Heart Transplant Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

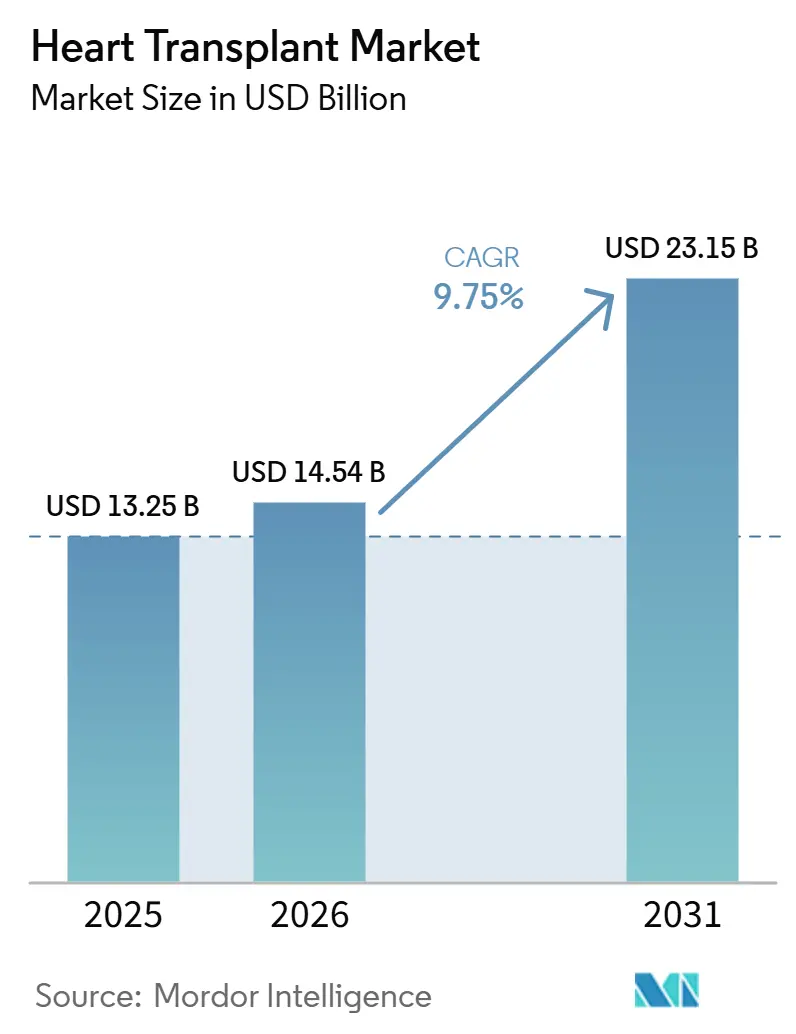

| Market Size (2026) | USD 14.54 Billion |

| Market Size (2031) | USD 23.15 Billion |

| Growth Rate (2026 - 2031) | 9.75% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Heart Transplant Market Analysis by Mordor Intelligence

The Heart Transplant Market size is projected to expand from USD 13.25 billion in 2025 and USD 14.54 billion in 2026 to USD 23.15 billion by 2031, registering a CAGR of 9.75% between 2026 to 2031.

The expansion of the heart transplant market is tied to a larger pool of advanced heart failure patients, with 6.7 million U.S. adults living with heart failure in 2025 and with the total projected to reach 8.7 million by 2030 and 11.4 million by 2050. The heart transplant market is also moving forward because organ preservation methods, bridge-to-transplant support, and donor matching tools are improving how centers use scarce donor hearts. Large transplant programs continue to gain an advantage because reimbursement support, dedicated procurement teams, and standardized protocols make it easier to manage complex cases at scale in the heart transplant market. The same market remains constrained by donor scarcity, with the heart waiting list at 4,037 patients as of March 2026, which keeps growth closely linked to allocation efficiency and preservation capability rather than demand alone. The result is a heart transplant market that is being shaped at the same time by stronger clinical capability, tighter donor supply, and growing concentration at high-output institutions.

Key Report Takeaways

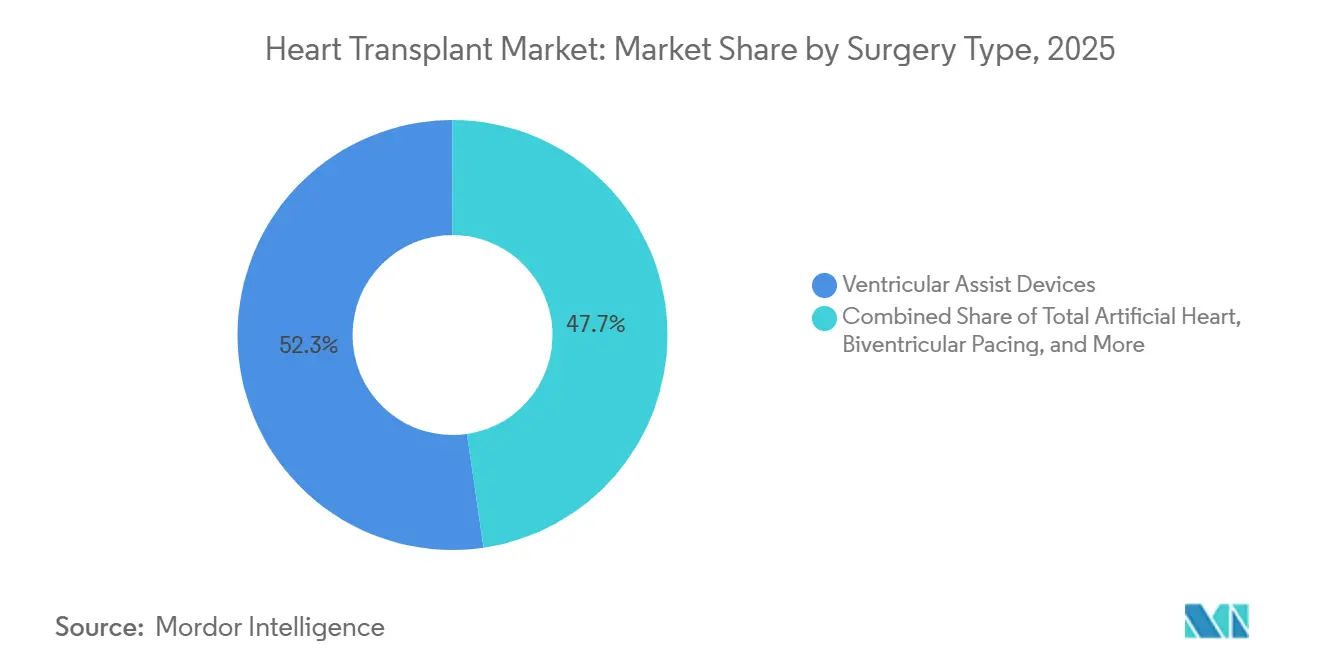

- By surgery type, Ventricular Assist Devices held 52.31% of the heart transplant market share in 2025, while Total Artificial Heart is projected to grow at an 11.38% CAGR through 2031.

- By transplant type, Orthotopic Heart Transplant accounted for 76.24% of the segment in 2025, while Heterotopic Heart Transplant is forecast to expand at a 10.52% CAGR through 2031.

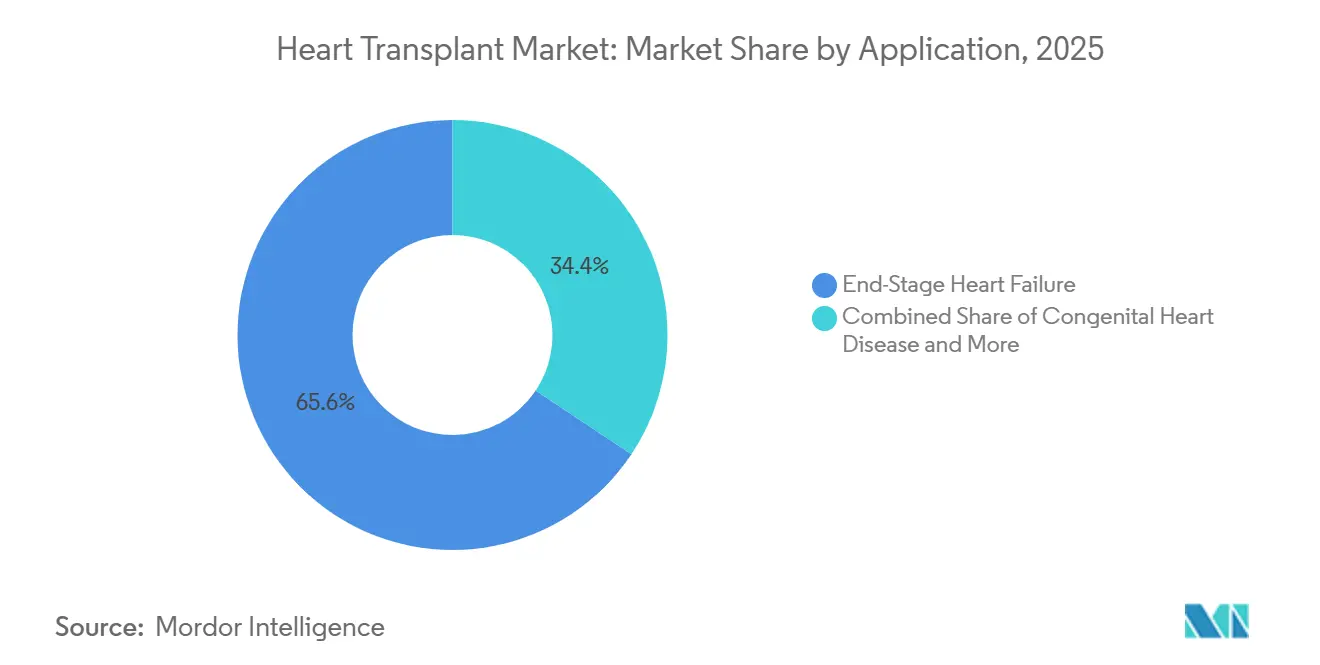

- By application, End-Stage Heart Failure represented 65.64% share of the heart transplant market size in 2025 and is expected to grow at 11.62% CAGR through 2031.

- By end user, Hospitals captured 60.66% of the segment in 2025, while Cardiac Institutes are projected to advance at a 10.95% CAGR through 2031.

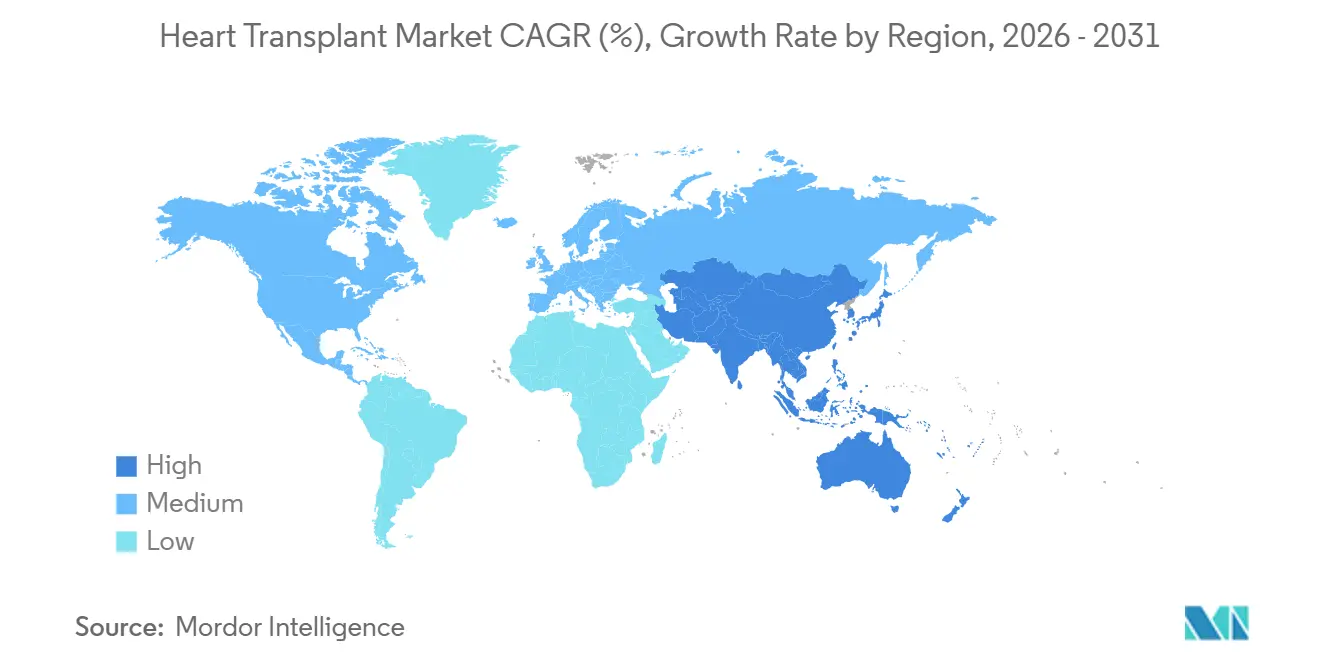

- By geography, North America accounted for 41.61% share of the market size in 2025, while Asia-Pacific is projected to expand at an 10.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Heart Transplant Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising End-Stage Heart Failure Burden | +2.3% | Global, with highest intensity in North America, Europe, and East Asia | Long term (≥ 4 years) |

| Aging Donor and Recipient Pool Complexity | +0.7% | North America and Europe for aging donor pools, APAC for older recipient cohorts | Medium term (2-4 years) |

| Wider Use of Normothermic Perfusion and Ex-Vivo Preservation | +1.6% | North America, Western Europe, early adoption in Australia | Medium term (2-4 years) |

| Greater Adoption of Mechanical Circulatory Support as Bridge-To-Transplant | +1.4% | North America primary, Europe secondary | Medium term (2-4 years) |

| AI-Assisted Donor Matching and Graft Risk Stratification | +1.0% | North America, with early spillover to Europe and APAC | Short term (≤ 2 years) |

| CMS and Private Payer Reimbursement Support for Advanced Cardiac Programs | +0.8% | United States primarily, early-stage parallels in Canada and Germany | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising End-Stage Heart Failure Burden

End-stage heart failure remains the main demand base for the heart transplant market because it is the largest application area and the most persistent source of late-stage patients. Heart failure contributed to 425,147 deaths in the United States in 2022, which represented 45% of all cardiovascular deaths. The patient pool is also changing because prevalence is growing faster in the 20 to 54 age band in middle and high-middle SDI countries, which broadens the future transplant candidate base. Ischemic and hypertensive heart disease together accounted for 57.1% of global heart failure etiology in 2023, so the heart transplant market is still closely tied to the larger cardiovascular disease burden. Programs that manage the full path from advanced medical therapy to mechanical support and then transplant are therefore positioned to capture a larger share of complex patient flow.

Wider Use of Normothermic Perfusion and Ex-Vivo Preservation

The heart transplant market is changing materially because organ preservation is no longer limited to a narrow cold-storage window. TransMedics received full FDA IDE approval in February 2026 for its next-generation OCS ENHANCE Heart trial and also introduced its Controlled Hypothermic Organ Preservation System as the control arm device, which shows that advanced preservation is moving toward a standard point of comparison[1]TransMedics Group, Inc., “TransMedics Receives Full and Unconditional FDA IDE Approval for Next-Generation OCS Heart ENHANCE Trial,” Press Release, investors.transmedics.com. Data presented for the PRESERVE trial at ISHLT 2026 reported 91.4% survival at day 365 and showed that 73.8% of cases exceeded the traditional 4-hour preservation window, which points to a wider usable donor pool when more advanced perfusion is used. The organizational effect is just as important because transplant centers with dedicated organ recovery teams can move faster and with more consistency than those still depending on ad hoc surgical retrieval models. As this shift continues, the heart transplant market should reward centers and suppliers that can link device performance, logistics, and procurement discipline in one operating model.

Greater Adoption of Mechanical Circulatory Support as Bridge-To-Transplant

Mechanical support is now a planned pathway in the heart transplant market rather than a last-resort intervention. A 2025 meta-analysis found 1-year post-transplant survival of 92.7% for temporary LVAD-bridged patients and 86.8% for durable LVAD patients, compared with 71.6% for VA-ECMO bridged patients, which is materially shaping device selection at leading centers. At the same time, durable support is not clinically neutral because LVAD bridging independently predicted higher acute rejection before discharge in a 2024 study, which means outcome planning continues after surgery and into immunosuppression management. Abbott’s HeartMate 3 remains a key reference point because its outcomes have brought long-term mechanical support closer to transplant-level survival in selected cases. This is pushing the heart transplant market toward a more tiered treatment sequence in which mechanical support, donor access, and timing are assessed together instead of in isolation.

AI-Assisted Donor Matching and Graft Risk Stratification

The heart transplant market is also gaining from the early operational use of AI in donor selection and acceptance decisions. A model presented at ISHLT 2025 delivered an AUROC of 0.884 compared with 0.832 for the SRTR baseline in predicting donor heart offer acceptance, which shows measurable improvement over legacy decision support. American Heart Association modeling also found that AI-optimized allocation could deliver a 22.9% gain in life-years if centers stopped refusing viable offers, and a 33.2% gain if geographic radius limits were expanded from 500 to 2,500 nautical miles. Deep learning tools for cardiac volume sizing have already shown value in size matching, particularly in pediatric settings where subjective assessment can introduce error. The practical effect is that the heart transplant market may become more concentrated around high-volume centers that can deploy data infrastructure, validate algorithms, and fold those tools into daily transplant workflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Donor Heart Scarcity | -1.7% | Global, most acute in North America and APAC where waitlists are growing fastest | Long term (≥ 4 years) |

| High Total Episode Cost, Including ICU and Long-Term Immunosuppression | -1.2% | High-income markets with limited cost-sharing mechanisms, South America and MEA most constrained | Medium term (2-4 years) |

| Workforce Bottlenecks in Perfusion, Procurement, and Transplant Surgery | -0.8% | North America, Western Europe, Australia and New Zealand | Medium term (2-4 years) |

| Xenotransplantation and Advanced Preservation Regulatory Uncertainty | -0.5% | Global, with regulatory variance highest across the United States, Europe, and China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Donor Heart Scarcity

The largest structural restraint in the heart transplant market is still the limited supply of donor hearts. The United States completed a record 48,149 organ transplants in 2024, but heart transplant volume was only 4,572, up very little from 4,545 in 2023, while the heart waiting list stood at 4,037 patients in March 2026. Donor quality is also becoming more complex because 48.2% of deceased donors in 2024 were aged 50 or older, which increases the need for better screening and preservation capability. The United Kingdom reported 174 adult heart transplants in 2024 to 2025, with 28% from DCD donors, but total volume still ran 13% below the prior year, which shows that even mature systems do not escape absolute supply limits[2]NHS Blood and Transplant, “Annual Report on Heart Transplantation 2024/2025,” NHSBT, nhsbtdbe.blob.core.windows.net. The heart transplant market therefore remains dependent on better DCD use, stronger preservation systems, and longer-term alternatives such as xenotransplantation before supply can loosen in a meaningful way.

High Total Episode Cost, Including ICU and Long-Term Immunosuppression

The heart transplant market remains exposed to high total treatment cost because care extends well beyond the operating room. Each case combines surgery, ICU care, inpatient recovery, surveillance testing, and long-term immunosuppression, which makes program economics difficult for providers and payers with limited room to absorb full episode costs. This burden slows expansion in geographies where broad reimbursement support is not yet in place and where transplant programs cannot spread fixed costs across large volumes. It also strengthens the role of larger centers because they are better able to manage cost intensity through scale, protocol standardization, and multidisciplinary follow-up. As a result, the heart transplant market may continue to add capacity unevenly even when clinical demand is strong.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Surgery Type: Total Artificial Heart Gaining Ground on VAD Dominance

Ventricular Assist Devices held 52.31% of the segment in 2025, which kept them in the leading position within the heart transplant market by surgery type. Their lead reflects their role as both a bridge-to-transplant option and, in selected cases, a durable therapy when a donor heart is not immediately available. Abbott’s HeartMate 3 remains central to this position because the HM3 SWIFT study supported thoracotomy as a non-inferior implant pathway, which widens use across different surgical settings. The current balance in this part of the heart transplant market favors VADs because they fit established workflows, clinician familiarity, and post-implant care models. This gives suppliers in the VAD category a stable base even as the technology mix becomes more competitive.

Total Artificial Heart is projected to grow at an 11.38% CAGR through 2031, making it the fastest-moving surgery type in the heart transplant market. That pace reflects demand for an option that reduces direct reliance on donor availability in patients with severe biventricular failure. A 10-year clinical study cited in the 2026 FACS Bulletin found that 79% of SynCardia TAH patients survived to transplantation compared with 46% on alternative bridging, which supports the category’s value where LVAD use is limited or contraindicated[3]American College of Surgeons Bulletin, “With ‘Real Momentum,’ Total Artificial Heart Technology Faces Defining Chapter,” FACS Bulletin, facs.org. Biventricular pacing and other surgery types still serve narrower clinical needs, and they are likely to remain secondary revenue contributors rather than major share challengers. Over time, the surgery type mix in the heart transplant market should move toward a stronger VAD and TAH pairing, with one anchored in mature adoption and the other lifted by unmet need.

By Transplant Type: Orthotopic Procedures Lead but Heterotopic is Reappraised

Orthotopic Heart Transplant commanded 76.24% of the segment in 2025, which made it the clear procedural standard in the heart transplant market by transplant type. Its leadership rests on long-standing clinical practice, broader surgeon familiarity, and strong registry visibility across mature transplant systems. A retrospective cohort analysis of 1,205 recipients through December 2024 reported 1-year adult survival of 85% under a standardized institutional orthotopic protocol, which reinforces the role of protocol discipline in sustaining outcomes. This keeps Orthotopic Heart Transplant at the center of program design, payer coverage decisions, and training models. It also means that most preservation and allocation improvements still flow first into orthotopic workflows.

Heterotopic Heart Transplant is projected to expand at a 10.52% CAGR through 2031, which makes it the faster-growing transplant type in the heart transplant market. Its growth comes from use in patients with severe pulmonary hypertension or marked donor-recipient size mismatch, where orthotopic procedures may carry higher early risk. Research published in 2024 found that heterotopic survival was statistically indistinguishable from orthotopic survival during the first 4 years after transplant in properly selected patients, which has supported a more favorable clinical view of the procedure. This change does not displace orthotopic leadership, but it does widen the clinical use case for programs that treat complex recipients. In turn, the heart transplant market gains an additional route for procedure growth in cases that might otherwise remain unserved.

By Application: End-Stage Heart Failure Sustains Dual Lead Position

End-Stage Heart Failure accounted for 65.64% of the segment in 2025 and is projected to grow at an 11.62% CAGR through 2031, which means it led both current scale and future expansion in the heart transplant market. It is the only application in which the largest share and the fastest growth rate sit in the same category. That dual lead reflects the severity and volume of advanced heart failure cases that continue to move through optimization, mechanical support, and eventual transplant consideration. The heart transplant market size for End-Stage Heart Failure remains the clearest indicator of how upstream cardiovascular burden converts into transplant demand. HFSA also projects that U.S. heart failure costs could reach USD 142 billion by 2050, which reinforces why providers and payers are building capacity around this application first.

Congenital Heart Disease remains a smaller application, but it carries distinct management complexity and a different outcome profile. OPTN and SRTR data for 2023 showed that adults with congenital heart disease had the lowest pretransplant mortality but also the lowest 5-year posttransplant survival at 76.1%, which points to a need for more tailored follow-up and protocol design. Other Cardiac Conditions, including ischemic cardiomyopathy, valvular disease, and retransplantation, continue to add incremental procedure volume across the heart transplant market. These cases benefit from the same preservation and bridging improvements, but they do not set the pace of demand in the way advanced heart failure does. Their role is important, though, because they broaden center case mix and help keep transplant programs clinically diversified.

By End User: Hospitals Dominant, Cardiac Institutes Accelerating

Hospitals captured 60.66% of the segment in 2025, which kept them in the leading end-user position across the heart transplant market. Their lead comes from the fact that tertiary hospitals can combine evaluation, surgery, ICU support, inpatient recovery, and long-term management under one institutional structure. This setup is especially important in a treatment pathway that depends on multidisciplinary care, rapid escalation, and complication management. The heart transplant market share held by hospitals also reflects their ability to handle high-acuity volume with established infrastructure and broader payer relationships. In most mature systems, hospitals remain the main entry point for listed transplant candidates.

Cardiac Institutes are projected to grow at a 10.95% CAGR through 2031, making them the fastest-growing end user in the heart transplant market. Their appeal rests on focused specialization, center-of-excellence positioning, and tighter integration of device use, candidate selection, and transplant follow-up. These institutes often adopt AI-assisted matching tools, novel bridge protocols, and new implant techniques earlier than broader hospital networks, which gives them a faster learning curve in selected high-complexity cases. The result is stronger momentum in settings where concentrated expertise can lower per-case complication risk and improve workflow consistency. This makes Cardiac Institutes especially relevant in regions that are centralizing transplant services around fewer, larger specialist centers.

Geography Analysis

North America held 41.61% of the global segment in 2025, which gave it the leading regional position in the heart transplant market. The United States remained the main driver because it performed 4,572 heart transplants in 2024 under OPTN oversight, supported by a large clinical base and established reimbursement channels. CMS also reinforced high-acuity transplant economics when the FY2026 Final IPPS Rule set the MS-DRG 001 reimbursement rate for heart transplant with MCC at USD 203,923. This framework continues to favor large academic centers that can manage donor logistics, advanced preservation, and complex post-operative care at scale. The heart transplant market size in North America remains strongly linked to U.S. procedure volume, infrastructure depth, and device adoption patterns.

Asia-Pacific is projected to expand at a 10.65% CAGR through 2031, making it the fastest-growing geography in the heart transplant market. China, Japan, and India remain the main growth anchors because each is scaling capacity from a different starting point. China is expanding hospital capability and specialist training, though transparent regulated volume data remain limited. Japan continues to face tight donor availability under its organ donation framework, which keeps interest high in alternative bridge strategies and highly specialized center models. India is seeing steady activity growth through large private cardiac hospitals and improved deceased donor procurement pathways, which makes the region an important future demand center in the heart transplant market.

Europe remains a major transplant base, led by Germany, France, the United Kingdom, and Spain. Cross-border coordination through Eurotransplant supports better organ sharing for member systems, while national performance still depends on domestic donor supply and program efficiency. The United Kingdom reported 174 adult heart transplants in 2024 to 2025, with 28% from DCD donors and a 90-day survival rate of 92.9%, which shows strong protocol maturity in DCD and NRP use. South America, the Middle East, and Africa remain more supply constrained, but they are still investing in capability and should add volume from lower current bases over time. The heart transplant market in these regions will depend heavily on donor system development, reimbursement support, and trained workforce growth.

Competitive Landscape

The heart transplant market shows moderate concentration at the device and technology level because a limited group of manufacturers leads the most important product categories while transplant procedures themselves are increasingly centered in high-output institutions. Abbott remains a key leader in VADs through HeartMate 3, and TransMedics holds a strong position in organ preservation through the OCS Heart platform. Competitive advantage in the heart transplant market is built less on broad product catalogs and more on evidence generation, workflow fit, and center relationships. Companies that can support procurement, implantation, and post-transplant coordination are gaining more durable positions than those offering stand-alone products. This keeps competition focused on a smaller number of high-impact technologies.

One of the clearest strategic moves came from TransMedics in February 2026, when it received full FDA IDE approval for the next-generation OCS ENHANCE Heart trial and introduced CHOPS as a control arm device. That move matters because it strengthens the company’s role not only in commercial supply but also in the clinical evidence pathway that can shape future standard practice. Abbott’s position has also been reinforced by published evidence for HeartMate 3 across different implant approaches, which helps defend its relevance as the heart transplant market keeps leaning on bridge-to-transplant therapy. A third important move came from United Therapeutics, which received FDA clearance to proceed with the EXPRESS clinical study for its 10-gene-edit UHeart xenotransplantation program. Although commercial use is still distant, the move introduces a longer-term challenge to a donor-limited market structure.

A further layer of competition is emerging in software and clinical decision support. AI-assisted donor matching and graft risk tools are not yet fully monetized by one clear leader, but they are becoming more important as centers seek fewer organ declines and better recipient fit. The 2026 ISHLT consensus statement on clinical cardiac xenotransplantation also helps by giving the field a more structured clinical framework, which could reduce some of the regulatory uncertainty around next-generation transplant models. Even so, near-term competition in the heart transplant market will remain grounded in today’s donor-based transplant ecosystem rather than in future replacement models. That keeps incumbents in a strong position, but it also leaves room for targeted disruption.

Heart Transplant Industry Leaders

Abbott Laboratories

TransMedics, Inc.

Medtronic plc

Getinge AB

SynCardia Systems, LLC (Picard Medical, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Picard Medical/SynCardia completed a successful series of acute in-vivo implant studies for the Emperor Total Artificial Heart at the University of Arizona and Banner University Medical Center. The achievement moved its next-generation, fully implantable platform closer to regulatory submission. The platform is designed to provide long-term circulatory support without external pneumatic drivers.

- April 2026: Supira Medical Inc. announced that the FDA approved the start of the SUPPORT II pivotal trial for its Supira percutaneous ventricular assist device (pVAD) system. The company noted that the Supira system remains an investigational device and is not approved for sale in the United States or anywhere else in the world.

Global Heart Transplant Market Report Scope

As per the scope of the report, the heart transplant market refers to the industry involved in the production, distribution, and clinical application of heart transplantation procedures and related medical devices. It encompasses the global demand for heart transplants, the supply of donor hearts, advancements in surgical techniques, and supporting technologies aimed at treating end-stage heart failure.

The heart transplant market is segmented by surgery type into total artificial heart, ventricular assist devices, biventricular pacing, and other surgery types; by transplant type into orthotopic heart transplant and heterotopic heart transplant; by application into end-stage heart failure, congenital heart disease, and other cardiac conditions; by end user into hospitals and specialty clinics, cardiac institutes, transplant centers, and other end users; and by geography into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Total Artificial Heart |

| Ventricular Assist Devices |

| Biventricular Pacing |

| Other Surgery Types |

| Orthotopic Heart Transplant |

| Heterotopic Heart Transplant |

| End-Stage Heart Failure |

| Congenital Heart Disease |

| Other Cardiac Conditions |

| Hospitals and Specialty Clinics |

| Cardiac Institutes |

| Transplant Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Surgery Type | Total Artificial Heart | |

| Ventricular Assist Devices | ||

| Biventricular Pacing | ||

| Other Surgery Types | ||

| By Transplant Type | Orthotopic Heart Transplant | |

| Heterotopic Heart Transplant | ||

| By Application | End-Stage Heart Failure | |

| Congenital Heart Disease | ||

| Other Cardiac Conditions | ||

| By End User | Hospitals and Specialty Clinics | |

| Cardiac Institutes | ||

| Transplant Centers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and forecast for the heart transplant market?

The heart transplant market was valued at USD 13.25 billion in 2025 and is forecast to reach USD 23.15 billion by 2031 at a 9.75% CAGR.

What is the main factor driving demand for heart transplant procedures?

The largest demand driver is end-stage heart failure, which held 65.64% of application share in 2025 and is projected to grow at an 11.62% CAGR through 2031.

Which surgery type leads today, and which one is growing fastest?

Ventricular Assist Devices led with 52.31% share in 2025, while Total Artificial Heart is the fastest-growing surgery type at an 11.38% CAGR through 2031.

Which region leads the global landscape?

North America led with 41.61% share in 2025, supported by U.S. transplant volume, reimbursement support, and strong device adoption.

Why is donor scarcity still a major issue?

The waitlist remained at 4,037 heart patients in March 2026, while donor heart availability grew much more slowly than clinical need, which keeps supply tight.

How are technology changes affecting competition?

Advanced perfusion, bridge-to-transplant devices, and AI-based donor matching are shifting advantage toward companies and centers that can combine evidence, workflow integration, and scale.

Page last updated on: