HBM Thermal Management and TIM Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

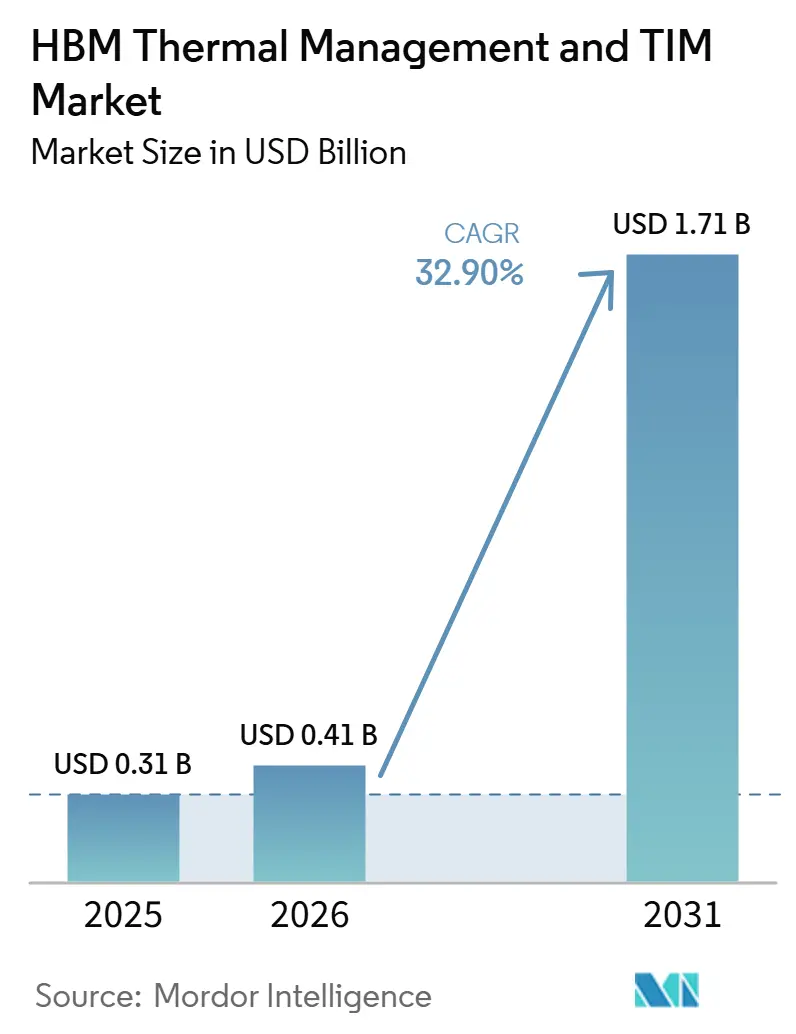

| Market Size (2026) | USD 0.41 Billion |

| Market Size (2031) | USD 1.71 Billion |

| Growth Rate (2026 - 2031) | 32.90% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HBM Thermal Management and TIM Market Analysis by Mordor Intelligence

The HBM thermal management and TIM market size is expected to increase from USD 0.31 billion in 2025 to USD 0.41 billion in 2026 and reach USD 1.71 billion by 2031, growing at a CAGR of 32.90% over 2026-2031. The HBM thermal management and TIM market is expanding much faster than the wider thermal interface materials space because AI compute platforms are moving to much higher power density and much tighter thermal limits within each package. Rising GPU thermal design power is forcing package designers to review every thermal layer, from die attach through the package lid and heatsink interface, because earlier material choices no longer provide enough headroom for new accelerator platforms. Growth is also being shaped by taller HBM stacks and more complex package geometries, which increase heat flux and make thermal performance a package-level design issue rather than a single-material selection task. Competition is moving toward earlier co-development with memory makers, chip companies, and packaging partners, which favors suppliers that can support simulation, qualification, and interface-specific tuning. The HBM thermal management and TIM market is also benefiting from sovereign semiconductor investment and domestic packaging expansion, but long qualification cycles and limited high-purity filler supply still slow the pace of new formulations scaling.

Key Report Takeaways

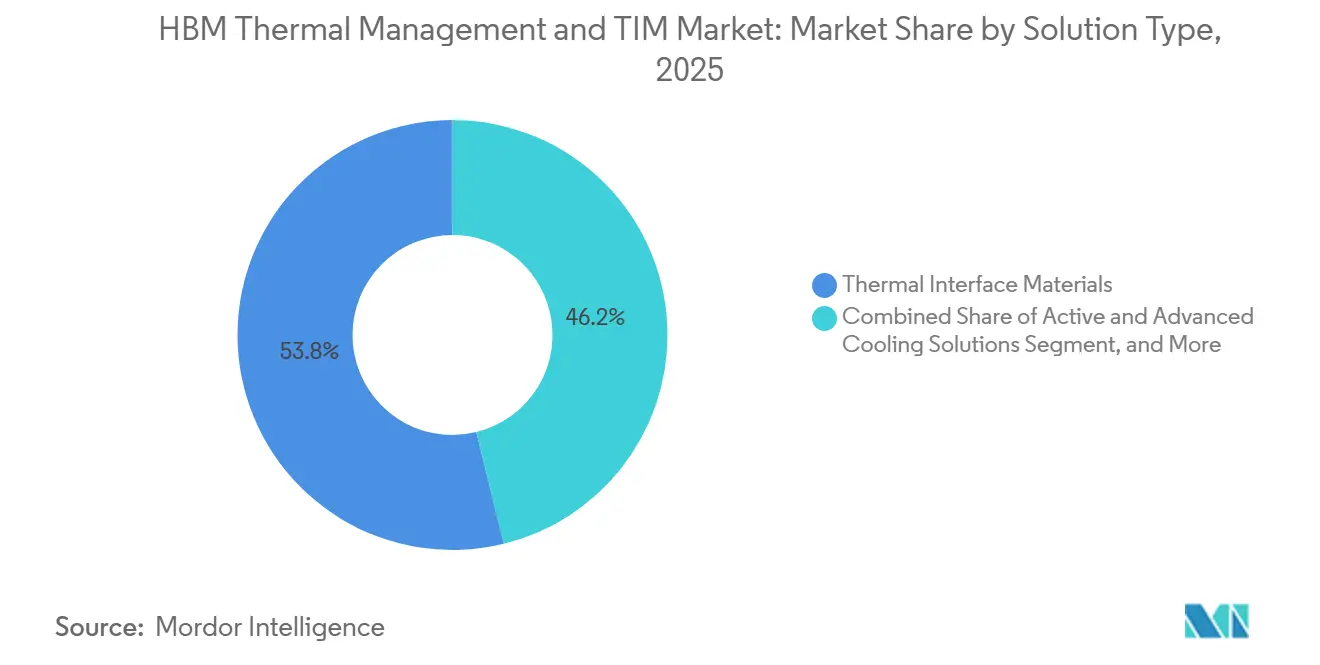

- By solution type, thermal interface materials held 53.83% of the HBM thermal management and TIM market share in 2025, while active and advanced cooling solutions are projected to expand at a 33.49% CAGR through 2031.

- By TIM type, silicone-based TIM accounted for 42.19% of the market share in 2025, while graphene and carbon-based TIM are expected to record the highest CAGR of 34.08% through 2031.

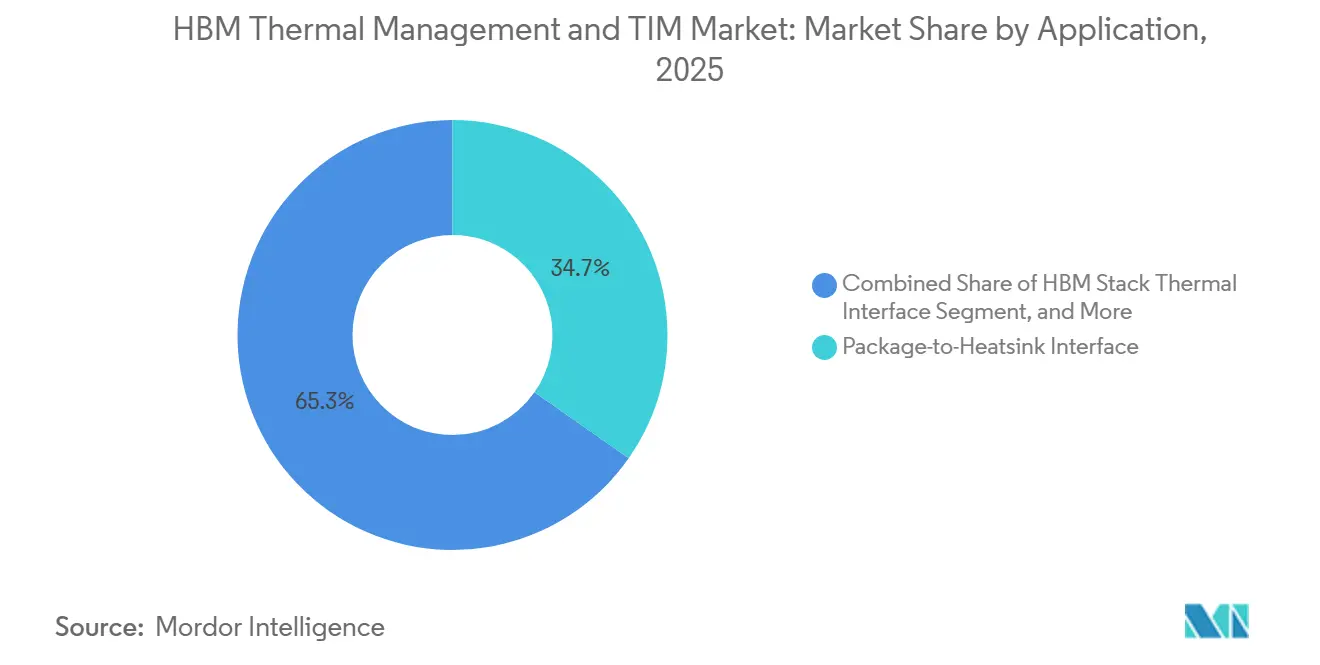

- By application, the package-to-heatsink interface captured 34.71% share in 2025, while the HBM stack thermal interface is projected to advance at a 33.88% CAGR through 2031.

- By end-use industry, AI accelerators and GPUs held 59.62% share of the HBM thermal management and thermal interface materials (TIM) market in 2025, while data centers are projected to grow at the fastest CAGR of 33.97% through 2031.

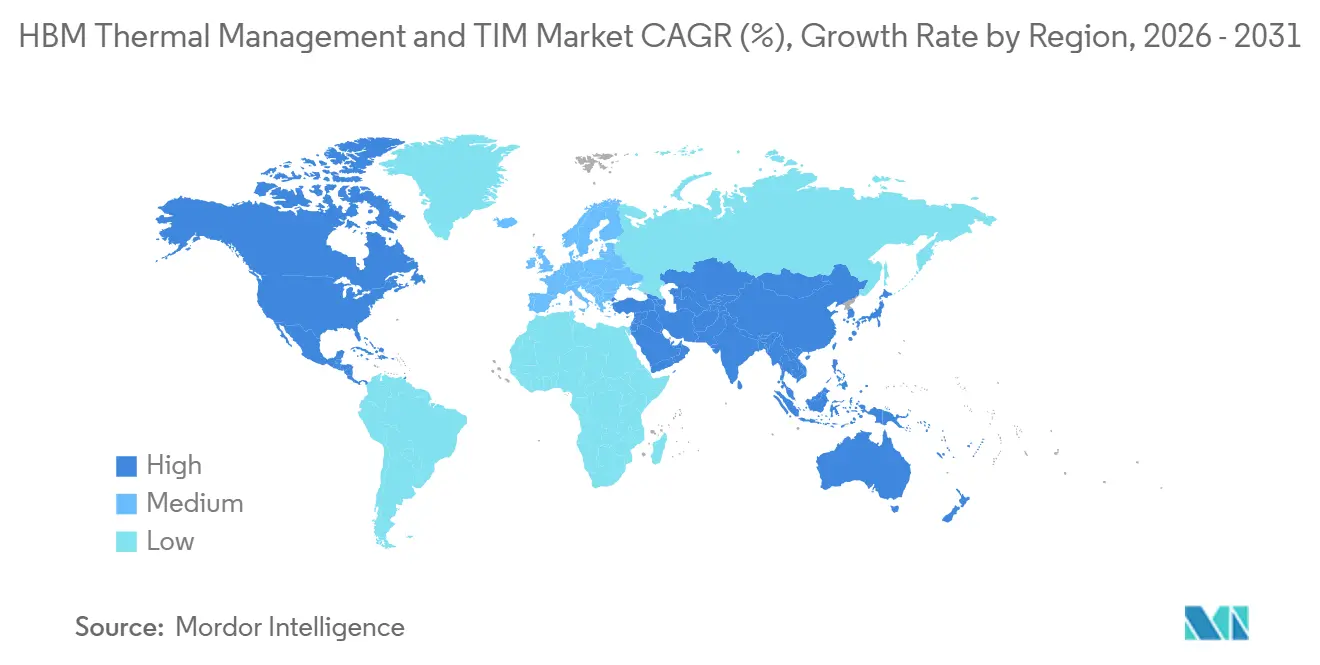

- By geography, Asia-Pacific held 64.96% share in 2025, while North America is projected to record the highest CAGR at 33.81% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HBM Thermal Management and TIM Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI Accelerator Power Density Escalation | +7.5% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| HBM Stack Height Growth Increasing Package Heat Flux | +6.8% | Asia-Pacific core, spill-over to North America | Short term (≤ 2 years) |

| Co-Packaged Memory and Logic Roadmaps Raising Thermal Qualification Thresholds | +5.2% | Global, with early gains in South Korea, Taiwan, and United States | Medium term (2-4 years) |

| Advanced Semiconductor Packaging Adoption in HBM Supply Chains | +4.6% | Asia-Pacific and North America | Medium term (2-4 years) |

| HBM Thermal Failure Margins Driving Premium TIM Adoption in Hyperscale Designs | +3.1% | North America and Asia-Pacific | Short term (≤ 2 years) |

| Under-Reported Demand for Package-Level Thermal Simulation and Design-In Services | +2.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI Accelerator Power Density Escalation

The HBM thermal management and TIM market is responding first to the sharp rise in GPU power envelopes, which moved from up to 700 W in NVIDIA H100 systems to 1,000 W in the Blackwell B200 path and to 1,400 W in the B300 path described in the source material.[1]Source: NVIDIA, “H200 GPU,” NVIDIA Data Center, nvidia.com That increase reduces the thermal margin across the entire package because the GPU die and the HBM stack must now share a much tighter heat-reduction path within the same footprint. Material choices that worked for earlier accelerator generations are becoming less suitable as junction temperature control now depends on lower resistance at multiple interfaces rather than just better bulk conductivity. NVIDIA also tied liquid cooling to lower operating costs in large AI facilities, giving customers a financial incentive to raise thermal specifications before the next memory node even reaches volume deployment. In the HBM thermal management and TIM market, this shift is driving supplier discussions away from simple conductivity claims toward co-design support, interface matching, and simulation capabilities during package development. Suppliers that can help customers balance heat flow between compute silicon and memory layers earlier in the design cycle are therefore gaining stronger design-in positions.

HBM Stack Height Growth Increasing Package Heat Flux

The HBM thermal management and TIM market is also being pushed by taller memory stacks, because JEDEC’s HBM4 standard, published in April 2025, supports up to 16-high stacks with 32 Gb die density and a maximum cube capacity of 64 GB. Each added tier expands the heat-generating area while lengthening the vertical path through which lower dies must release heat, making stack geometry itself a thermal constraint. Imec showed the scale of this issue when its 3D HBM-on-GPU study reported peak GPU temperatures of 141.7°C without mitigation, while a package with structural and cooling changes reduced them to 70.8°C. SK hynix addressed the same problem in May 2026 with iHBM, which places Integrated Cooling Elements at the D2D PHY layer and lowers thermal resistance by more than 30% versus indirect cooling approaches. For suppliers in the HBM thermal management and TIM market, this means stack-level interfaces are moving toward thinner bondlines, more localized hot spots, and performance requirements that extend beyond the validated range of many current silicone products. That shift raises the value of formulations that can hold thermal performance at very thin bondlines without sacrificing reliability under repeated thermal stress.

Co-Packaged Memory and Logic Roadmaps Raising Thermal Qualification Thresholds

The HBM thermal management and TIM market is being further shaped by the move toward more active logic within the memory package, as HBM4 expands the interface from 1,024 bits to 2,048 bits and increases the number of independent channels per stack to 32. That change makes the logic base die a more meaningful heat source at the die-to-die interface, so thermal load is no longer concentrated only in the main compute die. The practical result is that each co-packaged logic variant can have its own thermal profile, reducing the usefulness of a single pre-qualified TIM across customers and product generations. Qualification, therefore, has to be repeated across package design, logic configuration, and memory generation, which extends development cycles even when material performance looks strong in lab testing. In the HBM thermal management and thermal interface materials (TIM) market, suppliers participating in joint development programs with memory makers and chip companies have a structural advantage, as early access shortens the gap between prototype testing and package qualification. That advantage is becoming increasingly important as customers seek materials that can withstand a wider range of interface conditions without introducing new reliability risks.

Advanced Semiconductor Packaging Adoption in HBM Supply Chains

The HBM thermal management and TIM market is benefiting from the wider use of advanced packaging, as AI accelerators that use HBM are increasingly built around platforms such as CoWoS and EMIB, where thermal control depends on multiple connected interfaces rather than a single one. In these architectures, thermal behavior and mechanical behavior interact closely because silicon interposers, substrates, molding compounds, and lids respond differently to heat during operation and cycling. This means that TIM selection affects package warpage, thermal crosstalk, and long-term stability simultaneously, so the qualification task is broader than measuring conductivity in isolation. The number of thermal interfaces per compute package is also increasing, from die attach and die-to-die bonding through lid and heatsink contact, which expands the total addressable scope for suppliers that can qualify across more than one interface position. The HBM thermal management and TIM market, therefore, gains not only from higher performance requirements but also from a rising count of interface positions that require tailored materials and more package-level engineering support. Suppliers that can cover several of those positions with compatible materials and shared validation data are likely to win broader package content within the same platform.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight Reliability Windows for Long-Life AI and HPC Deployments | -2.4% | Global | Short term (≤ 2 years) |

| Material Qualification Cycles Delaying Commercial Scale-Up | -1.8% | Global, with early impact in North America and Asia-Pacific | Medium term (2-4 years) |

| Limited Supply of High-Purity Filler Systems for Advanced TIM Formulations | -1.5% | Global, raw material sourced from limited geographies | Long term (≥ 4 years) |

| Yield Loss Risk from Thermal-Mechanical Stress in 3D Stacked Memory | -1.2% | Asia-Pacific core, South Korea and Taiwan, spill-over to North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tight Reliability Windows for Long-Life AI and HPC Deployments

The HBM thermal management and TIM market faces a clear brake from the long service life expected in hyperscale and HPC hardware, because operators want systems to run under sustained heavy use for 5 to 7 years before replacement. Advanced materials such as graphene-enhanced gels and gallium-based liquid metals still have limited production scale and field history compared with incumbent silicone systems, even when their lab performance looks stronger. IEEE THERMINIC research in 2025 showed that TIM1 degradation in large die packages can be highly localized and shaped by assembly warpage and by material behavior under thermomechanical stress. This means bulk thermal conductivity alone does not predict field reliability well enough for buyers making long-life infrastructure decisions. Once a material is qualified and deployed, operators are reluctant to change it mid-cycle because replacement requires disassembly and renewed validation. That creates qualification lock-in in the HBM thermal management and TIM market, slowing the adoption of novel chemistries even when they can exceed the incumbent's thermal performance in controlled testing.

Material Qualification Cycles Delaying Commercial Scale-Up

The HBM thermal management and TIM market also slows when new formulations enter long qualification pipelines that include thermal resistance testing, bondline characterization, cycling, pump-out checks, and package-level thermal sign-off. These steps often run sequentially rather than in parallel, so the timeline stretches out further whenever a new HBM generation or a logic base die configuration forces a reset. NEDO-backed work in Japan on iron catalyst encapsulation for silicone TIM manufacturing shows there are credible paths to process improvement and lower cost, but those gains still need full commercial qualification before they can support volume scale-up. This favors suppliers that can integrate materials with in-house modeling and simulation support, as faster troubleshooting can reduce the time customers spend between prototype and sign-off. In the HBM thermal management and TIM market, qualification history itself becomes a competitive asset, since a proven record in earlier package programs lowers the risk of selection for the next one. As a result, new entrants can struggle to convert strong performance data into revenue unless they also reduce the operational burden of qualification for the customer.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Thermal Interface Materials Anchor The Market, Active Cooling Solutions Lead Growth

Thermal Interface Materials held 53.83% of the HBM thermal management and TIM market share in 2025, which reflected their long-established role across die attach, package lid, and heatsink interfaces in AI accelerator packages. That position came from installed base depth as much as from performance, because many current package designs still rely on silicone and polymer systems that are already qualified in automated production and assembly flows. Even so, the performance ladder in this category is moving upward as customers seek formulations that maintain lower resistance without sacrificing compliance during cycling and warpage. Research published in ACS Applied Energy Materials in 2025 showed that vertically aligned graphene arrays achieved a bulk thermal conductivity of 90.5 W m⁻¹ K⁻¹ at 30.07 wt% graphene loading, far above the range typical of conventional silicone pads. In the HBM thermal management and TIM market, that result matters because it supports the move from laboratory validation toward early commercial sampling for TIM1 and related high-heat interfaces.

Heat spreaders and thermal enhancement components occupy an important middle ground, supporting both current lidded packages and newer lid-integrated thermal path concepts that are gaining attention in HBM stack-level management. Active and Advanced Cooling Solutions is projected to expand at a 33.49% CAGR through 2031, making it the fastest-growing solution type as platform-level cooling moves closer to the package. NVIDIA’s 2025 commentary on Rubin described a fully liquid-cooled system direction with fan removal and warmer coolant, which changes the boundary conditions that downstream thermal materials must meet. Frore Systems reinforced that direction in March 2026 when it raised USD 143 million at a USD 1.64 billion valuation to scale its LiquidJet platform, showing that capital is also moving toward package-integrated active cooling concepts.

By TIM Type: Silicone-Based TIM Leads On Volume, Graphene And Carbon Formulations Set The Growth Tempo

Silicone-Based TIM accounted for 42.19% of the HBM thermal management and TIM market in 2025, reflecting its broad qualification base, mechanical compliance, and compatibility with existing automated dispensing processes. Graphene and Carbon-Based TIM is projected to record the fastest CAGR of 34.08% through 2031, as it offers a much higher theoretical conductivity ceiling and a stronger path toward next-generation hot-spot control. The same ACS Applied Energy Materials study cited in the input explains why interest remains high; graphene can translate its strong intrinsic thermal properties into bulk structures that deliver far better performance than legacy filler systems when processing challenges are addressed. In the HBM thermal management and TIM market, the issue is no longer whether carbon-rich systems can perform, but whether they can do so at scale with stable bondlines, clean processing, and repeatable package reliability. That is why the segment still balances growth potential against commercial readiness rather than moving immediately away from incumbent silicon systems.

Dow’s launch of DOWSIL TC-3120 Thermal Gel in May 2026 showed that incumbent silicone suppliers are still raising the performance ceiling, with thermal conductivity near 12 W/m·K and positioning for dense optical and electronic module interfaces.[2]Dow Inc., “Dow Launches DOWSIL TC-3120 Thermal Gel,” Dow Press Release, corporate.dow.com Non-silicone TIM and phase change materials remain relevant where silicone contamination is a concern, and Laird’s Tpcm 7000 provided a premium benchmark with 7.5 W/mK thermal conductivity and reliability across 2,000 aging test hours in the source material. Liquid metal systems continue to gain interest, with Indium’s gallium-based Indalloy formulations approaching 44 W m⁻¹ K⁻¹ and targeting TIM0 and TIM1 use in bare-die AI server processors and ASICs. The HBM thermal management and TIM industry is therefore not moving in a single direction, since the winning chemistry still depends on containment, contamination risk, manufacturability, and the interface position being served.

By Application: Package-To-Heatsink Interface Holds The Volume, HBM Stack Thermal Interface Drives The Growth Edge

Package-to-Heatsink Interface accounted for 34.71% of the HBM thermal management and TIM market in 2025, reflecting its broad installed base across CPUs, GPUs, and ASIC packages used in AI systems. HBM Stack Thermal Interface is projected to grow at a 33.88% CAGR through 2031, as thermal control is moving deeper into the memory package and creating a new class of thin, silicon-adjacent interface requirements. SK hynix made that shift visible with iHBM in May 2026 by placing cooling elements at the D2D PHY layer, thereby directly changing expectations for material performance in stacked memory assemblies. In the HBM thermal management and TIM market, this application is important because it increases the value of formulations that can perform at very thin bondlines while handling concentrated heat flow near the active silicon. It also moves the material problem from a more accessible external interface to a tighter internal one where processing tolerance and reliability are harder to manage.

Die attach and chip bonding continue to benefit from the shift toward high-performance materials that can close the gap between polymer systems and solder while still meeting present compliance requirements in many electronics applications. The input specifically pointed to semi-sintering and advanced die attach systems, such as Henkel’s LOCTITE ABLESTIK range, as examples of how the interface is being upgraded for both thermal and regulatory reasons. Interposer and silicon-bridge thermal management is also gaining importance because advanced packaging adds more points where thermal and mechanical stresses interact within the package. IEEE ECTC's work on heterogeneously integrated HBM-GPU modules with step height differences further supports the view that advanced heterogeneous packaging will become a stronger application beyond 2031 as research concepts move closer to production readiness.

By End Use Industry: AI Accelerators And GPUs Define The Market, Data Centers Accelerate As Infrastructure Scales

AI Accelerators and GPUs held a 59.62% share in 2025, making them the largest end-use segment in the HBM thermal management and thermal interface material (TIM) market and the clearest source of demand for premium thermal materials. Their lead reflects the extreme power density of modern AI compute silicon, where heat removal limits package performance, uptime, and memory stability simultaneously. The transition from H100-era systems toward the Blackwell and Rubin platform direction is forcing a broad reset in package thermal requirements, as liquid-first system design changes the heat-rejection conditions across the entire accelerator. In the HBM thermal management and TIM market, AI accelerators remain at the center of specification changes, supplier qualification work, and early product sampling. It also means that improvements adopted first for high-end accelerators can spread to adjacent compute categories as platforms and package standards mature.

Data Centers are projected to record the fastest CAGR of 33.97% through 2031, as liquid cooling expands the thermal materials opportunity beyond the accelerator package into cold plates, power electronics, and cooling distribution hardware. High-Performance Computing shares many of the same thermal requirements, but its longer refresh cycles slow near-term material replacement even when its reliability expectations remain very high. Automotive remains a smaller but meaningful outlet as electrified power electronics raise thermal load, and Wacker expanded silicone TIM production in Tsukuba during 2025 to support electromobility demand in the Asia-Pacific. The HBM thermal management and TIM industry, therefore, continues to center on AI infrastructure, while still building secondary demand from sectors that value long life, thermal stability, and certified production quality.

Geography Analysis

Asia-Pacific held 64.96% of the HBM thermal management and TIM market share in 2025, which reflected the region’s concentration of HBM manufacturing, advanced packaging, and supporting semiconductor materials capacity. South Korea remained central because Samsung Electronics and SK hynix anchor global HBM supply, while Taiwan supports the package side through large-scale advanced packaging activity tied to AI accelerator programs. The HBM thermal management and TIM market in Asia-Pacific is also supported by the faster adoption of taller HBM stacks and more complex package layouts, which increase the need for qualified interface materials near the memory and compute dies. JEDEC’s HBM4 release in 2025 and SK hynix’s iHBM launch in 2026 both reinforced the region’s role in setting practical thermal requirements for the next wave of package design.[3]JEDEC Solid State Technology Association, “JEDEC And Industry Leaders Collaborate To Release JESD270-4 HBM4 Standard, Advancing Bandwidth, Efficiency, And Capacity For AI And HPC,” JEDEC, jedec.org Japan also held strategic value through materials development and process work, with Wacker expanding local silicone TIM capacity and NEDO supporting manufacturing innovation to lower silicone TIM production costs.

North America is projected to post the fastest CAGR at 33.81% through 2031, driven by rapid AI data center buildout and the need to support denser compute clusters with liquid-ready thermal solutions. NVIDIA’s own discussion of liquid-cooling economics shows why this region is moving quickly, as thermal infrastructure decisions now affect both system performance and operating costs in large AI facilities. The HBM thermal management and TIM market in North America also benefits from domestic semiconductor packaging expansion under the current industrial policy, which broadens demand beyond hyperscale servers alone. That combination links component-level materials demand with a larger buildout in package, board, and cooling hardware.

Europe held a smaller position, but it remained technically important because its electronics and automotive base keeps demand focused on compliance, reliability, and research-led package development. The region’s RoHS and REACH frameworks still matter for suppliers using metal-rich or specialized filler systems, as material selection must align with stricter compliance requirements in industrial and mobility applications. South America, the Middle East, and Africa remained early-stage in direct HBM-related TIM demand, as local HBM production and advanced packaging activity remain limited. Even so, later-period AI infrastructure programs in parts of the Middle East could create incremental opportunity for the HBM thermal management and thermal interface material (TIM) market if local compute capacity moves from deployment planning to sustained hardware installation.

Competitive Landscape

The HBM thermal management and TIM market remained moderately fragmented in 2026, with large chemical suppliers holding broad qualification positions while smaller specialists focused on high-conductivity niches and emerging interface problems. Henkel AG and Co. KGaA, Dow Inc., DuPont de Nemours Inc., and Shin-Etsu Chemical Co. Ltd. retained visibility because they combine material science depth with relationships across semiconductor packaging customers. That matters in this market because buyers do not evaluate conductivity alone; instead, they look for process fit, reliability history, contamination control, and the ability to support multiple interfaces within the same package. The HBM thermal management and TIM market also leaves room for targeted challengers in liquid-metal, carbon-rich, and package-integrated cooling areas where incumbent catalogs do not yet cover every thin-bondline or internal-stack condition. As a result, competition is shaped by both chemistry and customer access, with qualification history often deciding who can turn technical performance into real production share.

Dow’s May 2026 launch of DOWSIL TC-3120 Thermal Gel showed how incumbents are still pushing silicone performance higher rather than giving ground to alternative chemistries. Indium also used 2026 product promotion and technical presentations to position gallium-based liquid metal and solder TIM solutions for AI and HPC packaging, which shows how specialist suppliers are targeting the hardest interfaces first. SK hynix’s iHBM launch was another meaningful strategic move because it pulled thermal control deeper into the HBM package, potentially shifting where material suppliers create value and how future interfaces are specified.[4]SK hynix Inc., “SK hynix Unveils ‘iHBM’ Thermal Solution To Boost AI Performance,” SK hynix Newsroom, news.skhynix.com Frore Systems added pressure from a different angle by raising USD 143 million to scale active cooling platforms, which signals that some competition is shifting from material supply alone to integrated thermal architectures.

The HBM thermal management and TIM market is therefore likely to favor suppliers that can combine materials, simulation support, and customer co-development rather than those selling only catalog products. The most attractive whitespace remains inside stack-level and thin-bondline package positions, where thermal resistance targets are rising faster than the validation base of standard commercial materials. Companies that already hold package qualifications can still defend share by extending current platforms into higher-performance versions, while newer entrants must prove both performance and operational readiness. This keeps the competitive picture open enough for innovation, but difficult enough that scale-up without direct customer development support remains a major barrier.

HBM Thermal Management and TIM Industry Leaders

Henkel AG and Co. KGaA

Dow Inc.

DuPont de Nemours, Inc.

Shin-Etsu Chemical Co., Ltd.

3M Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Indium Corporation announced participation at FINE 2026 in Shanghai, presenting on alloy composition optimization and interface structure design for metal TIM applications in AI and HPC packaging.

- May 2026: SK hynix launched the iHBM solution, embedding Integrated Cooling Elements at the D2D PHY layer within the HBM package, reducing thermal resistance by over 30% versus conventional designs. Built on SK hynix’s MR-MUF wafer-level packaging process, it targets HBM5 and subsequent products, directly redefining TIM design requirements for HBM stack interfaces in hyperscale AI systems.

- May 2026: Dow Inc. launched DOWSIL TC-3120 Thermal Gel, delivering 12 W/m·K thermal conductivity, the highest in Dow’s commercially available silicone gel portfolio. Designed for 800G and 1.6T optical modules and dense electronics, the product targets module-to-heatsink interfaces with tolerance stackups in high-speed data center deployments.

- May 2026: Indium Corporation’s Applications Development Engineer presented research on indium-based solder TIMs for AI and HPC thermal challenges at IEEE ECTC 2026 in Orlando, addressing indium’s compliance and low interfacial resistance advantages for large-die BGA packages.

Global HBM Thermal Management and TIM Market Report Scope

The HBM Thermal Management and Thermal Interface Material (TIM) Market comprises materials, components, and cooling technologies designed to manage heat dissipation in high-bandwidth memory (HBM) packages used in advanced semiconductor devices. These solutions enhance thermal conductivity, maintain junction temperatures within operating limits, improve reliability, and support the increasing power densities associated with AI accelerators, GPUs, high-performance computing (HPC), and other high-performance electronic systems. The market includes thermal interface materials, heat spreaders, thermal enhancement components, and active cooling solutions deployed across die, HBM stack, interposer, and package-level interfaces to optimize thermal performance in advanced heterogeneous packaging architectures.

The HBM Thermal Management and TIM Market Report is Segmented by Solution Type ( Thermal Interface Materials, Heat Spreaders and Thermal Enhancement Components, and Active and Advanced Cooling Solutions), TIM Type (Silicone-Based TIM, Non-Silicone TIM, Phase Change Materials, Liquid Metal TIM, Graphene and Carbon-Based TIM, and Indium and Metal Alloy TIM), Application (Die Attach and Chip Boarding, Interposer and Silicon Bridge Thermal Management, HBM Stack Thermal Interface, Package-to-Heatsink Interface, and Advanced Heterogeneous packaging), End Use Industry (AI Accelerators and GPUs, Data Centers, High-Performance Computing, Automotive, Telecom, and Consumer Electronics), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Thermal Interface Materials |

| Heat Spreaders and Thermal Enhancement Components |

| Active and Advanced Cooling Solutions |

| Silicone-Based TIM |

| Non-Silicone TIM |

| Phase Change Materials |

| Liquid Metal TIM |

| Graphene and Carbon-Based TIM |

| Indium and Metal Alloy TIM |

| Die Attach and Chip Bonding |

| Interposer and Silicon Bridge Thermal Management |

| HBM Stack Thermal Interface |

| Package-to-Heatsink Interface |

| Advanced Heterogeneous Packaging |

| AI Accelerators and GPUs |

| Data Centers |

| High-Performance Computing |

| Automotive |

| Telecom |

| Consumer Electronics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| India | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Solution Type | Thermal Interface Materials | |

| Heat Spreaders and Thermal Enhancement Components | ||

| Active and Advanced Cooling Solutions | ||

| By TIM Type | Silicone-Based TIM | |

| Non-Silicone TIM | ||

| Phase Change Materials | ||

| Liquid Metal TIM | ||

| Graphene and Carbon-Based TIM | ||

| Indium and Metal Alloy TIM | ||

| By Application | Die Attach and Chip Bonding | |

| Interposer and Silicon Bridge Thermal Management | ||

| HBM Stack Thermal Interface | ||

| Package-to-Heatsink Interface | ||

| Advanced Heterogeneous Packaging | ||

| By End Use Industry | AI Accelerators and GPUs | |

| Data Centers | ||

| High-Performance Computing | ||

| Automotive | ||

| Telecom | ||

| Consumer Electronics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and future size of the HBM thermal management and TIM space?

The HBM thermal management and TIM market was valued at USD 0.31 billion in 2025, stood at USD 0.41 billion in 2026, and is forecast to reach USD 1.71 billion by 2031 at a 32.90% CAGR.

What is driving demand for HBM thermal management and TIM solutions?

The strongest demand driver is the move to higher-power AI accelerators, taller HBM stacks, and more complex advanced packaging, which together raise heat flux and tighten thermal margins inside the package.

Which solution type currently leads revenue?

Thermal Interface Materials led with 53.83% share in 2025 because they remain essential across die attach, package lid, and heatsink interfaces in AI accelerator packages.

Which TIM chemistry is growing the fastest?

Graphene and Carbon-Based TIM is projected to grow at the fastest pace, with a 34.08% CAGR through 2031, as customers evaluate higher-conductivity options for next-generation hot spots.

Which application area is expanding the quickest?

HBM Stack Thermal Interface is expected to record the fastest growth at a 33.88% CAGR through 2031 as thermal control moves deeper into stacked memory structures.

Which region is strongest in this space?

Asia-Pacific led with 64.96% share in 2025 because it concentrates HBM manufacturing and advanced packaging capacity, while North America is projected to grow the fastest at a 33.81% CAGR through 2031.

Page last updated on: