Healthcare Smart Labels Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

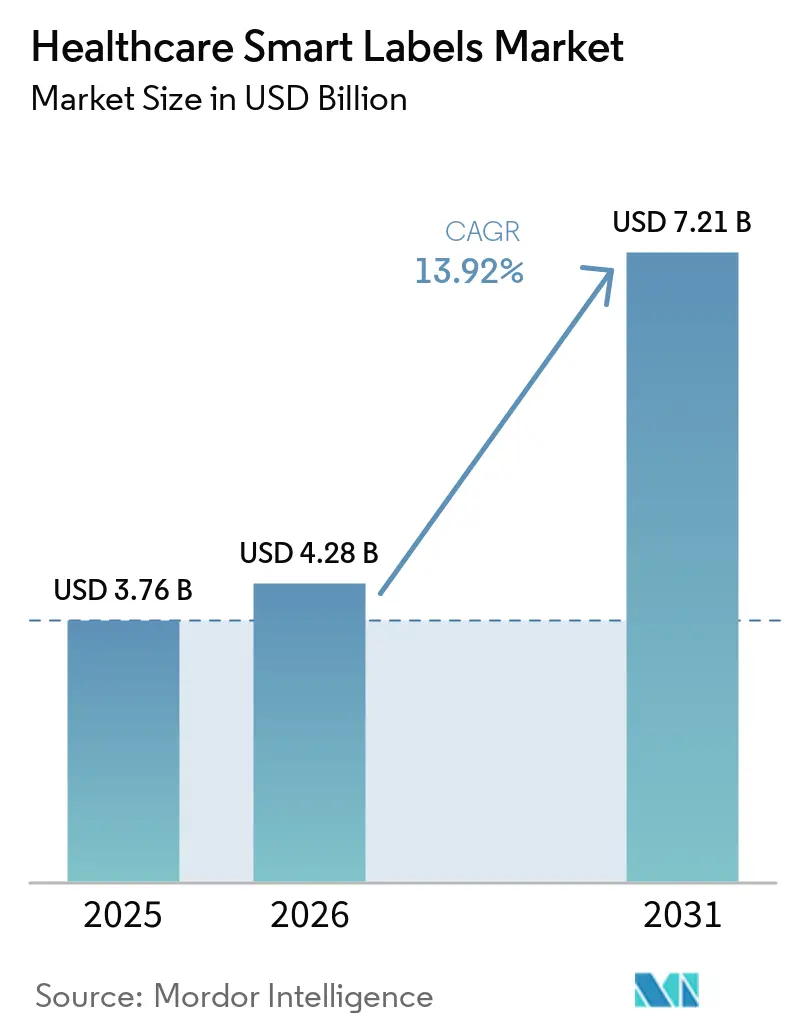

| Market Size (2026) | USD 4.28 Billion |

| Market Size (2031) | USD 7.21 Billion |

| Growth Rate (2026 - 2031) | 13.92% CAGR |

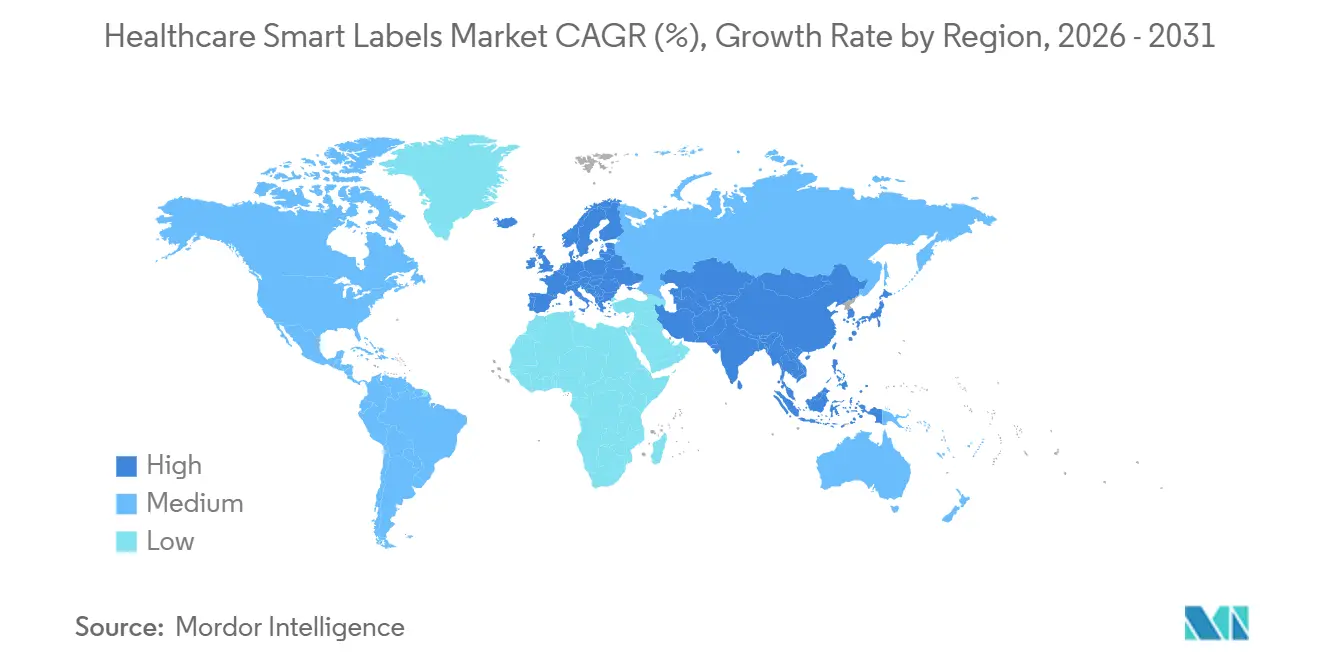

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Smart Labels Market Analysis by Mordor Intelligence

The Healthcare Smart Labels Market size is projected to expand from USD 3.76 billion in 2025 and USD 4.28 billion in 2026 to USD 7.21 billion by 2031, registering a CAGR of 13.92% between 2026 to 2031.

Demand aligns with DSCSA and EU FMD systems that require serialized identifiers and interoperable verification, which sustain ongoing investment in 2D barcode and RFID labeling across finished dose forms and secondary packaging. The expansion of biologics and specialty therapies in 2026 keeps cold-chain capacity tight, which raises the importance of time–temperature indicators and sensor labels on shippers, kits, and unit packs. Hospitals continue to digitize inventory, asset tracking, and patient identification, which lifts the value proposition for RFID, NFC, and barcode labels that tie into EMR, medication administration, and inventory systems. New data standards like EPCIS 2.0 support sensor events alongside serialized identifiers, which align label data with enterprise platforms for real-time decision making.

Key Report Takeaways

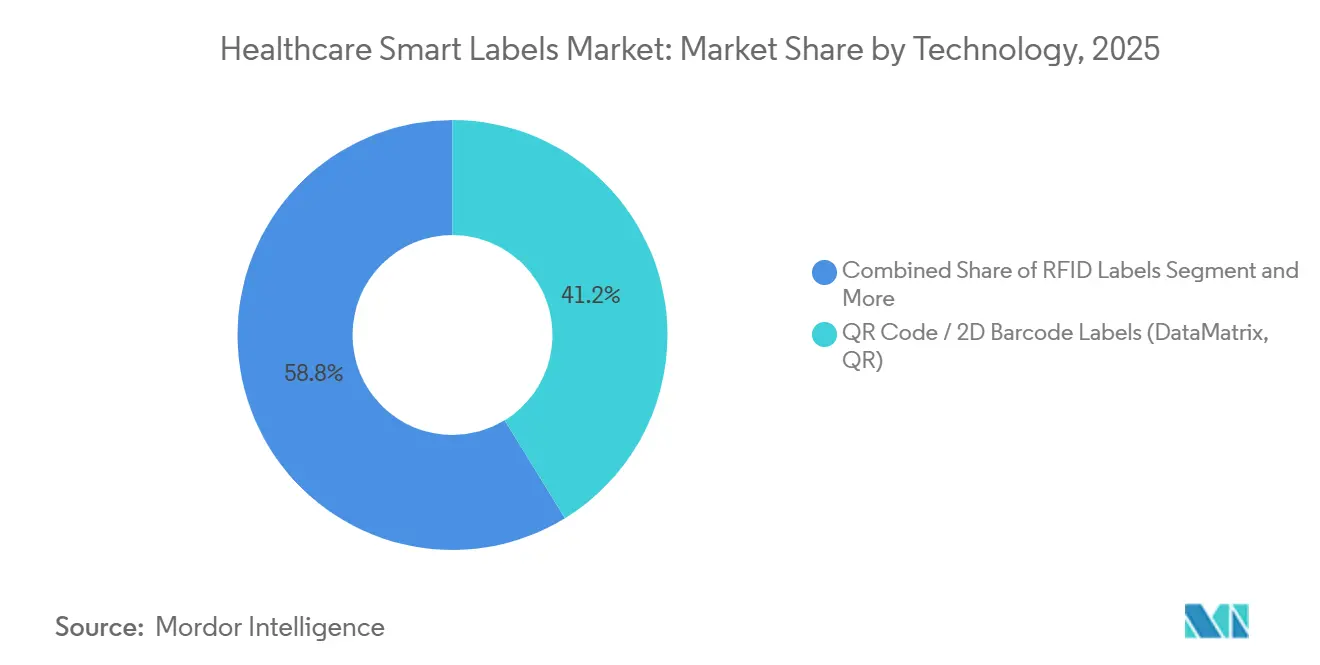

- By technology, QR Code and 2D Barcode labels led with 41.23% revenue share in 2025; sensing labels are projected to expand at a 14.65% CAGR through 2031 in the healthcare smart labels market.

- By component, microprocessors and ICs accounted for 42.96% in 2025; sensors are forecast to rise at a 14.82% CAGR over 2026-2031 in the healthcare smart labels market

- By application, drug tracking and serialization captured 39.37% in 2025; cold-chain monitoring is projected at a 14.48% CAGR through 2031 in the healthcare smart labels market.

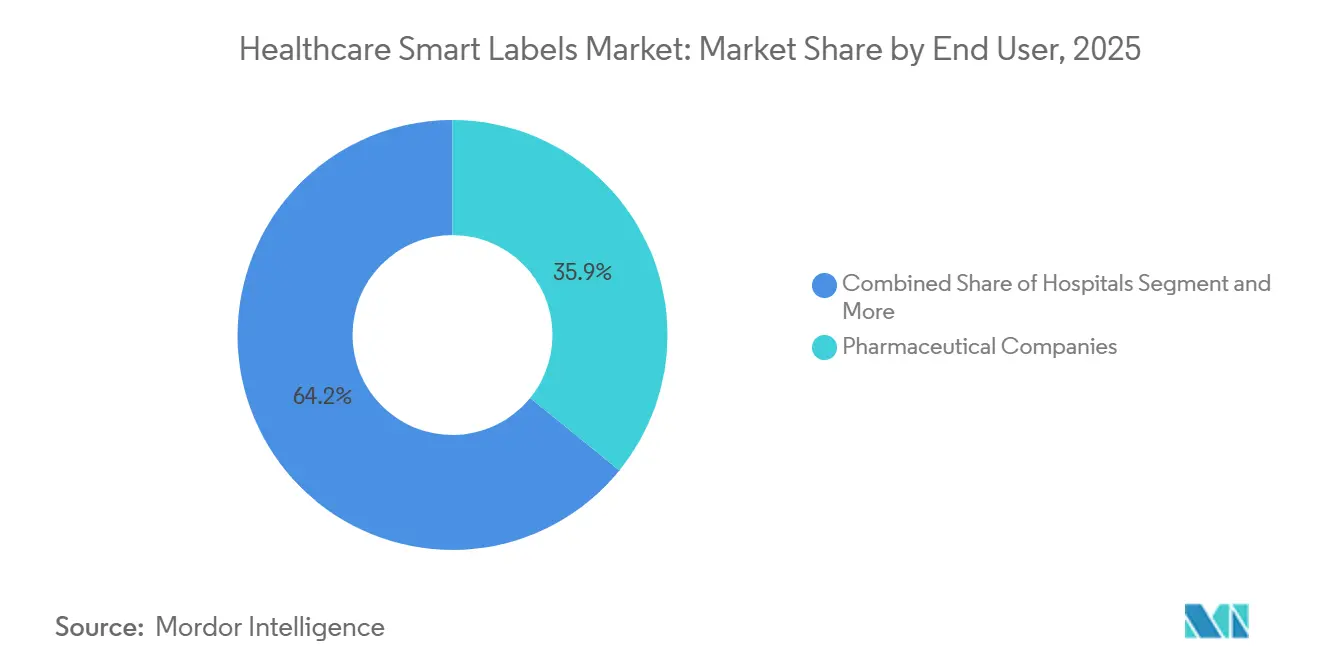

- By end user, pharmaceutical companies held 35.85% in 2025; CMOs/CDMOs are expected to grow at a 15.92% CAGR during 2026-2031.

- By geography, North America accounted for 43.14% in 2025; Asia-Pacific is set to record a 14.76% CAGR to 2031 in the healthcare smart labels market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare Smart Labels Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| DSCSA/EU FMD Serialization Mandates Accelerate Item-Level Labeling | +3.0% | United States, European Union | Long term (≥ 4 years) |

| Anti-Counterfeiting and Diversion Control Priorities in Pharma | +2.0% | Global | Long term (≥ 4 years) |

| Expansion of Biologics/Vaccines Cold-Chain Needs Temperature-Indicating Labels | +2.0% | Global, with emphasis on North America and Europe | Medium term (2-4 years) |

| Healthcare Digitalization and RFID/NFC Adoption in Hospitals and Pharma | +2.0% | Global, with emphasis on North America, Europe, and developed APAC | Medium term (2-4 years) |

| EPCIS 2.0 and Interoperable Data Exchange Enable Sensorized Smart Labels | +1.5% | North America & EU core, with global standards adoption | Long term (≥ 4 years) |

| Ambient IoT/BLE Sensing Brings Unit-Level Condition Visibility | +2.0% | North America early adoption, APAC scalability potential | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

DSCSA/EU FMD Serialization Mandates Accelerate Item-Level Labeling

Serialization requirements in the United States and Europe continue to lift demand for item-level labeling, with DSCSA emphasizing interoperable, electronic tracing and the EU FMD relying on pack-level verification through EMVS. The DSCSA enhanced distribution security framework requires trading partners to exchange serialized data and investigate suspect products, which encourages pharmaceutical manufacturers and distributors to standardize barcodes and RFID-based identifiers on unit packages and cases.[1]U.S. Food and Drug Administration, “Enhanced Drug Distribution Security,” U.S. Food and Drug Administration In the EU, the FMD architecture implements unique identifiers and anti-tamper devices on prescription medicines, making machine-readable 2D DataMatrix labels a default for verification at dispensing points, including hospital pharmacies. These requirements create a durable baseline for the healthcare smart labels market as companies refresh and expand labeling systems to remain compliant. The operational push for interoperable data also aligns with EPCIS-based exchange, which in turn favors serialized barcodes and RAIN RFID that integrate smoothly with enterprise systems.[2]GS1 US, “Drug Supply Chain Security Act (DSCSA),

Anti-Counterfeiting and Diversion Control Priorities in Pharma

Pharmaceutical stakeholders use smart labels to deter counterfeiting, detect diversion, and enable rapid recalls, with serialization and tamper-evidence working alongside mobile verification. Health authorities continue to warn that falsified medical products remain a threat, reinforcing the need for secure, scannable labels on each saleable unit as well as on secondary packaging.[3]World Health Organization, “Substandard and Falsified Medical Products,” World Health Organization Item-level barcodes and NFC tags support authentication and chain-of-custody checks across wholesalers, third-party logistics providers, and hospital pharmacies. In parallel, RFID enables automated counting and location tracking in warehouses and care settings, which helps reduce shrinkage and detect anomalies in high-value therapies. These capabilities together strengthen the healthcare smart labels market by reducing error and risk exposure across the regulated supply chain.

Expansion of Biologics/Vaccines Cold-Chain Needs Temperature-Indicating Labels

The growth of biologics and vaccines maintains a high standard for refrigerated transport and storage, which boosts demand for time–temperature indicators and sensorized labels at the shipper, case, and unit level. CDC guidance emphasizes continuous temperature monitoring to prevent exposure excursions that compromise vaccine potency, and time–temperature indicators on labels complement digital loggers to document integrity during transit and at the point of care.[4]Centers for Disease Control and Prevention, “Vaccine Storage and Handling Toolkit,” Centers for Disease Control and Prevention WHO best practices for vaccine management similarly support rigorous cold-chain processes that benefit from label-based indicators where simplicity and immediacy are valuable at clinics and pharmacies. Adoption of these labels persists as biologics volumes rise and distribution networks grow more complex with specialty pharmacies and home care. The cold-chain focus reinforces steady growth in the healthcare smart labels market as manufacturers expand temperature-protected SKUs and hospitals tighten handling compliance.

Healthcare Digitalization and RFID/NFC Adoption in Hospitals and Pharma

Hospitals and pharmaceutical manufacturers increase use of RFID and NFC to automate inventory counts, improve equipment tracking, and enhance patient identification. In clinical settings, RFID and RTLS improve operational visibility for devices and medication carts, while NFC on wristbands and unit packages supports bedside scanning and closed-loop medication administration. Integration with EHR, pharmacy systems, and materials management platforms elevates the business case for serialized barcodes alongside RFID because multi-modal scanning reduces reliance on any single technology. Pharma operations, including CMOs/CDMOs, apply RFID to manage WIP, serialized aggregation, and consignment inventory with hospitals and wholesalers. These workflows collectively contribute to growth in the healthcare smart labels market by aligning digital labels with day-to-day clinical and supply-chain processes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation and Infrastructure Cost Across Labels/Readers/Software | -2.5% | Global | Medium term (2-4 years) |

| Data Privacy, Security, and Interoperability Hurdles (HIPAA/GDPR/EPCIS) | -2.0% | United States, European Union | Medium term (2-4 years) |

| RFID Performance Challenges on Vials/Liquids/Metal-Rich Environments | -1.5% | Global | Short term (≤ 2 years) |

| Fragmented Standards and Compliance Workflows Across DSCSA/UDI/EMVS | -1.5% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Implementation and Infrastructure Cost Across Labels/Readers/Software

Total cost of ownership includes labels and inlays, readers and printers, encoding and verification stations, and the software needed to capture and exchange EPCIS events. Hospitals and pharma distribution sites must budget for systems integration and process changes, including staff training and change management to ensure compliance. Passive RFID systems can lower costs over time, but upfront investment in readers and infrastructure remains a barrier, especially for smaller facilities. Active BLE tags that incorporate batteries or advanced sensors carry higher unit costs, which narrows the range of use cases where ROI is immediately clear. These economic factors can delay some deployments in the healthcare smart labels market, particularly where the value density of products is moderate.

Data Privacy, Security, and Interoperability Hurdles (HIPAA/GDPR/EPCIS)

Patient data protections under HIPAA in the United States and GDPR in Europe drive strict controls on how label-linked events are captured, stored, and shared across systems. Organizations must enforce data minimization, encryption, and access controls for any workflow that could link identifiable patient information to label identifiers. While EPCIS helps standardize event data models and transport, interoperability challenges persist when organizations customize implementations or run hybrid legacy systems. Cross-border data exchange further complicates operations for multinational pharma companies and contract manufacturers that must align to multiple data protection regimes. These constraints can slow rollouts and add complexity to scaling the healthcare smart labels market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Barcode leads today while sensing accelerates through 2031

In 2025, QR Code and 2D DataMatrix labels led with 41.23% of the healthcare smart labels market share in technology, reflecting their central role in DSCSA and EMVS verification at the unit level in hospitals and pharmacies. Over 2026-2031, sensing labels that capture temperature and related conditions are projected to grow fastest at a 14.65% CAGR as biologics and vaccines expand, and stakeholders seek simple unit-level condition visibility across cold-chain movements. RAIN RFID continues to scale for automated counting and cabinet management in care settings, while NFC complements with patient-initiated taps for authentication and information access. EAS overlaps where item security is required in retail and hospital pharmacy settings that handle specialty therapies. Multi-technology strategies remain common, so clinical and logistics teams can scan 2D barcodes while inventory teams automate with RFID, preserving resilience in the healthcare smart labels market.

As data standards evolve, EPCIS 2.0 enables combined serialization and sensor events that increase the return from sensor labels and RFID deployments in regulated workflows. This integration makes sensing more attractive since condition data can be natively associated with unique identifiers and exchanged across trading partners. Hospital RTLS deployments that leverage BLE are complementary to RFID and barcodes, broadening visibility beyond fixed choke points. In this context, technology choices align with use-case priorities such as bedside verification, automated counting, or unit-level cold-chain assurance in the healthcare smart labels industry. The combined trajectory supports a balanced mix in which low-cost 2D barcodes remain ubiquitous while sensing and RFID gain share in high-impact applications of the healthcare smart labels market.

By Component: ICs dominate value today and sensors outpace growth

Microprocessors and ICs accounted for 42.96% of the component stack in 2025, reflecting their presence across RFID, NFC, and advanced sensor tag designs that drive value capture in the supply chain. Sensors are projected to grow at a 14.82% CAGR during 2026-2031 as cold-chain expansion, specialty therapy handling, and clinical telemetry use cases scale across manufacturing, distribution, and care delivery. Memory and transceivers remain essential enablers of reliable reads and data retention across temperature excursions and challenging RF environments. Batteries appear in active BLE and specialty labels where continuous broadcasting or condition logging is required, although energy-harvesting trends reduce the need for battery replacements over time. These component trends favor a durable shift toward condition-aware labeling in the healthcare smart labels market.

As EPCIS 2.0 supports sensor events, more solutions pair sensors with serialization data, which increases integration value without requiring custom data models. Hospitals and pharma distribution centers benefit when components enable labels that are reliable on metals and liquids, which depend on IC sensitivity, tuned antennas, and calibrated sensor elements. Vendors that optimize component stacks for small vials and curved surfaces unlock new footprints where conventional tags struggled. These advances reinforce the trajectory for sensors and high-performance ICs in the healthcare smart labels industry while the healthcare smart labels market attracts more solution diversity.

By Application: Serialization leads while cold-chain monitoring grows fastest

Drug tracking and serialization represented 39.37% in 2025, supported by DSCSA and EMVS verification workflows that rely on 2D barcodes and, in certain settings, RFID for automated handling and counting. Cold-chain monitoring is set to post the fastest growth at a 14.48% CAGR during 2026-2031 as pharmacies, clinics, and home-delivery channels expand and require condition assurance at more granular levels. Patient identification and safety rely on wristbands and unit labels that tie into EMR and medication administration workflows, emphasizing NFC and barcodes for bedside scanning. Laboratory sample tracking leverages 2D barcodes and RFID to maintain chain-of-custody and minimize labeling and handling errors. These applications provide a broad and durable demand for the healthcare smart labels market size, as serialization and safety stay at the center of operations.

Hospitals and pharmacies increasingly blend 2D barcode verification with RFID-based counting of serialized units so they can balance cost and automation. Medical equipment tracking extends label use to devices and trays, making RFID and BLE useful as they integrate with RTLS platforms in surgical and central sterile services. As sensor labels become easier to deploy and interpret, cold-chain monitoring expands from shipper-level loggers to carton- and unit-level indicators in the healthcare smart labels market. This creates a strong foundation for the healthcare smart labels market size to expand where condition data informs quality release and inventory disposition.

By End User: Pharma leads while CMOs/CDMOs expand fastest

Pharmaceutical companies held 35.85% in 2025, reflecting responsibility for serialization and verification readiness, as well as investment in labels that enable inventory management and product authentication in distribution. CMOs and CDMOs are expected to lead growth at 15.92% CAGR through 2031 as outsourcing expands and contract sites align labeling, encoding, and EPCIS data exchange with sponsor requirements. Hospitals apply labels across patient ID, medication administration, and equipment tracking, while pharmacies and retail pharmacies adopt verification and condition checks as specialty therapies grow. Diagnostic laboratories use smart labels for sample traceability and environmental controls across pre-analytical steps and transport. This end-user mix supports balanced growth across core nodes of the healthcare smart labels market.

Pharma companies and CMOs/CDMOs increasingly demand harmonized label specifications that map to DSCSA, EMVS, and UDI so they can consolidate encoding and verification processes across sites. Hospitals invest in RFID-enabled cabinets and BLE RTLS systems that complement serialized barcode scanning in clinical workflows. Pharmacies adopt serialized checks and condition indicators for specialty dispensing and returns processing. This alignment across end-users maintains momentum in the healthcare smart labels industry and supports recurring deployments in the healthcare smart labels market.

Geography Analysis

North America accounted for 43.14% in 2025, supported by DSCSA-driven serialization, hospital digitalization, and strong adoption of RFID and BLE infrastructure across care settings. Asia-Pacific is projected to grow at a 14.76% CAGR during 2026-2031 as regional healthcare systems scale hospital automation, expand biologics manufacturing, and adopt serialization in line with global trading partner expectations. Europe maintains robust demand through EMVS verification and hospital workflows that operationalize 2D barcode scanning with selective RFID adoption in clinical logistics. These regional demand patterns sustain the healthcare smart labels market as standards and infrastructure investments converge.

In North America, the United States sets the pace with DSCSA interoperability requirements and hospital investments in RFID-enabled cabinets and inventory systems, while Canada and Mexico raise digital readiness in hospital and distribution operations. In Europe, Germany, the United Kingdom, France, Italy, and Spain drive consistent pack-level verification and warehouse scanning for compliance and supply assurance. The rest of Europe expands as hospitals refresh scanning and verification equipment, and as specialty therapies grow in volume and value.

Across Asia-Pacific, China scales serialization and healthcare logistics technology, India deepens pharma manufacturing and CDMO capabilities, and Japan, Australia, and South Korea maintain high digital maturity in hospital operations. The Rest of Asia-Pacific introduces blended RFID and barcode workflows, often starting with high-value products and cold-chain shipments. In the Middle East and Africa, GCC markets lead with hospital modernization and specialty imports that require compliant labeling, while South Africa progresses with pharmacy and hospital traceability investments. In South America, Brazil and Argentina expand specialty distribution and hospital barcode verification, while returns processing and cold-chain management lift interest in condition-aware labels. These trends collectively sustain diversified growth in the healthcare smart labels market across regions.

Competitive Landscape

Competition features leading label converters and inlay makers, semiconductor suppliers, and device OEMs that provide readers and printers for healthcare. Companies with validated healthcare portfolios and on-metal or vial-friendly inlays sustain defensible positions because they help overcome common RF and handling challenges in hospitals and pharma. Vendors invest in expanding product families that cover 2D barcodes, RAIN RFID, NFC, BLE, and time–temperature indicators so customers can standardize on multi-technology solutions for compliance and automation. Providers differentiate through regulatory knowledge, EPCIS-ready software connectors, and field support for validation and change control. This combination of capabilities drives solution stickiness and supports the growth of the healthcare smart labels market.

Strategic moves include expanding healthcare-grade RFID inlays and introducing on-metal and small-form-factor tags that improve read performance on vials and instruments, as seen in portfolios from Avery Dennison and CCL for clinical environments. Device OEMs such as Zebra extend integrated solutions that include RFID printers and scanners configured for hospital and pharmacy workflows. Platform providers like Impinj emphasize RAIN RFID solutions for healthcare cabinets, consignment inventory, and asset visibility, reflecting a broader shift toward automation. These approaches help customers unify barcode and RFID programs in the healthcare smart labels market.

Market consolidation remains selective because specialized performance on small items, metals, and liquids still requires tailored engineering. Partnerships between component makers, inlay vendors, and label converters are common to accelerate validated designs and ensure global availability. Solutions increasingly ship with EPCIS connectors and sensor-data compatibility so enterprises can scale deployments across suppliers and trading partners. As hospitals and pharma emphasize resilience, vendors with global supply and service footprints maintain an edge. Competitive intensity continues to spur product innovation and ecosystem collaboration across the healthcare smart labels market.

Healthcare Smart Labels Industry Leaders

Alien Technology LLC

Avery Dennison Corporation

CCL Industries Inc.

Invengo Information Technology Co. Ltd.

SATO Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Novo Nordisk completed construction of a USD 556 million pharmaceutical manufacturing plant in Tianjin, China, expanding fill-finish capacity for GLP-1 injectables and other biologics. The facility implements full DSCSA-compliant serialization at line level with integrated temperature-sensing labels for cold-chain export shipments to U.S. and EU markets, representing the largest single-site pharma investment in China in 2025.

- October 2025: IFA Celtics became Mexico's first pharmaceutical company to deploy NFC anti-counterfeit technology at commercial scale, partnering with ForgeStop Technology Corp to embed encrypted EM Microelectronic NFC labels into millions of drug packs. The labels use AES-128 encryption and generate unique, one-time dynamic URLs for each scan, enabling patients, pharmacists, and regulators to verify product authenticity via smartphone without requiring an app.

- August 2025: Schreiner MediPharm launched robust RFID labels specifically engineered for Bluesight KitCheck Scanning Stations, optimizing digital inventory control in hospital pharmacies. The labels feature high-speed labeling compatibility, protection of integrated chips from mechanical stress via reinforced structure, and adaptability to primary containers with narrow radii (vials, syringes).

Global Healthcare Smart Labels Market Report Scope

As per the scope of the report, healthcare smart labels are advanced labeling solutions used in the healthcare industry that integrate technologies such as RFID, NFC, QR codes, or sensors to enable real-time tracking and data exchange. They help monitor critical parameters like temperature, humidity, and the location of pharmaceuticals, vaccines, blood products, and medical devices. These labels enhance patient safety, regulatory compliance, and supply chain transparency by reducing errors and improving traceability.

The healthcare smart labels market is segmented by technology, component, application, end user, and geography. By technology, the market is segmented into RFID labels, NFC (Near Field Communication) tags, sensing labels (temperature, humidity), electronic article surveillance (EAS), and QR Code / 2D barcode labels. By component, the market is segmented into batteries, microprocessors / ICs, transceivers, sensors, and memory. By application, the market is segmented into drug tracking & serialization, cold-chain monitoring, medical equipment tracking, patient identification & safety, and laboratory sample tracking. By end user, the market is segmented into hospitals, pharmaceutical companies, diagnostic laboratories, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| RFID Labels (RAIN UHF) |

| NFC (High Frequency) Tags |

| Sensing Labels |

| Electronic Article Surveillance (EAS) |

| QR Code / 2D Barcode Labels (DataMatrix, QR) |

| Batteries |

| Microprocessors / ICs |

| Transceivers |

| Sensors |

| Memory |

| Drug Tracking & Serialization |

| Cold-chain Monitoring |

| Medical Equipment Tracking |

| Patient Identification & Safety |

| Laboratory Sample Tracking |

| Hospitals |

| Pharmaceutical Companies |

| Diagnostic Laboratories |

| Pharmacies & Retail Pharmacies |

| Contract Manufacturers (CMOs/CDMOs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | RFID Labels (RAIN UHF) | |

| NFC (High Frequency) Tags | ||

| Sensing Labels | ||

| Electronic Article Surveillance (EAS) | ||

| QR Code / 2D Barcode Labels (DataMatrix, QR) | ||

| By Component | Batteries | |

| Microprocessors / ICs | ||

| Transceivers | ||

| Sensors | ||

| Memory | ||

| By Application | Drug Tracking & Serialization | |

| Cold-chain Monitoring | ||

| Medical Equipment Tracking | ||

| Patient Identification & Safety | ||

| Laboratory Sample Tracking | ||

| By End User | Hospitals | |

| Pharmaceutical Companies | ||

| Diagnostic Laboratories | ||

| Pharmacies & Retail Pharmacies | ||

| Contract Manufacturers (CMOs/CDMOs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the growth outlook for the healthcare smart labels market through 2031?

The healthcare smart labels market size is expected to increase from USD 4.28 billion in 2026 to USD 7.21 billion by 2031 at a 13.92% CAGR, anchored by compliance and expanding sensorized use cases.

Which technology areas are most attractive in the healthcare smart labels market?

QR Code and 2D DataMatrix labels remain the largest today, while sensing labels lead growth due to cold-chain and specialty therapy expansion, with RFID and NFC supporting automation and bedside verification.

Which applications will drive the most demand by 2031?

Drug tracking and serialization continue to lead, and cold-chain monitoring records the fastest growth as biologics and vaccines expand and pharmacies, clinics, and home delivery require condition assurance.

Who are the key end users adopting healthcare smart labels?

Pharmaceutical companies lead current adoption, while CMOs/CDMOs are the fastest-growing group; hospitals, pharmacies, and diagnostic laboratories expand combined barcode, RFID, and BLE deployments.

Which regions will offer the strongest opportunities?

North America remains the largest due to DSCSA and hospital digitization, while Asia-Pacific is the fastest-growing region on the back of serialization, biologics manufacturing, and hospital automation.

How does EPCIS 2.0 influence deployments in the healthcare smart labels market?

EPCIS 2.0 enables standardized sharing of both serialization and sensor events across trading partners, which reduces integration friction and boosts the value of sensorized labels in end-to-end workflows.

Page last updated on: