Healthcare Data Collection And Labeling Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.57 Billion |

| Market Size (2031) | USD 5.62 Billion |

| Growth Rate (2026 - 2031) | 16.94% CAGR |

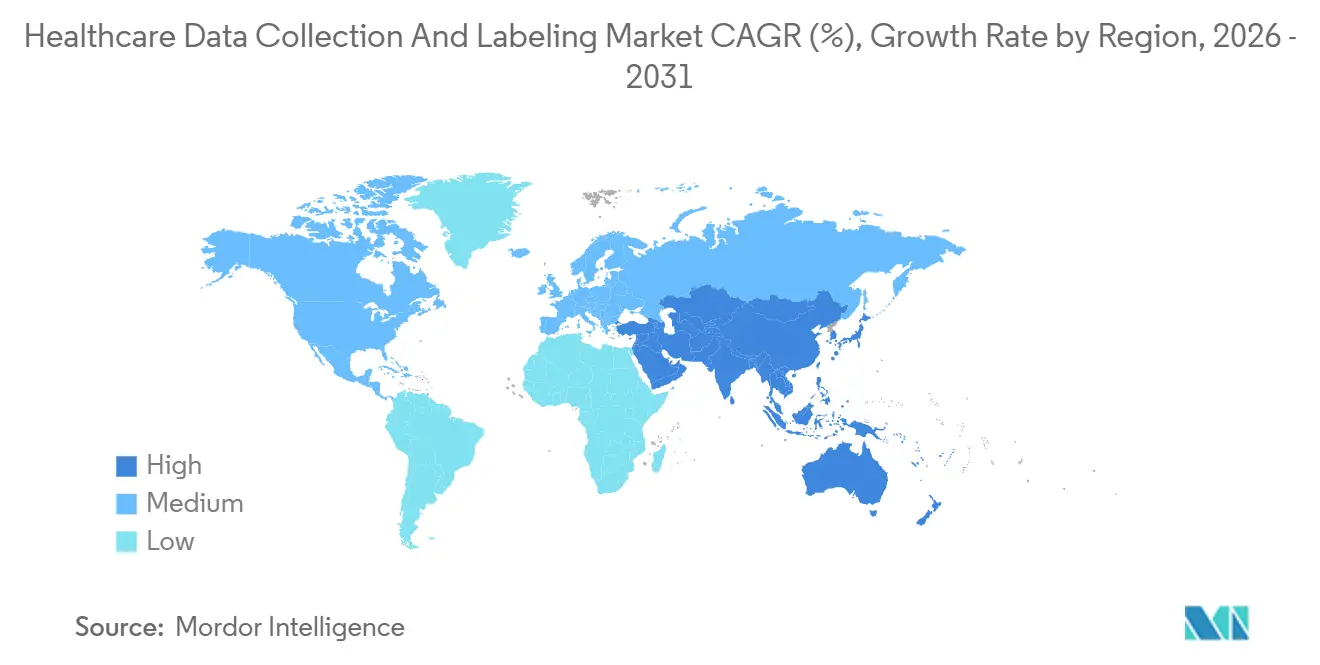

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Data Collection And Labeling Market Analysis by Mordor Intelligence

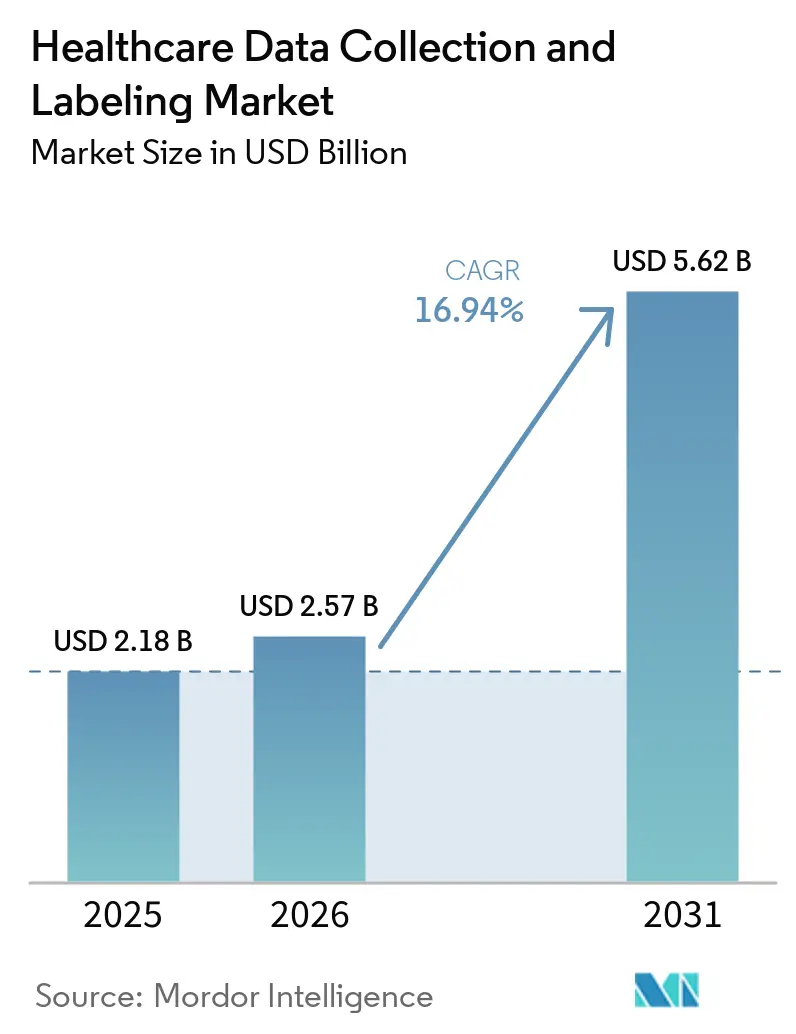

The Healthcare Data Collection And Labeling Market size is expected to grow from USD 2.18 billion in 2025 to USD 2.57 billion in 2026 and is forecast to reach USD 5.62 billion by 2031 at 16.94% CAGR over 2026-2031.

Imaging workflows dominate current spending because each FDA-cleared algorithm must be trained on rigorously curated datasets traceable to board-certified specialists, and this demand is spilling over into pathology and surgical robotics. Rapid regulatory approvals are shifting budgets from retrospective projects to continuously updated, audit-ready pipelines, while emerging capability in synthetic data generation is lowering the cost of cold-start annotation and expanding addressable use cases. Offshore, HIPAA-compliant annotation hubs in India and the Philippines deliver expert labels at one-third of U.S. rates, putting downward pressure on margins but broadening access for mid-size health-tech firms. At the same time, the carbon footprint of scaling to multi-million-image foundation models is prompting health systems to evaluate vendors’ sustainability disclosures before signing multi-year contracts. These intersecting trends position the healthcare data collection and labeling market as a critical enabler of next-generation clinical AI across imaging, multi-omics drug discovery, and real-world-evidence submissions.

Key Report Takeaways

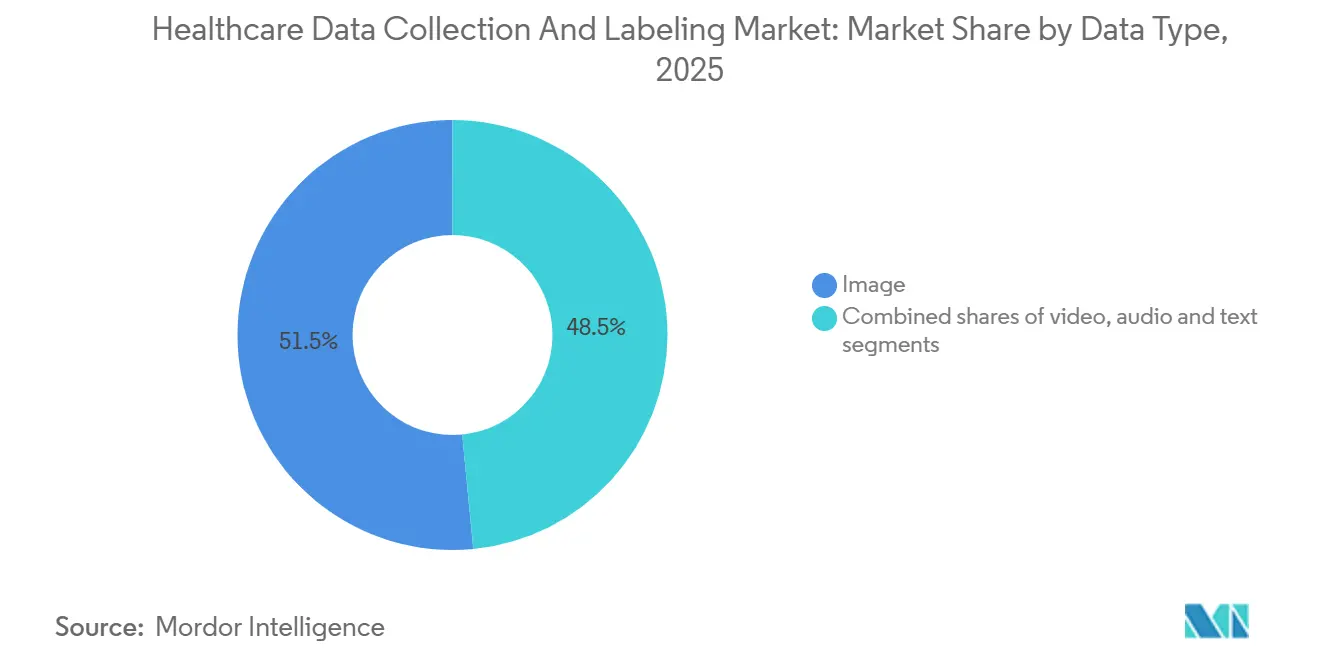

- By data type, image annotation held 51.54% of the healthcare data collection and labeling market share in 2025, while video annotation is forecast to expand at a 17.40% CAGR through 2031, reflecting a shift toward frame-level labeling for surgical robotics.

- By labeling approach, manual human-supervised workflows controlled 53.10% of the healthcare data collection and labeling market size in 2025; fully-automated tools are projected to grow at 17.90% CAGR as foundation models secure FDA acceptance.

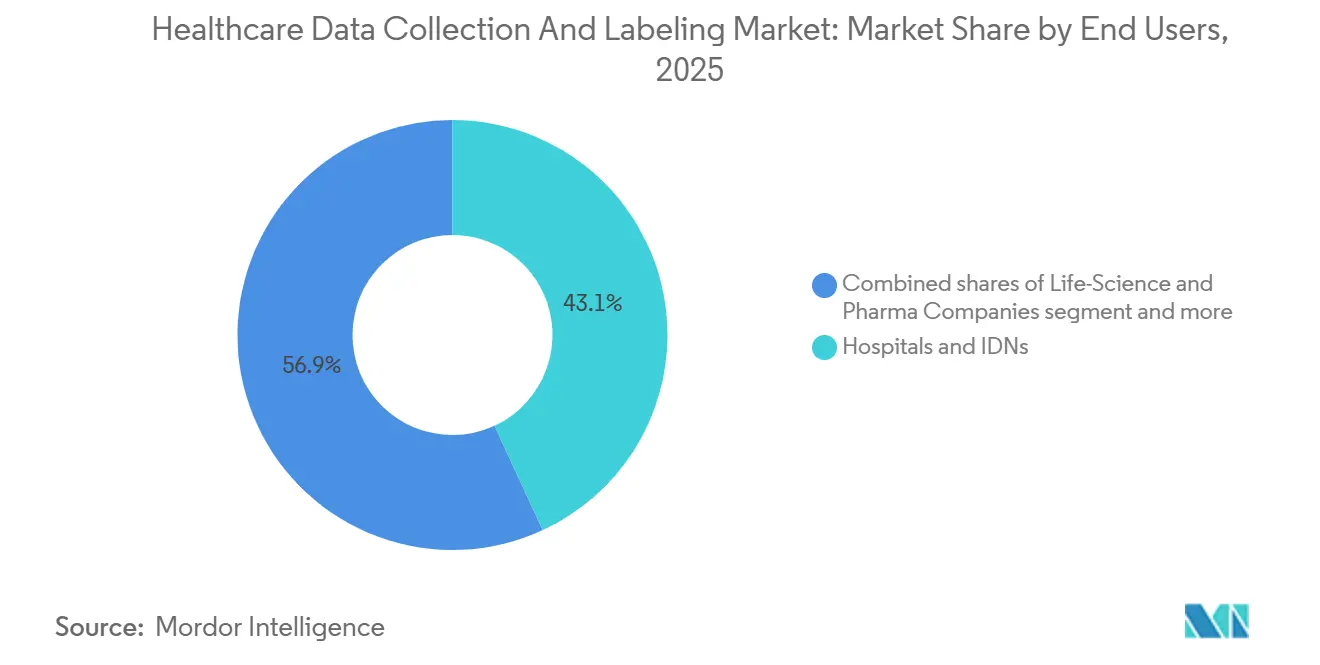

- By end user, hospitals and integrated delivery networks led with 43.10% revenue share in 2025, but life-science and pharmaceutical companies are set to advance at 17.60% CAGR on the back of multi-omics biomarker pipelines.

- By application area, diagnostic imaging AI accounted for 47.10% of spending in 2025, whereas drug discovery and biomarker identification will rise at 17.70% CAGR to 2031 as annotated real-world datasets become admissible primary evidence.

- By geography, North America secured a dominant 43.20% share in 2025, while Asia-Pacific is expected to achieve a 17.30% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare Data Collection And Labeling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of AI-Driven Medical Imaging Solutions | +3.2% | Global, led by North America and Europe | Medium term (2–4 years) |

| Expansion of Multi-Modal Clinical Data (EHR, Sensors, Genomics) | +2.8% | North America, Europe, APAC | Long term (≥4 years) |

| Regulatory Shift Toward Real-World Evidence in Approvals | +2.5% | North America (FDA), Europe (EMA), Japan (PMDA) | Short term (≤2 years) |

| Outsourced, HIPAA-Compliant Expert Labeling Networks Expand | +2.1% | Global, hubs in India and Philippines | Medium term (2–4 years) |

| Active-Learning Workflows That Cut Annotation Hours Per Case | +1.9% | Global, early adoption in North America and Europe | Short term (≤2 years) |

| Generative Synthetic Data Pipelines Reduce Cold-Start Needs | +1.7% | North America, Europe, APAC | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of AI-Driven Medical Imaging Solutions

The FDA cleared 882 AI-enabled medical devices by December 2025, up from 521 in 2023, and each approval requires datasets annotated under 21 CFR Part 11 audit trails [1]U.S. Food and Drug Administration, “Artificial Intelligence and Machine Learning (AI/ML)-Enabled Medical Devices,” fda.gov. Venture backing mirrors this regulatory velocity; Aidoc secured USD 30 million in late 2024 to train a foundation model on 2.5 million CT scans labeled for 14 pathologies. Whole-slide pathology imaging is following suit, with polygon-level tumor margin annotation times dropping from 45 minutes to 8 minutes per slide when active learning pre-selects ambiguous regions. Continuous-learning pipelines that retrain monthly are replacing one-off projects, giving annotation vendors recurring subscription revenue. Together, these forces amplify demand across radiology, pathology, and emerging 3-dimensional imaging modalities, reinforcing long-term growth in the healthcare data collection and labeling market

Expansion of Multi-Modal Clinical Data (EHR, Sensors, Genomics)

Drug developers now link EHR text, wearable-sensor streams, and genomic variants in unified datasets. Recursion Pharmaceuticals’ 2024 partnership with Tempus combined 23 petabytes of histopathology images with longitudinal records for 3 million patients, requiring annotation expertise across ICD-10, SNOMED CT, and genomic nomenclature. Wearable devices magnify scale; a single atrial-fibrillation patient produces 2.5 million ECG datapoints daily, pushing cardiologist review costs to USD 180 per hour. The FDA’s 2024 SaMD draft guidance mandates demographically balanced training sets, driving over-sampling of under-represented groups and annotation of social determinants that are often missing from legacy EHRs. Microsoft’s 2025 FHIR-native annotation API lets hospitals label clinical notes inside Epic workflows, cutting export latency by 80%. Multi-modal integration broadens addressable revenue pools and cements the role of the healthcare data collection and labeling market in precision medicine

Regulatory Shift Toward Real-World Evidence in Approvals

The FDA’s December 2024 final guidance permits annotated real-world datasets as primary evidence in device submissions. Europe’s Health Data Space regulation requires every cross-border record to carry standardized consent tiers, spawning demand for legal-expert annotators versed in GDPR Article 9. Japan’s PMDA insists that at least 20% of training data for imported AI devices originates domestically, catalyzing joint projects between U.S. vendors and Japanese hospitals. Datavant used its HIPAA-compliant network in 2024 to de-identify and annotate 50 million patient records, shrinking an evidence-generation timeline from 36 months to 14 months. These changes reposition annotation from a back-office task to a frontline regulatory requirement.

Outsourced, HIPAA-Compliant Expert Labeling Networks Expand

India’s Digital Personal Data Protection Act introduced GDPR-level penalties in 2023, elevating the country’s compliance credentials. iMerit opened a 1,200-seat medical-annotation center in Kolkata in 2024, paying USD 12–18 per hour and achieving HITRUST certification within six months. CloudFactory partnered with the Philippine College of Radiology in 2025 to train 500 technologists annually in DICOM standards, easing global expert shortages. Poland’s Medbravo employs ISO 15189-accredited pathologists at USD 80 per slide, half U.S. rates, while satisfying CE-mark requirements. These networks lower project costs and broaden capacity, reinforcing outsourcing as an enduring growth driver for the healthcare data collection and labeling market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Privacy Laws (HIPAA, GDPR, CCPA) Elevate Costs | –2.4% | Global, highest impact in North America and Europe | Short term (≤2 years) |

| Scarcity & High Hourly Rate of Domain Experts (Radiologists, Pathologists) | –1.8% | North America and Europe; spillover to APAC | Medium term (2–4 years) |

| High Carbon Footprint of Large-Scale Annotation Operations | –1.5% | Global, especially regions with carbon-intensive grids | Long term (≥4 years) |

| Liability Concerns Over Fully Automated Labels Slow Adoption | –1.3% | Global, pronounced in North America and Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Stringent Privacy Laws Elevate Costs

HIPAA enforcement collected USD 28 million in penalties during 2024, with 40% of violations traced to annotation vendors lacking Business Associate Agreements [2]U.S. Department of Health and Human Services, “HIPAA Compliance & Enforcement,” hhs.gov. GDPR Article 9 restrictions force platforms to deploy granular access controls; an Irish DPC audit suspended 18% of projects lacking lawful transfer bases. Only 47% of U.S. vendors had self-certified under the EU-U.S. Data Privacy Framework by mid-2025, prompting European hospitals to demand on-premises annotation at 30% price premiums. California’s CPRA gives patients deletion rights; one genomics company re-annotated 12,000 samples when 8% opted out, incurring USD 1.2 million in extra costs. Together, these mandates add 15–25% overhead to every project in the healthcare data collection and labeling market.

Scarcity and High Hourly Rate of Domain Experts

The U.S. is projected to lack 35,000 radiologists by 2033, pushing annotation rates to USD 150–250 per hour and even higher for subspecialists. The College of American Pathologists reported that retirements outpace new entrants 2:1, shrinking the pathologist pool. Offshore arbitrage offers partial relief. Indian radiologists charge USD 40–60 per hour, but only 22% of U.S. hospitals permit foreign annotations for FDA submissions, citing licensure concerns[3]American College of Radiology, “Survey on Offshore Annotation Practices,” acr.org Segment Analysis. Centaur Labs’ distributed network of 50,000 medical trainees delivers ensemble labels at USD 0.50–2.00 per case, yet widespread adoption awaits further real-world validation. Until supply meets demand, expert scarcity will temper the growth trajectory of the healthcare data collection and labeling market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Type: Video Annotation Captures Surgical-AI Investment Wave

Video annotation is projected to grow at a 17.40% CAGR from 2026 to 2031, the highest among data types in the healthcare data collection and labeling market. Intuitive Surgical disclosed that it had annotated 2.3 million robotic-surgery videos at USD 45 million, highlighting the capital intensity. Theator’s USD 100 million financing in 2024 targets 4K laparoscopic datasets comprising 127 procedural steps. Image data retained 51.54% healthcare data collection and labeling market share in 2025, thanks to established DICOM pipelines across radiology and pathology, yet the exponential frame count in surgery and endoscopy is shifting revenue toward video. Active-learning tools that pre-track instruments now cut labeling time by 70%, reducing per-project budgets but enabling more simultaneous engagements.

Text and audio remain smaller but strategically significant slices of the healthcare data collection and labeling market size. Large language models auto-code ICD-10 and CPT terms, slashing manual hours, yet FDA guidance still mandates human verification for billing-grade output. Audio annotation is emerging around voice biomarkers; Sonde Health’s Mayo Clinic partnership labeled 50,000 samples to detect respiratory distress with 89% sensitivity. Lack of unified ontologies across speech-based disorders keeps the vendor landscape fragmented, but standardization efforts by IEEE promise to unlock scale.

By Labeling Approach: Fully-Automated Tools Gain FDA Acceptance

Fully-automated workflows are forecast to expand at a 17.90% CAGR, the fastest among labeling approaches in the healthcare data collection and labeling market. Google’s Med-Gemini models tag chest X-rays for 14 pathologies at USD 0.02 per image, matching three-radiologist consensus. Nonetheless, human-supervised annotation maintained 53.10% of the healthcare data collection and labeling market share in 2025, as liability concerns keep experts in the loop for ambiguous cases. Semi-automated platforms dominate oncology and cardiology, where efficiency gains coexist with required clinician oversight.

The FDA’s 2024 guidance on predetermined change-control plans eases post-market dataset updates, encouraging vendors to invest in automation that continuously refreshes labels without new submissions. MD.ai’s smart-annotation tool reduced cardiologist labeling time by 73% for cardiac MRI, preserving accountability while accelerating throughput. Manual annotation remains necessary for rare diseases and for novel modalities such as photoacoustic imaging, where foundation models lack prior exposure. Over the forecast horizon, hybrid human-plus-AI workstreams will remain the dominant paradigm in the healthcare data collection and labeling market.

By End User: Life Sciences Pivot to Multi-Omics Biomarker Datasets

Life-science and pharmaceutical companies are projected to lead growth at a 17.60% CAGR to 2031 as real-world evidence becomes admissible in regulatory filings. Recursion’s 23 petabyte multi-omics dataset identified fibrosis drug targets in 18 months, underscoring the strategic value of comprehensive annotation. Hospitals commanded 43.10% of end-user revenue in 2025 as both data generators and AI deployers. CMS added AI-derived quality metrics to pay-for-performance programs in 2024, prompting hospitals to annotate prospective outcome data for sepsis and stroke prediction.

Medical-device firms face steep upfront annotation costs. Medtronic spent USD 38 million on cardiac-rhythm labeling but amortizes these costs over long product lifecycles. Health-tech startups prefer outsourcing; the majority of Series A companies contract external vendors because recruiting credentialed annotators takes 18 months. Contract research organizations and academic institutes perform RECIST annotations for oncology trials, adding USD 1.2 million per 500-patient cohort. This breadth of demand reinforces end-user diversity within the healthcare data collection and labeling market.

By Application Area: Drug Discovery Datasets Command Premium Pricing

Drug discovery and biomarker identification are forecast to grow at 17.70% CAGR through 2031, outpacing all other application areas in the healthcare data collection and labeling market. Insilico Medicine demonstrated that a 1.2 million-assay annotated dataset yielded a Phase II-ready fibrosis drug in 18 months, validating high ROI when annotation accelerates R&D. Diagnostic imaging AI held 47.10% spending share in 2025, bolstered by growing point-of-care ultrasound uptake. Still, commoditization is squeezing per-image fees below USD 2.

Clinical decision support systems rely on real-time EHR streaming; Epic’s sepsis predictor, trained on 500,000 annotated ICU stays, cut false alerts significantly. Population-health tools like Biofourmis’ heart-failure monitor annotate 2.5 million patient-days of biosensor data, underpinning FDA clearance. Rare-disease biomarker datasets fetch premium prices over USD 5 million per project because they require global expert consortia and irreplaceable patient samples. These dynamics diversify revenue streams across the healthcare data collection and labeling market.

Geography Analysis

North America retained 43.20% share in 2025 as 882 FDA-cleared AI devices demanded domestic, audit-ready datasets. Continuous-learning allowances in 2024 guidance make recurrent annotation a fixture, and Cleveland Clinic’s sepsis model, trained on 1.2 million encounters, generated USD 18 million in added reimbursement during its first deployment year. Canada’s Ontario Health digitized 5 million historical X-rays, awarding an USD 88 million contract that expands regional capacity. Mexico is emerging as a HIPAA-compliant near-shore hub, where technologists earn USD 8–12 per hour, shortening U.S. project turnarounds by 20%.

Asia-Pacific will post the fastest 17.30% CAGR, underpinned by China’s USD 15 billion Healthy China 2030 budget and India’s standardized EHR drive. Alibaba Cloud’s 2024 platform cut annotation timelines from 12 months to three, catalyzing 14 domestic AI startups. India’s partnership between Apollo Hospitals and Google Cloud labeled 8 million records, lowering diabetic-retinopathy screening costs by 60%. Japan’s requirement for 20% domestic data is driving U.S. vendor alliances with academic hospitals, as seen in Scale AI’s 500,000-report project with the University of Tokyo.

Europe contributed significant revenue in 2025. The European Health Data Space enforces consent-tier annotations and cross-border EHR interoperability, consolidating demand among platforms with robust governance. Germany approved 43 AI SaMD products in 2024 and began reimbursing AI-derived codes, reinforcing sustainable demand. The UAE’s USD 22 million Arabic-note annotation tender in 2024 and Brazil’s nine AI device approvals signal early momentum in the Middle East, Africa, and South America, though limited digitization and macroeconomic volatility temper near-term scale.

Competitive Landscape

The healthcare data collection and labeling market is moderately fragmented: the top five vendors, Scale AI, Amazon Web Services, Google Cloud, Microsoft Azure, and Labelbox, controlled significant share of 2025 revenue. Scale AI’s USD 1 billion Series F financing, FDA-regulated annotation partnerships with Mayo Clinic covering 1.5 million echocardiograms. AWS embeds labeling into HealthScribe, auto-generating clinical notes that cut manual transcription by 60% and feed downstream models. Google’s Vertex AI Data Labeling service ships pre-built medical ontologies that reduce onboarding to hours.

Niche specialists differentiate on workforce models or modality focus. Centaur Labs aggregates 50,000 medical trainees to deliver ensemble labels at USD 0.50–2.00 per case with 96% concordance to experts. Segmed blends synthetic and real data to generate privacy-preserving datasets for Bayer’s oncology AI. Sonde Health targets voice biomarkers, partnering with Mayo Clinic on respiratory distress detection.

White space opportunities center on federated annotation, carbon-neutral infrastructure, and seamless multi-modal integration. NVIDIA’s FLARE framework supports federated model training but lacks native labeling, creating room for plug-ins that maintain provenance across decentralized nodes. A 2024 HIMSS survey found that 34% of health systems require Scope 3 emission disclosures, yet only 12% of vendors comply, suggesting sustainability as a future differentiator. No platform yet unifies imaging, genomics, sensor, and EHR labeling end-to-end, keeping integration costs high and leaving space for consolidators in the healthcare data collection and labeling market.

Healthcare Data Collection And Labeling Industry Leaders

Scale AI

Google

Microsoft

Amazon

Labelbox

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: NVIDIA is expanding its family of open-source AI models with three new offerings designed to help developers build systems that can think, learn, and act in both digital and physical environments. The lineup now features NVIDIA Nemotron for agentic applications, NVIDIA Cosmos for robotics and other real-world tasks, and NVIDIA BioNeMo for accelerating biomedical research.

- February 2026: Fujitsu Japan and JMDC launched a large-scale healthcare data platform to support sustainable national health services.

- January 2025: Amazon Web Services and General Catalyst began a multi-year collaboration to accelerate enterprise-grade healthcare AI solutions.

Global Healthcare Data Collection And Labeling Market Report Scope

As per the scope of the report, healthcare data collection and labeling serve as the critical foundation for modern medical research and the development of reliable artificial intelligence (AI) systems. Data collection is the systematic process of gathering information from diverse sources, including electronic health records (EHRs), medical imaging like MRI and CT scans, wearable device sensors, and insurance claims. This information can be primary data collected directly for a specific study, or secondary data repurposed from existing clinical records.

The healthcare data collection and labeling market is segmented by data type, labeling approach, end users, and geography. By data type, the market is categorized into image, text, video, and audio. By the labeling approach, the market is divided into manual, semi-automated, and fully automated. By end users, the segmentation includes life-science & pharma companies, medical-device manufacturers, hospitals & IDNs, health-tech, and CROS & academic institutes. By application area, the segmentation includes diagnostic imaging AI, clinical decision support, drug discovery/biomarker identification, and population health & remote monitoring. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Image |

| Text |

| Video |

| Audio |

| Manual |

| Semi-Automated |

| Fully-Automated |

| Life-Science & Pharma Companies |

| Medical-Device Manufacturers |

| Hospitals & IDNs |

| Health-Tech |

| CROs & Academic Institutes |

| Diagnostic Imaging AI |

| Clinical Decision Support (CDS) |

| Drug Discovery / Biomarker Identification |

| Population Health & Remote Monitoring |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Data Type | Image | |

| Text | ||

| Video | ||

| Audio | ||

| By Labeling Approach | Manual | |

| Semi-Automated | ||

| Fully-Automated | ||

| By End User | Life-Science & Pharma Companies | |

| Medical-Device Manufacturers | ||

| Hospitals & IDNs | ||

| Health-Tech | ||

| CROs & Academic Institutes | ||

| By Application Area | Diagnostic Imaging AI | |

| Clinical Decision Support (CDS) | ||

| Drug Discovery / Biomarker Identification | ||

| Population Health & Remote Monitoring | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the healthcare data collection and labeling market?

The market is expected to reach USD 2.57 billion in 2026 and is projected to reach USD 5.62 billion by 2031.

Which data type is growing the fastest in healthcare annotation?

Video annotation leads with a 17.40% CAGR, driven by robotic-surgery and procedural-training applications.

Why are pharmaceutical companies increasing spending on data labeling?

FDA acceptance of real-world evidence and multi-omics biomarker strategies is pushing pharma to build expertly annotated datasets that shorten drug-discovery timelines

How are privacy regulations affecting annotation costs?

Compliance with HIPAA, GDPR, and CPRA can consume 15–25% of project budgets due to technical safeguards, legal audits, and patient data-deletion rights.

Which region will see the quickest growth through 2031?

Asia-Pacific is expected to record a 17.30% CAGR, propelled by large public investments in China, India, and Japan.

Page last updated on: