Heat Pump Dryer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.83 Billion |

| Market Size (2031) | USD 7.20 Billion |

| Growth Rate (2026 - 2031) | 8.31% CAGR |

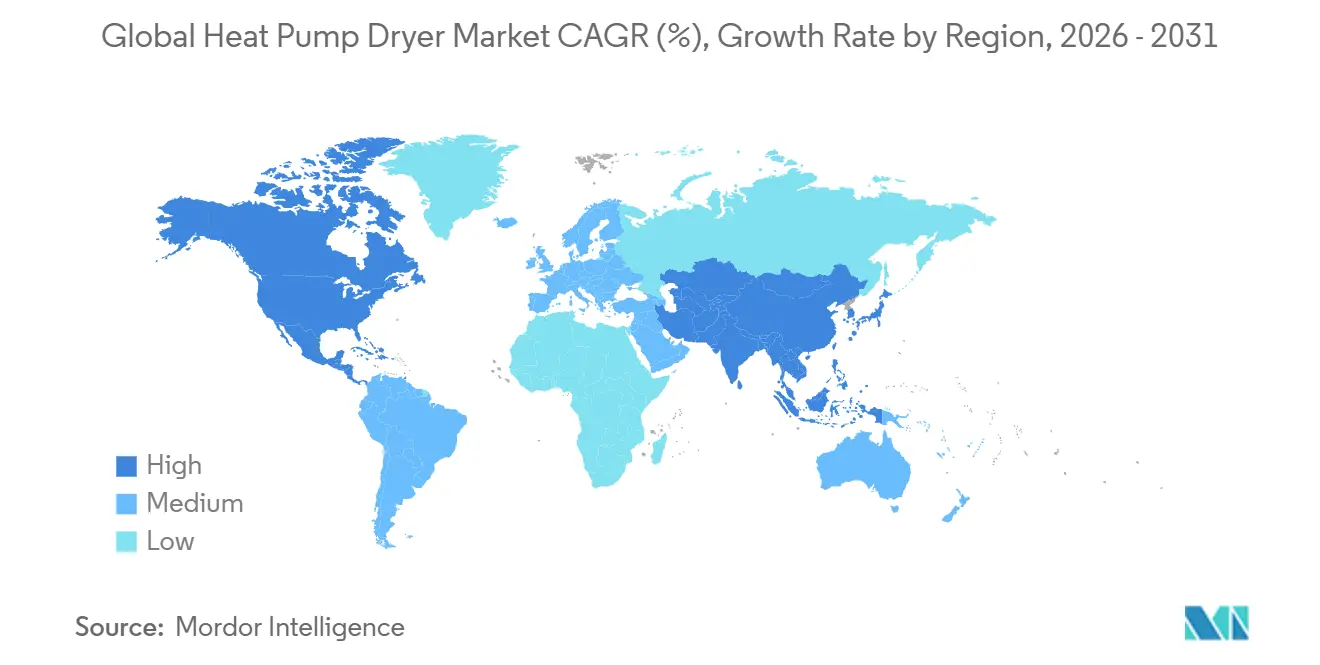

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

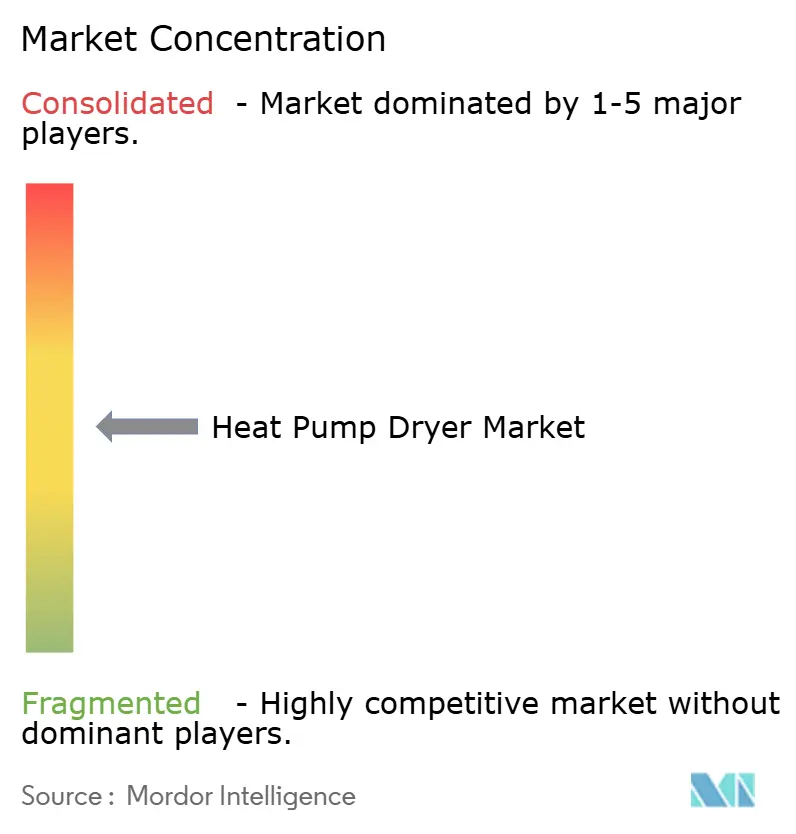

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Heat Pump Dryer Market Analysis by Mordor Intelligence

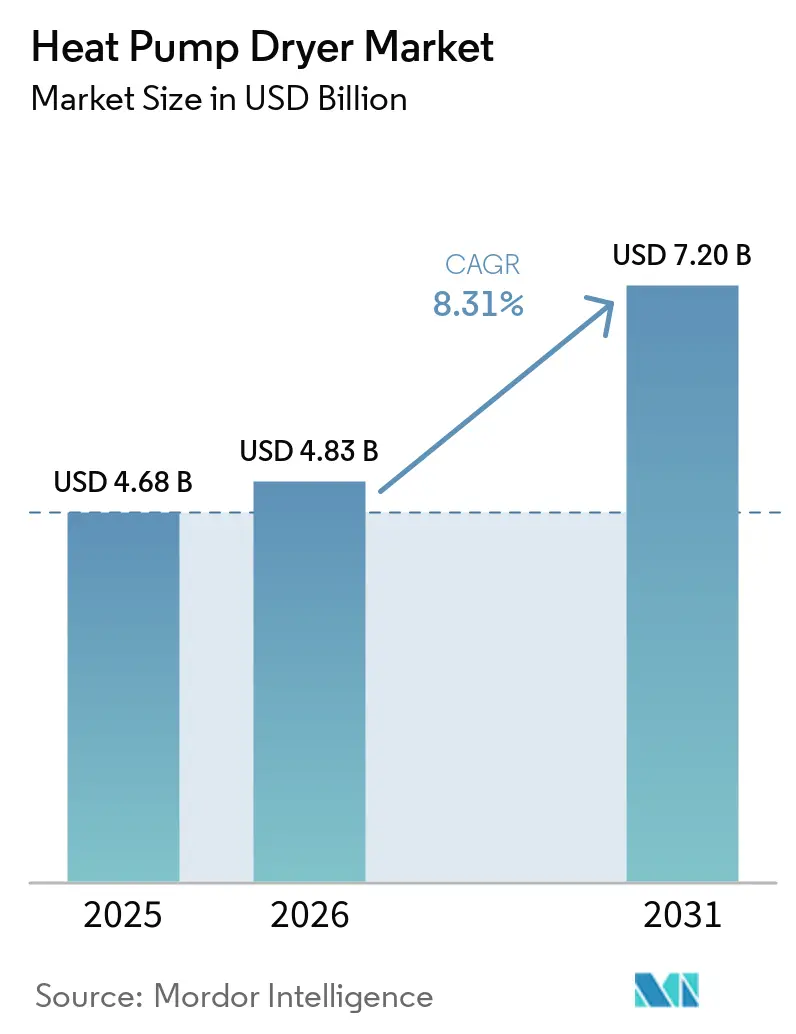

The global heat pump dryer market size is expected to increase from USD 4.68 billion in 2025 to USD 4.83 billion in 2026 and reach USD 7.20 billion by 2031, growing at a CAGR of 8.31% over 2026-2031. The global heat pump dryer market benefits from decisive regulatory shifts that raise efficiency floors and concentrate product development around heat pump technology and closed-loop drying system designs. The global heat pump dryer market also aligns with evolving North American standards, where updated Combined Energy Factor thresholds from March 1, 2028, redirect lagging electric models toward heat pump or hybrid architectures. The global heat pump dryer market is further supported by utility and state-administered rebates that compress payback, particularly where point-of-sale execution removes friction and closes price gaps at checkout. The global heat pump dryer market is also propelled by product innovation, including sensor-based drying with advanced Moisture Sensors, inverter-driven compressors, and adoption of low-GWP refrigerants under updated safety frameworks, which together address historical objections to dry time, noise, and reliability while reinforcing a low carbon footprint.

Key Report Takeaways

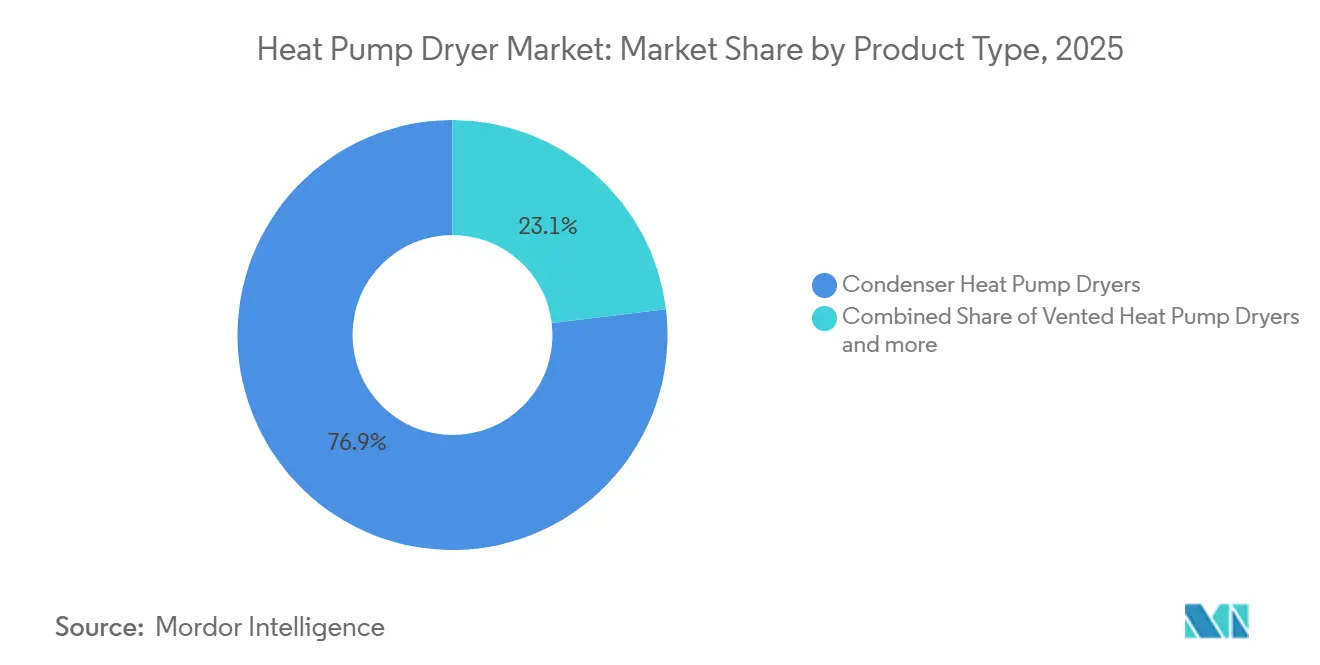

- By product type, condenser heat pump dryers captured 76.91% of the global heat pump dryer market in 2025, whereas integrated (built-in) heat pump dryers are projected to grow at 8.72% CAGR between 2026-2031.

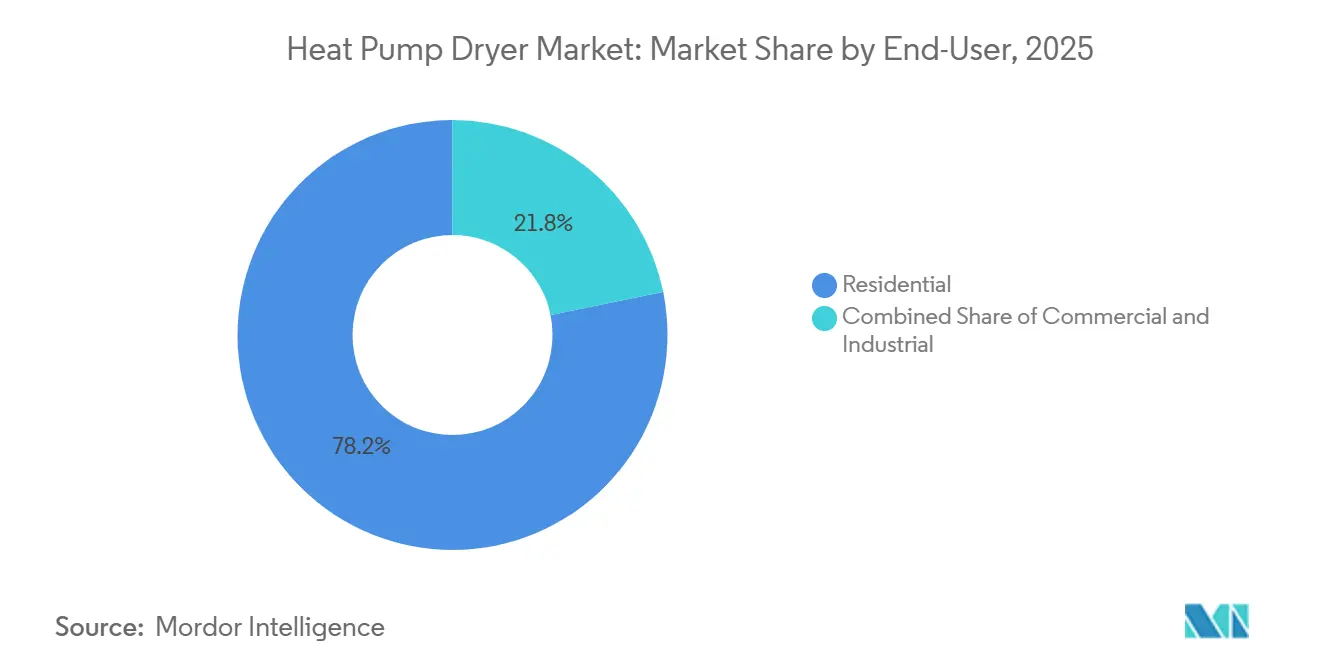

- By end user, residential captured 78.21% of the global heat pump dryer market in 2025, and commercial applications are projected to grow at 8.55% CAGR between 2026-2031.

- By capacity, the 9–10 kg range captured 42.83% of the global heat pump dryer market in 2025 as buyers balanced throughput and Fabric protection in standard alcoves with Ventless convenience; ≥11 kg units are projected to grow at 8.41% CAGR between 2026-2031.

- By distribution channel, B2C/Retail captured 82.58% of the global heat pump dryer market in 2025, reflecting consumer adoption of Energy-efficient dryer options; B2B/Direct Sales is projected to grow at 8.33% CAGR between 2026-2031.

- By region, Europe captured 44.93% of the global heat pump dryer market in 2025 on the back of ecodesign requirements, and the A–G label rescale that favors high-efficiency, closed-loop drying system models; Asia-Pacific is projected to grow at 9.57% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Heat Pump Dryer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Efficiency mandates and labeling accelerate heat-pump adoption | +2.3% | Global, with early gains in EU, Japan, South Korea | Medium term (2-4 years) |

| Utility rebates and incentives shorten payback | +1.8% | North America & EU | Short term (≤ 2 years) |

| Urban multifamily housing constraints favor ventless dryers | +1.5% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| OEM innovation improves cycle time, noise, and reliability | +1.2% | Global | Long term (≥ 4 years) |

| Premium-to-mid price migration expands addressable base | +0.9% | North America, Western Europe, urban APAC | Medium term (2-4 years) |

| Commercial laundry electrification and ESG targets | +0.6% | North America & EU, with expansion to hospitality sectors in MEA/Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Efficiency Mandates and Labeling Accelerate Heat-Pump Adoption

From July 1, 2025, only tumble dryers using heat pump technology may be placed on the EU market, eliminating vented electric and resistance-heated condenser alternatives and channeling R&D toward high-efficiency, closed-loop drying system designs[1]EUROPA.EU https://energy-efficient-products.ec.europa.eu/product-list/tumble-dryers_en. The EU also rescaled labels to an A–G range that preserves the top classes for the most efficient models, resets shopper expectations, and improves signaling at the point of sale across the global heat pump dryer market. In the United States, the Department of Energy’s direct final rule sets a March 1, 2028, compliance date with combined energy factor thresholds that pull lagging standard electric and compact ventless models toward heat pump or hybrid configurations, thereby supporting a low-carbon footprint at fleet scale. ENERGY STAR’s draft version 2.0 specification proposes CEF thresholds above DOE minimums and a cycle time cap, making high-CEF, Energy-efficient dryer platforms the credible path to premium labeling and retailer prominence. Safety standards in IEC 60335-2-11:2024 define requirements for appliances using flammable refrigerants, including detection, tightness, and remote operation provisions, enabling broader use of R290 while protecting household environments in the global heat pump dryer market.

Utility Rebates and Incentives Shorten Payback

Point-of-sale rebates for ENERGY STAR-certified heat pump clothes dryers apply discounts directly at checkout, reducing decision friction and turning long-run savings into immediate price parity for a wide range of households in the global heat pump dryer market. State programs that permit do-it-yourself installation for electric-to-electric replacements expand eligibility and cut labor overhead, speeding adoption of ventless convenience where building conditions allow. Georgia’s program adds a DIY pathway and wiring or panel allowances, which helps households with older electrical infrastructure reach energy-efficient dryer price points after incentives[2]GEORGIA.GOV Home Electrification and Appliance Rebates | Georgia's Home Energy Rebates . Utility rebates from providers like Minnesota Power and DTE Energy stack with federal benefits, raising the combined value and broadening the pool of buyers who can switch to heat pumps without budget tension in the global heat pump dryer market. Multifamily-oriented programs, such as SMUD’s incentives for gas-to-electric conversions, directly target shared laundry rooms and property portfolios, helping institutional owners standardize green technology and reduce operating costs.

Urban Multifamily Housing Constraints Favor Ventless Dryers

Ventless convenience is a practical solution for older buildings and compact apartments that lack adequate duct runs, since a closed-loop drying system does not require exterior venting and can be sited in closets and other tight spaces in the global heat pump dryer market[3]GEAPPLIANCES.COM GE Profile ENERGY STAR 4.8 cu. ft. Capacity UltraFast Combo with Ventless Inverter Heat Pump Technology Washer/Dryer - PFQ97HSPVDS - GE Appliances. Compact 24-inch dryers and washer-dryer combos reduce installation barriers while maintaining useful capacities, and newer platforms operate on common circuits, avoiding panel upgrades in many units. The EU’s ecodesign and energy labeling rules also reward high condensation efficiency and total energy performance, which generally favors condenser heat pump designs over vented setups and supports a low carbon footprint. Appliance declarations from leading brands confirm that A-class outcomes are achievable within standard cabinetry depths, boosting consumer confidence in in-unit upgrades. These siting advantages are central to the global heat pump dryer market in dense urban cores, where building codes and resident preferences converge on in-unit laundry capability.

OEM Innovation Improves Cycle Time, Noise, and Reliability

Advances in sensor-based drying, moisture sensors, and inverter control are closing gaps on dry time, acoustic levels, and service intervals, which sustains momentum across the global heat pump dryer market. Miele’s QuickPowerDry reduces the warm-up phase, so modest loads can complete in under an hour while preserving Fabric protection, addressing legacy objections associated with earlier cycles[4]MIELE.DE Even gentler, faster and more convenient – the new washing machines and tumble dryers from Miele. Multi-sensor arrays from leading brands read fabric temperature and moisture more precisely, then adjust airflow and compressor speeds to reach target dryness with fewer re-runs and shorter total times. Auto-cleaning condensers and layered filtration maintain airflow over time, reduce manual maintenance, and keep energy consumption aligned with label expectations across the product life. Connected diagnostics via SmartHQ and SmartThings shorten mean time to repair by providing fault data to technicians before site visits, sustaining uptime for residential and light commercial users in the global heat pump dryer market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher upfront price versus vented/condenser units | -0.7% | Global, acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Longer average cycle times in certain conditions | -0.5% | National, with resistance in North America and emerging Asia-Pacific | Short term (≤ 2 years) |

| Refrigerant transition (R290) adds redesign/certification burden | -0.4% | EU, North America (phased timelines) | Medium term (2-4 years) |

| Electrical capacity limits in older buildings slow retrofits | -0.3% | Urban cores in North America, select EU markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher Upfront Price Versus Vented/Condenser Units

Initial price premiums versus vented or resistance-heated condenser dryers remain a barrier for cost-sensitive households, even as lifecycle savings and rebates narrow gaps in many regions of the global heat pump dryer market. Point-of-sale rebates and utility incentives that stack with federal programs convert long-term savings into on-receipt discounts for qualifying buyers, which raises the addressable base for Energy-efficient dryer adoption. Commercial buyers also weigh capital budgets and throughput needs against operating savings, which can defer replacements to coordinated budget windows. As more brands deliver value configurations that preserve core efficiency while trimming extras, the premium narrows further, and adoption improves across income tiers in the global heat pump dryer market.

Longer Average Cycle Times in Certain Conditions

Dry times for heat pump dryers can be longer in cool or humid settings, and legacy user expectations can slow adoption, particularly in the global heat pump dryer market, where in-store education is limited. Hybrid drying systems that supplement early warmup and advanced airflow designs are closing this gap, making energy savings and acceptable dry times compatible outcomes. Documented commercial cycles also show that high-efficiency operation can coexist with short turnaround, which improves operator confidence. As sensor-based drying and moisture sensors cut over-drying and re-runs, the actual time difference narrows, and perceived performance improves across the global heat pump dryer market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Condenser Variants Dominate, Integrated Models Gain Premium Traction

Condenser heat pump dryers held 76.91% of the global heat pump dryer market share in 2025, and the segment continues to lead due to a closed-loop drying system that simplifies retrofits and supports ventless convenience in a wide range of dwellings. With heat pump technology now the regulatory baseline in the European Union and the clear premium pathway in North America, leading brands feature auto-cleaning condensers, inverter compressors, and app-connected controls as standard, which aligns with Energy-efficient dryer expectations. Vented heat pump models remain a niche as energy labels and building practices across major regions reward closed-loop efficiency and condensation performance, directing shelf space and incentives toward condenser configurations.

Integrated (built-in) models are the fastest-growing type through 2031. They are projected to grow at a 8.72% CAGR as premium buyers align around sensor-based drying, moisture sensors, and hybrid drying systems that improve performance without compromising aesthetics. The global heat pump dryer market is moving toward portfolio convergence, with condenser and integrated lines sharing compressors, sensors, and control boards, while differentiation centers on finish quality, installation complexity, and acoustic targets. European Union labels set a clear bar, and ENERGY STAR’s proposed criteria refine the United States' premium thresholds, together making efficiency achievements visible at retail and online. As a result, the global heat pump dryer market relies more on user experience, Fabric protection, and lifecycle service capabilities to differentiate beyond core efficiency claims.

By Capacity: Mid-Range Dominates, Large Drums Address North American Bedding

The 9–10 kg bracket captured 42.83% of the global heat pump dryer market in 2025, reflecting the core demand for standard alcove fit, balanced throughput, and fabric protection for typical household loads under ventless convenience. With A–G labeling in the European Union and a rising share of ENERGY STAR-certified products in North America, this capacity range often delivers top performance without imposing space or power burdens, thereby sustaining its central role across the global heat pump dryer market. Compact ≤8 kg dryers and washer dryer combos play a key role in apartments and secondary units where 120V operation and small footprints outweigh maximum capacity. Across sizes, AI controls, and Hybrid Drying Systems are compressing cycles while keeping temperature envelopes gentle, preserving textiles, and increasing real-world satisfaction.

Large-format units rated ≥11 kg are the fastest-growing capacity group, projected to grow at a 8.41% CAGR, as North American households and light commercial users aim to process bulky bedding and high-volume mixed loads without extending total time on task. Inverter speed control reduces the warm-up penalty, and enhanced Moisture Sensors help prevent over-drying even when drum fullness varies, supporting efficiency and fabric protection. The 9–10 kg range remains the center of gravity for the global heat pump dryer market because it pairs top label outcomes with available space constraints, while compact models sustain penetration in buildings that cannot accommodate larger cutouts or power changes. This three-lane capacity structure underpins steady growth in the global heat pump dryer market through 2031.

By End User: Residential Supremacy Faces Commercial Acceleration

Residential users accounted for 78.21% of 2025 demand in the global heat pump dryer market, as buyers converged on Energy-efficient dryer options that lower bills and support a low carbon footprint while adding Ventless convenience for homes without ducts. Code cycles and efficiency programs in major markets are aligning with premium labels and strong consumer education at retail, which creates clear upgrade paths when legacy dryers reach replacement age. Combo formats and compact 120V platforms broaden siting in older housing stock, and connected diagnostics reduce ownership anxiety by shortening time to fix when service is needed. As these factors compound, the global heat pump dryer market remains anchored by residential replacements over the medium term.

Commercial adoption is projected to grow at 8.55% CAGR, driven by laundromats, hospitality, healthcare, and multi-housing portfolios that pursue Energy-efficient dryer fleets to cut operating costs and document emissions progress at scale. Professional cycles that preserve turnaround windows while reducing electricity use by large margins build operator confidence and support Green Technology mandates in property and corporate standards. Utility and municipal incentives written for shared laundry rooms further reduce outlays and help justify portfolio-wide upgrades, which adds recurring volume to the global heat pump dryer market. Together, these dynamics create a balanced outlook where residential strength is complemented by institutional acceleration in the global heat pump dryer market.

By Distribution Channel: Retail Dominates, B2B Gains from Institutional Electrification

B2C/Retail captured 82.58% of 2025 sales in the global heat pump dryer market as big-box retailers, brand outlets, and e-commerce educated buyers on Ventless convenience, Energy-efficient dryer operation, and Fabric protection benefits. Direct-to-consumer platforms reinforce engagement through extended warranties and connected support, and trade-in programs help offset premiums when making replacement decisions. Retail installation services and haul-away simplify logistics for first-time heat pump buyers, improving conversion and satisfaction across the global heat pump dryer market. With point-of-sale rebates active in leading United States states, the retail channel remains the primary funnel through which incentives reach households.

B2B/Direct Sales is projected to grow at 8.33% CAGR across the global heat pump dryer market, supported by multifamily portfolios, hospitality brands, and healthcare systems that embed Green Technology and predictive diagnostics into procurement documents. Commercial-grade platforms reduce electricity use while maintaining operational tempo, improving economics, and helping meet property-level goals. OEM service networks that analyze remote diagnostics and stock parts preemptively help minimize downtime, which sustains confidence for contract renewals and portfolio expansions. Together, these factors expand institutional adoption and diversify revenue streams in the global heat pump dryer market.

Geography Analysis

Europe accounted for 44.93% of global revenues in 2025, underscoring the region’s role as an early mover on ecodesign and labeling rules that direct the product mix of the global heat pump dryer market toward A-class, closed-loop drying System designs. Regulation (European Union) 2023/2533 and the rescaled A–G label, effective July 1, 2025, set explicit floors and clear consumer cues, which lift the share of energy-efficient dryer products on retail floors and e-commerce listings. With standards harmonization under International Electrotechnical Commission (IEC) 60335 2 11:2024 enabling R290 adoption and clarifying detection and tightness requirements, European manufacturers align refrigerant choices with safety while pursuing a low carbon footprint.

Asia-Pacific is the fastest-growing region, with a projected 9.57% CAGR, as policy frameworks and urban housing realities converge on compact, ventless convenience platforms across the global heat pump dryer market. Japan’s TopRunner approach and South Korea’s efficiency schemes continue to push domestic champions to release high-performing, Sensor-Based Drying products, often debuting domestically before wider rollout. Vertical integration in China speeds cost curve improvements and supports broader access to Energy-efficient dryer options, which then influence global pricing and feature expectations. With urban density shaping alcove standards and consumer expectations, capacities in the 7–10 kilogram band coupled with advanced moisture sensors help Asia-Pacific buyers match fabric protection to smaller spaces in the global heat pump dryer market.

North America’s growth path is defined by the harmonization of federal standards by March 1, 2028, expanding availability of 120V and combo platforms, and the execution of stacked incentive programs that bring energy-efficient dryer models to price parity for qualifying households in the global heat pump dryer market. ENERGY STAR’s proposed criteria point premium buyers to high-Combined Energy Factor (CEF) products with cycle time caps, which guides retail stocking and online merchandising. State programs with point-of-sale rebates and DIY options for electric-to-electric swaps increase reach in older housing without full panel work, and compact combos unlock in unit laundry for many apartments. These elements provide durable catalysts for the global heat pump dryer market over the forecast window.

Competitive Landscape

The global heat pump dryer market is shaped by diversified incumbents that invest ahead of regulatory change, localize production where it matters, and differentiate with sensor-based drying, moisture sensors, and connected diagnostics. BSH has highlighted features such as Cool Dry and Air Max Dry, while Bosch integrates self cleaning condenser and the Home Connect platform to reduce maintenance and improve the user experience in the global heat pump dryer market. LG continues to deploy Dual Inverter configurations with Artificial Intelligence (AI) Sensor Dry across multiple capacities, and Samsung scales AI-enabled models tied to SmartThings for remote diagnostics and energy features. Electrolux Professional documents commercial-class savings while maintaining cycle times, which resonates with hospitality and healthcare operators.

Strategic moves include investing in manufacturing footprints in the United States and Mexico to serve the Americas efficiently, in sync with European Union (EU) and US code cycles that raise the floor for Energy-efficient dryer performance in the global heat pump dryer market. Premium warranties signal confidence in inverter motors and compressors, and product roadmaps emphasize Hybrid Drying Systems that compress time while safeguarding garments. Brands also right-size Stock Keeping Unit (SKU) counts to improve supply reliability and scale components across price tiers in the global heat pump dryer market.

Differentiation now balances three pillars across the global heat pump dryer market. First, efficiency beyond compliance, defined by the Combined Energy Factor (CEF) and energy-label outcomes, channels products to premium shelving and rebate eligibility. Second, user experience defined by shorter cycles, lower sound, Fabric protection, and Ventless convenience produces clear, testable claims at retail and in reviews. Third, lifecycle services and predictive diagnostics lower downtime and the cost of ownership, which drive portfolio standardization across residential and institutional customers in the global heat pump dryer market.

Heat Pump Dryer Industry Leaders

BSH Hausgeräte GmbH (Bosch, Siemens)

Electrolux Group (Electrolux, AEG, Zanussi)

Haier Smart Home (Haier, Candy, Hoover, GE Appliances)

Arçelik A.Ş. (Beko, Grundig)

Miele & Cie. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: At CES 2026, LG Electronics introduced its new LG Signature WashCombo washer-dryer featuring advanced heat pump drying technology, highlighting a major innovation in the Heat Pump Dryer Market. The appliance can complete washing and drying cycles in under 90 minutes while reducing energy consumption by more than 70% compared to conventional vented dryers. The launch reflects the growing industry focus on energy-efficient, compact, and AI-enabled laundry solutions, further accelerating the adoption of heat pump dryers in smart home appliances.

- September 2025: Bosch (BSH Hausgeräte) presented new Series 8 heat pump dryers at IFA 2025, combining top-tier energy performance with features like Self Cleaning Condenser and Air Max Dry, linked to Home Connect

- April 2025: Electrolux Professional reported that Line 6000 heat pump dryers reduce electricity consumption by up to 65% while maintaining cycle times comparable to those of conventional dryers in commercial settings.

- February 2025: LG showcased its DUAL Inverter heat pump washer and dryer pair at KBIS 2025, highlighting AI Direct Drive optimization, ventless design, ThinQ integration, and large-capacity premium models for North America.

Global Heat Pump Dryer Market Report Scope

| Condenser Heat Pump Dryers |

| Vented Heat Pump Dryers |

| Integrated (Built-in) Heat Pump Dryers |

| ≤ 8 kg |

| 9–10 kg |

| ≥ 11 kg |

| Residential |

| Commercial (Laundromats, Hospitality, Healthcare, Multi-housing) |

| Industrial (Light-Duty Laundry/Process Where Applicable) |

| B2C/Retail Channels | Multi-brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B/Direct Sales |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East And Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East And Africa |

| By Product Type | Condenser Heat Pump Dryers | |

| Vented Heat Pump Dryers | ||

| Integrated (Built-in) Heat Pump Dryers | ||

| By Capacity | ≤ 8 kg | |

| 9–10 kg | ||

| ≥ 11 kg | ||

| By End User | Residential | |

| Commercial (Laundromats, Hospitality, Healthcare, Multi-housing) | ||

| Industrial (Light-Duty Laundry/Process Where Applicable) | ||

| By Distribution Channel | B2C/Retail Channels | Multi-brand Stores |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Direct Sales | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East And Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the size outlook for the global heat pump dryer market by 2031?

The global heat pump dryer market size is expected to reach USD 7.20 billion by 2031 from USD 4.83 billion in 2026, at an 8.31% CAGR over 2026 2031.

Which segments are set to lead growth through 2031 in the global heat pump dryer market?

Integrated (built-in) models, commercial end uses, and ≥11 kg capacities are the fastest-growing groups based on forecast CAGRs cited in this analysis.

How do regulations shape the global heat pump dryer market roadmap?

EU rules from July 1, 2025 allow only heat pump dryers on the market, and U.S. DOE standards from March 1, 2028 push lagging models toward heat pump or hybrid designs.

Which features most improve user experience in the global heat pump dryer market?

Hybrid drying systems, sensor-based drying, and moisture sensors shorten cycles and prevent over-drying, while connected diagnostics reduce downtime and improve service outcomes.

Where will policy and incentives most influence adoption in the global heat pump dryer market?

Europe provides regulatory certainty via ecodesign and labeling, and North America advances with 2028 standards plus state rebates and DIY paths that improve economics for households and properties.

Which regions contribute most to near-term scaling of the global heat pump dryer market?

Europe holds the largest share with 44.93%, while Asia-Pacific grows fastest having CAGR of 9.57% on compact, Ventless convenience models, and North America expands through 120V innovation and stacked incentives.

Page last updated on: