Healthcare Environmental Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

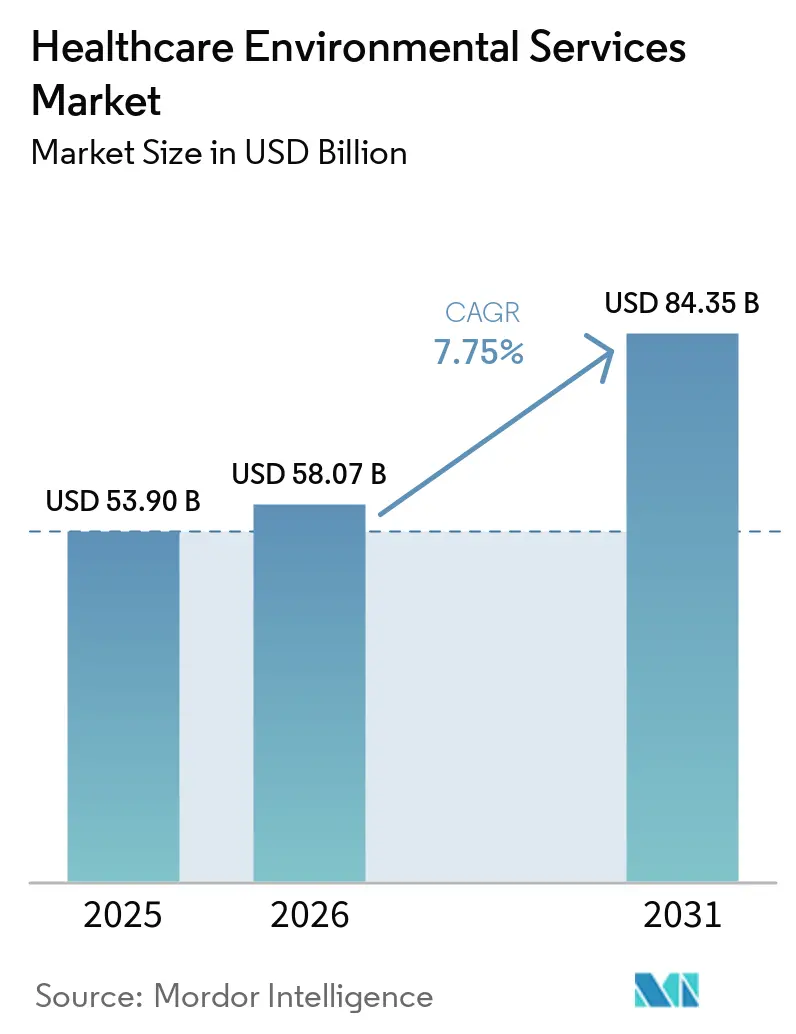

| Market Size (2026) | USD 58.07 Billion |

| Market Size (2031) | USD 84.35 Billion |

| Growth Rate (2026 - 2031) | 7.75% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Environmental Services Market Analysis by Mordor Intelligence

The Healthcare Environmental Services Market size is expected to increase from USD 53.90 billion in 2025 to USD 58.07 billion in 2026 and reach USD 84.35 billion by 2031, growing at a CAGR of 7.75% over 2026-2031.

Environmental services are now closely integrated with clinical quality, infection prevention, and facility compliance, driven by active national infection-reduction targets in acute care settings. Hospitals, ambulatory facilities, and long-term care operators increasingly rely on specialist vendors as cleaning, waste handling, linen workflows, pest control, and staff training significantly impact audit readiness, patient experience, and operational continuity. The healthcare environmental services market is influenced by leading integrated providers standardizing processes across multiple sites, while smaller regional firms focus on niche areas like waste management, linen services, pest control, and local support contracts. Labor turnover and wage pressures are prompting providers to adopt digital staffing tools, room-turnover systems, and automation to reduce reliance on headcount while maintaining compliance.

Key Report Takeaways

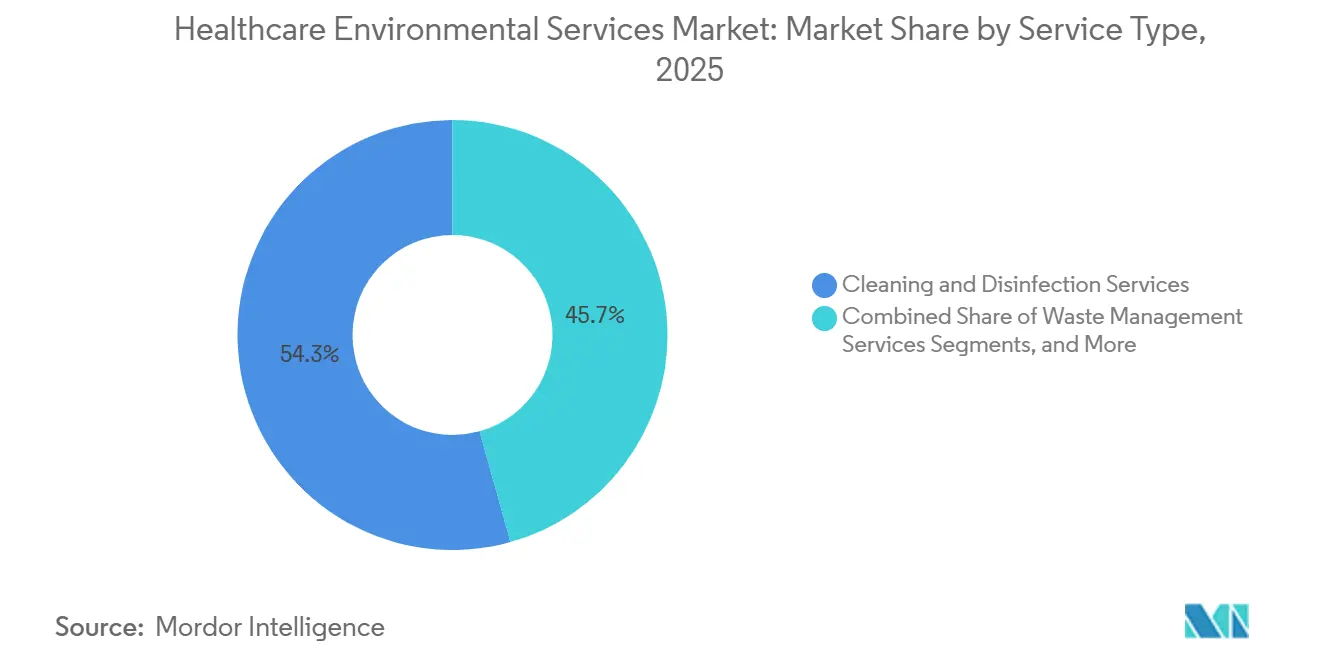

- By service type, cleaning & disinfection services held 54.35% of revenue in 2025, while linen & laundry services are projected to grow at an 8.75% CAGR through 2031.

- By delivery model, scheduled services held 82.45% of the healthcare environmental services market share in 2025, while on-demand services are expected to expand at an 8.25% CAGR through 2031.

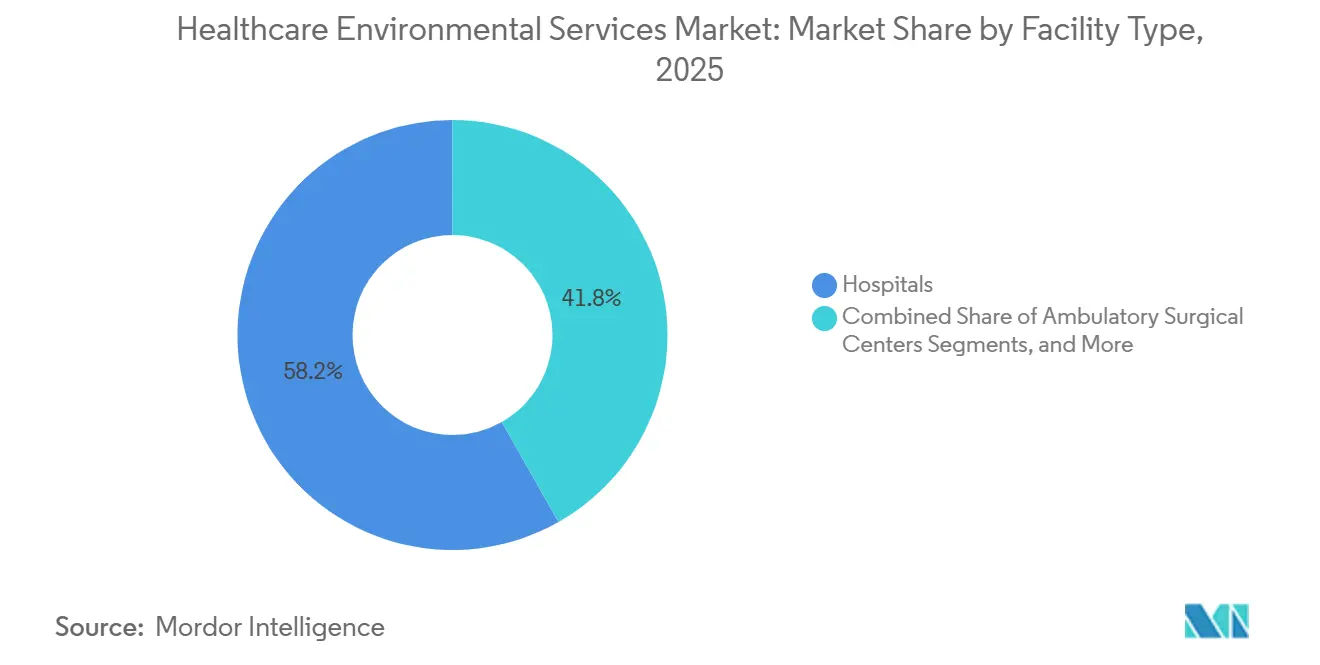

- By facility type, hospitals accounted for 58.22% of the healthcare environmental services market size in 2025, while ambulatory surgical centers are projected to advance at a 9.32% CAGR through 2031.

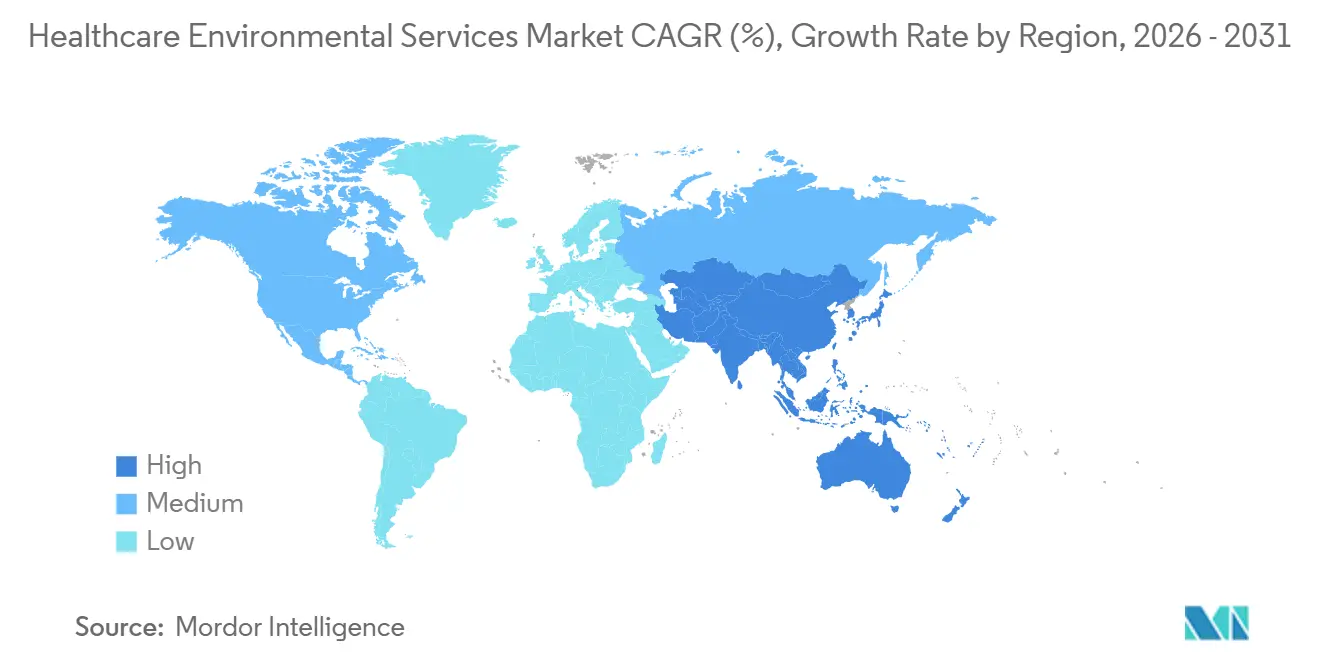

- By geography, North America held 39.77% revenue share in 2025, while Asia-Pacific is expected to grow at an 8.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare Environmental Services Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| HAI prevention and stricter hygiene standards | +2.5% | Global, with acute intensity in North America and Europe | Short term (≤ 2 years) |

| Outsourcing to lift HCAHPS and patient loyalty scores | +1.8% | North America core, with spillover to Australia and the UK | Medium term (2-4 years) |

| Higher hospital and ambulatory throughput | +1.5% | Global, particularly strong in Asia-Pacific and North America | Medium term (2-4 years) |

| Tightening medical and pharmaceutical waste regulations | +1.2% | North America and Europe, with secondary impact in Asia-Pacific | Medium term (2-4 years) |

| WASH and waste-service gaps in emerging markets | +0.9% | Asia-Pacific, Middle East and Africa, and South America | Long term (≥ 4 years) |

| Reusable sharps and circular-medtech programs | +0.6% | United Kingdom, Europe, and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

HAI Prevention and Stricter Hygiene Standards

Infection control remains a critical driver in the healthcare environmental services market, with surface hygiene, waste handling, and validated cleaning protocols now integral to patient safety. The HHS has set ambitious targets for reducing CLABSI, hospital-onset MRSA bacteremia, and CDI, emphasizing the need for enhanced disinfection methods. Persistent challenges with spore-forming pathogens are pushing providers to adopt advanced technologies like UV-C systems, electrostatic applications, and rigorous cleaning performance verification. Facilities are increasingly linking environmental service performance to infection outcomes rather than cleaning frequency.

Outsourcing to Lift HCAHPS and Patient Loyalty Scores

Patient experience scores are becoming increasingly important in the healthcare environmental services market, as cleanliness impacts both quality outcomes and patient loyalty. Sodexo expanded its partnership with Adventist Health, adding sites and employees, reflecting the trend of deepening outsourced EVS relationships. Similarly, Aramark’s agreement with the University of Pennsylvania Health System highlights the growing preference for partnerships that combine environmental services with other support functions. Outsourced providers leverage advanced tools across multiple sites, offering consistent cleaning, robust reporting, and flexible staffing solutions.

Higher Hospital and Ambulatory Throughput

Increased patient throughput is driving higher service frequency in the healthcare environmental services market, with workload influenced by room turnover and care transitions. The shift of surgeries and diagnostics to ambulatory settings has led to more cleaning events, faster turnaround expectations, and stricter disinfection standards. Ambulatory surgical centers, in particular, require efficient terminal cleaning to maintain scheduling. Service providers are adapting staffing models and workflows to meet these demands without compromising infection control.

Tightening Medical and Pharmaceutical Waste Regulations

Stricter waste compliance regulations are driving growth in the healthcare environmental services market, with facilities facing tighter requirements for hazardous and pharmaceutical waste management. The adoption of the EPA Hazardous Waste Pharmaceuticals Rule and amendments to generator rules have increased the focus on proper waste classification and disposal. The shift to electronic manifests is enhancing audit visibility, favoring providers with digital chain-of-custody systems and trained compliance workflows. Poor pharmaceutical waste management remains a global concern, further supporting demand for specialized waste capabilities.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| In-house EVS insourcing by large health systems | -1.5% | North America, with an emerging trend in the United Kingdom and Europe | Medium term (2-4 years) |

| Labor intensity, wage inflation, and turnover | -1.2% | Global, particularly acute in North America | Short term (≤ 2 years) |

| Incineration permitting and treatment-capacity constraints | -0.7% | North America and Europe, with specific concern in emerging Asia-Pacific | Medium term (2-4 years) |

| Waste misclassification and weak segregation practices | -0.4% | Global, with highest risk in the Middle East and Africa and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

In-house EVS Insourcing by Large Health Systems

Large health systems are increasingly insourcing environmental services to gain tighter control over infection prevention, cleanliness, and labor relations. This approach enables multi-hospital networks to bring specific functions in-house or adopt hybrid models while maintaining cleaning and waste handling needs. Executives are drawn to insourcing for its potential to enhance service consistency, staff accountability, and alignment with internal quality goals. However, insourcing often underestimates costs related to hiring, training, compliance monitoring, and technology maintenance, which become evident post-implementation. Accreditation and audit requirements continue to anchor many systems to specialist expertise, limiting the extent of pure insourcing.

Labor Intensity, Wage Inflation, and Turnover

Labor challenges remain a critical constraint in the healthcare environmental services market due to its reliance on frontline staffing. High turnover rates and wage pressures strain labor budgets, impacting nonclinical support functions. In environmental services, frequent staff churn increases quality risks as new hires require infection-control training and familiarity with site-specific protocols. Providers with strong retention programs, clear training pathways, and stable supervision maintain a competitive edge by ensuring consistent service quality. However, wage inflation and staffing instability continue to pressure margins, disrupt scheduling, and slow the expansion of outsourced contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Disinfection Dominates, But Linen Leads Growth

Cleaning & Disinfection Services dominate the healthcare environmental services market, holding 54.35% of the market share in 2025. This leadership reflects the critical need for surface decontamination in hospitals, clinics, and long-term care settings. The segment remains essential for infection prevention, as lapses in hygiene can impact patient outcomes, audits, and trust. Spending in this category remains resilient despite budget reviews.

Linen & Laundry Services are projected to grow at an 8.75% CAGR through 2031, making it the fastest-growing segment. Hospitals are increasingly outsourcing laundering to better manage utilities, water use, and contamination control. Innovations like RFID tracking and infection-barrier textiles are transforming linen services into critical clinical support functions.

By Delivery Model: Scheduled Contracts Anchor Revenue, On-demand Reshapes Margins

Scheduled Services accounted for 82.45% of revenue in 2025, anchoring the healthcare environmental services market. Fixed contracts ensure predictable cleaning schedules, defined staffing, and reliable documentation, making them the preferred choice for hospitals and long-term care facilities. These agreements also support inspection readiness and operational consistency.

On-demand Services are expected to grow at an 8.25% CAGR through 2031, driven by tools like real-time dispatch and occupancy signals that enhance labor efficiency. This model provides detailed records of cleaning activities, making it attractive for facilities prioritizing speed, auditability, and efficiency.

By Facility Type: Hospitals Hold the Anchor, ASCs Lead the Momentum

Hospitals accounted for 58.22% of the healthcare environmental services market size in 2025, solidifying their role as the largest demand center. Their 24/7 operations, higher infection-control needs, and diverse service requirements drive demand for comprehensive services, including cleaning, waste management, and staff training.

Ambulatory Surgical Centers are projected to grow at a 9.32% CAGR through 2031, fueled by the shift of procedures to outpatient settings. This trend increases demand for short-cycle cleaning, even in smaller facilities, while clinics, imaging centers, and laboratories further contribute to market growth.

Geography Analysis

In 2025, North America held a 39.77% share of the healthcare environmental services market, maintaining its leading position by revenue. The U.S. drives this dominance due to stringent cleanliness standards tied to reimbursements, strong accreditation benchmarks, and a mature outsourcing landscape. Sodexo's January 2026 partnership with Adventist Health, covering 26 sites with a projected value of USD 70 million, highlights the scale large providers can achieve. The region benefits from a diverse mix of vendors addressing cleaning, linen, pest control, hazardous waste, and training needs across hospital networks. Additionally, stricter pharmaceutical waste regulations in several states are driving recurring compliance demand for specialist service providers.

Europe remains a key player in the healthcare environmental services market, though outsourcing depth varies by country and procurement models. The UK and parts of continental Europe support broad outsourcing, while others retain more activities under hospital control. Vendors must adapt to local labor laws, union expectations, and public-sector contracting norms. Rising sustainability and waste management demands are increasing the value of specialist providers in pharmaceutical waste, linen handling, and traceable environmental reporting.

Asia-Pacific is projected to grow at an 8.98% CAGR through 2031, making it the fastest-growing region in the healthcare environmental services market. Growth is driven by expanding healthcare capacity, rising patient volumes, and gaps in water, sanitation, hygiene, and waste services in lower-middle-income regions. Developed markets like Japan, South Korea, and Australia are nearing European environmental standards, while Southeast Asia offers significant opportunities for full-scope outsourcing. The Middle East, Africa, and South America are gradually formalizing environmental service requirements, supported by public health initiatives around WASH and safer healthcare waste practices.

Competitive Landscape

In the healthcare environmental services market, large integrated providers compete for anchor hospital contracts, while smaller firms focus on specialized service lines. Industry leaders like Sodexo, Aramark, ISS, Compass Group, Rentokil Initial, and ABM Industries dominate broad environmental and support service contracts. Meanwhile, Ecolab, Daniels Health, Clean Harbors, and WM Healthcare Solutions excel in niches such as disinfection, sharps management, and regulated waste.

Competition is shifting toward tools that enhance productivity while maintaining infection-control standards. Sodexo's expansion with Adventist Health highlights the integration of UVD robots, dynamic cleaning tools, and predictive data features, embedding technology into contracts. Similarly, Aramark's agreement with the University of Pennsylvania Health System includes AIWX staffing tools and robotic applications across 7 hospitals and nearly 4,000 beds. Providers gain a competitive edge by demonstrating faster room turnovers, clearer audit trails, and optimized labor deployment at scale.

Opportunities are strongest in pharmaceutical waste compliance, reusable sharps programs, and workforce training, where demand is clear but supply remains fragmented. Daniels introduced the 24L SHARPSGUARD eco container in June 2025, made from 80% post-consumer recycled plastic, including 40% recovered from healthcare waste, showcasing the growing importance of circular products. Specialist providers are expanding local capacities to meet outpatient and ambulatory demand, moving beyond reliance on national networks.

Healthcare Environmental Services Industry Leaders

ABM Industries Incorporated

Compass Group PLC

Aramark

Healthcare Services Group, Inc.

Sodexo S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Clean Harbors acquired Terra Nova Solutions for USD 225 million, adding five waste treatment and processing sites in the Carolinas. The acquisition enhances wastewater treatment, solidification, and hazardous waste processing capacity, with projected annual revenues of USD 45-50 million and USD 15 million in adjusted EBITDA.

- January 2026: Sodexo expanded its environmental services contract with Adventist Health to 26 sites across California, Hawaii, and Oregon. The USD 70 million contract adds over 400 employees and incorporates UVD robots, predictive cleaning analytics, and AI-driven staffing platforms at 15 new sites.

- January 2026: Daniels Health opened its first medical waste facility in Long Island, New York, strengthening its U.S. treatment and transfer infrastructure. The facility increases capacity for regulated medical waste, sharps, and biohazardous materials to meet growing outpatient and ASC market demands in the Northeast.

- December 2025: Clean Harbors secured a 3-year, USD 110 million contract at Joint Base Pearl Harbor-Hickam for PFAS water and regenerative carbon filtration. The contract is expected to add USD 15-30 million in annual earnings and grow its PFAS services business by 20% in 2026.

Global Healthcare Environmental Services Market Report Scope

As per the scope of the report, Healthcare Environmental Services (EVS) refers to the specialized cleaning, disinfecting, and waste management processes used in medical facilities. Far beyond standard housekeeping, EVS is a vital component of infection control, functioning as the facility's "immune system" to prevent the spread of pathogens and hospital-acquired infections (HAIs).

The healthcare environmental services market is segmented by service type, delivery model, facility type, and geography. By service type, the market includes cleaning & disinfection services, linen & laundry services, waste management services, pest control services, and staff training & consultancy services. By delivery model, the market is segmented into scheduled services and on-demand services. By facility type, the market is categorized into hospitals, ambulatory surgical centers, clinics & physician offices, laboratories & research facilities, long-term care facilities, and diagnostic & imaging centers. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Cleaning & Disinfection Services |

| Linen & Laundry Services |

| Waste Management Services |

| Pest Control Services |

| Staff Training & Consultancy Services |

| Scheduled Services |

| On-demand Services |

| Hospitals |

| Ambulatory Surgical Centers |

| Clinics & Physician Offices |

| Laboratories & Research Facilities |

| Long-term Care Facilities |

| Diagnostic & Imaging Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Cleaning & Disinfection Services | |

| Linen & Laundry Services | ||

| Waste Management Services | ||

| Pest Control Services | ||

| Staff Training & Consultancy Services | ||

| By Delivery Model | Scheduled Services | |

| On-demand Services | ||

| By Facility Type | Hospitals | |

| Ambulatory Surgical Centers | ||

| Clinics & Physician Offices | ||

| Laboratories & Research Facilities | ||

| Long-term Care Facilities | ||

| Diagnostic & Imaging Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the healthcare environmental services space in 2026?

The healthcare environmental services market stands at USD 58.07 billion in 2026 and is forecast to reach USD 84.35 billion by 2031 at a 7.75% CAGR.

Which service category leads revenue generation?

Cleaning & Disinfection Services led with 54.35% of revenue in 2025, reflecting the non-discretionary role of surface hygiene across healthcare settings.

Which facility type is growing the fastest through 2031?

Ambulatory Surgical Centers are projected to expand at a 9.32% CAGR through 2031, supported by the migration of more procedures into outpatient settings.

Which region is expanding the fastest?

Asia-Pacific is the fastest-growing region, with an 8.98% CAGR through 2031, driven by healthcare capacity expansion and persistent WASH and waste-service gaps.

Why are hospitals outsourcing environmental services more often?

More hospitals are using specialist vendors because cleanliness, waste handling, linen management, and audit readiness now affect patient experience, infection control, and compliance at the same time.

What is the main operating risk for providers?

Labor intensity remains the biggest operating challenge because wage inflation, turnover, and training demands can compress margins and weaken service consistency if staffing is unstable.

Page last updated on: