HBM Through-Silicon Via (TSV) Technology and Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

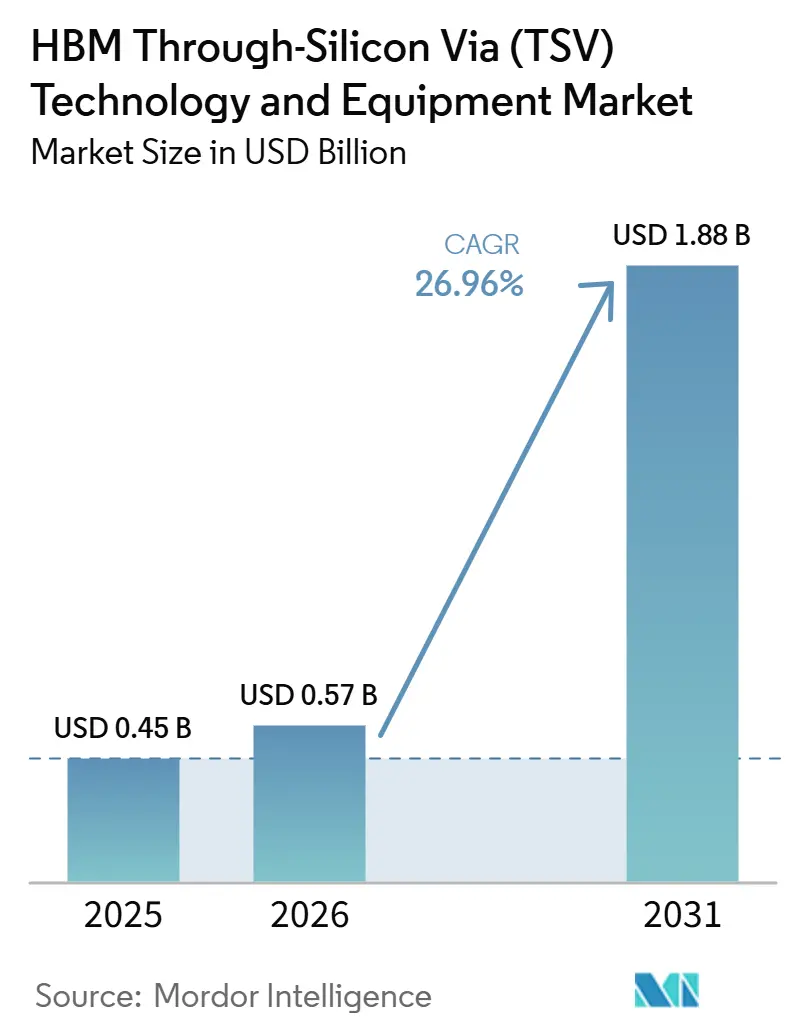

| Market Size (2026) | USD 0.57 Billion |

| Market Size (2031) | USD 1.88 Billion |

| Growth Rate (2026 - 2031) | 26.96% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HBM Through-Silicon Via (TSV) Technology and Equipment Market Analysis by Mordor Intelligence

The HBM Through-Silicon Via (TSV) technology and equipment market size is expected to increase from USD 0.45 billion in 2025 to USD 0.57 billion in 2026 and reach USD 1.88 billion by 2031, growing at a CAGR of 26.96% over 2026-2031. The HBM Through-Silicon Via (TSV) technology and equipment market is moving into a phase where packaging capability matters as much as memory design, because higher stack counts, tighter pitch, and faster data transfer now depend on stable vertical interconnect performance. Demand is being pulled by AI hardware programs that need more bandwidth per package, while supply is being shaped by a small set of memory manufacturers, equipment vendors, and packaging specialists that already control the hardest process steps. The HBM Through-Silicon Via (TSV) technology and equipment market is also seeing spending stay concentrated in tools, since capacity expansion still depends on etch, bonding, plating, thinning, inspection, and process control systems before materials can scale at the same pace. Competitive positioning is increasingly tied to whether vendors can support both current thermocompression flows and the next wave of hybrid bonding adoption, because customers do not want stranded tool investments when stack architectures change. This keeps the HBM Through-Silicon Via (TSV) technology and equipment market open to growth, but it also keeps execution risk high, especially where capex, qualification time, and bonding roadmaps must stay aligned across the same production line.

Key Report Takeaways

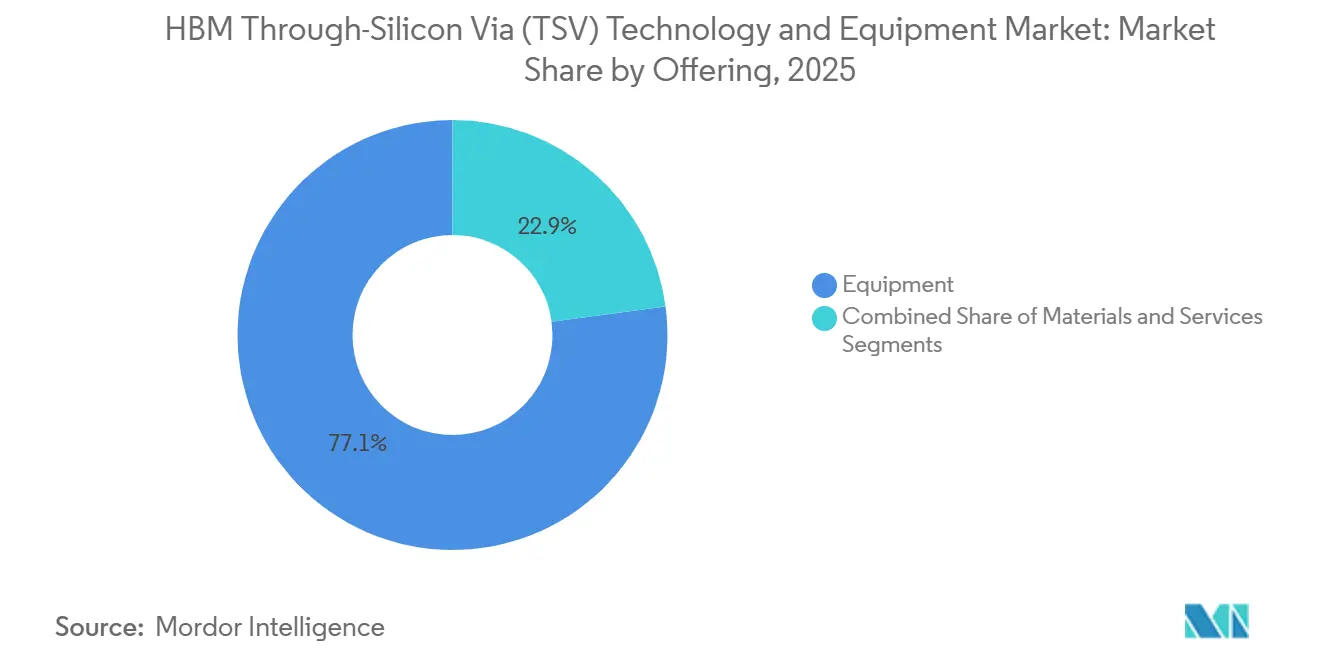

- By offering, equipment held 77.12% of revenue in 2025, while materials are projected to expand at a 27.56% CAGR through 2031.

- By TSV process type, via-middle held 62.52% of revenue in 2025, while via-middle is also projected to expand at a 27.51% CAGR through 2031.

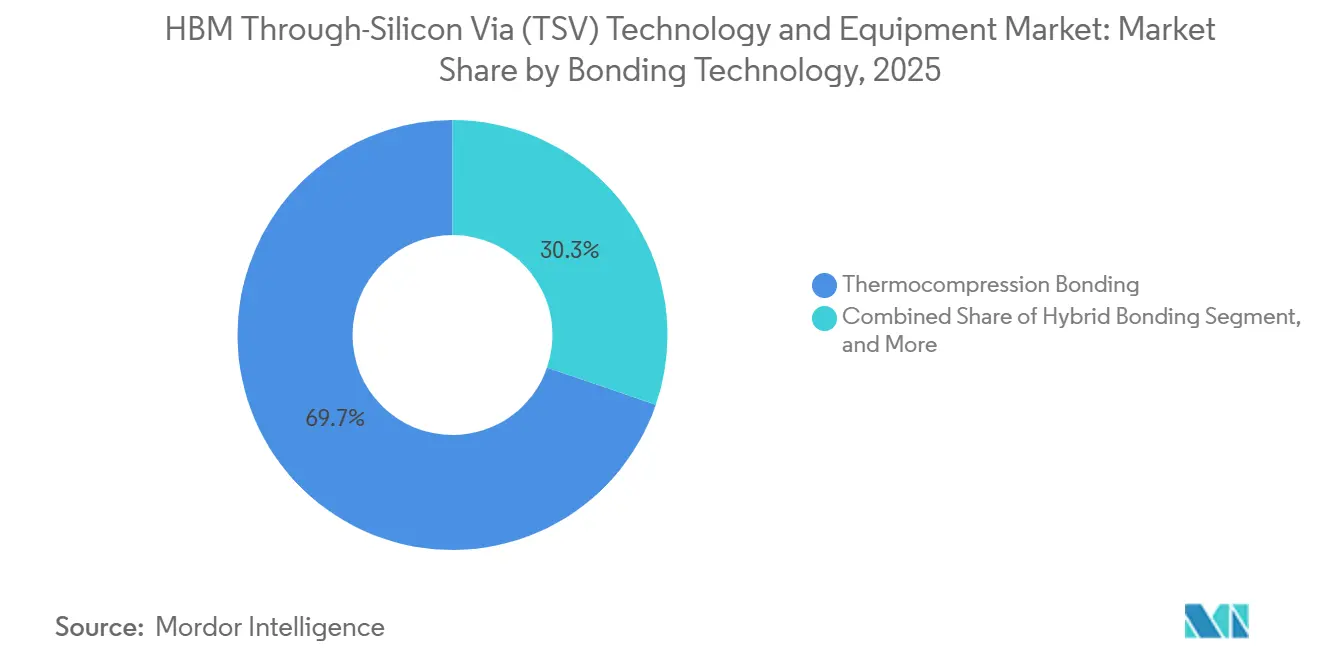

- By bonding technology, thermocompression bonding held 69.74% of revenue in 2025, while hybrid bonding is projected to expand at a 27.76% CAGR through 2031.

- By application, high bandwidth memory held 47.96% of revenue in 2025, while AI accelerators are projected to expand at a 28.16% CAGR through 2031.

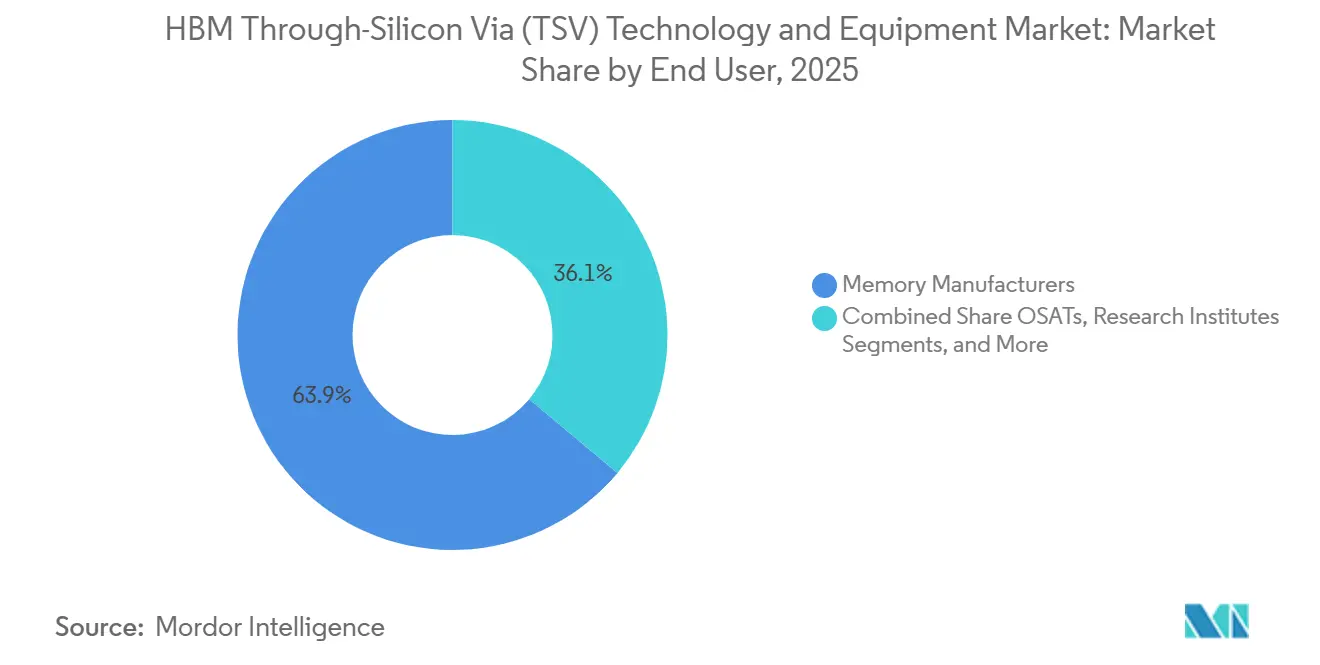

- By end user, memory manufacturers held 63.91% of revenue in 2025, while foundries are projected to expand at a 27.71% CAGR through 2031.

- By wafer size, 300 mm held 94.23% of revenue in 2025, while 300 mm is also projected to expand at a 27.53% CAGR through 2031.

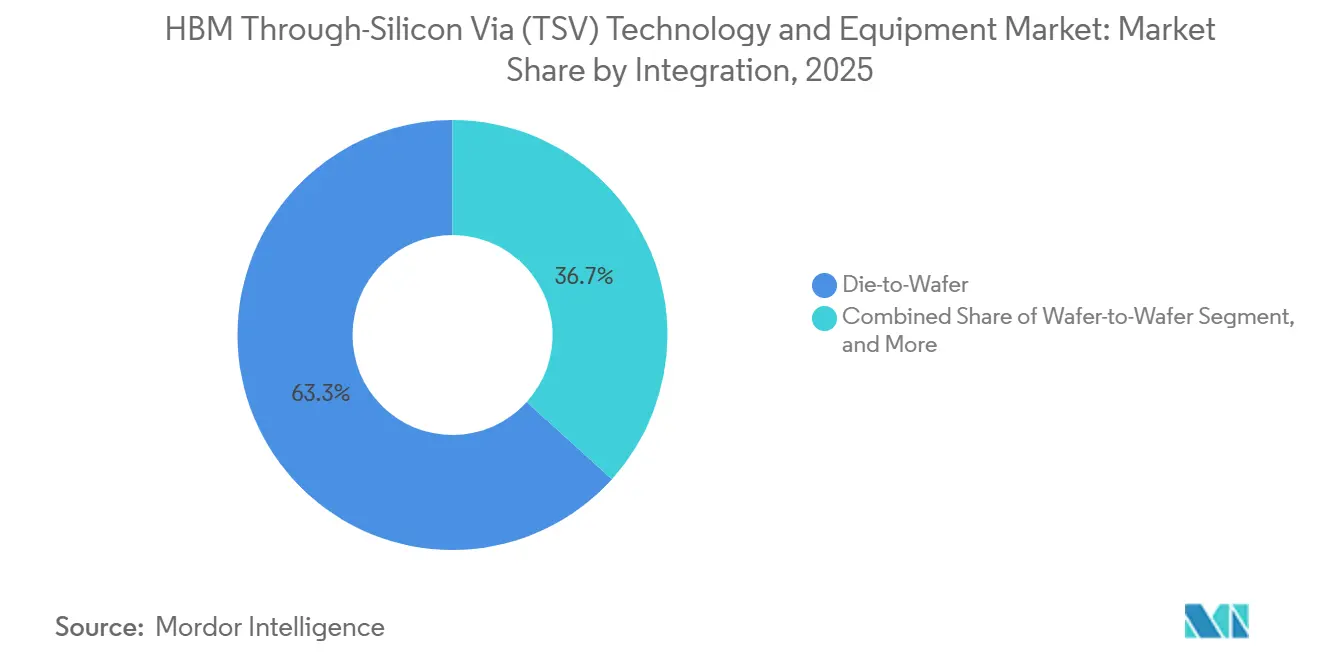

- By integration, die-to-wafer held 63.29% of revenue in 2025, while die-to-die is projected to expand at a 27.56% CAGR through 2031.

- By geography, Asia-Pacific held 77.83% of the HBM Through-Silicon Via (TSV) technology and equipment market share in 2025, while Asia-Pacific is projected to expand at a 27.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HBM Through-Silicon Via (TSV) Technology and Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI Accelerator HBM Stack Density Expansion | +8.5% | Global, strongest in North America demand centers and Asia-Pacific supply hubs | Short term (≤ 2 years) |

| Transition From Microbump to Hybrid Bonding in HBM4 and Beyond | +5.2% | Asia-Pacific core, with spillover into Taiwan and Europe | Medium term (2-4 years) |

| Advanced Packaging Capacity Additions by Foundries and OSATs | +4.8% | Asia-Pacific core, secondary in North America | Short term (≤ 2 years) to Medium term (2-4 years) |

| Domestic Semiconductor Subsidies for Advanced Packaging Buildouts | +3.1% | North America, Asia-Pacific, Europe | Medium term (2-4 years) |

| Yield Learning Curves in High-Aspect-Ratio TSV Etch and Fill | +2.4% | Global, concentrated in South Korea, Taiwan, and the United States | Medium term (2-4 years) to Long term (≥ 4 years) |

| Real-Time Metrology and In-Line Process Control Adoption | +1.8% | Global, with early gains in South Korea and the United States | Short term (≤ 2 years) to Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI Accelerator HBM Stack Density Expansion

Every major AI compute program now depends on HBM, so TSV performance has become a direct supply constraint for advanced accelerator packages. The HBM4 roadmap targets 12-16 Gbps per pin, 1.5-2.0 TB/s bandwidth per stack, and up to 128 GB through 16-layer stacking, which keeps pressure on via-middle integration, etch control, and stacking yield. Samsung Electronics confirmed in June 2026 that it had shipped commercial HBM4 memory, which shows that the next production cycle has already moved into live customer supply.[1]Samsung Electronics Co., Ltd., “Samsung Ships Industry-First Commercial HBM4 With Ultimate Performance for AI Computing,” Samsung Global Newsroom, news.samsung.com As stack height rises, the HBM Through-Silicon Via (TSV) technology and equipment market must support thinner dies, tighter alignment, cleaner copper fill, and more repeatable bonding windows across each layer. That is why capacity spending remains front-loaded into tools, because a missed yield target at the TSV or bonding stage can slow the output of the full memory stack rather than a single process step. The result is that the HBM Through-Silicon Via (TSV) technology and equipment market is growing in line with AI demand, but it is doing so under harder manufacturing conditions than earlier HBM generations.

Transition From Microbump to Hybrid Bonding in HBM4 and Beyond

The shift from microbump-based interconnects to hybrid bonding is changing how vendors plan the next equipment cycle, even before full volume adoption becomes standard. A 2025 review in Electronics reported that Cu-Cu hybrid bonding can lower joint thermal resistance by 20% versus MR-MUF while also improving I/O resistance and capacitance at finer pitch.[2]Misato Matsumoto et al., “Thermal Issues Related to Hybrid Bonding of 3D-Stacked High Bandwidth Memory, A Comprehensive Review,” Electronics, mdpi.com Samsung Electronics stated in June 2026 that it plans to use hybrid copper bonding from 16-layer HBM4E and then move further with HBM5, which gives the equipment base a clear direction even if the timing remains staggered by customer program. Imec and EV Group also demonstrated wafer-to-wafer hybrid bonding at 200 nm Cu interconnect pitch in May 2026, which confirms that the technology path is advancing toward very fine interconnect density. For the HBM Through-Silicon Via (TSV) technology and equipment market, this creates a two-speed demand pattern where thermocompression tools remain essential now, while hybrid bonding tools, surface preparation systems, and related materials move through qualification and line planning. That overlap matters because suppliers that win early qualification slots can influence future process standards long before high-volume ramps start.

Advanced Packaging Capacity Additions by Foundries and OSATs

Advanced packaging expansion is widening the customer base for the HBM Through-Silicon Via (TSV) technology and equipment market beyond the traditional group of memory manufacturers. Applied Materials stated in June 2026 that it expects its packaging revenue to grow more than 50% to over USD 2 billion in 2026, after more than tripling between 2020 and 2024, which signals that customers across the packaging chain are raising spending at the same time. The U.S. CHIPS packaging program and SK hynix’s Indiana project show that new buildouts are no longer limited to the existing East Asian production base.[3]National Institute of Standards and Technology, “U.S. Department of Commerce Announces USD 1.4 Billion in Final Awards to Support the Next Generation of U.S. Semiconductor Advanced Packaging,” NIST, nist.gov This matters because foundries and OSATs are taking a larger role in advanced package assembly, interconnect integration, and process ownership around heterogeneous compute designs. As that role expands, the HBM Through-Silicon Via (TSV) technology and equipment market gains a broader set of buyers for etch, bonding, metrology, and process support tools. It also means future procurement cycles will be shaped by more varied customer requirements, since memory makers optimize for stack yield while foundries and OSATs must also support mixed die, chiplet, and package-level integration models.

Domestic Semiconductor Subsidies for Advanced Packaging Buildouts

Public funding has become a direct support mechanism for the HBM Through-Silicon Via (TSV) technology and equipment market because it lowers the cost of building packaging capacity that would otherwise be difficult to justify on private economics alone. The U.S. Department of Commerce finalized USD 1.4 billion in CHIPS National Advanced Packaging Manufacturing Program awards in January 2025, including USD 1.1 billion for Natcast and USD 300 million for Absolics, Applied Materials, and Arizona State University. The same program framework also included support of up to USD 458 million for SK hynix’s Indiana advanced packaging project, which ties public funding directly to future HBM packaging capability. South Korea’s Ministry of Trade, Industry and Energy launched its 2026 advanced packaging infrastructure program with KRW 49.5 billion (USD32.81 million) in support for TSV, redistribution layer, and interposer capability upgrades, which reinforces the production base where HBM output is already concentrated. These programs matter because they do not just fund buildings, they also shape the pace of equipment orders, vendor eligibility, process localization, and the order in which new capacity becomes commercially useful. In practical terms, the HBM Through-Silicon Via (TSV) technology and equipment market benefits when state-backed packaging plans accelerate tool demand before end-market volumes fully catch up.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex for End-to-End TSV Toolchains | -4.2% | Global, most acute in North America and Europe where greenfield packaging builds remain early stage | Short term (≤ 2 years) to Medium term (2-4 years) |

| Thermal Stress and Keep-Out Zone Design Constraints | -2.8% | Global, most severe in high-density via arrays above 10:1 aspect ratio | Medium term (2-4 years) |

| Yield Loss Risk in High-Density Via Fill and Reveal Steps | -2.1% | Global, concentrated in South Korea and Taiwan where HBM volume is highest | Short term (≤ 2 years) |

| Tool Qualification Complexity Across Multi-Vendor HBM Supply Chains | -1.5% | Global, highest in multi-source HBM supply agreements | Medium term (2-4 years) to Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex for End-To-End TSV Toolchains

The HBM Through-Silicon Via (TSV) technology and equipment market remains difficult to enter because an HBM-grade line needs a full set of advanced tools rather than a single bottleneck machine. Applied Materials’ June 2026 launch covered TSV reveal, copper plating, dielectric deposition, and advanced inspection, which shows how many process layers must be funded together before a line becomes competitive. EV Group and SUSS MicroTec also continued to expand bonding and die-to-wafer platforms in 2025 and 2026, which underlines that no entrant can rely on a narrow tool footprint if it wants to support modern HBM assembly. That broad requirement pushes total line spending into a level that only a few memory makers, foundries, and top-tier packaging specialists can manage with confidence. It also makes timing more difficult, because customers must commit capital before it is fully clear how quickly hybrid bonding will move from qualification into large-scale production. The restraint is not just the size of the check, it is the risk of funding the wrong mix of tools for the next HBM generation.

Thermal Stress and Keep-Out Zone Design Constraints

Thermal stress remains a real limitation because TSV structures place copper and silicon with very different expansion behavior inside very dense memory stacks. The 2025 Electronics review on hybrid bonding highlighted how thermal management becomes more demanding as stack height rises and interconnect pitch shrinks, which is directly relevant to HBM roadmaps moving toward 12-layer and 16-layer designs. In practice, this means designers cannot chase higher via density without also protecting nearby active circuitry, managing package warpage, and controlling heat paths across thinner dies. Those constraints slow qualification because process engineers and device designers must solve mechanical and electrical problems together rather than in sequence. The issue matters for the HBM Through-Silicon Via (TSV) technology and equipment market because thermal stress can reduce the useful value of higher interconnect density if the surrounding die layout cannot support it. As a result, some gains in stack performance are likely to arrive only when bonding, materials, and design rules improve together.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Equipment Hegemony Masks a Materials Inflection

Equipment held 77.12% of revenue in 2025, which kept the largest share of spending concentrated in the tool base that enables etch, fill, thinning, bonding, and inspection across the production flow. In revenue terms, that position reflects how the HBM Through-Silicon Via (TSV) technology and equipment market still depends on each process step being too specialized to commoditize. Applied Materials said in June 2026 that it expects packaging revenue to exceed USD 2 billion in 2026 and introduced the Opta Quad CMP platform, Nokota VMax 2 ECD, and Producer Avila 2 PECVD to support TSV reveal, copper plating, and dielectric deposition. That launch makes clear that equipment leadership is not based on one machine category, but on the ability to cover multiple high-yield process steps with tightly integrated performance. The dominance of equipment also shows why new capacity plans remain vulnerable to lead times, because missing one critical tool can delay a full production ramp.

Materials are the fastest-growing offering at a 27.56% CAGR through 2031, which signals a change in where process difficulty is starting to migrate. As via dimensions move toward finer critical dimensions and bonding conditions become stricter, materials now carry more of the burden for thermal stability, copper purity, surface preparation, and temporary bonding performance. That shift does not remove the central role of tools, but it raises the value of specialized consumables that can stabilize yield under more aggressive process windows. Services remain the smallest part of the HBM Through-Silicon Via (TSV) technology and equipment market, yet they are becoming more important as vendors provide process tuning, integration support, and yield improvement work alongside equipment delivery. This matters because services can move practical know-how from the customer floor back into the vendor ecosystem, which can shape later buying decisions. The offering mix therefore still favors tools today, but it is slowly moving toward a more balanced model where equipment, materials, and integration support reinforce one another.

By TSV Process Type: Via-Middle Concentration Reveals an Architecture Lock-In

Via-middle captured 62.52% of process-type revenue in 2025, which shows that the HBM Through-Silicon Via (TSV) technology and equipment market remains centered on the process architecture already embedded in commercial HBM manufacturing. The same segment is projected to expand at a 27.51% CAGR through 2031, which means growth is coming from more capacity on the same process foundation rather than from a broad shift into a different TSV sequence. Future Memory Storage Conference material from 2025 showed that major HBM suppliers have standardized on via-middle TSV in production, which explains why its installed base remains strong. That standardization matters because it locks in not only process preference, but also the surrounding tool stack, operator know-how, and yield optimization routines. Once those elements are mature, customers become less willing to switch unless a new method offers a very clear gain in cost, density, or reliability.

Via-first remains relevant in narrower use cases where through-wafer connectivity must be built before later processing, especially in areas outside the main HBM volume base. Via-last still has a place in interposer and selected heterogeneous integration work where process flexibility can matter more than the dense vertical pitch needed in memory stacking. Neither of those routes has enough current pull to displace via-middle in the near term, because HBM production is where the largest commercial volumes continue to sit. This leaves the HBM Through-Silicon Via (TSV) technology and equipment market in a position where process innovation must often happen inside the via-middle framework rather than outside it. Vendors therefore compete by improving etch profile control, copper fill quality, wafer thinning stability, and downstream bonding compatibility instead of trying to replace the full architecture. The result is a market that looks dynamic from a revenue perspective, but structurally conservative in the process path that supports most of that growth.

By Bonding Technology: Thermocompression Durability and Hybrid Bonding's Ascent

Thermocompression bonding held 69.74% of revenue in 2025, which kept the largest installed base aligned with the method that has supported HBM2E through HBM3E production and remains central to current supply. That share shows how the HBM Through-Silicon Via (TSV) technology and equipment market still relies on process stability where commercial volume is already proven. Hybrid bonding is the fastest-growing technology at a 27.76% CAGR through 2031, reflecting the push toward finer pitch and lower thermal resistance in taller memory stacks. The 2025 Electronics review outlined why hybrid bonding is attractive for future HBM designs, especially where improved thermal and electrical performance becomes necessary at smaller pitch. Samsung Electronics also confirmed a roadmap that uses hybrid copper bonding from 16-layer HBM4E onward, which gives the segment a defined commercial direction even if the transition will not happen in one step.

The installed thermocompression base still matters because most near-term HBM output cannot wait for full hybrid conversion. That is why the HBM Through-Silicon Via (TSV) technology and equipment market is not seeing a clean replacement cycle, but a period where both technologies stay important for different production windows. BESI reported that Q1 2026 orders rose 104.5% year over year with hybrid bonding demand from multiple customers, which suggests that qualification activity is already translating into real capital commitments. Imec and EV Group’s 200 nm wafer-to-wafer demonstration also shows how far pitch scaling can go when the process is optimized for future integration density. Micro-bump and direct copper bonding still serve narrower roles, but the main competitive question now is which vendors can support present thermocompression needs while securing future hybrid bonding positions. That balance is likely to decide which suppliers stay embedded when memory stacks move beyond current layer counts.

By Application: HBM Anchors Revenue While AI Accelerators Set the Growth Pace

High bandwidth memory accounted for 47.96% of application revenue in 2025, which confirms that the HBM Through-Silicon Via (TSV) technology and equipment market is still anchored in the memory architecture it was built to serve. HBM remains the leading application because TSV was developed in close alignment with stacked memory needs, and that link is still shaping equipment demand today. AI accelerators are projected to expand at a 28.16% CAGR through 2031, which shows where the next layer of demand is forming even though HBM itself remains the largest direct use case. The HBM4 performance path described in 2025 conference material points to higher bandwidth, higher capacity, and more stacked layers, all of which tighten the relationship between memory packaging and AI system performance. Samsung’s commercial HBM4 shipment in June 2026 also signals that advanced accelerator supply is already moving into the next memory generation.

GPU packages and HPC processors continue to benefit from the same TSV ecosystem, though their stack requirements and production mix do not fully match dedicated HBM demand. Chiplet-based processors are becoming more important because they extend TSV relevance into broader heterogeneous integration, where memory, logic, and I/O components may come from different process nodes and still need dense package-level interconnects. That widens the scope of the HBM Through-Silicon Via (TSV) technology and equipment market beyond memory suppliers alone, even if memory remains the largest direct revenue source. Other advanced packaging applications such as photonics integration and automotive radar chiplets are still small, but they matter because they give OSATs and equipment vendors reasons to diversify their advanced packaging portfolios. The application mix therefore remains concentrated, but it is not static. Growth is strongest where HBM and AI infrastructure meet, which means application expansion is reinforcing the same technology requirements already visible in bonding, wafer size, and integration choices.

By End User: Memory Manufacturers Anchor the Market, Foundry Ambitions Reshape the Value Chain

Memory manufacturers held 63.91% of end-user revenue in 2025, which made them the clear center of demand in the HBM Through-Silicon Via (TSV) technology and equipment market. That leadership reflects the vertically integrated production model of SK hynix, Samsung Electronics, and Micron, where core TSV-related process steps stay close to the memory road map rather than being widely outsourced. The segment’s scale also shows why customer concentration remains high, because a limited number of buyers can influence tool choices across large parts of the supply chain. Foundries are projected to expand at a 27.71% CAGR through 2031, which indicates that packaging and integration services are becoming more important as chiplet and AI designs grow more complex. In practice, this means the HBM Through-Silicon Via (TSV) technology and equipment market is moving from a memory-led structure toward a broader advanced packaging structure without losing memory as its anchor.

Foundries matter because they can combine wafer fabrication, package integration, and customer-specific design support under one commercial relationship. That is attractive to hyperscale and custom compute programs that want fewer handoffs between design, fabrication, and packaging stages. OSATs and IDMs also remain relevant because they absorb overflow demand, build niche capabilities, and support specialized package assembly where full vertical integration is not practical. Standards compliance still shapes this segment because multi-vendor HBM and packaging ecosystems depend on consistent interface and qualification behavior, even when the commercial arrangements differ by customer. For the HBM Through-Silicon Via (TSV) technology and equipment market, that creates a more layered buyer base where leading memory makers still set the pace, but foundries and packaging specialists are becoming more active in both tool adoption and process ownership. The end-user picture therefore supports continued concentration, but it also points to a market that will not stay limited to its original customer group.

By Wafer Size: 300 mm Entrenchment and the Economics of Scale

The 300 mm segment held 94.23% of revenue in 2025, which made it the strongest sign of standardization anywhere in the HBM Through-Silicon Via (TSV) technology and equipment market. The 300 mm segment is also projected to expand at a 27.53% CAGR through 2031, so the largest wafer format is not only dominant, it is also growing fastest. This means the HBM Through-Silicon Via (TSV) technology and equipment market size for 300 mm is expanding on the back of both installed infrastructure and new capacity plans. The appeal of 300 mm is straightforward, because it offers much better die output per wafer and better economics once the process is stable. For TSV-heavy manufacturing, those economics matter even more because etch uniformity, copper fill consistency, and bonding throughput need to scale without pushing cost per die too high.

EV Group’s next-generation GEMINI system, which began taking orders in March 2025, was designed for 300 mm MEMS and advanced packaging applications with bond force up to 350 kN and high-vacuum capability. That product launch shows that vendors are still advancing performance inside the 300 mm framework rather than preparing for another shift in standard wafer size. The 200 mm segment remains relevant in specialized packaging environments, including lower-volume compound semiconductor and defense-oriented use cases where installed capacity still meets demand. Even so, its role is limited when compared with mainstream HBM production economics. The HBM Through-Silicon Via (TSV) technology and equipment market share tied to 300 mm therefore reflects more than scale, it reflects an ecosystem that has already aligned its tools, processes, and investment logic around one common manufacturing format. That degree of alignment raises barriers for entrants that do not already have access to 300 mm-capable lines and suppliers.

By Integration: Die-To-Wafer Dominance and the Die-To-Die Transition

Die-to-wafer held 63.29% of integration revenue in 2025, which made it the leading format for the current generation of advanced package assembly in the HBM Through-Silicon Via (TSV) technology and equipment market. Its lead comes from the practical advantage of stacking known-good dies onto a target wafer while preserving better yield control than broader wafer-to-wafer approaches can always provide. Die-to-die is projected to expand at a 27.56% CAGR through 2031, which makes it the fastest-moving integration route as chiplet architectures become more common. This means the HBM Through-Silicon Via (TSV) technology and equipment market size for die-to-die is rising with the need for finer placement accuracy, more flexible assembly, and better integration of components coming from different wafer sources. The growth case is especially strong in AI and heterogeneous compute packages where memory, logic, and I/O no longer need to come from the same process node or supplier.

SUSS MicroTec introduced the XBC300 Gen2 D2W platform in May 2025 as an integrated die-to-wafer hybrid bonding solution, which shows how vendors are building around high-volume production readiness rather than laboratory-scale proof points. Imec and EV Group’s 2026 wafer-to-wafer hybrid bonding demonstration shows that wafer-level integration still sets important technology benchmarks, especially in pitch scaling. Even so, wafer-to-wafer adoption remains constrained when stack yield is heavily affected by the compounded risk of bonding full wafers together. That keeps known-good-die logic highly relevant for commercial production. The HBM Through-Silicon Via (TSV) technology and equipment market is therefore shifting from a world dominated by one practical integration format to one where multiple formats stay active for different package designs. Over time, the strongest gains are likely to come from the formats that combine density with yield protection, which explains why die-to-die is attracting so much interest.

Geography Analysis

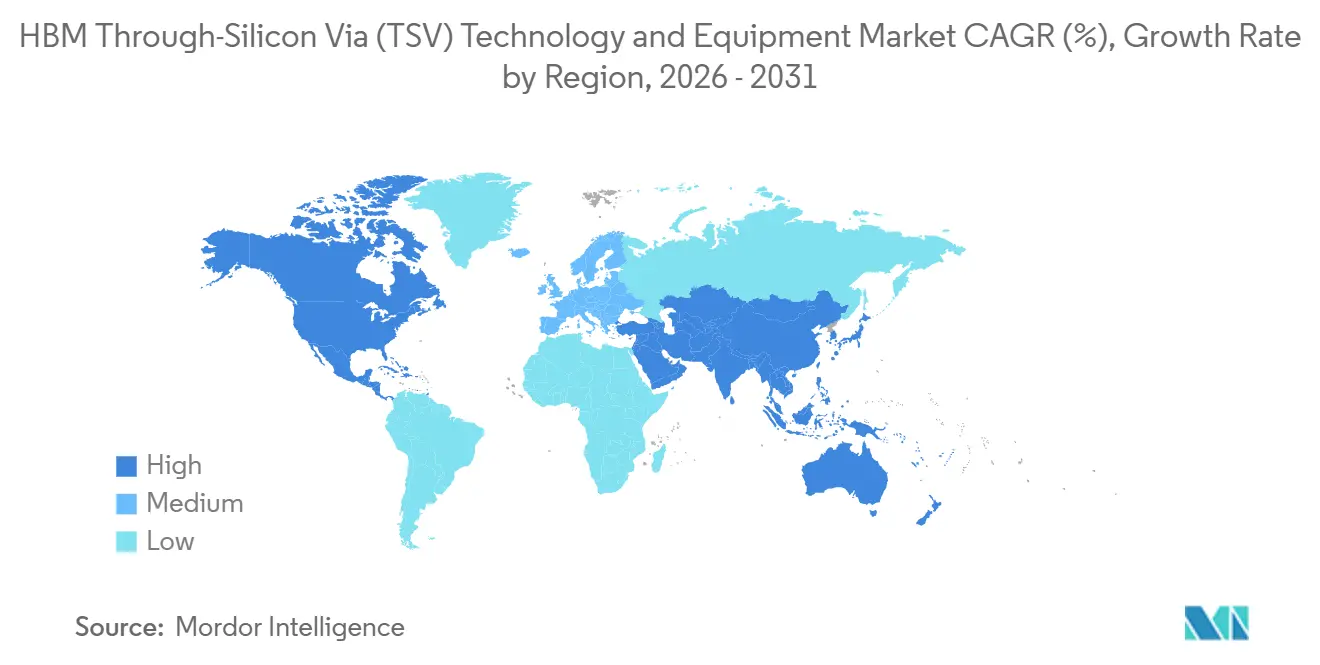

Asia-Pacific held 77.83% of the HBM Through-Silicon Via (TSV) technology and equipment market share in 2025 and is projected to expand at a 27.94% CAGR through 2031. That dual position reflects the fact that the region combines memory production, foundry packaging, OSAT support, and equipment supply in one interconnected footprint. South Korea remains central because Samsung Electronics and SK hynix anchor commercial HBM output, and the country also continues to back packaging capability through targeted public support. Taiwan strengthens the regional position through its foundry and OSAT base, which supports broader advanced packaging demand tied to AI compute programs. Japan remains important as an equipment and process ecosystem contributor, which helps keep Asia-Pacific ahead not only in output but also in tool availability and production readiness.

North America held a smaller position in 2025, but it is becoming more important as a funding, equipment, and future packaging capacity base for the HBM Through-Silicon Via (TSV) technology and equipment market. The U.S. government finalized USD 1.4 billion in CHIPS packaging awards in January 2025, which gave the region a stronger platform for prototyping, pilot production, and process development. The same policy direction supported up to USD 458 million for SK hynix’s Indiana project, linking public support to future HBM packaging capability inside the United States. KLA said its advanced packaging revenue was expected to rise from around USD 635 million in 2025 to around USD 1 billion in 2026, which shows how North American toolmakers are capturing value from this buildout cycle.

Europe maintained a specialized role in 2025, led by equipment vendors rather than large-scale HBM production lines. SUSS MicroTec and EV Group remain the main regional names in bonding and integration tools, and both stayed active in 2025 and 2026 through product and technology announcements. This gives Europe an important technical position inside the HBM Through-Silicon Via (TSV) technology and equipment market even though its manufacturing base is narrower than Asia-Pacific’s. South America and the Middle East and Africa remained at an early stage, with limited direct participation in TSV production and stronger relevance as downstream users of AI hardware than as core sources of HBM packaging capacity.

Competitive Landscape

The HBM Through-Silicon Via (TSV) technology and equipment market is moderately concentrated at the equipment layer and highly concentrated at the customer layer, because a small number of tool vendors sell into a very limited set of advanced packaging buyers. Applied Materials, Lam Research, Tokyo Electron, BESI, EV Group, SUSS MicroTec, KLA, and Onto Innovation are among the names that matter most across the core process chain. The competitive edge in this market usually comes from process-step ownership, qualification history, and the ability to stay present across several stages of the same line. That is why customers often favor vendors that can support not only one tool purchase, but also later process tuning, inspection, and migration into the next bonding or stacking generation.

Applied Materials has taken the clearest broad-platform approach in the HBM Through-Silicon Via (TSV) technology and equipment market. In April 2025, the company announced a 9% stake in BESI and extended a co-development agreement around die-to-wafer hybrid bonding, which gave it a stronger position in a critical transition technology. In May 2026, it agreed to acquire NEXX from ASMPT, which expanded its advanced packaging deposition portfolio for larger AI package formats. In the same month, Applied Materials disclosed a long-term collaboration with SK hynix at the EPIC Center to advance materials, process integration, and 3D packaging for future DRAM and HBM generations. These moves matter because they deepen customer alignment and make it harder for rivals to displace a vendor once process recipes and engineering teams become intertwined.

Other suppliers are focusing on narrower, but highly strategic positions. BESI reported strong hybrid bonding order growth in Q1 2026, which supports the view that bonding is one of the most contested process positions in the market. SUSS MicroTec strengthened its role in die-to-wafer hybrid bonding with the XBC300 Gen2 D2W platform, while EV Group continued to highlight bonding, layer transfer, and overlay metrology for advanced memory and packaging customers. Imec and EV Group’s 2026 hybrid bonding demonstration also shows that advanced pitch capability is becoming a public marker of technical credibility in this market. The HBM Through-Silicon Via (TSV) technology and equipment market therefore remains open to competition, but it favors vendors that can secure early qualification, stay close to top customers, and support both current volume needs and future process transitions.

HBM Through-Silicon Via (TSV) Technology and Equipment Industry Leaders

Applied Materials, Inc.

Lam Research Corporation

Tokyo Electron Limited

EV Group

ASM International N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Applied Materials introduced five new systems targeting critical TSV and advanced packaging process steps, the Opta Quad CMP system, Nokota VMax 2 ECD for copper plating in TSV fill, Producer Avila 2 PECVD for stress-balanced dielectric deposition around ultra-thin HBM dies, and two wafer-fab-grade eBeam metrology systems, VeritySEM 7AP and SEMVision G7AP, delivering sub-10 nm sensitivity for advanced packaging defect inspection.

- June 2026: Samsung Electronics confirmed it had shipped the industry's first commercial HBM4 memory to customers, marking the first sixth-generation HBM product to reach mass production. Samsung anticipated HBM sales to more than triple in 2026 compared to 2025 and confirmed sampling of HBM4E would begin in the second half of 2026, sustaining multi-year demand for via-middle TSV and bonding equipment.

- May 2026: Imec and EV Group demonstrated wafer-to-wafer hybrid bonding at 200 nm Cu interconnect pad pitch at the IEEE Electronic Components and Technology Conference, achieving record Cu pad alignment accuracy on a test vehicle with routable interconnects, establishing the most advanced publicly disclosed pitch benchmark for memory-to-logic tier stacking.

- May 2026: Applied Materials entered into a definitive agreement to acquire NEXX from ASMPT Limited, broadening its portfolio with panel-level electrochemical deposition equipment designed to enable larger-body AI accelerator packages and co-optimized fine-pitch I/O wiring for advanced packaging roadmaps.

Global HBM Through-Silicon Via (TSV) Technology and Equipment Market Report Scope

The Global HBM Through-Silicon Via (TSV) Technology and Equipment Market refers to the industry segment dedicated to the development, manufacturing, and deployment of advanced TSV-based packaging technologies and equipment used in High Bandwidth Memory (HBM) integration.

The HBM Through-Silicon Via (TSV) Technology and Equipment Market Report is Segmented by Offering (Equipment, Materials, and Services), TSV Process Type (Via-First TSV, Via-Middle TSV, and Via-Last TSV), Bonding Technology (Thermocompression Bonding, Hybrid Bonding, Micro-Bump Bonding, and Direct Copper Bonding), Application (High Bandwidth Memory, AI Accelerators, GPU Packages, HPC Processors, Chiplet-Based Processors, and Other Advanced Packaging Applications), End User (Memory Manufacturers, Foundries, Integrated Device Manufacturers (IDMs), OSATs, and Research Institutes), Wafer Size (200 mm, 300 mm, and Other Wafer Sizes), Integration (Wafer-to-Wafer, Die-to-Wafer, and Die-to-Die), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Equipment |

| Materials |

| Services |

| Via-First TSV |

| Via-Middle TSV |

| Via-Last TSV |

| Thermocompression Bonding |

| Hybrid Bonding |

| Micro-Bump Bonding |

| Direct Copper Bonding |

| High Bandwidth Memory |

| AI Accelerators |

| GPU Packages |

| HPC Processors |

| Chiplet-Based Processors |

| Other Advanced Packaging Applications |

| Memory Manufacturers |

| Foundries |

| Integrated Device Manufacturers (IDMs) |

| OSATs |

| Research Institutes |

| 200 mm |

| 300 mm |

| Other Wafer Sizes |

| Wafer-to-Wafer |

| Die-to-Wafer |

| Die-to-Die |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| India | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Offering | Equipment | |

| Materials | ||

| Services | ||

| By TSV Process Type | Via-First TSV | |

| Via-Middle TSV | ||

| Via-Last TSV | ||

| By Bonding Technology | Thermocompression Bonding | |

| Hybrid Bonding | ||

| Micro-Bump Bonding | ||

| Direct Copper Bonding | ||

| By Application | High Bandwidth Memory | |

| AI Accelerators | ||

| GPU Packages | ||

| HPC Processors | ||

| Chiplet-Based Processors | ||

| Other Advanced Packaging Applications | ||

| By End User | Memory Manufacturers | |

| Foundries | ||

| Integrated Device Manufacturers (IDMs) | ||

| OSATs | ||

| Research Institutes | ||

| By Wafer Size | 200 mm | |

| 300 mm | ||

| Other Wafer Sizes | ||

| By Integration | Wafer-to-Wafer | |

| Die-to-Wafer | ||

| Die-to-Die | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the HBM Through-Silicon Via (TSV) technology and equipment market size in 2026 and how large could it become by 2031?

The HBM Through-Silicon Via (TSV) technology and equipment market size stands at USD 0.57 billion in 2026 and is projected to reach USD 1.88 billion by 2031 at a 26.96% CAGR.

Which segment leads by offering in HBM Through-Silicon Via (TSV) technology and equipment?

Equipment led with 77.12% of revenue in 2025, showing that capital spending is still centered on the tool base needed for etch, plating, bonding, thinning, and inspection.

What is driving growth in HBM Through-Silicon Via (TSV) technology and equipment demand?

The main growth pull comes from AI accelerators and next-generation HBM stacks that need higher bandwidth, taller stack structures, and more reliable vertical interconnect performance.

Which bonding approach is growing fastest for future HBM packages?

Hybrid bonding is the fastest-growing bonding technology with a projected 27.76% CAGR through 2031, even though thermocompression bonding remained the largest segment in 2025.

Why is Asia-Pacific the key regional hub for this space?

Asia-Pacific held 77.83% share in 2025 and is also the fastest-growing region at 27.94% CAGR, because it combines HBM production, packaging capacity, and equipment support in one regional network.

Which end users matter most in this space today?

Memory manufacturers held 63.91% of revenue in 2025, while foundries are projected to grow fastest through 2031 as packaging and heterogeneous integration become more important.

Page last updated on: