Healthcare Data Storage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.49 Billion |

| Market Size (2031) | USD 14.70 Billion |

| Growth Rate (2026 - 2031) | 14.45% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Data Storage Market Analysis by Mordor Intelligence

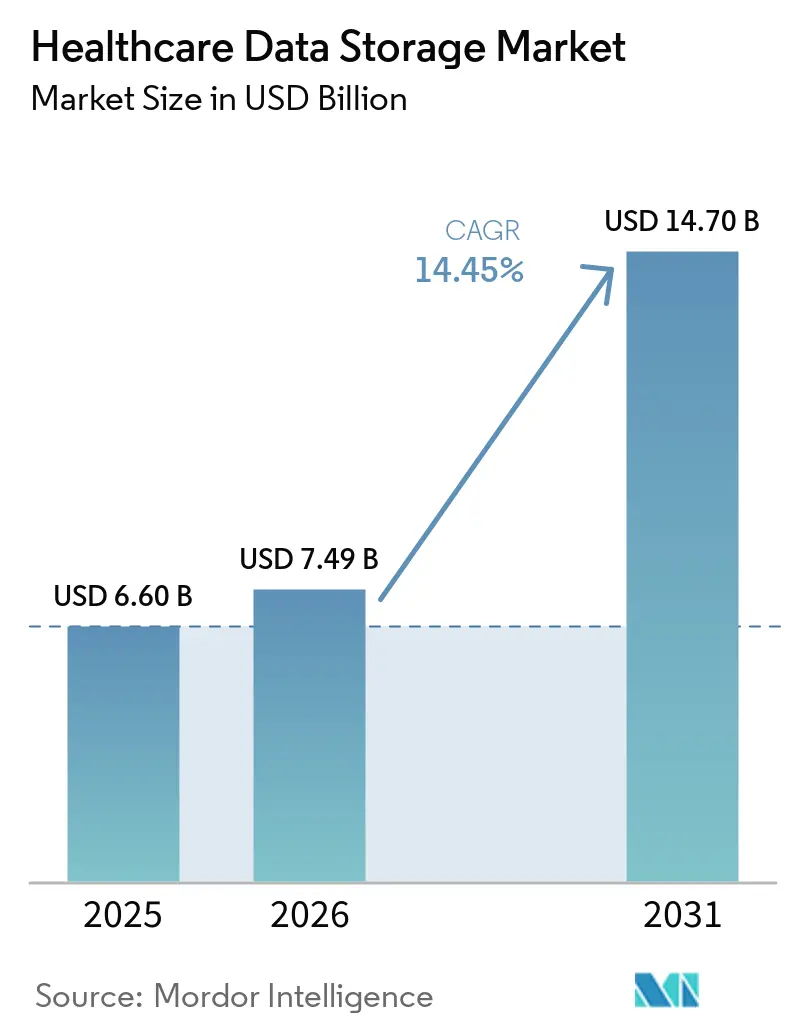

The healthcare data storage market size is expected to increase from USD 6.60 billion in 2025 to USD 7.49 billion in 2026 and reach USD 14.70 billion by 2031, growing at a CAGR of 14.45% over 2026-2031. Cloud deployment is advancing as clinical imaging, analytics, and disaster recovery move to scalable services with proven uptime and global access. Interoperability programs and real-time data exchange are expanding data volumes that must be retained across longer time frames, which amplifies lifecycle-tiered storage adoption. European data-residency rules are steering sensitive workloads to sovereign or in-region deployments, while U.S. interoperability and prior-authorization rules increase the cadence and volume of data transactions across payers and providers. Genomics and multi-omics pipelines increase throughput and persist large files, making object storage and hybrid cloud more attractive. The healthcare data storage market will see budgets shift from capital refresh cycles to subscription, lifecycle-tiering, and immutable backup strategies as risk and compliance demands increase.

Key Report Takeaways

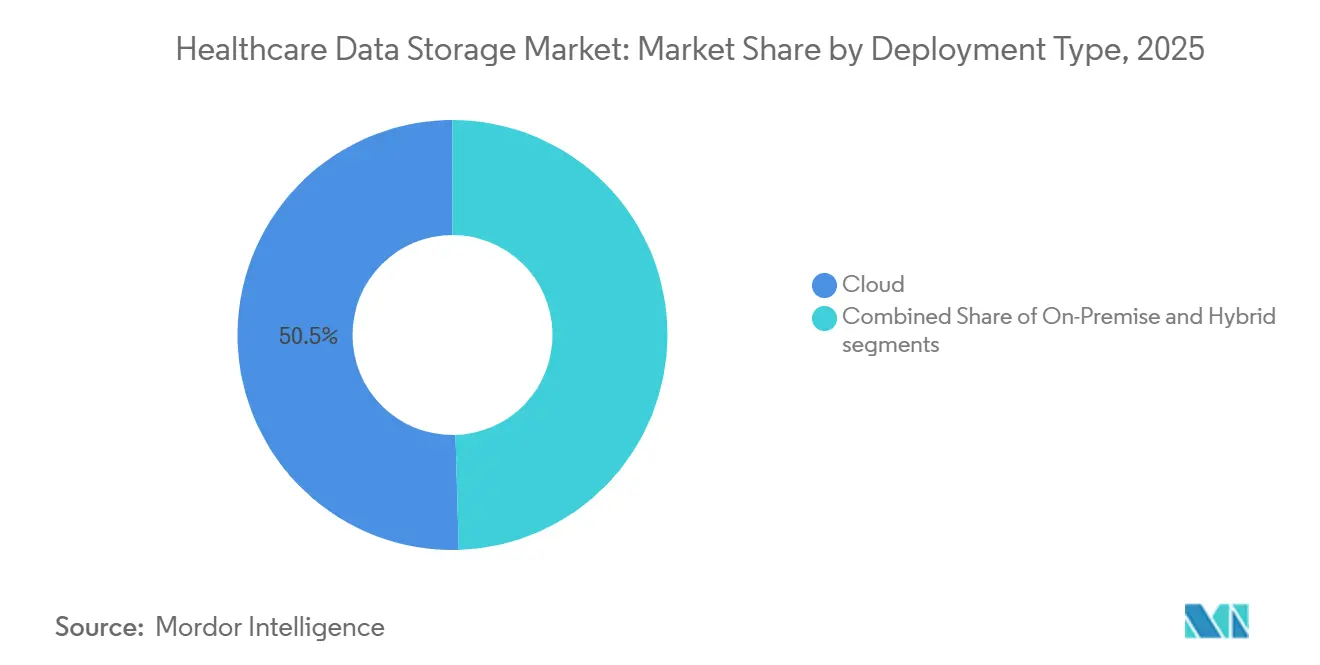

- By deployment mode, cloud led with 50.46% of the healthcare data storage market share in 2025, while it is forecast to expand at a 16.21% CAGR through 2031.

- By architecture, block storage held 47.43% share in 2025, while file storage is projected to grow at a 15.26% CAGR through 2031.

- By storage medium, SSD/Flash accounted for 46.39% share in 2025, while HDD is set to post a 15.47% CAGR through 2031.

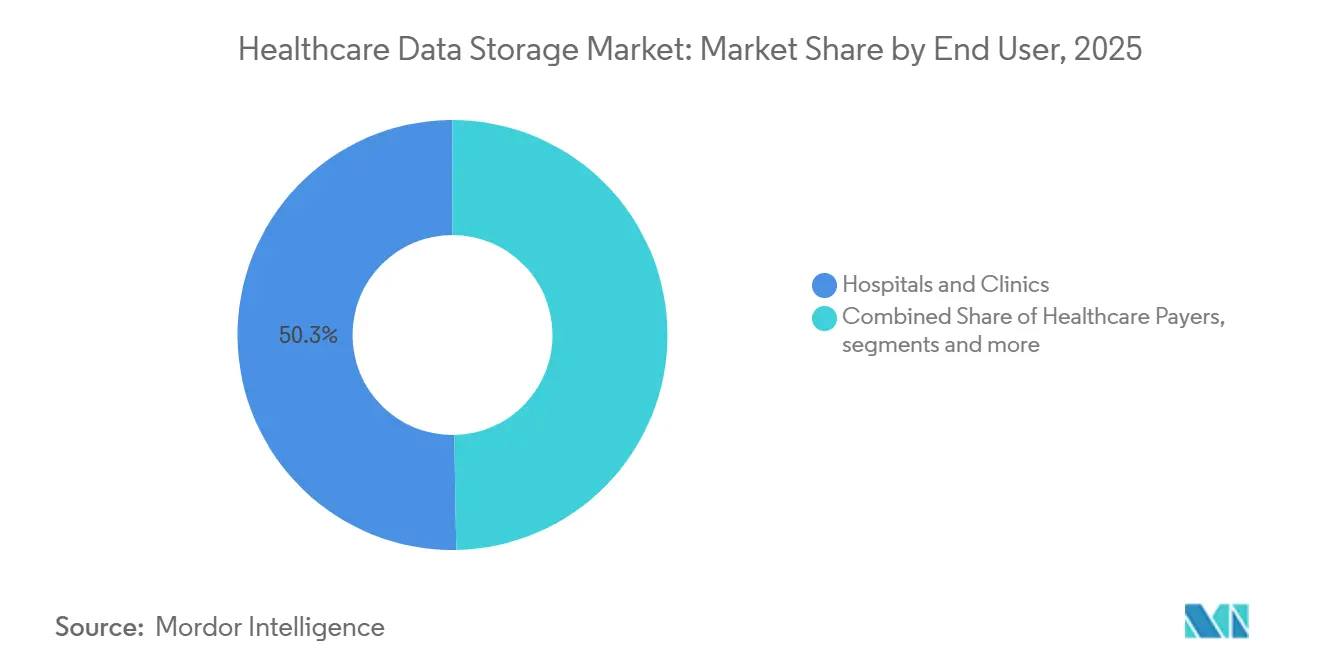

- By end user, hospitals and clinics captured 50.27% share in 2025, while pharmaceutical and biotechnology companies are projected to grow at a 15.78% CAGR through 2031.

- By application, PACS and enterprise imaging represented 44.47% share in 2025, while EHR/EMR and clinical data are forecast to advance at a 16.12% CAGR through 2031.

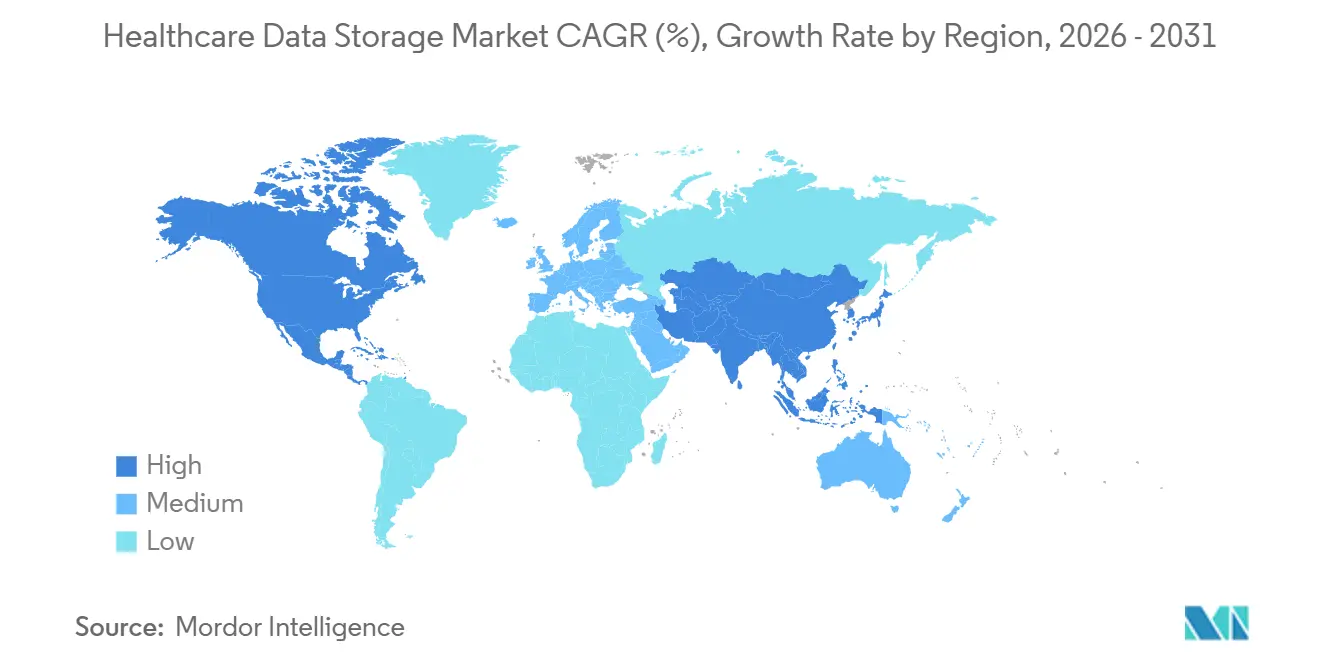

- By region, North America represented 48.56% share in 2025, while Asia-Pacific is forecast to advance at a 16.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare Data Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imaging and enterprise imaging expansion drives petabyte-scale storage | +3.2% | Global, concentrated in North America and EU with spillover to APAC core | Medium term (2-4 years) |

| EHR interoperability and patient access expand data volumes and retention | +2.8% | North America and EU primary, APAC adoption accelerating | Medium term (2-4 years) |

| Accelerating cloud adoption for imaging, analytics, and backup/disaster recovery | +4.1% | Global, highest in North America, rapid growth in APAC | Short term (≤ 2 years) |

| Genomics and multi-omics pipelines create high-throughput, high-volume datasets | +2.5% | North America and EU research hubs, emerging in China and South Korea | Long term (≥ 4 years) |

| Cybersecurity goals mandate immutable backups and centralized logging | +3.0% | Global, regulatory push in U.S., EU, and APAC | Short term (≤ 2 years) |

| Data-sovereignty rules spur sovereign and hybrid deployment | +1.9% | EU primary, national mandates emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Imaging and Enterprise Imaging Expansion Drives Petabyte-Scale Storage

Enterprise imaging has become the leading storage multiplier as radiology, cardiology, pathology, and other image-heavy specialties create sustained demand for low-latency reads and scalable archives. Providers report faster diagnostics and productivity gains as cloud-native PACS platforms deliver sub-second first-image load times and 2–3 times faster display speeds, which encourages larger-scale migrations to cloud deployment for new implementations. A large share of new diagnostic imaging customers now chooses cloud-first rollouts, reinforcing the shift from capital expenditures to predictable operating models in the healthcare data storage market.[1]AWS, “Accelerating PACS on AWS with Visage Imaging,” AWS Case Study, aws.amazon.com Vendors are also investing in purpose-built cloud services that handle DICOM workloads natively, support granular lifecycle tiering, and provide managed immutability to strengthen ransomware resilience for clinical systems. Targeted imaging platforms that layer vendor-neutral archive capabilities on scalable object storage are extending to mid-sized hospitals and multi-site imaging centers, combining compliance-ready architectures with lower operational overhead. Hyperscale cloud providers are aligning to European healthcare hosting standards, which enables hospitals and research organizations to move image management and analytics workloads while meeting residence requirements.

EHR Interoperability and Patient Access Expand Data Volumes and Retention

National interoperability programs have scaled quickly, with America’s TEFCA reporting nearly 500 million health records exchanged as of February 2026, which signals a step-change in the volume and velocity of clinical data movement across networks.[2]U.S. Department of Health and Human Services, “TEFCA, America’s National Interoperability Network, Reaches Nearly 500 Million Health Records Exchanged,” HHS Press Office, hhs.gov The CMS Interoperability and Prior Authorization Final Rule mandates a suite of FHIR-based APIs for patient access, provider access, payer-to-payer exchange, and prior authorization, with key capabilities due by January 1, 2027, and one-business-day response expectations that implicitly raise storage and logging needs for high-throughput transactions.[3]Centers for Medicare & Medicaid Services, “CMS Interoperability and Prior Authorization Final Rule (CMS-0057-F),” CMS, cms.gov These rules increase the number of payloads generated and retained across claims, encounters, prior authorizations, and clinical data elements, which accelerates lifecycle-tiered object storage adoption in the healthcare data storage market. The Federal Register entry clarifies how response timelines, data classes, and standardized formats converge on FHIR Release 4.0.1 and USCDI v3, which drives storage designs that are optimized for API-driven access, provenance, and auditability. As more APIs exchange clinical and administrative artifacts across payers and providers, organizations are expanding immutable logs and long-term archives to satisfy evidence and dispute needs under evolving federal oversight. The net effect is higher baseline storage demand, increased reliance on object storage with deep archive tiers, and closer integration between API platforms and storage policies in the healthcare data storage market.

Accelerating Cloud Adoption for Imaging, Analytics, and Backup/Disaster Recovery

Cloud-native imaging has proven implementation speed and resilience advantages, with deployments that complete within months and deliver measurable workflow gains for radiologists and referrers, motivating accelerated cloud adoption in the healthcare data storage market. Providers benefit from managed services that remove the burden of local RAID rebuilds, periodic hardware refreshes, and complex disaster-recovery drills while offering elastic scalability for peak periods. Imaging workloads pair naturally with object storage and lifecycle-tiered services that support immutability, which strengthens ransomware resilience without adding significant operational overhead. Platform vendors are also shipping integrated data services for healthcare, bundling FHIR, DICOM, and telemetry ingestion with enterprise controls and regional residency options that align to health-data regulations.[4]Microsoft Azure, “Pricing, Azure Health Data Services,” Microsoft Azure, azure.microsoft.com As AI inference and analytics move closer to clinical workflows, native integration with managed ML services improves time to value and encourages cloud-first designs for new data repositories. These operational and strategic advantages reinforce the cloud trajectory across imaging, analytics, and backup, further consolidating share gains for cloud deployment in the healthcare data storage market.

Genomics and Multi-Omics Pipelines Create High-Throughput, High-Volume Datasets

Population-scale and clinical genomics pipelines generate sustained data flows that challenge on-premise capacity planning and necessitate petabyte-scale object storage strategies in the healthcare data storage market. Peer-reviewed methods show that compressed index approaches such as MetaGraph can reduce storage demands for large public repositories by orders of magnitude while preserving the ability to query across many datasets, which helps organizations balance cost and performance. Sequencing platforms and optimized pipelines have improved throughput and unit costs, which makes broader applications in pharmacogenomics and clinical research viable and lifts storage requirements for raw, processed, and derived data products across cohorts. Workflow modernization by genomics service providers shows that re-architecting compute and storage paths can materially reduce per-run costs and speed turnaround, which signals continued momentum toward cloud-backed data strategies. Health-cloud providers now offer domain services for sequence storage, variant processing, and integrated analytics that scale across thousands of samples, and these components are being pulled into clinical and research settings that require security, provenance, and reproducibility. As multi-omics models combine genomics, transcriptomics, proteomics, and other modalities, file counts and intermediate artifacts multiply, which keeps storage growth elevated over the long term in the healthcare data storage market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget constraints and staffing shortages slow EI and cloud migrations | -2.3% | Global, acute in rural U.S., NHS UK, and public hospitals in APAC | Short term (≤ 2 years) |

| Interoperability challenges, VNA migrations, and multi-year archive transitions add risk | -1.8% | North America and EU health systems with legacy PACS | Medium term (2-4 years) |

| Cloud egress fees and vendor lock-in complicate lifecycle TCO | -1.5% | Global, especially multi-cloud in North America and EU | Medium term (2-4 years) |

| Localization and sovereignty restrict cross-border clinical-data storage | -1.2% | EU, China, Russia, India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Budget Constraints and Staffing Shortages Slow EI and Cloud Migrations

Health systems that face flat or declining budgets often delay large-scale PACS or VNA modernization and shift toward optimizing existing platforms, which reduces near-term migration volume for enterprise imaging. Survey findings published by healthcare IT vendors highlight a bifurcation in spending, where some organizations increase data management budgets while others reduce capital commitments and focus on incremental efficiencies, which slows broad-based adoption in the healthcare data storage market. Staffing shortages add friction, since imaging migration and multi-omics platform rollouts require specialized engineering and governance skill sets that are in short supply. Providers respond by elevating priorities like immutable backup, audit readiness, and consolidation of applications as bridging steps rather than full re-architecture in one cycle. Where modernization proceeds, teams often phase projects to limit parallel-run costs and to match scarce cloud and data engineering resources with the most time-sensitive objectives. These trade-offs moderate implementation velocity in the short term while reinforcing a hybrid adoption path in the healthcare data storage market.

Localization and Sovereignty Restrict Cross-Border Clinical-Data Storage

European rules for primary-use electronic health data are moving storage physically into the Union, which limits cross-border consolidation and raises the need for in-region deployments and governance controls for providers and national contact points. The European Health Data Space Regulation requires EHR systems to include defined interoperability and logging components and establishes structured pathways for both primary and secondary uses, which raises compliance-driven storage and audit requirements across hospitals and health agencies. Cloud providers and vendors respond by expanding EU coverage and certifying healthcare offerings under national schemes such as HDS, which enables migration but imposes residency and transparency obligations on data flows and remote access paths. Trusted Research Environments are emerging to address cross-border research under sovereignty rules, allowing analysis to move to data with only aggregated outputs leaving secure environments, which reduces the need to centralize patient-level data while preserving analytical reach. The added complexity raises cost and schedule risk for multinational programs and increases the number of region-specific archives, keys, and runbooks that operators must maintain. This structural friction reduces the speed of consolidation and pushes organizations toward hybrid architectures that split workloads across national or regional facilities in the healthcare data storage market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Dual-Cloud Economics Reshape Capital Planning

Cloud deployment captured 50.46% of the healthcare data storage market share in 2025, and it is forecast to grow at a 16.21% CAGR through 2031 as clinical imaging and data analytics consolidate on elastic platforms that compress implementation timelines. On-premise installations continue in bandwidth-constrained sites and where depreciation schedules or residency requirements support local control. Hybrid designs that use local caches for hot studies and cloud object storage for tiered archiving align to residency mandates while sustaining cross-facility access. Imaging-focused services now combine object storage and workflow orchestration to simplify operations for mid-sized hospitals and large imaging centers, which supports continued share gains for cloud in the healthcare data storage market. Implementation case studies demonstrate near-immediate access to images and higher radiologist throughput, which lowers the risk of migration and supports the conversion of capital budgets into operating expense commitments.

Five-year cost models that remove periodic refresh cycles and reduce on-site maintenance demand strengthen the budget case for cloud, even as organizations work to manage egress and network costs over the lifecycle. Many providers adopt a phased approach to cloud adoption, starting with disaster recovery or long-term archive tiers before moving diagnostic viewing and high-performance caches, which aligns with both risk posture and budget. API-first interoperability across EHR, imaging, and payer systems drives incremental object writes and immutable logs, which further tilts new capacity toward cloud services in the healthcare data storage market. For cross-border operators, in-region cloud facilities and HDS-certified platforms offer a path to compliance while retaining elasticity, which supports cross-site collaboration under residency constraints. As organizations improve observability and governance on cloud platforms, they use policies to optimize lifecycle tiering and retention schemes, which stabilizes cost while preserving performance envelopes.

By Architecture: Block Storage Dominates, File Storage Accelerates

Block storage held 47.43% share in 2025 on the strength of performance-sensitive transactional systems, imaging caches, and mission-critical databases, which require low-latency response profiles. File storage is the fastest-growing architectural tier at a 15.26% CAGR through 2031 as enterprise imaging expands to unify DICOM and non-DICOM content in vendor-neutral archives that use NAS collaboration and hierarchical namespaces. Object storage underpins many cloud-native platforms, offering effectively unlimited scale, granular immutability, and deep archive tiers that suit compliance and long retention windows in the healthcare data storage market. Vendors that pair file semantics for clinical users with object tiers for long-term storage create blended economics that improve total cost and durability, which aids migrations from legacy silos. Enterprise-grade storage portfolios that integrate FHIR and DICOM data services are establishing a playbook for hybrid architectures across hospital networks.

In practice, hospitals use block for hot-path clinical reads and writes, file for multidisciplinary collaboration and image management metadata, and object for persistent archiving and immutable backups. Imaging platforms that support direct-to-object writes reduce operational steps and improve retrieval performance at scale, which shortens time to first image for clinicians and improves system resilience in the healthcare data storage market. File growth is also linked to new modalities such as digital pathology and ophthalmology that contribute large files and benefit from SMB and NFS-based collaboration. As imaging merges with analytics, tiering policies are tuned for AI training, validation, and inference workloads that need to traverse hot, warm, and cold tiers for cost and speed. Over the forecast period, architectural convergence will continue, with policy engines mediating between clinical performance targets and retention obligations.

By Storage Medium: SSD/Flash Leads, HDD Growth Surprises

SSD/Flash commanded 46.39% share in 2025 as hot-path workloads such as PACS reading rooms, EHR logs, and AI inference pipelines require high throughput and low latency. Energy efficiency gains and the ability to consolidate racks drive further SSD deployments, while imaging acceleration benchmarks highlight AI throughput advantages on optimized flash platforms within clinical environments. HDD is the fastest-growing tier at a 15.47% CAGR through 2031 as cloud object storage and deep archive tiers standardize long-term retention for compliance and immutable backups in the healthcare data storage market. Tape remains relevant for air-gapped strategies and for organizations that need offline protection and the lowest cost per terabyte in regulated settings.

Most providers converge on a three-tier mix that places hot data on SSD, warm and cold object tiers on HDD-backed services, and compliance archives on either deep-cloud archive or tape. Imaging and multi-omics workloads benefit from this stratification as large files and derived datasets can be promoted and demoted based on access patterns and project phases. Platform providers are augmenting these tiers with immutable snapshot features and integrated data discovery to speed ransomware recovery and to support precise legal holds. As storage medium choices become policy-driven, the healthcare data storage market will continue to expand HDD consumption even as SSD maintains leadership in mission-critical paths.

By End User: Hospitals Anchor Demand, Pharma and Biotech Accelerate

Hospitals and clinics accounted for 50.27% share in 2025 as enterprise imaging consolidations, interoperability mandates, and audit-ready archives remain core investment themes. Cross-facility access, role-based security, and lineage-aware governance boost the importance of centralized repositories that can efficiently serve diverse departments in the healthcare data storage market. Pharmaceutical and biotechnology companies are the fastest-growing segment at a 15.78% CAGR through 2031 as clinical trials, pharmacogenomics, and real-world evidence programs expand data generation and retention. Genomics platforms and multi-omics workflows translate into persistent storage footprints across study lifecycles, which drives demand for object storage and policy-driven hierarchies.

Payers and integrated delivery networks are also building out FHIR repositories and prior-authorization interfaces that depend on robust storage, provenance, and audit capabilities. Academic medical centers and research institutes increase emphasis on secure analysis environments that keep data in place while allowing code to move, which suits cross-institutional collaborations under residency mandates. Across end users, immutable backup adoption increases, and disaster recovery is planned with tested recovery objectives, which reinforces investment in immutability and lifecycle-focused services in the healthcare data storage market. Vendor portfolios that combine clinical interoperability, research support, and sovereign cloud options gain strategic relevance.

By Application: PACS and Enterprise Imaging Largest, EHR/EMR and Clinical Data Fastest

PACS and enterprise imaging represented 44.47% share in 2025, which reflects the dominant role of imaging in clinical workflows and the persistent growth of imaging volumes. Advanced viewing and rapid prior retrieval make high-performance caches and scalable archives central to clinician productivity, and cloud PACS implementations demonstrate strong time-to-value improvements in the healthcare data storage market. EHR/EMR and clinical data are the fastest-growing applications at a 16.12% CAGR through 2031 as national interoperability initiatives broaden API-driven exchange and as payers implement FHIR-based interfaces under the CMS rule. These workflows generate and retain claims, encounters, authorizations, and clinical payloads that increase storage footprints across primary and secondary systems.

Genomics and multi-omics applications add sustained volume as whole-genome sequencing and integrated analyses become more routine, which magnifies storage needs for raw reads, intermediate files, and compressed indexes over long project timelines. Clinical analytics and AI pipelines depend on fast access to historical imaging and EHR data, which further promotes all-flash tiers for active datasets and automated tiering for cold data in the healthcare data storage market. Over the forecast period, wider adoption of TRE-style secure analysis environments will shape secondary-use storage designs, especially where strict residency rules apply.

Geography Analysis

North America captured 48.56% share in 2025, supported by a mature compliance regime, fast-growing interoperability networks, and a dense ecosystem of health-tech innovators. The TEFCA network’s progression to nearly 500 million records exchanged by February 2026 demonstrates live-scale national exchange, which expands storage and audit demands across providers and payers in the healthcare data storage market. Federal rulemaking on interoperability and prior authorization has set specific API and response benchmarks, which move storage closer to API platforms for durability and performance. Canada benefits from hyperscalers’ regional presence and from alignment with U.S.-style privacy frameworks, which supports cross-border vendor strategies that deliver unified architectures. In Mexico and select Latin subregions of North America, modernization efforts raise incremental deployments of EHR and imaging archives within public hospitals and private networks. Across the region, immutable backup adoption, SIEM integration, and hybrid disaster recovery are now standard program pillars that shape storage design.

Asia-Pacific is the fastest-growing region with a 16.36% forecast CAGR through 2031 as national digital-health missions expand data capture, imaging, and analytics. Cloud providers maintain multiple in-region facilities that give health systems the residency and performance needed to scale enterprise imaging and FHIR-based services in the healthcare data storage market. Health systems in Japan, South Korea, Singapore, and Australia are rolling out AI-augmented diagnostics and expanding remote care, which adds downstream storage requirements for images, telemetry, and longitudinal clinical records. China and India continue to emphasize sovereign data policies that increase reliance on in-country cloud regions and hybrid models. Staffing constraints in specialized data engineering and bioinformatics remain a pinch point for advanced genomics-scale storage across several APAC markets, which encourages managed services and platform approaches.

Europe holds a substantial share and faces distinct regulatory contours that guide deployment choices. The European Health Data Space Regulation sets obligations for EHR system interoperability, logging, and CE-marked conformity for primary uses, and it creates a framework for secondary uses under secure processing environments, which elevates storage, audit, and governance requirements in the healthcare data storage market. Cloud providers are certifying for healthcare hosting programs and expanding EU-region coverage to support hospitals, research centers, and life-sciences organizations under national residency rules. Smaller markets benefit from pan-EU cloud footprints, though budget constraints in public systems and GDPR-driven audits can slow enterprise imaging consolidations. The United Kingdom and Germany are advancing national digital-health infrastructure that will increase API-driven data exchange and reinforce audit-ready storage practices.

Competitive Landscape

The healthcare data storage market features hyperscale cloud providers alongside enterprise storage specialists, each pursuing strategies that couple performance, compliance, and AI-readiness. AWS, Microsoft Azure, and Google Cloud package FHIR and DICOM services with managed analytics and ML tooling, which helps health systems simplify pipelines while meeting logging and residency needs. Vendors differentiate with integrated workflows for imaging, EHR interoperability, and immutable backup that target clinical performance and governance controls in the healthcare data storage market. Healthcare customers continue to value certifications such as ISO 27001, HITRUST, and SOC 2, which are table stakes for production workloads in regulated settings.

Specialized storage and data-management suppliers are evolving to emphasize AI-era orchestration, immutability, and ransomware recovery at scale. Everpure, the rebranded Pure Storage, announced intent to acquire 1touch to add data discovery and semantic context that improves data intelligence and security posture across fleets. The vendor also introduced new offerings aligned to AI pipelines and simplified data streaming that can lower complexity for enterprise AI across healthcare and life sciences. Imaging-focused case studies show that cloud-native implementations deliver faster viewing, higher throughput, and reduced operational overhead, which underpins continued share gains by cloud in the healthcare data storage market.

Research platforms and TRE providers are growing as sovereignty and secondary-use frameworks mature. Lifebit’s Trusted Research Environment is an example of a model that keeps data in situ and moves compute to the data under rigorous controls, which aligns with EU secondary-use paradigms and reduces cross-border data movement. Hyperscalers are integrating more domain-specific features that ease multi-omics analysis and unify data products for downstream clinical use. Vendors that combine clinical interoperability, imaging performance, sovereign options, and AI-readiness are positioned to gain share as the healthcare data storage market shifts to hybrid-cloud and policy-forward architectures.

Healthcare Data Storage Industry Leaders

Dell Technologies

IBM

Hewlett Packard Enterprise (HPE)

Amazon Web Services (AWS)

NetApp

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Everpure (formerly Pure Storage) launched Evergreen//One for FlashBlade//EXA and announced the upcoming beta of Everpure Data Stream (launching later in 2026) to reduce costs and complexity in enterprise AI projects. FlashBlade//EXA achieved the highest SPEC Storage AI_Image benchmark score, powering 6,300 simultaneous AI jobs and moving data twice as fast as competitors using less than half a rack.

- February 2026: Pure Storage completed its rebranding to Everpure and announced intent to acquire 1touch, an innovator in data intelligence and orchestration, to enhance data management capabilities by adding data discovery and semantic context, making enterprise data secure, accessible, intelligent, and AI-ready at the source. The acquisition is expected to close in Q2 FY27, positioning Everpure as a leader in AI-era data platforms for healthcare and life sciences.

- February 2026: The U.S. Department of Health & Human Services announced that TEFCA, America's National Interoperability Network, reached nearly 500 million health records exchanged as of February 11, 2026, a substantial increase from approximately 10 million in January 2025. HHS also published the HTI-5 Proposed Rule suggesting removal of 34 certification criteria, potentially saving certified health IT developers an estimated USD 1.53 billion in compliance costs.

Global Healthcare Data Storage Market Report Scope

According to the report’s scope, healthcare data storage refers to secure digital systems that collect, organize, and maintain patient records, medical images, laboratory results, and other clinical or administrative data. These platforms ensure reliable access, regulatory‑compliant retention, and protected sharing of information across healthcare providers, supporting continuity of care and efficient operational workflows.

The healthcare data storage market is segmented into deployment mode, architecture, storage medium, end user, application, and geography. By deployment mode, the market is segmented into on-premise, cloud, and hybrid. By architecture, the market is segmented into block storage, file storage, and object storage. By storage medium, the market is segmented into HDD, SSD/flash, and tape. By end user, the market is segmented into hospitals & clinics, pharmaceutical & biotechnology companies, healthcare payers, and others. By application, the market is segmented into PACS/enterprise imaging, EHR/EMR and clinical data, genomics & multi-omics, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| On-Premise |

| Cloud |

| Hybrid |

| Block Storage |

| File Storage |

| Object Storage |

| HDD |

| SSD/Flash |

| Tape |

| Hospitals & Clinics |

| Pharmaceutical & Biotechnology Companies |

| Healthcare Payers |

| Others |

| PACS/Enterprise Imaging |

| EHR/EMR and Clinical Data |

| Genomics & Multi-omics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Deployment Mode | On-Premise | |

| Cloud | ||

| Hybrid | ||

| By Architecture | Block Storage | |

| File Storage | ||

| Object Storage | ||

| By Storage Medium | HDD | |

| SSD/Flash | ||

| Tape | ||

| By End User | Hospitals & Clinics | |

| Pharmaceutical & Biotechnology Companies | ||

| Healthcare Payers | ||

| Others | ||

| By Application | PACS/Enterprise Imaging | |

| EHR/EMR and Clinical Data | ||

| Genomics & Multi-omics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the healthcare data storage market size outlook to 2031?

The healthcare data storage market size is expected to increase from USD 6.60 billion in 2025 to USD 7.49 billion in 2026 and reach USD 14.70 billion by 2031 at a 14.45% CAGR.

Which deployment model is leading and how fast is it growing?

Cloud leads with 50.46% share in 2025, and it is forecast to grow at 16.21% CAGR through 2031 as imaging, analytics, and disaster recovery consolidate on elastic platforms.

Which application area contributes the largest share today?

PACS and enterprise imaging represents 44.47% share in 2025, reflecting the central role of imaging in clinical workflows and archiving.

Which region is growing the fastest and why?

Asia-Pacific is the fastest-growing region at a 16.36% forecast CAGR through 2031, supported by national digital-health programs, strong cloud-region coverage, and expanding enterprise imaging and analytics.

Page last updated on: