HBM For FPGA Acceleration Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

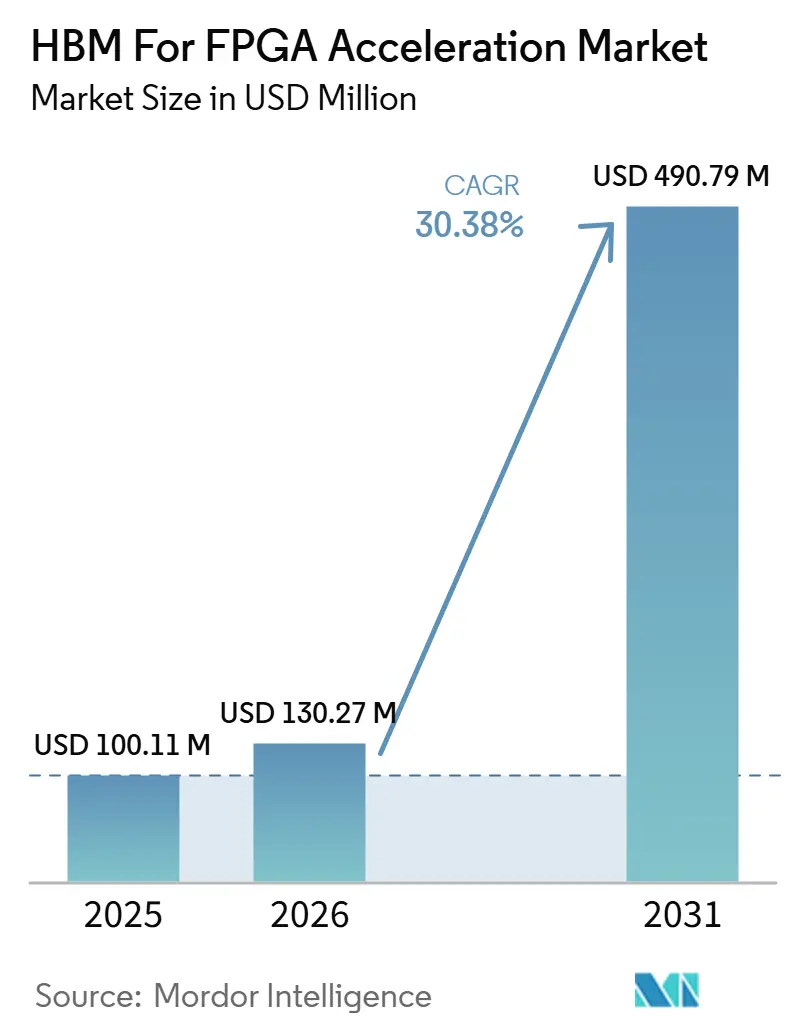

| Market Size (2026) | USD 130.27 Million |

| Market Size (2031) | USD 490.79 Million |

| Growth Rate (2026 - 2031) | 30.38% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HBM For FPGA Acceleration Market Analysis by Mordor Intelligence

The HBM for FPGA acceleration market size is expected to increase from USD 100.11 million in 2025 to USD 130.27 million in 2026 and reach USD 490.79 million by 2031, growing at a CAGR of 30.38% over 2026-2031. Demand is being shaped by workloads in which memory bandwidth and consistent response times matter as much as raw compute power. FPGA platforms paired with HBM are gaining attention in AI inference, packet processing, and low-latency trading because they can keep data movement more predictable within tight power limits. Product strategy is also shifting toward vendors that can secure packaging capacity, memory supply, and early-cycle design wins. HBM3E availability, open accelerator module designs, and hyperscaler interest are widening the range of deployments that can support the HBM for FPGA acceleration market over the next 5 years. High co-packaging cost, thermal design pressure, and limited packaging flexibility still keep broader rollout measured outside the highest-value use cases.

Key Report Takeaways

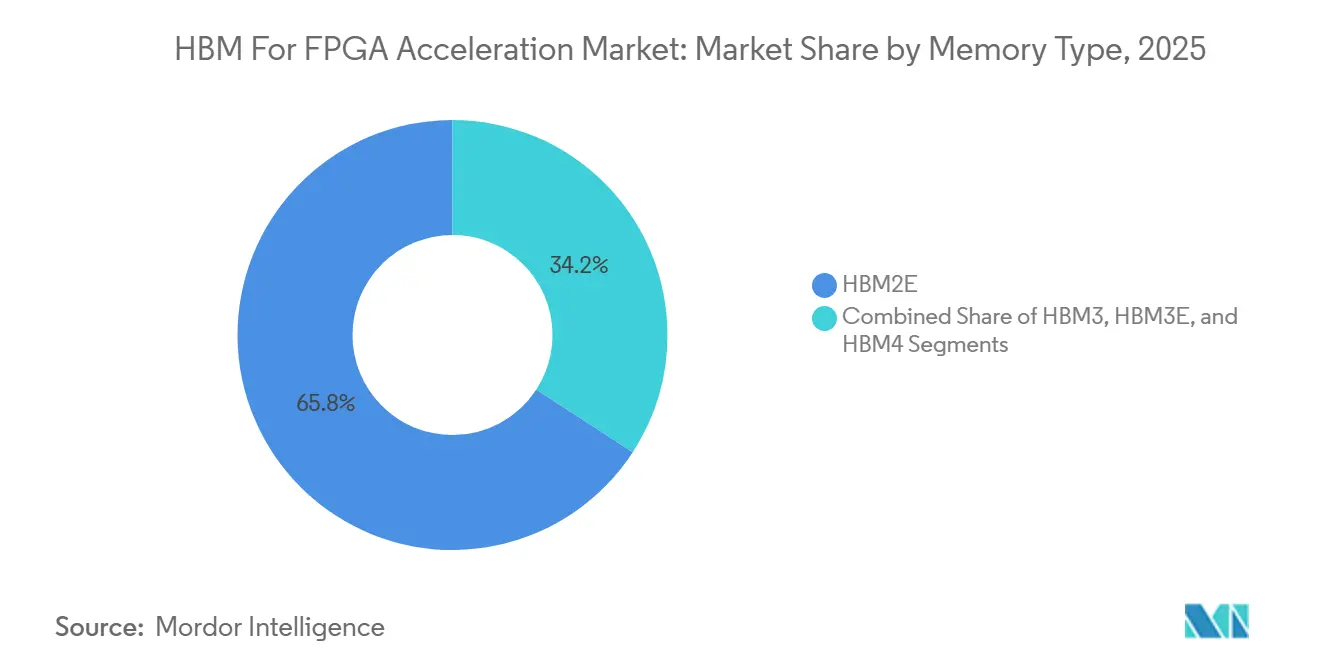

- By memory type, HBM2E held 65.83% of the market in 2025, while HBM3E is projected to expand at a 31.18% CAGR through 2031 in the HBM for FPGA acceleration market.

- By FPGA integration type, Standalone FPGA Accelerator Cards with HBM held 53.18% of the market in 2025, while OCP/OAM FPGA Accelerator Modules are projected to expand at a 31.08% CAGR through 2031 in the HBM for FPGA acceleration market.

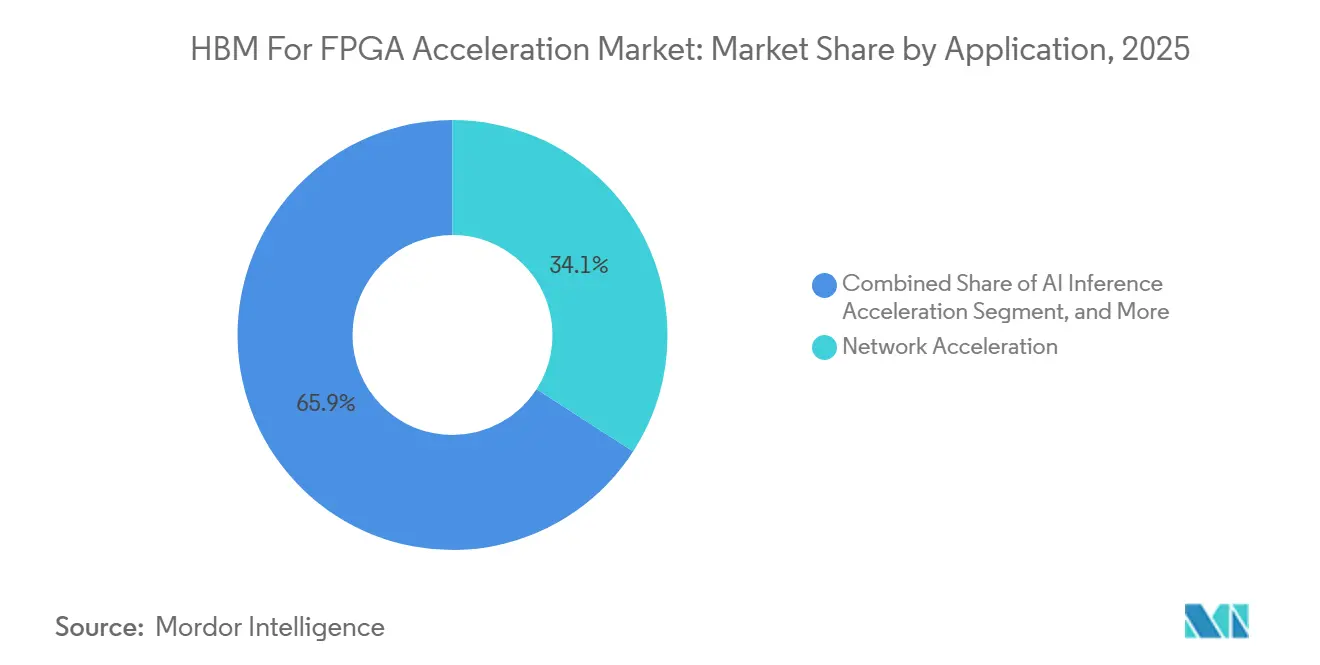

- By application, Network Acceleration accounted for 34.12% of the HBM for FPGA acceleration market size in 2025, while AI Inference Acceleration is projected to grow at a 31.58% CAGR through 2031 in the HBM for FPGA acceleration market.

- By end user, Hyperscalers and Cloud Service Providers held 41.76% of the HBM for FPGA acceleration market share in 2025 and are projected to expand at a 31.49% CAGR through 2031in the HBM for FPGA acceleration market.

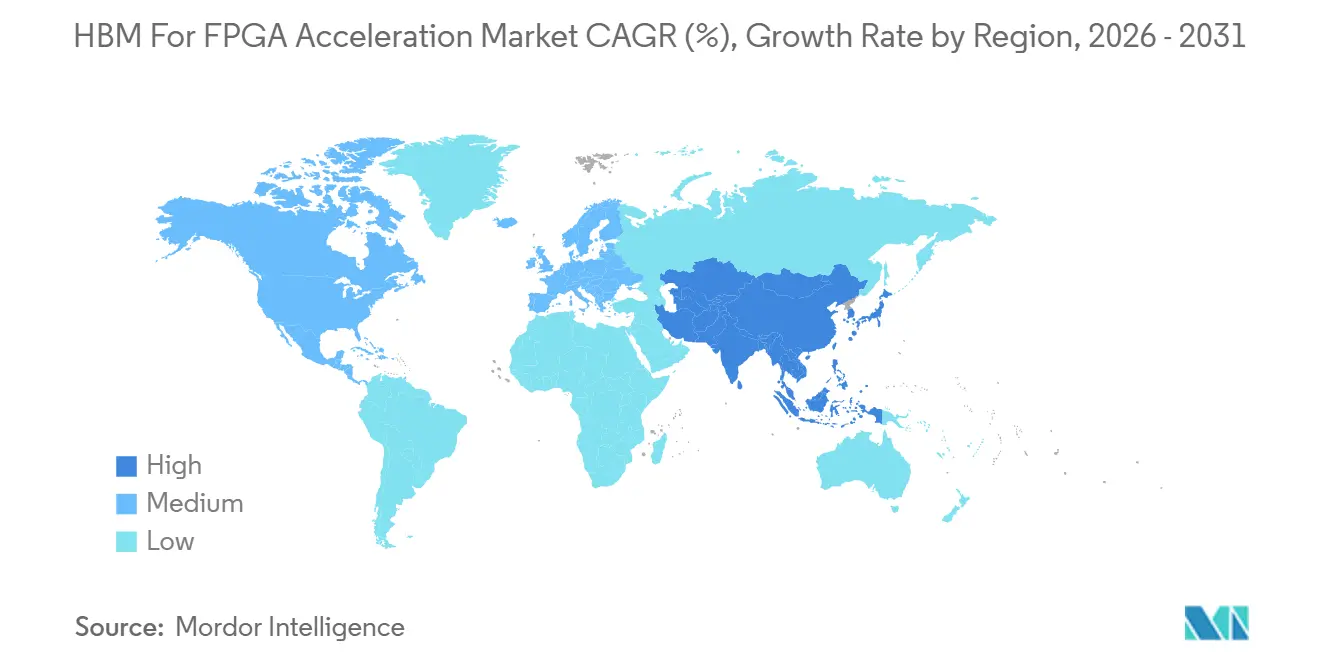

- By geography, North America held 44.94% of the market in 2025, while Asia-Pacific is projected to record the highest CAGR at 31.36% through 2031 in the HBM for FPGA acceleration market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HBM For FPGA Acceleration Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Deployment of HBM-Enabled FPGA Cards in Cloud and Edge Accelerators | +9.2% | Global | Short term (≤ 2 years) |

| Growing Need for Deterministic, Low-Latency Memory Access in Real-Time Workloads | +5.5% | North America and Europe | Short term (≤ 2 years) |

| Hyperscaler Shift Toward FPGA-Based Custom Acceleration for Select Workloads | +5.0% | North America | Medium term (2-4 years) |

| Wider Availability of HBM3 and HBM3E in High-End FPGA Platforms | +4.5% | Global, with early gains in Asia-Pacific supply chain | Medium term (2-4 years) |

| Increasing Importance of Power-Efficient Bandwidth Scaling vs Pure Compute Scaling | +3.0% | Global | Long term (≥ 4 years) |

| Co-Optimization of FPGA and HBM in Heterogeneous AI Inference Pipelines | +2.0% | North America and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Deployment of HBM-Enabled FPGA Cards in Cloud and Edge Accelerators

Cloud and edge systems are moving toward denser data paths, and that shift is making DDR-based FPGA designs less attractive in the most bandwidth-heavy environments. DYNANIC and Silicom demonstrated a 400G FPGA-based AI networking setup in September 2025 that paired Altera Agilex 7 M-Series silicon with HBM2e for low-latency packet handling in AI fabrics.[1]Dynanic, “DYNANIC and Silicom Showcase 400G FPGA-Based AI Networking at Altera Innovators Day 2025,” DYNANIC, dyna-nic.com Silicom’s ThunderFjord card demonstrated how an HBM-equipped board can support up to 32GB of HBM2e and 2 × 2.6Tbps of bandwidth in a form factor designed for high-speed data center networking. Altera also positions the Agilex family for data center acceleration use cases that need programmable logic, high memory throughput, and deployment flexibility across cloud infrastructure. This makes the HBM for FPGA acceleration market more dependent on card and module vendors that can package complete solutions rather than only supply chips. It also means that design wins in networking and inference can carry over into adjacent edge applications that require similar bandwidth behavior.

Growing Need for Deterministic, Low-Latency Memory Access in Real-Time Workloads

The HBM for FPGA acceleration market is benefiting from workloads that value timing consistency as much as throughput. In FPGA-based designs, memory channels can be assigned in hardware, which helps keep response behavior more predictable than in shared compute environments. AMD stated that its Alveo UL3422 accelerator achieved latency below 3 ns for electronic trading workloads, demonstrating that FPGA-based acceleration still plays a strong role in extremely low-latency settings. A 2025 arXiv paper on the RoCE BALBOA stack also showed direct HBM channel use for payload staging on data center FPGAs, achieving 100G throughput comparable to commercial NICs. The addressable demand base is therefore widening beyond classic trading applications into AI fabric control, packet inspection, and other services where jitter can hurt system performance. As these use cases expand, the HBM for FPGA acceleration market gains support from buyers willing to pay more for consistent timing behavior.

Hyperscaler Shift Toward FPGA-Based Custom Acceleration for Select Workloads

Hyperscalers are increasingly separating broad AI tasks from narrow tasks that need lower latency, tailored logic, or tighter power control. Altera’s data center positioning reflects this shift by placing FPGAs into AI networking, infrastructure offload, and scalable accelerator platforms rather than trying to replace every GPU deployment. In March 2026, Altera expanded its collaboration with Arm to connect HBM-equipped FPGAs with the Arm Neoverse CSS V3 AGI CPU for AI data center systems. That move matters because it supports mixed compute architectures in which FPGAs can run narrow, data-intensive jobs within a broader rack design. The HBM for FPGA acceleration market is likely to benefit as hyperscalers standardize around platforms that can host several accelerator types without a full infrastructure redesign. This also raises the value of vendors that can align silicon, software, and module design with hyperscaler operating models.

Wider Availability of HBM3 and HBM3E in High-End FPGA Platforms

The HBM for FPGA acceleration market is also gaining from the faster memory roadmap, now moving across the wider AI hardware supply chain. Siemens noted that per-pin data rates have advanced from HBM2E to HBM3E and HBM4, thereby materially expanding the memory bandwidth available to advanced accelerator packages. SK hynix said HBM3E was expected to account for nearly two-thirds of total HBM shipments in 2026, indicating that supply is entering a new volume phase. Samsung reported the world's first HBM4 mass-production shipment in February 2026, while Micron said its HBM4 shipments reached more than 11 Gbps per pin and over 2.8 TB/s bandwidth for next-generation AI systems. Better memory availability does not eliminate all supply pressure, but it increases the likelihood that future FPGA platforms can move beyond the current HBM2E-heavy installed base. This supports longer product planning and provides the FPGA-acceleration market for HBM a stronger path into higher-end inference and networking platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Advanced Packaging Capacity for FPGA-HBM Integration | -3.8% | Global, concentrated in Taiwan and South Korea | Short term (≤ 2 years) |

| High Bill-of-Materials Cost Compared with GDDR- and DDR-Based FPGA Designs | -2.5% | Global | Medium term (2-4 years) |

| Thermal and Board-Level Design Complexity in HBM-Enabled Accelerator Systems | -1.8% | Global | Long term (≥ 4 years) |

| Supply Concentration in HBM Manufacturing and Interposer Ecosystems | -1.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Advanced Packaging Capacity for FPGA-HBM Integration

The HBM for FPGA acceleration market still depends on advanced packaging flows that are harder to scale than standard board-level memory designs. HBM integration requires close coupling between the compute die, the memory stack, and the interconnect structure, so product timing can be affected by packaging availability even when logic demand is strong. AMD announced more than USD 10 billion in investments in Taiwan's ecosystem in May 2026 to expand advanced packaging manufacturing for AI infrastructure, underscoring how central packaging capacity has become across accelerator supply chains. Samsung’s HBM4 ramp and Micron’s HBM4 production progress also show that memory and packaging readiness now move together rather than as separate procurement steps. For FPGA vendors, this raises the importance of early planning and narrows the room for short-cycle volume expansion. The result is a market where qualified supply can remain tighter than end-user interest for longer periods.

High Bill-of-Materials Cost Compared With GDDR- and DDR-Based FPGA Designs

High system costs remain a real limit on broader deployment in the HBM-based FPGA acceleration market. HBM improves bandwidth density, but it also adds cost through memory stacking, package complexity, power delivery, and thermal management. Achronix has positioned its Speedster7t family as offering memory bandwidth comparable to HBM-based FPGA products at a fraction of the cost, underscoring the importance of price as a key point of competition. That message resonates with enterprise OEMs and system integrators that often need high throughput but not the highest memory density. Cost pressure is therefore pushing some buyers toward lower-priced alternatives until HBM-equipped designs show a clearer return on system value. This slows adoption among second-wave customer groups even as top-tier hyperscale and networking deployments continue to move forward.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Memory Type: HBM2E Leads the Installed Base While HBM3E Gains the Strongest Momentum

HBM2E held 65.83% of the HBM for FPGA acceleration market share in 2025, reflecting the strength of current installed platforms and the slower replacement cycle for qualified accelerator designs. Altera’s Agilex 7 M-Series integrates up to 32GB of HBM2e in a single device and provides up to 820GB/s of peak bandwidth, helping make HBM2E the practical baseline for shipping products.[2]Altera, “HBM2E (High-Bandwidth Memory) FPGA IP,” Altera, altera.com Source: Altera, “Data Center Solution,” Altera, altera.com That installed base matters because buyers in network, telecom, and infrastructure roles often keep the same hardware generation in service longer than hyperscale compute buyers. HBM3 remained a bridge tier in the segment because supply and platform planning moved quickly toward the next step in the memory roadmap. HBM3E is projected to grow at a 31.18% CAGR through 2031, reflecting stronger supplier focus, higher data rates, and better alignment with next-wave accelerator requirements.

JEDEC’s JESD235 standard family continues to support interoperability across HBM generations and helps shorten qualification work when vendors move between memory sources within shared design rules. Siemens said HBM3E has entered high-volume production across the AI accelerator ecosystem, and it also pointed to custom HBM4 base-die approaches as a future area of product differentiation. Samsung’s HBM4 shipment milestone and Micron’s HBM4 production progress show that the memory roadmap is moving faster than many FPGA product cycles, potentially shifting value toward vendors with stronger transition planning. The near-term HBM for FPGA acceleration market still centers on HBM2E shipments, but future platform roadmaps are increasingly being shaped by HBM3E readiness and the first HBM4 design paths.

By FPGA Integration Type: Standalone Cards Hold the Base While OAM Modules Expand the Fastest

Standalone FPGA Accelerator Cards with HBM held 53.18% of the HBM for FPGA acceleration market share in 2025, reflecting the maturity of PCIe-based deployment in enterprise and colocation environments. Card-based designs remain easier to qualify, easier to swap into existing servers, and easier for board partners to tailor around specific workloads. Silicom’s ThunderFjord product shows how current card designs can package HBM2e, high port throughput, and data center networking features into a familiar accelerator format. This is why standalone cards still anchor the commercial base of the HBM for FPGA acceleration market, even as newer module formats gather attention. PCIe card deployments also fit the procurement style of system integrators that need incremental upgrades rather than full rack redesigns.

OCP/OAM FPGA Accelerator Modules are projected to expand at 31.08% CAGR through 2031 as hyperscaler environments shift toward shared chassis and more flexible accelerator pools. Altera’s data center positioning supports this path by aligning programmable acceleration with rack-scale AI systems and open module deployment models. The March 2026 Altera and Arm collaboration also points to tightly integrated systems in which CPU, FPGA, and memory resources are planned together from the start. FPGA SoCs with integrated HBM and smaller PCIe modules will remain important in select designs, but the long-term direction for HBM in the FPGA acceleration market is toward module-based deployment in larger AI and networking fabrics.

By Application: Network Acceleration Sets the Current Revenue Base While AI Inference Lifts Future Demand

Network Acceleration accounted for 34.12% of the HBM for FPGA acceleration market in 2025, making it the largest application segment in the current revenue mix. That lead came from data center networking, packet inspection, SmartNIC functions, and AI cluster interconnect tasks that value steady data movement under load. DYNANIC and Silicom demonstrated how HBM-equipped FPGA hardware can support 400G AI networking use cases with low-latency packet processing, which reinforces the strength of this application base. Buyers in this segment are not only chasing throughput; they also need deterministic behavior to keep fabric performance stable across many nodes. This keeps network acceleration at the center of current HBM platform deployments.

AI Inference Acceleration is projected to grow at a 31.58% CAGR through 2031, reflecting the rising need for programmable, low-latency inference in specialized model-serving settings. Altera’s current data center messaging and its Arm collaboration both place programmable acceleration at the center of AI infrastructure roadmaps rather than treating it as a separate niche. Financial services remain a smaller-volume segment, but AMD’s below-3ns trading performance shows that low-latency applications still define the premium end of the HBM for the FPGA-acceleration market. Defense, aerospace, scientific simulation, and high-performance computing continue to support demand where reprogrammability, secure data flow, and bandwidth density matter more than lowest-cost deployment. Over time, the line between HPC and inference will continue to narrow as both are increasingly relying on memory-rich accelerator designs for targeted workloads.

By End User: Hyperscalers and Cloud Providers Shape Both Today’s Scale and Tomorrow’s Expansion

Hyperscalers and Cloud Service Providers held 41.76% share of the HBM for FPGA acceleration market in 2025, and they are projected to grow at 31.49% CAGR through 2031. This dual position shows that the largest buyers are also setting the pace for future platform choices, qualification schedules, and supply planning. Altera’s data center strategy is clearly aligned with this group through AI infrastructure, programmable networking, and support for accelerator modules. The Altera and Arm collaboration further supports hyperscale deployment patterns by linking HBM-equipped FPGAs with server-class CPU architecture for scalable AI systems. As a result, the HBM for FPGA acceleration market is being shaped by a buyer group that can influence both product design and upstream supply commitments.

Enterprise OEMs and system integrators remain the next important customer layer because they carry HBM-enabled platforms into medical imaging, telecom, industrial processing, and embedded compute systems. Their adoption path is slower because qualification cycles are longer and cost control is stricter than in hyperscale environments. Telecom and networking operators continue to support the HBM for FPGA acceleration industry through packet core, network offload, and infrastructure timing use cases that need both programmability and bandwidth. Financial institutions stay important at the premium end because they value latency behavior over volume, while research laboratories help test next-generation memory combinations before wider commercial rollout. This creates a demand structure in which a few large cloud buyers drive scale, while several smaller end-user groups preserve diversity in product requirements.

Geography Analysis

North America held 44.94% of the HBM for FPGA acceleration market share in 2025, making it the largest regional contributor to current revenue. The region benefits from a dense concentration of FPGA design teams, AI infrastructure spending, and system-level integration capabilities. Altera’s data center positioning and its collaboration with Arm both reinforce North America’s role as a base for programmable acceleration in AI server environments. AMD’s May 2026 commitment of more than USD 10 billion across the Taiwan ecosystem also reflected how North American accelerator demand is directly linked to upstream packaging and memory capacity in Asia. Financial services and low-latency infrastructure deployments add a premium demand layer in the United States, supporting continued use of FPGA-based acceleration for specialized workloads.

Asia-Pacific is projected to expand at a 31.36% CAGR through 2031, making it the fastest-growing geography in the HBM for FPGA acceleration market. The region combines memory manufacturing, deep packaging, electronics production, and rising AI data center demand within a single broad supply ecosystem. SK hynix said HBM3E was expected to account for nearly two-thirds of total HBM shipments in 2026, and Samsung reported HBM4 mass production shipment in February 2026, both of which underline South Korea’s importance in supply availability.[3]SK hynix, “2026 Market Outlook, SK hynix’s HBM to Fuel AI Memory Boom,” SK hynix, skhynix.com Micron’s progress in HBM4 production also strengthens Asia-Pacific’s role in the next stage of memory supply for advanced accelerator platforms. Taiwan remains critical because advanced packaging capacity there affects how quickly HBM-enabled systems can move from design to commercial shipment. Japan’s focus on semiconductor capacity and its role in memory expansion further support the region’s long-term weight in the HBM for FPGA acceleration market.

Europe, South America, and Middle East and Africa together account for a smaller share of current revenue, but each remains relevant for selected deployment paths. Europe matters most for defense, telecom, and industrial electronics applications, where programmability and secure processing remain important. The EU Chips Act commitment of EUR 43 billion (USD 48.6 billion) through 2030 could improve regional semiconductor capabilities over time, even though dependence on advanced packaging remains high today. South America, the Middle East, and Africa are still early-stage opportunities, and growth there is more closely tied to broader cloud investment and sovereign AI buildouts than to immediate HBM platform volume. These regions, therefore, contribute less to current sales, but they still expand the future opportunity set for HBM in the FPGA acceleration market.

Competitive Landscape

The HBM for FPGA acceleration market has a concentrated structure because only a small group of companies participate meaningfully across silicon, memory, packaging, and finished accelerator hardware. Altera holds a strong position in active HBM-enabled FPGA platforms through its Agilex 7 M-Series lineup and its broader data center push around AI infrastructure and programmable acceleration. One clear strategic move came in March 2026, when Altera expanded its collaboration with Arm to pair HBM-equipped FPGAs with the Arm Neoverse CSS V3 AGI CPU for AI data centers. That move supports tighter integration with hyperscale system architecture and raises the value of platform-level design alignment. Board partners such as Silicom and DYNANIC add another layer of competition by packaging those capabilities into deployable networking and accelerator products.[4]Dynanic, “DYNANIC and Silicom Showcase 400G FPGA-Based AI Networking at Altera Innovators Day 2025,” DYNANIC, dyna-nic.com

Achronix competes differently by emphasizing GDDR6-based products that aim to deliver high memory bandwidth without the full cost burden of HBM. Its Speedster7t positioning makes cost discipline a direct competitive lever, especially for buyers that need strong throughput but not the densest memory package available. This gives the HBM for FPGA acceleration market a clear split between premium HBM designs and lower-cost alternatives that serve adjacent demand. Competitive success, therefore, depends not only on raw bandwidth but also on whether vendors can match system cost to workload value. The balance of power is strongest in applications where memory density and deterministic behavior are hard to replace with standard board-level memory.

Memory suppliers are also central to competition because every platform roadmap depends on what SK hynix, Samsung, and Micron can deliver at the right time and generation. SK hynix’s shipment outlook for HBM3E, Samsung’s HBM4 production milestone, and Micron’s HBM4 launch each represent strategic moves that shape the technical ceiling for future FPGA accelerator designs. AMD’s more than USD 10 billion investment in Taiwan's ecosystem in 2026 was another strategic move because it directly targeted advanced packaging scale, which affects the wider accelerator supply environment FPGA vendors rely on. The HBM for FPGA acceleration market is therefore competitive, but not broad, because a narrow set of companies controls the most important supply and platform decisions. This structure favors firms with strong ecosystem ties, early access to memory, and clear deployment pathways into AI networking and inference systems.

HBM For FPGA Acceleration Industry Leaders

SK hynix Inc.

Samsung Electronics Co., Ltd.

Micron Technology, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: AMD announced more than USD 10 billion in investments across the Taiwan ecosystem to scale advanced packaging manufacturing for its Helios rack-scale AI platform, including HBM4 supply from Samsung for the Instinct MI450X GPU. The program indirectly scales CoWoS and chiplet packaging infrastructure relevant to FPGA-HBM co-integration.

- March 2026: Altera expanded its collaboration with Arm to integrate Altera's HBM-equipped FPGAs with the Arm Neoverse CSS V3 AGI CPU, targeting low-latency, highly scalable AI data center acceleration platforms. The initiative moves Altera's FPGA portfolio explicitly into the hyperscaler AI fabric market alongside GPU-based systems.

- February 2026: Samsung Electronics achieved a world-first HBM4 mass-production shipment, deploying a 1c DRAM node and a 4nm logic base die manufactured through its in-house foundry. Samsung projects its HBM revenue to more than triple in 2026 versus 2025, with the Pyeongtaek P5 facility designated as the core HBM production hub from 2028.

- February 2026: AMD launched the Kintex™ UltraScale+™ Gen 2 mid-range FPGA family on February 4, 2026, targeting industrial, defense, aerospace, and high-performance data-conversion markets, with a lifecycle commitment through at least 2040. Simulation tool support is scheduled for Q3 2026, with pre-production silicon sampling in Q4 2026.

Global HBM For FPGA Acceleration Market Report Scope

The HBM for FPGA Acceleration Report is Segmented by Memory Type (HBM2E, HBM3, HBM3E, and HBM4), Integration Type (Standalone FPGA Accelerator Cards with HBM, FPGA SoCs with Integrated HBM, PCIe FPGA Accelerator Modules, and OCP/OAM FPGA Accelerator Modules), Application (AI Inference Acceleration, High-Performance Computing, Network Acceleration, Financial Services and Low-Latency Trading, Defense, Aerospace, and Secure Systems, and Scientific and Industrial Simulation), End User (Hyperscalers and Cloud Service Providers, Enterprise OEMs and System Integrators, Telecom and Networking Operators, Defense and Government Organizations, Financial Institutions, and Research Institutes and Laboratories), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| HBM2E |

| HBM3 |

| HBM3E |

| HBM4 |

| Standalone FPGA Accelerator Cards with HBM |

| FPGA SoCs with Integrated HBM |

| PCIe FPGA Accelerator Modules |

| OCP/OAM FPGA Accelerator Modules |

| AI Inference Acceleration |

| High-Performance Computing |

| Network Acceleration |

| Financial Services and Low-Latency Trading |

| Defense, Aerospace, and Secure Systems |

| Scientific and Industrial Simulation |

| Hyperscalers and Cloud Service Providers |

| Enterprise OEMs and System Integrators |

| Telecom and Networking Operators |

| Defense and Government Organizations |

| Financial Institutions |

| Research Institutes and Laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| India | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Memory Type | HBM2E | |

| HBM3 | ||

| HBM3E | ||

| HBM4 | ||

| By FPGA Integration Type | Standalone FPGA Accelerator Cards with HBM | |

| FPGA SoCs with Integrated HBM | ||

| PCIe FPGA Accelerator Modules | ||

| OCP/OAM FPGA Accelerator Modules | ||

| By Application | AI Inference Acceleration | |

| High-Performance Computing | ||

| Network Acceleration | ||

| Financial Services and Low-Latency Trading | ||

| Defense, Aerospace, and Secure Systems | ||

| Scientific and Industrial Simulation | ||

| By End User | Hyperscalers and Cloud Service Providers | |

| Enterprise OEMs and System Integrators | ||

| Telecom and Networking Operators | ||

| Defense and Government Organizations | ||

| Financial Institutions | ||

| Research Institutes and Laboratories | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and forecast for the HBM for FPGA acceleration market?

The HBM for FPGA acceleration market stood at USD 130.27 million in 2026 and is forecast to reach USD 490.79 million by 2031 at a 30.38% CAGR.

Which memory type leads today and which one is growing the fastest?

HBM2E led with 65.83% share in 2025, while HBM3E is projected to record the fastest growth at 31.18% through 2031.

Why are hyperscalers important in this space?

Hyperscalers and cloud service providers held 41.76% share in 2025 and are also the fastest-growing end-user group at 31.49% CAGR, which gives them major influence over product direction.

Which application generates the most revenue right now?

Network acceleration led with 34.12% share in 2025 because high-speed packet processing and AI fabric networking remain the most established deployment areas.

What is pushing adoption higher over the next 5 years?

The main growth factors are stronger demand for deterministic low-latency memory access, wider use of HBM-enabled accelerator cards, hyperscaler adoption, and better availability of HBM3E and HBM4-class memory.

What still limits broader adoption?

Advanced packaging dependence and high bill-of-materials cost remain the main barriers, especially for enterprise buyers that need clear cost justification before moving to HBM-based designs.

Page last updated on: