HBM4 Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

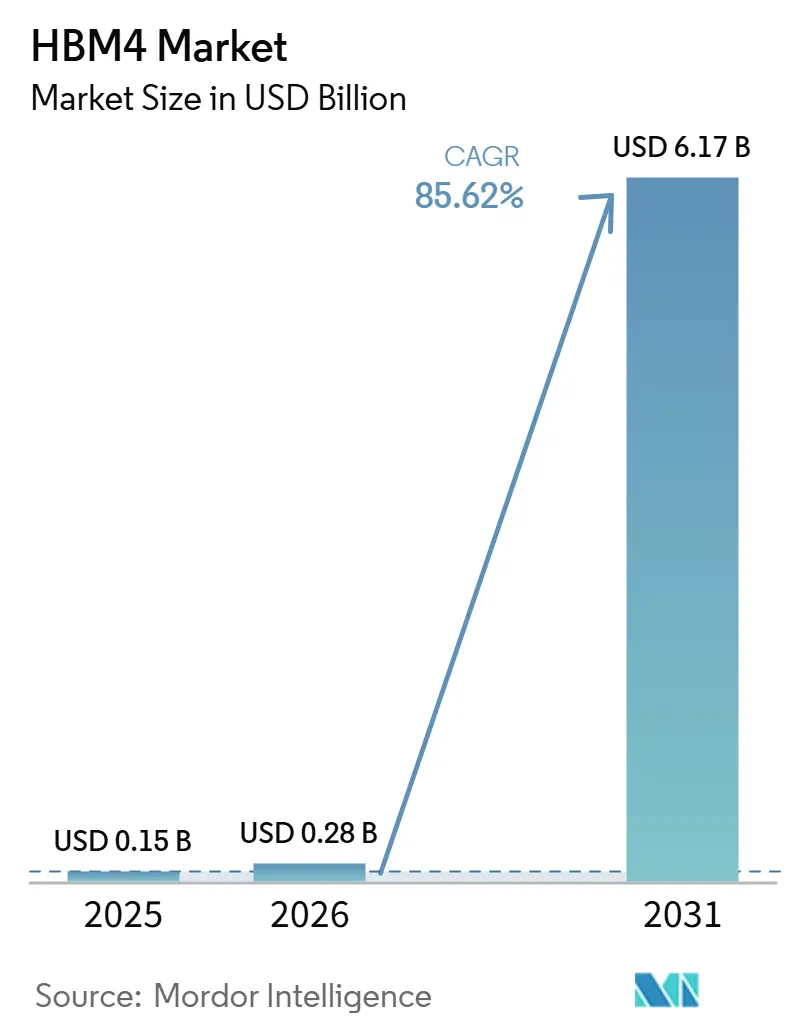

| Market Size (2026) | USD 0.28 Billion |

| Market Size (2031) | USD 6.17 Billion |

| Growth Rate (2026 - 2031) | 85.62% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HBM4 Market Analysis by Mordor Intelligence

The HBM4 market size is expected to increase from USD 0.15 billion in 2025 to USD 0.28 billion in 2026 and reach USD 6.17 billion by 2031, growing at a CAGR of 85.80% over 2026-2031. The HBM4 market is moving on the back of a clear shift in AI system design, where memory bandwidth has become a direct limit on training and inference performance. In the HBM4 market, qualification timing now acts as a launch gate for entire accelerator platforms, so a change in platform specification can delay revenue recognition across suppliers, packaging partners, and system builders. The HBM4 market also reflects a supply chain that is highly responsive to AI infrastructure spending, with procurement centered in a small number of hyperscale cloud and AI operators that shape allocation priorities across the value chain. The HBM4 market remains structurally concentrated, with a limited supplier base, heavy reliance on advanced packaging capacity, and a strong dependence on hybrid bonding and high-yield stack production for higher-capacity products. That leaves the HBM4 market exposed to export compliance rules, packaging bottlenecks, and yield constraints even as platform launches, sovereign AI buildouts, and custom silicon programs continue to widen the opportunity set.

Key Report Takeaways

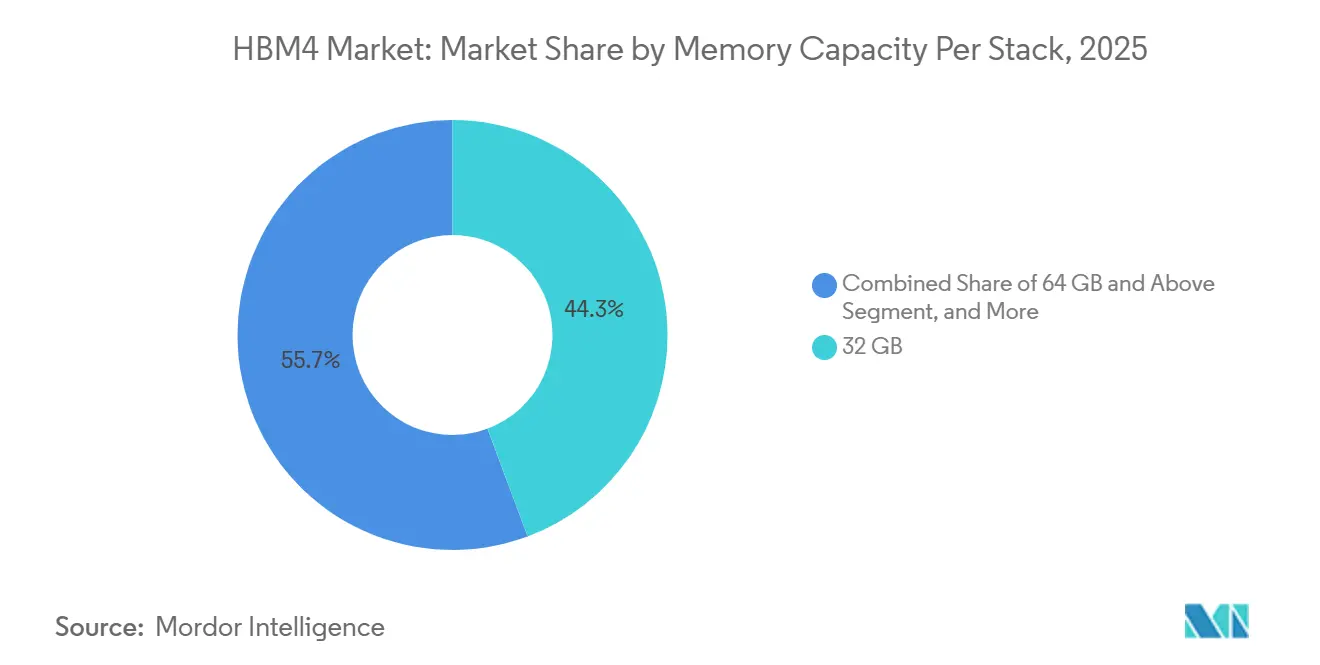

- By memory capacity per stack, 32 GB led with 44.31% of the HBM4 market in 2025, while 64 GB and above is projected to expand at a 86.78% CAGR through 2031.

- By processor interface, GPU held 76.83% of the HBM4 market share in 2025, while AI Accelerator and ASIC are projected to grow at a CAGR at 86.71% through 2031.

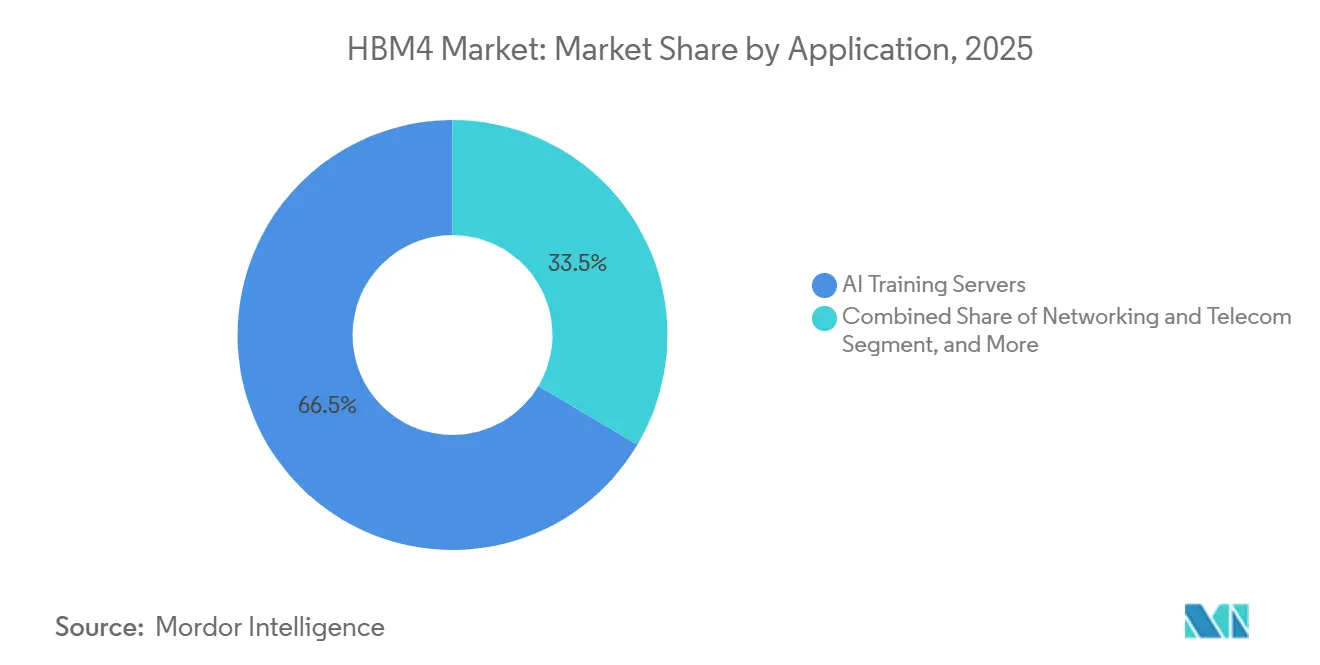

- By application, AI Training Servers accounted for 66.48% of the HBM4 market size in 2025, while AI Inference Servers are projected to advance at a 86.63% CAGR through 2031.

- By end use industry, Cloud Service Providers held 71.29% of the HBM4 market share in 2025 and are also projected to grow at a CAGR at 86.67% through 2031.

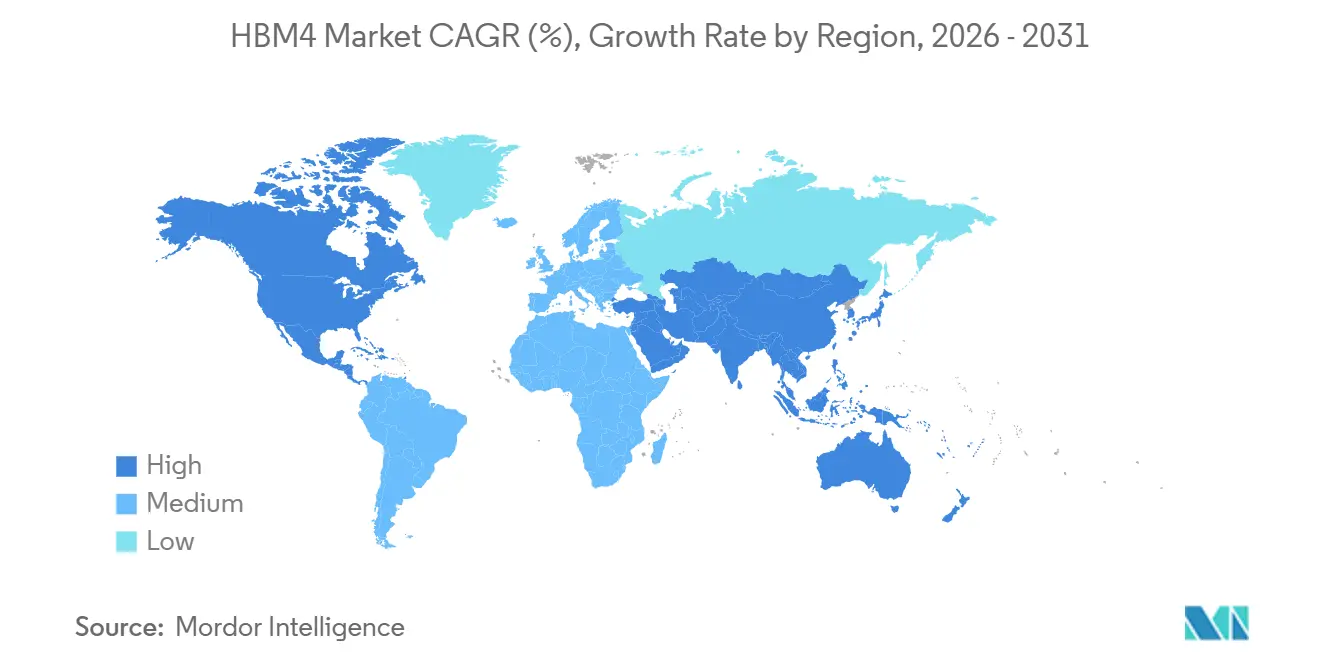

- By geography, North America accounted for 48.33% of the HBM4 market in 2025, while Asia-Pacific is projected to expand at a 86.79% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HBM4 Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating AI Accelerator Bandwidth Demand | +25.0% | Global | Short term (≤ 2 years) |

| HBM4 Qualification Tied to Next-Gen GPU Launch Cycles | +18.0% | Global | Short term (≤ 2 years) |

| Hybrid Bonding and Advanced Packaging Upscaling | +14.0% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Rising Memory Intensity in Sovereign AI Data Centers | +10.0% | Global | Medium term (2-4 years) |

| Defense and High-Reliability Compute Adoption | +5.0% | North America and Europe | Long term (≥ 4 years) |

| Thermal and Power-Efficiency Advantage Versus GDDR and HBM3E | +4.0% | Global | Short term (≤ 2 years), Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating AI Accelerator Bandwidth Demand

The HBM4 market is being driven by AI model scaling, which now requires far more memory bandwidth within a practical power envelope than prior generations could deliver. Samsung shipped commercial HBM4 in February 2026 with a processing speed of 11.7 Gbps and up to 3.3 TB/s of bandwidth per stack, marking a major performance step over HBM3E and giving system designers a direct path to denser AI memory subsystems.[1]Samsung Electronics, “Samsung Ships Industry-First Commercial HBM4 With Ultimate Performance for AI Computing,” Samsung Global Newsroom, news.samsung.com Micron also positioned HBM4 above 11.0 Gbps with a 2,048-pin bus and more than 2.8 TB/s per stack, indicating that the HBM4 market is scaling around a shared bandwidth target rather than isolated vendor claims. JEDEC formalized the 2,048-bit interface and 32 independent channels per stack in April 2025, which made the bandwidth jump durable at the standards level and reduced uncertainty for long-cycle platform developers. That matters because training clusters, long-context inference, and mixture-of-experts workloads are using memory bandwidth more aggressively, so the HBM4 market is benefiting from a performance need that sits closer to the architecture than to a short product cycle. As a result, buyers are not treating HBM4 as an optional premium part, but as a practical requirement for top-tier AI systems that need sustained throughput at scale.

HBM4 Qualification Tied to Next-Gen GPU Launch Cycles

The HBM4 market behaves like a launch-synchronized ecosystem, because qualification status determines whether a supplier can participate in a new accelerator generation at volume. When platform requirements exceeded 11 Gbps during the 2025 qualification cycle, suppliers had to resubmit samples and adjust their timelines, underscoring how a single specification change could reset commercial windows across the HBM4 market. Samsung met that higher threshold in mass production at 11.7 Gbps, while Micron's current HBM4 product also exceeded 11.0 Gbps, narrowing the field to suppliers that could meet stricter platform demands on schedule. SK hynix completed HBM4 development in September 2025, achieving performance above JEDEC's 8 Gbps baseline, giving it an early qualification position and strengthening its role in first-wave allocation. The HBM4 market, therefore, rewards suppliers that secure qualification early, because qualification can lock in multi-year revenue visibility before the broader supply base reaches the same yield and speed levels. It also means customers increasingly plan memory procurement alongside platform milestones, rather than treating memory sourcing as a later-stage component decision.

Hybrid Bonding And Advanced Packaging Upscaling

The HBM4 market is also being shaped by a packaging transition, because the move from 1,024-bit HBM3E to 2,048-bit HBM4 sharply increases interconnect density and pushes the stack toward finer-pitch bonding methods. TSMC's CoWoS and SoIC capabilities sit at the center of that transition, making advanced packaging a co-determinant of HBM4 supply rather than a backend step after memory fabrication. JEDEC's HBM4 standard supports up to 16-high configurations and up to 64 GB per stack, but that roadmap only becomes commercial when bonding, interposer integration, and base-die logic scale together with acceptable yield. Samsung's in-house base-die approach and Micron's product configuration show that the HBM4 market is increasingly integrating memory design, logic integration, and packaging strategy into a single competitive decision set. This underscores the importance of manufacturing execution, because any delay in packaging scale-up can keep end demand from being recognized as revenue even when customer interest remains strong. It also explains why capacity expansion in bonding and interposer lines carries the same strategic weight as front-end memory wafer capacity.

Rising Memory Intensity in Sovereign AI Data Centers

The HBM4 market is gaining a second demand center from sovereign AI programs that are building nationally controlled compute capacity outside the normal hyperscale buying cycle. Deutsche Telekom opened Germany's first AI factory in Munich in February 2026, demonstrating that European sovereign AI investment had moved from planning to live deployment. SoftBank Group also announced in May 2026 that it and Sesterce will develop a 1 GW AI data center in Bosquel, France, which reinforced the scale at which sovereign and strategic AI infrastructure is now being commissioned in Europe. The HBM4 market benefits from this pattern because sovereign buyers are working to policy and deployment schedules that are often less sensitive to short-term component pricing than commercial operators. South Korea's domestic buildout plans further support that direction, as the country combines a leading role in production with a large future demand base for AI compute systems. This creates a more geographically distributed demand structure for the HBM4 market, while still keeping the highest-value procurement tied to advanced AI infrastructure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Advanced Packaging Capacity | -6.0% | Global | Short term (≤ 2 years), Medium term (2-4 years) |

| TSV Yield and Stacking Complexity at Higher Layer Counts | -4.5% | APAC core, spill-over to Global | Short term (≤ 2 years), Medium term (2-4 years) |

| Qualification Risk and Design-In Delays | -3.0% | Global | Short term (≤ 2 years) |

| Export Controls and Supply Chain Fragmentation | -2.5% | Global | Medium term (2-4 years), Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Advanced Packaging Capacity

The HBM4 market is most directly constrained by the availability of advanced packaging, especially CoWoS-class interposer integration and hybrid bonding capacity. TSMC's own materials show how central CoWoS has become to high-performance packaging, and the draft makes clear that booking queues have stretched well beyond normal planning windows for accelerator programs. That bottleneck matters because the HBM4 market does not scale through memory wafer starts alone, since base dies, silicon interposers, bonding tools, backend assembly, and final test all have to expand together. Micron's March 2026 acquisition of PSMC's Tongluo site was one direct response, because it added manufacturing infrastructure and strengthened its production footprint in Taiwan. Even so, additions at this stage usually take time to influence usable throughput, which means near-term customer demand can still outrun the part of the chain that converts dies into deployable HBM4 stacks. The result is that smaller AI chip customers face delayed integration windows even when their end applications remain attractive and commercially ready.

TSV Yield and Stacking Complexity at Higher Layer Counts

The HBM4 market also faces a technical restraint in stack yield, as taller stacks amplify the effect of any single-die defect across the entire assembly. JEDEC's April 2025 standard supports 16-high configurations and up to 64 GB per stack, but the draft ties that roadmap to much thinner dies and tighter package constraints than 12-high production needs. That makes warpage, bonding precision, and defect management more important for the HBM4 market, especially as the industry pushes from 12-high launch products toward 16-high commercial volume. Samsung's current commercial range and Micron's 36 GB production device still sit within the more manageable early ramp zone, which shows that near-term supply is centered on configurations with a more stable yield profile. The practical effect is that the highest-density segment can show strong forecast growth in the HBM4 market while remaining physically limited by how fast learning curves improve in stacking and bonding. This is why demand for 64 GB and above products can build faster than commercial shipments during the first years of the forecast period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Memory Capacity Per Stack: Higher-Density Stacks Hinge on Yield Maturation

The 32 GB tier accounted for 44.31% of the HBM4 market in 2025, making it the largest commercial capacity segment at the start of the forecast period. Its position reflected the balance between usable yield, bandwidth gains, and launch timing, since 12-high stacks offered a practical path into early commercial deployment without waiting for 16-high yield stability. Samsung's first commercial HBM4 shipments in February 2026 were built around 24 GB to 36 GB configurations on its 1c DRAM process, confirming that the HBM4 market opened with products concentrated around capacity points ready for high-volume qualification. Micron's HBM4 product for current platform demand also ships as a 36 GB 12-high stack, which further shows that the initial HBM4 market favors configurations with a lower production learning burden than taller stacks.[2]Micron Technology, “HBM4,” Micron, micron.com This capacity band, therefore, anchors current revenue because it is close enough to the performance frontier to win AI allocations, while still fitting the manufacturing envelope suppliers can support at scale.

The 64 GB and above segment is projected to grow at an 86.78% CAGR through 2031, and that pace is tied directly to the commercial readiness of 16-high stacking. JEDEC supports up to 64 GB per stack in a 16-high structure, which means the roadmap is defined, but the HBM4 market still depends on thinner dies and tighter process control before that roadmap translates into broad shipment volume. SK hynix presented a 48 GB 16-layer HBM4 device in early 2026, which places the 48 GB tier in a bridge position between current 12-high volume ramps and higher-density future products. Smaller 16 GB and 24 GB offerings remain relevant for networking, telecom, and edge AI workloads where bandwidth needs are lower and cost discipline matters more. The 48 GB tier is likely to benefit as tooling broadens and customers want more memory per package before the full 64 GB class reaches steady commercial yield. That leaves the HBM4 market with a clear density ladder, where current revenue is led by practical launch capacities and future upside sits in taller stacks that are still moving through the yield curve.

By Processor Interface: GPU Dominates but Custom Silicon Restructures Demand Structure

GPU-attached products accounted for 76.83% of processor interface revenue in 2025, making GPU the dominant interface in the HBM4 market at launch. That share reflected the scale of the existing accelerator ecosystem and the way platform transitions in AI compute pull memory demand into concentrated, high-volume procurement waves. The HBM4 market remains tied closely to GPU programs because commercial qualification, allocation priority, and system-level design all begin with the highest-volume accelerator platforms. At the same time, the interface mix already shows that memory suppliers are preparing for a broader demand structure than a pure GPU-led model. CPU-attached products continue to serve scientific simulation and high-performance compute workloads, while FPGA demand remains relevant in specialized signal processing and routing environments.

AI Accelerator and ASIC are projected to grow at an 86.71% CAGR through 2031, making it the fastest-growing processor interface segment in the HBM4 market. This rise reflects hyperscaler efforts to use custom silicon to reduce dependence on standard GPU pricing and to tune systems more closely to inference economics. The HBM4 market becomes more strategically complex under this shift, as custom ASIC programs require base-die and controller alignment earlier in the design cycle than standard GPU programs typically do. Siemens EDA stated in April 2026 that HBM4 controller architecture breaks backward compatibility with HBM3 and HBM3E, so non-GPU developers face full controller redesign rather than a simple upgrade path. That extends design-in timelines, but it also increases the value of suppliers that can support earlier technical engagement and more tailored memory integration. Over time, this will make the HBM4 market less dependent on one interface even if GPU remains the near-term revenue anchor.

By Application: Training Anchors Volume but Inference Commands the Growth Inflection

AI Training Servers accounted for 66.48% of application revenue in 2025, which kept training as the largest use case in the HBM4 market. That lead reflected the straightforward economics of training clusters, where sustained memory bandwidth utilization makes higher-bandwidth memory easier to procure. Training systems also benefit from concentrated deployment cycles, which help suppliers allocate early HBM4 volume into a smaller number of large installations. This is why the HBM4 market first gained traction in environments where memory bandwidth is already recognized as a hard performance limit. HPC servers remain a stable adjacent application because they value memory proximity and deterministic throughput, while networking and telecom continue to play a role in high-throughput routing and emerging AI-driven network functions.

AI Inference Servers are projected to grow at an 86.63% CAGR through 2031, which makes inference the strongest growth application in the HBM4 market, even though it started from a smaller base. That shift reflects how long-context models and mixture-of-experts architectures are making inference increasingly memory-bandwidth-bound rather than compute-bound. The HBM4 market, therefore, benefits from a widening deployment case, where memory performance improves the economics of serving large models, not just training them. Automotive and edge AI remain a longer-horizon application set because the power-efficiency gain over HBM3E is relevant, but packaging, qualification, and environmental reliability rules extend adoption cycles. Networking and telecom demand also benefits from lower-latency memory access, though those deployments remain more selective than hyperscale AI server rollouts. The application mix shows that the HBM4 market is expanding from a training-led base toward a broader operating model where inference becomes the main growth trigger.

By End Use Industry: Cloud Service Providers Set The Tempo For Every Other Segment

Cloud Service Providers held 71.29% of the HBM4 market share in 2025, which made them the decisive end-user group for allocation, platform timing, and supplier visibility. Their lead is reinforced by the fact that the same segment is projected to grow at an 86.67% CAGR through 2031, so the HBM4 market remains most concentrated in areas with the deepest AI capital spending. This concentration matters because hyperscalers not only buy the largest volumes, but also influence which memory configurations get priority qualification and packaging capacity. In practice, that means the HBM4 market is paced by a small number of operators whose deployment schedules shape the economics of the entire supply chain. It also means other customer groups often enter the queue after the cloud segment has already secured the earliest and best-specified supply.

Enterprise IT is becoming increasingly relevant as regulated sectors build private AI inference capacity, where public cloud is not the preferred option. Telecommunications demand remains linked to AI-based network slicing, core optimization, and traffic management in 5G and planned 6G environments. Automotive demand is tied to future edge compute needs, but adoption moves more slowly because thermal, reliability, and validation requirements are stricter than those in data centers. Aerospace and defense represent an emerging path for the HBM4 market because power efficiency matters in airborne, satellite, and other constrained compute platforms. These smaller end-use categories do not currently match hyperscaler volumes, but they widen the addressable demand base and improve long-term diversification. The end-use structure therefore shows a market led by cloud operators today, with the next layers of demand forming around private AI, networks, and mission-critical compute.

Geography Analysis

North America accounted for 48.33% of the HBM4 market in 2025, making it the largest regional revenue contributor at the start of the forecast period. That position reflected the concentration of hyperscale cloud operators, the central role of U.S. accelerator platforms, and the region's influence on allocation priorities across the HBM4 market. The region also shapes trade behavior, because BIS export controls introduced under ECCN 3A090 in December 2024 brought advanced HBM products into a tighter compliance framework. BIS issued further enforcement guidance in May 2026, which clarified that license requirements also apply based on the headquarters status of certain entities, regardless of transaction location.[3]Bureau of Industry and Security, “Guidance Regarding Enforcement of License Requirements for Advanced Computing Items for Entities Headquartered in Country Group D:5 and Macau,” U.S. Department of Commerce, media.bis.gov Canada is also adding support to the regional demand base through investments in cloud and AI infrastructure, which helps broaden North American pull beyond the United States.

Asia-Pacific is projected to expand at a 86.79% CAGR through 2031, making it the fastest-growing geography in the HBM4 market. The region is unique because it combines the largest supply role with rising domestic demand, especially in South Korea and Taiwan. South Korea hosts SK hynix and Samsung Electronics, while Taiwan anchors advanced packaging through TSMC and now also carries added importance through Micron's Tongluo acquisition. South Korea's large AI data center plans strengthen the region's demand profile, because a major producer is also preparing to absorb more HBM4-equipped compute domestically. This dual role gives Asia-Pacific a structurally different position in the HBM4 market than other regions, since supply expansion and consumption growth are reinforcing each other within the same geography.

Europe started from a smaller base in 2025, but the HBM4 market is gaining strategic weight there as sovereign AI programs move into active deployment. Deutsche Telekom's Munich AI factory and SoftBank Group's 1 GW project in France show that large-scale AI infrastructure is now being built with institutional and strategic backing. South America remained early in adoption during 2025 and 2026, while the Middle East and Africa moved faster through sovereign AI investment and large planned data center capacity. That leaves the HBM4 market geographically concentrated today, but with a wider future demand map that is being shaped by policy-led compute programs and not only commercial cloud expansion.

Competitive Landscape

The HBM4 market operates as a tight supply group, with SK hynix, Samsung Electronics, and Micron Technology as the only commercially qualified memory suppliers entering 2026. The HBM4 market is therefore concentrated before packaging partners, equipment providers, and system companies are even considered, because memory production is limited to 3 suppliers. SK hynix led 2026 shipment share in the draft, followed by Samsung and Micron, which shows that competitive position is closely linked to qualification timing, scale readiness, and access to major platform programs. This keeps pricing power, allocation control, and roadmap influence in a narrow part of the value chain, even as the broader ecosystem continues to expand.

Competitive strategy inside the HBM4 market already differs sharply by supplier. Samsung took a vertically integrated route, beginning commercial HBM4 shipments in February 2026 and pairing that launch with a 4 nm logic base-die approach that supports tighter internal coordination between memory and foundry operations. SK hynix completed HBM4 development in September 2025 and later aligned with TSMC on HBM4E base dies, which shows a partnership-led strategy built around packaging and advanced logic collaboration. Micron began mass production shipments for current HBM4 demand and strengthened its footprint through the Tongluo acquisition in March 2026, which points to a capacity and geographic hedging approach. These moves show that the HBM4 market is not competing on a single dimension, because memory design, logic integration, packaging access, and site strategy all influence future share. They also explain why early shipment rank does not settle long-term competitive outcomes, since supply scale and platform fit still depend on execution in adjacent layers.

A second layer of rivalry sits around the HBM4 market in packaging, design enablement, testing, and equipment. TSMC holds a critical position because advanced packaging throughput decides how quickly qualified memory reaches deployed AI systems.[4]TSMC, “CoWoS Technology,” TSMC 3DFabric, 3dfabric.tsmc.com Siemens EDA identified a full controller redesign requirement for HBM4 relative to HBM3 and HBM3E, which raises the role of design tools and interface support in non-GPU adoption. Micron's acquisition, Samsung's commercial launch, and SK hynix's development lead are examples of strategic moves that show how tightly the HBM4 market links supplier competition to decisions across manufacturing, packaging, and customer enablement. As a result, competitive advantage depends not only on memory performance, but also on how effectively each company coordinates the broader ecosystem that makes HBM4 deployable at scale.

HBM4 Industry Leaders

Hewlett Packard Enterprise Company

Samsung Electronics Co., Ltd.

SK hynix Inc.

Micron Technology, Inc.

NVIDIA Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Micron Technology's HBM4 sales also surpassed USD 1 billion, with the company planning to raise its HBM market share into the 20% range by year-end 2026 and advancing its Tongluo, Taiwan packaging facility completion from late 2027 to mid-2027 to accelerate capacity contribution.

- May 2026: Micron Technology began mass shipments of HBM4 for NVIDIA's Vera Rubin AI platform, featuring a 36 GB 12-high stack with greater than 2.8 TB/s of bandwidth per stack and a wider 2,048-pin bus interface operating at 11.0 Gbps or higher.

- March 2026: Micron completed its USD 1.8 billion acquisition of PSMC's Tongluo (P5) fab in Taiwan, securing front-end manufacturing capacity and establishing PSMC as an advanced packaging partner, with the transaction materially expanding Micron's HBM production infrastructure and geographic footprint.

- September 2025: SK hynix completed the world's first HBM4 development and announced mass production readiness on September 12, 2025, with its HBM4 device exceeding JEDEC's 8 Gbps operating standard at over 10 Gbps using the 1bnm process and Advanced MR-MUF packaging and achieving an expected AI service performance improvement of up to 69% versus HBM3E.

Global HBM4 Market Report Scope

HBM4 refers to the fourth generation of High Bandwidth Memory, a 3D-stacked DRAM technology designed to deliver high data transfer rates, improved bandwidth, and better energy efficiency for data-intensive applications. The scope includes its use in applications such as artificial intelligence, high-performance computing, graphics processing, data centers, and advanced networking systems.

The HBM4 Market Report is Segmented by Memory Capacity Per Stack (16 GB, 24 GB, 32 GB, 48 GB, and 64 GB and Above), Processor Interface (GPU, CPU, AI Accelerator and ASIC, FPGA, and Other Processor Interfaces), Application (AI Training Servers, AI Inference Servers, High-Performance Computing (HPC) Servers, Networking and Telecom, Automotive and Edge AI, Other Applications), End Use Industry (Cloud Service Providers, Enterprise IT, Telecommunications, Automotive, Aerospace and Defense, and Other End Use Industries), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| 16 GB |

| 24 GB |

| 32 GB |

| 48 GB |

| 64 GB and Above |

| GPU |

| CPU |

| AI Accelerator and ASIC |

| FPGA |

| Other Processor Interfaces |

| AI Training Servers |

| AI Inference Servers |

| High-Performance Computing (HPC) Servers |

| Networking and Telecom |

| Automotive and Edge AI |

| Other Applications |

| Cloud Service Providers |

| Enterprise IT |

| Telecommunications |

| Automotive |

| Aerospace and Defense |

| Other End Use Industries |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| India | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Memory Capacity Per Stack | 16 GB | |

| 24 GB | ||

| 32 GB | ||

| 48 GB | ||

| 64 GB and Above | ||

| By Processor Interface | GPU | |

| CPU | ||

| AI Accelerator and ASIC | ||

| FPGA | ||

| Other Processor Interfaces | ||

| By Application | AI Training Servers | |

| AI Inference Servers | ||

| High-Performance Computing (HPC) Servers | ||

| Networking and Telecom | ||

| Automotive and Edge AI | ||

| Other Applications | ||

| By End Use Industry | Cloud Service Providers | |

| Enterprise IT | ||

| Telecommunications | ||

| Automotive | ||

| Aerospace and Defense | ||

| Other End Use Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the HBM4 market size through 2031?

The HBM4 market size is USD 0.28 billion in 2026 and is forecast to reach USD 6.17 billion by 2031, with an 85.80% CAGR over 2026-2031.

Which application leads HBM4 demand today?

AI Training Servers led in 2025 with 66.48% of application revenue, showing that current demand is still anchored in bandwidth-intensive model training.

Which application is growing the fastest?

AI Inference Servers are projected to expand at an 86.63% CAGR through 2031, reflecting rising memory intensity in large-model serving workloads.

Which buyer group has the strongest influence on adoption?

Cloud Service Providers had 71.29% of end-use revenue in 2025 and are also the fastest-growing end-use segment at an 86.67% CAGR, so they set allocation and deployment pace.

Why is advanced packaging so important for HBM4 adoption?

HBM4 supply depends on more than memory wafer output, because interposer integration, hybrid bonding, backend assembly, and test capacity all need to scale together.

Which region is expanding the fastest?

Asia-Pacific is projected to grow at an 86.79% CAGR through 2031, supported by its role as the main production hub and a fast-rising center for AI infrastructure demand.

Page last updated on: