Hemp-based Foods Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

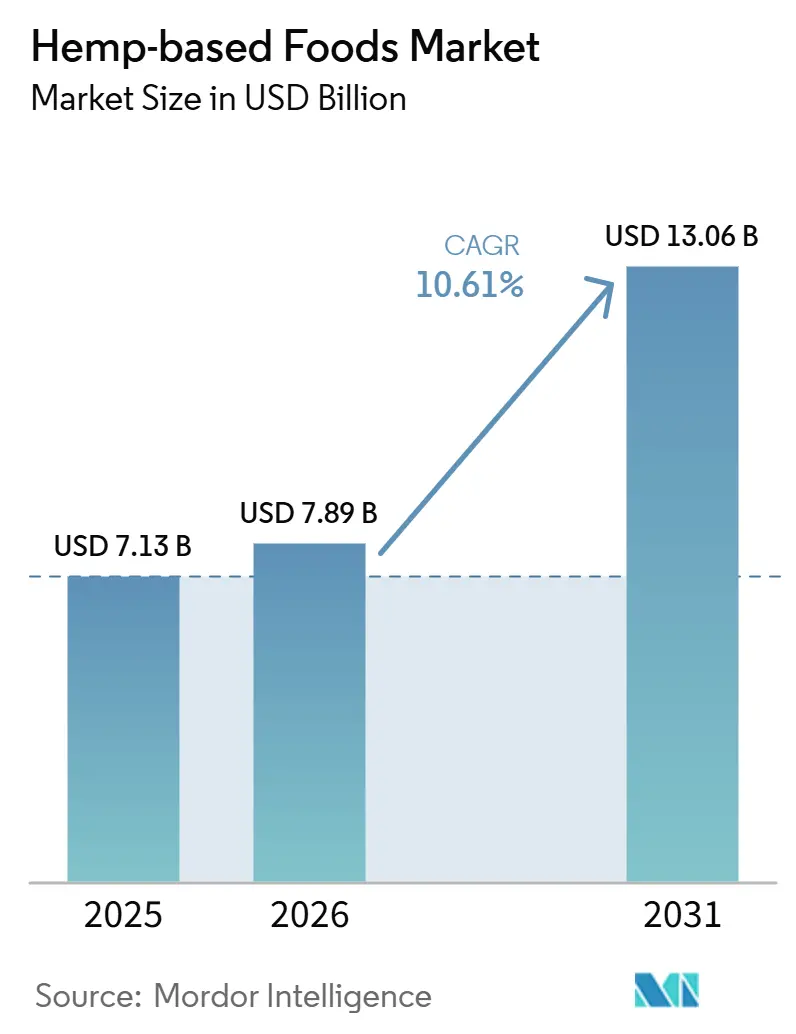

| Market Size (2026) | USD 7.89 Billion |

| Market Size (2031) | USD 13.06 Billion |

| Growth Rate (2026 - 2031) | 10.61% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hemp-based Foods Market Analysis by Mordor Intelligence

The Hemp-based Foods Market size was valued at USD 7.13 billion in 2025 and is estimated to grow from USD 7.89 billion in 2026 to reach USD 13.06 billion by 2031, at a CAGR of 10.61% during the forecast period (2026-2031).

The hemp-based foods market is expanding from a niche wellness category into a broader food category, supported by rising plant-based protein consumption and stronger consumer focus on ingredient quality, allergen status, and sustainability. Hemp continues to gain traction as it offers a complete amino acid profile, supports clean-label product development, and is suitable for packaged foods, snacks, oils, and supplements. The market also benefits from wider retail visibility, with hemp products increasingly available in mainstream grocery chains rather than only in natural food stores. Organic-certified products continue to influence premium shelf placement and product innovation, while the market faces challenges from uneven regulations, persistent confusion between hemp foods and cannabis products, and higher ingredient and processing costs compared to soy and pea protein.

Key Report Takeaways

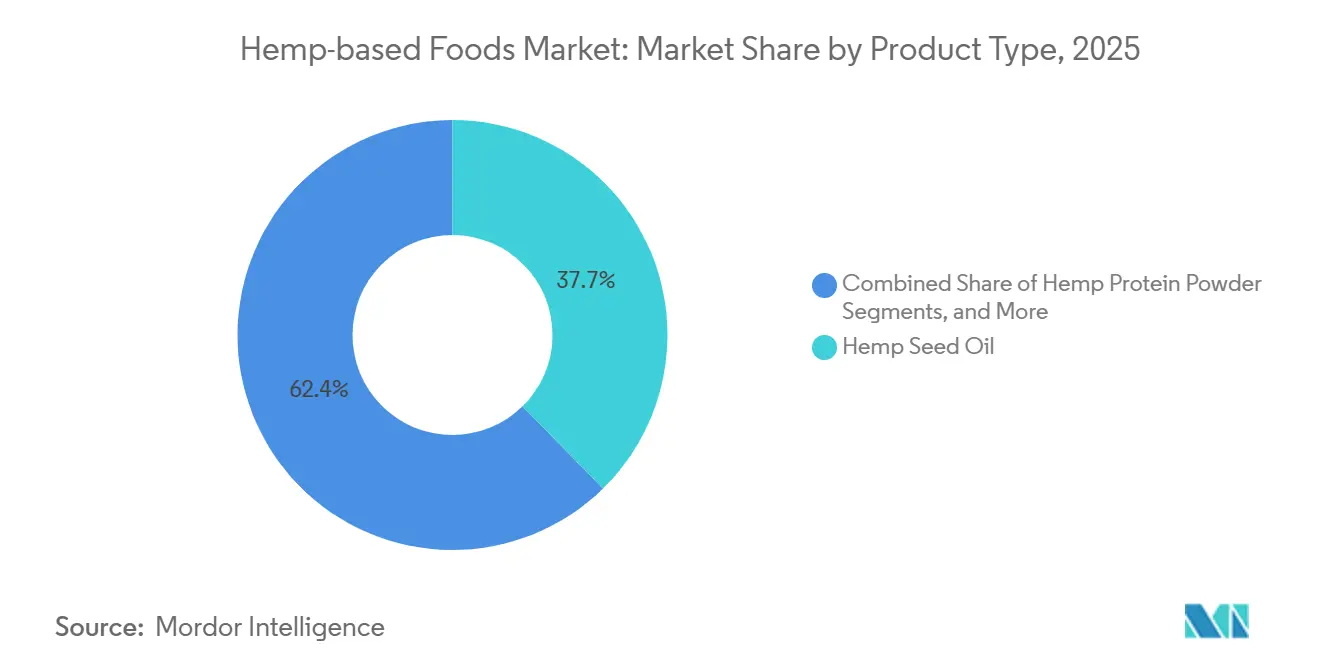

- By product type, hemp seed oil held 37.65% of revenue in 2025, while hemp protein powder is projected to grow at an 11.93% CAGR through 2031.

- By category, organic accounted for 65.23% of revenue in 2025 and is also forecast to expand at a 12.67% CAGR through 2031.

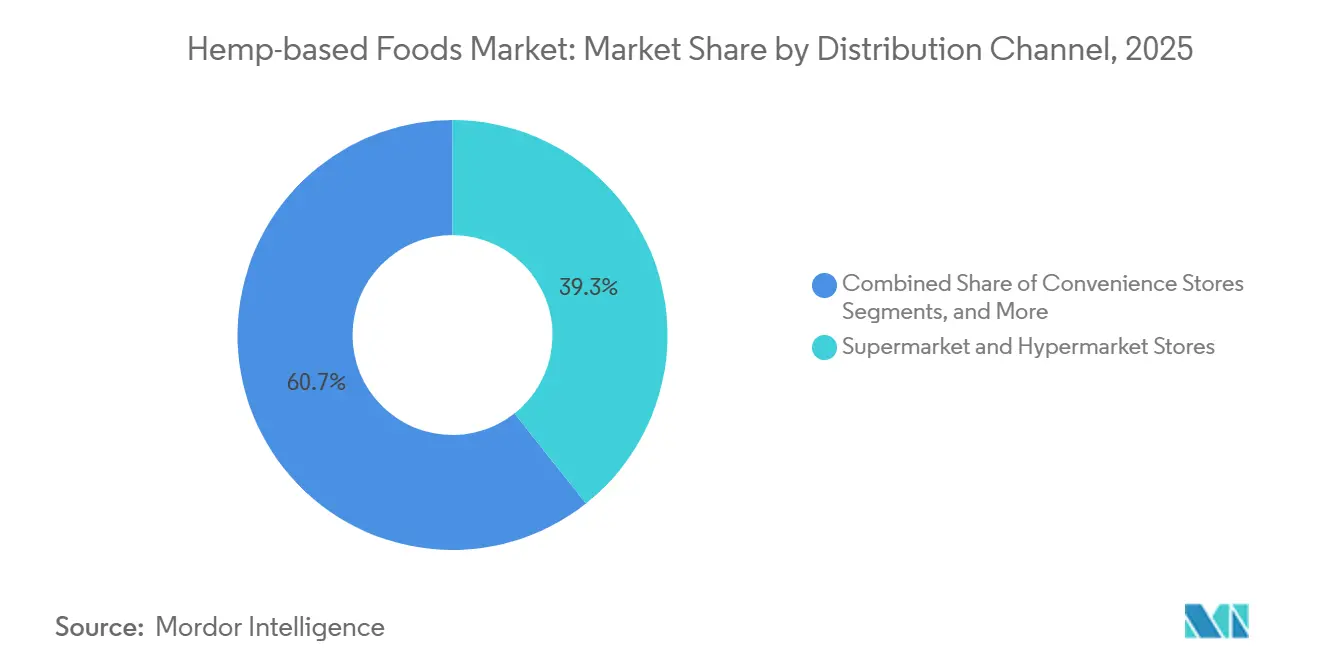

- By distribution channel, supermarket and hypermarket Stores led with 39.34% share in 2025, while online retail is expected to record the highest CAGR at 11.35% through 2031.

- By application, bakery and confectionery captured 42.88% of the hemp-based foods market share in 2025, while nutraceuticals and dietary supplements is projected to grow at a 12.78% CAGR through 2031.

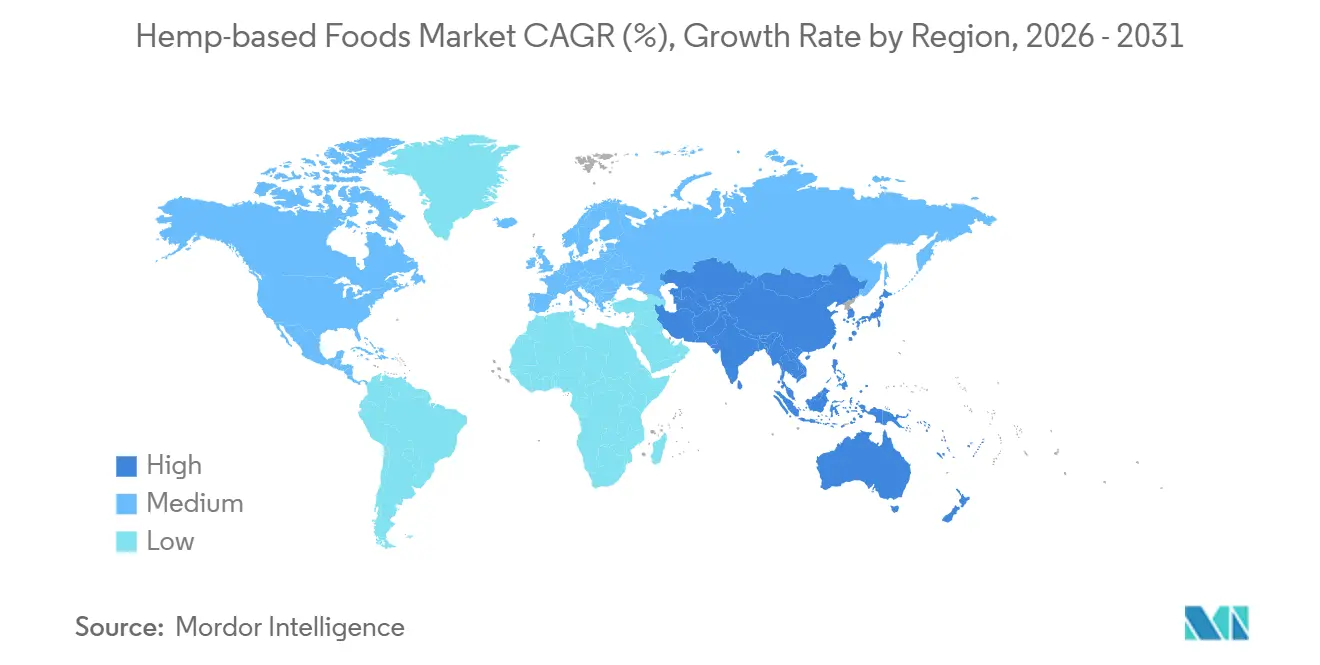

- By geography, North America represented 40.56% of the hemp-based foods market size in 2025, while Asia-Pacific is forecast to advance at a 13.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hemp-based Foods Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising demand for plant-based protein alternatives | +3.2% | Global, with highest intensity in North America and Western Europe | Medium term (2-4 years) |

| Expanding clean-label and allergen-free food claims | +1.9% | North America and Europe, with spillover to APAC premium segments | Medium term (2-4 years) |

| Retail mainstreaming of hemp ingredients beyond specialty channels | +1.6% | North America, Europe, and emerging APAC markets | Short term (≤ 2 years) |

| Product innovation in hemp-based functional foods | +1.4% | Global, led by North America and Germany | Long term (≥ 4 years) |

| Volatility in conventional protein supply chains | +1.1% | Global, especially in APAC import-dependent markets | Short term (≤ 2 years) |

| Traceability-driven premiumization of organic hemp | +0.8% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Plant-Based Protein Alternatives

The hemp-based foods market is benefiting from the wider shift toward plant-based diets across mature and emerging economies. Manufacturers are also seeking alternatives as soy and corn protein prices faced volatility after climate-related harvest disruptions in 2024. Hemp protein contains all essential amino acids, giving it a stronger nutritional profile than some other plant proteins used in mainstream formulations. In April 2025, Victory Hemp Foods commissioned North America’s largest hemp heart protein and oil processing line, designed to support sourcing from more than 20,000 acres of hemp by 2030 while generating USD 18 million annually for U.S. farmers.[1]Victory Hemp Foods, “Victory Hemp Foods Answers Food & Beverage Demand With the Launch of North America’s Largest Hemp Heart Protein & Oil Processing Line,” BusinessWire, businesswire.com

Expanding Clean-Label and Allergen-Free Food Claims

Clean-label demand has become a mainstream product requirement, supporting the expansion of the hemp-based foods market into wider retail channels. Hemp ingredients enable shorter ingredient lists and help brands avoid allergen concerns linked to oats, nuts, and other plant-based inputs. In its June 2025 retail launch, Manitoba Harvest’s Hemp+ range combined Regenerative Organic Certified, Non-GMO Project Verified, Kosher, and Vegan positioning, strengthening its shelf appeal in premium channels. Hemp also helps manufacturers support multiple claims within a single product, reducing the need for separate claim-based product lines.

Retail Mainstreaming of Hemp Ingredients Beyond Specialty Channels

The hemp-based foods market is expanding as hemp products gain placement in large retail chains instead of remaining concentrated in specialty wellness stores. Broad shelf access improves visibility, normalizes the category, and supports repeat purchases among mainstream consumers. However, wider distribution increases price comparisons with soy, whey, and pea protein, requiring stronger differentiation to protect premium pricing. Manitoba Harvest pursued a steady retail activation strategy through exclusive launches with major partners, including Whole Foods in 2025 and Sprouts Farmers Market in 2026.

Product Innovation in Hemp-Based Functional Foods

Functional positioning is expanding hemp’s role in the hemp-based foods market beyond traditional seed and oil formats. Brands are incorporating hemp into products associated with immunity, energy, mood, gut health, and sports recovery, moving the category into higher-value applications. In 2025, Nepra Foods introduced a hemp protein ingredient for egg-free baking to improve gelation performance in bakery formulations where standard hemp proteins had been less effective. As manufacturers resolve formulation challenges, the market can move further toward processed and function-led products instead of relying mainly on base ingredients.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Regulatory fragmentation across food-grade hemp markets | -1.4% | Europe as the core pressure point, with transitional effects in North America | Medium term (2-4 years) |

| Consumer confusion between hemp foods and cannabis products | -0.7% | Global, with stronger impact in APAC and Middle East markets | Short term (≤ 2 years) |

| Higher ingredient and processing costs versus commodity proteins | -0.6% | Global, especially in price-sensitive South and Southeast Asian markets | Long term (≥ 4 years) |

| Limited food-grade processing capacity and infrastructure | -0.4% | APAC, South America, and parts of MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Fragmentation Across Food-Grade Hemp Markets

The hemp-based foods market continues to face uneven regulations across countries, creating barriers for companies seeking regional scale. Traditional hemp seed, hemp seed oil, and hemp seed protein have clearer acceptance in some markets, while adjacent formats remain exposed to policy uncertainty. This limits product planning, raises compliance costs, delays investment, and slows commercial rollouts. In the United States, ongoing policy discussions around consumable hemp products continue to create uncertainty for some formats, while in Europe, Novel Food requirements continue to influence innovation pathways.

Higher Ingredient and Processing Costs Versus Commodity Proteins

Hemp protein remains more expensive than soy and pea protein in many commercial settings, limiting adoption in price-sensitive food categories such as institutional food service and mass-market packaged foods. Organic certification adds costs through verified cultivation, third-party audits, and supply chain separation, while smaller players face high capital requirements for advanced extraction and handling systems. Victory Hemp Foods stated that its April 2025 processing expansion used a patented solvent-free and minimal-heat extraction method to produce a 70% protein concentrate while supporting organic supply chains. The cost gap may narrow first in premium functional products, while price-driven segments are likely to remain harder to penetrate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hemp Seed Oil Anchors Revenue While Hemp Protein Powder Drives Faster Expansion

Hemp Seed Oil hold 37.65% of product revenue in 2025, making it the largest product category in the hemp-based foods market. Hemp Protein Powder is the fastest-growing product type and is projected to expand at an 11.93% CAGR through 2031. The market continues to rely on established seed-oil consumption, while growth is shifting toward protein-led formulations. Manufacturers use Hemp Seed Oil in culinary products, nutraceutical formats, and packaged food ingredient systems, supported by its omega fatty acid profile, cold-pressed positioning, and non-GMO appeal.

Hemp Protein Powder is gaining importance as a differentiated ingredient rather than a basic plant protein substitute. Demand remains strongest in sports nutrition, functional beverages, and meal replacement products, where protein quality and ingredient origin are key purchase factors. Whole Hemp Seed and Hulled Hemp Seed continue to support demand in granola, smoothie toppings, trail mixes, and seed-based snacks. Tilray Brands launched The Humble Seed Whole Wheat Protein Crackers in August 2025, offering 5 g of plant-based protein per 30 g serving through select Whole Foods Market stores.

By Category: Organic’s Lead Remains Strong and Growth Is Still Concentrated in Certified Supply Chains

Organic accounted for 65.23% of category revenue in 2025, giving it the largest share of the hemp-based foods market. It is also the fastest-growing category, with a 12.67% CAGR projected through 2031. This strong position reflects the focus of retail buyers, premium shelves, and product innovation budgets on certified products. Many natural and specialty retailers treat organic certification as a baseline requirement for hemp-based listings, giving certified brands a structural advantage.

Certified superfood portfolios are attracting investor interest as durable growth platforms. Laird Superfood completed its acquisition of Navitas LLC in March 2026 for USD 38.5 million, supported by a concurrent USD 50 million investment from Nexus Capital Management. Regenerative Organic Certified positioning is adding another premium layer above baseline organic status, especially for brands focused on soil health and sustainability claims. Conventional products remain relevant in value-focused and food-service channels, but premium shelf expansion and new product investment continue to center on certified lines.

By Distribution Channel: Supermarkets Hold the Largest Base While Online Retail Builds the Faster Growth Story

Supermarket and Hypermarket Stores hold 39.34% of channel revenue in 2025, giving them the largest presence in the hemp-based foods market. Online Retail is projected to record the highest CAGR, at 11.35%, through 2031. Mainstream grocery continues to provide the strongest volume base, while digital channels are capturing faster growth in repeat wellness purchasing. Supermarkets have increased hemp product visibility and placed these products alongside other plant-based and functional food alternatives.

Online channels are expanding because they allow brands to explain hemp benefits, target dietary needs, and build recurring revenue through subscription models. These advantages are important for products that still require consumer education before purchase. The channel also supports higher basket values in several wellness categories, improving customer lifetime value for direct-to-consumer brands. Manitoba Harvest combined major retail launches with broader consumer visibility, reflecting a two-channel strategy followed by many brands in the hemp-based foods market.

By Application: Bakery Provides the Largest Revenue Base While Nutraceuticals and Dietary Supplements Lead Growth

Bakery and Confectionery accounted for 42.88% of the hemp-based foods market size in 2025, making it the largest application segment. Nutraceuticals and dietary supplements are the fastest-growing applications and are forecast to expand at a 12.78% CAGR through 2031. Current revenue remains concentrated in familiar food applications, while future growth is moving toward functional formats. Hemp seed oil, hemp flour, and seed inclusions fit well into breads, bars, and premium confectionery, supporting a stable application base.

Growth in nutraceuticals and dietary supplements reflects the use of hemp for specific wellness goals, including mood, energy, immunity, recovery, and satiety. Manitoba Harvest expanded this approach in June 2025 with Hemp+ Mood, Hemp+ Energy, and Hemp+ Immunity smoothie boosters, including 8 g of protein per serving in the energy variant. Bakery is also evolving as ingredient developers address functional limitations in egg-free and gluten-free systems. Nepra Foods introduced a hemp protein for egg-free baking in 2025 to improve performance in that application.

Geography Analysis

North America accounted 40.56% of global revenue in 2025, securing the largest regional position in the hemp-based foods market. The region benefits from strong retail infrastructure, a developed hemp supply chain, and higher mainstream awareness of hemp nutrition than other markets. The United States remains the primary demand center, with hemp products increasingly available across broad retail networks, while Canada strengthens the regional market through its established cultivation base and seed-to-shelf supply chain links.

Europe remains the second-largest region, supported by demand for traditional hemp food ingredients such as seeds, oil, and protein. However, a mixed regulatory environment across member states continues to slow broader ingredient innovation and shifts commercial focus toward accepted product formats. Organic trade flows also support the region, and U.S.-EU organic equivalence enables easier movement of certified products across the Atlantic.

Asia-Pacific is the fastest-growing region and is projected to expand at a 13.56% CAGR through 2031. China and India are leading this growth from a smaller base, supported by rising disposable income, broader interest in plant-based diets, and increasing digital access to wellness products. Japan remains a steady market, while South Korea and Australia offer mid-tier growth potential; South America, the Middle East, and Africa remain earlier-stage areas with emerging opportunities through urban health-food retail and organized grocery expansion.

Competitive Landscape

The hemp-based foods market is moderately fragmented, with branded leaders operating in premium retail and regional ingredient suppliers competing across commodity and co-manufacturing channels. Manitoba Harvest, Nutiva, Navitas Organics, and Elixinol Wellness remain among the better-known companies in the branded tier. Competition is driven by retail shelf access, certification depth, processing quality, and supply chain control, rather than scale alone. Companies that combine strong sourcing capabilities with visible consumer-facing brands hold a clear advantage, while consolidation is increasing around organic and superfood platforms.

Laird Superfood acquired Navitas LLC in March 2026 for USD 38.5 million, supported by a USD 50 million investment from Nexus Capital Management, highlighting investor interest in certified superfood portfolios with hemp as a core ingredient set. In April 2026, Laird acquired Terrasoul Superfoods with an additional USD 60 million convertible preferred equity investment from Nexus Capital, extending the same aggregation strategy. Manitoba Harvest built a broad branded presence across North America and used repeated exclusive launches with major retailers to maintain visibility across product cycles. This approach strengthened retailer confidence and helped sustain brand relevance in the hemp-based foods market.

Processing technology is becoming a more durable source of competitive advantage in the hemp-based foods market. Victory Hemp Foods expanded in April 2025 with North America’s largest hemp heart protein and oil processing line, using a solvent-free and minimal-heat process to support premium ingredient quality. Food manufacturers increasingly seek cleaner processing, reliable functionality, and compatibility with organic supply chains. Nexus Agriscience acquired Biotech Institute’s hemp division intellectual property portfolio in January 2026, showing that genetics and seed assets are becoming part of the long-term competitive strategy, while white space remains strongest in ingredient formats with improved gelation or emulsification and bakery applications requiring specialized performance.

Hemp-based Foods Industry Leaders

Hemp Foods Australia Pty Ltd.

Manitoba Harvest Inc.

Nutiva Inc.

Navitas Organics, LLC

Hempro International GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Manitoba Harvest launched Superfood Smoothie Boosters exclusively at Sprouts Farmers Market nationwide, expanding its hemp-based functional nutrition range.

- January 2026: Nexus Agriscience acquired Biotech Institute’s hemp division intellectual property portfolio, including patents, genetic materials, and seed inventory.

- June 2025: Manitoba Harvest expanded its Hemp+ portfolio with Hemp+ Mood, Hemp+ Energy, and Hemp+ Immunity smoothie boosters; the energy variant offered 8 g of protein per serving.

- April 2025: Victory Hemp Foods commissioned North America’s largest hemp heart protein and oil processing line to support sourcing from more than 20,000 hemp acres by 2030.

Global Hemp-based Foods Market Report Scope

As per the scope of the report, hemp-based foods are edible products derived from the seeds, leaves, or oil of the Cannabis sativa plant, specifically cultivated as industrial hemp. They are celebrated as nutritional powerhouses, prized for their high complete-protein content, perfect ratio of essential fatty acids (Omega-3 and Omega-6), and allergen-free profile.

The hemp-based foods market is segmented by product type, category, distribution channel, application, and geography. By product type, the market includes hemp seed oil, hemp protein powder, whole hemp seed, hulled hemp seed, and other hemp food products. By category, the market is segmented into organic and conventional. By distribution channel, the market is segmented into supermarkets and hypermarkets, convenience stores, specialty stores, online retail, and other distribution channels. By application, the market is segmented into bakery and confectionery, beverages, dairy alternatives, snacks and cereals, nutraceuticals and dietary supplements, and other applications. By geography, the market is analyzed across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Hemp Seed Oil |

| Hemp Protein Powder |

| Whole Hemp Seed |

| Hulled Hemp Seed |

| Other Hemp Food Products |

| Organic |

| Conventional |

| Supermarket and Hypermarket Stores |

| Convenience Stores |

| Specialty Stores |

| Online Retail |

| Other Distribution Channels |

| Bakery and Confectionery |

| Beverages |

| Dairy Alternatives |

| Snacks and Cereals |

| Nutraceuticals and Dietary Supplements |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Hemp Seed Oil | |

| Hemp Protein Powder | ||

| Whole Hemp Seed | ||

| Hulled Hemp Seed | ||

| Other Hemp Food Products | ||

| By Category | Organic | |

| Conventional | ||

| By Distribution Channel | Supermarket and Hypermarket Stores | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail | ||

| Other Distribution Channels | ||

| By Application | Bakery and Confectionery | |

| Beverages | ||

| Dairy Alternatives | ||

| Snacks and Cereals | ||

| Nutraceuticals and Dietary Supplements | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the hemp-based foods sector?

The hemp-based foods market stood at USD 7.89 billion in 2026 and is projected to reach USD 13.06 billion by 2031 at a CAGR of 10.61%.

Which product category leads revenue in hemp-based foods?

Hemp Seed Oil was the leading product type in 2025 with 37.65% of revenue, supported by broad use in culinary and nutraceutical products.

Which application is growing the fastest in hemp-based foods?

Nutraceuticals and Dietary Supplements is the fastest-growing application, with a projected CAGR of 12.78% through 2031.

Why are organic hemp food products growing so quickly?

Organic products held 65.23% of category revenue in 2025 and continue to lead because premium retailers and certified wellness brands prioritize organic positioning.

Which region is growing the fastest for hemp-based foods?

Asia-Pacific is the fastest-growing regional segment, with a forecast CAGR of 13.56% through 2031, led by expanding plant-based demand in China and India.

What is holding wider adoption back in hemp-based foods?

The main constraints are uneven regulation across markets, consumer confusion between hemp foods and cannabis products, and higher ingredient and processing costs compared with soy and pea protein.

Page last updated on: