Healthcare Specialty Enzymes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

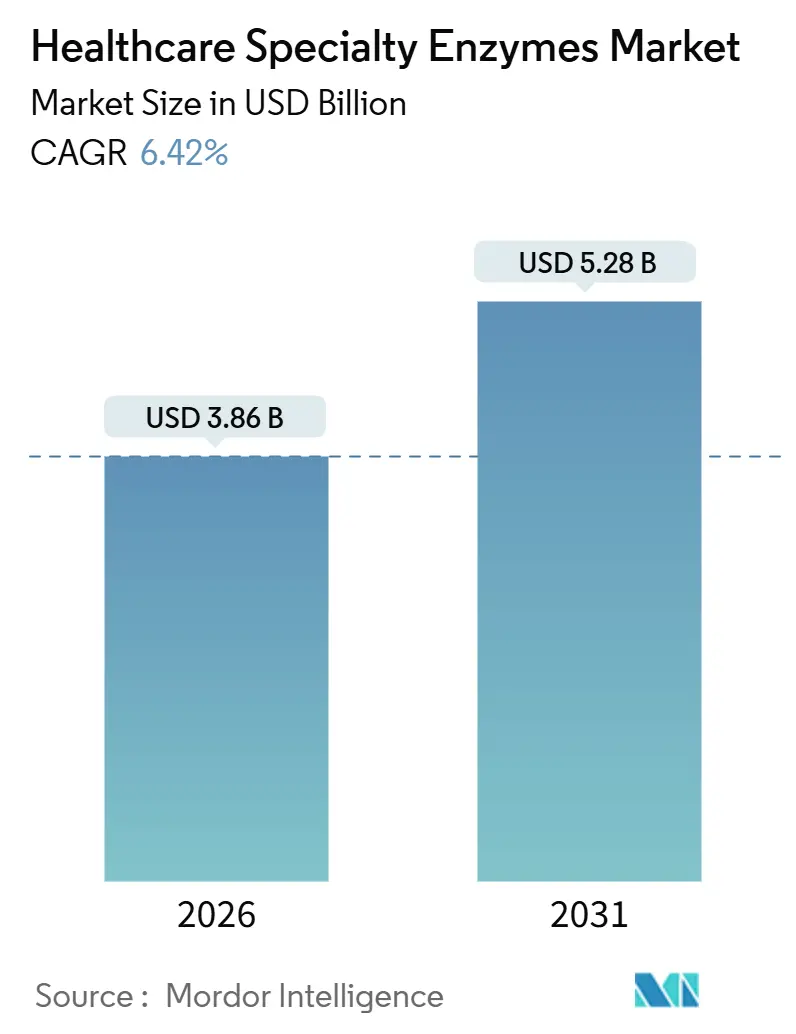

| Market Size (2026) | USD 3.86 Billion |

| Market Size (2031) | USD 5.28 Billion |

| Growth Rate (2026 - 2031) | 6.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Specialty Enzymes Market Analysis by Mordor Intelligence

The Healthcare Specialty Enzymes Market size is estimated at USD 3.86 billion in 2026, and is expected to reach USD 5.28 billion by 2031, at a CAGR of 6.42% during the forecast period (2026-2031).

Uptake is propelled by the clinical validation of CRISPR-based therapies, the migration toward continuous biomanufacturing that favors immobilized catalysts, and rising demand for point-of-care molecular diagnostics in decentralized settings. Investment in collaboration centers that co-develop custom enzymes, expanding reimbursement for rapid tests, and vertical integration by biosimilar producers are improving access while creating margin pressure. Suppliers able to deliver high-fidelity, thermostable, and ambient-temperature-stable formulations are best positioned to capture these expanding opportunities across the healthcare specialty enzymes market.

Key Report Takeaways

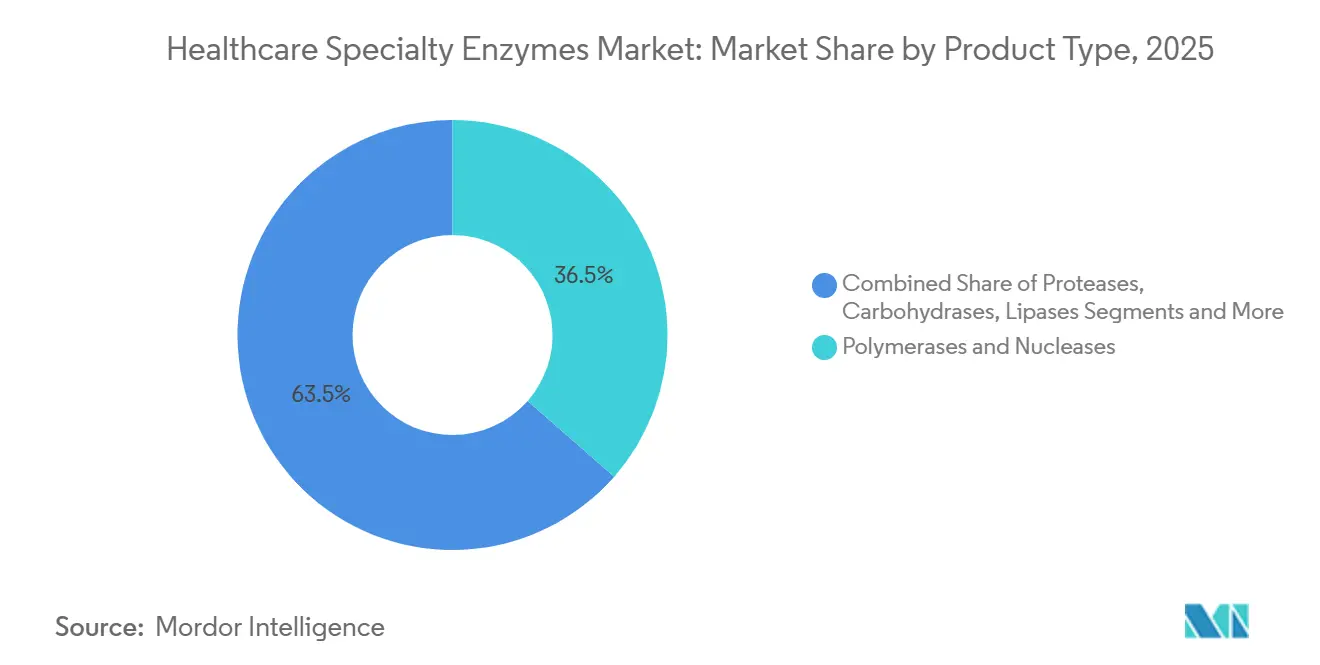

- By product type, polymerases and nucleases led with 36.46% revenue share in 2025, while lipases are projected to expand at a 9.36% CAGR through 2031.

- By source, microbial production captured 58.25% of 2025 revenue, whereas recombinant and engineered enzymes are forecast to grow at a 10.32% CAGR between 2026 and 2031.

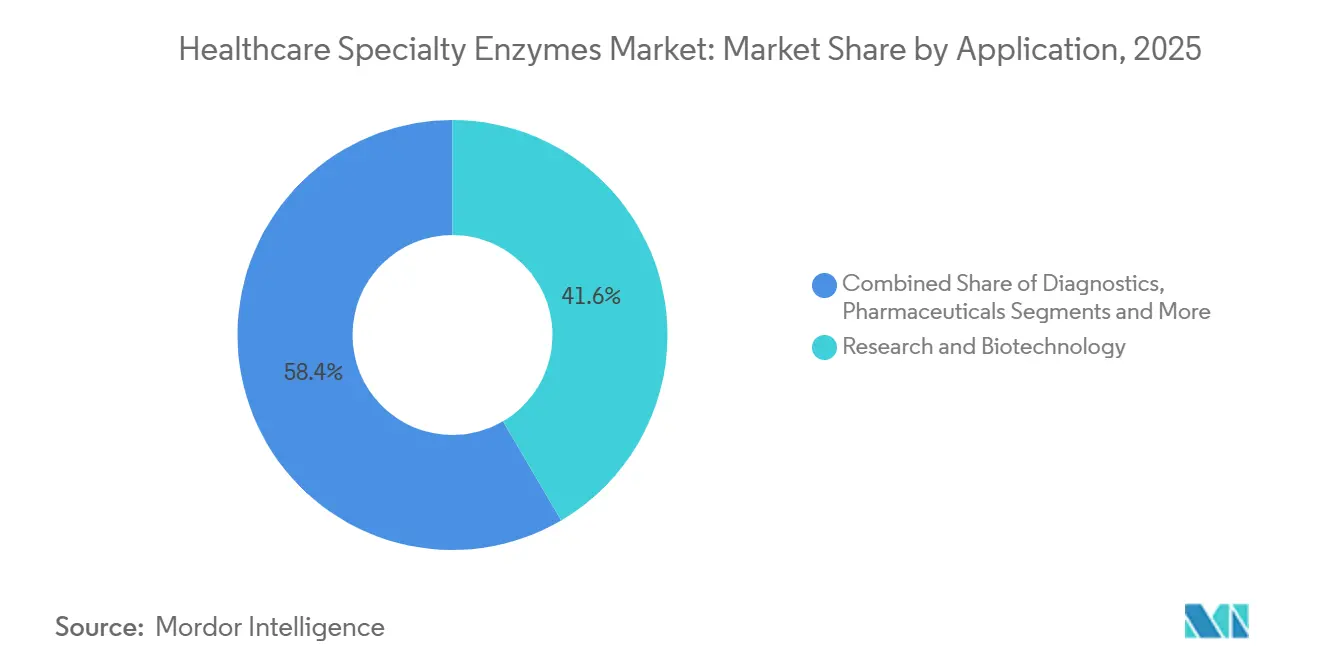

- By application, research and biotechnology accounted for 41.56% of revenue in 2025, while diagnostics is set to advance at a 9.67% CAGR through 2031.

- By end user, pharmaceutical and biotechnology companies held 33.67% share in 2025, whereas hospitals and diagnostic laboratories are expected to record an 8.24% CAGR to 2031.

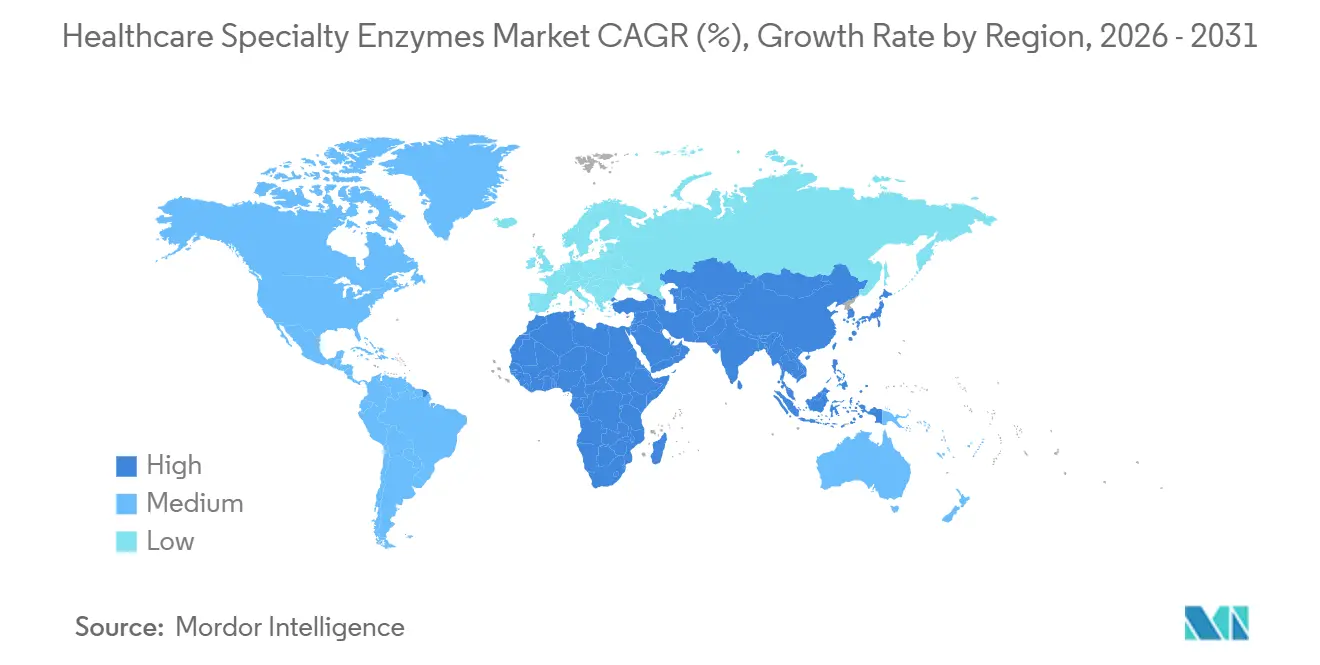

- By geography, North America dominated with 37.84% revenue share in 2025, while Asia-Pacific is anticipated to post the fastest 8.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare Specialty Enzymes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Polymerase & Nuclease Enzymes in Molecular Diagnostics | 1.2% | Global, with peak adoption in North America and Europe | Short term (≤ 2 years) |

| Rising Prevalence of Chronic Diseases Driving Enzyme-Based Therapeutics | 0.9% | Global, with highest burden in Asia-Pacific and North America | Medium term (2-4 years) |

| Expansion of Biopharma R&D Budgets for High-Fidelity Research Enzymes | 1.1% | North America, Europe, and emerging in China and India | Medium term (2-4 years) |

| Accelerating Demand for Enzyme-Enabled Point-of-Care Test Kits | 0.8% | Global, with rapid uptake in Asia-Pacific and Africa | Short term (≤ 2 years) |

| CRISPR & Gene-Editing Boom Creating Niche for Novel Nucleases | 1.0% | North America and Europe, with early-stage adoption in Asia-Pacific | Long term (≥ 4 years) |

| Shift Toward Continuous Pharma Manufacturing Needing Immobilized Enzymes | 0.7% | North America and Europe, with pilot projects in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Polymerase and Nuclease Enzymes in Molecular Diagnostics

Regulators cleared 14 new polymerase chain reaction assays in 2024, shortening review cycles from 12 months to 6 months for equivalent devices.[1]U.S. Food and Drug Administration, “FDA Approves First CRISPR Gene-Editing Therapy,” fda.gov The World Health Organization prequalified three additional point-of-care nucleic acid tests in 2025, unlocking procurement for international health agencies that collectively distribute over 200 million kits annually. Integrated cartridges such as Roche’s cobas Liat now carry lyophilized enzymes that withstand ambient storage, broadening deployment in urgent-care clinics.[2]Roche, “EndoCleave Endonuclease for Viral Vector Manufacturing,” roche.com Next-generation sequencing (NGS) assays demand high-fidelity polymerases capable of amplifying degraded samples while maintaining specificity, a requirement that justifies premium pricing. Together these regulatory and technological shifts are reinforcing enzyme consumption patterns within the healthcare specialty enzymes market.

Rising Prevalence of Chronic Diseases Driving Enzyme-Based Therapeutics

Global diabetes prevalence surpassed 830 million adults in 2022, expanding demand for pancreatic enzyme replacement therapies.[3]Nature Biotechnology, “Engineered Cas9 Variant Demonstrates Tenfold Specificity Increase,” nature.com Two new biologics for lysosomal storage disorders received approval in 2024, and five additional enzyme therapeutics are in Phase III trials as of early 2026. Cancer incidence is projected to rise 47% by 2050, fueling consumption of proteases and nucleases used in antibody-drug conjugate and CAR-T manufacturing. Biosimilar launches by Biocon in 2024 reduced treatment costs by up to 40%, increasing patient access in price-sensitive markets. These developments keep therapeutic enzymes on a sustained growth trajectory across the healthcare specialty enzymes market.

Expansion of Biopharma R&D Budgets for High-Fidelity Research Enzymes

Biopharmaceutical R&D spending reached USD 244 billion in 2024, with cell and gene therapies accounting for 18% of the total. Updated FDA guidance now recommends error rates below 1 in 1 million base pairs for clinical-grade polymerases, raising the performance bar. Thermo Fisher Scientific’s collaboration center opened in November 2025 to co-develop custom nucleases with a dozen sponsors, transforming suppliers into strategic partners. GenScript integrated plasmid and enzyme production in 2025, capturing higher margins through vertical integration. Government grants worth USD 500 million earmarked for domestic enzyme supply have further stimulated local innovation.

Accelerating Demand for Enzyme-Enabled Point-of-Care Test Kits

Point-of-care platforms consumed an estimated 12,000 kilograms of specialty enzymes in 2025, triple the 2020 level. FDA clearance of nine additional near-patient molecular tests in 2024, together with expanded reimbursement, incentivized hospitals to shift testing away from central labs. Sekisui Diagnostics introduced a room-temperature glucose oxidase reagent that halves logistics costs in sub-Saharan markets. WHO’s Emergency Use Listing of three portable assays in 2025 enhanced access for 1.2 billion people in low-resource settings. These forces jointly reinforce diagnostic enzyme demand inside the healthcare specialty enzymes market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent & Regionally Fragmented Regulatory Approval Processes | -0.6% | Global, with highest friction in Europe and emerging markets | Medium term (2-4 years) |

| High Production Costs & Price Pressure from Commoditization | -0.5% | Global, with acute pressure in Asia-Pacific and generics-heavy markets | Short term (≤ 2 years) |

| Supply-Chain Bottlenecks for Rare Enzyme Cofactors | -0.3% | Global, with critical dependencies on China and India | Short term (≤ 2 years) |

| Limited Thermostability Restricting Use in High-Temperature Processes | -0.4% | North America and Europe, where continuous manufacturing is advancing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent and Regionally Fragmented Regulatory Approval Processes

Divergent classification rules across the United States, European Union, China, and India prolong launch timelines by 12–18 months for new enzymes. EU in-vitro diagnostic regulation now mandates notified-body review for most test components, increasing compliance cost and complexity. China’s 2024 requirement for local clinical data delays therapeutic enzyme entry and adds USD 10–15 million per product. Only 40% of suppliers hold ISO 13485 certification despite 80% of hospitals requesting it, curbing market access for smaller firms. These frictions collectively weigh on growth across the healthcare specialty enzymes market.

High Production Costs and Price Pressure from Commoditization

Specialty enzymes cost between USD 5,000 and USD 50,000 per kilogram, yet biosimilar entrants trim prices 20–30% each year as patents expire. Fermentation yields improved fivefold since 2020, lowering barriers for contract manufacturers in China and India. Immobilized catalysts that last 30 days reduce per-batch enzyme demand by 80%, squeezing volume growth unless suppliers monetize services. Currency appreciation of the U.S. dollar in 2024 further eroded export competitiveness for European and Asian producers. These forces create persistent margin pressure throughout the healthcare specialty enzymes market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Nucleases Anchor Revenue as Lipases Accelerate

Polymerases and nucleases accounted for a dominant 36.46% healthcare specialty enzymes market share in 2025, reflecting entrenched use in diagnostics and gene-therapy scale-up. The cohort benefits from high-fidelity variants and novel CRISPR editors that satisfy stringent regulatory thresholds. Lipases are forecast to post a 9.36% CAGR through 2031, the strongest among product categories, propelled by enzyme replacement therapies for pancreatic insufficiency and mRNA vaccine lipid nanoparticle formulation.

Proteases represented about 22% of 2025 revenue. Their role in site-specific antibody conjugation is expanding as antibody-drug conjugates move deeper into pipelines. Carbohydrases, led by cellulases and amylases, gained traction following two FDA approvals for metabolic-disorder therapies in 2024. The broader “other specialty enzymes” cluster grows at 7.8% through 2031 on synthetic-biology use cases such as enzyme-based DNA synthesis. High-purity grades that meet new FDA residual-enzyme guidance command 40% price premiums, adding a value layer within the healthcare specialty enzymes market.

By Source: Engineered Platforms Outpace Conventional Fermentation

Microbial production routes delivered 58.25% of revenue in 2025, supported by scalable bacterial and fungal fermentation. Recombinant and engineered formats are projected to expand at a 10.32% CAGR between 2026 and 2031, outstripping all other sources, as platforms like CodeEvolver cut development cycles from three years to six months.

Plant-derived enzymes hold about 12% share but face variability and scale issues, whereas animal sources are slipping due to supply risk and cultural barriers. Engineered Pichia pastoris strains achieve fivefold higher secretion titers, slicing costs by 60% and advancing adoption. Europe’s draft requirement for full host-cell genomic sequencing may lengthen approvals, yet companies see the hurdle as manageable given the performance gains. The mix shift toward engineered products reinforces premium growth avenues within the healthcare specialty enzymes market.

By Application: Diagnostics Lead Growth as Testing Moves Near Patient

Research and biotechnology retained a 41.56% revenue share in 2025. Diagnostics, however, are projected to advance at a 9.67% CAGR through 2031, the highest among applications, riding the wave of decentralized molecular testing. Multiplexed cartridges that integrate six enzyme reactions in one unit exemplify demand for robust formulations.

Pharmaceutical therapeutics constituted about 28% of 2025 income, steered by enzyme replacement therapies and gene-editing manufacturing. The “other” bucket grows at 6.5% yet faces commoditization. ISO 13485 certification has become a default purchasing prerequisite, filtering suppliers and elevating standards. This application pivot enriches downstream opportunities in the healthcare specialty enzymes market.

By End User: Hospitals and Diagnostic Labs Shift Testing Paradigm

Pharmaceutical and biotech companies generated 33.67% of 2025 demand. Hospitals and diagnostic labs are set to expand at an 8.24% CAGR through 2031 as reimbursement shifts favor near-patient molecular testing. Abbott’s ID NOW platform deployed in 15,000 U.S. clinics during 2024 indicates broad clinical acceptance.

Academic institutes hold roughly 25% share, backed by expanding genomics grants. CROs accounted for close to 12% in 2025 and grow at 7.9% as sponsors outsource enzyme-intensive tasks. Vertical integration by large pharma into custom enzyme production tightens supply relationships, yet also intensifies price negotiation, influencing value capture in the healthcare specialty enzymes market.

Geography Analysis

North America claimed 37.84% of the healthcare specialty enzymes market in 2025, buoyed by expedited FDA pathways and concentrated gene-therapy pipelines. Thermo Fisher Scientific’s Massachusetts collaboration center exemplifies infrastructure that locks in local supply arrangements. Canada and Mexico are growing above 7% but remain fringe contributors due to limited domestic production.

Asia-Pacific is set to record the fastest regional CAGR at 8.55% through 2031. Wuxi Biologics added 200,000 liters of bioreactor capacity in 2024, translating into 8,000 kilograms of incremental annual enzyme demand. Biocon’s biosimilar launches widened access across India and select ASEAN markets. Japan approved its first domestic CRISPR therapy in 2024, and six local firms have joined the race, enlarging nuclease consumption. Rest-of-APAC, supported by WHO prequalification of three portable tests in 2025, is projected to expand at 9.2%.

Europe contributed roughly 28% in 2025, moderated by fragmented regulatory processes that add 12–18 months to market entry. Germany, France, and the United Kingdom generate 60% of regional revenue, aided by robust pharma manufacturing networks. Novozymes’ Danish thermostable enzyme hub signals continued R&D strength, though products will arrive only in 2027. Southern Europe grows at 6.8% on lower healthcare spend. The Middle East and Africa, plus South America, remain emerging yet promising; Brazil invested USD 120 million in local diagnostic manufacturing in 2024, while South Africa lifted molecular capacity by 25%.

Competitive Landscape

The market is moderately fragmented. Thermo Fisher Scientific, Roche, Novonesis, BASF, and DSM-Firmenich anchor leadership, while specialized players target high-value niches. Biocon’s 2024 biosimilar enzyme entries price 35% below originators, heightening competition. Thermo Fisher Scientific’s client-embedded model secures multi-year custom nuclease contracts, dampening commoditization.

Codexis leverages CodeEvolver to cut enzyme design time to six months, enabling four new pharma alliances in 2024 worth up to USD 10 million each. Patent activity rose 40% in 2024, underlining the importance of intellectual property. Genovis disrupted analytics niches with FabRICATOR Xtra, capturing share from legacy protease providers. ISO 13485 compliance is now a competitive gatekeeper as hospitals mandate certified suppliers, prompting consolidation among smaller manufacturers.

White-space opportunities persist in thermostable enzymes that support continuous manufacturing and ambient-temperature stable formulations that remove cold-chain hurdles. Novozymes’ immobilized protease breakthrough shows promise but still faces validation hurdles for mainstream biologics. Regional adoption disparities also create room for targeted growth strategies within the healthcare specialty enzymes market.

Healthcare Specialty Enzymes Industry Leaders

F. Hoffmann-La Roche AG

DSM-Firmenich

Codexis, Inc.

Novozymes A/S

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Microbiome Labs launched DigestMate, a dual enzyme and probiotic formulation aimed at comprehensive macronutrient breakdown and gut barrier support.

- March 2025: Primrose Bio introduced Prima RNApols ExTend, engineered RNA polymerases that improve long-template mRNA vaccine manufacturing efficiency.

- March 2025: FDA cleared SineuGene Therapeutics’ IND for SNUG01, an rAAV9-based gene therapy for ALS that leverages recombinant enzyme technology for neuroprotection.

Global Healthcare Specialty Enzymes Market Report Scope

The healthcare specialty enzymes market comprises high-purity proteins, such as proteases, lipases, and polymerases, used as biocatalysts in pharmaceuticals, diagnostics, and biotechnology research to accelerate biochemical reactions for drug development, diagnostics, and therapeutic applications.

The Healthcare Specialty Enzymes Market Report is segmented by Product Type, Source, Application, End User, and Geography. By Product Type, the market is segmented into Polymerases & Nucleases, Proteases, Carbohydrases, Lipases, and Other Specialty Enzymes. By Source, the market is segmented into Microbial, Plant, Animal, and Recombinant/Engineered. By Application, the market is segmented into Diagnostics, Research & Biotechnology, Pharmaceuticals, and Others. By End User, the market is segmented into Hospitals & Diagnostic Labs, Pharma & Biotech Companies, Academic & Research Institutes, CROs, and Others. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Polymerases & Nucleases |

| Proteases |

| Carbohydrases |

| Lipases |

| Other Specialty Enzymes |

| Microbial |

| Plant |

| Animal |

| Recombinant/Engineered |

| Diagnostics |

| Research & Biotechnology |

| Pharmaceuticals (Therapeutics) |

| Others |

| Hospitals & Diagnostic Laboratories |

| Pharmaceutical & Biotechnology Companies |

| Academic & Research Institutes |

| Contract Research Organisations (CROs) |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Polymerases & Nucleases | |

| Proteases | ||

| Carbohydrases | ||

| Lipases | ||

| Other Specialty Enzymes | ||

| By Source | Microbial | |

| Plant | ||

| Animal | ||

| Recombinant/Engineered | ||

| By Application | Diagnostics | |

| Research & Biotechnology | ||

| Pharmaceuticals (Therapeutics) | ||

| Others | ||

| By End User | Hospitals & Diagnostic Laboratories | |

| Pharmaceutical & Biotechnology Companies | ||

| Academic & Research Institutes | ||

| Contract Research Organisations (CROs) | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the healthcare specialty enzymes market by 2031?

The market is forecast to reach USD 5.28 billion by 2031.

Which product category is expected to grow fastest?

Lipases, with a projected 9.36% CAGR through 2031, outpace other product types.

Why are hospitals increasing enzyme demand?

Expanded reimbursement for point-of-care molecular tests is driving hospitals and diagnostic labs to adopt on-site enzyme-enabled assays.

Which region will post the highest growth?

Asia-Pacific is set to expand at an 8.55% CAGR, buoyed by large-scale biologics manufacturing investments in China and India.

What is the biggest regulatory hurdle for suppliers?

Fragmented approval pathways across major regions extend launch timelines and elevate compliance costs.

Page last updated on: