HBM For HPC and Supercomputing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.76 Billion |

| Market Size (2031) | USD 2.01 Billion |

| Growth Rate (2025 - 2031) | 21.47% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

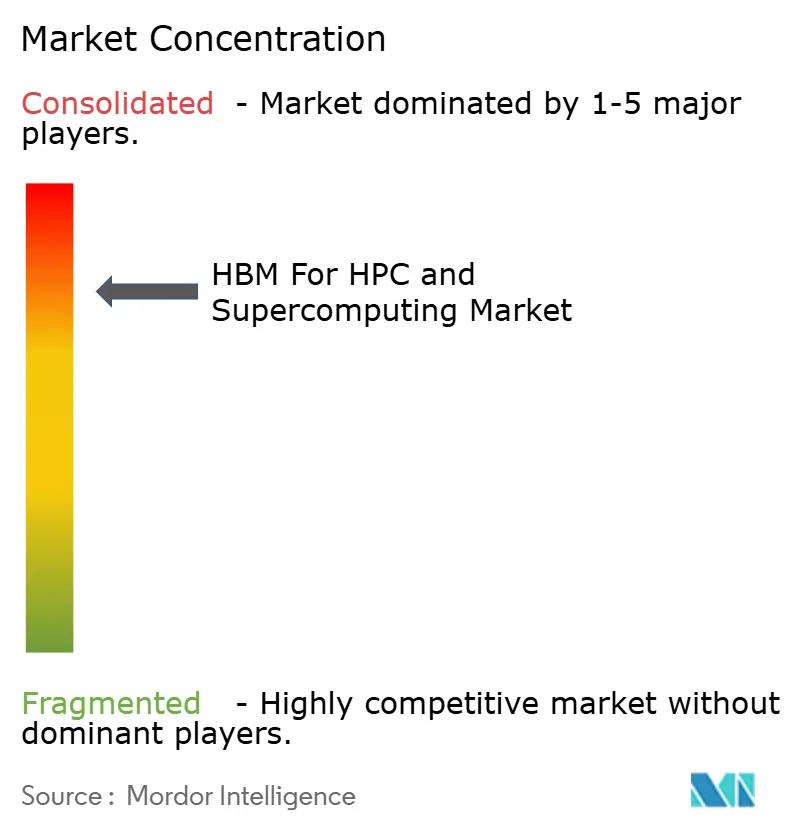

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HBM For HPC and Supercomputing Market Analysis by Mordor Intelligence

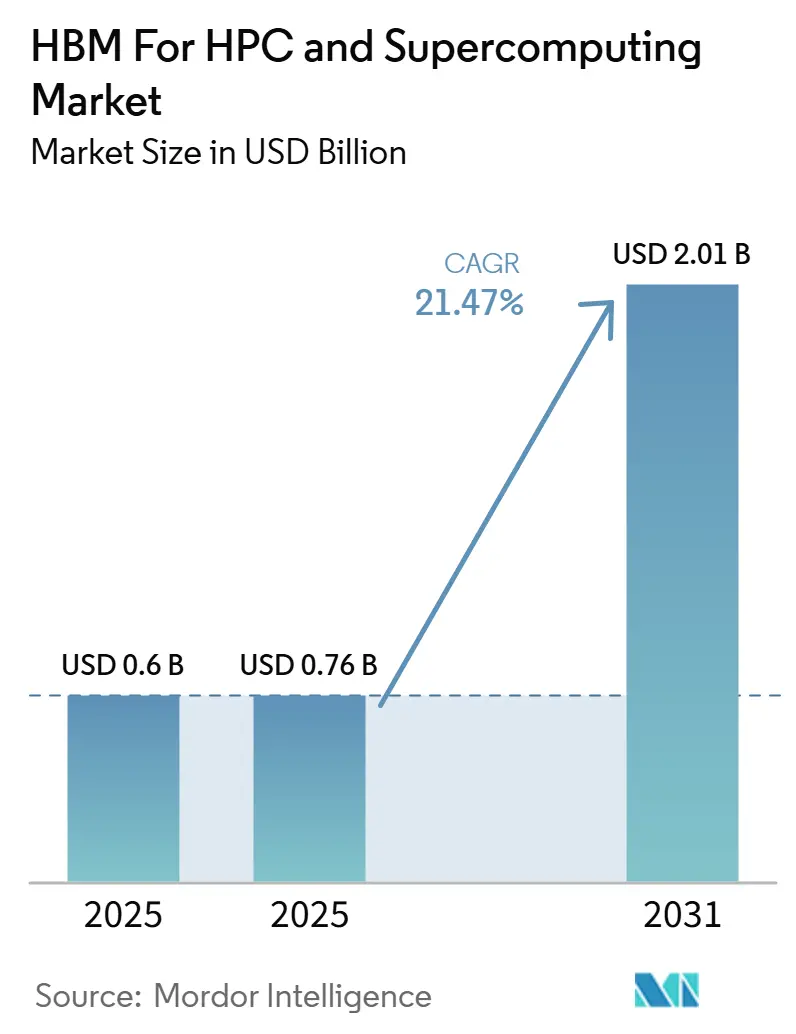

The HBM for HPC and supercomputing market size is expected to increase from USD 0.60 billion in 2025 to USD 0.76 billion in 2026 and reach USD 2.01 billion by 2031, growing at a CAGR of 21.47% over 2026-2031. The market has moved beyond early premium adoption because major exascale and pre-exascale systems deployed since 2024 now use HBM across accelerator nodes and, in some cases, CPU nodes as well. Demand is being shaped by the overlap between large AI training workloads and classical HPC simulation, both of which are pushing conventional DRAM bandwidth limits and increasing the need for stacked memory architectures. Export control rules tied to advanced computing and HBM are also reshaping supply chains and pushing more domestic investment into memory capacity across the United States, South Korea, and Japan. Buying patterns now reflect a mix of national laboratories, hyperscalers, and sovereign compute programs, broadening the demand base and giving the market greater durability through the forecast period. Competition is also shifting from simple qualification to yield, packaging depth, allocation discipline, and thermal performance, which creates clear openings for vendors that can scale newer HBM generations reliably.

Key Report Takeaways

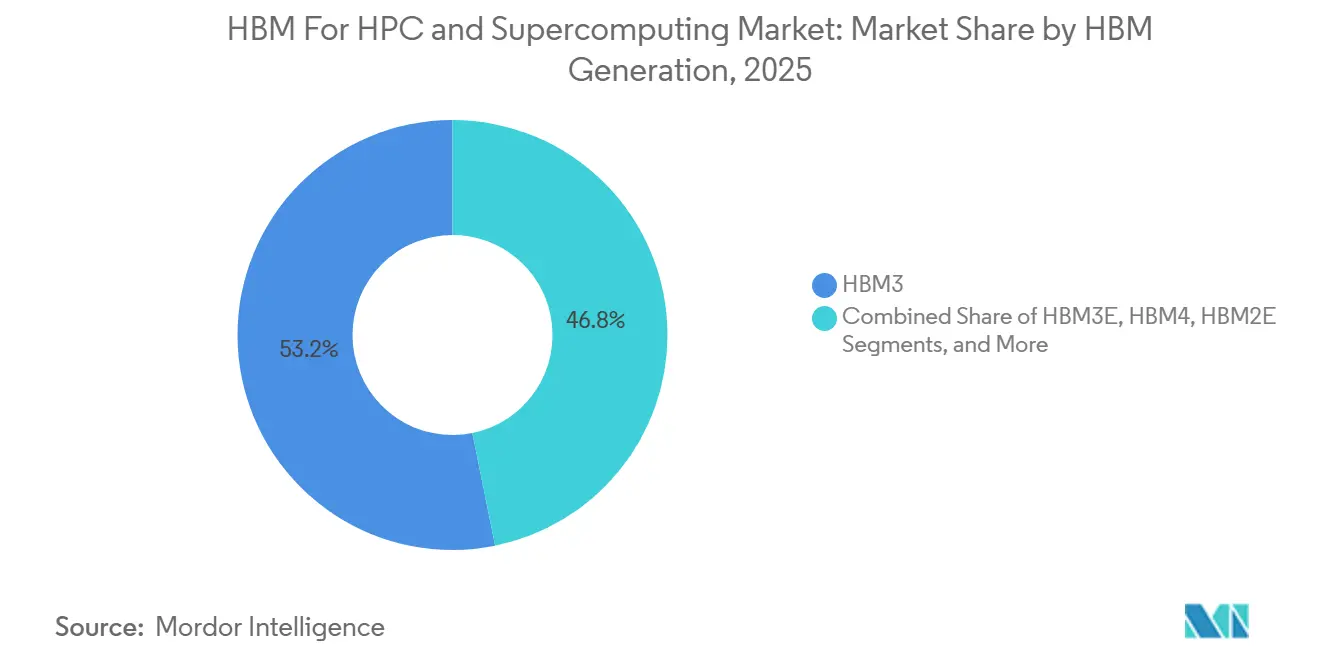

- By HBM generation, HBM3 led with 53.18% revenue share in 2025, while HBM4 is projected to expand at a 22.29% CAGR through 2031 in the HBM for HPC and supercomputing market.

- By memory capacity, 16 GB to 32 GB accounted for 48.63% of the HBM for HPC and supercomputing market in 2025, while capacities above 32 GB are projected to grow at a 22.21% CAGR through 2031.

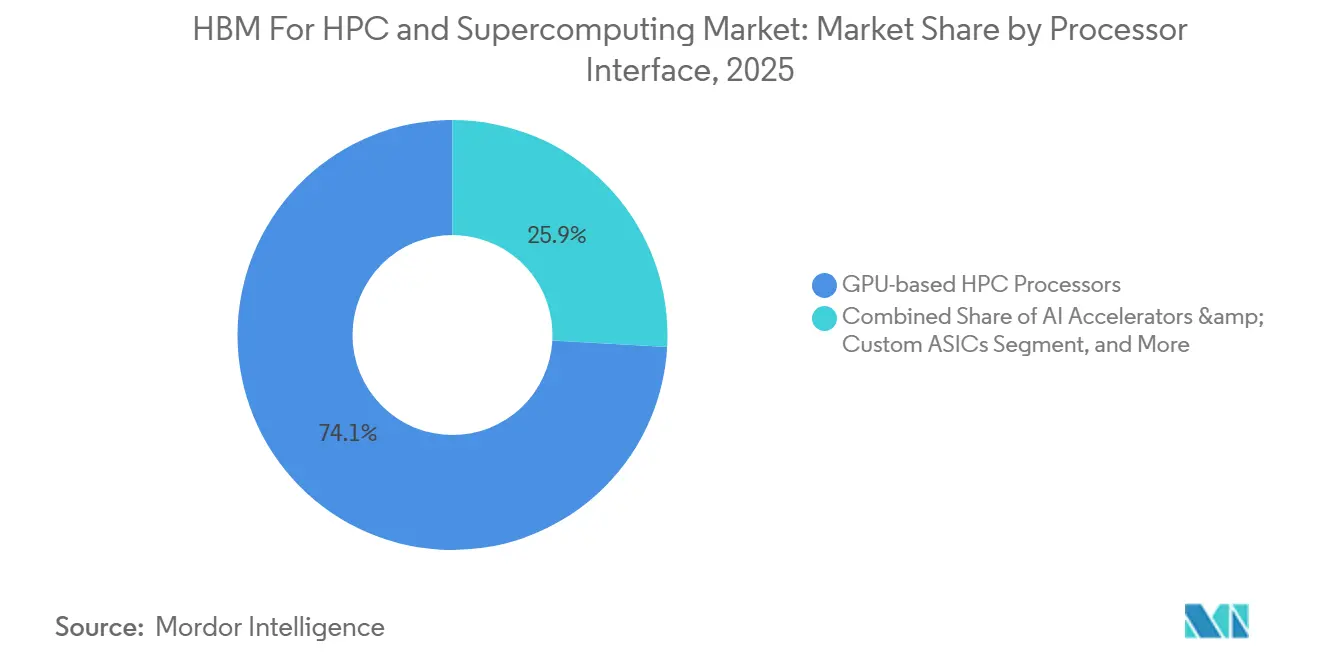

- By processor interface, GPU-based HPC processors held 74.12% of the HBM for HPC and supercomputing market share for HPC and supercomputing in 2025, while AI accelerators and custom ASICs are projected to grow at a 22.08% CAGR through 2031 in the HBM market for HPC and supercomputing.

- By application, scientific computing accounted for 32.76% of the HBM for the HPC and supercomputing market in 2025, while AI-enabled HPC workloads are projected to expand at a 22.48% CAGR through 2031.

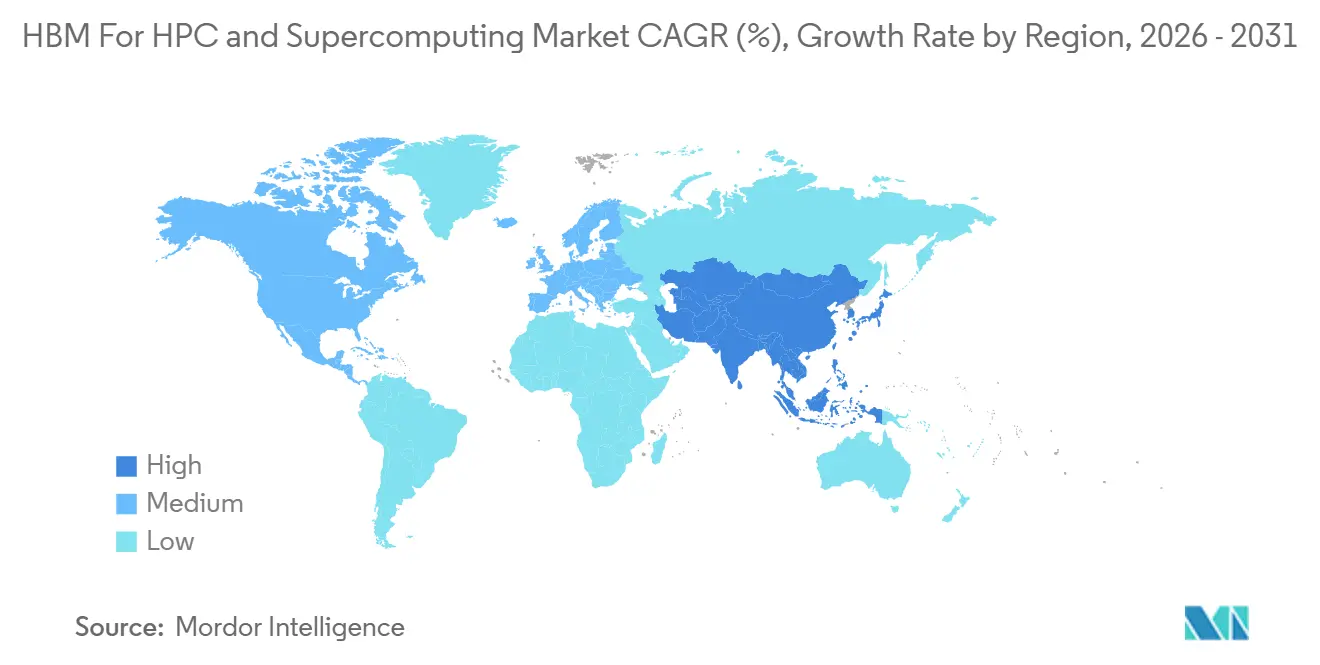

- By geography, North America held 43.39% share in 2025, while Asia-Pacific is projected to grow at a 22.34% CAGR through 2031 in the HBM for HPC and supercomputing market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HBM For HPC and Supercomputing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating AI Training And Supercomputing Demand | +5.5% | Global | Short term (≤ 2 years) |

| HBM3E And HBM4 Adoption In Next-Gen Accelerators | +4.8% | Global, concentrated in North America and Asia-Pacific | Short term (≤ 2 years) |

| Memory-Bound Workloads In HPC Clusters | +3.2% | North America and Europe, extending to Asia-Pacific | Medium term (2-4 years) |

| Co-Packaged Memory Architectures In Exascale Systems | +2.5% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Export-Control-Driven Localization Of Advanced Memory Supply Chains | +2.1% | North America, South Korea, Japan | Medium term (2-4 years) |

| Yield Improvement Through TSV And Advanced Packaging Automation | +1.8% | South Korea, Taiwan, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating AI Training And Supercomputing Demand

The HBM for HPC and supercomputing market is benefiting from the growing overlap between generative AI training and classical simulation, as both workloads now compete for the same memory-intensive compute clusters. SK hynix says the current memory cycle is being led by HBM demand, tying that momentum to the production ramp of platforms that use HBM3E and HBM4 at scale.[1]SK hynix Newsroom, “2026 Market Outlook, Focus On The HBM-Led Memory Supercycle,” SK hynix Inc., news.skhynix.com NVIDIA now positions Vera Rubin for scientific computing as well as AI, with Los Alamos systems such as Mission, Vision, and Veritas set to combine Rubin GPUs with Vera CPUs for open and classified workloads. This broadens the HBM's buyer base in the HPC and supercomputing market beyond commercial cloud into national laboratory and sovereign compute programs. It also means suppliers are serving a demand pool supported by both model training scale and the growing use of AI models in simulation workflows.

HBM3E And HBM4 Adoption In Next-Gen Accelerators

The HBM for HPC and supercomputing market is also being driven by the move from HBM3 to HBM3E and HBM4, as the shift changes both bandwidth and capacity at the platform level. Samsung began HBM4 mass production in February 2026 and said its new stack reaches 11.7 Gbps and 3.3 TB/s per stack, marking a clear performance step over prior generations. NVIDIA says each Vera Rubin R200 GPU features 288 GB of HBM4 and delivers 22 TB/s of memory bandwidth, locking system designers into a new memory generation rather than a minor upgrade path. In the HBM market for HPC and supercomputing, this means procurement timing is increasingly tied to HBM allocation schedules rather than just processor availability. Export rules tied to advanced HBM performance thresholds also narrow the qualified end-user base for the most advanced configurations, reinforcing concentration among approved buyers and supply routes.

Memory-Bound Workloads In HPC Clusters

The HBM for HPC and supercomputing market benefits from a simple hardware problem, because processor throughput has scaled faster than off-chip memory bandwidth in many HPC systems. Research presented at ISC 2025 on Aurora showed that HBM-enabled Intel Xeon Max CPUs outperformed DDR5 alternatives on memory-intensive applications such as HACC and QMCPACK, especially in flat memory mode. Aurora itself uses Intel GPU Max accelerators with 128 GB of HBM and Xeon Max CPUs with 64 GB of HBM on-package, showing that HBM is no longer limited to accelerator-only nodes. In the HBM for HPC and supercomputing market, this widens the memory capacity per server because architects are placing HBM on both the GPU and CPU components of the node. That change supports the faster growth of higher-capacity stacks, especially in the Above 32 GB tier over the forecast period.

Co-Packaged Memory Architectures In Exascale Systems

The HBM market for HPC and supercomputing is being shaped by exascale designs that treat HBM as a co-packaged part of the processor rather than a separate memory choice. Aurora used Intel Foveros 3D integration to place HBM near compute tiles, and NVIDIA now uses NVLink-C2C in Vera Rubin to keep HBM tightly linked to the compute package. This lowers signal latency and power use, but it also makes memory vendors part of chip architecture decisions much earlier in the design cycle. The HBM for HPC and supercomputing market, therefore, favors suppliers that can meet tighter qualification windows and deeper co-design requirements with accelerator makers and system builders. The same pattern is visible in Europe, where Alice Recoque was selected to support climate modeling, digital twins, and energy research with an HBM-centered system design.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited HBM Supply And Long Qualification Cycles | -2.4% | Global | Short term (≤ 2 years) |

| Extreme Dependence On A Few Qualified Memory Suppliers | -1.8% | Global, concentrated risk in South Korea and Japan | Medium term (2-4 years) |

| Thermal Density And Power Integrity Constraints In Dense Stacks | -1.2% | Global | Medium term (2-4 years) |

| High Cost Per Bit Versus Alternative Memory Architectures | -0.9% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited HBM Supply And Long Qualification Cycles

The HBM for HPC and supercomputing market remains constrained by qualification cycles that are much longer than standard DRAM ramps, especially as stack heights rise. Samsung’s own patent work on dummy die structures for future high-stack designs indicates severe yield pressure in 16-layer designs, with reported losses of 40%-60% compared to 8-layer designs. Micron says fiscal 2026 capital expenditure is expected to exceed USD 25 billion, indicating how much spending remains before supply relief becomes meaningful. For the HBM market in HPC and supercomputing, these long cycles translate into configuration lock-in risk, as systems ordered under one memory roadmap may face timing or specification changes before delivery.

Extreme Dependence On A Few Qualified Memory Suppliers

The HBM market for HPC and supercomputing is also limited by its heavy reliance on 3 qualified suppliers: SK hynix, Samsung, and Micron. Shipment data for the first half of 2026 placed SK hynix at 45%, Samsung at 32%, and Micron at 23%, which shows that the entire supply base remains concentrated even after Micron’s faster ramp. Two of these 3 suppliers still rely on primary HBM fabrication in South Korea, which concentrates geopolitical and disruption risk in a narrow area. BIS guidance issued in May 2026 also confirms that advanced computing export controls continue to apply to D:5-linked entities, which keeps supply planning tightly tied to compliance decisions. In the HBM for HPC and supercomputing market, this leaves buyers with limited price leverage, because all 3 qualified vendors have been operating with tight allocation discipline through 2026.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By HBM Generation: HBM4 Ascent Redefines The Generational Mix

HBM3 held 53.18% of the HBM for the HPC and supercomputing market in 2025, reflecting the installed base of Hopper-era systems purchased through 2024 and 2025. HBM2 and HBM2E remained present in legacy clusters, but their roles continued to shrink as operators began upgrading capabilities across flagship systems. HBM3E emerged as the transition layer for HBM in the HPC and supercomputing markets, bridging current deployment cycles with the upcoming move to HBM4. SK hynix says HBM3E will continue to account for a large share of total HBM shipments through 2026, which supports that transition view.[2]SK hynix Newsroom, “2026 Market Outlook, Focus On The HBM-Led Memory Supercycle,” SK hynix Inc., news.skhynix.com

HBM4 is the fastest-growing generation with a 22.29% CAGR from 2026 to 2031, and that rise is tied directly to NVIDIA Vera Rubin and AMD Instinct MI455X configurations. Samsung says its HBM4 mass production uses a 6th-generation 1c DRAM die and can scale from 11.7 Gbps to 13 Gbps, indicating the product line is already being designed for a further speed step. The HBM for HPC and supercomputing industry is therefore moving through a compressed roadmap, because HBM4E samples aimed at 16-layer and 48 GB configurations had already entered customer sampling by mid-2026. In the HBM for HPC and supercomputing market, that compression raises capital planning pressure on integrators, because each generation now has a shorter stable window before the next one enters qualification.

By Memory Capacity: High-Stack Density Accelerates Beyond 32 GB

The 16 GB to 32 GB tier accounted for 48.63% of the HBM market share in the HPC and supercomputing market in 2025, as 8-high HBM3 and HBM3E stacks remained the main volume configuration across leading accelerator platforms. That tier should remain the primary shipment base in the near-term transition, as Blackwell Ultra and comparable systems are still ramping in volume. At the same time, the HBM for the HPC and supercomputing market is shifting toward denser stacks as both performance and total memory per package rise. This keeps the middle tier important in the current cycle, even as buyer attention shifts toward higher densities.

The Above 32 GB band is set to grow at a 22.21% CAGR from 2026 to 2031, driven by designs such as NVIDIA Vera Rubin R200 and AMD MI455X that require much larger per-GPU memory pools. A 2025 peer-reviewed study found that hybrid bonding in 3D-stacked HBM creates increasing thermal and mechanical stress at 12+ layers, which explains why this part of the HBM for the HPC and supercomputing market faces both strong demand and significant process risk. Lower-capacity tiers still matter in the HBM for HPC and supercomputing markets, including edge HPC, FPGA deployments, and embedded simulation systems, where power limits matter more than absolute capacity. Standards compliance also remains important across all tiers, as interoperability decisions must still align with formal HBM interface specifications and packaging rules.

By Processor Interface: GPU Platforms Hold Structural Share As ASICs Accelerate

GPU-based HPC processors held 74.12% of the processor interface segment in 2025, which made them the anchor of the HBM for HPC and supercomputing market. That strength came from NVIDIA’s large installed base and AMD’s growing position in hyperscaler and national lab deployments. The HBM for HPC and supercomputing market still favors GPUs because interposer routing, software maturity, and packaging ecosystems are far more established for this interface path. That advantage gives GPU-linked HBM designs a durable lead even as competing compute approaches expand.

AI accelerators and custom ASICs are projected to grow at a 22.08% CAGR from 2026 to 2031, driven by programs such as Google TPU v7, AWS Trainium, and internal silicon efforts at major cloud providers. This changes the HBM landscape for the HPC and supercomputing industries because hyperscaler ASIC programs now compete directly with traditional HPC buyers for the same HBM4 allocation windows. CPU-based interfaces still hold a secondary but meaningful role, and Aurora shows that clearly through its pairing of Xeon Max CPUs with Intel GPU Max accelerators in the same node design. FPGA-based accelerators remain a niche part of the HBM for HPC and supercomputing market for defense signal processing, weather workflows, and latency-sensitive tasks where timing control matters more than peak throughput.

By Application: Scientific Computing Leads While AI-Enabled Workloads Converge

Scientific computing accounted for 32.76% of the application mix in 2025, keeping it at the center of the HBM for the HPC and supercomputing market. That lead came from long-established codes in molecular dynamics, quantum chemistry, and nuclear simulation that were already tuned for bandwidth-heavy architectures. NVIDIA presented Vera Rubin with workload targets that include fluid dynamics, climate modeling, and quantum chemistry, which shows that scientific use cases still shape product planning in 2026. This preserves a strong core demand base for the HBM in the HPC and supercomputing markets, even as AI receives more attention.

Defense and national security computing remain important for the HBM for HPC and supercomputing market, and Los Alamos is preparing Rubin-based systems under the NNSA Advanced Simulation and Computing program. Weather modeling, climate research, and engineering simulation are also converging, as new national systems are being designed to support digital twins and AI model training in a single compute environment. AI-enabled HPC workloads are set to expand at a 22.48% CAGR through 2031, which makes them the fastest-growing application path in the HBM for HPC and supercomputing industry. The practical change is that inference and training engines are now placed within simulation pipelines, so memory bandwidth must support both numerical models and AI surrogates simultaneously.

Geography Analysis

North America held 43.39% of the HBM market share for the HPC and supercomputing market in 2025, making it the largest regional base for current deployments. The region’s lead reflects the concentration of national laboratories, hyperscalers, and advanced computing procurement programs that already buy memory-rich architectures at scale. Aurora at Argonne and the planned Doudna system at NERSC show how the HBM for the HPC and supercomputing market in North America is tied to very large public computing programs with long buying cycles.[3]Argonne National Laboratory, “Aurora,” Argonne Leadership Computing Facility, alcf.anl.gov Export control rules under ECCN 3A090.c also shape the HBM for the HPC and supercomputing markets in this region, because the most advanced configurations are closely tied to compliance and allied-country access. Demand visibility is therefore stronger in North America than in many other regions, since agencies such as DARPA and NNSA continue to support multiyear compute programs.

Europe remained smaller in 2025, but its role in the HBM for HPC and supercomputing market is rising with new EuroHPC spending. JUPITER in Germany and Alice Recoque in France reflect a clear scale-up in European HBM use, especially for climate research, AI training, and quantum-oriented simulation workloads. HLRS Stuttgart’s HammerHAI and NVIDIA’s broader EuroHPC-linked plans show that the HBM for HPC and supercomputing market in Europe is moving from selective adoption to wider institutional rollout. Data sovereignty and certification requirements also matter more here, which adds a compliance layer to memory sourcing and system design.

Asia-Pacific is projected to grow at a 22.34% CAGR from 2026 to 2031, which makes it the fastest-growing regional part of the HBM for HPC and supercomputing market. The region has a dual role, because it is both the main production base for HBM and a growing demand center for sovereign AI and HPC programs. Samsung and SK hynix announced combined regional investment of KRW 240 trillion (USD 168.8 billion) in July 2026, including Samsung’s KRW 56 trillion (USD 39.4 billion) and SK hynix’s KRW 20 trillion (USD 14.1 billion), which shows how much new capacity and packaging depth are being directed into the supply side. Japan also backed Micron’s Hiroshima expansion with JPY 500 billion (USD 3.3 billion) in support, while the facility investment itself was stated at USD 9.3 billion and is aimed at future HBM shipments around 2028 UPI. China remains smaller by current HBM consumption, but domestic HBM efforts could become a stronger variable over the next 3-4 years if technology gaps narrow and export control workarounds remain contested.

Competitive Landscape

The HBM market for HPC and supercomputing is highly concentrated, as qualified supply still comes from SK hynix, Samsung Electronics, and Micron Technology. Shipment data for the first half of 2026 placed SK hynix at 45%, Samsung at 32%, and Micron at 23%, indicating the HBM market for HPC and supercomputing remains fully controlled by 3 suppliers, even after Micron narrowed the gap. SK hynix has defended its position through technical moves and scale, and its iHBM thermal solution announced in May 2026 reduced thermal resistance by 30% through integrated cooling elements within the HBM package. That move matters in the HBM for HPC and supercomputing market because thermal management is becoming a differentiator as stacks grow taller and racks become denser. It gives SK hynix an advantage that extends beyond supply volume and into system-level operating stability.

Samsung is pursuing a different strategy in the HBM market for HPC and supercomputing, combining memory, foundry, and logic strengths into a broader integrated offering. The company also said HBM4 mass production began in February 2026, which supported its push to raise output and deepen its role in next-generation accelerator programs. Micron is using capital spending and a location strategy to strengthen its position, with fiscal 2026 capital expenditure expected to exceed USD 25 billion, and the Hiroshima expansion reinforcing supply diversity for allied customers.[4]Micron Technology, “Fiscal Year 2026 Capital Expenditure Guidance,” Micron Investor Relations, investors.micron.com These steps show that competition in the HBM for the HPC and supercomputing market is no longer centered solely on first qualification, as the focus has shifted toward yield, production depth, and trusted supply routes.

Demand-side influence is also unusually strong in the HBM for HPC and supercomputing market, because NVIDIA, AMD, Broadcom, and Marvell shape interface requirements, stack configurations, and package choices that effectively pre-screen suppliers. NVIDIA’s Rubin roadmap is especially important because it sets memory capacity and bandwidth targets that suppliers must meet to gain access to the largest near-term accelerator volumes. There is still room for expansion in custom ASIC co-design, CPU-GPU package integration, and thermal management licensing within HBM for the HPC and supercomputing market. Qualcomm’s High Bandwidth Compute approach is one possible alternative path, as it proposes stacked compute and LPDDR to bypass some CoWoS-related supply pressure for inference-heavy workloads. Even so, the present balance of power in the HBM for HPC and supercomputing market remains with the 3 qualified memory vendors and the accelerator companies that define system architecture.

HBM For HPC and Supercomputing Industry Leaders

SK hynix Inc.

Samsung Electronics Co., Ltd.

Micron Technology, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Micron Technology broke ground on a USD 9.3 billion expansion of its Hiroshima, Japan facility, backed by JPY 500 billion (approximately USD 3.3 billion) in METI subsidies, targeting HBM production capacity with shipments expected around summer 2028. The investment positions Micron as Japan's sole DRAM and HBM manufacturer, reducing South Korea's share of allied-nation HBM supply.

- July 2026: Samsung Electronics filed a patent for a new HBM dummy die structure to enhance high-stack reliability, targeting warpage and thermal expansion mismatch in 16-layer HBM5 configurations, addressing yield loss that Samsung's own research estimates at 40%-60% for 16-layer stacks. The filing signals Samsung's preparation for HBM5 production ramp as competition in next-generation HBM intensifies.

- June 2026: NVIDIA announced that all 3 HBM4 vendors, SK hynix, Samsung, and Micron, were fully qualified and in production for the Vera Rubin platform. The shift from SK hynix's prior HBM4 monopoly to a 3-vendor structure moves competitive pressure from qualification to yield, allocation, and pricing.

Global HBM For HPC and Supercomputing Market Report Scope

The HBM for HPC and Supercomputing Market is segmented by HBM Generation (HBM2 and HBM2E, HBM3, HBM3E, and HBM4), Memory Capacity (Up to 8 GB, 8-16 GB, 16-32 GB, and Above 32 GB), Processor Interface (GPU-based HPC Processors, CPU-based HPC Processors, AI Accelerators and Custom ASICs, and FPGA-based Accelerators), Application (Scientific Computing, Weather and Climate Modeling, Defense and National Security Computing, Engineering Simulation and Digital Twins, and AI-enabled HPC Workloads), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| HBM2 and HBM2E |

| HBM3 |

| HBM3E |

| HBM4 |

| Up to 8 GB |

| 8 GB to 16 GB |

| 16 GB to 32 GB |

| Above 32 GB |

| GPU-based HPC Processors |

| CPU-based HPC Processors |

| AI Accelerators and Custom ASICs |

| FPGA-based Accelerators |

| Scientific Computing |

| Weather and Climate Modeling |

| Defense and National Security Computing |

| Engineering Simulation and Digital Twins |

| AI-enabled HPC Workloads |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| India | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By HBM Generation | HBM2 and HBM2E | |

| HBM3 | ||

| HBM3E | ||

| HBM4 | ||

| By Memory Capacity Per Stack | Up to 8 GB | |

| 8 GB to 16 GB | ||

| 16 GB to 32 GB | ||

| Above 32 GB | ||

| By Processor Interface | GPU-based HPC Processors | |

| CPU-based HPC Processors | ||

| AI Accelerators and Custom ASICs | ||

| FPGA-based Accelerators | ||

| By Application | Scientific Computing | |

| Weather and Climate Modeling | ||

| Defense and National Security Computing | ||

| Engineering Simulation and Digital Twins | ||

| AI-enabled HPC Workloads | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the HBM for HPC and supercomputing market size in 2026 and where will it reach by 2031?

The market stands at USD 0.76 billion in 2026 and is forecast to reach USD 2.01 billion by 2031, growing at a 21.47% CAGR over 2026-2031.

Why is HBM becoming a standard choice in exascale computing systems?

Exascale systems need far more memory bandwidth than conventional DRAM can provide, and many new systems now use HBM on GPU nodes and, in some cases, CPU nodes as well.

Which HBM generation is expanding the fastest through 2031?

HBM4 is the fastest-growing generation, with a projected CAGR of 22.29%, supported by NVIDIA Vera Rubin and AMD Instinct MI455X deployments.

Which processor interface currently leads HBM demand in HPC deployments?

GPU-based HPC processors lead with 74.12% share in 2025, mainly because the installed base and packaging ecosystem remain strongest around GPU platforms.

Which region is growing the fastest for HBM use in high performance computing?

Asia-Pacific is the fastest-growing region, with a forecast CAGR of 22.34% from 2026 to 2031, supported by its dual role as a production base and a rising demand center.

What is the main supply-side risk for buyers of HBM-based systems?

The main risk is concentration in 3 qualified suppliers combined with long qualification cycles, which can limit allocation flexibility and raise configuration lock-in risk for buyers.

Page last updated on: