Healthcare UV Disinfection Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.31 Billion |

| Market Size (2031) | USD 2.31 Billion |

| Growth Rate (2026 - 2031) | 12.05% CAGR |

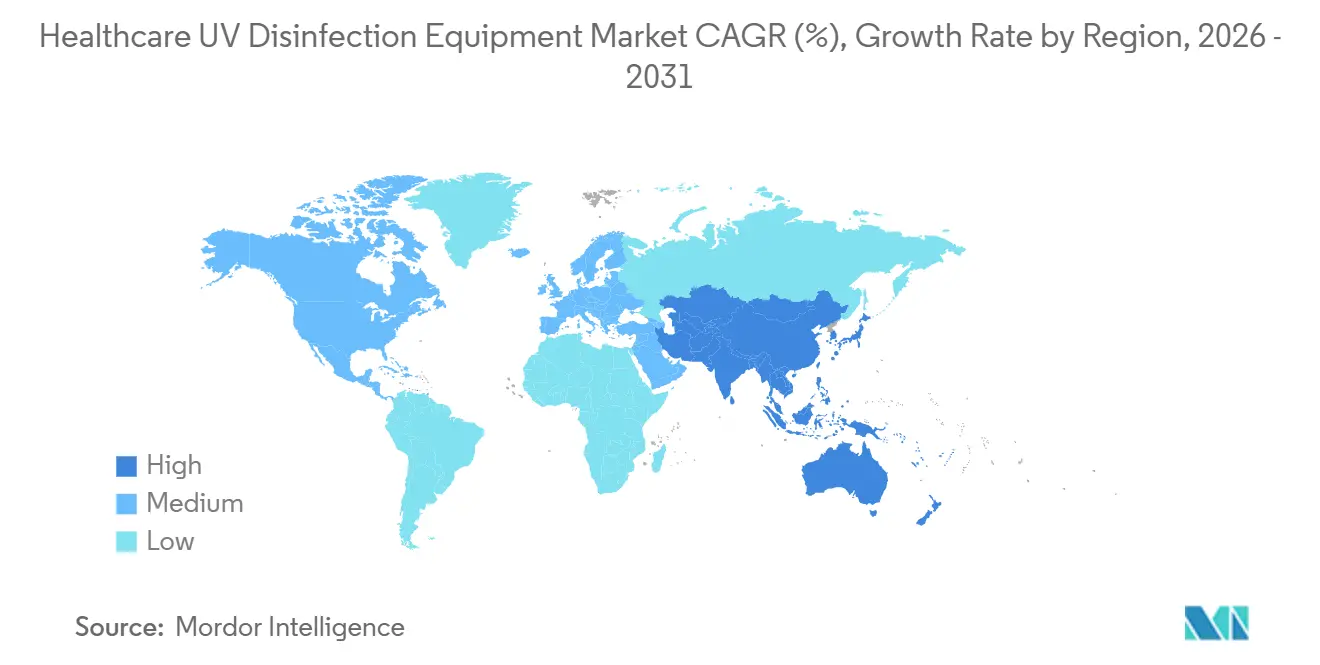

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare UV Disinfection Equipment Market Analysis by Mordor Intelligence

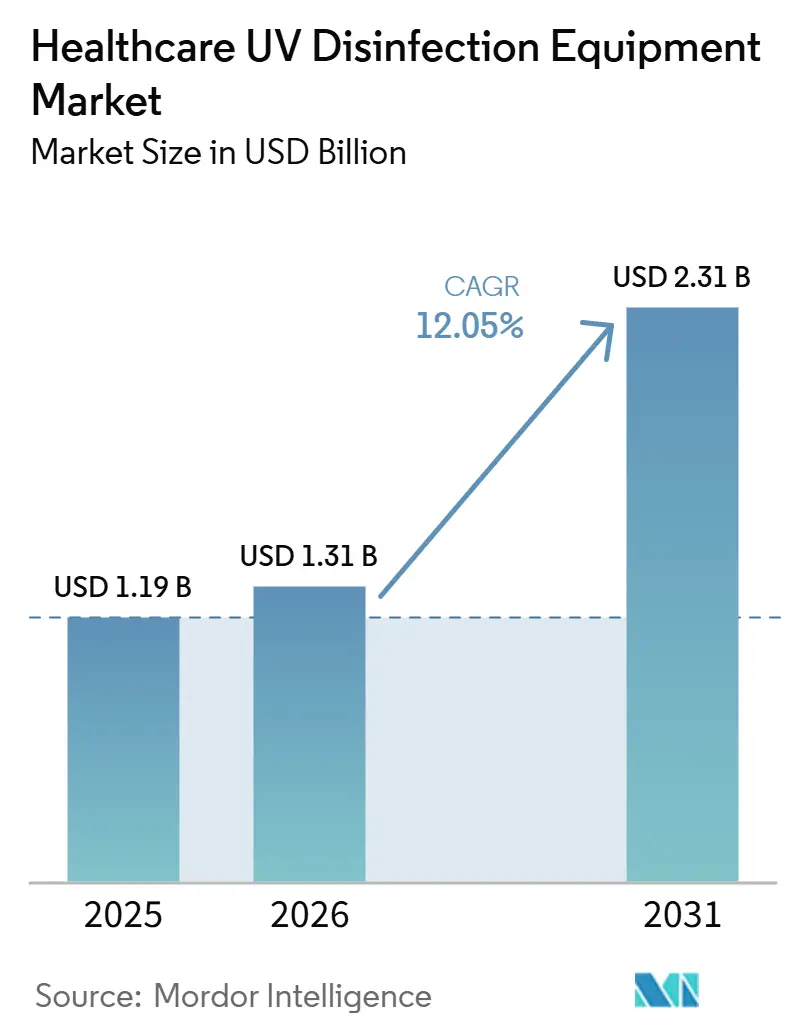

The healthcare UV disinfection equipment market is expected to increase from USD 1.19 billion in 2025 to USD 1.31 billion in 2026 and reach USD 2.31 billion by 2031, growing at a CAGR of 12.05% over 2026-2031. Demand remains tied to the ongoing burden of healthcare-associated infections, with the CDC reporting that 1 in 31 U.S. hospital patients had at least 1 healthcare-associated infection on any given day in 2024. The healthcare UV disinfection equipment market is also being shaped by procurement standards, validation needs, and product performance expectations high across the supplier base. Technology adoption is moving from legacy mercury systems toward LED-based platforms as energy efficiency improves and mercury rules tighten, with Stanley Electric reporting 7.5% wall-plug efficiency for 265 nm UV-C LEDs in March 2026 and mass production planned from October 2026. The healthcare UV disinfection equipment market is also widening through stronger adoption in operating rooms and long-term care settings, where recent clinical studies have shown meaningful reductions in contamination and infection events under far-UVC deployment. Asia-Pacific is the fastest-growing region at 15.3% through 2031, while vendor strategy still has to account for shadowing limits in complex rooms, certification costs, and concentration in deep-UV component supply.

Key Report Takeaways

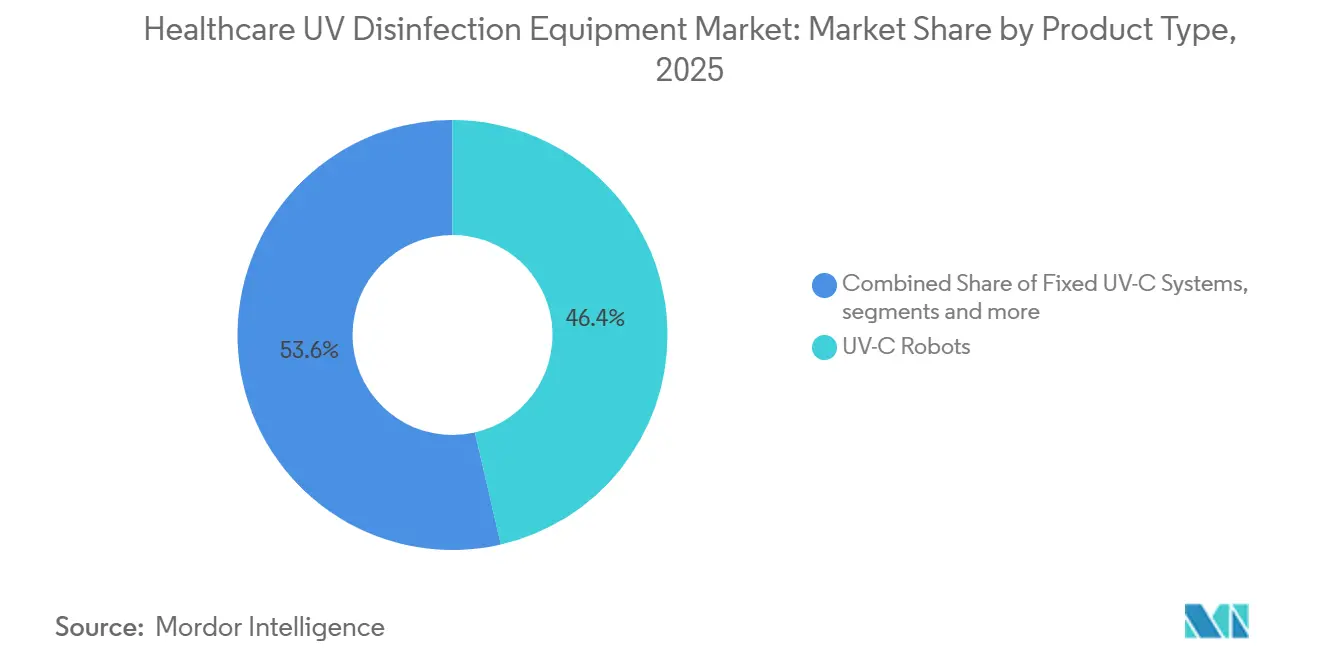

- By product type, UV-C robots led with 46.38% of the healthcare UV disinfection equipment market share in 2025, while handheld UV-C devices are forecasted to grow at 12.62% CAGR through 2031.

- By technology, low-pressure mercury lamp-based systems accounted for 49.72% of the healthcare UV disinfection equipment market size in 2025, while UV-C LED systems are projected to expand at 14.18% CAGR through 2031.

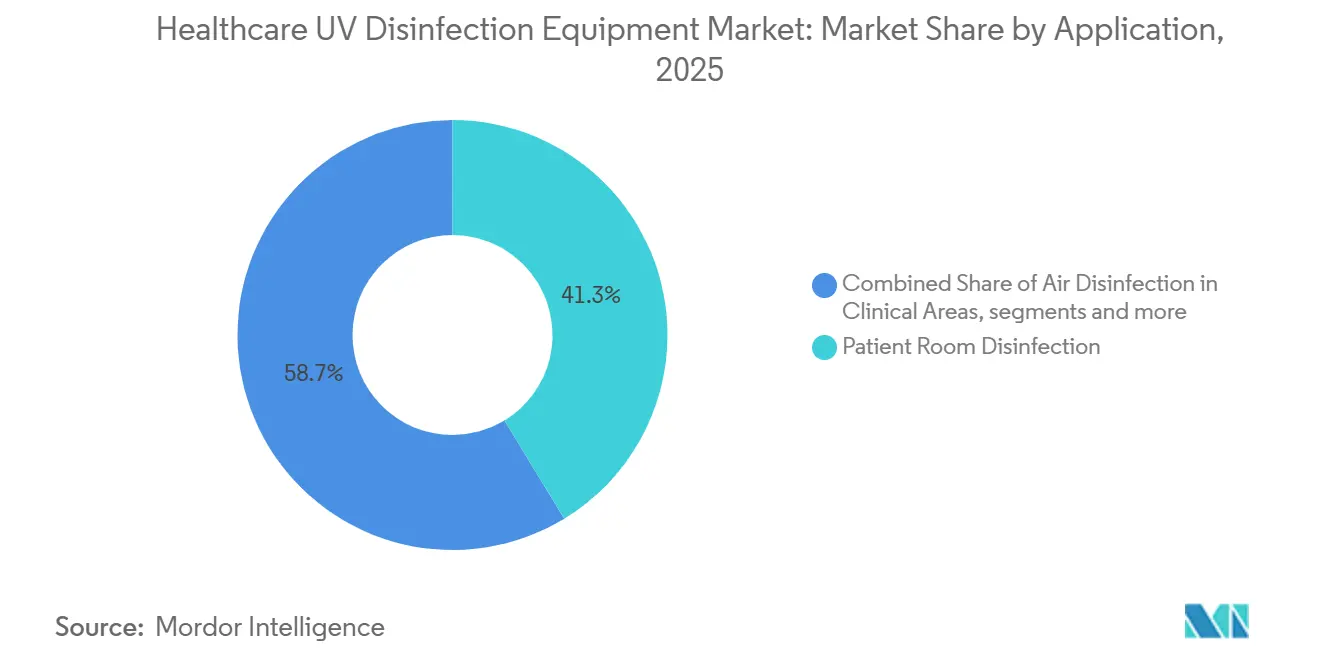

- By application, patient room disinfection held 41.26% of the healthcare UV disinfection equipment market size in 2025, while operating room sterilization is expected to advance at 14.74% CAGR through 2031.

- By end-user, hospitals captured 52.84% of the healthcare UV disinfection equipment market size in 2025, while long-term care facilities are forecasted to grow at 13.96% CAGR through 2031.

- By geography, North America held 42.19% of the healthcare UV disinfection equipment market share in 2025, while Asia-Pacific is projected to expand at 15.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare UV Disinfection Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Healthcare-Associated Infection Pressure in High-Acuity Care | +3.2% | Global, with highest intensity in North America and Europe | Short term (≤ 2 years) |

| Shift Toward Continuous, Chemical-Free Disinfection in Occupied Spaces | +2.5% | Global, adoption led by North America and Western Europe | Medium term (2-4 years) |

| Expansion Of UV-C Use Beyond Terminal Cleaning into Air, Surfaces, And Devices | +1.8% | North America, Europe, APAC core markets | Medium term (2-4 years) |

| Retrofit Demand from HVAC And Upper-Air Infection-Control Upgrades | +1.0% | North America and EU, with spillover to GCC and APAC | Medium term (2-4 years) |

| Declining UV-C LED Costs and Improved Energy Efficiency | +2.0% | Global, with concentrated gains in APAC manufacturing hubs | Long term (≥ 4 years) |

| Need For Audit-Ready Disinfection Traceability in Regulated Facilities | +0.7% | North America, EU, APAC early adopters including Japan and South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Healthcare-Associated Infection Pressure in High-Acuity Care

The healthcare UV disinfection equipment market continues to draw its strongest support from the persistence of healthcare-associated infections in hospital settings. The CDC’s 2024 national report, published in January 2026, showed a 11% decline in hospital-onset C. difficile and a 7% decline in MRSA bacteremia versus 2023, which confirms that infection control remains a central operating priority for providers.[1]Centers for Disease Control and Prevention, “2024 National and State Healthcare-Associated Infections Progress Report,” CDC, cdc.gov The same report also showed that abdominal hysterectomy surgical site infections increased 8% in 2024, which suggests that important gaps remain despite broader progress in other infection categories. Global infection pressure remains large as industry association data cited a WHO estimate that 10% of hospitalized patients acquire a healthcare-associated infection, while antimicrobial resistance is linked to 136 million related cases each year.[2]ISSA, “Global HAI Data 2025, Trends, Risks, and the Role of Training,” ISSA, issa.com In this setting, the healthcare UV disinfection equipment market benefits because UV-C systems address pathogens without adding chemical residue or antimicrobial resistance pressure. That is why purchasing teams increasingly view these devices as part of baseline infection control capacity rather than as an optional add-on.

Shift Toward Continuous, Chemical-Free Disinfection in Occupied Spaces

The healthcare UV disinfection equipment market is also gaining from the move away from periodic room shutdowns toward continuous germ control in occupied spaces. A 2025 study in Infection Control & Hospital Epidemiology found that ceiling-mounted far-UVC fixtures reduced surface bioburden in occupied clinical areas even during routine staff and patient activity.[3]Emilie Hage Mogensen et al., “Ceiling-Mounted Far-UVC Fixtures Reduce the Surface Bioburden in Occupied Clinical Areas,” Infection Control & Hospital Epidemiology, doi.org The healthcare UV disinfection equipment market therefore has room to grow in wards, laboratories, and care areas where steady occupancy makes manual disinfection harder to repeat at the needed frequency. A 2025 installation in a Swedish palliative care ward also reported staff sick leave of 0.4% compared with a regional average near 6%, which is helping far-UVC enter more operational conversations beyond intensive care settings.

Expansion of UV-C Use Beyond Terminal Cleaning into Air, Surfaces, and Devices

The healthcare UV disinfection equipment market is expanding because UV-C is no longer limited to end-of-day terminal cleaning. Air disinfection is also becoming a stronger use case, with a 2025 study in a 24-chair dental clinic showing that 222 nm far-UVC reduced culturable airborne bacteria by 39.5% in an occupied setting. Device and instrument decontamination is entering a more formal product path as well, with the FDA clearing the UV Smart D60 in December 2025 under the classification for ultraviolet radiation disinfection chamber devices. This broadening use pattern matters because each hospital relationship can now involve rooms, air systems, handheld tools, and chamber devices instead of a single equipment category. The healthcare UV disinfection equipment market is therefore gaining depth as well as breadth.

Declining UV-C LED Costs and Improved Energy Efficiency

The healthcare UV disinfection equipment market is moving through a real technology shift as UV-C LED performance improves and compliance pressure rises on mercury systems. Stanley Electric announced in March 2026 that it achieved 7.5% wall-plug efficiency at 265 nm, with product lifetime extended to 25,000 hours from 10,000 hours and mass production planned from October 2026. At the same time, the EU mercury framework and the review of the RoHS exemption for UV-spectrum mercury lamps are making replacement planning more urgent across healthcare installations in Europe. The healthcare UV disinfection equipment market is likely to see this pressure translate into replacement demand rather than just incremental new-build demand. That creates a clear opening for vendors that already have validated mercury-free alternatives and can support healthcare buyers through migration planning.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Line-of-Sight Limitations in Cluttered Clinical Rooms | -1.4% | Global, with the strongest effect in dense-equipment environments such as operating rooms and intensive care units | Short term (≤ 2 years) |

| Safety, Certification, and Operator Exposure Constraints | -0.8% | North America and EU, with spillover to APAC as regulations tighten | Medium term (2-4 years) |

| High Capex and Service Burden for Hospital-Grade Systems | -1.1% | Global, with the strongest effect in cost-sensitive markets such as South America and Southeast Asia | Long term (≥ 4 years) |

| Supply Concentration in Deep-UV Components and Replacement Parts | -0.6% | Global supply chain, with primary production concentrated in East Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Line-of-Sight Limitations that Reduce Efficacy in Cluttered Clinical Rooms

The healthcare UV disinfection equipment market still faces a basic performance challenge in rooms with dense equipment and irregular surfaces. Intensive care units, operating rooms, and medication spaces often create shadowed areas that receive a weaker dose than exposed surfaces. The healthcare UV disinfection equipment market therefore still depends on multi-position cycles, added emitters, or better room mapping to close the gap between dose delivery and real-world room geometry. Until those features become more consistent across products, hospitals will continue to scrutinize claims around whole-room effectiveness.

High Capex and Service Burden for Hospital-Grade Systems

The healthcare UV disinfection equipment market also faces slower adoption where buyers need clear proof that performance gains justify the full ownership cost. Large hospital systems can absorb higher equipment and validation spending more easily than ambulatory surgical centers or long-term care operators. The healthcare UV disinfection equipment market also remains sensitive to service concentration when suppliers control maintenance, consumables, and software support within the same contract structure. Buyers want stronger leverage over lifecycle costs, especially when infection control budgets compete with broader facility modernization needs. Subscription models and service-based pricing are starting to appear, but they remain early and do not yet remove the cost barrier across the full provider base.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: UV-C Robots Lead While Handheld Devices Expand Access

UV-C robots held 46.38% of the product type segment in 2025, which made them the largest category in the healthcare UV disinfection equipment market. Their position reflects strong adoption in high-acuity facilities that want autonomous, dose-verified room disinfection with limited dependence on manual technique. Hospitals also favor these systems where patient turnover is high and infection prevention teams need repeatable workflows. The healthcare UV disinfection equipment industry therefore treats robotic platforms as the core reference category for large-site procurement.

Handheld UV-C devices are forecasted to grow at 12.62% CAGR through 2031, which makes them the fastest-rising product format in the healthcare UV disinfection equipment market. A 2025 genomic analysis also reported mean colony-forming unit reductions of 53% to 83% across armchairs, keyboards, and workroom surfaces with a far-UVC handheld device. Their flexibility matters because staff can target shadowed or irregular surfaces that room robots may not fully address. That makes handheld tools a complement to robots instead of a simple low-cost substitute.

By Technology: Mercury Systems Still Leads While LED Platforms Gain Momentum

Low-pressure mercury lamp-based systems retained 49.72% of the technology segment in 2025, which means they still represented the largest installed technology base in the healthcare UV disinfection equipment market. Their position reflects long-standing use in hospital UV-C deployments and familiar germicidal performance at 254 nm. These systems remain embedded in procurement cycles because many facilities already understand their operating profile and replacement needs. The healthcare UV disinfection equipment market therefore still carries a large installed-base effect that favors existing mercury platforms in the near term.

UV-C LED systems are projected to grow at 14.18% CAGR through 2031, which makes them the fastest-growing technology in the healthcare UV disinfection equipment market. Far-UVC systems at 222 nm add another layer of change because they can be used in occupied spaces under clinical conditions now being tested more widely. As a result, the technology shift is being driven by both component progress and a broader change in how facilities want to apply UV disinfection.

By Application: Patient Rooms Anchor Revenue While Operating Rooms Grow Faster

Patient room disinfection held 41.26% of the application segment in 2025, giving it the largest share of the healthcare UV disinfection equipment market. The segment benefits from the volume of room turnover in acute care and the ongoing attention on transmission pathways linked to inpatient surfaces and shared equipment. Patient rooms remain the base case for adoption because they combine heavy usage, clear cleaning workflows, and measurable infection prevention targets.

Operating room sterilization is projected to grow at 14.74% CAGR through 2031, which makes it the fastest-growing application in the healthcare UV disinfection equipment market. Air disinfection is also gaining support, with a 2025 systematic review confirming that UV-C air treatment reduced airborne microbial contamination and lowered infection rates in high-risk healthcare environments. Medical equipment decontamination is becoming more formal as FDA-cleared chamber devices set clearer performance expectations for this use case. That combination of room, air, and instrument use is widening the application scope beyond traditional terminal cleaning.

By End-User: Hospitals Dominate While Long-Term Care Facilities Advance Quickly

Hospitals held 52.84% of end-user revenue in 2025, which gave them the leading position in the healthcare UV disinfection equipment market by customer group. Their lead reflects patient throughput, the concentration of higher-risk procedure areas, and stronger pressure to document infection outcomes. Public health reporting frameworks also keep hospital infection metrics visible, which supports continued investment in validated disinfection workflows. Ambulatory surgical centers and diagnostic laboratories remain meaningful secondary users, especially where compact systems fit fast-cycle workflows and surface-sensitive equipment handling.

Long-term care facilities are projected to grow at 13.96% CAGR through 2031, making them the fastest-growing end-user segment in the healthcare UV disinfection equipment market. The Danish phase II trial showed that far-UVC in common rooms cut hospital-treated infection incidence sharply and also halved antibiotic prescription rates. Ceiling-mounted far-UVC and handheld devices fit this setting well because they offer a lower operational barrier than full robot fleets.

Geography Analysis

North America held 42.19% of global revenue in 2025, which gave it the largest position in the healthcare UV disinfection equipment market share by region. The region benefits from high awareness of healthcare-associated infections and stronger alignment between infection outcomes, procurement standards, and hospital operating priorities. Hospitals across the United States continue to face visible HAI reporting pressure, which helps sustain demand for validated environmental disinfection tools. Canada is also becoming more relevant in regional procurement, with Xenex receiving Health Canada registration for LightStrike6 in January 2026. Mexico and Canada offer additional room for expansion, though the U.S. remains the main revenue anchor.

Europe remains one of the core pillars of the healthcare UV disinfection equipment market because infection control awareness is high and the installed base is large. Germany, the United Kingdom, France, Italy, and Spain continue to anchor demand through broad hospital infrastructure and replacement cycles. The review of the RoHS exemption for UV-spectrum mercury lamps is pushing buyers to think earlier about mercury-free alternatives in long-term capital plans. Procurement standards also matter, with IEC 62471 and UL 8802 shaping the technical expectations around germicidal UV equipment and system safety.

Asia-Pacific is expected to be the fastest-growing regional block in the healthcare UV disinfection equipment market, with a projected CAGR of 15.31% through 2031. Growth is tied to hospital expansion, infection-control modernization, and rising interest in LED-based systems across China, India, Japan, South Korea, and Australia. Japan and South Korea are ahead in robotic adoption, while India and Southeast Asia are earlier in the uptake curve and are more likely to favor systems with lower capital intensity. The Middle East and Africa remain earlier-stage markets, although GCC hospital expansion programs are creating demand for integrated UV-C installations, and South Africa has the most advanced sub-Saharan base for adoption. South America is still developing, with Brazil and Argentina leading regional demand as private hospital investment gradually improves access to these technologies.

Competitive Landscape

The healthcare UV disinfection equipment market is moderately fragmented, with more than 20 active participants across robots, fixed systems, chamber devices, LED components, and contract manufacturing. Competition is no longer defined only by lamp output or automation level, because buyers now place more value on validation, safety documentation, and traceable dose delivery. The healthcare UV disinfection equipment market is, therefore, moving toward a structure where proof of performance matters as much as hardware design. Vendors that can combine device efficacy, compliant documentation, and smoother workflow integration are likely to win more hospital tenders. Smaller suppliers still have room to compete, but they face a tighter path when procurement teams want audit-ready systems instead of stand-alone equipment.

Large companies are using acquisitions and partnerships to close product gaps and reach adjacent care environments. In March 2026, Blue Ocean Robotics entered a distribution agreement with PSC Biotech to commercialize the UVD Robot Pharma platform in the United States, Australia, and Singapore for pharmaceutical manufacturing environments. The same month, the company also appointed AB Scientific as its United Kingdom partner for the pharmaceutical sector. These moves show that suppliers are no longer chasing only acute-care hospital demand.

Technology suppliers are also shaping the direction of competition through component-level advances. Stanley Electric’s March 2026 efficiency milestone strengthens the case for LED-based platforms that can replace legacy mercury systems over time. Vendors that add real-time dosimetry, digital disinfection logs, and integration with hospital reporting workflows are building a stronger case in regulated buying environments. The most open white-space areas remain compact chamber systems for diagnostic laboratories, subscription-style handheld programs for ambulatory surgical centers, and ceiling-mounted far-UVC networks for long-term care facilities. The healthcare UV disinfection equipment market is therefore fragmented today, but the next stage of competition is likely to reward vendors that can pair clinical validation with practical deployment models.

Healthcare UV Disinfection Equipment Industry Leaders

Signify N.V.

Xenex Disinfection Services, Inc.

UltraViolet Devices, Inc.

Tru-D SmartUVC

STERIS plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Advanced Sterilization Products (ASP), part of Fortive Corporation (NYSE: FTV), acquired a majority stake in UV Smart, a Netherlands-based developer of UV-C High Level Disinfection technology with operations in over 35 countries. UV Smart's D60 device achieves HLD of specialty ultrasound probes in minutes versus hours using chemical methods, with a 510(k) clearance secured from the FDA in December 2025. The acquisition expands ASP's infection prevention portfolio and extends UV-C HLD capabilities across cardiology, gynecology, and ENT applications globally.

- March 2026: Blue Ocean Robotics (parent of UVD Robots) entered a distribution agreement with PSC Biotech Corporation to commercialize the UVD Robot Pharma platform across the United States, Australia, and Singapore, targeting pharmaceutical manufacturers seeking to meet Annex 1 and contamination control strategy requirements. The deal expands UVD Robots' geographic footprint into regulated cleanroom environments beyond hospital disinfection.

- March 2026: Blue Ocean Robotics appointed AB Scientific as its UK distribution partner for the pharmaceutical sector, enabling the UVD Robot Pharma to enter GMP-controlled manufacturing environments across the United Kingdom. The partnership supports contamination control strategy compliance and Annex 1 readiness for pharmaceutical manufacturers.

Global Healthcare UV Disinfection Equipment Market Report Scope

According to the report’s scope, the healthcare UV disinfection equipment market comprises ultraviolet (UV)-based systems used to disinfect air, surfaces, and water in healthcare facilities. These technologies help reduce pathogen transmission, support infection prevention, and enhance environmental hygiene in hospitals, clinics, laboratories, and other healthcare settings.

The healthcare UV disinfection equipment market is segmented into product type, technology, application, end-user, and geography. By product type, the market is segmented into UV-C robots, fixed UV-C systems, handheld UV-C devices, UV-C cabinets and chambers. By technology, the market is segmented into low-pressure mercury lamp-based systems, pulsed xenon systems, UV-C LED systems, and far-UVC Systems. By application, the market is segmented into patient room disinfection, air disinfection in clinical areas, operating room sterilization, and medical equipment disinfection. By end-user, the market is segmented into hospitals, ambulatory surgical centers, diagnostic laboratories, and long-term care facilities. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| UV-C Robots |

| Fixed UV-C Systems |

| Handheld UV-C Devices |

| UV-C Cabinets and Chambers |

| Low-Pressure Mercury Lamp-Based Systems |

| Pulsed Xenon Systems |

| UV-C LED Systems |

| Far-UVC Systems |

| Patient Room Disinfection |

| Air Disinfection in Clinical Areas |

| Operating Room Sterilization |

| Medical Equipment Disinfection |

| Hospitals |

| Ambulatory Surgical Centers |

| Diagnostic Laboratories |

| Long-Term Care Facilities |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | UV-C Robots | |

| Fixed UV-C Systems | ||

| Handheld UV-C Devices | ||

| UV-C Cabinets and Chambers | ||

| By Technology | Low-Pressure Mercury Lamp-Based Systems | |

| Pulsed Xenon Systems | ||

| UV-C LED Systems | ||

| Far-UVC Systems | ||

| By Application | Patient Room Disinfection | |

| Air Disinfection in Clinical Areas | ||

| Operating Room Sterilization | ||

| Medical Equipment Disinfection | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Diagnostic Laboratories | ||

| Long-Term Care Facilities | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2031 value of the healthcare UV disinfection equipment market?

The market is forecasted to reach USD 2.31 billion by 2031, rising from USD 1.19 billion in 2025 to USD 1.31 billion in 2026 at a 12.05% CAGR.

Which product category leads hospital demand?

UV-C robots led product revenue with a 46.38% share in 2025, supported by demand for autonomous and dose-verified disinfection.

Which technology is growing fastest through 2031?

UV-C LED systems are expected to be the fastest-growing technology segment with a projected 14.18% CAGR, supported by higher efficiency and pressure to replace mercury systems.

Which region is expanding the fastest?

Asia-Pacific is expected to be the fastest-growing region with a projected 15.31% CAGR through 2031, driven by hospital construction and infection-control upgrades.

Page last updated on: