HER2 Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

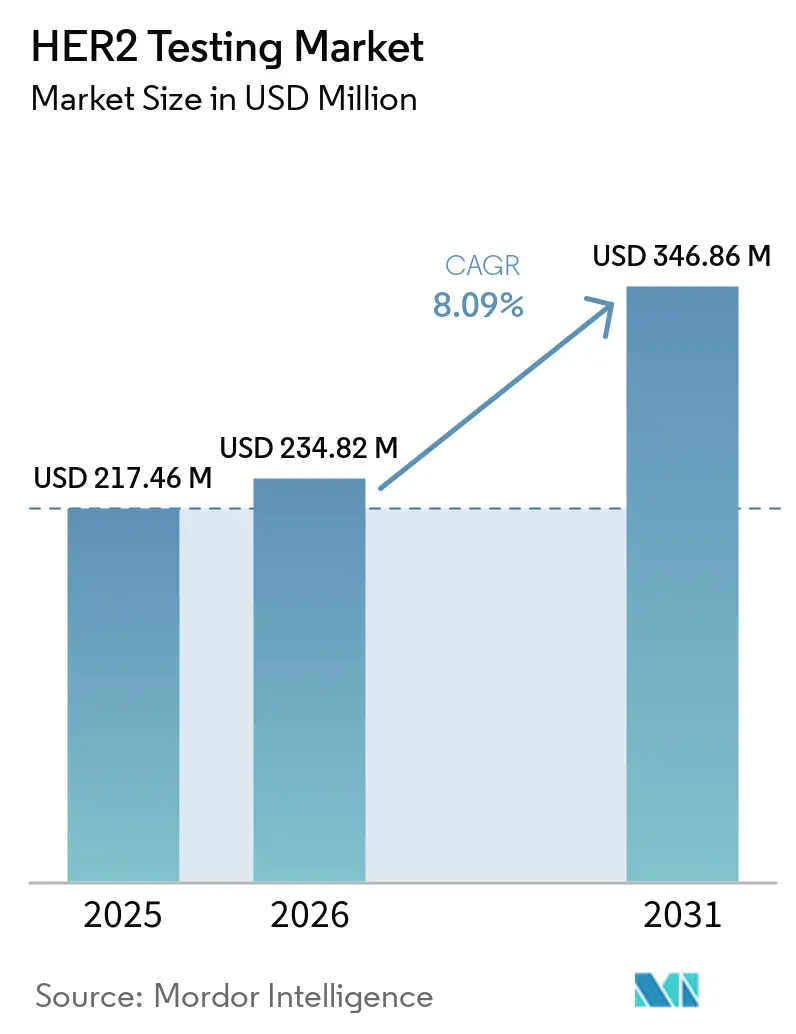

| Market Size (2026) | USD 234.82 Million |

| Market Size (2031) | USD 346.86 Million |

| Growth Rate (2026 - 2031) | 8.09% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HER2 Testing Market Analysis by Mordor Intelligence

The HER2 Testing Market size was valued at USD 217.46 million in 2025 and is estimated to grow from USD 234.82 million in 2026 to reach USD 346.86 million by 2031, at a CAGR of 8.09% during the forecast period (2026-2031).

Growth is being lifted by therapeutic approvals that recognize HER2-low and HER2-ultralow tumors, compelling laboratories to refine scoring protocols and invest in digital image analysis that can resolve subtle membrane-staining differences. Regulatory bodies in the United States, the European Union, and Japan now tie reimbursement for antibody-drug conjugates to accurate stratification across the full HER2 spectrum, which widens the eligible testing pool and raises per-patient test volumes. Vendors are responding with automated immunohistochemistry (IHC) stainers, cloud-based slide viewers, and AI algorithms that accelerate turnaround while reducing inter-observer variability. At the same time, comprehensive genomic profiling panels that embed ERBB2 copy-number and mutation calls are capturing share as oncologists prefer single-assay work-ups that guide therapy selection for multiple biomarkers.

Key Report Takeaways

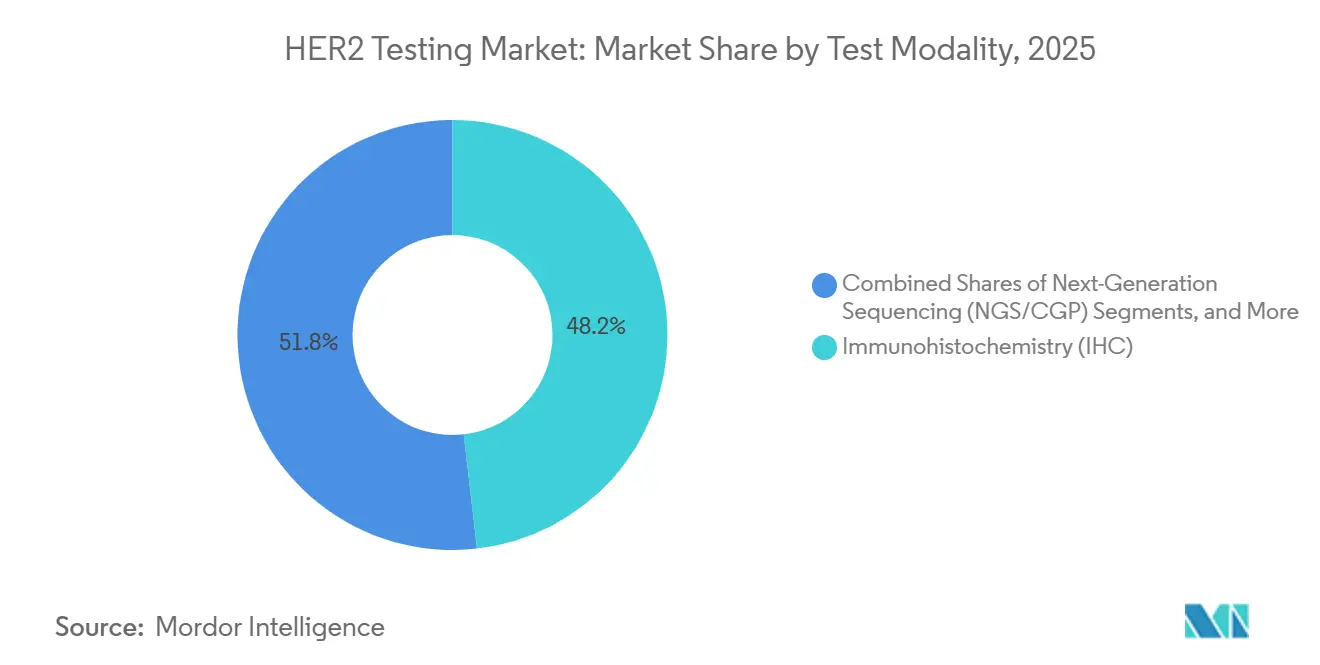

- By test modality, immunohistochemistry led with 48.19% of the HER2 testing market share in 2025, while next-generation sequencing is projected to post the fastest CAGR at 9.56% to 2031.

- By sample type, FFPE tissue accounted for 85.19% share of the HER2 testing market size in 2025 and liquid biopsy is on track to expand at 10.56% CAGR through 2031.

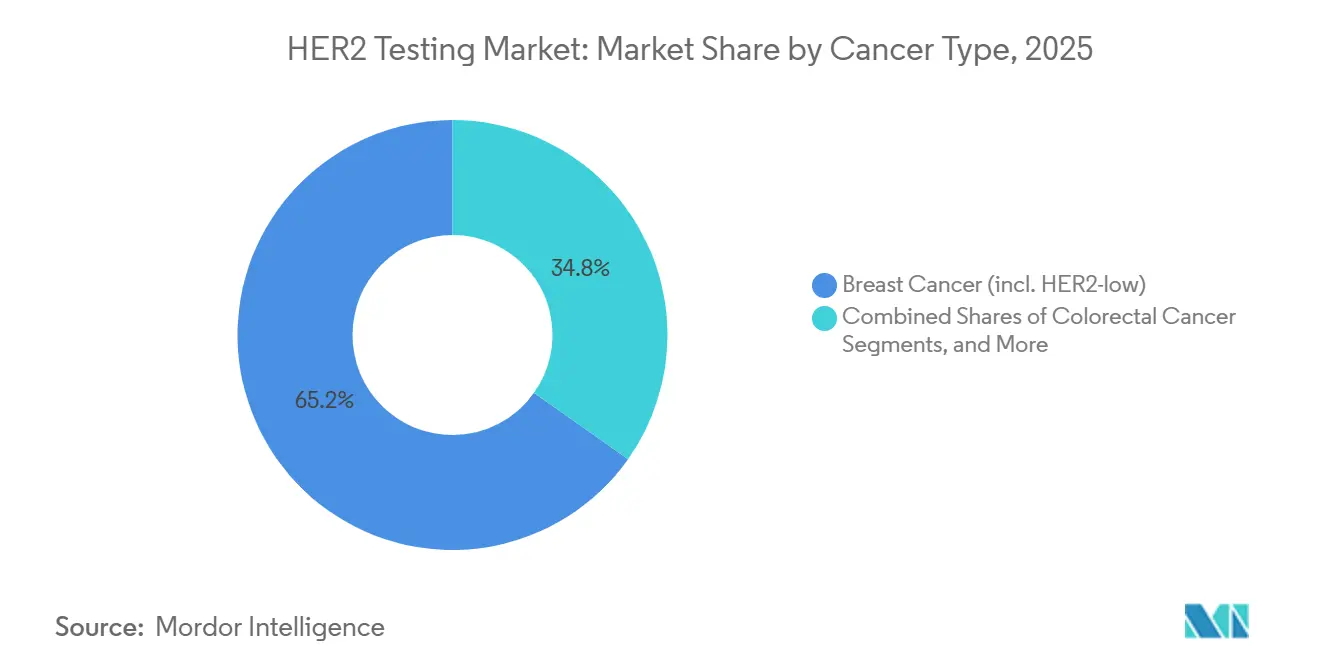

- By cancer type, breast cancer testing contributed 65.19% of 2025 revenue in the HER2 testing market and colorectal cancer is forecast to climb at a 10.32% CAGR to 2031.

- By end user, hospital pathology labs held 47.18% of 2025 revenue, whereas independent reference labs are projected to grow at 9.97% through 2031.

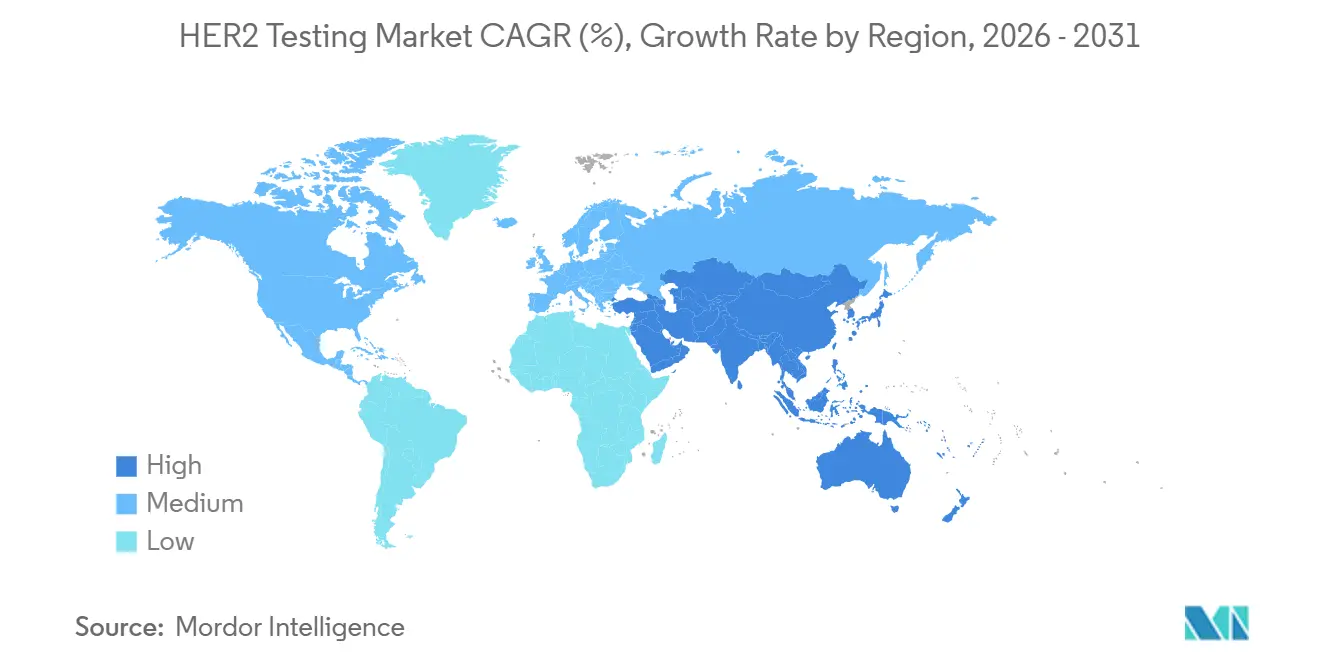

- By geography, North America generated 43.12% of 2025 revenue in the HER2 testing market, yet Asia-Pacific is anticipated to register the quickest regional CAGR of 10.43% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HER2 Testing Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| HER2-low eligibility expands tested population | 2.1% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Tumor-agnostic HER2-positive approvals widen testing across tumor types | 1.8% | Global, APAC acceleration post-2026 | Long term (≥ 4 years) |

| Guideline-mandated testing in breast and gastric/GEJ cancers | 1.3% | Global | Short term (≤ 2 years) |

| Hospital and lab infrastructure upgrades, automation | 1.0% | North America, EU, APAC core | Medium term (2-4 years) |

| Digital pathology and AI adoption improve HER2 scoring throughput | 1.2% | North America, EU, APAC urban centers | Medium term (2-4 years) |

| Liquid biopsy and CGP panels broaden access to ERBB2 assessment | 0.7% | North America, EU, spill-over to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

HER2-Low Eligibility Expands Tested Population

In January 2025, the FDA approved Roche’s PATHWAY HER2 (4B5) rabbit monoclonal antibody, enabling the identification of HER2-ultralow expression.[1]Roche, “PATHWAY HER2 (4B5) Assay Cleared for Ultralow Detection,” roche.com This significant development expanded the eligibility for trastuzumab deruxtecan to patients previously classified as HER2-negative. Laboratories are now required to differentiate between IHC 0 and 1+, a process that increases slide volumes and drives demand for external proficiency programs. Studies in 2024 revealed only 60–75% agreement among pathologists in HER2-low scoring, prompting the adoption of whole-slide imaging and AI to standardize readings. The rise in retest rates has led to higher reagent consumption and more frequent quality-control runs, contributing to the steady growth of the HER2 testing market.

Tumor-Agnostic HER2-Positive Approvals Widen Testing Across Tumor Types

In March 2026, Japan granted a tumor-agnostic authorization for trastuzumab deruxtecan, requiring pathologists to evaluate HER2 levels across nearly all solid tumors.[2]Caris Life Sciences, “Pan-Tumor HER2 IHC Study,” carislifesciences.com This decision mirrored an FDA tissue-agnostic approval in April 2024, which prompted U.S. oncology centers to incorporate HER2 immunostaining into protocols for colorectal, lung, biliary, and pancreatic cancers. A July 2025 analysis of 65,000 tumors identified actionable HER2 positivity in nearly 10% of bladder and endometrial cancers, highlighting untapped sample volumes.[3]American Society of Clinical Oncology, “HER2 Testing Guidelines Update,” ascopubs.org This expanded testing requirement has driven significant revenue growth for independent reference laboratories, particularly those bundling HER2 with KRAS, BRAF, and MSI markers in comprehensive panels, further strengthening the HER2 testing market.

Guideline-Mandated Testing in Breast and Gastric/GEJ Cancers

The 2024 ASCO/CAP update mandates reflex in situ hybridization for ambiguous IHC 2+ breast tumors and recommends clear reporting of HER2-low status. Gastric cancer guidelines align with this approach, establishing HER2 as a standard treatment for metastatic cases. These directives stabilize baseline testing volumes and justify investments in automated stainers, which, as demonstrated in a 2024 pilot study, can reduce hands-on time by 30–40%. Predictable testing throughput enables laboratories to negotiate favorable reagent volume discounts, a cost-saving measure that supports margin expansion within the HER2 testing market.

Hospital and Lab Infrastructure Upgrades, Automation

To address rising daily case volumes, academic centers and major reference labs are deploying high-capacity IHC robots and FISH processors. In 2025, a validated digital pathology workflow reduced HER2 IHC turnaround times from 48 to 24 hours, enabling same-day treatment planning. Middleware solutions that track fixation times and reagent batches are improving compliance with ISO 15189 standards, an accreditation increasingly required by payers. These operational efficiencies allow facilities to adopt competitive pricing strategies without compromising profitability, expanding access to testing and strengthening the HER2 testing market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Low-end (0 Vs 1+) IHC reproducibility challenges | -0.9% | Global, acute in emerging markets | Short term (≤ 2 years) |

| IHC–ISH discordance and pre-analytical variability | -0.7% | Global | Medium term (2-4 years) |

| Skilled personnel and QC burden for consistent HER2 reads | -0.5% | APAC, MEA, Latin America | Medium term (2-4 years) |

| Limited Validation of Ctdna for HER2-low/ultralow | -0.4% | Global, constrains liquid biopsy adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low-End (0 vs 1+) IHC Reproducibility Challenges

Subtle membrane-staining differences between IHC 0 and 1+ result in variable readings, potentially withholding therapy from eligible patients. A 2024 survey in Sweden indicated that only half of laboratories met proficiency benchmarks on low-expression samples. Variation arises from factors such as cold ischemia, under-fixation, and antibody selection, driving the demand for external quality assessment programs and digital image analysis. These ongoing inconsistencies reduce physician confidence and limit the growth of the HER2 testing market, particularly in resource-constrained regions.

IHC–ISH Discordance and Pre-Analytical Variability

Mismatch between IHC and in situ hybridization occurs when pre-analytical conditions degrade antigenicity or DNA integrity. In 2024, cold ischemia lasting over one hour was identified as a key factor contributing to false negatives. Middleware systems that connect operating-room timestamps to laboratory information systems can alert staff to suboptimal fixation, but adoption remains inconsistent, especially in community hospitals. This variability necessitates reflex testing, which increases costs and delays diagnosis, thereby restricting efficiency improvements in the HER2 testing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Modality: IHC Anchors Workflow, NGS Gains Share

Guidelines favoring protein visualization on tissue helped immunohistochemistry secure 48.19% of the HER2 testing market's 2025 revenue. Next-generation sequencing, projected to grow at an annual rate of 9.56% through 2031, is being integrated into laboratories' comprehensive panels for ERBB2 copy-number and mutation analysis. The market for NGS-based HER2 testing is set to rise alongside companion-diagnostic labels for zanidatamab and zongertinib. While in situ hybridization is the go-to confirmatory method for ambiguous IHC 2+ cases, its share is declining as AI-enhanced IHC improves first-pass accuracy.

By Sample Type: Tissue Dominates, Liquid Biopsy Accelerates

FFPE tissue accounted for a dominant 85.19% of the HER2 testing market's 2025 volume, thanks to its longstanding role in histopathology. Tissue, being the gold standard for protein and gene assessment, enjoys robust reimbursement support. While the market size for liquid biopsy in HER2 testing is smaller, it is on a rapid ascent, projected to grow at a 10.56% CAGR through 2031. Plasma-based assays are proving invaluable for inaccessible metastatic lesions and enable serial monitoring without the need for new biopsies.

By Cancer Type: Breast Anchors Demand, Colorectal Surges

Guidelines dictate HER2 assessments for breast cancer from diagnosis to recurrence, leading to breast cancer accounting for 65.19% of the HER2 testing market's 2025 revenue. With trastuzumab deruxtecan's label expansion into the HER2-low category, patients are seeing an uptick in slide counts. Following U.S. approvals of zanidatamab and trastuzumab deruxtecan for ERBB2-amplified metastatic colorectal disease, colorectal cancer is set to experience a 10.32% CAGR growth through 2031. Despite its 3–5% prevalence, the large absolute incidence translates to significant sample numbers.

By End User: Hospital Labs Lead, Reference Labs Gain Velocity

In 2025, hospital and academic pathology departments secured 47.18% of the HER2 testing market's revenue, thanks to their ability to deliver same-day results to multidisciplinary teams. Strong government reimbursement for in-house IHC tests bolsters capital investments in automated stainers. Independent reference laboratories are on track for a 9.97% growth through 2031, capitalizing on consolidating send-out testing from community hospitals that lack digital pathology capabilities.

In March 2025, NeoGenomics bolstered its national network by acquiring Pathline, enhancing AI-assisted HER2 readings. LabCorp, in May 2025, broadened its offerings to include HER2-ultralow categorization, catering to oncologists seeking precise biomarker resolutions. With their scale, reference labs can negotiate better reagent discounts and establish nationwide logistics, amplifying their margins and solidifying their position in the HER2 testing market.

Geography Analysis

In 2025, North America accounted for 43.12% of the HER2 testing market revenue, driven by extensive insurance coverage and rapid adoption of digital pathology. The U.S. benefits from a consistent pipeline of FDA companion-diagnostic approvals, integrating HER2 assessments into treatment pathways. Meanwhile, Canada's adherence to U.S. guidelines, supported by its publicly funded healthcare system, ensures stable testing volumes.

Asia-Pacific is projected to achieve a 10.43% CAGR through 2031, as regulators in China and Japan expand indications for trastuzumab deruxtecan. China's approval in March 2026 for neoadjuvant breast cancer advances HER2 testing to earlier disease stages, increasing the number of slides required per patient. In 2024, Tata Memorial Centre in India implemented a hub-and-spoke digital pathology model, enabling regional hospitals to access centralized expert readings. South Korea's K-MASTER platform incorporates HER2 testing into a national precision medicine initiative, ensuring reimbursement and promoting standardization.

Europe, guided by consistent ESMO guidelines and ISO quality standards, faces price variability due to differing reimbursement policies, which slows the adoption of premium NGS panels. Germany, France, and the U.K. lead in volume, supported by Roche's CE-marked navify image analysis, which accelerates turnaround times. While Latin America and the Middle East encounter infrastructure challenges, strategic investments in Turkey, Saudi Arabia, and Brazil are establishing new laboratories and expanding the HER2 testing market's reach.

Competitive Landscape

The HER2 testing market sees dominance from F. Hoffmann-La Roche AG, Danaher Corporation, Agilent Technologies Inc., Abbott Laboratories, Illumina Inc., particularly in IHC and ISH platforms with multiple FDA companion-diagnostic claims. Roche's PATHWAY HER2 (4B5) antibody, cleared in 2025 for HER2-ultralow detection, strengthens Roche's leading position and integrates users into its staining ecosystem. Meanwhile, Agilent and Danaher leverage their extensive autostainer installations, making it financially challenging for laboratories to switch vendors.

Disruptors like Illumina, Guardant Health, Tempus, and Foundation Medicine are embedding ERBB2 analysis into comprehensive genomic panels. This approach challenges the traditional single-marker model and appeals to oncologists seeking consolidated reporting. Guardant focuses on longitudinal monitoring through its liquid biopsy, while Illumina positions its TruSight Oncology 500 assay for universal tissue approvals. Additionally, AI companies such as PathAI, Ibex, and Visiopharm provide algorithms compatible with various hardware vendors, introducing a competitive edge centered on software innovation.

Reference laboratories are consolidating to secure national contracts. For example, NeoGenomics, in February 2026, launched PanTracer Pro, a liquid biopsy designed for early detection, marking its expansion into screening populations. While pricing remains competitive, it is moderated by the high costs of accreditation and the stringent requirements of companion-diagnostic compliance. However, as companies compete for the next HER2-associated therapy label, the pace of innovation is accelerating, ensuring intense competition in the HER2 testing market.

HER2 Testing Industry Leaders

F. Hoffmann-La Roche AG

Danaher Corporation

Agilent Technologies Inc.

Abbott Laboratories

Illumina Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: NeoGenomics unveiled PanTracer Pro, a multi-cancer liquid-biopsy panel that includes HER2 analysis within an early-detection workflow.

- December 2025: Roche secured CE mark for navify Digital Pathology HER2 (4B5) image analysis, enabling automated IHC scoring across European laboratories.

- August 2025: The FDA approved zongertinib (Hernexeos) for HER2-mutant non-small cell lung cancer, adding mutation analysis to routine reflex NGS workflows.

Global HER2 Testing Market Report Scope

As per the scope of the report, HER2 testing is a laboratory procedure that measures the amount of human epidermal growth factor receptor 2 (HER2) protein or gene copies in cancer cells, typically from breast, stomach, or esophageal tumor tissue. It identifies "HER2-positive" cancers that grow rapidly but respond to targeted therapy. Also known as the HER2/neu test or c-erbB-2 test, it is crucial for guiding cancer treatment decisions.

The HER2 testing market is segmented by test modality, sample type, cancer type/application, end-user, and geography. By test modality, the market includes immunohistochemistry (IHC), in situ hybridization (FISH, CISH, SISH), PCR/dPCR, and next-generation sequencing (NGS/CGP). By sample type, the market is segmented into tissue/FFPE biopsy and liquid biopsy (plasma ctDNA). By cancer type/application, the market is categorized into breast cancer (including HER2-low), gastric & gastroesophageal junction adenocarcinoma, non-small cell lung cancer (HER2-altered), colorectal cancer (HER2-amplified subset), and biliary tract & pancreatic cancers (HER2-positive subset). By end-user, the market includes hospitals & academic pathology laboratories, independent reference & central laboratories, and research institutes & CROs (including clinical trials and translational research). By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Immunohistochemistry (IHC) |

| In Situ Hybridization (FISH, CISH, SISH) |

| PCR/dPCR |

| Next-Generation Sequencing (NGS/CGP) |

| Tissue/FFPE Biopsy |

| Liquid Biopsy (Plasma ctDNA) |

| Breast Cancer (incl. HER2-low) |

| Gastric & Gastroesophageal Junction Adenocarcinoma |

| Non-Small Cell Lung Cancer (HER2-altered) |

| Colorectal Cancer (HER2-amplified subset) |

| Biliary Tract & Pancreatic Cancers (HER2-positive subset) |

| Hospital & Academic Pathology Laboratories |

| Independent Reference/Central Laboratories |

| Research Institutes & CROs (clinical trials, translational) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Test Modality | Immunohistochemistry (IHC) | |

| In Situ Hybridization (FISH, CISH, SISH) | ||

| PCR/dPCR | ||

| Next-Generation Sequencing (NGS/CGP) | ||

| By Sample Type | Tissue/FFPE Biopsy | |

| Liquid Biopsy (Plasma ctDNA) | ||

| By Cancer Type / Application | Breast Cancer (incl. HER2-low) | |

| Gastric & Gastroesophageal Junction Adenocarcinoma | ||

| Non-Small Cell Lung Cancer (HER2-altered) | ||

| Colorectal Cancer (HER2-amplified subset) | ||

| Biliary Tract & Pancreatic Cancers (HER2-positive subset) | ||

| By End User | Hospital & Academic Pathology Laboratories | |

| Independent Reference/Central Laboratories | ||

| Research Institutes & CROs (clinical trials, translational) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the HER2 testing market?

The HER2 testing market size is expected to reach USD 234.82 million in 2026 and grow to USD 346.86 million by 2031.

How fast is the market growing?

The market is projected to advance at a CAGR of 8.09% between 2026 and 2031.

Which test modality contributes the most revenue?

Immunohistochemistry accounted for 48.19% of 2025 revenue, retaining the largest share of the HER2 testing market.

Which region is expanding the fastest?

Asia-Pacific is forecast to post the quickest CAGR at 10.43% to 2031, driven by recent approvals in China and Japan.

How significant is liquid biopsy in HER2 testing?

Liquid biopsy presently holds a small share but is on course for a 10.56% CAGR to 2031 as companies validate ctDNA for HER2, ER, and PR detection.

Who are the leading vendors?

Roche, Agilent, and Danaher lead established IHC and ISH platforms, while Illumina, Guardant Health, and NeoGenomics are gaining ground through NGS and liquid-biopsy solutions.

Page last updated on: