Hereditary Testing Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

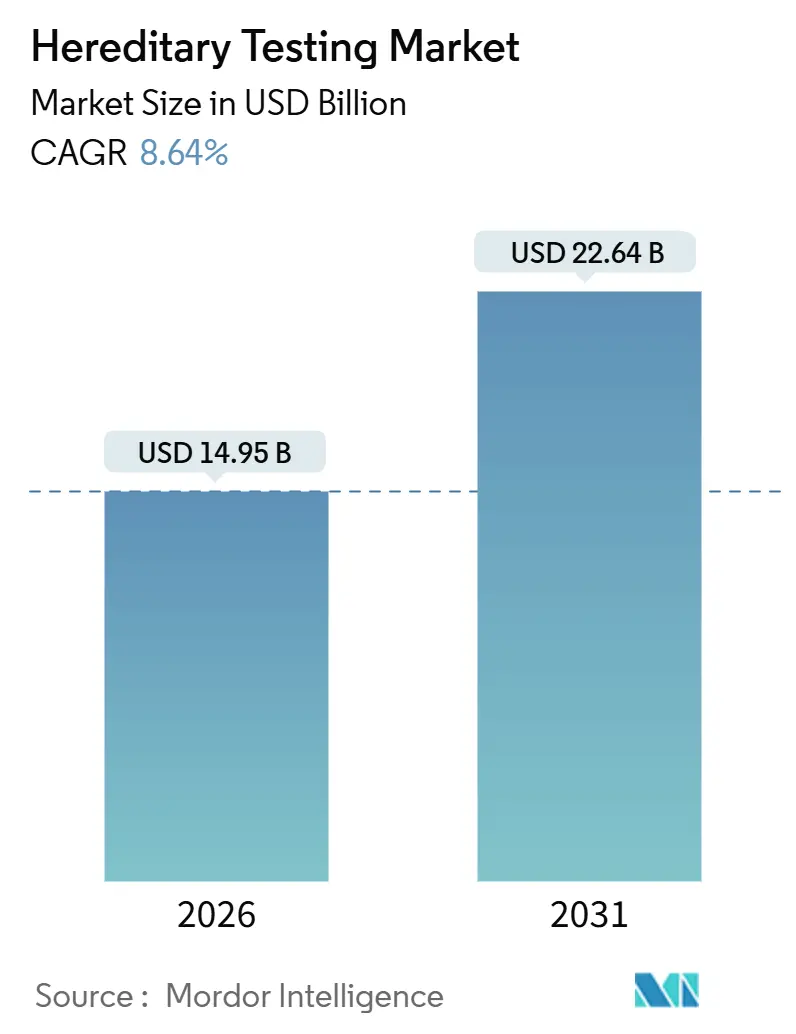

| Market Size (2026) | USD 14.95 Billion |

| Market Size (2031) | USD 22.64 Billion |

| Growth Rate (2026 - 2031) | 8.64% CAGR |

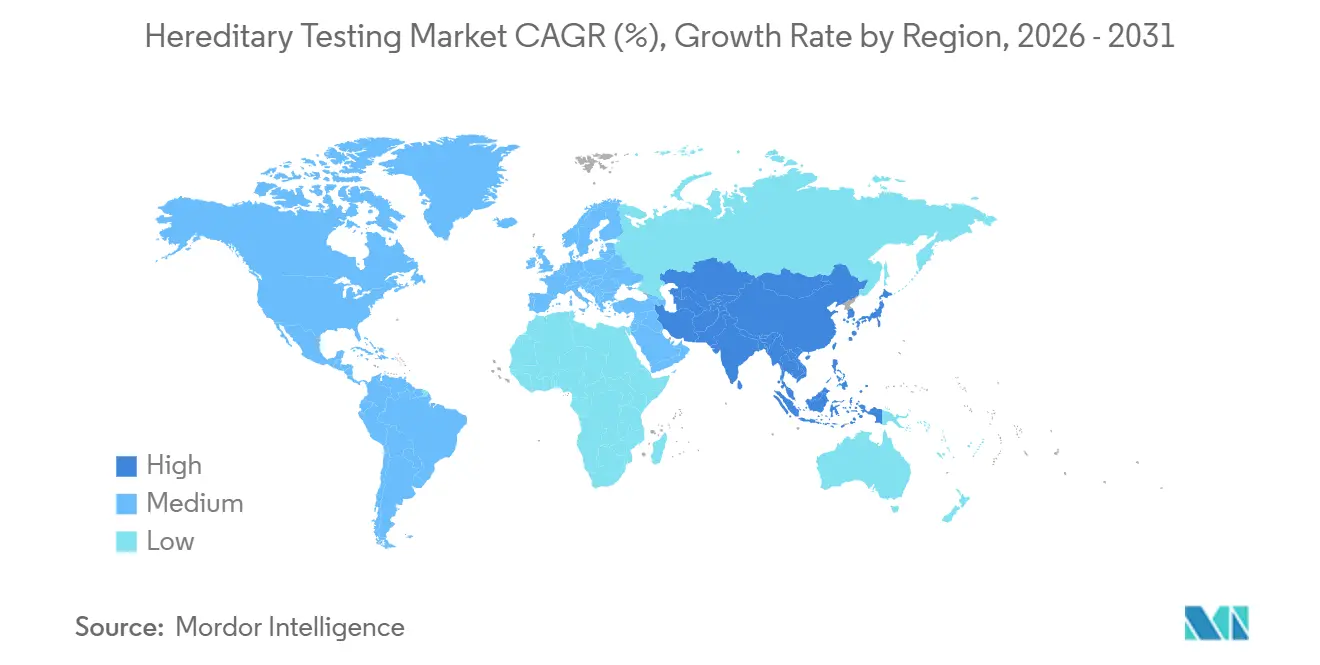

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

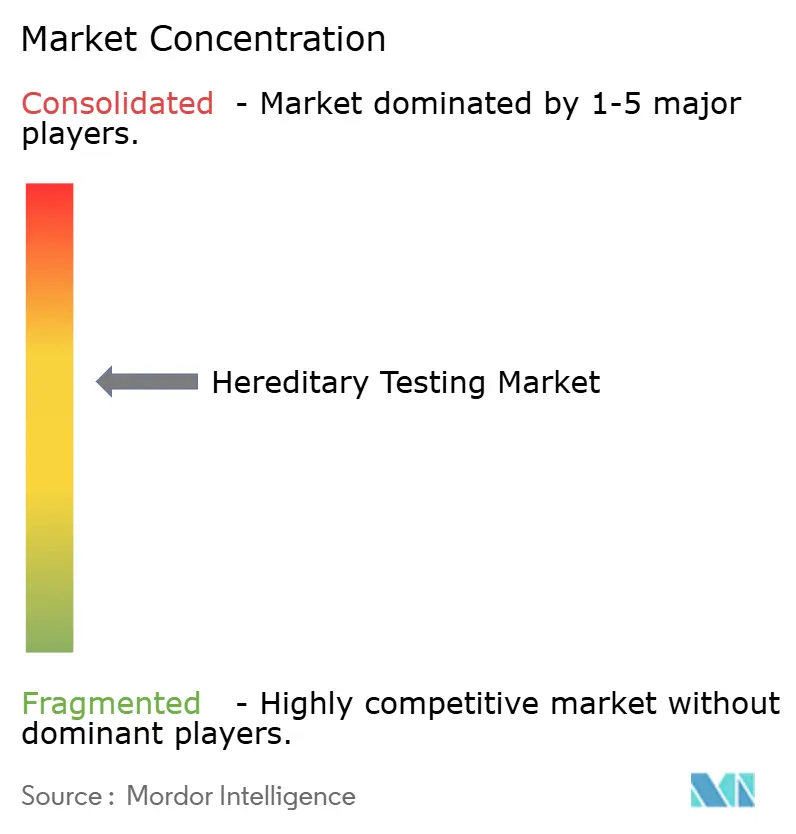

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hereditary Testing Market Analysis by Mordor Intelligence

The Hereditary Testing Market size is estimated at USD 14.95 billion in 2026, and is expected to reach USD 22.64 billion by 2031, at a CAGR of 8.64% during the forecast period (2026-2031).

This growth pattern positions the hereditary testing market at the center of a transition from episodic diagnostics to proactive genomics, where payer policy, guideline mandates, and falling sequencing costs converge to expand test volumes. Ongoing reductions in per-genome costs, broader reimbursement for multi-gene panels, and AI-enhanced variant interpretation are collectively reshaping laboratory economics. Simultaneously, the hereditary testing market is benefiting from population-scale programs that add hundreds of thousands of exomes each year, creating virtuous data cycles that feed discovery and reclassification. Competitive intensity is rising as platform vendors leverage reagent-rental contracts while service laboratories differentiate through turnaround time and counseling access, yet no single player commands more than 15% revenue, keeping the hereditary testing market strategically attractive for new entrants.

Key Report Takeaways

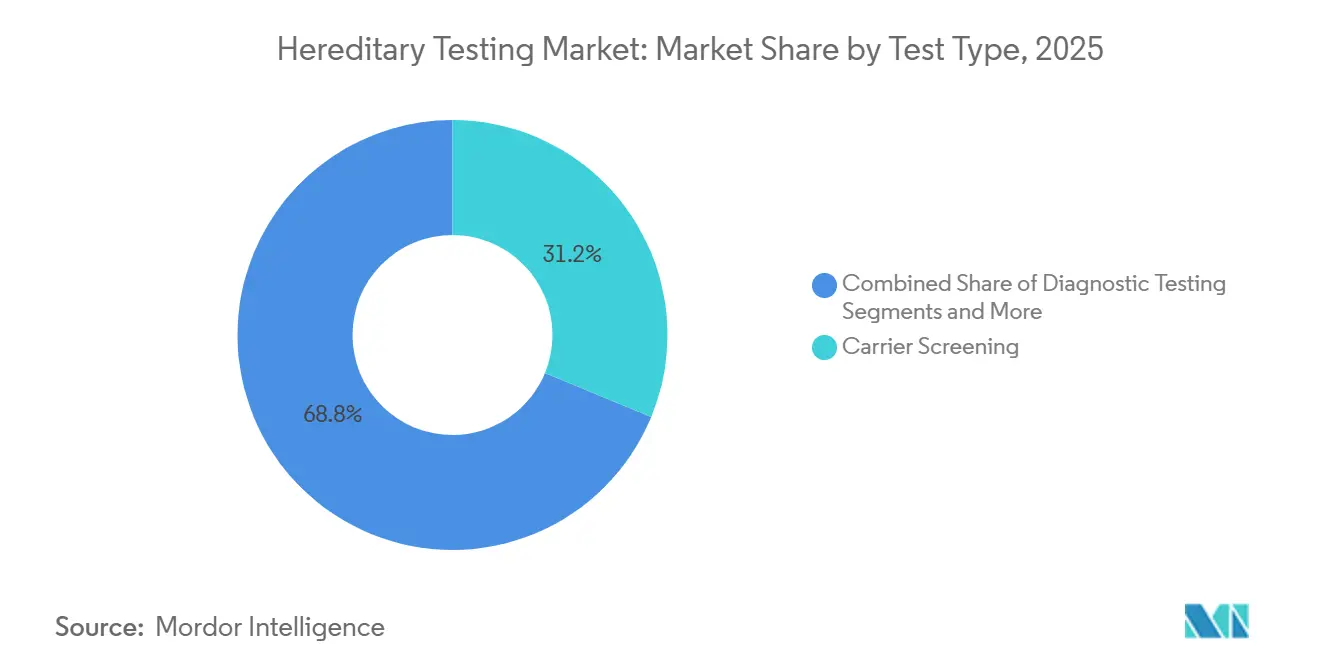

- By test type, carrier screening led with 31.22% hereditary testing market share in 2025, while pharmacogenomic testing is projected to expand at a 12.56% CAGR through 2031.

- By offering, laboratory and interpretive services accounted for 39.35% of the hereditary testing market size in 2025; software and solutions will grow the fastest at 12.78% CAGR to 2031.

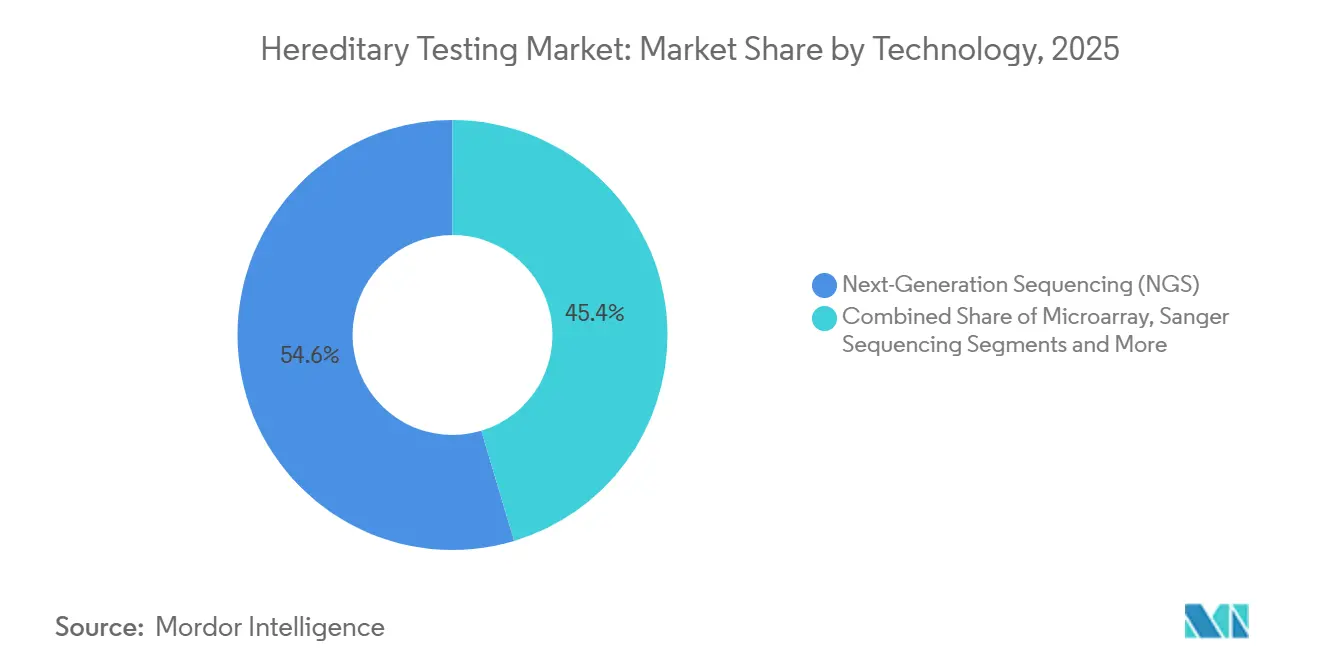

- By technology, next-generation sequencing captured 54.64% hereditary testing market share in 2025 and is advancing at an 11.45% CAGR to 2031.

- By application, oncology remained dominant with 43.25% of 2025 revenue, yet neurological testing registers the highest 10.44% CAGR through 2031.

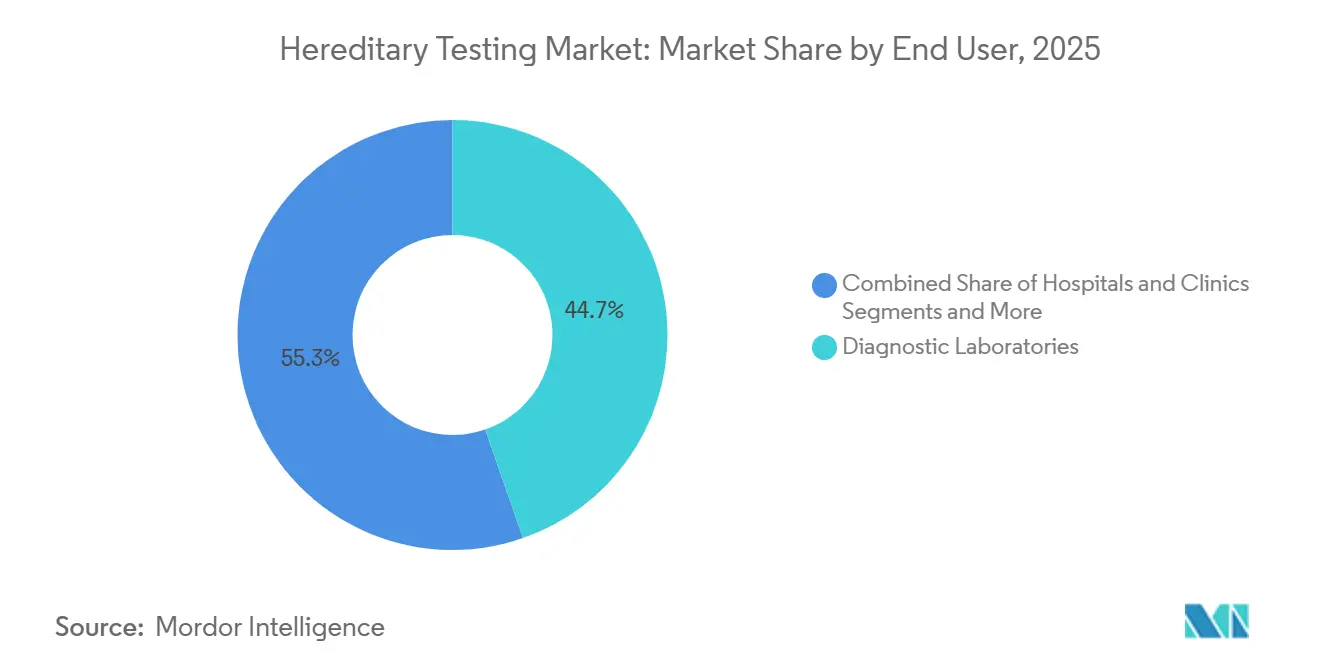

- By end user, diagnostic laboratories represented 44.68% of 2025 revenue, while academic and research institutes will post a 10.33% CAGR to 2031.

- By geography, North America held 43.25% of 2025 revenue; Asia-Pacific is forecast to grow at a 10.09% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hereditary Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Widespread Payer Adoption of Genetic-Based Preventive Care Programs | +1.8% | North America, Western Europe (early gains in Germany and United Kingdom) | Medium term (2-4 years) |

| Declining Cost-Per-Genome from NGS Chemistry and Cloud Bioinformatics | +1.5% | Global, accelerated uptake in Asia-Pacific and Middle East & Africa | Short term (≤ 2 years) |

| Integration of Hereditary Panels into Oncology Clinical Guidelines | +1.3% | North America, Europe, Australia, urban Latin America | Medium term (2-4 years) |

| Direct-To-Consumer Kits Expanding Awareness Beyond High-Risk Groups | +0.9% | North America, Western Europe, emerging Brazil and South Korea | Long term (≥ 4 years) |

| AI-Driven Variant Curation Reducing Inconclusive Rates | +1.0% | Global, early adoption in North America and Europe | Short term (≤ 2 years) |

| Employer-Funded Population Genomics Benefits | +0.7% | North America, pilots in Singapore and United Arab Emirates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Widespread Payer Adoption of Genetic-Based Preventive Care Programs

Commercial insurers in the United States covered hereditary cancer panels for 78% of eligible members by late 2025, up from 52% in 2023, after actuarial models showed USD 180,000 average lifetime savings per BRCA carrier who opts for prophylactic surgery.[1]Deborah Schrag, “Prophylactic Surgery Cost-Savings Among BRCA Carriers,” Journal of Clinical Oncology, ascopubs.org Coverage widened again in early 2026 when Medicare removed prior-authorization barriers for multi-gene hereditary cancer testing, unlocking an 8 million-member anticoagulation cohort and lifting overall hereditary testing market volumes. European reimbursement is following 18 months behind; Germany’s statutory system lowered its BRCA risk threshold to 10% in late 2025, effectively doubling the test-eligible population. Large U.S. employers are now bundling carrier, pharmacogenomic, and polygenic risk screens into annual wellness benefits adopted by 12% of Fortune 500 firms, signaling durable demand beyond specialist clinics. Collectively these actions elevate baseline utilization and anchor the hereditary testing market in mainstream preventive care.[2]Seema Verma, “Medicare Expands Coverage for Hereditary Cancer Panels,” Centers for Medicare & Medicaid Services, cms.gov

Declining Cost-Per-Genome from NGS Chemistry and Cloud Bioinformatics

Illumina’s NovaSeq X hit USD 200 per genome in early 2026, a 60% drop from the prior flagship platform, while Oxford Nanopore’s benchtop PromethION 2 Solo delivers whole genomes for under USD 300, enabling mid-tier labs to bring sequencing in-house. Cloud pipelines from Amazon and Google cut compute cost by 40% over 2024-2026 through serverless architectures, pushing all-inclusive hereditary panel pricing below the USD 1,000 threshold that most payers view as cost-effective. Thermo Fisher’s Genexus removes hand-offs between library prep and sequencing, slicing 30% labor cost. BGI’s DNBSEQ-T20 already achieves USD 165 per exome in China, aligning with national reimbursement schedules. These convergent cost drops raise margins even as average selling prices fall, sustaining investment across the hereditary testing industry.

Integration of Hereditary Panels into Oncology Clinical Guidelines

NCCN’s January 2026 update mandates germline multi-gene testing for every epithelial ovarian cancer case, irrespective of family history, expanding the U.S. eligible pool by 35%.[3]William Daly, “NCCN Widens Germline Testing for Ovarian Cancer,” National Comprehensive Cancer Network, nccn.org ASCO’s 2025 opinion requires BRCA1/2 and PALB2 testing before initiating PARP inhibitors for metastatic prostate cancer, creating a 14-day turnaround requirement that favors high-throughput labs. ESMO extended Lynch syndrome screening to colorectal cancers diagnosed before age 70. As guideline compliance links directly to therapy approvals, laboratories experience more predictable incoming volumes, strengthening the hereditary testing market’s revenue visibility.

Direct-To-Consumer Kits Expanding Awareness Beyond High-Risk Groups

23andMe added 2.3 million customers in 2025 via a USD 229 Health + Ancestry kit that reports carrier results without physician orders. Color Health subsidized hereditary panels for 450,000 employees through corporate wellness deals, while Invitae’s consumer portal contributed USD 42 million—11% of 2025 sales—demonstrating willingness to self-pay when price points remain below USD 250. Updated 2025 FDA guidance legitimized consumer pharmacogenomic tests provided results are confirmed in CLIA labs, expanding public genomic literacy that ultimately funnels patients to clinical confirmatory pipelines and enlarges the hereditary testing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Reimbursement Outside Oncology & Rare Diseases | -1.2% | Latin America, Southeast Asia, parts of Europe | Medium term (2-4 years) |

| Shortage of Certified Genetic Counselors Delaying Test Ordering | -0.8% | North America, Europe, severe gaps in Middle East & Africa | Long term (≥ 4 years) |

| Data-Privacy Legislation Classifying Genomics as High-Risk | -0.6% | Europe, spillover to Canada and Australia | Short term (≤ 2 years) |

| Patent Thickets around Multi-Gene Panels Hindering Entrants | -0.5% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Reimbursement Outside Oncology & Rare Diseases

Medicare and most U.S. payers still restrict hereditary cardiovascular panels to patients with documented family history, excluding 60% of familial hypercholesterolemia cases that present asymptomatically. European insurers have yet to cover pharmacogenomic testing for antidepressants despite 30% fewer therapy failures in randomized studies. Latin American public systems reimburse fewer than 10 hereditary tests, pushing multi-gene panel costs above median monthly income. These gaps confine the hereditary testing market to niche indications and delay broader chronic-disease integration.

Shortage of Certified Genetic Counselors Delaying Test Ordering

Only 5,800 board-certified counselors served the entire United States in mid-2025, growing at 6% a year while test volumes rise 15%. Germany and France combined employ under 400 counselors, leading to 8-12-week waits that discourage physician orders. Tele-counseling platforms increased capacity by one-third in 2025, yet state licensure and cross-border rules fragment supply, capping hereditary testing market velocity even when reimbursement exists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Pharmacogenomics Outpaces Reproductive Screening

Carrier screening held 31.22% revenue in 2025 as expanded panels reached broader ancestries, while pharmacogenomic testing is set to grow at 12.56% CAGR to 2031. Pharmacogenomics benefits from 28 new CPIC guidelines and FDA label mandates on seven oncology drugs, turning optional tests into therapy prerequisites. Diagnostic testing captured 28% of 2025 revenue, anchored in rare metabolic and neurological disorders yielding >35% diagnoses via exome sequencing. Predictive testing inching into neurodegeneration as disease-modifying trials begin. Prenatal and newborn programs accounted for 18%, buoyed by non-invasive screening that detects microdeletions down to 7 Mb with 99% sensitivity. The pharmacogenomic panels are projected to grow at 12.56% CAGR, underscoring the shift from one-time risk assessment to lifetime therapy guidance. Carrier screening faces headwinds from declining fertility rates, yet remains essential in premarital programs across the Middle East.

The pharmacogenomics trajectory is reinforced by Vanderbilt’s PREDICT program, which pre-emptively genotypes surgical patients and prevented 340 adverse drug events in 2025, highlighting clinical value beyond oncology. The VA’s Million Veteran Program will genotype 950,000 participants, adding racial diversity to gene–drug databases and accelerating variant validation for the hereditary testing market. Meanwhile, falling birth rates constrain carrier volumes in high-income countries, and diagnostic exome yields plateau after first-pass testing, shifting growth momentum squarely toward pharmacogenomics.

By Offering: Software Gains as Interpretation Becomes the Bottleneck

Laboratory and interpretive services generated 39.35% of 2025 revenue, but software and solutions are slated for a 12.78% CAGR through 2031 as AI platform adoption quickens. Test kits and consumables remained a stable 32% share, with Roche’s KAPA HyperPlus gaining 18% of that subcategory by enabling low-input cfDNA workflows. Sequencing instruments have a capital cycle average of six years, pushing vendors toward reagent-rental deals that lock in recurring income. The software solutions are expected to grow as labs integrate automated curation directly into electronic health records. Qiagen’s QCI Interpret grew its install base to 240 labs in 2025 and slashed counselor review time by 40%, evidencing demand for interpretive efficiency.

Interpretation, not sequencing, now dictates turnaround. NovaSeq X and PromethION commoditize raw data, so differentiation shifts to variant calling accuracy and report readability, prompting labs to license cloud software rather than expand wet-lab capacity. Instruments face lumpy sales; hence vendors bundle them with consumables or analysis licenses to smooth revenue. Meanwhile, open-source library-prep protocols pressure reagent prices, making software and counseling services the hereditary testing industry’s new profit pools.

By Technology: NGS Dominates but Faces Niche Competition

Next-generation sequencing accounted for 54.64% of 2025 technology revenue and will post an 11.45% CAGR to 2031, underpinned by advances in chemistry that eliminate most confirmatory Sanger runs. PCR has small share for single-gene and pharmacogenomics assays needing less than 24-hour results. Microarrays for developmental delay evaluations, though prenatal use is waning as NIPT expands. Sanger sequencing’s is niche is tied to regulatory filings and confirmation of difficult regions. Long-read platforms from Oxford Nanopore and PacBio are gaining in structural variant analysis for conditions like Fragile X syndrome, yet remain capacity-constrained for routine panels.

NGS error rates in homopolymer regions fell an order of magnitude in 2025, enabling labs to drop Sanger confirmation in most contexts and shortening reports by two days. PCR’s edge in speed supports inpatient pharmacogenomics, Spartan Cube returns CYP2C19 genotypes in 60 minutes, while microarrays risk obsolescence if whole-genome sequencing achieves reimbursement. Hybrid workflows that pair NGS discovery with PCR confirmation optimize cost and accuracy, and their adoption supports continued double-digit growth for the hereditary testing market.

By Application: Neurological Testing Emerges from Oncology’s Shadow

Oncology accounted for 43.25% of 2025 revenue, yet neurological panels will expand 10.44% CAGR through 2031 as pharmacogenomics for epilepsy and psychiatry gains reimbursement. Cardiovascular panels captured 18% but face clinical-diagnosis substitutes; metabolic disorders held 12% driven by newborn screening. Polygenic risk scores for Alzheimer’s disease, validated in 2025 to quintuple dementia risk among top-decile profiles, could unlock preventive testing demand once disease-modifying drugs prove effective. Oncology growth is shifting from germline-only tests to integrated tumor–normal sequencing, increasing sample complexity and raising software demand. Neurological advances, such as Invitae’s 170-gene epilepsy panel demonstrating 25% diagnostic yield, underscore new use cases nudging the hereditary testing market into chronic-disease management spheres.

By End User: Academic Institutes Drive Innovation Cycles

Diagnostic laboratories held 44.68% of 2025 revenue due to payer contracts and throughput scale, but academic and research institutes will chart a 10.33% CAGR by 2031 as they power population-genomics cohorts like all of US and UK Biobank. Hospitals and clinics remain 30% share, with capital constraints pushing most community hospitals to send out hereditary panels. Academic centers act as technology test beds, Broad Institute adopted PacBio Revio for autism structural variant studies in 2025, then commercial labs translate findings into higher-yield clinical panels 18 months later. This symbiosis ensures continuous sample flow, reinforcing the hereditary testing market’s innovation pipeline.

Geography Analysis

North America retained 43.25% of 2025 revenue, buoyed by broad insurance coverage and a mature counseling workforce. Europe's reimbursement heterogeneity prompted cross-border testing to Germany and Austria. Asia-Pacific is projected to grow 10.09% CAGR to 2031, led by China’s mandate to screen 29 disorders in all newborns from January 2026, equating to 10 million annual births. India’s MedGenome expansion into tier-2 cities and Japan’s reimbursement for CYP2C19 genotyping illustrate regional momentum. The hereditary testing market size in Asia-Pacific is expected to overtake Europe by 2030 as population-scale programs capitalize on falling per-genome costs.

The Middle East & Africa are concentrated in the Gulf premarital screening. South America’s is tempered by currency volatility; Brazil’s 12% real depreciation in 2025 raised reagent costs, slowing uptake. As South Korea permits direct-to-consumer wellness genetic tests and Dubai funds national genome sequencing, regional tailwinds diversify the hereditary testing industry’s revenue base. However, counselor shortages and patchwork reimbursement remain universal constraints.

Competitive Landscape

The hereditary testing market remains moderately fragmented. Illumina’s reagent-rental model secures 52% of installed NovaSeq systems, generating annuity-like consumable revenue. Thermo Fisher’s vertical workflow sells instruments, reagents, and cloud informatics as a bundle appealing to hospital labs seeking in-house control. Roche leverages Foundation Medicine to integrate germline-somatic oncology testing, cementing hospital relationships. Natera and Invitae compete on patient experience through online portals and bundled counseling.

Disruptors intensify rivalry: Oxford Nanopore’s portable MinION sequencer opens resource-limited markets, Element Biosciences reduces reagent costs by 30%, and Blueprint Genetics delivers subspecialty panels with 40%-plus diagnostic yields. Consolidation is continuing; Eurofins acquired three European genetics labs in 2025, and LabCorp integrated Invitae assets post-restructuring in 2024. Patent litigation shapes strategy—cross-licensing deals include geographic non-competes, and EPO’s revocation of Illumina’s cluster patent widens European sequencing options.

Barriers lie in accreditation; CAP, CLIA, and ISO 15189 compliance demand robust quality systems few startups can afford. As algorithms gain regulatory recognition, competitive moats shift from hardware toward interpretive software and proprietary variant databases, reinforcing the hereditary testing market’s bifurcation into platform and service value chains

Hereditary Testing Industry Leaders

Illumina, Inc.

Myriad Genetics, Inc.

Thermo Fisher Scientific Inc.

Natera, Inc.

F. Hoffmann-La Roche Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Oxford Nanopore Technologies launched a 258-gene Hereditary Cancer Panel to expand inherited cancer risk testing.

- May 2025: Guardant Health introduced the Guardant Hereditary Cancer test, adding germline risk profiling to its portfolio.

- February 2025: Foundation Medicine announced FoundationOne Germline and FoundationOne Germline More through a partnership with Fulgent Genetics for hereditary cancer screening.

Global Hereditary Testing Market Report Scope

Heredity testing is the medical analysis of DNA, chromosomes, or proteins to detect mutations that can cause or increase the risk of genetic conditions or diseases such as cancer, or to determine the likelihood of passing a disorder to offspring. This process guides medical decisions, treatment, and family planning by identifying inherited patterns through the examination of genetic material from samples like blood or saliva.

The Hereditary Testing Market Report is Segmented by Test Type, Offering, Technology, Application, End User and Geography. By Test Type, the market is segmented into Diagnostic Testing, Predictive & Presymptomatic Testing, Carrier Screening, Prenatal & Newborn Testing, and Pharmacogenomic Testing. By Offering, the market is segmented into Test Kits & Consumables, Instruments/Sequencing Platforms, Laboratory & Interpretive Services, and Software & Solutions. By Technology, the market is segmented into NGS, PCR-based, Microarray, and Sanger. By Application, the market is segmented into Oncology, Cardiovascular, Neurological, Metabolic, and Others. By End User, the market is segmented into Hospitals & Clinics, Diagnostic Laboratories, Academic & Research Institutes, Others. By Geography, the market is segmented into North America, Europe, Asia-Pacific, MEA, South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Diagnostic Testing |

| Predictive & Presymptomatic Testing |

| Carrier Screening |

| Prenatal & Newborn Testing |

| Pharmacogenomic Testing |

| Test Kits & Consumables |

| Instruments / Sequencing Platforms |

| Laboratory & Interpretive Services |

| Software & Solutions |

| Next-Generation Sequencing (NGS) |

| PCR-based Testing |

| Microarray |

| Sanger Sequencing |

| Oncology |

| Cardiovascular Disorders |

| Neurological Disorders |

| Metabolic Disorders |

| Others |

| Hospitals & Clinics |

| Diagnostic Laboratories |

| Academic & Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Test Type | Diagnostic Testing | |

| Predictive & Presymptomatic Testing | ||

| Carrier Screening | ||

| Prenatal & Newborn Testing | ||

| Pharmacogenomic Testing | ||

| By Offering | Test Kits & Consumables | |

| Instruments / Sequencing Platforms | ||

| Laboratory & Interpretive Services | ||

| Software & Solutions | ||

| By Technology | Next-Generation Sequencing (NGS) | |

| PCR-based Testing | ||

| Microarray | ||

| Sanger Sequencing | ||

| By Application | Oncology | |

| Cardiovascular Disorders | ||

| Neurological Disorders | ||

| Metabolic Disorders | ||

| Others | ||

| By End User | Hospitals & Clinics | |

| Diagnostic Laboratories | ||

| Academic & Research Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the hereditary testing market and its expected growth to 2031?

The market is valued at USD 14.95 billion in 2026 and is projected to reach USD 22.64 billion by 2031, reflecting an 8.64% CAGR.

Which test type is growing the fastest within hereditary testing?

Pharmacogenomic panels are growing the fastest, registering a 12.56% CAGR through 2031 as payer coverage and FDA label mandates expand.

How much of 2025 revenue did next-generation sequencing generate?

Next-generation sequencing contributed 54.64% of 2025 revenue, making it the dominant technology platform.

Why is Asia-Pacific a high-growth region for hereditary testing?

China’s mandate to screen 29 newborn disorders, India’s expanding private diagnostics sector, and Japan’s reimbursement for pharmacogenomics together drive a 10.09% CAGR forecast.

Which companies currently lead instrument and reagent sales?

Illumina, Thermo Fisher Scientific, and Roche are the primary platform vendors, with Illumina’s reagent-rental contracts securing recurring consumable revenue.

What is limiting test uptake outside oncology?

Limited reimbursement, counselor shortages, and privacy regulations are key constraints suppressing demand in cardiovascular, psychiatric, and metabolic applications.

Page last updated on: