Heat Pump Water Heater Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 12.96 Billion |

| Market Size (2031) | USD 22.76 Billion |

| Growth Rate (2026 - 2031) | 11.92% CAGR |

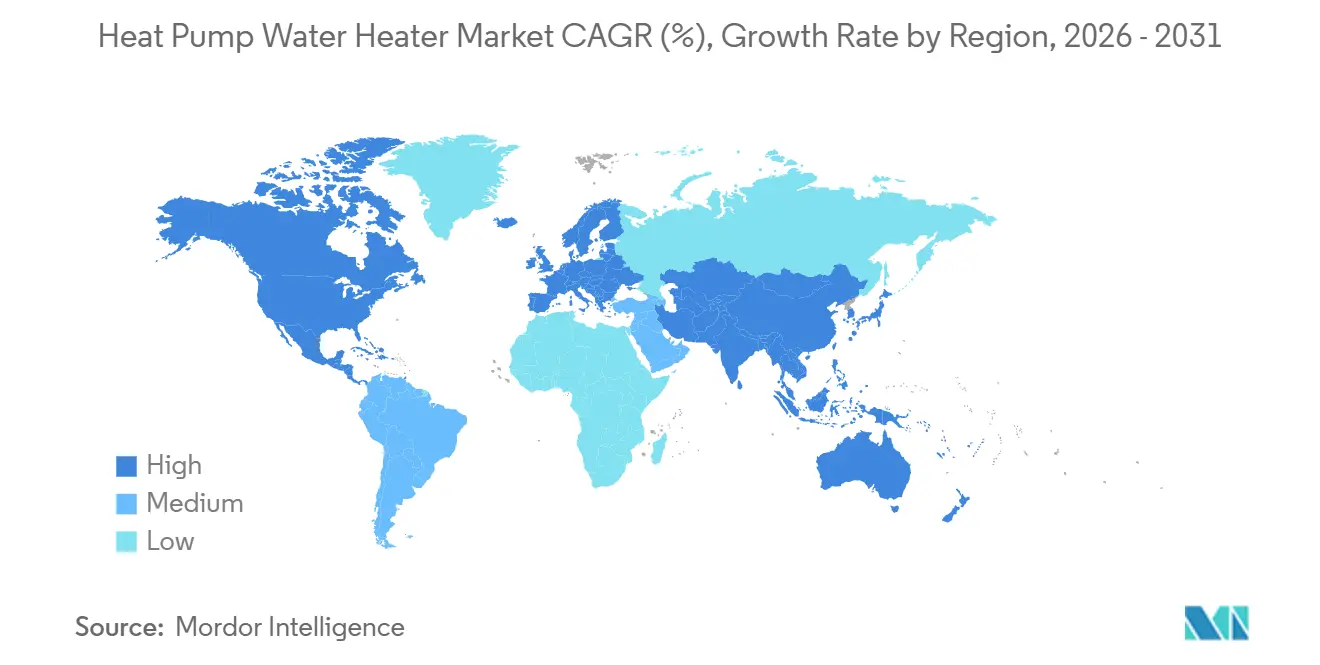

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Heat Pump Water Heater Market Analysis by Mordor Intelligence

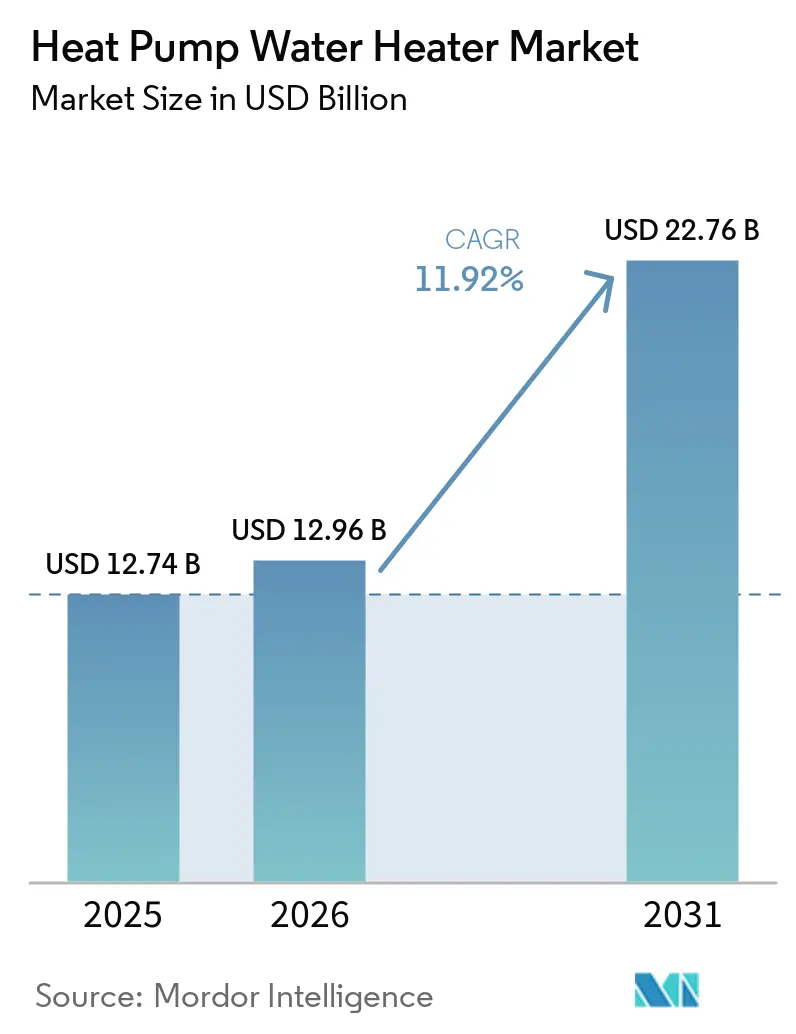

The heat pump water heater market size is expected to grow from USD 12.74 billion in 2025 to USD 12.96 billion in 2026 and is forecast to reach USD 22.76 billion by 2031 at 11.92% CAGR over 2026-2031. Policy is the strongest growth lever as national efficiency standards converge with refrigerant phase-downs and local zero-emission rules, shifting the replacement decision from efficiency upgrades to technology changeovers across both residential and commercial projects [1]U.S. Department of Energy, “Energy Conservation Standards for Consumer Water Heaters Final Rule,” U.S. Department of Energy, energy.gov. The United States Department of Energy’s April 2024 final rule, which takes effect in May 2029, raises performance thresholds for electric storage water heaters above 35 gallons into a range achievable only with heat pump architectures. This trigger accelerates adoption and retools product portfolios well before the compliance date. European Union Regulation 2024/573 tightens the pathway to low-GWP refrigerants, while California proposals for zero-emission equipment by 2030 complement these changes, reinforcing the deployment of Energy-Efficient Water Heating Systems and Sustainable Water Heating Solutions as default choices rather than niche options. Financial incentives amplify this policy momentum, with the federal Section 25C credit covering 30% of installed costs up to USD 2,000 and the IRA’s Household Energy Appliance Rebates reducing net ownership costs, thereby shortening paybacks and advancing Carbon Emission Reduction outcomes in typical households. As utilities expand load flexibility programs, Smart Heat Pump Water Heaters with CTA-2045 connectivity align with grid needs by shifting electric water heating to cleaner, cheaper hours, adding an operational tailwind to the heat pump water heater market.

Key Report Takeaways

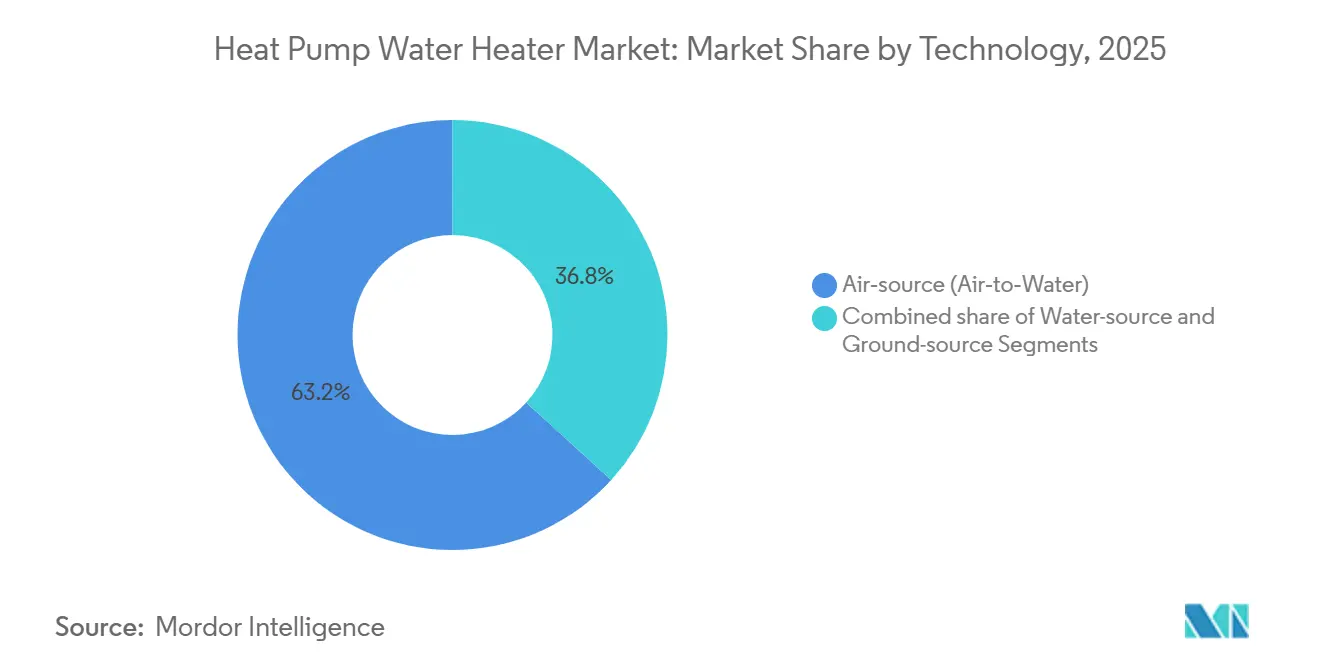

- By technology, air-source systems led with a 63.22% revenue share in 2025 in the heat pump water heater market, while ground-source systems are projected to expand at a 12.43% CAGR through 2031.

- By capacity, units above 500 L accounted for 38.41% of the heat pump water heater market in 2025, and the 200–500 L range is projected to grow at a 12.22% CAGR through 2031.

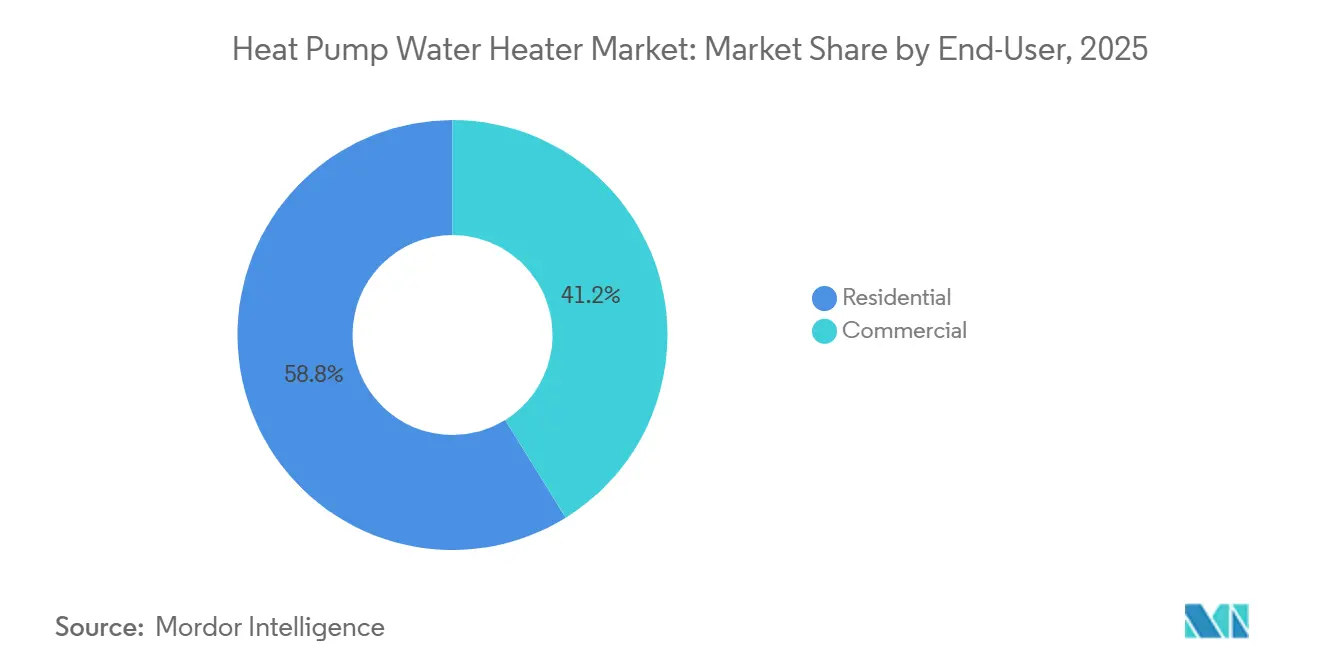

- By end-user, residential held 58.84% share in 2025, while the commercial heat pump water heater market size is projected to expand at a 12.14% CAGR through 2031.

- By distribution channel, B2C captured 63.75% share in 2025 in the heat pump water heater market, with B2B or direct sales expected to grow at a 12.06% CAGR through 2031.

- By geography, Asia-Pacific led the heat pump water heater market with 44.91% share in 2025, while North America is projected to grow at a 12.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Heat Pump Water Heater Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| United States DOE 2024 final efficiency standards for water heaters (2029 compliance) catalyze HPWH adoption in residential and commercial DHW | +3.2% | North America, with spill-over to Canada and Mexico, aligning codes | Medium term (2-4 years) |

| Consumer and installer incentives (e.g., United States 25C tax credit/rebates) lower the effective upfront cost and accelerate replacements | +2.1% | North America, selective European Union states (Germany, France, Poland), Australia | Short term (≤ 2 years) |

| Asia-Pacific ECO Cute installed base scale effects (Japan) normalize awareness, channel familiarity, and service infrastructure | +1.4% | Asia‑Pacific core (Japan, South Korea), with early adoption in Taiwan and Singapore | Long term (≥ 4 years) |

| Improving electricity-to-gas price ratios and grid decarbonization support HPWH operating cost advantages | +2.5% | Global, strongest in Northern Europe, California, Australia | Long term (≥ 4 years) |

| Grid-interactive HPWH (CTA-2045/OpenADR) enables demand flexibility and VPP monetization for utilities and aggregators | +1.7% | North America (West Coast), Oceania, and selective European Union pilots (Netherlands, United Kingdom) | Medium term (2-4 years) |

| High-temperature HPWH (R744/R290) meets 60 °C+ health codes, expanding commercial retrofits in hospitals, hotels, and multifamily | +2.3% | Europe (GWP compliance-driven), Japan, North America commercial corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

United States DOE 2024 final efficiency standards for water heaters (2029 compliance) catalyze HPWH adoption in residential and commercial DHW

The United States Department of Energy’s May 2024 final rule adopts tighter standards for consumer electric storage water heaters above 35 gallons that effectively require heat pump technology to reach uniform energy factor levels within the 2.30 to 2.50 range, creating a discontinuity in replacement economics and accelerating pre-compliance product transitions by major OEMs. Compliance starts in May 2029 for covered products, which alters purchase decisions several years earlier as distributors and installers align inventories and training with the new baseline. The rule also shifts the commercial arc, as more buyers evaluate high-temperature CO₂ and propane systems to meet facility health and safety codes at scale without combustion, expanding the heat pump water heater market in central plants and distributed DHW rooms. DOE projects cumulative energy savings of 17.6 quads over thirty years and consumer benefits of over USD 25 billion, which locks in the scale benefits needed to support greater localization of component supply and broader installer training networks. Larger platform redesigns that accompany these standards tend to concentrate share among manufacturers with stronger R&D pipelines and certification capacity, reinforcing the structural demand shift rather than incremental efficiency gains. These moves not only lift residential replacement volumes but also reframe commercial specification lists, where heat pumps will increasingly become the default option as code compliance and lifecycle costing converge.

Consumer and installer incentives (e.g., United States 25C tax credit/rebates) lower the effective upfront cost and accelerate replacements

The Section 25C Energy Efficient Home Improvement Credit covers 30% of qualified project costs, up to USD 2,000, for eligible heat pump water heater installations each year through 2032, reducing the net upfront burden and supporting a shorter payback window for typical residential systems [2]Internal Revenue Service, “Instructions for Residential Energy Credits,” Internal Revenue Service, irs.gov. Households also benefit from the IRA’s appliance rebate programs, including targeted rebates for income-qualified customers, further compressing the net installed cost of Smart Heat Pump Water Heaters in many markets. Together, these incentives address key buying barriers that historically favored gas storage replacements, advancing HVAC Electrification as consumers evaluate lower operating costs and improved comfort. The annual reset feature of Section 25C allows phased upgrades across multi-tenant and single-family portfolios, helping property managers match with budget cycles without losing eligibility. Administrative features that require manufacturer product identification for credit eligibility also stabilize the contractor channel by reinforcing compliant model selection, which favors established brands that maintain complete certification documentation. This framework positions the heat pump water heater market for steady conversion of electric resistance stock over the forecast horizon as incentive awareness increases.

Improving electricity-to-gas price ratios and grid decarbonization support HPWH operating cost advantages

Time-of-use pricing and rising renewable shares shift the cost balance toward flexible electric loads that can preheat and store thermal energy when the grid is cleaner and cheaper, thereby enhancing the lifetime value of grid-connected Smart Heat Pump Water Heaters. When paired with CTA-2045 or comparable demand-response interfaces, these systems preheat during off-peak or high-renewable windows and limit resistive-element overrides, lowering average operating costs even in colder climates where compression work is higher. Regions with high hydro or wind penetration, such as Nordic markets, reinforce this advantage by providing ample low-carbon electricity, which widens the appeal of Energy-Efficient Water Heating Systems across seasons. As market rules provide participation pathways, commercial projects can stack grid services revenues with energy savings. At the same time, residential customers benefit from set-and-forget optimization that prioritizes preheating and storage over on-peak draws. This dynamic makes Sustainable Water Heating Solutions more compelling as part of whole home or building electrification plans that target Carbon Emission Reduction and bill stability. The result is a stronger long-run pull for the heat pump water heater market as fuel-switching economics tilt toward clean electricity.

High-temperature HPWH (R744/R290) meets 60 °C+ health codes, expanding commercial retrofits in hospitals, hotels, and multifamily

Commercial buyers in healthcare, hospitality, and multifamily need 60°C or higher delivery temperatures for Legionella control and sanitation, which is now achievable with R744 and R290 heat pumps that deliver 90°C to 130°C outlet temperatures at meaningful coefficients of performance. Local rules that phase out gas-fired tank units strengthen the appeal of these all-electric options for central plants and point-of-connection retrofits in buildings subject to stricter air-quality codes, which supports the commercial arc of the heat pump water heater market. Vendors are launching modular arrays that scale multi-hundred-kilowatt blocks, enabling phased deployment strategies across large properties and helping facility managers match capital cycles to equipment swaps. Commercial Heat Pump Water Heaters that meet high setpoints reduce the need for fossil-fuel backup and ease water-quality compliance in sensitive environments, which was a critical barrier for electric-only systems until R744 and R290 platforms matured. New monobloc designs that meet GWP thresholds also reduce on-site refrigerant handling and simplify permitting procedures in many European jurisdictions as building codes evolve. These advances broaden the addressable base well beyond residential replacements, lifting the heat pump water heater market in segments previously locked to combustion technologies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost and installer capacity shortages slow roll-outs and elongate project timelines | -2.8% | Global, acute in North America and Japan (aging technician base) | Short term (≤ 2 years) |

| Refrigerant transition (F-gas phase-down) adds redesign, certification, and handling complexity for OEMs and installers | -1.6% | Europe (Regulation 2024/573 compliance), selective Asia markets | Medium term (2-4 years) |

| Design risks for Legionella/thermal disinfection and scald protection in retrofits raise CapEx and controls complexity | -1.1% | Global commercial, stringent in the European Union healthcare, and North America institutional | Long term (≥ 4 years) |

| Interoperability gaps for grid-signals (CTA-2045 variants/utility programs) limit scalable DR aggregation today | -0.9% | North America West Coast, selective European Union pilots, Oceania | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High upfront cost and installer capacity shortages slow roll-outs and elongate project timelines

Installed costs remain a major friction point for many households and small businesses, especially when projects require a 240V circuit, a condensate pump, and adequate airflow clearances that do not apply to like-for-like gas swaps. Emergency replacement scenarios often favor available gas stock when installers cannot schedule a visit in time, an operational reality that slows unit conversions even in areas with strong incentives. Regions with aging technician pools face additional constraints, as retirements and certification requirements compress available labor even as policy pushes raise demand for installations. OEMs have responded with designs that reduce installation time, including top-water connections and duct-ready enclosures, which reduce field modifications and simplify retrofits through familiar contractor practices. Broader adoption of installer training programs and standardized commissioning checklists will be essential to converting interest into completed projects at scale, particularly in cold-climate zones where sizing and sitting require additional diligence [3]Daikin Europe, “R290 Monobloc Portfolio and Technical Guidance,” Daikin Europe, daikin.eu. In the near term, these workforce and cost frictions mute some of the growth upside even as the policy and incentive signals strengthen the long-run case for the heat pump water heater market.

Refrigerant transition (F-gas phase-down) adds redesign, certification, and handling complexity for OEMs and installers

Regulation 2024/573 accelerates the phase-down of higher-GWP refrigerants across heat pump classes. It introduces compliance windows that require model redesigns and parallel inventory strategies, adding costs and operational complexity for OEMs and installers. European integrators have introduced new R290 monoblocs and split systems to navigate the thresholds and still deliver elevated water temperatures in retrofit conditions, representing a significant refresh of the installed base pipeline. Certification and testing requirements for new refrigerants and controls add time and expense to product launches. At the same time, installers adopt new protocols for flammable refrigerants to maintain site safety in occupied spaces. The regulation harmonizes long-term market direction toward low-GWP refrigerants, but it also creates transitional complexity that stretches training resources and increases project risk for first-time adopters. With the policy now in force, early movers in R290 and R744 portfolios gain a timing advantage as compliance dates tighten and legacy HFC inventories run down. This carries near-term friction but clarifies the pathway for OEM investment and installer certification that will support the heat pump water heater market over the forecast horizon.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Ground-Source Gains Share Through Grid-Integration Optionality Despite Installation Premiums

Air-source systems held 63.22% share in 2025, while ground-source posted the fastest trajectory at a 12.43% CAGR through 2031 as buyers weigh lifecycle performance and grid-integration benefits that support load flexibility. Air Source Heat Pump Water Heater platforms benefit from familiarity and shorter installation windows for emergency replacements, which helps preserve their volume lead in the heat pump water heater market. Ground-source systems sustain high seasonal efficiency by avoiding deep defrost penalties and stabilizing COPs near or above 4.0, which fits colder zones that also value predictable operating costs. As grid operators promote flexible loads, geothermal loops can operate as long-duration thermal batteries that enhance demand response and arbitrage time-of-use tariffs, thereby serving as a strategic lever in large buildings and campus settings [4]American Council for an Energy-Efficient Economy, “Flexible Loads and Water Heating Controls,” American Council for an Energy-Efficient Economy, aceee.org. This performance profile appeals to institutions that optimize energy savings, maintenance, and grid-service revenue. This mix strengthens the heat pump water heater market in projects that emphasize the total cost of ownership.

Air-source leadership remains solid as distributors and contractors manage two-day lead times across many markets, and new monobloc offerings simplify permitting in markets with strict refrigerant-handling rules, which keeps first-cost and scheduling advantages in their favor. Ground-source adoption is concentrated in new construction and planned retrofits because drilling costs and site logistics extend timelines, even when performance benefits are compelling. Water-source configurations remain niche, serving coastal, district energy, or process-heat recovery applications where stable source temperatures and system integration are already in place. Across both mainstream paths, Smart Heat Pump Water Heaters that integrate with building automation systems and DR platforms improve operating economics and serviceability, which supports the broader heat pump water heater industry as companies design for connectivity by default. The outlook preserves air-source volume leadership but favors rising ground-source share, which aligns with the policy and grid conditions that backload value into lifecycle metrics rather than only into initial price.

By Capacity (Tank Volume): Mid-Range 200–500 L Units Lead Growth as Commercial Retrofits Scale Beyond Residential Replacement Cycles

Above 500 L tanks captured 38.41% of 2025 demand, while the 200–500 L band is forecast to grow at 12.22% through 2031 as specifiers prioritize modular thermal storage and staged deployments across multifamily and light commercial sites. Mid-size systems allow preheating during low-cost periods and smoother recovery during peaks, which limits resistive-element overrides and improves the economics of grid-interactive operation. Commercial projects value redundancy and service continuity, so arrays of 200–500 L units can replace a single large tank while reducing downtime risk, which is attractive in hospitality and healthcare. Above 500 L retains a strong role in central plants, where hydronic networks and system controls are already designed for large buffer volumes and sustained circulation, which is well-suited to hotels and campus-scale facilities. Scaling across these bands supports the heat pump water heater market as code requirements, and Legionella controls push projects toward higher storage temperatures and better mixing strategies.

Sub-200 L configurations hold their share in compact living spaces and point-of-use duty cycles, meeting the needs of small households and workspace kitchenettes without reconfiguring mechanical rooms. The 300–500 L range aligns well with demand-response use cases because the additional stored thermal energy supports Advanced Load Up strategies that avoid peak-period compressor stress, thereby increasing the value of connected control in DR programs. Food service and healthcare applications that store at 60°C and deliver at 49–50°C via thermostatic mixing valves add modest capital to ensure scald protection, which is a manageable design step compared to gas-fired replacements subject to local zero-NOx rules. The balance between redundancy, storage, and controls drives capacity selection, which keeps the 200–500 L band on a faster growth path even as very large tanks remain essential in centralized systems. This pattern underpins a broader shift toward modularity in the heat pump water heater market as customers weigh resilience alongside efficiency.

By End-User: Commercial Growth Outpaces Residential as Institutional Buyers Prioritize Lifecycle Economics and Grid-Service Revenue

In the heat pump water heater market, residential accounted for 58.84% in 2025, while commercial is projected to grow at 12.14% through 2031 as facility owners factor in lifecycle savings, uptime, and demand-response participation, in addition to compliance needs for hot-water delivery temperatures. Residential Heat Pump Water Heaters continue to benefit from federal incentives and local rebates that shorten paybacks, while connected features like leak detection and smartphone control increase homeowner confidence and reduce contractor callbacks. Large facilities turn to high-temperature R744 and R290 systems that achieve 60°C to 90°C or more, replacing gas-fired boilers and aligning with air-quality and safety rules that limit on-site combustion. In commercial settings, multifamily and hospitality stand out for their high DHW loads and predictable occupancy patterns, which align well with load shifting and thermal storage. These use cases lift the heat pump water heater market in segments that once relied on fossil backup to meet peak temperatures and recovery times.

On the residential side, incentive awareness and contractor readiness act as leading indicators for conversion rates, so programs that streamline paperwork and prequalify equipment accelerate adoption. Commercial adopters give greater weight to service contracts, controls integration, and installer training than retail buyers, which favors B2B channels that bundle commissioning and utility program enrollment. Hospitals and hotels now have viable all-electric options where code rules previously prevented lower-temperature heat pumps from operating without boost, expanding the pipeline for commercial Heat Pump Installation Cost models that include grid-service revenues. This shift raises the strategic value of Smart Heat Pump Water Heaters and supports the long run mix change within the heat pump water heater market as ESG and compliance priorities tighten. The net effect is a balanced profile where residential volume leads while commercial outgrows on the back of performance, compliance, and connectivity.

By Distribution Channel: B2B Direct Sales Gain Share Through Turnkey Installation Bundling and Utility Program Integration

In the heat pump water heater market, B2C, or retail, accounted for 63.75% in 2025, while B2B, or direct channels, are projected to grow at 12.06% through 2031, as commercial and institutional buyers favor integrated equipment, installation, and multi-year service structures that reduce project risk. Retail remains central to homeowner replacements, with exclusive models and connected features that guide brand selection, while in-app diagnostics cut after-sales costs and support warranty management. Direct sales organizations combine installer training with commissioning and DR enrollment, enabling commercial buyers to capture value streams beyond energy savings and keep systems up to date with current code and program rules. This approach supports ESG tracking, safety protocols for refrigerant handling, and ongoing optimization that many retail processes cannot bundle efficiently. As a result, the heat pump water heater market is seeing B2B expansion, where lifecycle service models and program integration make the case for premium features and controls.

Retail continues to scale connected offerings through app ecosystems that deliver notifications, remote adjustments, and energy usage insights, aligning with consumer expectations for smart home products. Direct channels offer advantages for large retrofits involving electrical work, permit sequencing, and safety coordination for flammable refrigerants, where applicable, which require trained teams and documented standard operating procedures. The channel split reflects differences in buyer priorities and project complexity, which sustains retail leadership in volume and B2B leadership in growth and margin capture. As utilities expand program requirements and verification standards, direct channels are positioned to scale faster due to established training infrastructure and service teams. This structure supports continued expansion of the heat pump water heater market across both consumer and professional pathways, while favoring turnkey bundles for complex sites.

Geography Analysis

North America is projected to grow at a 12.62% CAGR through 2031, supported by federal standards that require heat pump performance for electric storage units above 35 gallons and by layered incentives that reduce ownership costs for households and rental properties. DOE’s 2024 final rule with a May 2029 compliance date pushes product roadmaps and contractor training ahead of schedule, which sets a strong policy anchor for the heat pump water heater market in the region. Section 25C’s 30% credit up to USD 2,000 per year complements IRA rebate programs for eligible households, which compresses payback periods and supports conversions from electric resistance and gas replacements. Local rules that restrict gas-fired tank units in future installations increase the likelihood that all-electric designs will become the standard in many urban codes, affecting both central plants and distributed DHW systems.

Asia-Pacific led with 44.91% of global demand in 2025, reflecting a long-running installed base and channel experience in Japan that normalized consumer expectations and service availability for CO₂-based systems. Product evolution in the region includes daytime heating CO₂ models that integrate solar radiation forecasts to shift heating cycles to cheaper, cleaner hours, demonstrating advanced controls aligned with broader grid decarbonization. Vendor roadmaps also address compact footprints and installation constraints in dense urban housing to expand penetration beyond detached homes, which helps close the gap in multifamily settings. These adaptations keep the heat pump water heater market on a strong footing in Asia-Pacific as utility programs and tariff designs promote flexible loads across electrification plans.

Europe navigates the F-gas phase-down and aligns public funding with installer capacity-building in the heat pump water heater market. Regulation 2024/573 advances low-GWP refrigerants and compresses compliance timelines, driving an accelerated refresh of product portfolios and installer training modules for flammable refrigerant handling. European manufacturers have ramped up R290 monoblocs and commercial arrays that can meet hot-water requirements of 60°C to 75°C without backup systems in many retrofit scenarios, expanding the all-electric pathway for central DHW. Factory investments and regional production of components, such as inverter compressors, position the supply base to meet demand while complying with the new regulatory framework, helping stabilize lead times and pricing. Localized air quality and safety rules continue to set differences across markets. Still, the direction of travel supports a larger opportunity set for the heat pump water heater market across replacements and new construction.

Competitive Landscape

Global competition features HVAC incumbents with deep contractor channels, Asian specialists with CO₂ expertise for high-temperature applications, and European integrators aligning portfolios with the F-gas phase-down. This mix stabilizes the long-term expansion path of the heat pump water heater market. In the United States, brands with top-connected plumbing designs and duct-ready enclosures reduce retrofit time and simplify jobs for plumbers and HVAC contractors, which underpins stickiness in those channels. Asian OEMs are leveraging vertical integration in compressors and controls to expand their offerings for cold-climate and high-setpoint applications, widening options for commercial and multifamily retrofits. European leaders build on low-GWP refrigerant portfolios with R290 monoblocs and multi-module arrays that scale to district and campus loads, a strategy aligned with evolving codes and grid conditions. This spread of competencies positions the market to cover a full range of hot water duty cycles across climates and building types.

Differentiation is shifting from headline efficiency to integration capability and service ecosystems that support commissioning, DR enrollment, and predictive maintenance, which sustains value beyond the initial sale. Vendors that operate training centers for CTA-2045 connectivity and refrigerant handling build loyalty and reduce callbacks, encouraging specifiers to standardize on platforms with strong field support. Grid service aggregators illustrate that monetizing flexible loads favors integrated models or close OEM-aggregator partnerships, which place a premium on open APIs and secure data sharing. On the consumer side, connected apps for diagnostics and leak alerts reinforce brand reputation and enable subscription-based maintenance, thereby lengthening relationships and protecting installed bases. The combination of service depth and software maturity helps define where the heat pump water heater market captures higher margins and customer lifetime value.

Product roadmaps across regions reflect both regulatory requirements and customer demand for higher setpoints, modularity, and simplified installations, with examples including R290 monobloc releases, modular arrays for large facilities, and connected residential offerings for retail. Joint ventures have formed to localize key components for low-GWP platforms, supporting compliance while mitigating logistics and tariff risks. Residential lines that emphasize smartphone control and leak detection have broadened retail appeal. At the same time, CO₂-centric product families target commercial kitchens, healthcare facilities, and hotels that maintain strict sanitation and Legionella control standards. This innovation tempo sustains competitive intensity while sharpening the path for the heat pump water heater market to grow across both residential and commercial domains.

Heat Pump Water Heater Industry Leaders

Rheem Manufacturing

A. O. Smith

Ariston Group

Panasonic

Midea Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Panasonic Holdings launched the Aqua-G EVO R290 heat pump series at ISH Frankfurt. The lineup delivers 75°C water at -2°C ambient in 60kW, 80kW, and 110kW modules that can be cascaded. It is engineered to comply with European F-gas regulations, removing GWP-750+ refrigerants from split systems above 12kW by January 2029. Production will ramp at the EUR 320 million Czech facility, targeting 1.4 million units per year by 2030. The system reports a COP of 4.94 for propane with a GWP of 3, reflecting the market shift from HFC inventory to natural alternatives under Regulation (EU) 2024/573 and aligning with Sustainable Water Heating Solutions and broader Carbon Emission Reduction goals.

- March 2026: Haier Smart Home introduced the Yujia X6 central air-conditioning platform with AI-optimized dual-cylinder compression and an operating range from -37°C to 67°C. The launch marks Haier’s entry into heat pumps for cold-climate retrofits in northern China and export markets. It positions the company against established OEMs such as Daikin and Mitsubishi Electric in high-temperature segments that R744 specialists once dominated, signaling deeper upstream integration into compressor technology by Chinese manufacturers.

- January 2026: JEXSYS unveiled a high-temperature CO₂ heat pump at HVAC&R Japan 2026 rated for 130°C outlet. The unit provides 500kW of heating capacity with a COP of 4.8 and delivers 4.2 metric tons per hour of pressurized hot water for 120–130°C sanitary applications in food and beverage processing. The R744 platform targets fossil-fuel boiler replacements and qualifies for Japanese subsidy programs when configured for dual heating and cooling, supporting energy-recovery mandates in manufacturing and advancing Energy-Efficient Water Heating Systems that contribute to Carbon Emission Reduction.

- November 2025: Panasonic released the Ohisama Eco Cute slim CO₂ heat pump water heater with 44 cm depth as a compact daytime-heating model. It achieves 3.0 JIS annual efficiency and qualifies for subsidies up to 170,000 yen under Japan’s Hot Water Energy Saving 2025 Project. The design addresses multifamily retrofit constraints, such as elevator weight limits and limited mechanical-room space, with an Eco-Cute penetration of 3.3%, compared with 24.1% in detached homes. The product supports Japan’s 2050 carbon-neutrality goal across a 36.5-million-unit target base and exemplifies Smart Heat Pump Water Heaters within Sustainable Water Heating Solutions.

Global Heat Pump Water Heater Market Report Scope

Heat pump water heaters, unlike conventional electric resistance models, utilize electricity to transfer heat rather than generate it directly. This method allows them to achieve energy efficiency rates two to three times greater than their conventional counterparts. Essentially, heat pumps operate similarly to a refrigerator, but in reverse.

The Heat Pump Water Heater Market is Segmented by Technology (Air-source, Water-source, Ground-source), Capacity (Up to 200 L, 200–500 L, Above 500 L), End-User (Residential, Commercial), Distribution Channel (B2C Retail and B2B Direct Sales), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

| Air-source (Air-to-Water) |

| Water-source (Water-to-Water) |

| Ground-source (Geothermal) |

| Up to 200 L |

| 200–500 L |

| Above 500 L |

| Residential |

| Commercial |

| B2C/Retail Channels | Multi-brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B/Direct Sales |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia‑Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia‑Pacific | |

| Middle East And Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Technology | Air-source (Air-to-Water) | |

| Water-source (Water-to-Water) | ||

| Ground-source (Geothermal) | ||

| By Capacity (Tank Volume) | Up to 200 L | |

| 200–500 L | ||

| Above 500 L | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail Channels | Multi-brand Stores |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Direct Sales | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia‑Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia‑Pacific | ||

| Middle East And Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the size and growth outlook of the heat pump water heater market to 2031?

The heat pump water heater market size was USD 12.74 billion in 2025 and is projected to reach USD 22.76 billion by 2031 at an 11.92% CAGR.

Which technology segments lead and which grow fastest in the heat pump water heater market?

Air-source leads at 63.22% share in 2025, while ground-source is forecast to be the fastest-growing segment at a 12.43% CAGR through 2031.

How do incentives affect adoption for residential heat pump water heaters?

The Section 25C credit covers 30% of project costs, up to USD 2,000 per year, and IRA rebate programs reduce net outlays, shortening paybacks and supporting conversions.

Which regions show the strongest role in the heat pump water heater market?

Asia-Pacific led with a 44.91% share in 2025, and North America is projected to grow the fastest, at a 12.62% CAGR, through 2031.

Which codes and regulations are shaping the adoption of high-temperature commercial heat pump water heaters?

United States DOE standards for 2029, the European Union F-Gas Regulation 2024/573, and local gas restrictions, including in San Francisco, are driving all-electric options that reach 60°C to 90°C or higher.

How are distribution channels evolving for heat pump water heaters?

B2C remains the larger channel at 63.75% in 2025, while B2B and direct sales are growing faster at a 12.06% CAGR, as buyers value turnkey installation, commissioning, and service bundles.

Page last updated on: