HDI Printed Circuit Board Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

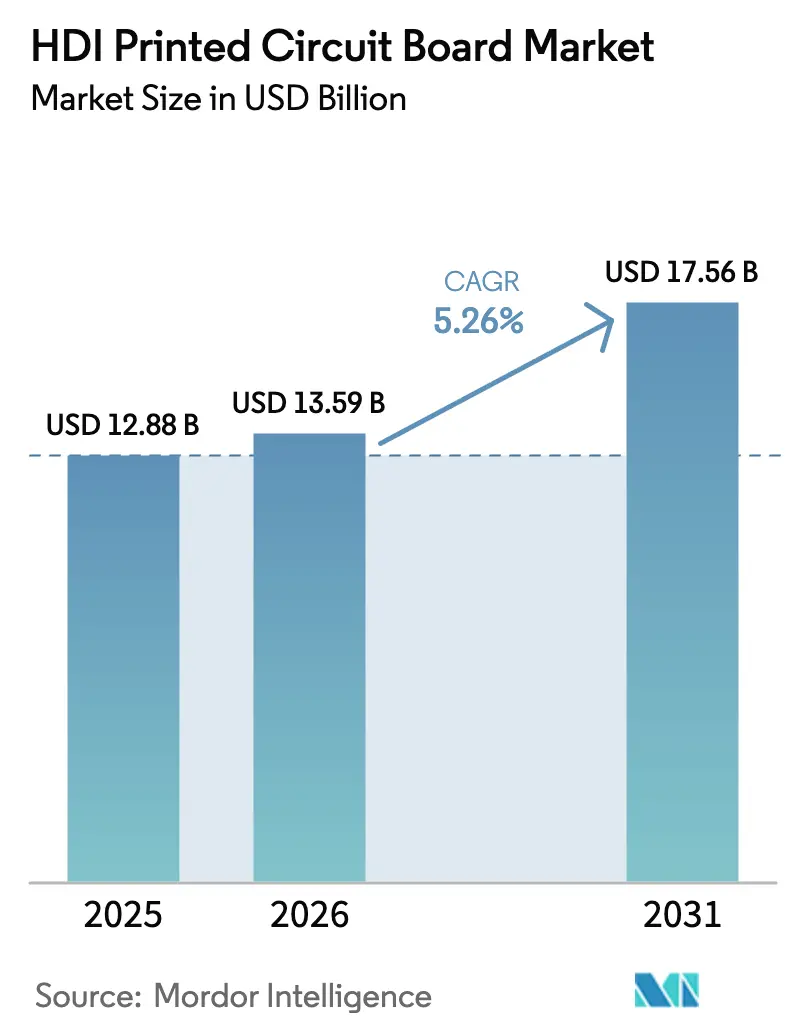

| Market Size (2026) | USD 13.59 Billion |

| Market Size (2031) | USD 17.56 Billion |

| Growth Rate (2026 - 2031) | 5.26% CAGR |

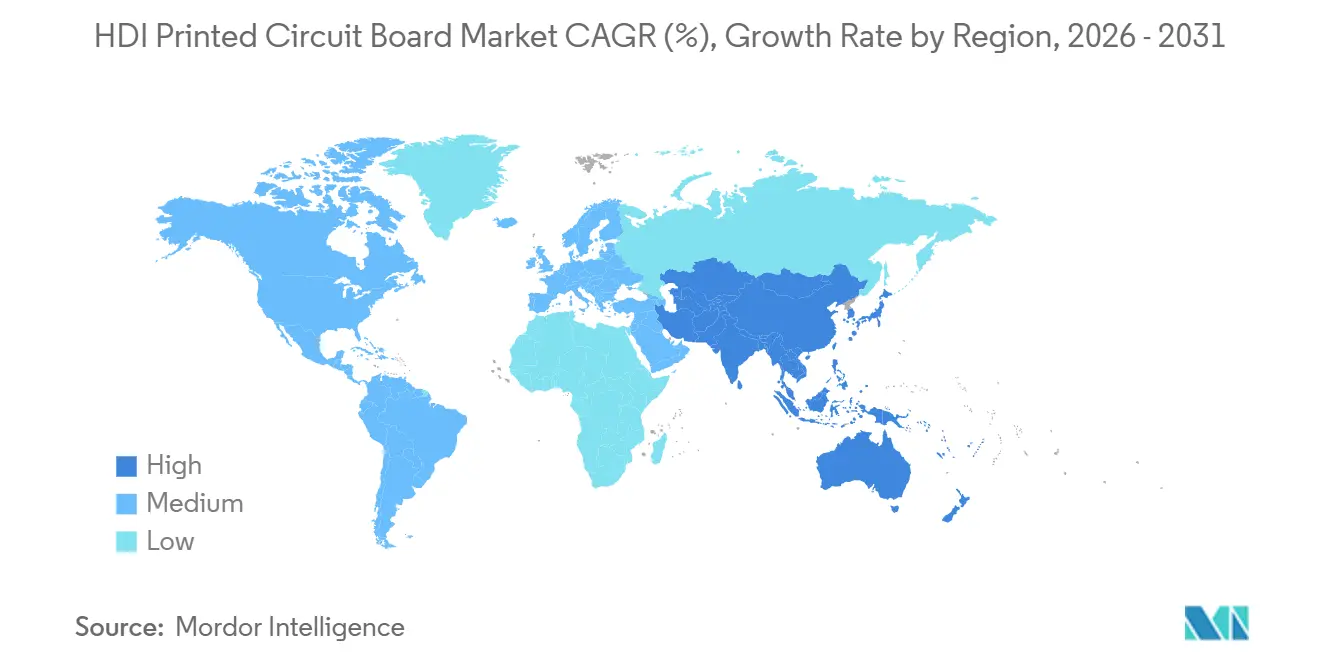

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HDI Printed Circuit Board Market Analysis by Mordor Intelligence

The HDI Printed Circuit Board Market size is projected to expand from USD 12.88 billion in 2025 and USD 13.59 billion in 2026 to USD 17.56 billion by 2031, registering a CAGR of 5.26% between 2026 to 2031.

The growth trajectory mirrors the industry’s shift from cost-driven volume production toward ultra-precision substrates that support sub-5 µm line widths, any-layer microvia architectures, and glass-core packaging for high-speed computing. Rising demand for 5G infrastructure, electric-vehicle electronics, and AI server boards is expanding premium laminate consumption, elevating average layer counts, and compressing product life cycles. Fabricators that master stacked microvia yield, resin smear removal, and dielectric thickness control are capturing disproportionate share as OEMs prioritize signal integrity over material cost. Meanwhile, regulatory pressure on PFAS compounds and volatile copper pricing inject margin risk, prompting vertical integration and raw-material hedging among leading Asian suppliers. Competitive dynamics are therefore tilting toward players that blend proprietary process recipes with captive laminate capacity, while regional newcomers in India and Vietnam vie for mid-tier programs under localization incentives.

Key Report Takeaways

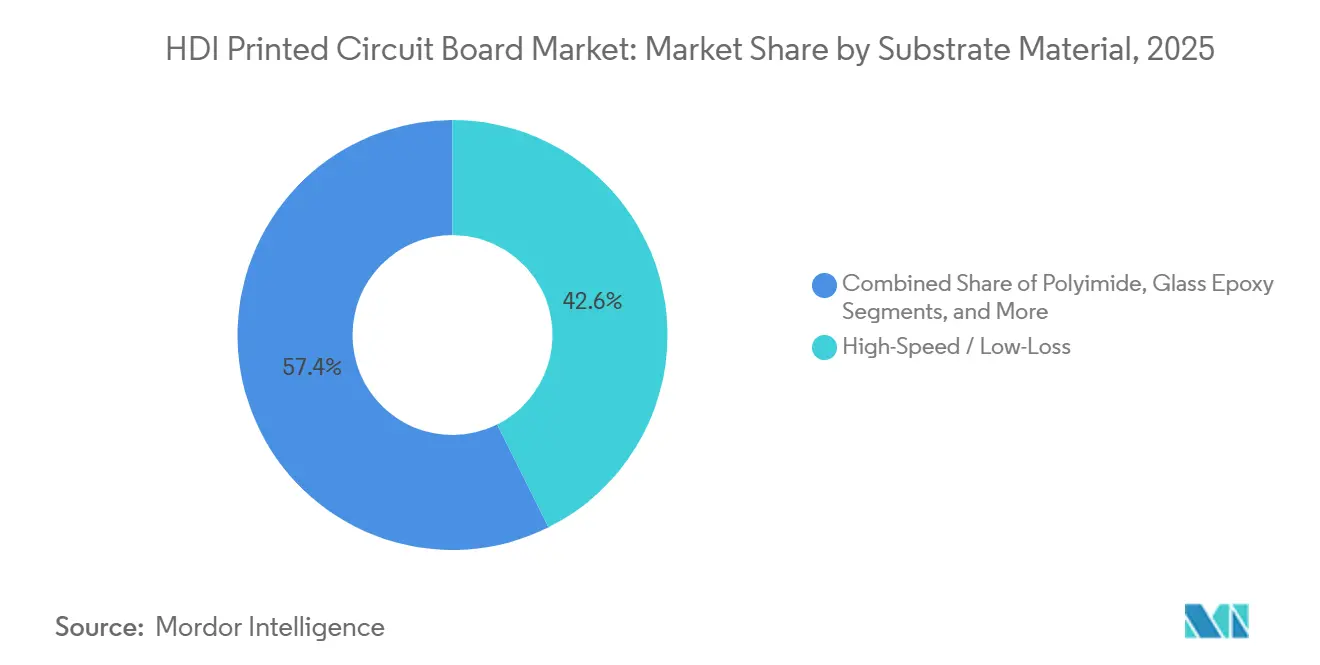

- By substrate material, high-speed / low-loss laminates commanded 42.63% of HDI Printed Circuit Board Market share in 2025 and is forecast to expand at 5.82% through 2031.

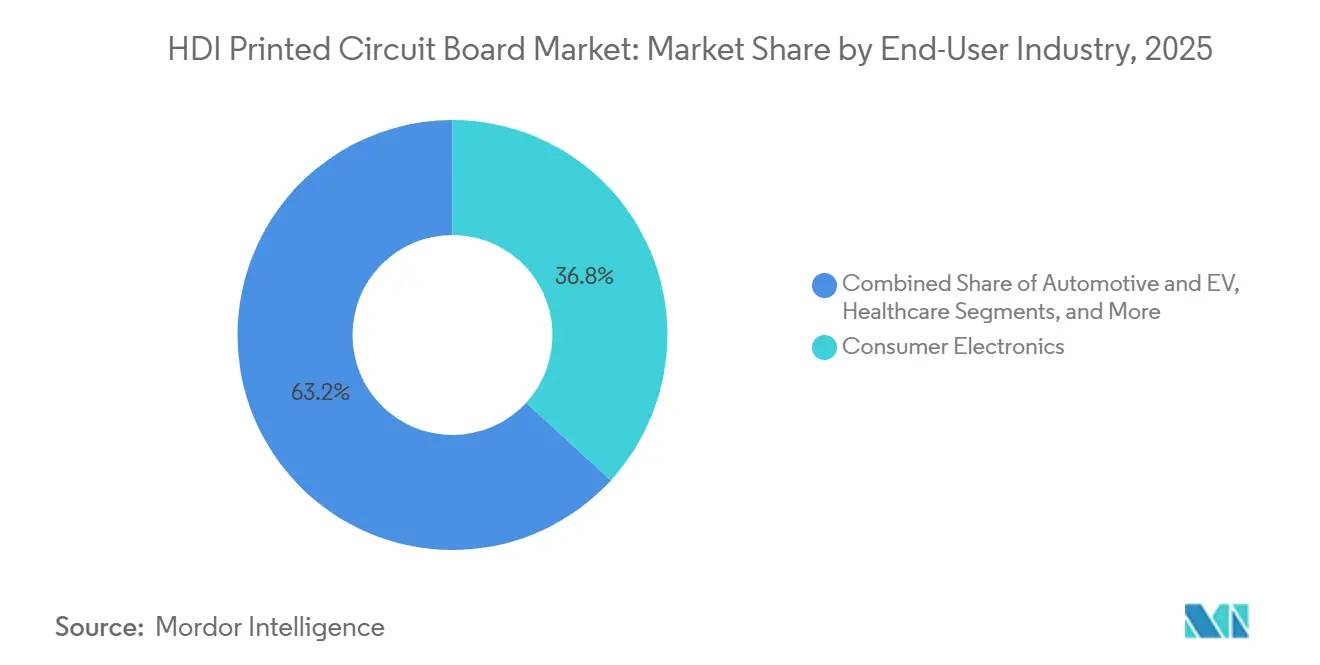

- By end-user industry, consumer electronics commanded 36.82% of market share, whereas telecommunications equipment is projected to grow at a 6.11% CAGR through 2031, outpacing all other segments.

- By geography, Asia-Pacific retained 81.74% production share in 2025 and is forecast to expand at 6.46% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HDI Printed Circuit Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of 5G Smartphones and Wearables | +1.2% | Global, with APAC core and spillover to North America and Europe | Medium term (2-4 years) |

| Growing Adoption of ADAS in Electric Vehicles | +0.9% | Global, with early gains in China, United States, and Germany | Long term (≥4 years) |

| Rising Demand for High-Performance Computing and Data Centers | +1.4% | North America and APAC core, spillover to Europe | Short term (≤2 years) |

| Emergence of Glass Core Substrates Enabling Sub-5/5 µm SLP | +0.7% | APAC core (Taiwan, Japan), with pilot deployments in United States | Long term (≥4 years) |

| Localization Incentives for Substrate Production in India and Vietnam | +0.5% | India and Vietnam, with regional spillover to Southeast Asia | Medium term (2-4 years) |

| Mini-LED Backlighting Driving Stacked Microvia HDI | +0.6% | APAC core (China, Taiwan, South Korea), spillover to Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of 5G Smartphones and Wearables

Flagship smartphones now incorporate 10-14 microvia layers to route mmWave antenna arrays and multi-camera modules inside sub-8 mm chassis, boosting PCB content value by 18% year over year in 2025.[1]Samsung Electro-Mechanics, “2024 Annual Report,” samsungsem.com Apple’s iPhone 15 Pro and Samsung’s Galaxy S24 Ultra adopted any-layer HDI to mitigate crosstalk while sustaining 3 Gbps peak throughput. Wearable devices impose even tighter design windows, driving demand for flex and rigid-flex variants with bend radii below 2 mm. Mid-tier Android handsets are transitioning from 4-layer to 8-layer boards as MediaTek and Qualcomm chipsets require robust power-delivery networks. These design shifts compel fabricators to install laser-drill systems capable of 25 µm capture pads and presses that hold ±15 µm registration, widening the addressable HDI Printed Circuit Board Market.

Growing Adoption of ADAS in Electric Vehicles

Electric-vehicle platforms embed up to 30 electronic control units, with lidar, radar, and camera modules relying on automotive-grade HDI verified to AEC-Q200. Tesla’s Hardware 4 computer employs a 14-layer board linking redundant processors via 10 Gbps Ethernet, while General Motors’ Ultifi architecture consolidates domain controllers onto 12-layer polyimide substrates to endure 1,000 thermal cycles at 150 °C. Tier-1 suppliers such as Bosch and Continental are dual-sourcing boards from Vietnam and India to mitigate geopolitical exposure. The elevated reliability bar drives higher layer counts, premium resin uptake, and expanded HDI Printed Circuit Board Market opportunity across the EV supply chain.

Rising Demand for High-Performance Computing and Data Centers

Hyperscale operators are populating AI racks with NVIDIA GB200 and AMD MI300X accelerators that demand 20-layer motherboards capable of sub-1 dB/inch insertion loss at 112 Gbps PAM4 signaling. Intel’s Gaudi 3 server cards specify Rogers RO4000 or Isola TerraGreen laminates, pushing average board value per server from USD 180 in 2024 to USD 240 in 2025. Transition to DDR5 memory and PCIe Gen5 interfaces forces fabricators to tighten dielectric thickness tolerance to ±0.5 mil, rewarding suppliers that invest in fully automated impedance-control lines. The result is a sustained uplift for the HDI Printed Circuit Board Market as AI workloads proliferate across cloud and enterprise data centers.

Emergence of Glass Core Substrates Enabling Sub-5 µm SLP

Nippon Electric Glass and Intel validated glass-core substrates featuring 10 µm vias and 2 µm redistribution layers, effectively merging package and board functions. AT&S completed phase-one of the glass-core pilot, with a capacity of 50,000 units per year, targeting the high-performance computing and automotive domains. Although current yields lag FR-4 equivalents by 30 percentage points and material cost is 3× higher, coefficient-of-thermal-expansion parity with silicon promises superior warpage control in chiplet designs. Commercial adoption after 2027 could reallocate premium revenue to early movers, expanding the HDI Printed Circuit Board Market for substrate-like PCBs.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Copper and Resin Pricing | -0.8% | Global | Short term (≤2 years) |

| Supply-Chain Concentration in Taiwan and South Korea | -0.6% | Global, with acute exposure in North America and Europe | Medium term (2-4 years) |

| Yield-Loss Challenges at Sub-30 µm Any-Layer HDI | -0.5% | APAC core, with spillover to Global | Long term (≥4 years) |

| PFAS Regulations Limiting Advanced Photoresists | -0.4% | Europe and United States, with spillover to Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Copper and Resin Pricing

Copper foil and epoxy resin represent up to 50% of substrate cost, and London Metal Exchange prices fluctuated from USD 8,200 per ton in early 2024 to USD 10,400 in late 2025.[2]London Metal Exchange, “LME Copper Prices,” lme.com Epoxy resin trended 12% higher year over year in 2025 as petrochemical capacity tightened. Long-term supply contracts delay pass-through, compressing margins by up to 5 percentage points for smaller fabricators. The shift toward low-loss laminates amplifies exposure because Rogers and Isola resins cost 2-3x standard FR-4. Leading players hedge with captive laminate production, but volatility still tempers HDI Printed Circuit Board Market expansion.

Supply-Chain Concentration in Taiwan and South Korea

Taiwan and South Korea accounted for 68% of global HDI capacity in 2025, with the top 10 vendors accounting for 55% of revenue. A single geopolitical or seismic event could disrupt shipments for up to a year, given 18-month equipment lead times. North American and European OEMs are qualifying secondary sites in Southeast Asia and Eastern Europe, yet early-stage yields lag incumbents by 10-15 percentage points. High capital intensity- USD 150 million to USD 300 million per fab- slows diversification, placing a drag on HDI Printed Circuit Board Market resilience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Substrate Material: High-Speed Laminates Gain Share

High-speed / low-loss laminates secured 42.63% revenue in 2025 and are projected to grow at 5.82% through 2031, outpacing the overall HDI Printed Circuit Board Market. Rogers RO4000 and Isola TerraGreen 200 support 56 Gbps and 112 Gbps links in 5G base stations and AI backplanes, whereas FR-4 remains dominant in consumer devices due to its 50–60% cost advantage. Polyimide substrates serve the aerospace and medical implantable markets, operating at 200 °C and 100,000 bend cycles. Collectively, PTFE, ceramic-filled epoxy, and liquid-crystal polymer account for less than 8% of HDI Printed Circuit Board Market size, given processing complexity and price hurdles. Material vendors now publish insertion-loss metrics at 10 GHz, 20 GHz, and 40 GHz under IPC-4101 to standardize performance. The migration from FR-4 to advanced laminates reduces retimer IC demand, delivering system-level savings despite a 40% higher board price, and expands the HDI Printed Circuit Board Market share of premium substrates.

Demand for high-speed laminates will intensify as automotive OEMs adopt zonal architectures that consolidate domain controllers onto fewer but more complex boards. Polyimide adoption is also rising in battery-management systems, where rigid-flex designs replace wire harnesses. Material suppliers are balancing halogen-free compliance with low dielectric constants, ensuring UL 94 V-0 flame resistance without sacrificing electrical performance. These advances reinforce the trajectory of the HDI Printed Circuit Board Market toward performance-driven differentiation.

By End-User Industry: Telecommunications Accelerates

Consumer electronics absorbed 36.82% of spending in 2025, yet telecommunications and 5G infrastructure are set to grow at 6.11% CAGR through 2031, eclipsing handset growth. Base stations and small cells require IP67-rated HDI boards that operate from -40 °C to 65 °C, sustaining price premiums of up to 35%. AI servers extend computing demand, raising layer counts to 20 and boosting substrate value per server. Automotive programs are shifting from 6-layer to 12-layer boards in ADAS modules, while lidar sensor units alone require 10-layer HDI.

Healthcare players deploy HDI in pacemakers and glucose monitors using biocompatible polyimide, and aerospace contractors pay 2–3x commercial rates for MIL-PRF-55110 compliance. Open RAN adoption increases PCB content per cell site by 40-60% as radio functions disaggregate onto commercial servers. Although smartphone replacement cycles lengthen, foldable devices and AR headsets sustain multi-layer complexity, keeping the HDI Printed Circuit Board Market diversified across verticals.

Geography Analysis

Asia-Pacific’s 81.74% share of production in 2025 underscores a dense ecosystem of laminate suppliers, equipment makers, and process engineers. Taiwan’s Zhen Ding and Unimicron operate laser-drill fleets that achieve 25 µm capture pads, while South Korean players leverage vertical integration in materials to defend margins. China’s USD 40 billion PCB output relies heavily on imported low-loss resins, limiting its stake in premium applications.

Southeast Asian sites in Vietnam and Malaysia are absorbing tier-2 programs as OEMs diversify, though they mainly build 4- to 8-layer boards. India’s Production-Linked Incentive offers 4-6% rebates on incremental sales, yet deficits in clean-room infrastructure and deionized water supply delay the adoption of high-mix HDI.

North America accounted for 8.2% of production in 2025, led by TTM Technologies and Sanmina, which specialize in ITAR-compliant aerospace and defense boards. Europe’s 6.1% share is led by AT&S and Schweizer, both targeting automotive and glass-core pilot programs. The CHIPS and Science Act directs USD 52.7 billion to semiconductors but leaves PCB fabrication largely dependent on Asian capacity, keeping the HDI Printed Circuit Board Market geographically concentrated.

Competitive Landscape

The top 10 vendors controlled a considerable amount of revenue in 2025, reflecting moderate concentration within the HDI Printed Circuit Board Market. Taiwanese leaders Zhen Ding and Unimicron supply Apple and Dell, maintaining 18-24% gross margins through scale and captive laminate lines. Samsung Electro-Mechanics and LG Innotek focus on high-end smartphones and AI servers, leveraging in-house material science to differentiate.

Japanese players Ibiden and Meiko serve automotive and industrial niches that demand IPC Class 3 reliability. TTM Technologies and AT&S thrive in aerospace and medical segments where North American and European customers value traceability and engineering proximity over cost.

Glass-core substrates represent an emerging battleground, with Intel pilots and AT&S’s USD 339 million Austrian line poised for commercialization from 2027 onward.[3]AT&S AG, “AT&S Invests EUR 300 Million in Glass Core Substrate Technology,” ats.net Patent activity in stacked microvia and glass-core metallization rose 28% year over year in 2025, signaling an intellectual-property arms race. Fabricators that implement closed-loop yield analytics and machine-vision inspection at sub-30 µm geometries are winning high-speed computing programs, reinforcing a performance-driven competitive paradigm within the HDI Printed Circuit Board Market.

HDI Printed Circuit Board Industry Leaders

Zhen Ding Technology Holding Limited (ZDT)

Unimicron Technology Corp.

Compeq Manufacturing Co., Ltd.

AT&S AG

Samsung Electro-Mechanics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: AT&S completed phase-one glass-core substrate pilot capacity of 50,000 units per year in Leoben, Austria, after investing EUR 300 million (USD 339 million).

- November 2025: Samsung Electro-Mechanics announced a KRW 180 billion (USD 135 million) plan to expand any-layer HDI capacity in Busan by 30% through 2027.

- October 2025: Unimicron reported TWD 28.4 billion (USD 880 million) Q3 revenue and confirmed glass-core qualification for 2027 production.

- September 2025: TTM Technologies acquired a 150,000 ft² HDI fab in Penang, Malaysia, for USD 45 million, marking its first Southeast Asian site.

- August 2025: LG Innotek earmarked KRW 200 billion (USD 150 million) to raise flex and rigid-flex capacity for foldable smartphones, starting Q2 2026.

Global HDI Printed Circuit Board Market Report Scope

The HDI Printed Circuit Board Market Report is Segmented by Substrate Material (Glass Epoxy FR-4, High-Speed / Low-Loss, Polyimide, Other Substrate Materials), End-user Industry (Consumer Electronics, Computing and Data Centers, Telecommunications and 5G, Automotive and EV, Healthcare / Medical, Aerospace and Defense, Other End-user Industries), and Geography (North America, Europe, Asia-Pacific, Rest of World). The Market Forecasts are Provided in Terms of Value (USD).

| Glass Epoxy |

| High-Speed / Low-Loss |

| Polyimide |

| Other Substrate Materials |

| Consumer Electronics |

| Computing and Data Centers |

| Telecommunications and 5G |

| Automotive and EV |

| Healthcare / Medical |

| Aerospace and Defense |

| Other End-user Industries |

| North America | United States |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Taiwan | |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Rest of World |

| By Substrate Material | Glass Epoxy | |

| High-Speed / Low-Loss | ||

| Polyimide | ||

| Other Substrate Materials | ||

| By End-user Industry | Consumer Electronics | |

| Computing and Data Centers | ||

| Telecommunications and 5G | ||

| Automotive and EV | ||

| Healthcare / Medical | ||

| Aerospace and Defense | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Taiwan | ||

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Rest of World | ||

Key Questions Answered in the Report

What is the projected revenue for the HDI Printed Circuit Board (PCB) Market in 2031?

The HDI Printed Circuit Board (PCB) Market is forecast to reach USD 17.56 billion by 2031.

Which substrate material segment is growing fastest?

High-speed / low-loss laminates are expanding at 5.82% CAGR through 2031 due to 5G and AI server demand.

Why is telecommunications driving new HDI demand?

5G base stations and Open RAN deployments require IP67-rated boards with premium laminates, fueling a 6.11% CAGR in the segment.

How concentrated is global HDI production geographically?

Asia-Pacific commands more than 80% of output, with Taiwan and South Korea alone accounting for most sub-30 µm any-layer capacity.

What emerging technology may redefine HDI designs after 2027?

Glass-core substrates enabling sub-5 µm line-widths promise package-like PCBs for chiplet architectures.

Page last updated on: