HBM For Network Switching and Packet Processing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

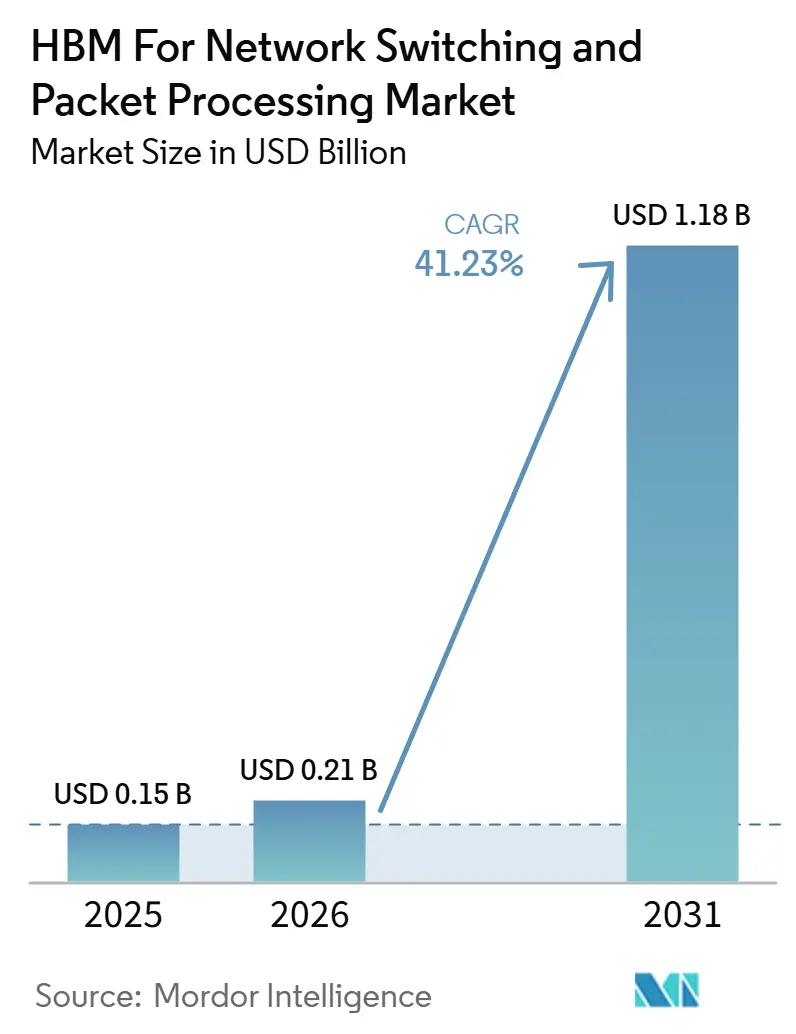

| Market Size (2026) | USD 0.21 Billion |

| Market Size (2031) | USD 1.18 Billion |

| Growth Rate (2026 - 2031) | 41.23% CAGR |

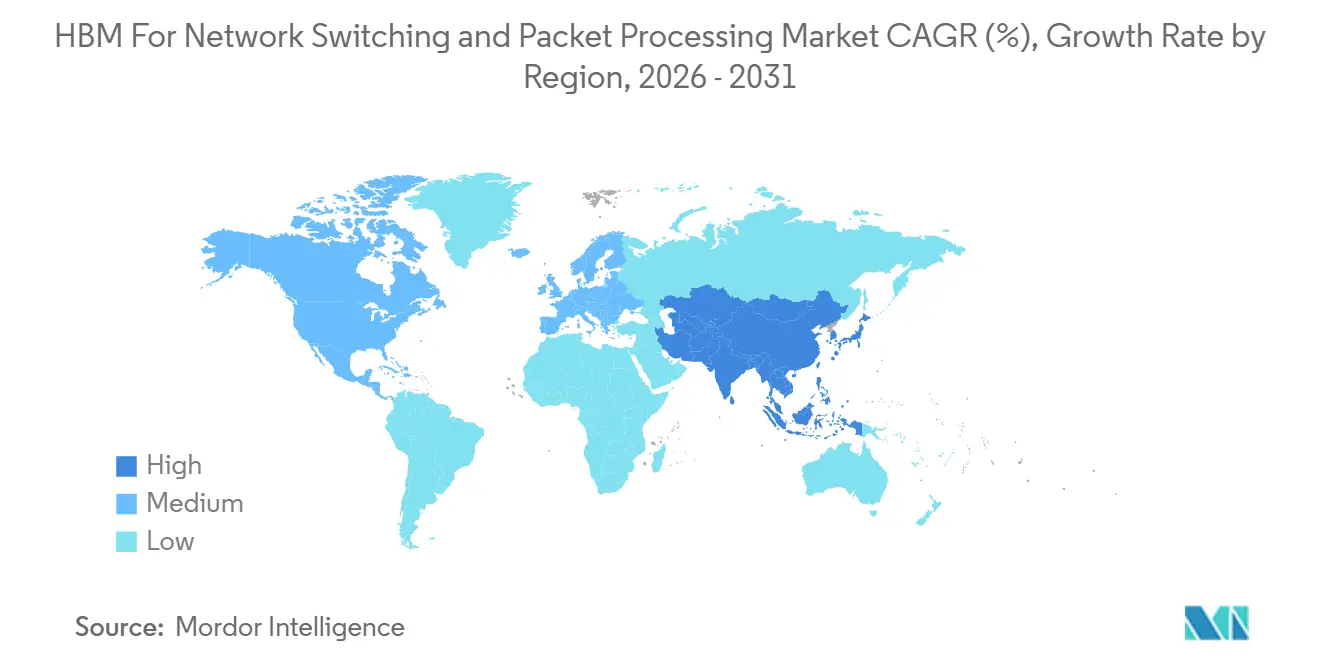

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

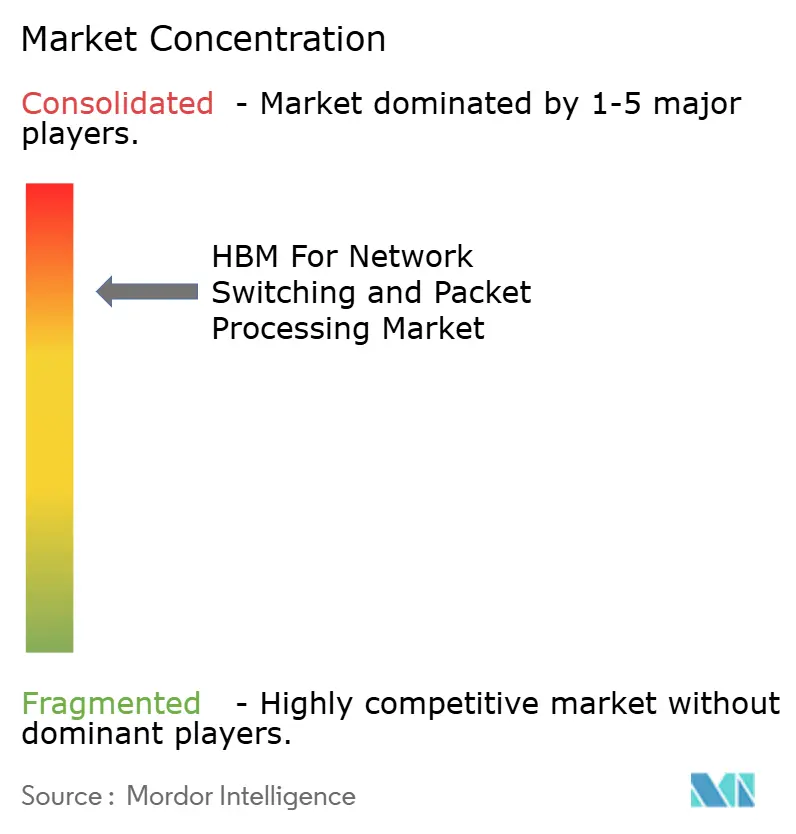

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HBM For Network Switching and Packet Processing Market Analysis by Mordor Intelligence

The HBM for network switching and packet processing market is expected to increase from USD 0.15 billion in 2025 to USD 0.21 billion in 2026, and reach USD 1.18 billion by 2031, growing at a CAGR of 41.23% over 2026-2031. The market is being lifted by sustained AI infrastructure spending because very large training clusters are pushing network devices into a memory-bound design model rather than a simple throughput model. The shift from conventional DDR-based packet buffering to 3D-stacked HBM inside switch ASICs is changing how vendors design platforms for terabit-class traffic, low latency, and power efficiency. Production shipments of 102.4 Tbps switch silicon in 2026 showed that this transition had moved beyond early sampling and into commercial deployment. Multi-year agreements between hyperscalers and silicon vendors are improving long-range demand visibility and giving larger buyers stronger control over supply access. Advanced packaging limits and export compliance requirements still create uneven access for buyers, favoring the largest cloud operators and raising the bar for smaller networking vendors.

Key Report Takeaways

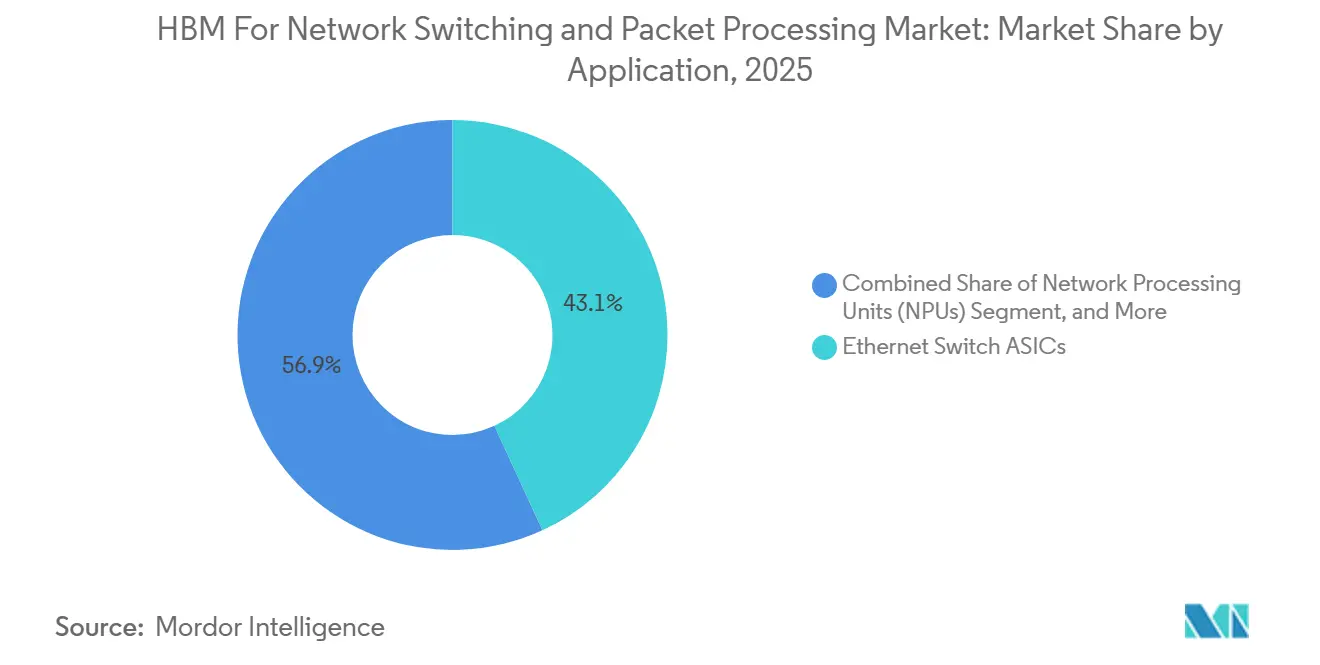

- By application, Ethernet switch ASICs held 43.13% revenue share in 2025, while AI networking fabric switches are projected to expand at a 42.03% CAGR through 2031 in the HBM for network switching and packet processing market.

- By HBM generation, HBM3 commanded a 55.92% share in 2025, while HBM4 is projected to grow at a 42.21% CAGR through 2031 in the HBM for network switching and packet processing market.

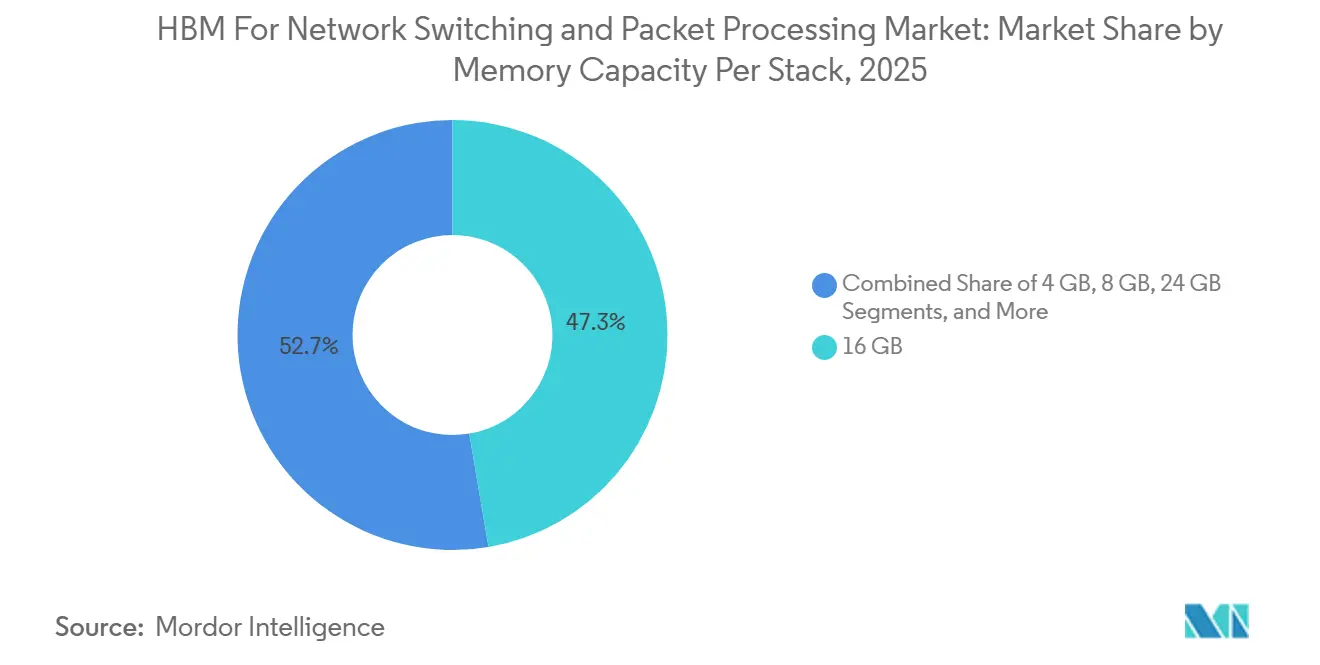

- By memory capacity per stack, 16 GB captured a 47.32% share in 2025, while 32 GB and above is projected to advance at a 42.17% CAGR through 2031 in the HBM for network switching and packet processing market.

- By end-user industry, cloud data centers accounted for 78.03% of demand in 2025, while high-performance computing networks are projected to grow at a 42.09% CAGR through 2031 in the HBM for network switching and packet processing market.

- By geography, North America held 44.68% share in 2025, while Asia-Pacific is projected to expand at a 42.23% CAGR through 2031 in the HBM for network switching and packet processing market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HBM For Network Switching and Packet Processing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising AI Switch ASIC and Packet Buffer Bandwidth Needs | +12.5% | Global, concentrated in North America and Asia-Pacific hyperscale clusters | Short term (≤ 2 years) |

| Co-Packaged HBM Adoption in Terabit-Class Switching Platforms | +9.0% | Global, with packaging centered in Taiwan | Medium term (2-4 years) |

| Hyperscale Data Center Shift Toward Memory-Bound Network Architectures | +8.0% | North America and Asia-Pacific core, with spillover to Europe | Short term (≤ 2 years) |

| 800G and 1.6T Ethernet Rollouts Raising Buffer Depth Needs | +5.5% | Global, with early deployments in North America, then Europe and Asia-Pacific | Medium term (2-4 years) |

| Thermal and Power Efficiency Gains from Near-Compute Memory Integration | +4.0% | Global, with stronger relevance in power-constrained European and Japanese data centers | Medium term (2-4 years) |

| HBM-Rich Edge Networking for Deterministic Telecom Packet Processing | +2.0% | Asia-Pacific and Europe, with spillover to Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising AI-Optimized Switch ASIC and Packet-Buffer Bandwidth Requirements

As AI training clusters moved past 100,000 accelerators, the HBM market for network switching and packet processing was pushed by a clear memory bandwidth limit that conventional on-die SRAM could not address on its own. A January 2026 IEEE paper on the HBM-NS architecture reported 32.1% lower energy use and 55% lower latency than switchless HBM configurations, supporting the case for near-memory switching as a practical network design option. The Themis paper presented at NSDI 2026 found that HBM-based hybrid buffer management improved end-to-end network performance by up to 2.8 times at 400 Gbps port speeds, providing a strong performance case for the HBM network-switching and packet-processing market beyond simple bandwidth claims. The pressure also rises faster than port speed alone suggests, because larger AI clusters create longer congestion events and denser traffic bursts as networks move from 400G to 800G and then toward 1.6T. That pattern is increasing demand for deeper buffer pools and helping higher-capacity HBM configurations gain ground across the HBM market for network switching and packet processing.

Co-Packaged HBM Adoption in Terabit-Class Network Switching Platforms

The HBM for network switching and packet processing market gained an early packaging blueprint when Broadcom introduced the first 51.2 Tbps co-packaged optics Ethernet switch platform in March 2024 with HBM, silicon photonics, and switch logic assembled in one package.[1]Broadcom Inc., “Broadcom Delivers Industry's First 51.2-Tbps Co-Packaged Optics Ethernet Switch Platform for Scalable AI Systems,” Broadcom Investor Relations, investors.broadcom.com Broadcom extended that model in October 2025 with the Tomahawk 6 Davisson at 102.4 Tbps, which doubled the bandwidth of earlier co-packaged switch designs while keeping HBM at the center of the system architecture. Marvell reinforced this direction in June 2026, when it launched the 102.4 Tbps Teralynx T100 with multiple packaging options for AI and cloud data center networking. This co-packaged approach changes the buying unit within the HBM for the network switching and packet processing market, as hyperscalers increasingly evaluate a combined HBM-ASIC package rather than separate memory and switch components. Vendors that can align memory roadmaps, packaging access, and switch silicon schedules earlier are therefore in a better position to capture the largest deployment cycles.

Hyperscale Data Center Migration Toward Memory-Bound Network Architectures

The HBM for network switching and packet processing market is also being shaped by a deeper redesign in hyperscale data centers, where the network fabric is being treated more like a distributed memory layer than a transport-only layer. Google disclosed in 2026 that its Virgo network linked 134,000 TPU chips in a flat two-layer non-blocking topology and delivered up to 47 petabits per second of bisectional bandwidth. A fabric operating at that scale needs much deeper switching buffers and steadier latency behavior across training, inference, and preprocessing workloads, which strengthens the design case for HBM-backed switch silicon in the HBM for network switching and packet processing market. Broadcom’s April 2026 partnership with Meta, which runs through 2029, showed how hyperscalers are moving toward multi-generation infrastructure commitments that combine AI chips and networking platforms under one planning framework. Broadcom’s long-term agreement with Google through 2031 followed the same pattern, indicating that the HBM for the network switching and packet processing market is increasingly tied to large buyers with long supply visibility and roadmap control.

800G and 1.6T Ethernet Rollouts Increasing Buffer Depth and Latency Sensitivity

The HBM for network switching and packet processing market is moving into a faster port-speed cycle as hyperscalers and switch vendors push from 400G into 800G systems and prepare for 1.6T platforms. Marvell said in March 2026 that it had expanded its optical DSP portfolio for the 1.6T era, indicating that the supporting optical stack was already moving toward commercial readiness. Arista followed in June 2026 with its 7060XE7 portfolio for rack-scale AI infrastructure, including a 64-port 1.6T air-cooled system targeted for Q4 2026 production. Higher port speeds create denser packet bursts and make short congestion events harder to absorb, which raises the practical value of larger HBM-backed buffers in the HBM for network switching and packet processing market. As 1.6T systems move closer to deployment, HBM-buffered switch silicon is becoming a baseline expectation rather than a premium design option for the top tier of AI fabrics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Advanced Packaging Capacity for High-Volume HBM Integration | -4.5% | Global, concentrated in Taiwan and major OSAT partners | Short term (≤ 2 years) |

| Export Controls and Qualification Constraints on Advanced DRAM Nodes | -3.0% | Predominantly China and entities with D:5 ultimate parents globally | Medium term (2-4 years) |

| Yield Risk Rising with Higher-Stack HBM Architectures | -2.0% | Global, concentrated in South Korean HBM manufacturing | Short term (≤ 2 years) |

| Tight Coupling to Custom ASIC Roadmaps Slowing Broader Adoption | -1.5% | Global, with strongest effect in enterprise networking and telecom edge | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Advanced Packaging Capacity for High-Volume HBM Integration

The HBM market for network switching and packet processing still depends on advanced packaging capacity that remains tighter than end demand, especially for designs that place HBM and switching logic in a single package. Broadcom’s latest Tomahawk and Jericho platforms, along with Marvell’s Teralynx T100, all point to a design direction that relies on sophisticated packaging rather than stand-alone memory attachment. That creates direct competition for packaging access between networking silicon and AI accelerators, giving the largest buyers and earliest reservers an obvious advantage in the HBM for network switching and packet processing market. Smaller networking vendors, therefore, face a harder path to scale, even when their technical roadmaps are sound and customer demand is present. The result is a two-speed supply environment in which top hyperscalers can move faster, while second-tier OEMs and enterprise-oriented vendors face slower ramp timing.

Export Controls and Qualification Constraints on Advanced DRAM Nodes

Export controls are adding qualification overhead to the HBM for the network switching and packet processing market, especially for vendors that ship advanced systems across several jurisdictions. In May 2026, the Bureau of Industry and Security confirmed that license requirements for advanced computing items continued to apply for entities headquartered in Country Group D:5 and Macau under the relevant export control provisions. That matters because current switch and router roadmaps are tied to advanced HBM generations rather than legacy memory nodes, so compliance now affects core product planning rather than a small edge case. Suppliers and OEMs must review end users, shipment routes, and entity ownership with more care, which adds cost and can lengthen qualification cycles for restricted destinations. Those delays do not stop the HBM for network switching and packet processing market from growing, but they do slow deployment timing and complicate supply-chain execution for global vendors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Ethernet Switch ASICs Lead Revenue While AI Fabric Switches Grow Fastest

Ethernet switch ASICs held 43.13% of the HBM market share for network switching and packet processing in 2025, while AI networking fabric switches are projected to grow at a 42.03% CAGR from 2026 to 2031. That revenue lead reflected years of deployment in hyperscale leaf-spine Ethernet environments, where deep-buffer switching had already become a practical requirement for large east-west traffic loads. Broadcom said Jericho4 delivered 160 times the packet buffer capacity of standard on-chip memory, which explains why deep-buffer Ethernet platforms remained central to high-performance AI network design in 2025 and 2026. At the same time, the HBM for network switching and packet processing market is being pulled toward custom AI fabrics, and NVIDIA’s March 2026 partnership with Marvell, backed by a USD 2 billion investment, has more tightly linked advanced packet management and scale-up networking to HBM-aware designs.[2]NVIDIA Corporation, “NVIDIA and SK hynix Announce Multiyear Technology Partnership to Advance Memory for AI Factories,” NVIDIA Investor Relations, investor.nvidia.com

The next layer of demand comes from interface and packet-processing devices that sit closer to the server, the network edge, or the telecom control plane. Broadcom’s BCM88690 datasheet showed that network processing hardware already used dual HBM Gen2 cubes for a total of 8 GB of packet buffer and supported up to 128,000 programmable queues, which kept NPUs relevant for deterministic traffic handling beyond the largest AI fabrics. That matters for the HBM in the network switching and packet processing industry because it shows that the technology is not limited to top-end switch ASICs and can also support queue-heavy, latency-sensitive packet processing workloads. Over time, application demand is likely to keep widening from the highest-performance switching tier into adjacent devices as memory yields improve, per-bit economics ease, and HBM-backed traffic management becomes easier to justify across more networking functions.

By HBM Generation: HBM3 Holds the Base While HBM4 Sets the Next Ceiling

HBM3 commanded a 55.92% share in 2025, giving it the largest position in the HBM for network switching and packet processing market size by HBM generation, while HBM4 is projected to expand at a 42.21% CAGR through 2031. HBM3 built that lead because Broadcom’s StrataDNX Jericho family and Tomahawk-class systems moved into production across 2024 and 2025, which gave this generation the strongest commercial footing in deployed switching platforms. HBM2 and HBM2E remained in legacy deep-buffer platforms, but their bandwidth-per-pin profile is becoming less suitable as networks move deeper into 400G-and-above switching. Broadcom’s BCM88480 documentation illustrated that earlier HBM Gen2 designs still served installed router systems with 4 GB of in-package buffer memory, which shows why older generations did not disappear immediately, even as newer ones gained share.

The HBM market for network switching and packet processing is now moving toward HBM3E and HBM4, as next-generation switch silicon requires wider interfaces and greater bandwidth per stack. Research from Technion, UC Berkeley, and UC San Diego showed that a router-in-a-package design using 4 HBM4 stacks could deliver 81.92 Tbps of combined switching bandwidth, which highlighted the architectural headroom of the next memory generation. Samsung began HBM4 mass production in February 2026, and NVIDIA and SK Hynix formalized a multiyear technology partnership in June 2026 to advance next-generation memory for AI factories, both of which improved visibility around the future supply base. Those moves support the view that the HBM market for network switching and packet processing will continue shifting toward wider 2,048-bit interfaces and higher per-stack bandwidth as the next switching wave reaches production.

By Memory Capacity Per Stack: 16 GB Anchored the Base While 32 GB and Above Gains Speed

The 16 GB configuration captured 47.32% of the HBM for network switching and packet processing market size in 2025, while configurations of 32 GB and above are projected to grow at a 42.17% CAGR through 2031. That 16 GB position matched the needs of 25.6 Tbps to 51.2 Tbps platforms, where 2 to 4 stacks were enough to support deep buffering without pushing package cost beyond mainstream hyperscale tolerance. The 8 GB tier still fits telecom NPUs and cost-sensitive edge switches, while 24 GB has emerged as a practical middle step between leaf switching and large fabric routing platforms. The 4 GB tier is losing relevance because newer AI traffic patterns can quickly consume shallow buffer pools when both packet bursts and congestion duration rise.

At the high end, 32 GB and above is gaining momentum because HBM4 roadmaps are moving toward 32 GB to 64 GB per stack, and larger AI fabrics need more room to absorb congestion across racks and sites. Micron said its entire 2026 HBM supply was committed under price-and-volume agreements, indicating very strong demand for high-capacity stacks across accelerator and networking deployments. Samsung said its 2026 HBM revenue would more than triple year over year as HBM4 ramps, supporting stronger future availability of taller stacks that can fit high-end networking and compute use cases. This pattern suggests that the HBM for the network switching and packet processing market will continue to shift toward larger buffer pools, as distributed AI networks are making longer, more complex congestion events the norm rather than the exception.

By End-User Industry: Cloud Data Centers Dominate Spending While HPC Networks Grow Fastest

Cloud data centers held 78.03% share in 2025, while high-performance computing networks are projected to expand at a 42.09% CAGR through 2031, making them the fastest-growing end-user group in the HBM for network switching and packet processing market. Cloud spending dominated because the largest buyers were already building clusters with very high accelerator counts, and those environments increasingly relied on 800G Ethernet fabrics and deep-buffer switches to maintain steady performance under mixed AI workloads. The HBM for network switching and packet processing market, therefore, remained closely tied to hyperscale capital cycles, where scale, availability, and roadmap certainty matter as much as raw silicon performance. That balance explains why cloud demand led revenue even while some of the sharpest technical requirements came from smaller but more demanding research and national computing environments.

Government-backed HPC programs were a strong growth signal because the National Nuclear Security Administration awarded USD 18 million to Cornelis Networks in 2025 for next-generation high-performance networking work. Cornelis also announced the CN5000 deployment for the NNSA environment at Lawrence Livermore National Laboratory, demonstrating that deterministic high-speed interconnect performance was moving into real procurement rather than remaining a lab concept. Telecommunications operators formed a second demand stream as 5G standalone core deployments continued to rely on packet processors with rich queue control and deterministic latency behavior, while enterprise and government-defense demand remained smaller but steady. That mix means cloud buyers will likely stay the main source of volume, while HPC will continue to influence the most advanced design requirements within the HBM for network switching and packet processing market.

Geography Analysis

North America held 44.68% of the HBM for the network switching and packet processing market share in 2025. The region led because the United States was home to the largest hyperscale buyers of advanced switch silicon and was the first to adopt high-end HBM-backed networking platforms at scale. Google disclosed in 2026 that its Virgo network linked 134,000 TPU chips in a flat, non-blocking design and delivered up to 47 petabits per second of bisectional bandwidth, reflecting the scale of infrastructure that North American operators were already planning and deploying.[3]Google Cloud, “Introducing Virgo Network Megascale Data Center Fabric,” Google Cloud Blog, cloud.google.com That kind of deployment favors switches with far deeper memory bandwidth and packet buffering than conventional designs can provide, which keeps the HBM for network switching and packet processing market closely aligned with the region’s hyperscale spending cycle. Government demand also supported the regional base after the NNSA backed next-generation networking work with Cornelis Networks for national computing programs.

Europe contributed a meaningful share in 2025, with Germany, the United Kingdom, France, and the Nordic countries hosting major cloud campuses and high-capacity network deployments. The region also benefited from 5G standalone core upgrades, which supported ongoing interest in packet processors and routing systems with richer memory subsystems. National AI programs in the United Kingdom and Germany are helping sustain future data center investment, which should support the gradual uptake of advanced switching silicon over the forecast period. Europe also has a strategic interest in reducing long-term dependence on semiconductor and packaging capabilities, even though Taiwan remains the central packaging hub for HBM in the network switching and packet processing market today.

Asia-Pacific is projected to grow at a 42.23% CAGR through 2031, making it the fastest-growing region in the HBM for network switching and packet processing market. South Korea sits at the center of supply because SK hynix posted record FY25 results, and NVIDIA entered a multiyear technology partnership with SK hynix in June 2026 for next-generation memory used in AI infrastructure. Taiwan remains indispensable because the most advanced AI-focused switch platforms from Broadcom and Marvell rely on package-intensive assembly paths that are deeply linked to the island’s semiconductor ecosystem. India and Southeast Asia are earlier in adoption, but domestic cloud investment is beginning to create future demand for HBM-integrated switching platforms. South America,d the Middle East,t and Africa remain longer-horizon opportunities, where enterprise modernization and government network upgrades are more important near-term drivers than large AI fabric deployments.

Competitive Landscape

The HBM market for network switching and packet processing remained concentrated at the memory supply layer, with Samsung, SK Hynix, and Micron accounting for commercial HBM availability across current generations. Competition was broader at the switch ASIC layer, where Broadcom, Marvell, Cisco, and NVIDIA followed different approaches to buffers, optics, scale-up fabrics, and system-level partnerships. Broadcom reinforced its position when it began shipping Tomahawk 6 in production volume in March 2026, after shipping Jericho4 in August 2025 for distributed AI computing use cases. It also secured long-horizon demand through a Google networking supply assurance agreement through 2031 and an expanded Meta partnership through 2029, which reduced uncertainty around future design wins and supply planning. Marvell responded by launching the Teralynx T100 in June 2026 and tying its roadmap more closely to NVIDIA through the March 2026 NVLink Fusion partnership, which gave it a protected route into AI factory networking programs.

The HBM market for network switching and packet processing still has room to grow in telecom edge and enterprise networking, where fewer vendors offer HBM-integrated packet-processing hardware tailored for deterministic traffic management. Another possible shift is the rise of memory disaggregation through CXL, which could change how future systems balance local packet buffering and shared memory access. Marvell’s March 2026 launch of the Structera S 30260 CXL switch showed that rack-level memory pooling was moving from concept into commercial silicon. If that approach scales, some cost-sensitive tiers may lean less on fully co-packaged HBM and more on shared memory fabrics around the switch system.

On the memory side, supplier relationships are becoming more strategic than transactional in the HBM for network switching and packet processing market. NVIDIA and SK hynix formalized a multiyear technology partnership in June 2026, while Micron said its 2026 HBM supply was fully committed under price-and-volume agreements, both of which signaled that future availability is increasingly tied to long-range commercial commitments.[4]NVIDIA Corporation, “NVIDIA AI Ecosystem Expands as Marvell Joins Forces Through NVLink Fusion,” NVIDIA Investor Relations, investor.nvidia.com Samsung also began HBM4 mass production in 2026, which indicated that the next stack generation was moving from roadmap discussion into actual output. These strategic moves raise the entry barrier, because new challengers must match not only chip performance but also advanced memory access, package readiness, and multi-year supply assurance. That combination leaves the HBM for network switching and packet processing market concentrated in supply, while still allowing active competition for the largest system design wins.

HBM For Network Switching and Packet Processing Industry Leaders

SK hynix Inc.

Samsung Electronics Co., Ltd.

Micron Technology, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: NVIDIA and SK hynix announced a multiyear technology partnership to advance next-generation memory for the global AI factory buildout, covering advanced memory supply and next-generation semiconductor design collaboration aligned to NVIDIA's AI infrastructure roadmap. The agreement formalizes what was previously a deep co-engineering relationship into a contractual supply-and-development commitment.

- June 2026: Marvell Technology launched the Teralynx T100, the industry's first 102.4 Tbps switch silicon purpose-built for the AI era networking, fabricated on a 3 nm process node with multiple packaging configurations, ball grid array, co-packaged copper, and co-packaged optics, and sampling to customers. The T100 directly competes with Broadcom's Tomahawk 6, challenging Broadcom's estimated 80% market share in the highest-bandwidth tier of Ethernet switching ASICs.

- April 2026: Broadcom entered a multi-year, multi-generation strategic partnership with Meta to supply chip and networking technology supporting Meta's Training and Inference Accelerator chips through 2029, with Broadcom's Ethernet-based rack-scale interconnects forming the AI data center network backbone and addressing evolving memory hierarchies.

- April 2026: Broadcom and Google signed a long-term agreement for Broadcom to develop and supply custom tensor processing units and a supply assurance agreement for networking and other components for Google's next-generation AI racks through 2031, a contract that commits HBM-integrated switch silicon roadmaps at hyperscale volumes across a multi-generation timeframe.

Global HBM For Network Switching and Packet Processing Market Report Scope

The HBM for Network Switching and Packet Processing Market is Segmented by Application (Ethernet Switch ASICs, Data Processing Units (DPUs), SmartNICs, Network Processing Units (NPUs), and AI Networking Fabric Switches), HBM Generation (HBM2, HBM2E, HBM3, HBM3E, and HBM4), Memory Capacity Per Stack (4 GB, 8 GB, 16 GB, 24 GB, and 32 GB and Above), End-User Industry (Cloud Data Centers, Telecommunications, Enterprise Networking, Government and Defense, and High-Performance Computing Networks), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Ethernet Switch ASICs |

| Data Processing Units (DPUs) |

| SmartNICs |

| Network Processing Units (NPUs) |

| AI Networking Fabric Switches |

| HBM2 |

| HBM2E |

| HBM3 |

| HBM3E |

| HBM4 |

| 4 GB |

| 8 GB |

| 16 GB |

| 24 GB |

| 32 GB and Above |

| Cloud Data Centers |

| Telecommunications |

| Enterprise Networking |

| Government and Defense |

| High-Performance Computing Networks |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| India | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Application | Ethernet Switch ASICs | |

| Data Processing Units (DPUs) | ||

| SmartNICs | ||

| Network Processing Units (NPUs) | ||

| AI Networking Fabric Switches | ||

| By HBM Generation | HBM2 | |

| HBM2E | ||

| HBM3 | ||

| HBM3E | ||

| HBM4 | ||

| By Memory Capacity Per Stack | 4 GB | |

| 8 GB | ||

| 16 GB | ||

| 24 GB | ||

| 32 GB and Above | ||

| By End-User Industry | Cloud Data Centers | |

| Telecommunications | ||

| Enterprise Networking | ||

| Government and Defense | ||

| High-Performance Computing Networks | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast size of the HBM for network switching and packet processing space?

The HBM for network switching and packet processing market size is expected to rise from USD 0.15 billion in 2025 to USD 0.21 billion in 2026 and reach USD 1.18 billion by 2031, at a 41.23% CAGR.

Which application leads revenue today?

Ethernet switch ASICs led revenue with a 43.13% share in 2025 because they already had a broad installed base in hyperscale Ethernet fabrics.

Which HBM generation is growing fastest?

HBM4 is the fastest-growing HBM generation segment, with a projected 42.21% CAGR through 2031, as next-generation switch silicon moves toward wider interfaces and higher bandwidth per stack.

Why are cloud data centers the main buyers?

Cloud data centers represented 78.03% of demand in 2025 because hyperscalers were the first to build very large AI clusters that needed deep-buffer, low-latency switching platforms.

Which region shows the strongest growth outlook?

Asia-Pacific is projected to grow at a 42.23% CAGR through 2031, supported by South Korea's HBM supply base and Taiwan's role in advanced semiconductor packaging.

What is the biggest supply-side challenge for vendors?

Advanced packaging remains the main near-term constraint because HBM-integrated switch designs compete with AI accelerators for the same package-intensive manufacturing capacity.

Page last updated on: