Healthcare Biosensors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 21.51 Billion |

| Market Size (2031) | USD 34.11 Billion |

| Growth Rate (2026 - 2031) | 9.67% CAGR |

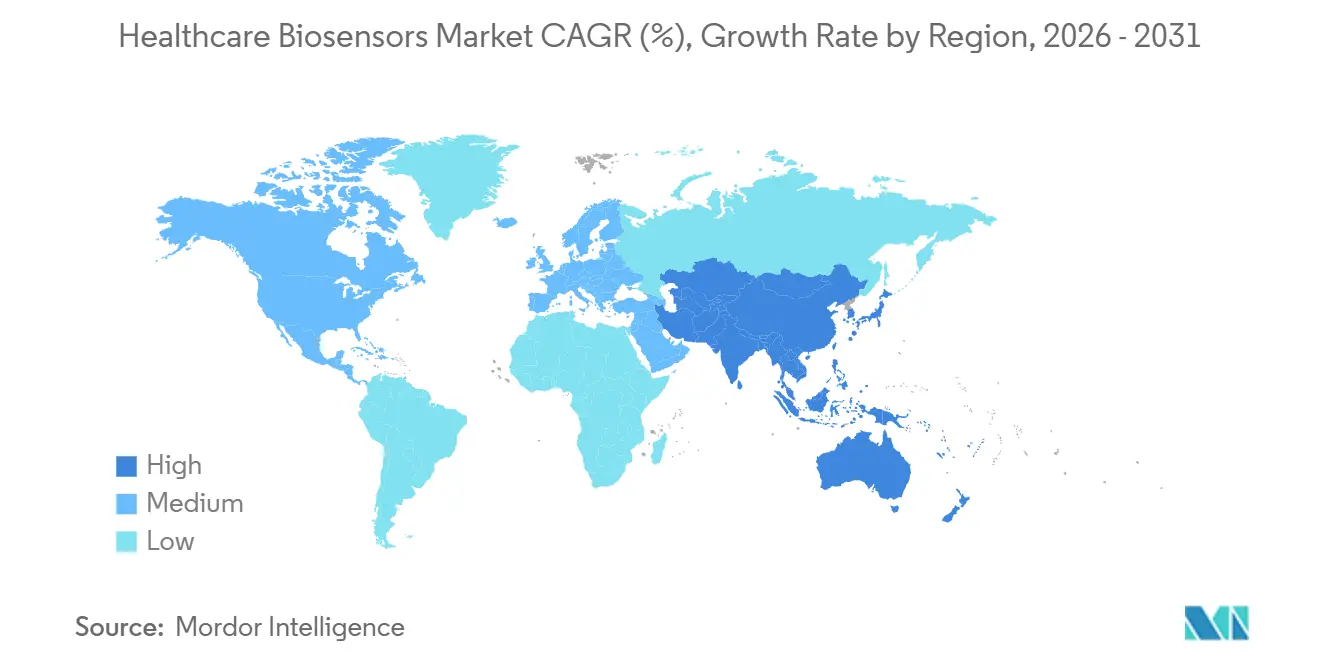

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

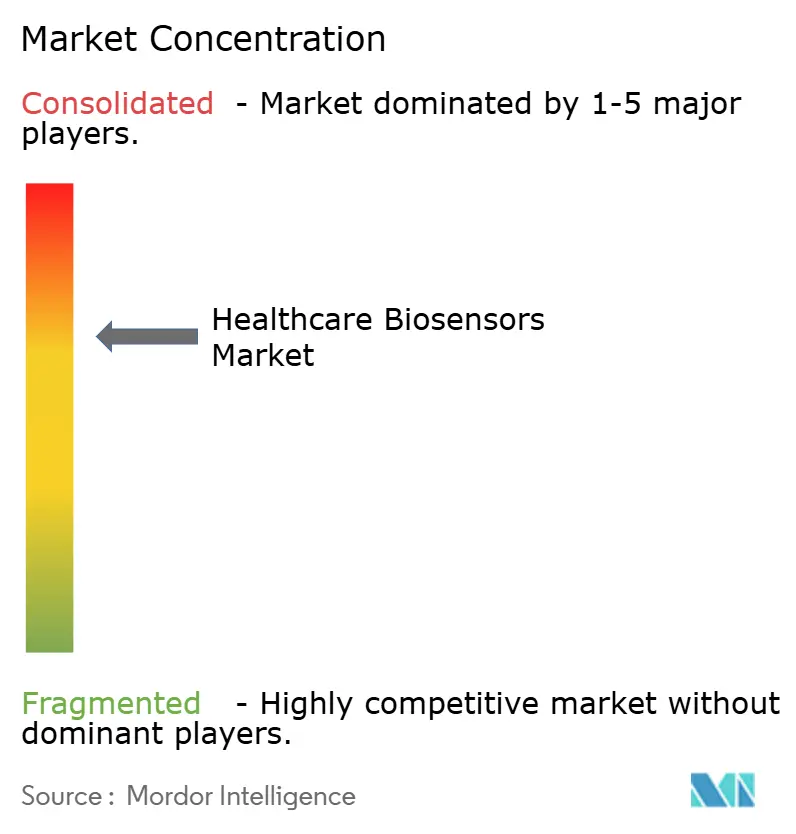

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Biosensors Market Analysis by Mordor Intelligence

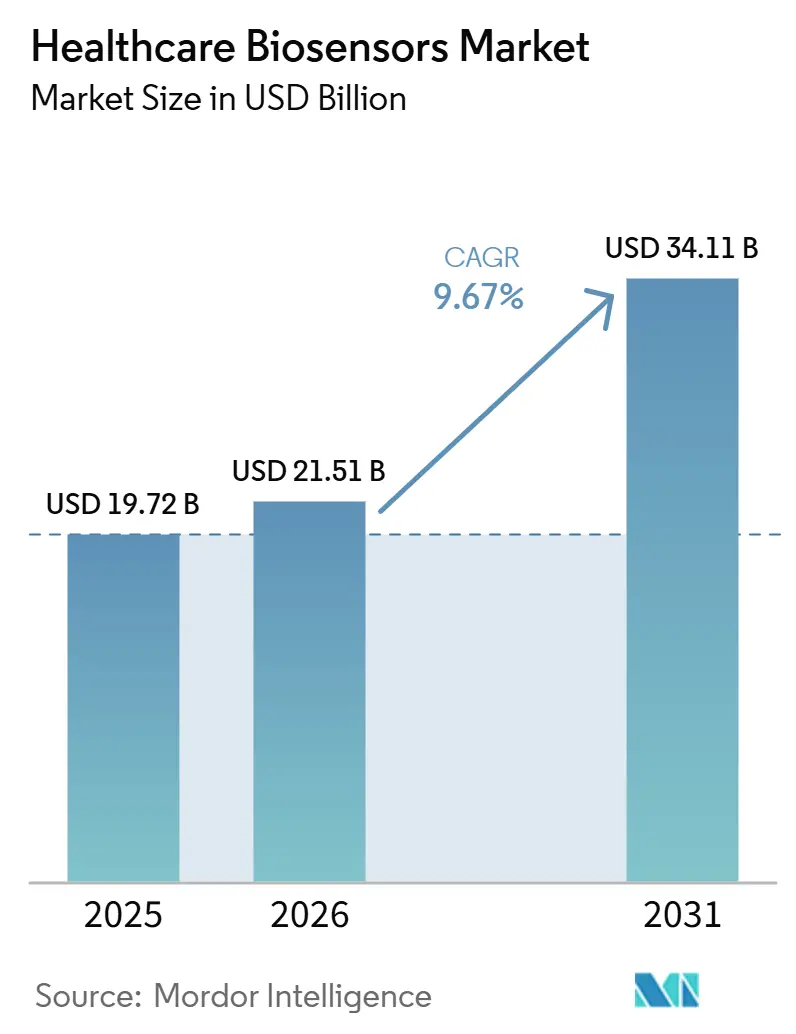

The healthcare biosensors market is expected to increase from USD 19.72 billion in 2025 to USD 21.51 billion in 2026 and reach USD 34.11 billion by 2031, growing at a CAGR of 9.67% over 2026-2031. The healthcare biosensors market is moving on the back of a larger chronic disease burden, especially diabetes and cardiovascular conditions that need continuous tracking and quicker clinical response. Demand is also shifting toward testing closer to the patient, because pharmacies, clinics, and home settings are taking on a larger role in routine monitoring and rapid decision making. At the same time, device makers are widening product value through AI-supported sensing, multi-analyte detection, and recurring data services that extend revenue beyond hardware sales in the healthcare biosensors market. Reimbursement support for remote patient monitoring is improving the business case for provider adoption, while stricter regulatory pathways in Europe are raising compliance demands and favoring companies with deeper validation and scale. Competition therefore remains active between global medtech companies with broad clinical platforms and smaller innovators that focus on wearables, miniaturization, and software-led monitoring models in the healthcare biosensors market.

Key Report Takeaways

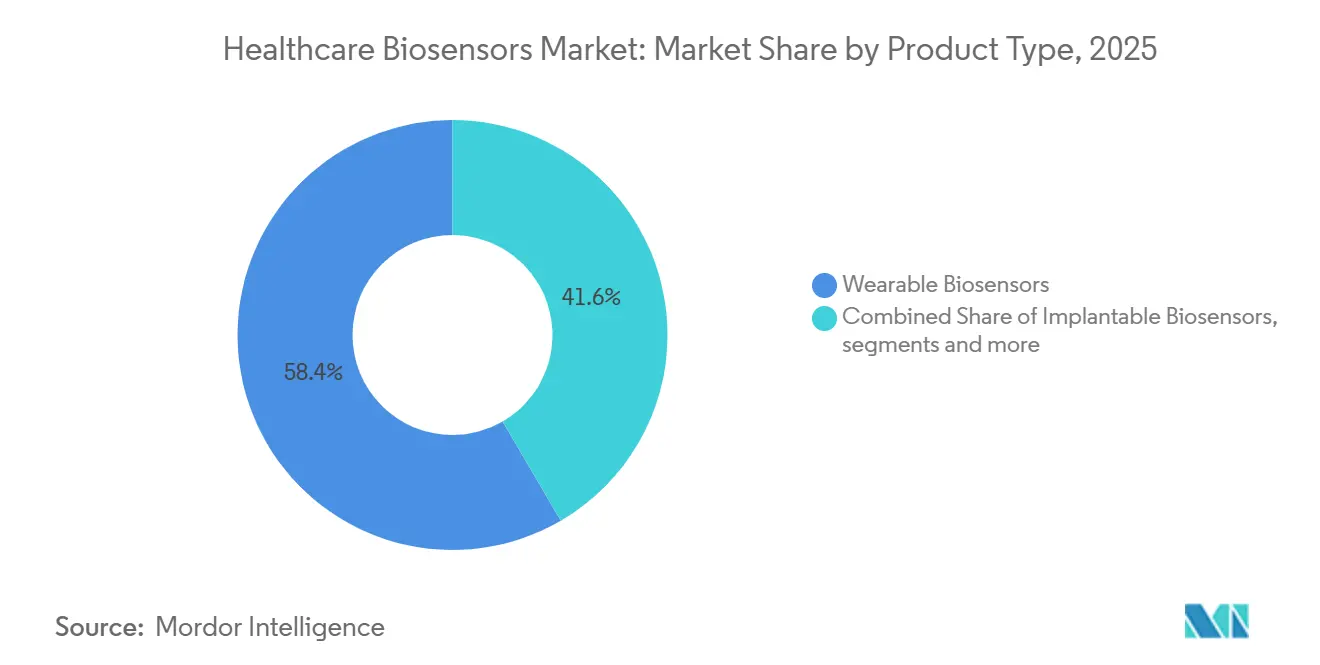

- By product type, wearable biosensors led with 58.40% revenue share in 2025, while point-of-care biosensors recorded the highest projected CAGR at 11.80% through 2031.

- By technology, electrochemical biosensors held 61.70% share in 2025, while piezoelectric biosensors are forecasted to expand at a 12.40% CAGR through 2031.

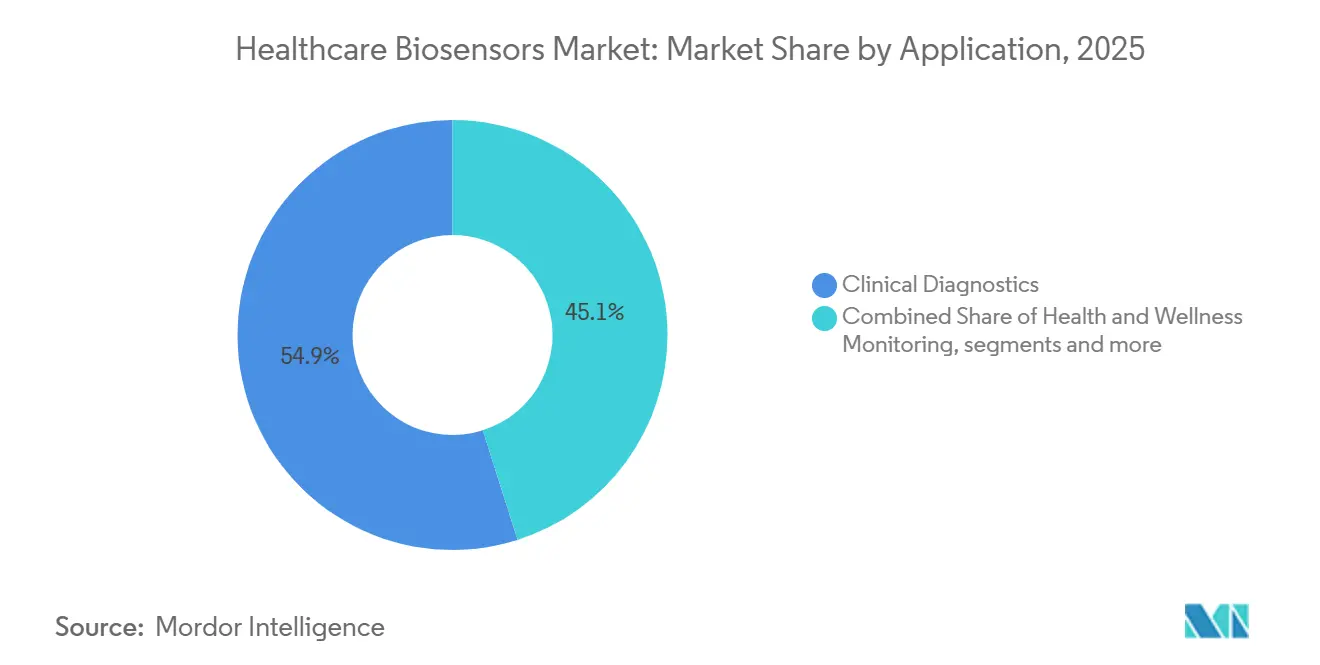

- By application, clinical diagnostics accounted for 54.90% share in 2025, while chronic disease management is anticipated to advance at a 12.90% CAGR through 2031.

- By end-user, hospitals and clinics captured 48.20% share in 2025, while homecare settings are projected to grow at an 11.60% CAGR through 2031.

- By geography, North America held 42.50% share in 2025, while Asia-Pacific is projected to expand at a 12.30% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare Biosensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Point-of-Care and At-Home Testing Demand | +2.5% | Global, concentrated in North America, APAC, and select EU markets | Short term (≤ 2 years) |

| Growing Diabetes and Cardiometabolic Burden | +2.2% | Global, highest intensity in North America, Middle East and Africa, and APAC | Long term (≥ 4 years) |

| Miniaturization, AI, And Multi-Analyte Sensing Integration | +1.8% | Global, with R&D leadership in North America, Japan, and Germany | Medium term (2-4 years) |

| Reimbursement Expansion for Remote Monitoring Use Cases | +1.2% | North America and EU, with spillover to Australia and South Korea | Short term (≤ 2 years) |

| Data-Linked Service Models, Not Just Device Sales | +0.9% | North America, then EU and core APAC markets | Medium term (2-4 years) |

| Clinical Validation Advantage for Non-Invasive Biosensing | +0.8% | Global, with regulatory benefits concentrated in North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Point-of-Care and At-Home Testing Demand

The healthcare biosensors market is being shaped by a lasting move away from central laboratories and toward pharmacies, clinics, and patient homes. Health systems in North America and Western Europe continue to face staffing and capacity pressure, which supports testing models that place faster diagnostic tools closer to the patient. The FDA’s TEMPO pilot, launched in December 2025, supports this shift by allowing eligible digital health technologies for chronic conditions to enter the market under enforcement discretion while real-world performance data is collected.[1]U.S. Food and Drug Administration, “FDA Launches TEMPO, A First-of-Its-Kind Digital Health Pilot to Expand Access to Chronic Disease Technologies,” FDA, fda.govThat framework lowers practical entry barriers for biosensor developers that target lower acuity cardio-metabolic use cases. As a result, the healthcare biosensors market is seeing broader room for mid-tier manufacturers that may not have the resources required for the longest and most expensive approval routes.

Growing Diabetes and Cardiometabolic Burden

The healthcare biosensors market has a strong demand base because diabetes and cardiometabolic conditions require regular monitoring over long periods. The IDF Diabetes Atlas 2025 reported that 589 million adults were living with diabetes in 2024, and more than 4 in 10 remained unaware of their condition.[2]International Diabetes Federation, “IDF Diabetes Atlas 11th Edition 2025,” IDF, idf.orgThat large undiagnosed population supports demand for both screening and continuous management tools, especially across glucose monitoring and remote care. The WHO’s 2025 monitor also kept cardiovascular disease at the center of noncommunicable disease mortality, which supports continued use of cardiac biomarker biosensors in emergency and routine care. The healthcare biosensors market is therefore likely to see a larger share of long-term volume growth come from regions where diabetes prevalence is high and monitoring infrastructure is still expanding.

Miniaturization, AI, And Multi-Analyte Sensing Integration

The healthcare biosensors market is advancing as smaller sensor designs and software support make devices more usable outside controlled clinical settings. Flexible materials, MEMS fabrication, and on-device machine learning are improving the reliability of wearable and implantable formats. Research in 2026 highlighted that flexible piezoelectric biosensors are progressing across wearable and implantable applications, while still facing tradeoffs between flexibility and detection sensitivity.[3]J. Liang and others, “Advances in Flexible Piezoelectrics for Wearable and Implantable Medical Devices,” npj Flexible Electronics, nature.comAI integration is also addressing sensor drift by identifying accuracy changes in real time and guiding recalibration with less user input. This is widening the clinical usefulness of the healthcare biosensors market because better signal stability supports longer wear periods and stronger trust in homecare settings.

Reimbursement Expansion for Remote Monitoring Use Cases

The healthcare biosensors market is also benefiting from reimbursement policies that now support remote monitoring more directly. CMS expanded Medicare coverage for continuous glucose monitoring to include patients on basal insulin and those with problematic hypoglycemia, which widened the addressable patient pool in the United States. The 2025 Physician Fee Schedule confirmed that providers can earn USD 90-110 per patient per month through common RPM billing codes, which made biosensor programs more practical for smaller practices. A proposed CMS rule in July 2025 also pointed to competitive bidding for CGM payment rates, which may pressure supplier margins but can improve patient access if out-of-pocket costs fall. Europe is seeing a parallel effect in the healthcare biosensors market, where compliance spending is rising under IVDR and companies with stronger regulatory capacity are better placed to keep products available.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Clinical Validation and Cybersecurity Compliance | -1.2% | Global, most acute for Class C and D devices in the EU and FDA PMA-track products in the U.S. | Medium term (2-4 years) |

| Fragmented Regulatory Classification Across Device and Digital Health Pathways | -0.9% | Global, particularly EU, U.S., and APAC divergence | Long term (≥ 4 years) |

| Sensor Drift, Bioreceptor Stability, and Calibration Burden | -0.7% | Global, with greatest operational impact in homecare and chronic monitoring settings | Medium term (2-4 years) |

| Interoperability Gaps Between Sensors, Apps, and Payer Workflows | -0.5% | North America and EU, with emerging pressure in digitizing APAC and Middle East and Africa markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Clinical Validation and Cybersecurity Compliance

The healthcare biosensors market faces higher cost pressure as validation standards become more demanding for devices tied to therapeutic decisions and automated care pathways. The FDA’s 2025 guidance on AI-enabled device software functions added lifecycle documentation expectations for AI components, which extends work beyond first approval. Implantable products face an even steeper burden because they often require long trial periods and separate evidence packages across indications and geographies. These added costs are making it harder for mid-sized companies to keep up when compared with diversified medtech groups and well-funded startups. As a result, the healthcare biosensors market is likely to see more consolidation pressure where validation, cybersecurity, and software upkeep costs keep rising together.

Fragmented Regulatory Classification Across Device and Digital Health Pathways

The healthcare biosensors market is also constrained by the fact that medical devices, in vitro diagnostics, and digital health tools do not move through identical classification pathways across major regions. A product that fits one route in the United States may require a different evidence package or notified body process in Europe. That mismatch slows international rollout and raises the cost of entering multiple markets at the same time. It also creates an advantage for larger firms that can manage separate regulatory tracks without delaying launch plans. This means the healthcare biosensors market may continue to reward scale and regulatory specialization even when product innovation is strong across smaller developers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Wearables Anchor Revenue While Point-Of-Care Accelerates

Wearable biosensors held 58.40% of the healthcare biosensors market in 2025, which made them the largest product category by revenue. Their lead reflects strong adoption in continuous glucose monitoring, cardiac rhythm surveillance, and oxygen saturation tracking, along with higher comfort for repeated daily use. The healthcare biosensors market has favored these formats because clinicians and patients both value continuous and non-intrusive data over periodic spot testing. That preference has supported steady demand for wrist-based, patch-based, and other body-worn monitoring formats across acute and chronic care settings.

Point-of-care biosensors are projected to grow at an 11.80% CAGR through 2031, making them the fastest-moving product segment in the healthcare biosensors market. Their growth is tied to primary care expansion, pharmacy diagnostics, and the continued use of rapid testing outside large hospital laboratories. Implantable biosensors are also gaining relevance as CMS added HCPCS codes G0564 and G0565 in 2025 for 365-day implantable interstitial glucose sensors. Benchtop and laboratory biosensors are growing more slowly, while home-use devices remain closely linked to payer coverage and the availability of simple monitoring workflows.

By Technology: Electrochemical Leadership Meets Piezoelectric Expansion

Electrochemical biosensors retained 61.70% share in 2025, which kept them at the core of the healthcare biosensors industry and the broader healthcare biosensors market. Their position rests on mature manufacturing, broad clinical evidence, and established use in glucose testing, cardiac troponin assays, and infectious disease diagnostics. Research published in 2025 showed that AI-integrated electrochemical biosensors are moving toward portable autonomous diagnostics with multiplexed capability. This extends their relevance beyond traditional analytes and supports continued volume strength across institutional and decentralized testing.

Piezoelectric biosensors are forecasted to grow at a 12.40% CAGR through 2031, making them the fastest-growing technology in the healthcare biosensors market. Their appeal comes from label-free mass-based detection, which supports pathogen detection and cancer biomarker screening without the same need for electroactive reagents. A 2025 review documented expanding medical diagnostic applications for piezoelectric chemosensors and biosensors across cancer and infectious disease testing. Optical, thermal, and nanomechanical platforms remain smaller, while compliance requirements for homecare devices continue to shape design choices across the healthcare biosensors industry.

By Application: Clinical Diagnostics Holds the Largest Base While Chronic Disease Management Grows Faster

Clinical diagnostics accounted for 54.90% of the healthcare biosensors market size in 2025, which kept it as the leading application area. This demand came from glucose monitoring, cardiac marker assays, infectious disease rapid tests, and pregnancy diagnostics that remain widely used across hospitals and outpatient settings. The healthcare biosensors market therefore continues to expand into indications that previously depended on more invasive or less accessible testing methods.

Chronic disease management is projected to grow at a 12.90% CAGR through 2031 in the healthcare biosensors market. Growth is being supported by the rising diabetic population, the spread of CGM platforms, and care models that reward continuous monitoring over episodic intervention. Health and wellness monitoring is also growing, although clinical diagnostics and chronic disease management still account for the main revenue center of the healthcare biosensors market.

By End-User: Hospitals Lead Revenue While Homecare Changes the Growth Pattern

Hospitals and clinics held 48.20% of the healthcare biosensors market share in 2025, which made them the largest end-user group by revenue. Their lead came from central procurement, stricter accuracy requirements, and the use of biosensors in intensive care, emergency care, and surgical monitoring. The healthcare biosensors market still relies on hospitals as the primary channel for higher-value clinical-grade devices. Large provider networks are also placing more weight on total cost of ownership, service support, and integration with existing records systems when selecting suppliers.

Homecare settings are expected to grow at an 11.60% CAGR through 2031, which makes them the fastest-growing end-user segment in the healthcare biosensors market. CMS reimbursement for remote patient monitoring is helping this shift because clinicians can now support home-based biosensor use through a recurring payment model. Diagnostic laboratories remain stable as they add sensor-and-software offerings, while research institutions, pharmaceutical companies, and military health programs stay smaller but active users. The end-user pattern shows that the healthcare biosensors industry is moving toward more distributed monitoring without removing the hospital’s central role in high-acuity applications.

Geography Analysis

North America held 42.50% share in 2025, which made it the largest regional contributor to the healthcare biosensors market. The region benefits from high CGM use, a developed remote patient monitoring framework, and strong private insurance support for continuous monitoring devices. The healthcare biosensors market also gains from North America’s concentration of research and product development activity in major U.S. innovation centers. Canada and Mexico remain smaller, but coverage expansion and stronger health program support are widening the regional base.

Europe was the second-largest regional block in the healthcare biosensors market, but it is operating under a more complex regulatory setting. Germany and the United Kingdom remain the main revenue hubs, while Europe is also serving as an early launch market for differentiated products such as Abbott’s Libre Duo and Roche’s Elecsys pTau217. This means the healthcare biosensors market in Europe combines strong clinical demand with higher regulatory barriers that can favor better-prepared manufacturers.

Asia-Pacific is projected to grow at a 12.30% CAGR through 2031, which makes it the fastest-growing region in the healthcare biosensors market. China remains the largest APAC country market, and Abbott’s FreeStyle Libre holds a 35% share of China’s CGM segment, while Sinocare has listings in 15 provincial insurance plans. The healthcare biosensors market in Asia-Pacific is being supported by China’s large diabetes management base and by India’s expanding device manufacturing capacity. Japan also adds momentum through its strong healthcare technology base. The Middle East and Africa and South America remain smaller, but infrastructure spending is improving the case for affordable point-of-care and community screening products.

Competitive Landscape

The healthcare biosensors market is moderately concentrated at the top, with Abbott, Dexcom, Medtronic, Roche, and Siemens Healthineers shaping a large share of global clinical-grade revenue, while the field remains fragmented below that leading tier. The main competitive pattern in 2026 is platform depth rather than sensor hardware alone. Suppliers are trying to link sensors, dosing systems, analytics, and clinical reporting tools into one workflow that is difficult to replace once installed. The healthcare biosensors market is therefore rewarding companies that can combine clinical evidence, manufacturing reach, and software continuity.

A second competitive theme in the healthcare biosensors market is the push into new diagnostic categories where biomarker sensing still has limited commercial penetration. Medtronic’s MiniMed Go Smart MDI clearance in January 2026 is another example because it strengthened a connected monitoring and insulin management setup that can hold users within one clinical workflow. This keeps switching costs higher and raises the value of data continuity, provider familiarity, and payer alignment.

White space in the healthcare biosensors market remains strongest in multiplexed sensing, non-diabetes implantables, and AI-led signal interpretation. Multiplexed platforms still have clear laboratory promise, but large-scale commercial use remains limited across routine care settings. Non-diabetes implantables also have fewer commercial entrants despite evidence that longer duration monitoring could support cardiac and perioperative use cases. AI-based drift correction and signal interpretation are becoming more important because they improve long-term reliability and help suppliers differentiate when base sensor performance starts to converge. For that reason, the healthcare biosensors market still leaves room for newer companies that can solve practical problems in accuracy, wear duration, and care integration rather than only introducing a new form factor.

Healthcare Biosensors Industry Leaders

Abbott Laboratories

DexCom, Inc.

F. Hoffmann-La Roche Ltd

Medtronic plc

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Roche received CE Mark for Elecsys pTau217, the first validated blood-based biosensor test for amyloid pathology as an indicator of Alzheimer's disease, developed with Eli Lilly. The test uses the same cutoffs across primary and secondary care settings, enabling broad deployment from community clinics to tertiary centers.

- May 2026: MiniMed announced plans to collaborate with Abbott on dual glucose-ketone sensors designed to integrate with its smart dosing systems, expanding an existing CGM supply relationship with Abbott. MiniMed reported the expansion on its first earnings call since going public in March 2026, signaling continued platform investment in multi-analyte sensing.

- March 2026: MiniMed received CE Mark for the MiniMed 780G system integrated with Abbott's Instinct sensor, expanding the closed-loop insulin delivery option to European markets with a commercial launch planned for summer 2026.

Global Healthcare Biosensors Market Report Scope

According to the report’s scope, the healthcare biosensors market refers to the global industry focused on the development, manufacturing, and commercialization of biosensor devices that use biological recognition elements and transducers to detect, measure, and monitor physiological or biochemical parameters for healthcare applications. These biosensors are widely used in disease diagnosis, glucose monitoring, patient monitoring, point-of-care testing, and personalized healthcare management.

The healthcare biosensors market is segmented into product type, technology, application, end-user, and geography. By product type, the market is segmented into Wearable biosensors, implantable biosensors, point-of-care biosensors, benchtop/laboratory biosensors, and home-use biosensors. By application, the market is segmented into clinical diagnostics, health and wellness monitoring, chronic disease management / therapeutic monitoring, and other applications. The clinical diagnostic application is further segmented into glucose monitoring, infectious disease testing, cardiac marker testing, pregnancy and fertility testing, and other clinical diagnostics. By end-user, the market is segmented into hospitals and clinics, homecare settings, diagnostic laboratories, and other end-users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Wearable Biosensors |

| Implantable Biosensors |

| Point-of-Care Biosensors |

| Benchtop/Laboratory Biosensors |

| Home-Use Biosensors |

| Electrochemical Biosensors |

| Optical Biosensors |

| Piezoelectric Biosensors |

| Thermal Biosensors |

| Nanomechanical Biosensors |

| Clinical Diagnostics | Glucose Monitoring |

| Infectious Disease Testing | |

| Cardiac Marker Testing | |

| Pregnancy and Fertility Testing | |

| Other Clinical Diagnostics | |

| Health and Wellness Monitoring | |

| Chronic Disease Management / Therapeutic Monitoring | |

| Other Applications |

| Hospitals and Clinics |

| Homecare Settings |

| Diagnostic Laboratories |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Wearable Biosensors | |

| Implantable Biosensors | ||

| Point-of-Care Biosensors | ||

| Benchtop/Laboratory Biosensors | ||

| Home-Use Biosensors | ||

| By Technology | Electrochemical Biosensors | |

| Optical Biosensors | ||

| Piezoelectric Biosensors | ||

| Thermal Biosensors | ||

| Nanomechanical Biosensors | ||

| By Application | Clinical Diagnostics | Glucose Monitoring |

| Infectious Disease Testing | ||

| Cardiac Marker Testing | ||

| Pregnancy and Fertility Testing | ||

| Other Clinical Diagnostics | ||

| Health and Wellness Monitoring | ||

| Chronic Disease Management / Therapeutic Monitoring | ||

| Other Applications | ||

| By End-User | Hospitals and Clinics | |

| Homecare Settings | ||

| Diagnostic Laboratories | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the healthcare biosensors market by 2031?

The healthcare biosensors market is projected to reach USD 34.11 billion by 2031, rising from USD 19.72 billion in 2025 to USD 21.5 1 billion in 2026 at a 9.67% CAGR.

Which product category leads revenue generation?

Wearable biosensors led with 58.40% share in 2025 because they support continuous and non-intrusive monitoring across glucose, cardiac, and oxygen tracking.

Which application area is growing the fastest?

Chronic disease management is forecasted to grow at a 12.90% CAGR through 2031, supported by diabetes prevalence, CGM expansion, and continuous care models.

Which region currently leads global demand?

North America held 42.50% share in 2025 due to high CGM use, reimbursement support, and strong product development activity.

Page last updated on: