classifications continue to favor established incumbents. This interplay positions the high performance IMU market for steady but contested expansion as suppliers race to align performance, cost, and regulatory compliance.

High Performance IMU Industry Leaders

Honeywell International Inc.

Northrop Grumman Corporation

Safran SA

Collins Aerospace (Raytheon Technologies Corporation)

Analog Devices Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Northrop Grumman won a USD 240 million U.S. Navy contract to deliver navigation-grade IMUs for Columbia-class ballistic submarines over five years.

- August 2024: Safran acquired a specialty optical fiber plant in France for EUR 85 million (USD 93 million) to secure FOG supply and meet 40% internal fiber needs by 2026.

- April 2024: Advanced Navigation received a USD 15 million Australian Defence Force contract to supply tactical-grade IMUs for autonomous underwater vehicles.

- March 2024: Analog Devices unveiled a hybrid MEMS-optical IMU prototype targeting Level 4 vehicle autonomy.

Global High Performance IMU Market Report Scope

High Performance IMU Market encompasses cutting-edge inertial measurement units tailored for accurate navigation, positioning, and motion tracking across sectors like aerospace, defense, automotive, marine, and industrial robotics.

The High Performance IMU Market Report is Segmented by Component (Gyroscopes, Accelerometers, Magnetometers, Other Components), Technology (Ring Laser Gyro, Fiber Optic Gyro, MEMS, HRG, Others), Grade (Navigation, Tactical, Industrial, Commercial), Platform (Airborne, Land, Marine, Space), End-User Industry (Industrial Automation, Aerospace and Defense, Automotive, Marine, Oil and Gas, Others), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Gyroscopes |

| Accelerometers |

| Magnetometers |

| Other Components |

| Ring Laser Gyro (RLG) |

| Fiber Optic Gyro (FOG) |

| Micro-Electro-Mechanical Systems (MEMS) |

| Hemispherical Resonator Gyro (HRG) |

| Others Technologies |

| Navigation Grade |

| Tactical Grade |

| Industrial Grade |

| Commercial Grade |

| Airborne |

| Land |

| Marine |

| Space |

| Industrial Automation |

| Aerospace and Defense |

| Automotive |

| Marine |

| Oil and Gas |

| Others End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Gyroscopes | |

| Accelerometers | ||

| Magnetometers | ||

| Other Components | ||

| By Technology | Ring Laser Gyro (RLG) | |

| Fiber Optic Gyro (FOG) | ||

| Micro-Electro-Mechanical Systems (MEMS) | ||

| Hemispherical Resonator Gyro (HRG) | ||

| Others Technologies | ||

| By Grade | Navigation Grade | |

| Tactical Grade | ||

| Industrial Grade | ||

| Commercial Grade | ||

| By Platform | Airborne | |

| Land | ||

| Marine | ||

| Space | ||

| By End-User Industry | Industrial Automation | |

| Aerospace and Defense | ||

| Automotive | ||

| Marine | ||

| Oil and Gas | ||

| Others End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How rapidly is demand for inertial sensors from commercial space constellations growing?

Space applications are projected to register a 7.19% CAGR to 2030, driven by mega-constellations launching dozens of satellites per month.

Which technology is gaining share in power-constrained platforms?

Hemispherical resonator gyro units are advancing at a 6.88% CAGR as spacecraft and oilfield tools favor their low power draw.

Why are tactical-grade IMUs popular in unmanned defense systems?

They provide sub-degree accuracy adequate for multi-hour missions yet cost less than navigation-grade units, fitting expendable drones and loitering munitions budgets.

What limits the adoption of high-end IMUs in automotive programs?

High calibration and testing costs still exceed automakers’ bill-of-material targets, although new automated test infrastructure may reduce expenses over time.

Page last updated on: