Healthcare Cold Chain Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 137.27 Billion |

| Market Size (2031) | USD 223.39 Billion |

| Growth Rate (2026 - 2031) | 10.23% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Healthcare Cold Chain Market Analysis by Mordor Intelligence

The Healthcare Cold Chain Market size is projected to expand from USD 124.53 billion in 2025 and USD 137.27 billion in 2026 to USD 223.39 billion by 2031, registering a CAGR of 10.23% between 2026 to 2031.

Demand momentum reflects a steady pivot to temperature-sensitive biologics as 43% of newly approved drugs in recent years required cold storage, which raises the bar for validated equipment, data integrity, and continuous monitoring to ensure product quality. Large global immunization initiatives and catch-up campaigns reinforce steady volume flows, while HPV scale-up in lower-income countries adds recurring, distributed demand patterns across last-mile networks. Cell and gene therapies expand the addressable scope of the healthcare cold chain market as cryogenic and ultra-low temperature use cases become routine in commercial and late-phase programs. Real-time visibility and IoT-enabled decision support are now standard expectations, replacing retrospective data checks with active intervention at lane, asset, and shipment levels. The broader cold chain logistics context across food and pharma is expanding as well, which informs long-term capital planning for carriers, 3PLs, and packaging vendors.

Key Report Takeaways

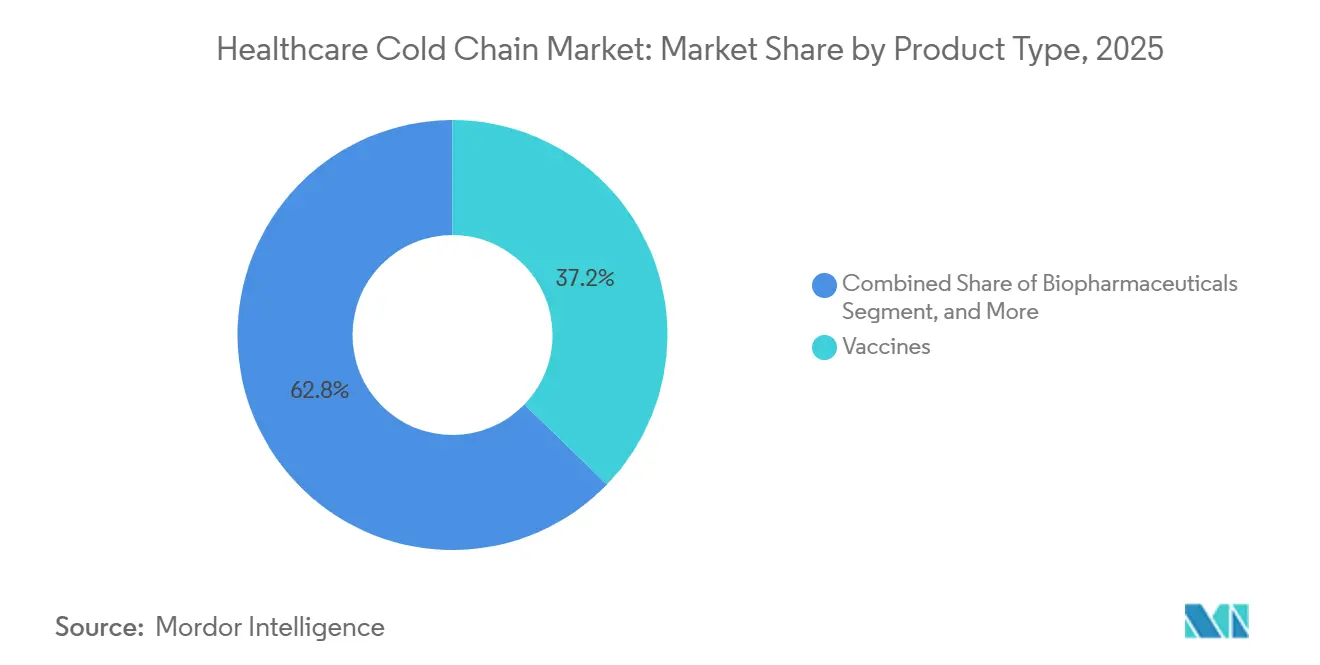

- By product type, vaccines led with 37.23% revenue share in 2025; cell and gene therapies are forecast to expand at a 10.80% CAGR through 2031 in the healthcare cold chain market.

- By service type, transportation held 45.20% share in 2025; monitoring and tracking systems are projected to grow at an 11.50% CAGR to 2031 in the healthcare cold chain market.

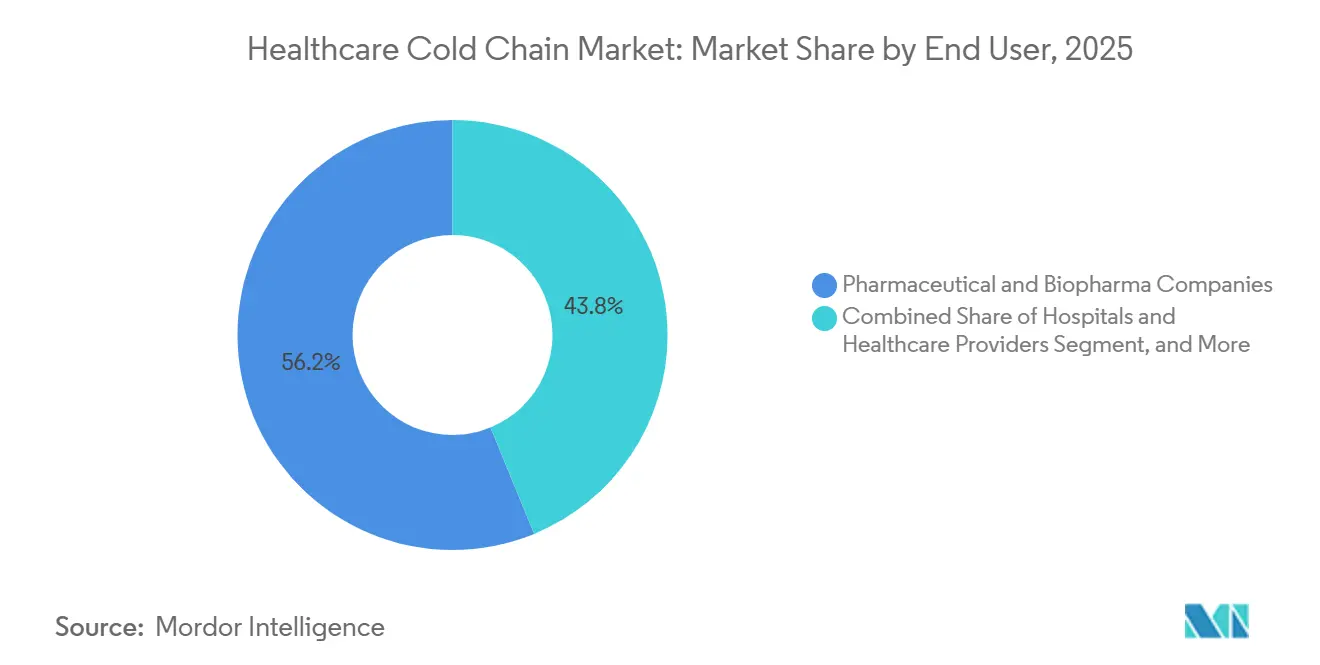

- By end user, pharmaceutical and biopharma companies commanded 56.20% share in 2025; CROs and clinical trial organizations are projected to expand at a 12.45% CAGR through 2031.

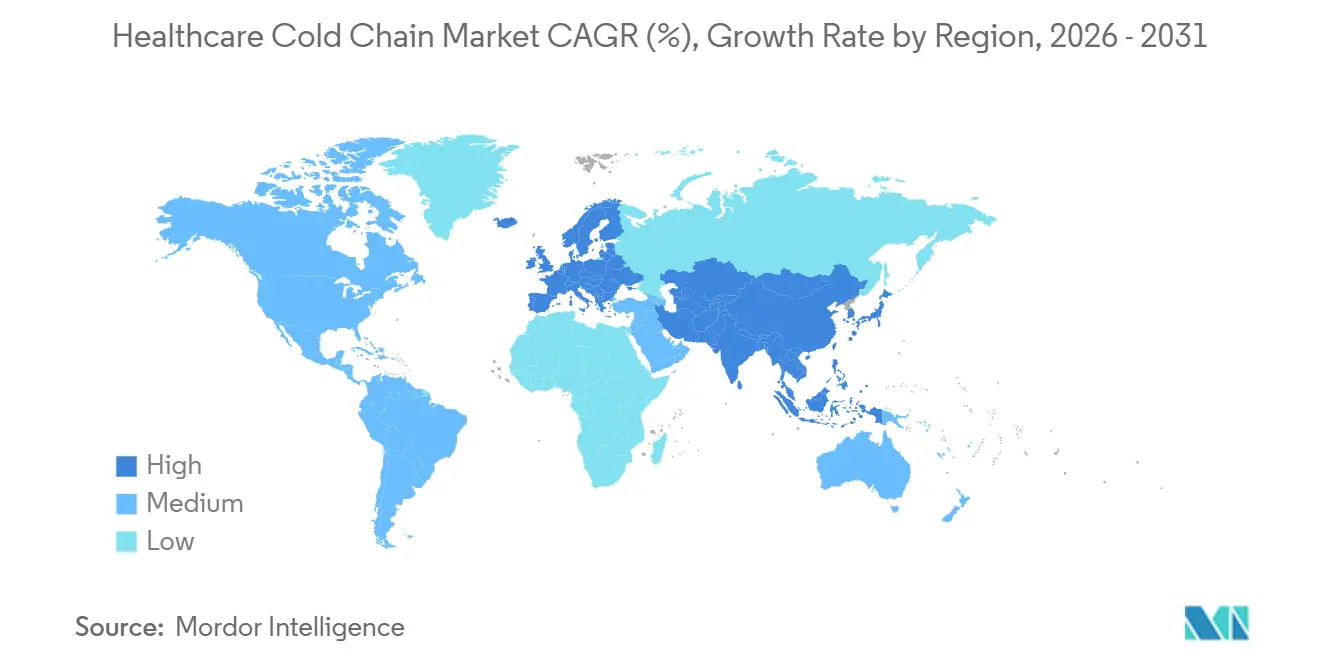

- By geography, North America held 43.12% of the healthcare cold chain market share in 2025, while Asia-Pacific recorded the highest projected CAGR at 14.65% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare Cold Chain Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Biologics and Specialty Drugs | +2.8% | Global, with concentration in North America, Western Europe, China, and India | Medium term (2-4 years) |

| Global Vaccine Expansion and Immunization Programs | +1.9% | Global, strongest gains in Sub‑Saharan Africa, South Asia, and Gavi‑eligible countries | Short term (≤ 2 years) |

| Growth of Clinical Trials and Decentralized/Direct‑To‑Patient | +1.4% | North America and EU core, expanding to Asia‑Pacific | Medium term (2-4 years) |

| Technological Advancements in IoT, Real‑Time Visibility, Analytics | +2.1% | Global, led by North America and Western Europe | Short term (≤ 2 years) |

| Sustainability Mandates Reshaping Procurement and Packaging | +0.7% | Europe, North America, expanding to Asia‑Pacific | Long term (≥ 4 years) |

| Cell And Gene Therapy Scale‑Up Needing ULT/Cryogenic Networks | +1.3% | North America, Western Europe, early adoption in Japan and South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Biologics and Specialty Drugs Accelerates Cold Chain Infrastructure

Biologics now anchor investment priorities in the healthcare cold chain market as 43% of drugs approved over 2018 2023 required refrigerated or frozen handling, which raises operating rigor from fill finish to last mile. Temperature excursions can degrade protein-based therapies, so validated storage, lane qualification, and continuous temperature monitoring are central to protecting product integrity and patient safety.[1]National Institutes of Health, “Regulatory Knowledge Guide for Biological Products,” NIH SEED Compliance frameworks such as USP 1079 reinforce risk-based controls for storage and transportation and call for robust performance qualification that reflects worst-case conditions.[2]United States Pharmacopeia, “USP General Chapter <1079> Risks and Mitigation Strategies for the Storage and Transportation of Finished Products,” WHO vaccine packaging and shipping guidance, together with PQS equipment specifications, also inform equipment choices, acceptance testing, and lane procedures for international shipments in the healthcare cold chain market.[3]World Health Organization, “Guidelines for the International Packaging and Shipping of Vaccines, 7th ed.,” Packaging investment is scaling in response, with industry vendors reporting strong multi-year growth in insulated shippers, phase change materials, and vacuum insulated panels aligned to tougher qualification standards. The healthcare cold chain market benefits from this shift since biologics pipelines sustain recurring replenishment cycles, wider geographic distribution, and tighter compliance baselines across manufacturers and 3PLs.

Global Vaccine Expansion Drives Distributed Cold Chain Networks

Expanded immunization programs are reshaping the healthcare cold chain market as Gavi-supported countries protected 72 million children in 2024 and recorded USD 255 million in co-financing, which signals durable national ownership of vaccine budgets.[4]Gavi, the Vaccine Alliance, “2024 global immunization coverage estimates: understanding the picture in lower-income countries,” HPV coverage in lower-income countries rose from 3% in 2019 to 25% in 2024, with 32.6 million girls immunized in 2024, more than double the prior year, which increases demand for refrigerated transport and storage at subnational levels.[5]International Vaccine Access Center, “Global Vaccine Introduction and Implementation Report - VIEW-hub,” Johns Hopkins Bloomberg School of Public HealthGavi also reported progress on measles and DTP3 coverage in 2024, though pockets of zero-dose children remain, which underscores the need for resilient last-mile equipment and power solutions in fragile and conflict-affected settings. WHO’s Essential Program on Immunization recommends medical-grade refrigerators with forced air circulation, backup power, and temperature mapping to identify hot and cold spots, all of which improve inventory integrity in primary health centers. WHO PQS prequalified solar direct drive vaccine refrigerators and freezers offer reliable performance in off-grid locations and align with energy resilience priorities in distributed networks. As programs widen coverage and introduce more antigens, the healthcare cold chain market gains from scaled replenishment, upgraded equipment fleets, and broader transport lanes, especially for national immunization programs and partners.

IoT, Real Time Visibility, and Predictive Analytics Transform Passive Monitoring into Active Intervention

IoT sensors and real-time visibility platforms are moving the healthcare cold chain market from retrospective audits to proactive control. System Loco reports more than 200 million data points processed daily across 2.8 million deployed devices, which supports one-click compliance records and predictive quality flags that reduce exception handling time. Sensitech’s TempTale GEO X, launched in February 2024, extends real-time monitoring across the −95°C to +55°C range and integrates with SensiWatch for automated product disposition to cut cycle time on accept-reject decisions. Vendors also cite predictive maintenance that uses equipment telemetry, such as compressor vibration and power draw, to anticipate failures and reduce unplanned downtime and repair costs in temperature-controlled fleets. Logistics route optimization is scaling as well, with fleet systems like ORION raising on-time performance and lowering fuel use, which helps reduce both unit cost and emissions on validated lanes in the healthcare cold chain market. Industry pilots have also explored blockchain to create tamper-evident traceability across complex handoffs, which supports anti-counterfeit controls when combined with serialization and real-time telemetry.

Cell and Gene Therapy Scale Up Requires ULT and Cryogenic Networks

Cell and gene therapy programs are building a specialized substratum of the healthcare cold chain market as clinical and commercial volumes increase. Industry tracking indicates more than 35 approvals by early 2026 and a healthy late-stage pipeline, which sustains demand for liquid nitrogen-enabled storage, cryogenic lane certification, and “vein to vein” orchestration in autologous therapies. Specialized logistics for these shipments operate below −150°C and require a strict chain of identity and chain of custody controls, which amplifies the need for GPS-enabled IoT devices, lane playbooks, and exception response teams. The commercial and clinical value at risk per shipment is very high, which pushes operators to tighten SOPs, build redundancy, and invest in PQS-aligned hardware across both storage and transport assets in the healthcare cold chain market. Strategic moves underscore this focus, such as Cryoport’s divestiture of CRYOPDP to DHL to strengthen global specialty courier coverage while concentrating on regenerative medicine services and infrastructure. With growth continuing through 2031, cryogenic capacity, dry shipper management, and end-to-end digital traceability remain priority buildouts for the healthcare cold chain market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Operational and Infrastructure Costs | -2.3% | Global, most acute in developed markets with aging facilities and high energy costs | Short term (≤ 2 years) |

| Regulatory Complexity and Compliance Burden | -1.5% | Global, with fragmentation across jurisdictions increasing administrative overhead | Medium term (2-4 years) |

| Dry Ice/LN2 Supply Volatility and Cost Shocks | -0.9% | Global, with notable exposure in Europe | Short term (≤ 2 years) |

| Certified Lane and Airport Capacity Bottlenecks for Pharma Air Cargo | -0.8% | Sub‑Saharan Africa, Latin America, select APAC corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Operational and Infrastructure Costs Constrain Capacity Expansion

Operating costs weigh on near-term margin structure as refrigeration power is the dominant warehouse load, and energy expenses make up a large share of cold storage operating costs for the healthcare cold chain market. Vendors also report steady rent inflation and capacity tightness since 2019, which lifts carrying costs and complicates network design in legacy real estate. Labor remains a structural pressure where GxP-trained roles are scarce, and wage rates rise, which increases dependence on automation and digital monitoring in storage and in transit. Temperature excursions impose major economic risk as industry sources estimate significant annual losses from cold chain failures, which reinforces the case for better packaging, visibility, and standard work in the healthcare cold chain market. Dry ice and liquid nitrogen procurement can also be volatile at the corridor level, so shippers diversify sources and optimize charging protocols to stabilize supply. Packaging specifications continue to evolve with the use of high-performance insulation and phase change materials to hold lane performance under more stringent qualification regimes, a trend reinforced by supplier guidance and customer validation programs.

Regulatory Complexity and Fragmented Compliance Standards Elevate Administrative Burden

Serialization, electronic traceability, and GDP controls increase administrative and IT workloads, especially for smaller wholesalers and regional carriers. USP guidance on storage and transportation, together with WHO packaging and shipping guidelines, sets out risk-based qualification and continuous temperature monitoring practices that must be met across distributed networks. Industry playbooks also align with IATA’s temperature control requirements for airfreight and emphasize labeling, acceptance checklists, and handler training to mitigate tarmac risks for the healthcare cold chain market. U.S. traceability mandates and EU GDP rules continue to phase in system changes and audit expectations, which raise interface, data quality, and SOP harmonization needs across partners. Cross-border shipments for advanced therapies add more complexity since country classification and permit lead times vary, which requires earlier planning and active brokerage coordination for cryogenic moves in the healthcare cold chain market. The net effect is a larger baseline of documentation, training, and digital connectivity that determines supplier selection, audit readiness, and risk posture.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vaccines Dominate Current Share, Cell and Gene Therapies Chart the Fastest Expansion

Vaccines accounted for 37.23% of the healthcare cold chain market share in 2025 as routine immunization and pandemic preparedness drove steady replenishment and last-mile traffic. Gavi-supported countries protected 72 million children in 2024 and achieved record co-financing, which boosted volumes across countries and subnational warehouses. HPV coverage climbed to 25% in 2024 across lower-income countries, with 32.6 million girls vaccinated that year, which widened recurring demand for 2°C to 8°C capacity in district stores and clinics. WHO’s Essential Program on Immunization frames equipment and operating standards and guides the upgrade path from domestic fridges to medical-grade units with forced air circulation and backup power. Temperature requirements differ by antigen class as most vaccines ship at 2°C to 8°C while some viral vaccines ship frozen, and mRNA products may need ultra cold lanes, so lane design must align with product label and qualification evidence in the healthcare cold chain market. WHO PQS prequalified solar direct drive refrigerators and freezers improve service continuity in off-grid areas and reduce dependence on bottled gas or unstable mains power.

Cell and gene therapies post the steepest growth trajectory through 2031, supported by approvals, late stage trials, and specialized logistics that require cryogenic handling. The healthcare cold chain market size for cell and gene therapies is projected to expand at a 10.80% CAGR through 2031 as programs scale and more centers come online. Cryogenic shipping under −150°C relies on liquid nitrogen dry shippers with multilayer qualification, GPS tracking, and chain of identity controls to eliminate mix ups in batch of one workflows. Commercial shipments carry high value per movement, so playbooks emphasize redundancy on dewars, lanes, and carriers as part of risk mitigation in the healthcare cold chain market. Cryoport’s sale of CRYOPDP to DHL in June 2025 broadened the specialty courier footprint while allowing Cryoport to focus on integrated regenerative medicine services and storage, and it strengthened network options for CGT customers. With more late phase trials in flight, commercial launches will add to demand for validated cryogenic networks that integrate with manufacturing sites, treatment centers, and regional depots.

By Service Type: Transportation Holds the Largest Share, Monitoring Systems Grow the Fastest

Transportation services accounted for 45.20% of the healthcare cold chain market in 2025, as refrigerated trucking, time and temperature-sensitive airfreight, and multimodal lanes require capital, certifications, and trained personnel. IATA temperature control rules call for special labeling, acceptance checklists, and handler training, and these steps reduce tarmac exposure risks and mis-sorts during handoffs. DHL Group is expanding dedicated airfreight capacity on pharma lanes, including a Boeing 777 freighter on the Brussels–Cincinnati corridor and pharma-only zones at BRUcargo to scale compliant throughput for the healthcare cold chain market. UPS Healthcare completed the acquisitions of Frigo Trans and BPL to extend Europe’s temperature-controlled coverage across −196°C to +25°C ranges, which supports everything from cryopreserved therapies to controlled room temperatures. These commitments align transport capacity with new product classes, higher service levels, and wider geographic reach in the healthcare cold chain market.

Monitoring and tracking systems are projected to post an 11.50% CAGR through 2031. The healthcare cold chain market size for monitoring and tracking systems is therefore set to increase as compliance baselines embed continuous logging, audit trails, and proactive alerting. USP guidance and WHO documents underscore the need for accurate and frequent temperature logging, and data integrity controls that stand up to regulatory scrutiny. Industry analysis highlights rapid expansion in cold chain monitoring hardware and software, with hardware such as sensors, RFID, and GPS capturing most of the revenue today. System Loco reports that greater visibility can reduce temperature excursions and audit preparation time, which helps lower waste and improves on time releases in the healthcare cold chain market. Kelsius launched CoolTrak365 in January 2026 to deliver real time excursion alerts and automated uploads, which reduces manual entry errors and supports GxP alignment. Packaging innovation remains part of the control stack as phase change materials and VIPs maintain lane stability and offset external shocks, in line with supplier guidance for the healthcare cold chain market. Industry sources continue to emphasize that temperature excursions drive large global losses, so better sensors, analytics, and packaging are strategic levers to improve service quality and reduce waste.

By End User: Pharmaceutical and Biopharma Companies Lead Demand, CROs Surge with Decentralized Trials

Pharmaceutical and biopharma companies represented 56.20% of demand in 2025, reflecting their role as primary manufacturers and distributors of temperature-sensitive products across global networks. The share of new FDA approvals requiring cold storage underscores this reliance on cold chain capacity. It helps explain recurring investment in storage, packaging, and in-transit monitoring in the healthcare cold chain market. Vendors report sustained growth in pharmaceutical cold chain packaging that aligns with larger biologics pipelines and higher validation standards. Cencora announced a USD 1 billion multi-year investment program to expand and modernize U.S. distribution, which includes a 530,000 square foot national hub in Ohio and significant refrigerated capacity in Alabama, and this strengthens regional service levels for the healthcare cold chain market. DHL’s dedicated airfreight corridors and pharma-only zones complement these manufacturers’ needs by lifting compliant throughput on core transatlantic lanes. These investments emphasize efforts to strengthen networks for high-value, multi-year pharmaceutical products, focusing on direct-to-patient delivery, point-of-care services, and maintaining the quality of in-transit therapeutics within the healthcare cold chain market.

CROs and clinical trial organizations show the fastest growth outlook as decentralized and direct-to-patient models spread. The healthcare cold chain market size for CROs and clinical trial organizations is projected to expand at a 12.45% CAGR through 2031 as protocol designs add home delivery, site-to-patient shipments, and remote monitoring. Cryoport reported support for hundreds of trials across phases, which highlights growing demand for cryogenic storage, specialty couriers, and an integrated chain of identity controls for batch of one therapies. Autologous cell therapy workflows require “vein to vein” orchestration and tight delivery windows for cryogenic returns, so digital and operational controls must extend across sites, couriers, and depots in the healthcare cold chain market. Hospitals and integrated delivery networks also handle point-of-care cold chains for vaccines and biologics, which increases the value of automated monitoring and alerting to safeguard inventory at the last mile. Research and academic institutes continue to scale their investigational product flows within national networks, supported by standardized packaging and PQS-aligned equipment to reduce the risk of excursions in the healthcare cold chain market.

Geography Analysis

North America holds 43.12% of the 2025 healthcare cold chain market, supported by U.S. leadership in biologics manufacturing, strong FDA-aligned compliance practices, and broad adoption of IoT visibility. The region benefits from large-scale investments across distribution centers, dedicated healthcare fleets, and specialized cryogenic services that match the complexity of CGT and biologics portfolios in the healthcare cold chain market. Cencora’s USD 1 billion program includes a 530,000 square foot national distribution center in Ohio that is scheduled for spring 2027 and a large increase in refrigerated capacity in Alabama scheduled for fall 2026, which lifts throughput and resilience. UPS Healthcare’s acquisitions of Frigo Trans and BPL expand temperature-controlled capabilities within Pan European corridors and reinforce integrated coverage for North American shippers with Europe-bound flows, ranging from cryogenic to controlled room temperatures. With continued emphasis on real-time visibility and route optimization, operators aim to compress exception rates and stabilize on-time performance in the healthcare cold chain market.

Europe is a major hub for compliant distribution due to rigorous GDP expectations and strong biologics consumption across Germany, Switzerland, and the United Kingdom. DHL’s EUR 2 billion (USD 1.16 billion) program to expand its airfreight cold chain network includes a dedicated 777 freighter between Brussels and Cincinnati and pharma-only zones at BRUcargo, which enhances bidirectional connectivity with the United States in the healthcare cold chain market. UPS expanded its European cold chain capability via Frigo Trans and BPL, which adds certified lanes and warehousing that span −196°C to +25°C and tightens control across handoffs. Cencora is improving its Pan European logistics footprint through partnerships and new facilities planned for 2026, which increases options for specialty distribution and trial supply in the healthcare cold chain market. Industry investment patterns and regulatory alignment continue to raise service standards while keeping focus on audit readiness, validated equipment, and orchestrated exception handling.

Asia-Pacific is projected to post the fastest regional growth rate at a 14.65% CAGR through 2031 as manufacturers scale in China and India and as regional hubs in Singapore, Japan, and South Korea add specialized capacity. The healthcare cold chain market size in the Asia-Pacific is therefore set to expand as more facilities come online with GMP-compliant storage and cryogenic services for advanced therapies and clinical research. DHL allocated EUR 500 million for Asia-Pacific through 2030 and opened a EUR 10 million dedicated pharmaceutical hub in Singapore in February 2026 with specialized temperature zones from cryogenic to ambient near Tuas Biomedical Park. The Singapore facility includes GMP-compliant infrastructure that supports biologics, vaccines, and clinical trial logistics, which strengthens a regional anchor for the healthcare cold chain market. Governments in Southeast Asia are investing in capacity and digitalization, including new cold stores in the Philippines and route optimization with solar-powered equipment and telemetry in Indonesia, which reduces spoilage risk and raises visibility. WHO guidance continues to shape equipment selection and qualification, helping health systems raise last-mile reliability in the healthcare cold chain market.

Competitive Landscape

Global integrators such as DHL Group (Deutsche Post AG), UPS Healthcare (United Parcel Service, Inc.), and FedEx Corporation operate multimodal networks and certified storage footprints that offer scale advantages, while specialty firms like Cryoport, Marken, and World Courier focus on premium cold chain niches that include cryogenic services for cell and gene therapies. U.S. wholesale and specialty distributors such as Cencora, Cardinal Health, and McKesson own critical distribution infrastructure and deep manufacturer relationships, which make them central nodes in national networks for the healthcare cold chain market. Competitive intensity is highest in margin-rich categories like CGT moves and time and temperature-sensitive air cargo, where service differentiation relies on validated equipment, digital visibility, and consistent exception management. Technology roadmaps center on continuous monitoring, predictive maintenance, and digital traceability, which are now basic requirements in tenders and quality agreements. Together, these dynamics reinforce moderate fragmentation with clear leadership pockets across corridors and service categories in the healthcare cold chain market.

DHL Group’s multi-year EUR 2 billion program adds dedicated air capacity and pharma-only zones across Europe and North America to raise throughput and consistency on key lanes. DHL also acquired CRYOPDP from Cryoport in 2025 to deepen its specialty courier network across 15 countries and add capacity for time critical healthcare shipments in the healthcare cold chain market. UPS Healthcare completed the acquisitions of Frigo Trans and BPL to extend its European temperature controlled capabilities from cryogenic to controlled room temperature and connect more certified locations. These moves expand gateway options, build redundancy, and offer manufacturers more validated lanes at scale in the healthcare cold chain market.

Cryoport’s divestiture of CRYOPDP and sustained investments in BioStorage and BioServices highlight a shift to integrated regenerative medicine services, supporting hundreds of clinical trials and multiple commercial therapies. Cencora announced a USD 1 billion program to strengthen U.S. distribution, including a large national hub and greater refrigerated capacity to improve throughput for specialty products in the healthcare cold chain market. EVERSANA expanded to over 1.25 million square feet with a 358,000 square foot center in Memphis, which adds controlled room temperature and cold storage capacity and deploys automation to raise efficiency. World Courier expanded its cryogenic network to support next era CGT logistics, highlighting demand for consistent chain of identity and end to end traceability in the healthcare cold chain market. Peli BioThermal expanded its Frankfurt hub to unlock more capacity for European cold chain flows, which supports a wider mix of pharmaceuticals and clinical trial materials.

Healthcare Cold Chain Industry Leaders

-

Biocair International Ltd.

-

Berlinger & Co. AG

-

DHL Group (Deutsche Post AG)

-

FedEx Corporation

-

UPS Healthcare (United Parcel Service, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: DHL Group expanded its dedicated Airfreight Cold Chain Network, part of a EUR 2 billion investment in DHL Health Logistics. The initiative includes a dedicated Boeing 777 freighter on the Brussels–Cincinnati corridor, connecting over 30 GDP-compliant aviation hubs and 45,000 square meters of pharma-only zones at BRUcargo, targeting pharmaceuticals, vaccines, and cell and gene therapies.

- February 2026: DHL Health Logistics Singapore unveiled a EUR 10 million Pharmaceutical Hub near Tuas Biomedical Park, featuring specialized temperature zones from ambient to ultra-deep frozen (below −180°C) and GMP-compliant infrastructure. The facility supports pharmaceutical, clinical trial, and medical device logistics, part of a EUR 500 million regional investment by 2030.

- January 2026: Kelsius launched CoolTrak365, a healthcare cold chain monitoring solution offering real-time excursion alerts, regulatory compliance aligned with GxP standards, and automated data uploads to streamline operations for medicines, vaccines, and temperature-sensitive medical products.

Global Healthcare Cold Chain Market Report Scope

As per the scope of the report, the healthcare cold chain refers to a temperature-controlled supply chain system used to store, handle, and transport sensitive healthcare products such as vaccines, biologics, and pharmaceuticals. It ensures that these products are maintained within specific temperature ranges throughout the entire lifecycle, from manufacturing to end use. The system includes refrigerated storage, specialized packaging, transportation, and monitoring technologies to preserve product quality, safety, and efficacy.

The healthcare cold chain market is segmented by product type, service type, end user, and geography. By product type, the market is segmented into vaccines, biopharmaceuticals, clinical trial materials, blood & plasma products, and cell & gene therapies. By service type, the market is segmented into transportation, storage & warehousing, packaging solutions, and monitoring & tracking systems. By end user, the market is segmented into pharmaceutical & biopharma companies, hospitals & healthcare providers, research & academic institutes, and CROs / clinical trial organizations. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Vaccines |

| Biopharmaceuticals |

| Clinical Trial Materials |

| Blood & Plasma Products |

| Cell & Gene Therapies |

| Transportation |

| Storage & Warehousing |

| Packaging solutions |

| Monitoring & tracking systems |

| Pharmaceutical & Biopharma Companies |

| Hospitals & Healthcare Providers |

| Research & Academic Institutes |

| CROs / Clinical Trial Organizations |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Vaccines | |

| Biopharmaceuticals | ||

| Clinical Trial Materials | ||

| Blood & Plasma Products | ||

| Cell & Gene Therapies | ||

| By Service Type | Transportation | |

| Storage & Warehousing | ||

| Packaging solutions | ||

| Monitoring & tracking systems | ||

| By End User | Pharmaceutical & Biopharma Companies | |

| Hospitals & Healthcare Providers | ||

| Research & Academic Institutes | ||

| CROs / Clinical Trial Organizations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the healthcare cold chain market?

The healthcare cold chain market size is USD 124.53 billion in 2025 and is projected to reach USD 223.39 billion by 2031 at a 10.23% CAGR.

Which product category holds the largest share in 2025?

Vaccines led with 37.23% share in 2025, supported by national immunization programs and growing HPV coverage in lower income countries.

Which end user shows the fastest growth through 2031?

CROs and clinical trial organizations show the fastest trajectory, with a projected 12.45% CAGR as decentralized and direct to patient models scale.

What service line is expanding the quickest?

Monitoring and tracking systems are projected to grow at an 11.50% CAGR, driven by real time visibility, electronic records, and audit ready data.

How are cell and gene therapies changing logistics needs?

CGT requires cryogenic handling below −150°C with GPS enabled tracking and strict chain of identity controls, which expands specialized capacity.

Which region is poised for the fastest expansion?

Asia-Pacific is projected to grow the fastest through 2031, supported by new GMP compliant hubs, cryogenic services, and large scale investments.

Page last updated on: