Healthcare IT Sustainability Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

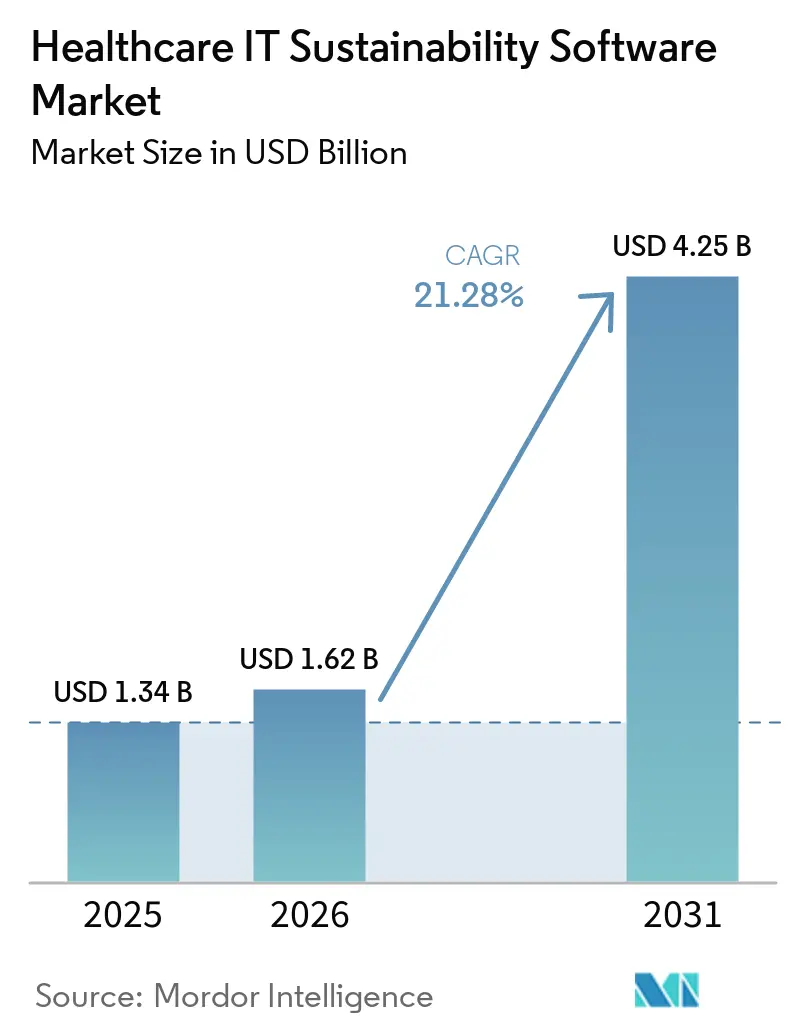

| Market Size (2026) | USD 1.62 Billion |

| Market Size (2031) | USD 4.25 Billion |

| Growth Rate (2026 - 2031) | 21.28% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare IT Sustainability Software Market Analysis by Mordor Intelligence

The healthcare IT sustainability software market size is expected to increase from USD 1.34 billion in 2025 to USD 1.62 billion in 2026 and reach USD 4.25 billion by 2031, growing at a CAGR of 21.28% over 2026-2031. The healthcare sustainability software market is entering a period in which compliance deadlines are shaping buying decisions more directly than discretionary digital spending. Demand is rising because hospitals and health systems now need auditable emissions baselines, clearer energy data, and stronger reporting workflows across large operating footprints. The market is also benefiting from broader digital infrastructure upgrades in hospital estates, where building systems, procurement data, and finance platforms are increasingly linked. Competition is developing along two clear lines, with large enterprise software vendors focusing on integration depth and specialist vendors focusing on healthcare-specific workflows. Growth remains strong, even amid data integration and budget constraints, because mandatory reporting timelines have created a durable demand base for the healthcare sustainability software market.

Key Report Takeaways

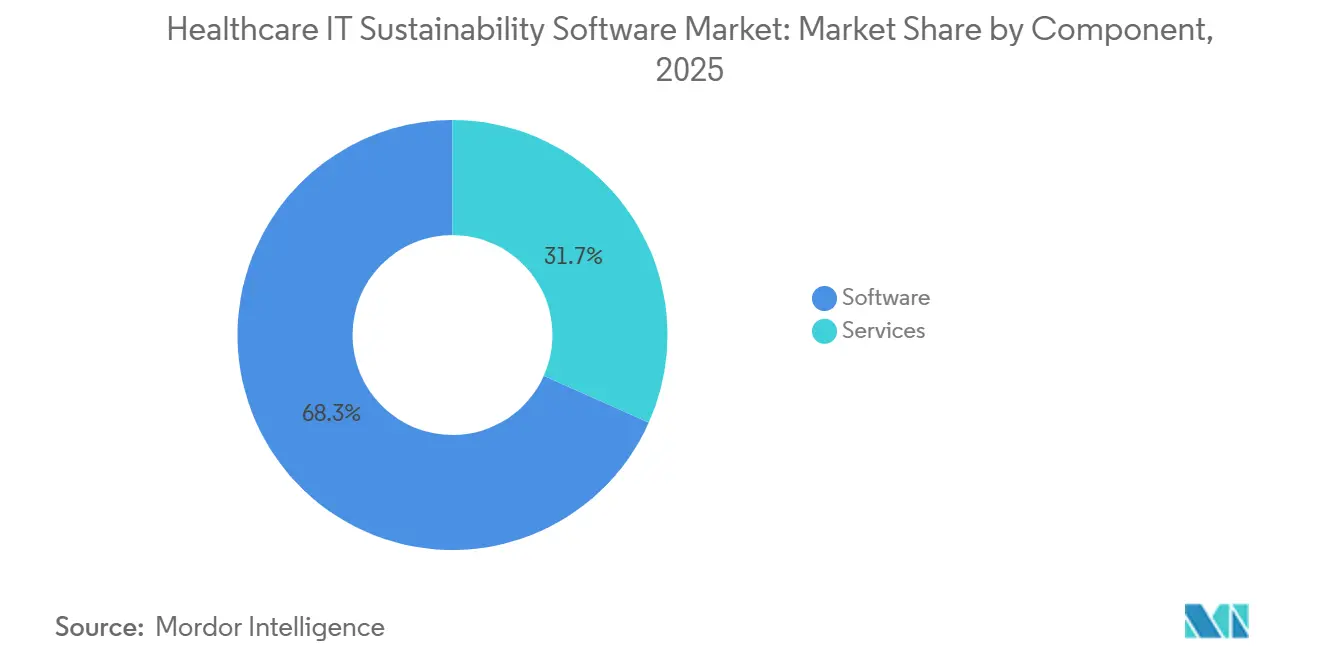

- By component, software held 68.32% of the market in 2025, while services are projected to expand at a 21.97% CAGR through 2031.

- By deployment mode, cloud-based deployment held 72.92% of the healthcare IT sustainability software market in 2025, while hybrid deployment is projected to expand at a 22.83% CAGR through 2031.

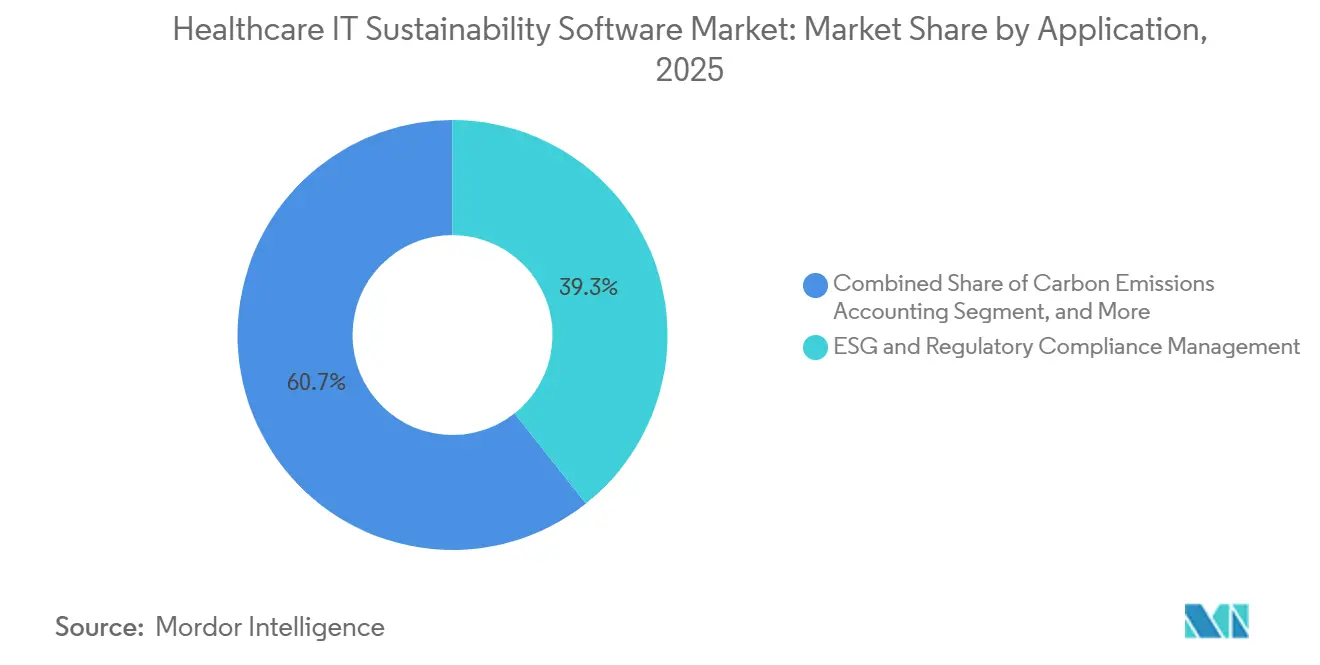

- By application, ESG and regulatory compliance management accounted for 39.34% share in 2025, while sustainability analytics and performance benchmarking are projected to grow at a 24.11% CAGR through 2031.

- By end-user, hospitals accounted for 27.82% share in 2025, while health systems and IDNs are projected to expand at a 22.19% CAGR through 2031.

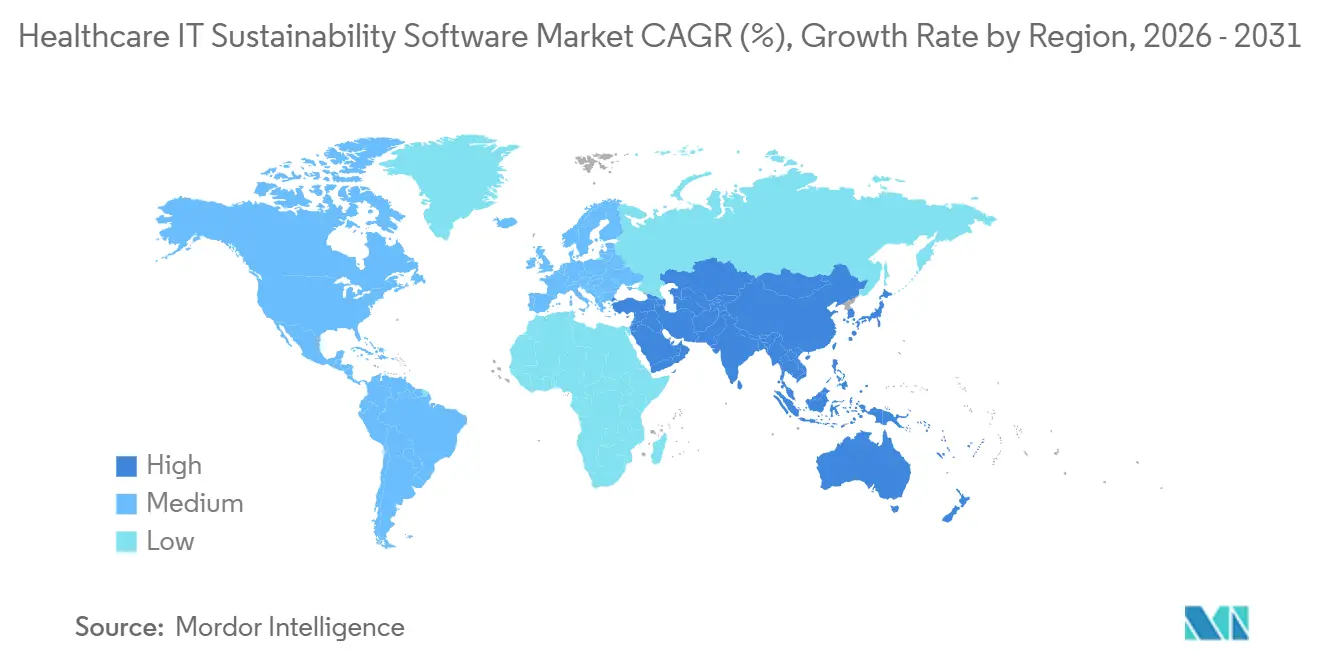

- By geography, North America held 37.64% share in 2025, while the Asia-Pacific is projected to grow at a 23.17% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare IT Sustainability Software Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising Hospital Net Zero Commitments and Decarbonization Mandates | +4.8% | Global, with concentrated compliance pressure in North America, Europe, and Australia | Medium term (2-4 years) |

| Growth of Scope 1, Scope 2, and Scope 3 Emissions Reporting Requirements | +4.3% | North America and Europe, spillover to Asia-Pacific and Middle East | Short term (≤ 2 years) |

| Rising Energy Cost Pressure Across Acute Care and Campus Facilities | +3.2% | North America and Europe, with emerging pressure in Middle East and Asia-Pacific | Short term (≤ 2 years) |

| Expansion of Digital Building Operations in Smart Hospitals | +2.9% | Asia-Pacific, North America, and Europe | Medium term (2-4 years) |

| Need for Automated ESG Data Consolidation Across Multi-Site Health Systems | +2.4% | Global, with IDN and health system density highest in North America and Western Europe | Medium term (2-4 years) |

| Rising Demand for Measurable Sustainability ROI in Healthcare Capital Planning | +1.8% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Hospital Net Zero Commitments and Decarbonization Mandates

Hospital decarbonization targets have shifted from broad policy statements to operational deadlines, accelerating the healthcare IT sustainability software market. NHS England continued to anchor this shift with its net zero pathway, which targets an 80% reduction in directly controlled emissions by 2028-2032 and full net zero by 2040. In the United States, the HHS Decarbonization and Resilience Initiative created a clearer framework for hospitals that want public recognition for annual emissions reporting, which adds reputational weight to more structured data collection. The healthcare IT sustainability software market is, therefore, seeing shorter procurement windows because organizations with near-term decarbonization milestones cannot wait for long manual baseline exercises. Health systems also face wider pressure because healthcare facilities account for 4.4% of global greenhouse gas emissions, which keeps emissions management visible to boards, regulators, and institutional stakeholders.[1]US Department of Health and Human Services, “A Roadmap to Addressing Scope 3 Emissions for Healthcare Organizations,” HHS, hhs.gov As a result, the healthcare IT sustainability software market is becoming more tied to capital planning cycles, governance reviews, and systemwide operating targets.

Growth of Scope 1, Scope 2, and Scope 3 Emissions Reporting Requirements

The expansion of Scope 1, Scope 2, and Scope 3 reporting rules is one of the clearest demand drivers for the healthcare IT sustainability software market. HHS noted that Scope 3 emissions for healthcare organizations often exceed Scope 1 and Scope 2 emissions combined because they include pharmaceuticals, devices, transport, and other external supply chain activities.[2]World Health Organization, “Measuring Greenhouse Gas Emissions in Health Systems,” World Health Organization, who.int WHO also published a measurement framework aligned with the GHG Protocol, which helped turn emissions accounting from a broad ambition into a defined internal capability for health systems. This changes software buying behavior because hospitals moving into Scope 3 work need supplier engagement tools, automated data ingestion, and regular methodology updates that basic spreadsheet systems do not handle well. Massachusetts acute hospitals were already required to submit verified Scope 1 and Scope 2 emissions reports by June 2025, which shows how reporting expectations are moving from voluntary disclosure into more formal oversight. The healthcare IT sustainability software market is benefiting because these requirements make robust reporting architecture harder to defer.

Rising Energy Cost Pressure Across Acute Care and Campus Facilities

Energy cost pressure is strengthening the commercial case for the healthcare IT sustainability software market, especially in large acute care campuses. EnergyCAP reported that 88% of hospitals and clinics experienced utility budget increases in the prior year, and healthcare respondents were 1.4 times more likely than the cross-industry average to report double-digit utility cost spikes. The same source noted that hospitals occupy 4% of U.S. commercial floorspace but consume 9% of commercial building energy, which keeps utility management close to the core of operating performance. This is important for the healthcare IT sustainability software market because energy modules are increasingly being purchased not only for compliance, but also for bill control, benchmarking, and investment prioritization. EnergyCAP also cited ENERGY STAR findings that 30% of hospital energy use could be eliminated through better insights, audits, and targeted upgrades. When cost containment becomes the immediate operating priority, the healthcare IT sustainability software market gains a broader value story than carbon reporting alone.

Expansion of Digital Building Operations in Smart Hospitals

The spread of smart hospital infrastructure is giving the healthcare IT sustainability software market a stronger operational foundation. EUBAC reported that upgrades across 13 public healthcare buildings in Tuscany delivered 40% energy savings and reduced CO₂ emissions by 8,400 tonnes through an integrated building automation and control approach. Johnson Controls also reported that its OpenBlue deployment at Children's of Alabama reduced natural gas use by 69% and generated annual combined energy, operations, and maintenance savings of USD 681,000.[3]Johnson Controls, “How OpenBlue Turns Sustainability into Business Value,” Johnson Controls, johnsoncontrols.com These cases matter because sustainability applications perform better when HVAC, lighting, water, and meter data flow directly from building systems rather than being manually uploaded. European regulatory momentum is also reinforcing this path, as building automation requirements are being phased in through the Energy Performance of Buildings framework. The healthcare IT sustainability software market is therefore gaining from both new digital hospital projects and retrofit programs that improve data visibility at the facility level.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Fragmented Facility and Clinical Data Architecture | -2.8% | Global | Medium term (2-4 years) |

| Long Replacement Cycles for Legacy Building and IT Systems | -2.3% | North America and Europe | Long term (≥ 4 years) |

| Budget Constraints in Small and Mid-Sized Healthcare Providers | -1.9% | South America, Africa, South Asia, and Southeast Asia | Medium term (2-4 years) |

| Cybersecurity and Data Privacy Concerns in Cloud-Based Sustainability Platforms | -1.5% | Global, with heightened sensitivity in Europe and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Facility and Clinical Data Architecture

A major barrier for the healthcare IT sustainability software market is the fragmented way hospitals manage facility data, clinical systems, procurement records, and utility information. A 2025 systematic review in Frontiers in Health Services found that healthcare data ecosystems often operate as isolated and heterogeneous software environments without standardized integration structures. The National Academy of Medicine also highlighted the need for a national health digital and data architecture, underscoring the continued incompleteness of interoperability across the sector. In practical terms, this means sustainability platforms must often connect to building systems, electronic records, meters, and procurement tools that were never designed to exchange data smoothly. The healthcare IT sustainability software market continues to advance under those conditions, but implementation work becomes longer, more service-intensive, and less predictable for mid-tier operators. This slows adoption because many organizations want faster reporting than their current data architecture can support.

Long Replacement Cycles for Legacy Building and IT Systems

Long replacement cycles for hospital infrastructure continue to limit the pace at which the healthcare IT sustainability software market can scale across older estates. Many healthcare campuses still rely on building controls, sub-metering systems, and enterprise platforms that were installed well before current interoperability and reporting needs became standard. That matters because sustainability applications depend on timely data feeds, while older systems often provide only manual exports or infrequent batch files. The healthcare IT sustainability software market therefore expands fastest in facilities that already have modernized automation systems or are undergoing major retrofit and new-build programs. This issue is especially visible in North America and Europe, where large hospital campuses often combine modern digital tools with much older physical infrastructure. As a result, vendors in the healthcare IT sustainability software market must often position integration planning and staged deployment as core parts of implementation rather than optional support.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Commands Revenue While Services Deepen Adoption

Software accounted for 68.32% of the market in 2025, while services are projected to grow at a 21.97% CAGR through 2031. In the healthcare IT sustainability software market, that mix shows that buyers still prefer platforms that can be updated centrally as reporting rules and carbon accounting methods change. The software layer remains the anchor because hospital groups want repeatable workflows for data capture, audit trails, and enterprise reporting instead of one-time advisory work. At the same time, services are expanding quickly because implementation rarely ends with installation in the healthcare sustainability software industry. Every change in reporting scope, supplier data needs, or operating footprint tends to create new demand for configuration, integration, and support.

This relationship gives the healthcare IT sustainability software market a revenue model where software secures the long-term system of record, and services help institutions keep it useful. The input also points to a shift in vendor positioning, with enterprise providers trying to turn large software contracts into multiyear service relationships. ISG assessed 20 providers across sustainability management, sustainability insights, and sustainability compliance categories, and named Workiva, Salesforce, and Oracle as overall leaders, which supports the view that full-suite vendors are competing on breadth as much as functionality. The announcement of SAP sustainability AI agents, with promised reductions of more than 50% in compliance review hours and a fall in scenario simulation time from one day to 20 minutes, also suggests that some service-heavy tasks may be automated over time.[4]SAP, “Autonomous Enterprise, SAP Announces New Sustainability AI Agents,” SAP News, news.sap.com Even so, the healthcare IT sustainability software market is likely to keep meaningful services demand because healthcare operating environments remain highly varied across sites, owners, and regulatory contexts.

By Deployment Mode: Cloud Leads While Hybrid Gains Speed

Cloud-based deployment held 72.92% share in 2025, while hybrid deployment is projected to expand at a 22.83% CAGR through 2031. The healthcare IT sustainability software market size in cloud deployment remained ahead because major vendors already embed sustainability modules into broader cloud suites used for finance, HR, procurement, and supply chain functions. This lowers adoption friction for large health systems that want to extend existing technology relationships rather than introduce a separate stack. Hybrid deployment is still the fastest growing option because many organizations need cloud-scale analytics without moving all facility and operational data into public cloud environments. In the healthcare IT sustainability software market, this is less a matter of technical taste and more a response to compliance architecture.

The healthcare sustainability software industry is also seeing hybrid models gain favor among health systems that operate across several regulatory jurisdictions. These organizations need stronger control over sensitive operational data while still supporting complex Scope 3 calculations and systemwide benchmarking. On-premise deployments continue to lose share, but they remain relevant in government owned hospital networks and other settings where sovereignty requirements are stricter. Vendor documentation on data residency, security controls, and design requirements is now a routine part of procurement evaluations under privacy-focused governance frameworks. The healthcare sustainability software market, therefore, keeps cloud at the center of scale, but hybrid models are becoming the practical bridge between compliance needs and the ambition for advanced analytics.

By Application: Compliance Leads While Analytics Expands Faster

ESG and regulatory compliance management accounted for 39.34% of the market in 2025, while sustainability analytics and performance benchmarking is projected to advance at a 24.11% CAGR through 2031. That split shows that the healthcare IT sustainability software market is still led by immediate reporting obligations, but it is steadily moving toward performance management. Many organizations first entered the category because they needed audit-ready disclosure tools, standardized workflows, and defensible emissions records. Once those basics were in place, the next step became scenario modeling, peer comparison, and identification of carbon and cost reduction opportunities. In the healthcare IT sustainability software market, that progression reflects a maturing buyer base rather than a change in underlying policy pressure.

The compliance segment still leads because regulatory deadlines arrive before most providers develop full operational maturity in sustainability analytics. California reporting expectations, European disclosure requirements, and national climate commitments have all increased the need for accurate reporting foundations. The input also groups energy and utility optimization management with carbon emissions accounting and reporting as a strong secondary cluster, which matches the link between operating cost control and emissions measurement. Environmental resource management remains smaller, but it is gaining support as water and waste metrics become more visible in hospital sustainability programs and accreditation-linked practices.[5]Practice Greenhealth, “2025 Health Care Sustainability Metrics Report,” Practice Greenhealth, practicegreenhealth.org The healthcare sustainability software market size for advanced analytics is therefore rising because organizations that began with compliance now want tools that support operating improvement as well.

By End-User Industry: Hospitals Form the Base While IDNs Scale Faster

Hospitals accounted for 27.82% of the healthcare IT sustainability software market share in 2025, while health systems and IDNs are projected to grow at a 22.19% CAGR through 2031. Hospitals remain the largest absolute user base because they represent the broadest installed footprint of care delivery facilities. Even so, the healthcare IT sustainability software market is scaling faster in integrated delivery networks because centralized procurement and governance make enterprise deployment more efficient. A platform spanning 20, 50, or 100 facilities delivers a stronger return profile than separate site-by-site licenses. This gives large systems a clear advantage when turning sustainability reporting into a managed operating capability.

The same consolidation trend also creates added integration complexity because acquired community hospitals often bring older systems and fragmented data structures into larger groups. That is why the healthcare IT sustainability software market sees faster demand growth in IDNs, but not always simpler implementation. Ambulatory surgical centers, clinics, and physician practices remain less penetrated because their energy intensity is lower, and vendor offerings have historically been built for larger institutions. Long-term care operators and academic medical centers exhibit different adoption patterns: long-term care responds to national emissions frameworks, while academic centers link sustainability disclosure to research and community benefit priorities. The healthcare sustainability software market continues to widen across end users, but platform depth and procurement speed remain strongest where scale, governance, and reporting pressure converge.

Geography Analysis

North America held 37.64% share of the market in 2025, and that lead reflects the strongest combination of regulatory pressure, digital readiness, and large enterprise healthcare operators. The healthcare IT sustainability software market share in North America remained the highest because the region has a dense base of integrated health systems, IDNs, and academic medical centers that can support enterprise-wide reporting and analytics. In the United States, emissions reporting expectations, climate pledges, and procurement maturity are pushing hospitals toward more formal software-backed sustainability management. HHS guidance on Scope 3 and broader decarbonization planning also supports a shift from manual reporting to more structured data systems. Canada is also contributing to the healthcare IT sustainability software market through smart infrastructure models, including the long-term digital hospital partnership highlighted at Cortellucci Vaughan Hospital.

Europe is shaped by reporting regulation and building efficiency mandates, which gives the healthcare IT sustainability software market a structurally policy-led profile. Germany stands out because sector participants expect a large share of hospitals to fall under sustainability reporting obligations, and DKTIG has partnered on a sector-focused sustainability management software platform aligned with CSRD and ESRS requirements. The United Kingdom is also advancing through the NHS net zero pathway and trust-level green plans that place more emphasis on energy monitoring and reporting systems. Southern Europe is benefiting from retrofit economics, as the Tuscany healthcare building upgrade showed a practical path from automation investment to measurable energy savings and lower emissions. South America remains earlier in adoption, but large private hospital groups in Brazil and Argentina are the most likely entry point as external capital markets place more weight on ESG readiness.

Asia-Pacific is projected to expand at a 23.17% CAGR through 2031, making it the fastest-growing regional part of the healthcare IT sustainability software market size. The region benefits from a mix of disclosure momentum, digital hospital investment, and large healthcare organizations that are strengthening enterprise data capabilities. Japan offers a visible example, where Astellas adopted IBM Envizi ESG Suite for CSRD and ESRS-related disclosure work, and Fujitsu Japan started a project with Osaka Hospital around generative AI and sustainable hospital management. India is beginning to show interest as healthcare digitalization advances alongside broader climate commitments. The Middle East and Africa remain smaller in current value, but they are strategically relevant because ESG infrastructure investment is rising under national transformation agendas, especially in Saudi Arabia. The healthcare IT sustainability software market is therefore broadening geographically, with North America leading in installed scale, Europe in policy structure, and Asia-Pacific in growth speed.

Competitive Landscape

The healthcare IT sustainability software market remains moderately fragmented, with large enterprise software vendors and specialist providers competing on different strengths. IBM Corporation, SAP SE, Oracle Corporation, and Microsoft Corporation benefit from installed relationships in ERP, finance, cloud, and supply chain systems used by hospital groups. In the healthcare IT sustainability software market, the installed base reduces switching friction because sustainability modules can be layered onto platforms that health systems already know. SAP reinforced this position when it was recognized as a leader in carbon accounting and management applications, with emphasis on its ERP-embedded model that connects financial, operational, and sustainability data.

Specialist vendors compete differently in the healthcare IT sustainability software market, focusing on workflow depth rather than enterprise breadth. Cority Software, EnergyCAP, EcoOnline, Intelex Technologies, and FigBytes are positioned around reporting templates, utility bill management, environmental compliance support, and Scope 3 supply chain features. Cority's Cortex AI launch in December 2025 is a good example, because it introduced invoice scanning and other automation tools that address the manual data capture burden smaller operators often face. EnergyCAP also retained visibility in cost and utility management, which fits hospitals that enter the category through energy control before broader ESG programs mature. This leaves room in the sub-enterprise segment, where ambulatory centers and physician groups still rely heavily on spreadsheets and have not yet settled around a dominant vendor.

A third competitive angle comes from building automation companies that are extending into the healthcare IT sustainability software market through vertically linked data and reporting capabilities. Johnson Controls, Schneider Electric, and Honeywell can connect metering, controls, and building operations more directly with energy and carbon reporting layers. Johnson Controls showed this value path through Children's of Alabama and Cortellucci Vaughan Hospital, where digital building systems supported measurable savings and broader sustainability outcomes. SAP also strengthened its position with sustainability AI agents that are expected to cut compliance review time and speed scenario analysis, which shows how larger vendors are automating tasks that once created service dependence. The healthcare IT sustainability software market still has open space, but the strongest competitive positions now sit with vendors that can combine audit-ready reporting, integration depth, and lower implementation friction.

Healthcare IT Sustainability Software Industry Leaders

IBM Corporation

SAP SE

Microsoft Corporation

Oracle Corporation

Schneider Electric SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: SAP SE announced that its new suite of sustainability AI agents will reach general availability by end of 2026. Beta capabilities include a Footprint Optimization Agent that cuts carbon scenario simulation time from one day to 20 minutes, and a Sustainability Regulatory Readiness Agent that reduces CSRD materiality-to-reporting scope mapping effort by more than 50%, with direct applicability to large hospital systems managing multi-jurisdictional ESG reporting.

- April 2026: IBM launched Envizi Emissions Calculations in Excel, an Excel add-in that brings standardized GHG Protocol-aligned emissions calculations directly into spreadsheet workflows for sustainability teams beginning or scaling Scope 3 emissions accounting. Available via the Microsoft App Marketplace, the tool lowers the barrier to entry for smaller healthcare providers not yet operating enterprise sustainability platforms.

- January 2026: SAP SE and Fresenius announced a strategic partnership to build a jointly developed, scalable healthcare platform for connected, data-driven hospital operations, with both companies committing a mid-three-digit million euro investment in the medium term. The platform is anchored in SAP Business Data Cloud and SAP Business AI, and is designed to support interoperable healthcare data management aligned with HL7 FHIR standards.

- December 2025: Cority launched Cortex AI, an embedded intelligence layer for its CorityOne platform, introducing a Sustainability Invoice Scanning Agent that uses AI to extract emissions-relevant data from utility invoices and feed it directly into carbon emissions calculations, eliminating a major manual data collection step for healthcare sustainability teams.

Global Healthcare IT Sustainability Software Market Report Scope

Healthcare IT Sustainability Software refers to a category of digital solutions designed to assist healthcare organizations, including hospitals, clinics, and life sciences companies, in managing their environmental impact. These platforms optimize IT infrastructure, reduce energy consumption, monitor carbon emissions, and ensure compliance with ESG standards. By integrating sustainability data into healthcare workflows such as electronic health records, medical devices, and data centers, these solutions enable audit-ready reporting, regulatory compliance, and the adoption of environmentally sustainable healthcare operations.

The Healthcare IT Sustainability Software Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud Based, On Premise, and Hybrid), Application (Energy and Utility Optimization Management, Carbon Emissions Accounting and Reporting, Environmental Resource Management (Water and Waste), ESG and Regulatory Compliance Management, and Sustainability Analytics and Performance Benchmarking), End-User Industry (Hospitals, Health Systems and IDNs, Ambulatory Surgical Centers, Clinics and Physician Practices, Long-Term Care Facilities, Academic and Teaching Medical Centers, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | |

| Services | Implementation and Integration Services |

| Support and Maintenance Services |

| Cloud Based |

| On Premise |

| Hybrid |

| Energy and Utility Optimization Management |

| Carbon Emissions Accounting and Reporting |

| Environmental Resource Management (Water and Waste) |

| ESG and Regulatory Compliance Management |

| Sustainability Analytics and Performance Benchmarking |

| Hospitals (Standalone and Multi-specialty) |

| Health Systems and IDNs |

| Ambulatory Surgical Centers |

| Clinics and Physician Practices |

| Long-Term Care Facilities |

| Academic and Teaching Medical Centers |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Component | Software | |

| Services | Implementation and Integration Services | |

| Support and Maintenance Services | ||

| By Deployment Mode | Cloud Based | |

| On Premise | ||

| Hybrid | ||

| By Application | Energy and Utility Optimization Management | |

| Carbon Emissions Accounting and Reporting | ||

| Environmental Resource Management (Water and Waste) | ||

| ESG and Regulatory Compliance Management | ||

| Sustainability Analytics and Performance Benchmarking | ||

| By End-User Industry | Hospitals (Standalone and Multi-specialty) | |

| Health Systems and IDNs | ||

| Ambulatory Surgical Centers | ||

| Clinics and Physician Practices | ||

| Long-Term Care Facilities | ||

| Academic and Teaching Medical Centers | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2026 size of the healthcare IT sustainability software sector?

The healthcare IT sustainability software market stood at USD 1.62 billion in 2026 and is forecast to reach USD 4.25 billion by 2031 at a 21.28% CAGR.

What is driving adoption among hospitals and health systems?

The main drivers are emissions reporting rules, net zero targets, utility cost pressure, and the wider use of digital building systems across hospital campuses.

Which application area is growing the fastest?

Sustainability analytics and performance benchmarking is the fastest-growing application, with a projected 24.11% CAGR through 2031.

Which deployment model is most widely used?

Cloud-based deployment led with 72.92% share in 2025, while hybrid deployment is growing faster as organizations balance analytics scale with data control needs.

Which regions are leading and growing fastest?

North America led with 37.64% share in 2025, while Asia-Pacific is expected to post the fastest growth at a 23.17% CAGR through 2031.

Why are integrated delivery networks adopting faster than standalone providers?

IDNs can spread platform costs across large multi-site portfolios and manage procurement centrally, which improves return on investment and supports enterprise reporting.

Page last updated on: